Abstract

Third-party administrators (TPAs), an important member of the managed care model in India, service health insurance claims and intermediate between health insurance companies, service providers and customers. Auditing TPA performance is not a prevalent industry practice because of a lack of regulation. This study explores the rationale behind the trend of insurance companies bringing TPA services in-house and investigates if the performance parameters for TPAs vary based on ownership. Analytical Hierarchy Process (AHP) was used to formulate the hierarchy of performance parameters for the TPA. Assessment of the efficiencies and quality of claims management between internal and external TPAs will enable insurance companies to make more informed decisions on managed healthcare models. Consequently, insurance premiums can be reduced, making health insurance a more viable option and could pave the way towards achieving the objective of universal health coverage. This study’s motivation stems from the possible impact that the performance evaluation of internal and external TPAs has on healthcare delivery, control and costs. The results show that both internal and external TPAs have their own efficiencies and advantages due to their operational models.

Keywords

Introduction

India’s healthcare sector is one of the fastest-growing sectors of its economy (Sengupta & Rooj, 2019). Increase in cost of care and proliferation of healthcare technologies has necessitated the search for financing options to tackle increasing healthcare costs. Therefore, health insurance is swiftly emerging as an effective tool for financing people’s health needs (Anchan et al., 2011; Bhat & Reuben, 2002; Pandit, 2016; Thomas & Vel, 2011). Enhanced health awareness, increase in lifestyle diseases, increased costs, proliferation of health technologies and access to insurance are reasons behind the growth of health insurance (Bhat & Reuben, 2002; Pandit, 2016). Recently, the role of health insurance has increased through government-funded programs and private health insurance purchases, making health insurance an integral part of the Indian healthcare landscape (Malhotra et al., 2018).

Health insurance companies tie up with Third Party Administrators (TPAs), who manage claims and coordinate between insurance companies, healthcare providers and customers (Bhat & Babu, 2004). TPAs were modelled on the managed care system. The prologue of TPAs in India was in anticipation of improved services to the insured, service providers as well as insurers and controlling costs (Bawa & Verma, 2011). As per IRDA (2019), 26 TPAs are operating in India. Although TPAs were introduced along the lines of managed care and Health Management Organisations (HMO) in the US, some differences exist between them. First, HMOs can underwrite risk; second, HMOs can source business on their own; thirdly, HMOs can offer hospital services and can own hospitals (Bawa & Verma, 2011). Lastly, HMOs have the authority to admit the insured at hospitals of their choice to curtail the cost of treatment, whereas TPAs have no control over which hospital the insured gets treated. The insurance companies enter into service level agreements (SLA) with TPAs, the salient features include enrolment and issuing identity cards to members, provision of 24*7 helpline, entering into contracts with hospitals, provision of data for standardisation of rates and cost control, providing insurers the charges at hospitals and data for appropriate underwriting.

A prominent restriction during the TPA introduction was that they should be independent of insurance companies (Bhat & Babu, 2004). Insurance companies such as ICICI Lombard, Bajaj Allianz, Star Health, Cholamandalam, have their TPA services in-house, intending to provide superior customer service with significant control over the quality and cost of healthcare delivery (Mehta, 2010; Mint, 2019; Neogi, 2019; PTI, 2010; Shetty, 2011; Thakur, 2010). There are no regulations requiring an audit of the performance of TPAs. The authors have not come across research establishing the advantages of having internal TPAs. Thus, this study attempts to investigate the relative importance of the various performance metrics for TPAs based on their ownership, the type of claims (cashless and reimbursement), and provides a comparison of the competencies in claim management between internal and external TPAs. The outcomes of the study are important as this evaluation will enable insurance companies to decide on TPA partnerships improving cost control through enhanced efficiency across services rendered, customer satisfaction and thus resulting in a healthier portfolio for the insurance company. These ensuing benefits can be passed on by the insurance companies, making health insurance more affordable and responsive to consumers. Thus, the findings of the work enable better implementation of effective claims management practices leading to improved delivery of healthcare and contributes to literature on health claims management and outsourcing of services.

In the remainder of the article, the second section deals with literature review and research objective, the third section explains the methodology, the fourth section discusses the results and the fifth section deals with conclusions and limitations.

Literature Review and Research Objective

The Indian healthcare sector is projected to reach 372 billion dollars in 2022 from 140 billion dollars in 2016, making it one of the major sectors in employment and revenue (Diwanji, 2020). Yet, the sector is severely underfunded and neither the government nor the common citizens have the capacity to pay for quality medical treatment (Thomas & Vel, 2011). Socioeconomic differences, poor healthcare infrastructure and inadequate risk-pooling mechanisms contribute to inequity and increasing costs (Sengupta & Rooj, 2019; Shahi & Singh, 2015). This situation has resulted in health insurance having wide acceptance and playing a major role in aiding to meet healthcare financing shortfalls (Anchan et al., 2011; Thomas & Vel, 2011). Enhanced health awareness, increased precedence of lifestyle diseases, increasing costs, proliferation of health technologies and access to insurance are reasons behind the growth of health insurance (Bhat & Reuben, 2002; Pandit, 2016).

TPAs were introduced with an objective to provide enhanced efficiency, standardisation, cashless services to policyholders and expanding health insurance coverage. Besides, TPAs face several challenges; first, there is a lack of clarity on minimum standards of care resulting in TPAs having less influence on cost control. Second, the unsustainable growth in healthcare expenditure has necessitated the need for better managed-care models. There should be an evaluation of performance of both insurance companies and TPAs for identifying an efficient and equitable health market (Gupta et al., 2004). Any successful execution would involve ongoing learning about the effectiveness of the different approaches to payment, reorganisation and clinical improvement (Goldsmith, 2011).

Rising dissatisfaction among stakeholders has forced insurance companies to revamp their model of claim handling, resulting in in-house TPA services (Mehta, 2010, 2011; Nair, 2011; Shetty, 2011; Thakur, 2010). Outsourcing literature states that efficient firms allocate their resources to value creating activities for which they enjoy comparative advantage and outsource non-core processes (Sia et al., 2008). Performing core activities in-house improves organisational performance (De Vita et al., 2011; Kotabe & Murray, 1996). Reducing costs and increasing efficiency are the primary reasons for outsourcing (Li et al., 2006). Outsourcing enables firms to access business partner’s resources and benefit from their competencies and skills thus realising process improvements (Barney, 1999; Wernerfelt, 1984). Prior research is not conclusive if outsourcing or in-house is better but states that those activities which were outsourced and are not being performed satisfactorily, can be chosen to be internalised, in order to improve their performance (Cabral et al., 2014; Espino-Rodríguez et al., 2008). Transaction Cost Economics (TCE) disseminates that managers are required to decide on the governing structure (outsourcing versus insourcing) and the degree of integration which is appropriate to achieve adequate performance (Cruz et al., 2014). Therefore developing the ability to control and leverage critical capabilities irrespective of whether they reside within the organisation or otherwise is more vital than the ownership of capabilities (Gottfredson et al., 2005). Research analysing the characteristics or attributes of outsourcing activities and their impact on outcomes has been limited (Espino-Rodríguez & Ramírez-Fierro, 2017). Almost all studies on TPAs are aimed at understanding the roles of TPAs as per the regulations (Bhat & Babu, 2004; Bhat et al., 2005; Gupta et al., 2004; Jaswal, 2010; Kalyani, 2004; Mahal, 2002; Parekh, 2003; Sureka, 2003). Our study addresses this gap in the literature as the authors have not come across research conducted on ownership of TPA activities and attempts to analyse the context and impact of bringing TPA services in-house on performance and customer satisfaction adopting the methodology of AHP.

Methodology

Analytic Hierarchy Process (AHP) is adopted for structuring the problem of rating the performance indicators of TPAs. AHP is insightful in providing more efficient decisions by structuring and assessing the relative attractiveness of competing operations or alternatives (Saaty, 1977, 1990). AHP have been used in diverse areas like new product designs, selection of bridges and research projects, new product pricing, degree programs, computer integrated manufacturing (CIM) benefits and risks, use of technologies, supplier selection and facilities location/layout (Ho & Ma, 2018; Khalil et al., 2016; Meena & Thakkar, 2014; Saaty, 1990; Saaty & Vargas, 1994; Singh & Nachtnebel, 2016; Sipahi & Timor, 2010; Thanki et al., 2016; Tummala & Wan, 1994; Vaidya & Kumar, 2006; Veisi et al., 2016). Although there have been applications of AHP in various fields, the authors have not come across studies adopting AHP to TPA performance.

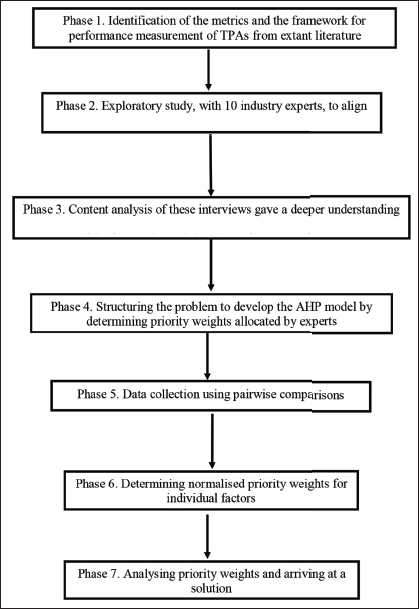

Using AHP, complicated problems are broken into numerous sub-problems, comprising hierarchical levels wherein every level shows a collection of criteria pertaining to each sub-problem. In the hierarchy, the top-level represents the goal (performance measurement of TPAs), the intermediate levels correspond to the strategic level and the operational factors. The decision elements at each hierarchical level are compared pairwise and their relative weights indicate the strength of dominance of one element over the other. Subsequently, the local and global priority weights are determined based on these pairwise comparison matrices. The pairwise comparison rankings on a nine-point scaling system are inputs provided by evaluators (Saaty, 1990). Further, AHP provides options for segregation and dependence—independence relations within attributes enabling decision-makers to evaluate pairwise comparisons reducing assessment bias. Despite concerns on the use of AHP due to particular measurement problems, the calculation of priority values are based on classical eigenvalue problem and hence there is no disagreement about this issue (Saaty, 1994). Figure 1 details the steps followed to arrive at the solution.

Flow Chart of Phases under Analytical Hierarchy Process (AHP).

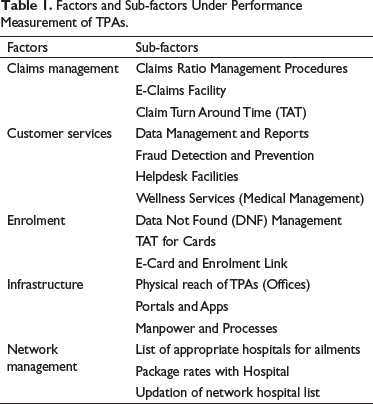

The metrics and framework for performance measurement of TPAs were identified from extant literature and an exploratory study, involving 10 industry experts was undertaken to align the metrics with industry practice. Hierarchy of the factors and sub-factors was formulated using AHP. Based on the identified performance metrics and expert interviews, the performance measurement problem was structured as a series of hierarchies wherein each level represents one set of performance indicators as shown in Table 1.

Factors and Sub-factors Under Performance Measurement of TPAs.

The factors and sub-factors were given relative weights through questionnaire administration that involved experts. The nine-point scale developed by Saaty was adopted to assign relative importance (Saaty, 1990, 1994; Saaty & Vargas, 1994). The respondents included employees of insurance companies, TPAs and insurance brokers, from three metropolitan cities (Bengaluru, Chennai and Mumbai) in India. All the respondents had more than eight years of relevant experience. Twenty-seven responses were obtained for internal TPAs while thirty-three responses were obtained for the external TPAs. The valid responses with a consistency index less than 0.1, based on Saaty (1994), are shown in Table 2.

Responses with Consistency Index.

Findings and Discussion

The first phase of AHP resulted in the development of a questionnaire based on the performance hierarchy for TPAs, and it was administered to experts. Follow-up interviews with the experts provided additional insights. The first and second sub-section of the fourth section highlight the findings for internal TPAs and external TPAs, respectively.

Cashless and Reimbursement Claims Processed by Internal TPA

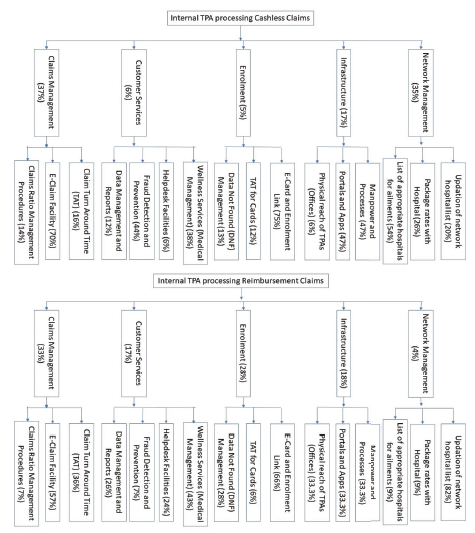

Claims management refers to the steps and procedures undertaken by TPAs to manage claims. Claims management is the most important factor for both cashless (37%) and reimbursement (33%) claims serviced by internal TPAs (Figure 2) and E-claims facility is the most important sub-factor for both cashless (70%) and reimbursement (57%) claims. E-claims facility enables real-time tracking of claim status and provides details of documents or reports pending for claim approval. Clearing pending documents is important for processing of both cashless and reimbursement claims.

Relative Importance of Factors for Internal TPA while Processing Cashless and Reimbursement Claims.

Network management (35%) is the second key factor for cashless claims being serviced by internal TPAs wherein the claim is restricted to network hospitals. Hospitals to be included in the network are determined by inputs from insured and insurance companies, location, negotiating power, existing relation with the hospital and the ability to provide value-added services like mass health check-ups and preventive care. Under network management, the list of appropriate hospitals for ailments (54%) is the most important sub-factor. Internal TPAs provides network management services that are customised to the requirements of the insurance company based on the insured’s preference and the geographical spread of the insured population. TPAs negotiate with hospitals regarding package rates for ailments as per the insurance covers. The insured opts for reimbursement claim either because the treatment is at a non-network hospital or because of an emergency. The insured should be an enrolled member under the insurance policy for the claim to be processed. There are times when the insured is not enrolled under the policy, either because the policy has been renewed recently and the details of the members covered under the policy are awaited or because the insured is an addition under the policy. These cases are called data not found (DNF) cases. TPAs use E-card and enrolment links for enrolment (28%), which is the second important factor for reimbursement claims being serviced by internal TPAs.

Infrastructure is the third important parameter for both cashless (17%) and reimbursement (18%) claims under internal TPAs. For cashless claims, portals and apps (47%) and manpower and processes (47%) are the two important sub-factors. Internal TPAs are guided by the vision and processes of the parent insurance company with respect to both information technology (IT) as well as physical infrastructure. Claim processing involves interfaces with the stakeholders including the network hospitals and should seamlessly integrate with the infrastructure of the parent insurance company. User-friendly portal and mobile apps using recent technologies like artificial intelligence and machine learning act as platforms for the smooth provision of these services. Qualified and trained manpower help to efficiently process the claims resulting in better turn-around-time (TAT) for cashless claims. For reimbursement claims, it is found that all sub-factors under the category of infrastructure, that is, physical reach of TPAs (offices), portals and apps. and manpower and processes, are equally important (33.33%). Reimbursement claims are spread all over the country and proximity to the TPA office handling the claim plays an important role and helps in the submission of claim documents, follow-up on pending documents as well as enquiries regarding claim status. Alternately, few TPAs have centralised operations, where all claims are processed from a central TPA office.

Customer service is the next important parameter for cashless (6%) and reimbursement (17%) for internal TPAs. Fraud detection and prevention (44%) was the most important sub-factor for internal TPAs servicing cashless claims. Internal TPAs, being an integral part of the insurance company, play a very important role in designing interventions like hospital checks, screening of bills and blacklisting service providers to prevent and control fraud. Wellness management is the next important sub-factor for cashless (38%) as well as reimbursement (43%) claims. Wellness management refers to the services aimed at improving patient care and reducing the need for long term medical care by aiding patients and caregivers to effectively manage health conditions. These are proactive control measures, which, when implemented over a period, will lead to better health and wellness of the members. Proactive health checks and workshops aimed at addressing the general health of the insured helps to control the number and cost of claims for commonly prevailing ailments.

Cashless and Reimbursement Claims Processed by External TPA

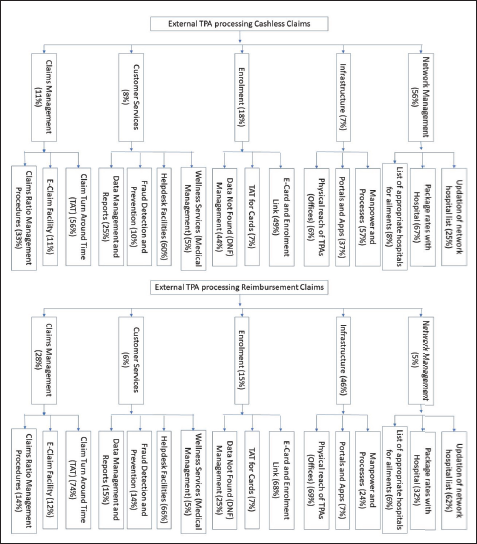

Figure 3 shows the order of relative importance of performance parameters for external TPAs servicing cashless claims is network management (56%), enrolment (18%), claims management (11%), customer service (8%) and infrastructure (7%). Package rates with hospitals (67%) and updation of network hospital list (25%) are the important sub-factors under network management and they help to control claim costs. E-card and enrolment link (49%) and DNF management (44%) are the important sub-factors under enrolment (18%) for external TPA servicing cashless claims. E-card facilities and enrolment links enable the insured to enrol themselves and their dependents under the policy, leading to hassle-free servicing of the insured’s claim. When encountered with a DNF case, the TPA raises a query with the insurance company. The claim is processed only after the DNF issue is resolved. Hence, the TPA has to design its DNF handling process to ensure that the time taken for resolving is within reasonable limits.

Relative Importance of Factors for External TPA while Processing Cashless and Reimbursement Claims.

Infrastructure (46%) and claims management (28%) are the most important parameters for external TPAs servicing reimbursement claims. The physical reach of TPAs (offices) (69%) and manpower and process (24%) are the most important sub-factors under infrastructure, while claim TAT (74%) is the most important sub-factor under claims management. Under enrolment (15%), e-card and enrolment link (68%) and DNF management (25%) are the important sub-factors for external TPAs handling reimbursement claims. E-card and enrolment link enables hassle-free enrolment of insured members and helps the insured to take a print of their cards. These facilities aid the efficient processing of reimbursement claims.

Internal TPAs can streamline their claim processes through an e-claim facility with exception handling options enabling efficient and timely claim processing. The communication between the insured, hospital, TPA and insurance company happens seamlessly in case of an internal TPA due to lesser contact points as compared to external TPAs. Internal TPAs have a better understanding of the hospital network requirements and have greater flexibility in the selection of network hospitals. Being an internal TPA enables it to seamlessly use E-card and enrolment links and address the DNF issue more effectively. User-friendly portals and apps and optimised processes and trained manpower lead to better turn-around-time (TAT) and efficient claim processing. Internal TPAs have access to the underwriting information of the insurance policies and can design and implement effective wellness management initiatives aimed at improving the health of the insured and controlling instances of claims.

External TPAs face diverse requirements from numerous insurance companies and policies that they service. It is a very challenging task to be able to arrive at package rates that are acceptable to all insurance companies and hence external TPAs end up having far larger number of hospitals in their network. Regular updation of the network hospitals and packages based on inputs from the insurance companies is of prime importance. TPAs need to design the infrastructure and processes to ensure that the claim processing is within reasonable time limits. E-card and enrolment links need to be customised to the requirements of the diverse customers and need to enable hassle-free enrolment of insured members.

Conclusion, Limitations and Future Direction

This study has established that the relative importance of performance metrics for TPAs change based on the TPA being internal or external and type of the claim. Having an internal TPA enables the insurer to build key differentiators around the claims handling front, the network of hospitals and claim TAT. In-house claim processing is more convenient, hassle-free, transparent and takes lesser time. There is far more accountability with in-house TPAs as they offer end-to-end services for health insurance policies. External TPAs have hospital networks that are mostly larger than that of an in-house TPA, catering to diverse requirements of partner insurance companies. The success of the external TPA while servicing cashless claims depends on its ability to regularly update the network hospitals and to negotiate with the service providers for better rates to cater to the diversity of its customers.

However, in-house TPAs will result in higher administrative costs as the insurance companies have to undertake huge groundwork, tie-up with hospitals, and maintain a 24×7 helpline but in the long run, it will lead to a reduction of claims (Nair, 2011). The processes and infrastructure of the internal TPAs are designed to add value to the customers not only for insurance products but a wide range to wellness and pre-emptive diagnosis and follow-up of ailments while also providing options for second expert opinion for cases where the insured require medical inputs. Technologically advanced TPAs can offer better services. Market trends show consumers are looking at insurance companies to offer complete healthcare solutions such as wellness services, and prompt replies on queries related to products, systems and services, expert advice and second opinion. Having an internal TPA helps in these areas as they have a direct connection with all stakeholders: insurers, customers and service providers.

Cost containment in health insurance is a broad area that includes all features like provider payment mechanisms, benefit packages, claims processing and monitoring, fraud control, data analysis and course correction, medical technology and IT innovations (Reddy et al., 2011). Further, health insurers are increasingly utilising quality information for performance-based payments and provider contracting (Van der Wees et al., 2014). To meet the demand for cost containment and delivery of high quality of service, it is imperative that TPAs need to develop suitable systems and management structures aiming at cost control, develop procedures to minimise unnecessary treatments/investigations and improve the quality of services. The growth of the health insurance industry lies in enhanced customer orientation in terms of standardisation of procedures and definitions across the industry and servicing the customers (Goswami & Roy, 2014). Having an internal TPA seems to be a step towards achieving this objective. There is a need for IRDA to evaluate the performance of both internal as well as external TPAs and build systems that can drive the necessary changes in the health care industry and help build a more sustainable model. There is an immediate need to link TPA incentives with their comprehensive performance rather than a fixed percentage of the policy premium (Pandit, 2016). TPAs need to move up the value chain by providing seamless service to end consumers and striving to improve efficiency.

There are a few limitations to this study. This study deals with TPAs and insurance companies. Further studies can be carried to find the perspective of insured and service providers like hospitals and clinics. This could help further our understanding of performance metrics for TPAs as viewed by these stakeholders and provide inputs to the regulator on any modifications or changes required in the role and responsibilities of the TPA and the relation between the TPA and the insurance company. The sample size for the study could have been bigger, though Saaty (1994) had suggested that 19 experts are sufficient for a study of this nature.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.