Abstract

The purpose of the study is to explore dividend behaviour of Indian manufacturing and service sector firms and to investigate similarities/differences between the same. First, the analysis is conducted using pooled, fixed and random effects OLS regression for panel data on 452 manufacturing and service sector firms for the period of 2007–2015. Further, dynamic panel data analysis has been used to deal with the heteroscedasticity and endogeneity issues among the variables for the study to capture asymptotic efficient estimates. The result refutes significant differences in terms of firm-level factors that determines dividend policy. However, manufacturing sector is significantly efficient in declaring dividends (59.63 per cent) in comparison to service sector (34.33 per cent). Further analysis suggests that firm size and cash holdings have significant positive relationship to dividend paid, whereas age and net working capital are negatively significant for dividend declarations in the service sector. However, the analysis of manufacturing sector suggests that profitability and firm size and profitability are positively significant, while net working capital is negatively significant for dividend decisions.

Keywords

Introduction

The decision of firms to declare dividend or to retain earnings for future growth has always been dynamic and sought to be explained through different theories. Theoretical and empirical works abound since more than half a century. Various theories explain dividend behaviour providing a strong literature base to amend the dividend policy as per financial status of the firm. Dividend irrelevance 1 (Miller & Modigliani, 1961) was the first of such attempts describing that firm’s value is independent of its dividend policy. Bird in hand 2 theory (Gordon, 1963; Lintner, 1962) argues that investor will make a trade-off between the dividends paid today or the opportunity of capital gains in the future, strongly emphasizing the effect of dividend policy on the value of the firm. Agency cost 3 (Easterbrook, 1984; Jensen & Meckling, 1976; Rozeff, 1982) theory explains the importance of dividends in minimizing the agency cost to the firm thus, contributing to the value of the firm. Later, Life cycle 4 (Mueller, 1972), Information asymmetry and signalling theory 5 (Bhattacharya, 1979) and free cash flow hypotheses 6 (Lang & Litzenberger, 1989) tried to explain the role of firm-level factors in determining dividend policy. Firm-level factors such as age, size, ownership classification, cash holdings, leverage, net working capital, risk, growth and profitability were used as the main explanatory variables to validate the theories empirically. However, the convergence on these theories is yet to be achieved due to the assumptions linked to each theory. Literature suggests strong evidence that dividend policy varies to a large number of factors ranging from macroeconomic, industry- and firm-level factors. Previous studies were primarily focussed on explaining the probability of dividend distribution taking firm-level factors as control variables using the heterogeneous sample of firms from predefined indexes or set of firms. Also, some studies focussed on the industry- and country-level variances to explain the dividend behaviour of the firms (Denis & Osobov, 2008). However, sectoral differences between the firms were often overlooked in the understanding of dividend policies of the firms. The objective of the current study is to explore the determinants of dividend policy among manufacturing and service sector among Bombay Stock Exchange (BSE)-listed firms. The study is motivated from the fact that there is a vast difference in the way these sectors work. Manufacturing sector is highly dependent on the investments on plant and machineries, whereas service sector is more dependent on human capital that requires lesser initial investment. Service sector has grown tremendously during last two decades beating the orthodox odds of dependence of profitability of firm on huge plant and machineries. However, the stability of service sector firms is still subjected to various questions ranging from their survival, life cycle and profitability. Manufacturing sector in India has faced a diminishing growth rate during the same period of time. The important point that we want to address is that there exists a considerable amount of difference between these sectors that may cause variations in dividend behaviour of these sectors. The study will contribute to understand the relative role of financial factors to understand the existing dividend behaviour in manufacturing and service sector firms of India. The article is formatted into seven sections which includes, first, the introduction to the article followed by review of literature and objectives of the study along with model proposed in the second and third section, respectively. Data and methodology followed by descriptive statistics is discussed in the fourth and fifth section. The article is concluded into results and discussion in the sixth section and finally, conclusion in the seventh section.

Review of Literature

Several studies have been conducted to explore the determinants of dividend policy around the globe. Literature suggests theoretical and empirical support for variables such as corporate size, age, ownership structure, market risk, cash holdings, leverage, growth opportunities, net working capital and profitability of the firm. The aforementioned factors have been explicitly discussed in the following section to provide base for the model proposed.

Age

The importance of age can be understood from the fact that there is a huge gap between the number of start-ups and survival of the firms which reflects that it takes a significant time to achieve their break-evens and become profitable. Since dividend is usually paid out of profits there is a high probability that younger firms will try to retain profits for future growth opportunities. According to a study conducted on Swiss firms addressing success of start-up firms by Tobias Stucki (2014), only found 12 per cent firms were able to survive in the sample period of 1996–2006 since incorporation out of 7,112 firms. Further, many studies have reported age as a significant factor for credit constraints, that is, younger firms are more credit constraint than older firms which means that younger firms will try to avoid dividend payments (Cabral & Mata, 2003). Hadlock and Pierce (2010) said that age is the best proxy for judging the firms credit constraints. Firms which are financially constrained will try to avoid dividend payments due to internal funding requirements.

Ownership Structure

Ownership structure of the firms is responsible for various characteristics of the firm. In most of the cases firms associated with a business group have easier access to funds for the future investment opportunities. Such firms are always considered less risky due to association with the diversified business group. Most of the funding requirements are done through parent company and external finance is available at a relatively cheaper rate than for individual companies. Short, Zhang and Keasey (2002) reported a positive association between dividend pay-out policy and business group affiliation by taking evidence from a UK panel data set. The model was analysed by taking reference from dividend models of Lintner (1956) and Fama and Babiak (1968). Firms also use dividend policy as a trade-off to lower agency cost for the group companies (Chen & Steiner, 1999; Shleifer & Vishny, 1986). Chen, Cheung, Stouraitis and Wong (2005) reported insignificant relationship between ownership structure and dividend policy. Subramaniam, Tang, Yue and Zhou (2011) reported that there is a positive significant relationship between ownership structure and dividend policy.

Risk

Market risk is an important determinant for the dividend policy as it reflects the stability of the firm in the eyes of the investor. Higher volatility in the share price reflects information asymmetry and larger dependence on external finance. According to the study conducted by Rozeff (1982), risk has a negative influence on the dividend pay-out of the firm. Later, D’Souza and Saxena (1999) confirmed the aforementioned results on the international perspective using DataStream database and World scope disclosure reports. Amidu and Abor (2006) also reported negative influence of market risk on dividend policy in their study conducted on the firms listed on the Ghana stock exchange. Recent research by Bartram, Brown & Waller (2015) and Baker and Jabbouri (2016) also reported a significant negative relation between dividend policy and firm risk.

Cash

The amount of cash that a company holds can be seen as the indicator of growth opportunities available to the firm. Firms may hold more cash either because of paucity of opportunities or in anticipation of future opportunities (Jensen, 1986). Such firms may choose to pay dividends instead of choosing sub-optimum investment options, but smaller firms might choose to stock cash to meet up future funding requirements rather than going for costly external finance. There is large thread of literature which shows a positive relationship between cash flows and dividend policy (Agrawal & Jayaraman, 1994; Chen, Chou, & Lee, 2014; Lang & Litzenberger, 1989; Subramaniam et al., 2011). However, Denis, Denis and Sarin (1994) did not support the overinvestment problem and reported insignificant relationship between cash flow and dividend policy.

Leverage

Capital structure is the main characteristic which derives the value of the firm. The optimal mix of debt and equity is the prime objective to achieve to maximize the value of the firm. Leverage is also discussed as an important determinant of dividend policy as highly levered firm will prefer to pay back the principle debt instead of paying dividends. The interest expenses are directly proportional to the degree of financial leverage. Also firms prefer to fund the investment opportunities from external finance for the sake of tax benefits rather than issuing risky equity shares for the project. The literature suggests a negative relationship between leverage and dividend policy (Fan & Sundaresan, 2000; Jensen, Solberg, & Zorn, 1992; John & Muthusamy, 2010; Papadopoulos & Charalambidis, 2007).

Growth Opportunities

Profitable investment opportunities available to the firms are termed as growth opportunities. Firms would prefer cheaper internal finance to fund these growth opportunities rather than resort to costly external finance (Myers & Majluf, 1984). Rozeff (1982), Lloyd Jahera & Page (1985) and Manos (2002) reported significant negative relationship between growth opportunities and dividend policy of the firm. Presence of growth opportunities diminish the possibility of dividend pay-out.

Net Working Capital

Net working capital is a major factor for the firm as recognized by famous economist Adam Smith. Authors such as Schiff and Lieber (1974), Smith (1980) and Kim and Chung (1990) reported that firm performance is affected by working capital decisions. While empirical evidence suggests that efficient working capital management enhances profitability (Deloof, 2003; Jose, Lancaster, & Stevens, 1996; Shin & Soenen, 1998; Wang, 2002), reducing working capital investment is likely to bring affirmative results to profitability (Juan García-Teruel & Martinez-Solano, 2007). Hence, efficient working capital management or reduced working capital holding is likely to facilitate dividend decisions.

Profitability of the Firm

The primary source of dividend payments is from the profits of the firm hence it is considered that higher the profitability of the firm more will be the chances of dividend pay-out (Anil & Kapoor, 2008). Seminal work of Lintner (1956) found that earnings are the most important determinants of dividend policy which was later supported by Fama and Babiak (1968), Ryan (1974), Shevlin (1982) and Allen (1992). Further studies by Baker, Farrelly and Edelman (1985), Pruitt and Gitman (1991) and Baker and Powell (1999) reported that future earnings and the pattern of past dividends were the main determinants of dividend payments. They also found that current dividends are influenced by the current as well as past level of earnings as also the growth rate of earnings. Significant positive relationship between profitability and dividend policy is confirmed by Nissim and Ziv (2001), Amidu (2007), Howatt, Zuber, Gandar and Lamb (2009) and Ajanthan (2013).

While these results are highly intuitive and plausible, Farsio, Geary and Moser (2004) and John and Muthusamy (2010) reported insignificant and negative relationship between profitability and dividend policy. Farsio et al. (2004) explained his results by using a longer period of analysis (1988–2002). Further, latest study from Batra and Kalia (2016) reported corporate profitability as the driver for dividend payments.

Size of the Firm

Size of the firm is one of the most important determinant of the dividend policy as suggested by the literature. Large companies pay more dividends in comparison to smaller firms as they have saturated growth rates and access to cheap external finance. Dividends are used as a tool to avoid information asymmetry problems (Bhattacharya, 1979) later on also supported by (Aharony & Swary, 1980; John & Williams, 1985; Miller & Rock, 1985). Previous studies also suggest that larger firms pay dividends to signal financial soundness and lower agency conflicts for the firm (Jensen & Meckling, 1976). Another important reason for smaller firms for paying dividends is the costly external finance which they would require if a profitable investment opportunity would be available to them (Holder, Langrehr, & Hexter, 1998). Larger firms usually have access to diversified technology, market and trusted business partners which reduces the risk of the firm in comparison to small firms (Behr & Güttler, 2007; Harhoff & Körting, 1998). Lower risk rates can help in improving profitability of large firms which can be linked to dividend decisions of the firms.

Objectives of the Study and Model Proposed

The main objective of the study is to find out the sectoral divergence in terms of dividend behaviour among Indian-listed manufacturing and service sector firms, if any. It also analyse the same for the managerial implications derived out of the relationship among the factors of the study. The model proposed for the study used variables that affected dividend policy as suggested by the literature. The variables are analysed using OLS regression, and OLS using fixed and random effects estimator Equation (3). Further dynamic panel data equation as specified by Arellano and Bond (1991) is used by taking lags of the dependent variable and instrumental variables to control for heterogeneity in Equation (4).

Equation (1) represents the basic simple linear regression equation where Y is the dependent variable for the firm i at time t. X is the vector of firm specific factors which effects the dependent variable and ε is the error term for the firm i at time t. Equation (2) shows the panel data equation for fixed and random effects where z represents the time-invariant factors and δ represents coefficients for the same while other factors remain same as defined in Equation (1). Equation (3) shows dynamic panel data equation where Yi,t–1 shows the lag for the independent variable and ρ as the coefficient for the dependent variable. The error term is represented by εi,t and ui is an unobserved time-invariant effect which allows for the heterogeneity in the dependent variable in the series across individuals (idiosyncratic error). Equations (4) and (5) highlights dependent and independent variables substituted in Equations (2) and (3). We have not shown detailed basic OLS equation as the only difference from Equation (2) was the treatment of time-invariant variable in the vector X instead of a separate vector Z.

Data and Methodology

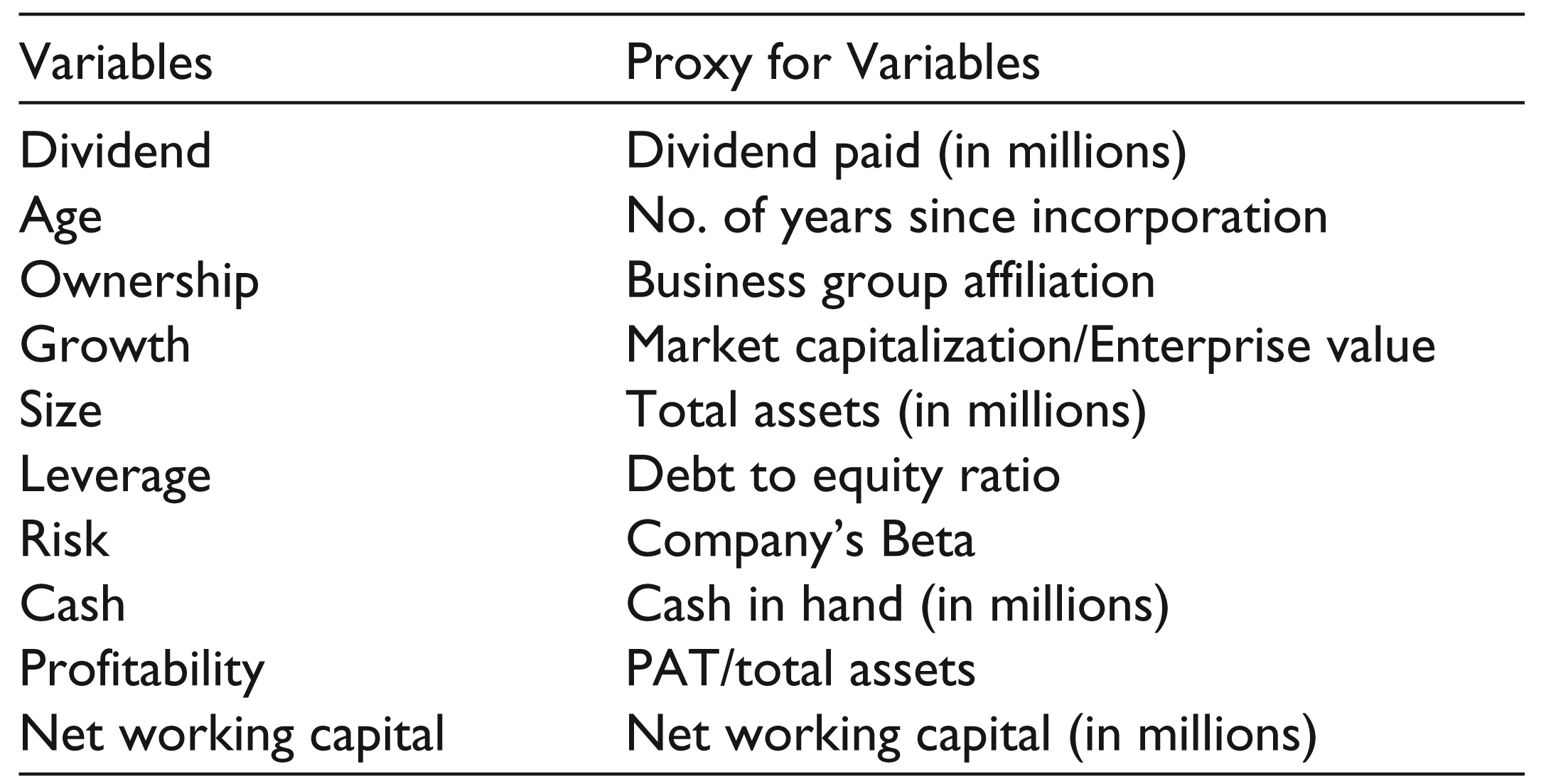

In our study, the data is extracted from Centre for Monitoring Indian Economy (CMIE) Prowess database which is India’s largest database for the firm-level data of the Indian companies. It constitutes the firm-level data from the annual reports, financial statements and other published reports for the Indian firms. The database has the collection of 26,000 Indian firms across various sectors. Table 1 shows variables and their proxies used for the analysis.

The study is conducted on manufacturing (transport equipment and machinery) and service sector firms (IT and business consultancy) listed on BSE. The reason for picking aforementioned sectors is the coherence to represent respective sectors regarding their working behaviour. We extracted data for 264 manufacturing firms and 188 services firms listed on BSE for the period of 9 years from 2007 to 2015. The regression model proposed in the study takes dividend as dependent variable, whereas size, age, ownership group, cash holdings, net working capital, risk, leverage, cash and profitability as explanatory variables.

The primary analysis is done using simple linear OLS model which assume all the independent variables are exogenous and the error term is not serially correlated. The linear OLS model will be biased whenever aforementioned conditions are not satisfied. To take care of aforementioned biases, OLS estimator with fixed and random effects is used. In the fixed effects model, the intercept or slope of variables is assumed to be time invariant but will differ among individuals and the error term intercepts as time variant. To find out which model is appropriate Hausman test (1978) for fixed and random effects was applied with the null hypotheses stating that random model is appropriate. In the fixed effect model age and ownership are omitted because of collinearity conditions and time-variant effect on the independent variables.

Proxy for Variables

We estimate Equation (5) using the one-step and two-step generalized method of moments (GMM) estimator for dynamic panel data model developed by Arellano and Bond (1991). GMM is among the most frequently used methods due to its capacities of convenience in deriving normally distributed estimators of the statistical model Hall (2005). The advantage of using GMM is the efficient results which it brings by taking the unobserved heterogeneity into account. Further, two-step GMM is used to improve asymptotic efficiency in comparison to one-step estimates. Also endogeneity problems are taken care of by using lag of dependent variable and substituting instruments for explanatory variables. We allowed maximum one lag of dependent variable to be used as instruments. The autoregression of order AR (2) is used in the analysis.

Descriptive Statistics

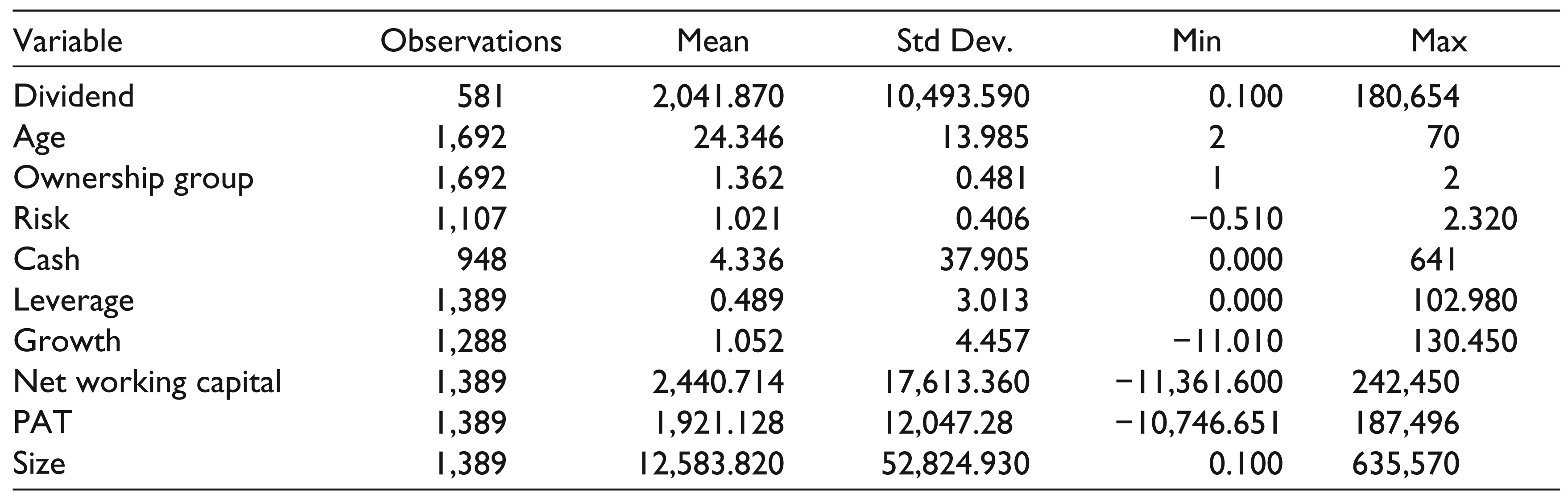

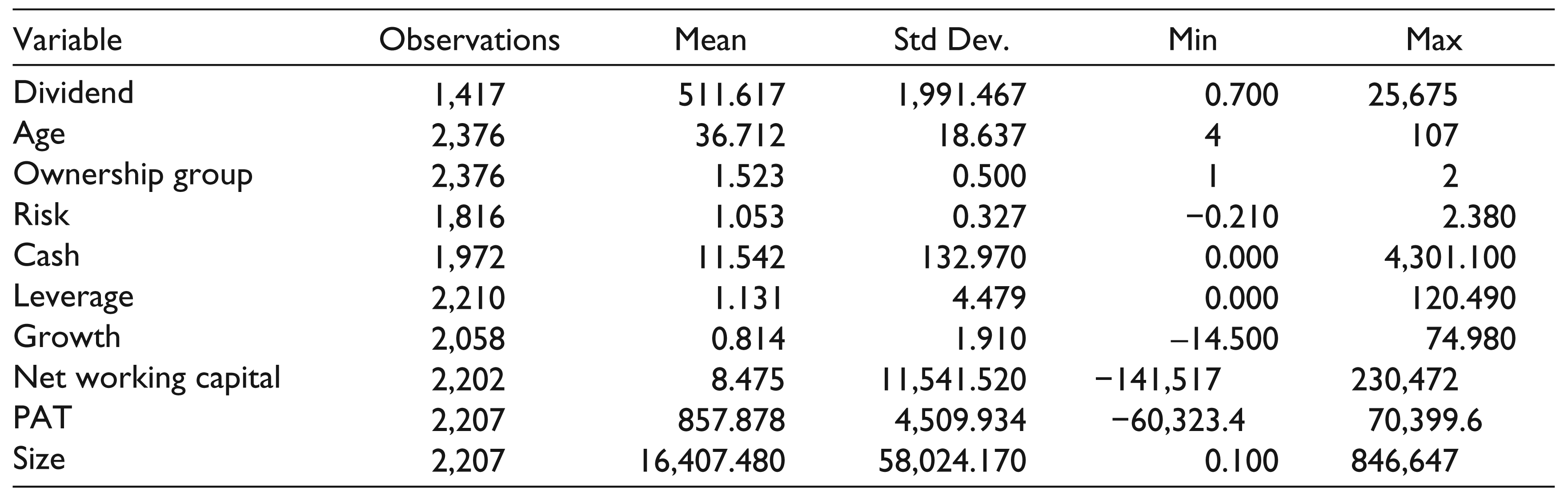

The descriptive statistics of variables taken for manufacturing and service sector has been shown in Tables 2 and 3, respectively. Maximum observations are recorded for age and ownership for manufacturing (2,376) and service sector (1,692), respectively. Dependent variable dividend is recorded only for 581 out of 1,692 observations in service sector while manufacturing sector recorded 1,417 out of 2,376 observations. Overall manufacturing sector has exhaustive data compared to service sector in terms of missing values. Data clearly suggest that manufacturing firms are much efficient than service sector in declaring dividends (59.63 per cent in comparison to 34.33 per cent).

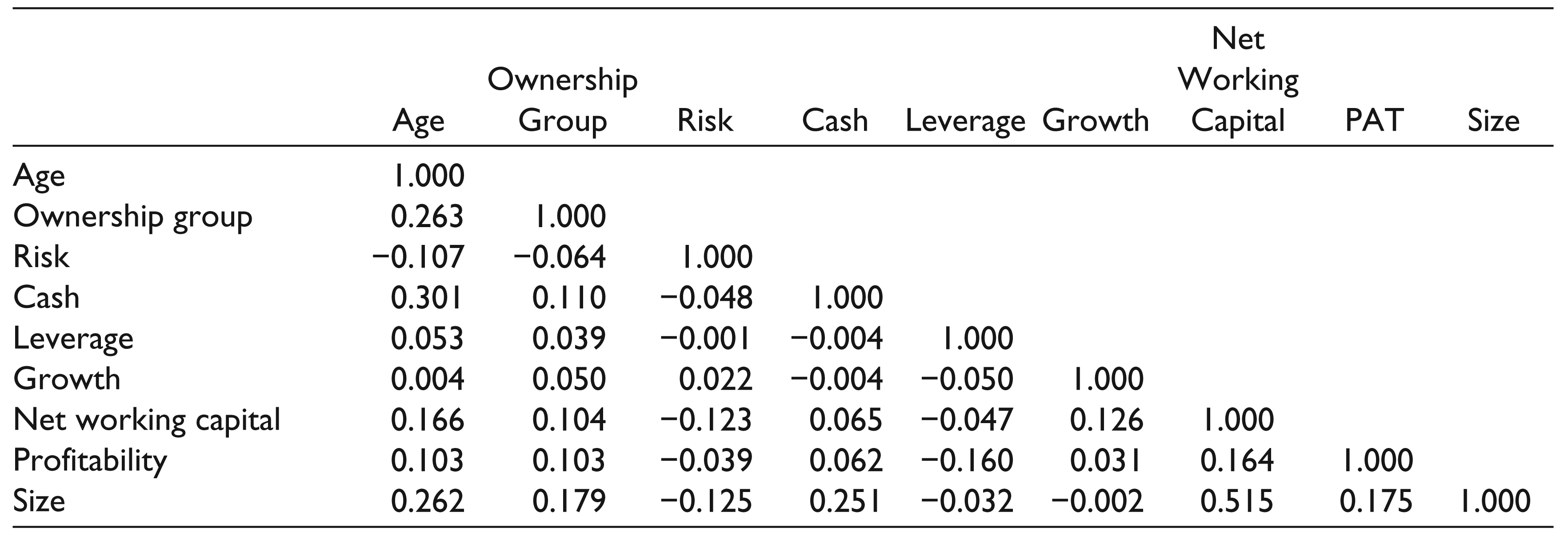

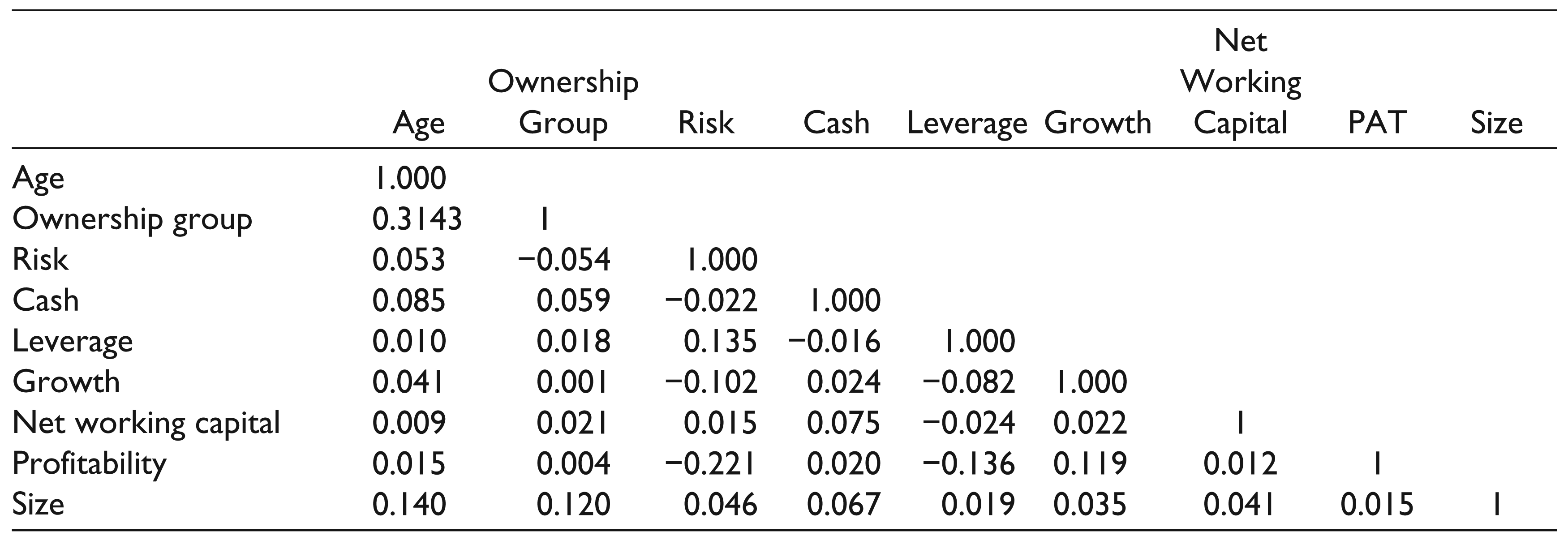

The correlation matrix for independent variables has been shown in Tables 3 and 4. In the service sector, size is reported to be highly correlated with net working capital with the positive correlation of 0.515 which shows positive association between size and net working capital of the firm. In addition, cash is also found to be correlated with size and age with the positive values of 0.251 and 0.301 implying that larger and older firms are probable to have more cash holdings. In manufacturing sector, the only notable inference is between age and ownership group with positive value of 0.314 which highlights that older firms have higher probabilities of having group affiliation. However, the methodology used takes care-of endogeneity problem which might be caused due to correlation between the variables. Tables 4 and 5 show the correlation matrix for service and manufacturing sector, respectively.

Summary Statistics Service Sector

Summary Statistics Manufacturing Sector

Correlation Matrix Service Sector (Independent variables)

Correlation Matrix Manufacturing Sector (Independent variables)

Analysis

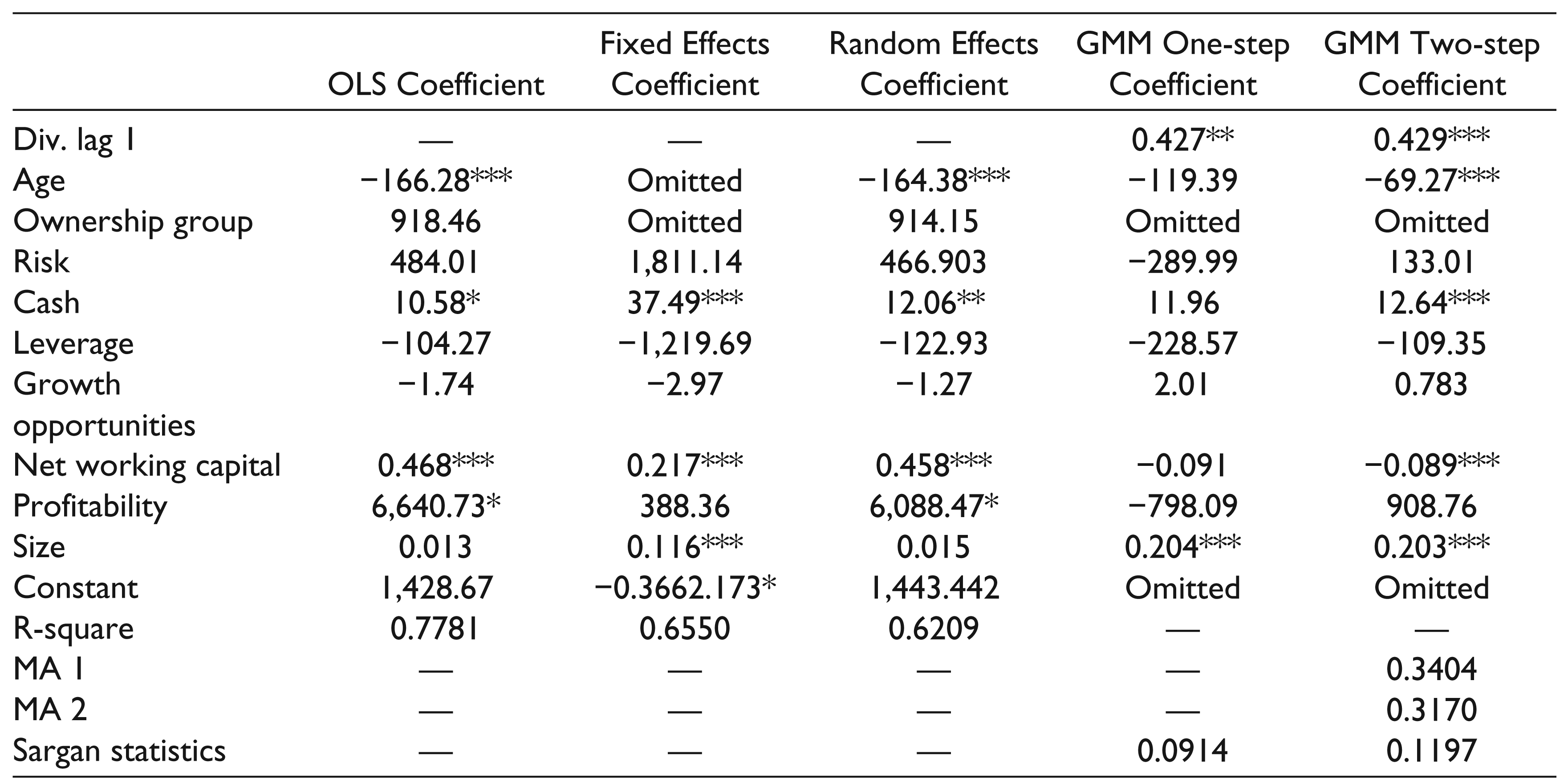

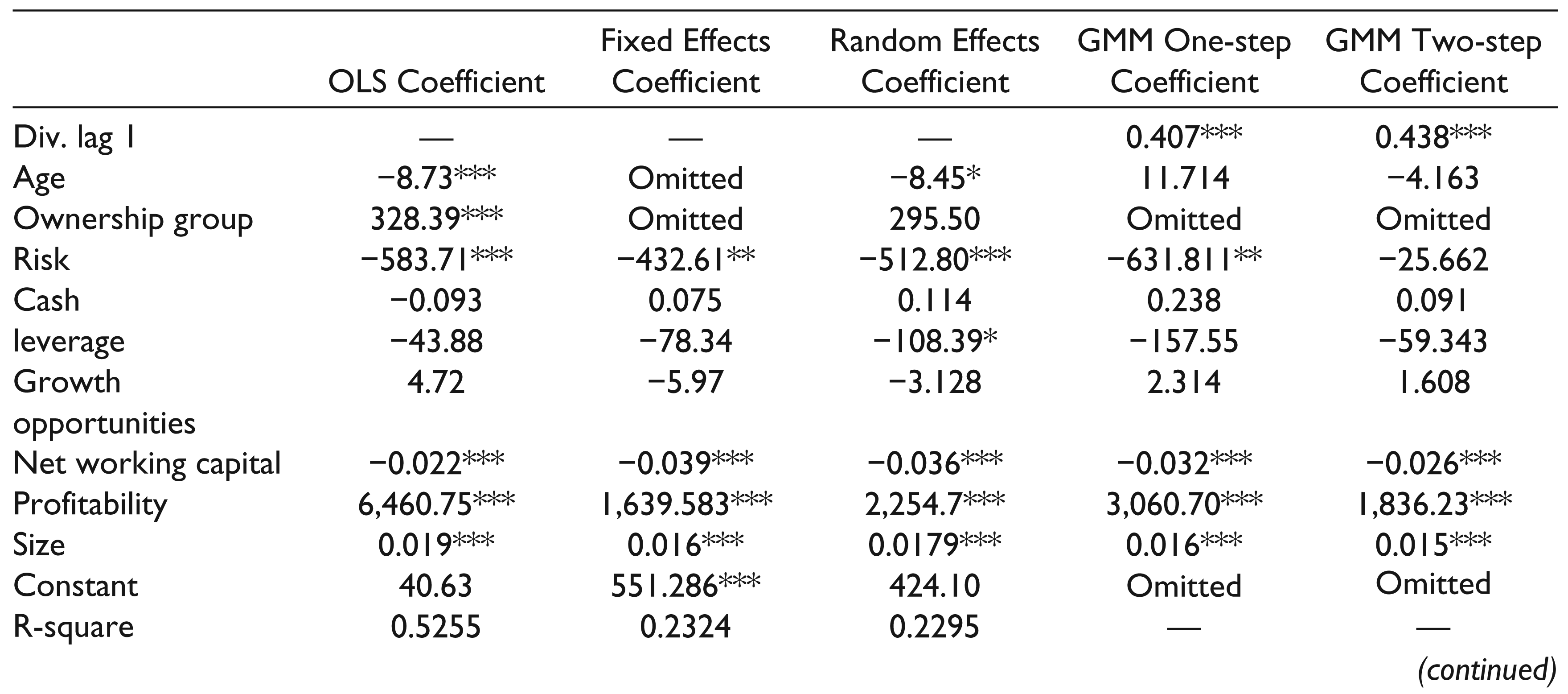

The results from primary analysis from linear OLS regression suggests that age have a negative significance, while size has a positive significant relationship on dividend pay-out for the service sector. The reason for the result can be the technology driven orientation of service sector where innovation and sustainability are the key drivers of the profitability, which can also linked to the size of the firm. Cash holdings and profitability are also found positively significant but only at the confidence interval of 90 per cent highlighting limited participation of the factors towards dividend payments in the service sector. However, manufacturing sector has age, ownership, risk, net working capital, profitability and size as significant variables. Age, risk, and net working capital are found negatively significant, while ownership, size and profitability are positively significant. Manufacturing sector’s efficiency depends a lot on effective working capital management and the risk scenario which is highlighted in the aforementioned results. The final results from altered methods have been shown for service and manufacturing sector in Tables 6 and 7 correspondingly.

The fixed and random effects regression is used to deal out the complexities of the error term and collinearity biases. Age and ownership are omitted in both the sectors due to collinearity and the omitted variable bias in the results. The results from Hausman test (1978) suggested rejection of null hypotheses (Ho; random model is appropriate) for both the sectors and, hence, confirmed the omitted variable bias and found fixed effect model to be appropriate for the results. The findings suggest that size, cash holdings and net working capital are the only significant variables for service sector with the positive relationship. There is a negative correlation between regressors and the error term (−0.6561). The intra-class correlations between the firms are found to be (rho = 0.4865) which means 48.65 per cent of the total variance explained R2 (65.50 per cent) is due to heterogeneity among the firms. Further results of manufacturing sector found that firm size and profitability are positively significant while, risk and networking capital are negatively influencing the dividend decisions. The correlation between error term and independent variables is (0.1207) and intra-class correlation is found to be (rho = 0.6998) 69.98 per cent of the total variance explained R2 (23.24 per cent). Models for both the sectors are found to be significant at 99 per cent confidence intervals.

Results Service Sector (Dividend/PAT as dependent variable)

Results Manufacturing Sector (Dividend/PAT as dependent variable)

*, ** and *** are significant at 90%, 95% and 99% confidence intervals, respectively.

The final analysis using GMM found that size and cash holdings are positively significant, whereas networking capital is negatively significant for the service sector. The result improved the fixed effects regression estimate which reported networking capital to be positively significant with the dividend paid which appeared conflicting to the literature. However, results for manufacturing sector report size and profitability as positively significant but networking capital as negatively significant to dividend paid by the firm.

To evaluate whether our model is correctly specified, we use two criteria: the Arellano and Bond test (1991) for zero autocorrelation and Sargan test (1958) for over-identifying restrictions also known as j-statistics. In the first test, we found that both first order and second order p values do not allow us to reject null hypotheses which says that there is no autocorrelation in the model specified for both the sectors. The second test for over-identifying restriction also rejects null hypotheses of over-identifying restrictions. Hence, we can say that the models used for analysis are appropriate and applicable to both the sectors.

Conclusion

The study explores the dividend behaviour of the manufacturing and service sector firms listed on the BSE. It is found that manufacturing firms are more efficient in terms of dividend pay-outs in comparison to service sector (59.63 per cent in comparison to 34.33 per cent). This illustrates that manufacturing sector is much more consistent and stable as compared to service sector for dividend declarations. Detailed analysis suggests that firm size and cash holdings positively influence dividend policy, whereas age and net working capital has negative effect for service sector. This shows that firms with more cash holdings and large firm size have higher chances of declaring dividends. Older firms pay lesser dividends than younger firms, and high net working capital will diminish the likelihood of dividend payments for the service sector. The analysis of manufacturing sector suggests that profitability and firm size are positively significant while networking capital is negatively significant. This implies that profitability is an important factor for manufacturing sector than service sector and net working capital is found to be negatively significant for both the sectors. The results illustrate the need for internal funds which reduce chances of dividend payments irrespective of sector to which a firm belongs. Also, it explains that higher profitability does not necessarily convert to higher dividend declarations for service sector. Age is a major factor for service sector but statistically insignificant for manufacturing sector. The result signifies that older service sector firms are likely to pay dividends, whereas manufacturing sector lacks any such evidences. Younger firms may choose to hold cash and defer dividend payment because of higher growth prospects in service sector implying better investment opportunities. Other factors are found insignificant in either one or all the methods used for analysis. Finally, we do not find any significant differences regarding fundamentals apart from variance in terms of sensitivities of the variables to dividend payments. However, manufacturing firms are more inclined to dividend payments in comparison to service sector which is reported empirically in the study. The counter intuitive results in service sector can overall be attributed to the expectation of higher returns from business opportunities, especially in the case of younger firms.

The study offers insights to both the firms and investors to understand the dividend behaviour of manufacturing and service sector firms. The managers can work on the significantly influencing factors to keep an equilibrium of the investors’ sentiments on the profit distributions. It will also help to understand the sectoral divergence dividend behaviour of firms. India is a developing economy, and results can also be used to understand the dividend behaviour of the countries with similar structure of manufacturing and service sectors, especially South Asian economies. This study is limited in terms of capturing macroeconomic factors that help a particular sector to grow rapidly because of government policies such as foreign direct investment (FDI) or tax subsidies.

The future research may be conducted by considering both micro and macroeconomic factors together to understand the effects of macroeconomic factors. Also, multiple industries can be included in the study to improve the application of the results.

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.