Abstract

Plastic cards are the neglected innovation as far as its research on diffusion and adoption from bankers’ perspective is concerned. The study emphasizes on the identification of factors which may have influenced the banks to adopt Automated Teller Machine (ATM) cum debit cards along with their traditional banking services. Bank-specific variables were investigated to deepen the understanding of the diffusion and adoption of ATM cum debit cards. The sample of the study is confined to 50 commercial banks, out of which 23 are private and 27 are public sector banks. The empirical findings reveal that size, non-interest income, non-performing assets, profitability, age and market share of the bank are the variables which have contributed significantly in the diffusion and adoption of ATM cum debit cards. The present study would serve as the roadmap for the regulators to frame policies and guidelines while introducing new technology in the industry, which are best suited to customers as well as bankers.

Introduction

Diffusion is the process through which innovation is spread across ultimate users. It includes all those activities which ultimately help the innovation to reach the social system by various communication channels (Rogers, 1995). However, adoption and diffusion could be seen as the two sides of the same coin (Sarosa, 2007), as diffusion of innovation helps the final adoption of innovation by ultimate users. Then again, it is the individual adoption decision which enables the new technology to diffuse completely throughout the system (Khan, 2004). Thus, the main objective of diffusion is to convey the innovation message and encourage the potential adopters to accept the innovation. However, in order to capture how new products and services spread in the system, managers should try to understand how the interactions among individuals and within the system contribute to the adoption of new products. Hence, technology can diffuse in multiple ways and with significant variations, depending upon the particular technology, across time, over space and between different industries and enterprises (Frei, Harker, & Hunter, 1998).

Innovation is the key to transforming people’s lives. It is widely recognized that innovation plays a crucial role in improving efficiency and productivity. Scientific research and novel technologies deliver real benefits only when innovators appropriately apply them to improve the lives of ordinary people (Melnick & Melnick, 2007). Thus, the objective of innovation in the financial market can be diverse as it can be understood as something new which is supposed to reduce costs, risk, or provide improved product, service, that better meets needs of demand of financial market’s participants demand. Hence, in the financial sector, the main entities participating in the creation, implementation and taking advantage of innovation are financial institutions, customers, regulation institutions, technology suppliers, society as a whole and also entities from the organization itself such as owners, workers and managers.

It is diffusion rather than invention or innovation that ultimately determines the pace of economic growth and the rate of change of productivity (Hall & Khan, 2002). Hence, technology can diffuse in multiple ways and with significant variations, depending upon the particular technology, across time, over space and between different industries and enterprises (Frei et al., 1998).

Thus, the main objective of diffusion is to convey the innovation message and encourage the potential adopters to accept the innovation. However, in order to capture how new products and services spread in the system, managers should try to understand how the interactions among individuals and within the system contribute to the adoption of new products.

The technological trajectory helped banks in satisfying the mass consumption of banking services, increasing return to scale and enhancing their ability to expand in size with the installation of innovations in product and services (Buzzacchi, Colombo, & Mariotti, 1995). Electronic banking innovations have thus become a strategic weapon that no bank can ignore. Plastic cards can be referred as one of the innovations with non-clerical and customer self-serve banking channel (Chen, 1999). However, in spite of the striking potential benefits, many banks still hesitate to adopt or fail to implement plastic cards successfully. According to Frame and White (2004), banks generally do not have a reputation for rapid adoption of innovative technologies. Nevertheless, new technologies eventually enter the banking sector, as banking firms are profit maximizers.

Hence, there are various basic questions which need to be explored in the Indian banking sector. Why did some banks adopt electronic banking earlier than the others? Why and how did banks vary in the extent of implementation of innovative products? In the present study, the main objective is to explore the factors which may have helped to drive the plastic cards innovation in the Indian banking sector. In light of this, the study has thus tried to unfold various questions: does time really matter in the diffusion process? If yes, then what are the various determinants significantly affecting the diffusion of plastic cards? Is adoption the function of variability in bank-specific characteristics? If yes, how much do these factors affect the decision of adoption by banks?

The availability of different types of cards in the banking industry like Automated Teller Machine (ATM) cum debit cards, credit cards and smart cards, which suit to different type of customers has brought in many diversifications. The oldest one out of these is ATM cum debit cards which had been adopted by all the commercial banks in India by 2007. It took almost 20 years to diffuse ATMs in India entirely since its introduction in the Indian banking sector in the year 1987. The ATM has both process and product innovation characteristics. As a process innovation, it substitutes the automated delivery of services. However, the ATM additionally offers services not previously available; for example, 24 hours a day access and cash provision in locations remote from bank branches. Moreover, the ATM is also a product innovation, with implications for consumer demand (Haynes & Thompson, 2000). The present study aims to describe the various determinants which tend to affect the adoption and diffusion of ATM cum debit cards in banks.

The present study has been divided into six sections. The first section describes the introductory part, while the second section reviews the existing literature. The third section focusses on the main objectives of the study. Apart from it, data collection methods, sample design and statistical tools used for the analysis have been enlightened in the fourth section. The fifth section assesses and predicts the determinants and adoption of plastic cards in the Indian banking sector. Finally, the sixth section of the study provides the summary of findings, implications and suggestions/recommendations of the current study.

Review of Literature

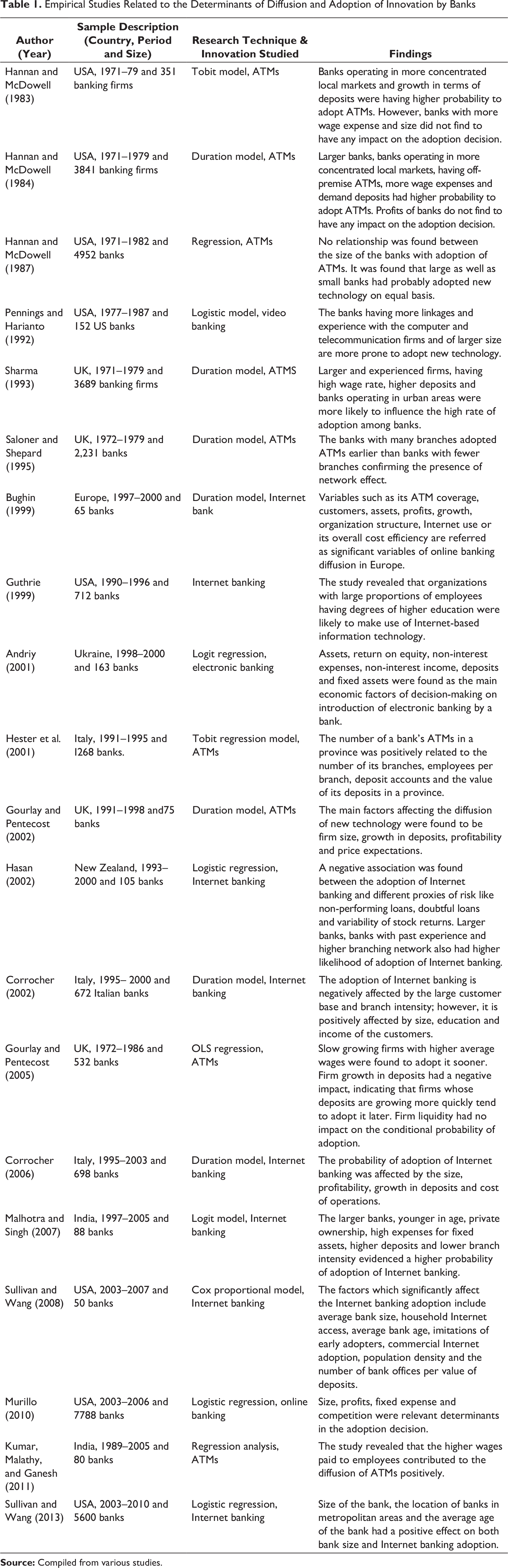

Diffusion theories provide tools, both quantitative and qualitative, for assessing the likely rate of diffusion of a technology and also identify the various factors which facilitate or hinder technology adoption and implementation. These factors include characteristics of the technology, characteristics of adopters and means by which adopters learn about and are persuaded to adopt the technology (Fichman, 1992). Much efforts have been made by different scholars across the countries to identify the determinants of diffusion of innovations in the banking industry.

Hannan and McDowell (1984) using a sample of 351 banks for the period of 9 years, that is, 1971–1979, found that larger banks and banks operating in more concentrated local banking markets were having a higher probability of adopting new technology. It was concluded that the interbank variables like wage, growth, profits and its location in the urban area had a positive impact on the probability of adoption of ATMs. Almost similar results have been reported by another study of Hannan and Mcdowell (1984).

Pennings and Harianto (1992), based on a sample of 152 of the largest 300 banks in the USA, covering a period of 11 years, that is, 1977–1987, found that previous experiences in the information technology in relation to a variety of inter-firm linkages affected the banks’ decision to adopt the innovation. Sharma (1993) also examined the impact of firm characteristics and market structure on the adoption of ATMs by banking organizations in the USA. The study found that larger firms, prior adopters in the market, high wage rate, higher demand deposits and banks operating in urban areas were more likely to influence the high rate of adoption among banks.

While studying the network effects, Saloner and Shepard (1995) used data of 2,231 banks for analyzing their adoptions level of ATMs in the UK. The study identified the average wage in the bank’s area, the bank’s labour expense per employee, the average number of branches per bank in the state, the growth rate of the bank’s deposits, the growth rate of all banks in the bank’s state and the concentration index for deposits in the bank’s state which might influence adoption. Moreover, the study showed that the banks with many branches adopted ATMs earlier than banks with fewer branches, which confirmed the presence of network effect.

Bughin (2003), and Guthrie (1999) tried to investigate the learning and doing effects on the adoption of innovation. Bughin (2003) attempted to model the S curve of Internet banking diffusion for a sample of 65 European major banks. He concluded that Internet literacy is a key determinant of online banking penetration. Moreover, it was also explained that various bank-specific variables such as its ATM coverage, customers, assets, profits, growth, organization structure, Internet use or its overall cost efficiency as a large part of the ‘S-curve’. On the other hand, Guthrie (1999) evaluated the use of Internet-based technology by US organizations and taking a sample of 712 organizations in the USA. The study revealed that organizations with large proportions of employees having higher education degrees were likely to make use of Internet-based information technology.

Gourlay and Pentecost (2002) investigated the role of firm and industry-specific factors in the diffusion of ATMs in the UK financial sector. The main factors such as endogenous learning, cumulative learning-by-doing effects, firm size, growth, profitability and price expectations, institution size, growth in deposits and profitability were found to have a positive and significant effect on the conditional probability of adoption.

Empirical Studies Related to the Determinants of Diffusion and Adoption of Innovation by Banks

Hasan (2002) described the current state of Internet banking in Italy while using the sample of 105 banks constituting over 80 per cent of the overall commercial banking assets in Italy, during the period 1993–2000. A negative association was found between the adoption of Internet banking and different proxies of risk like non-performing loans, doubtful loans and variability of stock returns. However, it has also been revealed that there was a higher likelihood of adopting active Internet activities by larger banks, banks with past experience and higher branching network.

Gourlay and Pentecost (2005) also studied the impact of network effects on the timing of adoption of ATMs by UK banks between 1972 and 1986 using regression models. The network effects were proxied by the number of branches a firm had and found that a one-unit increase in the number of branches increased the 1-year conditional probability of adoption, which ensures its impact. Slow growing firms with higher average wages were found to adopt it sooner. The average bank wage was found to have increased the rate for substituting ATMs for human tellers. Firm growth in deposits had a negative impact, indicating that firms whose deposits were growing more quickly tend to adopt it later. Firm liquidity had no impact on the conditional probability of adoption, indicating that there would be no funding constraints for ATM adoption.

The average age of a state’s banks also found to be significantly related to both website adoption and asset size. Corrocher (2006) attempted a study to examine the drivers of the adoption of the Internet banking and analyzed the role of firm-specific and non-firm-specific (technology, market and environment) characteristics in influencing the decision to adopt online banking transactions in Italy. It was found that the probability of adoption of Internet banking was positively affected by the size variable, meaning that large banks tend to adopt the technology more quickly than small banks. Malhotra and Singh (2007) attempted to discover the factors affecting a bank’s decision to adopt Internet banking in India. The results showed that the larger banks, banks with younger age, private ownership, higher expenses for fixed assets, higher deposits and positive branch intensity evidenced a higher probability of adoption of this new technology.

Murillo (2010) studied the determinants of banks’ decision to adopt a transactional website for their customers. The study showed that bank-specific characteristics such as size and standard measures of financial health were found as relevant determinants in the adoption decision. While Kumar et al. (2011) aimed at analyzing the substitution effect of ATMs with respect to the human tellers. The study revealed that the higher wages paid to employees contribute to the diffusion of ATMs positively. However, according to the study, ATM is not the perfect substitute for the tellers.

The voluminous studies and research have been conducted on financial innovation services. However, the maximum emphasis has been given on the adoption and diffusion of Internet banking and online banking (Bughin, 1999; Corrocher, 2002; Guthrie, 1999; Hasan, 2002; Kaur, 2010; Kumar, 2008; Malhotra & Singh, 2007; Murillo, 2010; Noor, Noor, & Ahmad, 2012; Pennings & Harianto, 1992; Sullivan & Wang, 2008). Few studies have also been conducted on the adoption and diffusion of ATM cards in different parts of the world (Gourlay & Pentecost, 2002; Hannan & McDowell, 1983, 1984; Hester et al., 2001; Saloner & Shepard, 1995; Sharma, 1993) other than India.

Plenty of information can be gathered on the nature and scope of innovation in banking, but there is least evidence about the adoption and diffusion of innovation by the banks. Moreover, empirical studies have taken into account the introduction of Internet banking the most. Thus, the diffusion and adoption of plastic cards by the banks have not done so far and is an untouched area. Furthermore, most of the studies were conducted in the developed economies like the USA, the UK and Italy as the adoption rate of new technologies and financial innovation is comparatively more there. While following these economies, the developing economies like India also try to match themselves with the need of an hour taking initiatives to incorporate innovations in their system. Thus, the factors influencing the banks’ decision to adopt new technology is an interesting area to explore in India too. The present study tends to fill the gap by analyzing the adoption pattern and diffusion of ATM cum debit cards in Indian banking Industry.

Objective of the Study

The need for banks to respond adequately and timely to the available opportunities becomes inevitable. But, whenever such an innovation floats in the industry, some firms respond quickly and adopt it at the early stage. However, some of them are there which do not plan to adopt till it becomes necessary for them to survive in the industry. From the above, it may be derived that the determination of factors affecting the decision of bankers towards plastic cards adoption becomes imperative. In light of this, the present study aims to explore the factors which may have helped to drive the diffusion and adoption of ATM cum debit cards in the Indian banking sector.

Database and Research Methodology

Sample Description

The sample of the study is confined to 50 commercial banks out of which 23 are private and 27 are public sector banks. Foreign sector banks have not been taken since the information regarding their adoption pattern is not available. The time period has been taken from the year 1991 to 2007 as the banks in the sample have already adopted the ATM cum debit cards till the year-end 2007.

The Regression Model

The study emphasizes on the identification of factors which may have influenced the banks to adopt ATM cum debit cards along with their traditional banking services. In order to analyze the effect of variables on the adoption decision, OLS regression has been applied. The number of years taken by the bank to adopt ATM cum debit cards has been taken as the dependent variable. Following model has been used to examine the effect of various explanatory variables on the time taken by the bank to adopt ATM cum debit cards.

where Y1 (TIME) is the dependent variable, that is, time taken by a bank (in years) to diffuse ATM cum debit cards into its operations.

and Xi are selected explanatory variables where i = 1, 2, 3,…, 10 (as per Table 2)

List of Determinants of Diffusion and Adoption of Plastic Cards in the Indian Banking Sector

Analysis

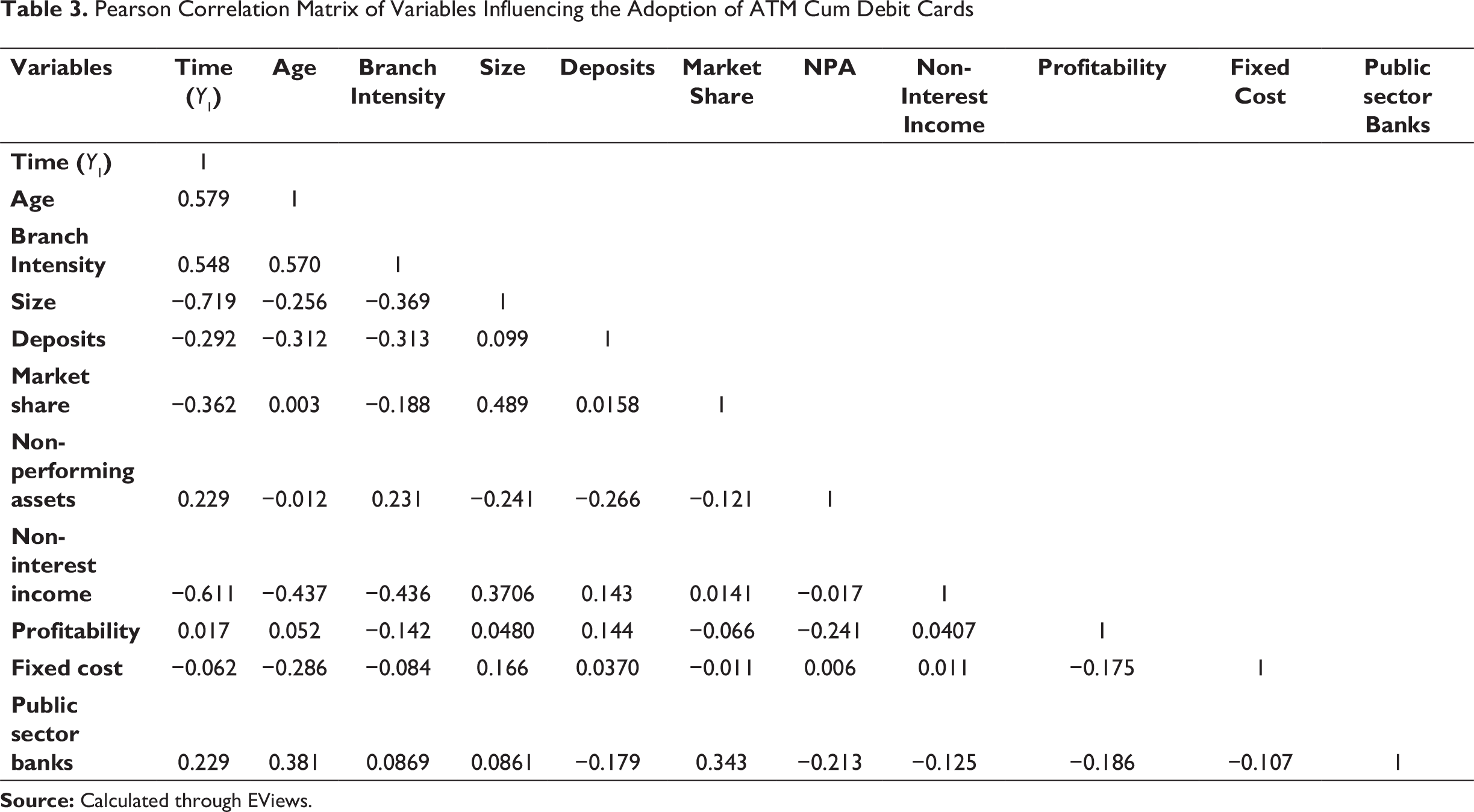

Firstly, to find out the significant determinants of diffusion of ATM cum debit cards, pairwise correlation of all independent variables and dependent variable (Time) were calculated. Table 3 reveals that several statistically significant correlations exist among dependent and independent variables. Time taken by banks to diffuse ATM cum debit cards into its operations (Y1) is significantly and positively associated with age, branch intensity, non-performing assets and profitability. Its negative association is observed with deposits, size, fixed cost, non-interest income and market share.

In order to check the problem of multicollinearity, Variance Inflating Factors (VIFs) values were computed for all the explanatory variables. The White procedure was used to ensure that the coefficient is not heteroscedastic. To check the autocorrelation in the disturbances ei, Durbin Watson statistics have also been computed. Hence, no problem of multicollinearity, heteroscedasticity and autocorrelation was found.

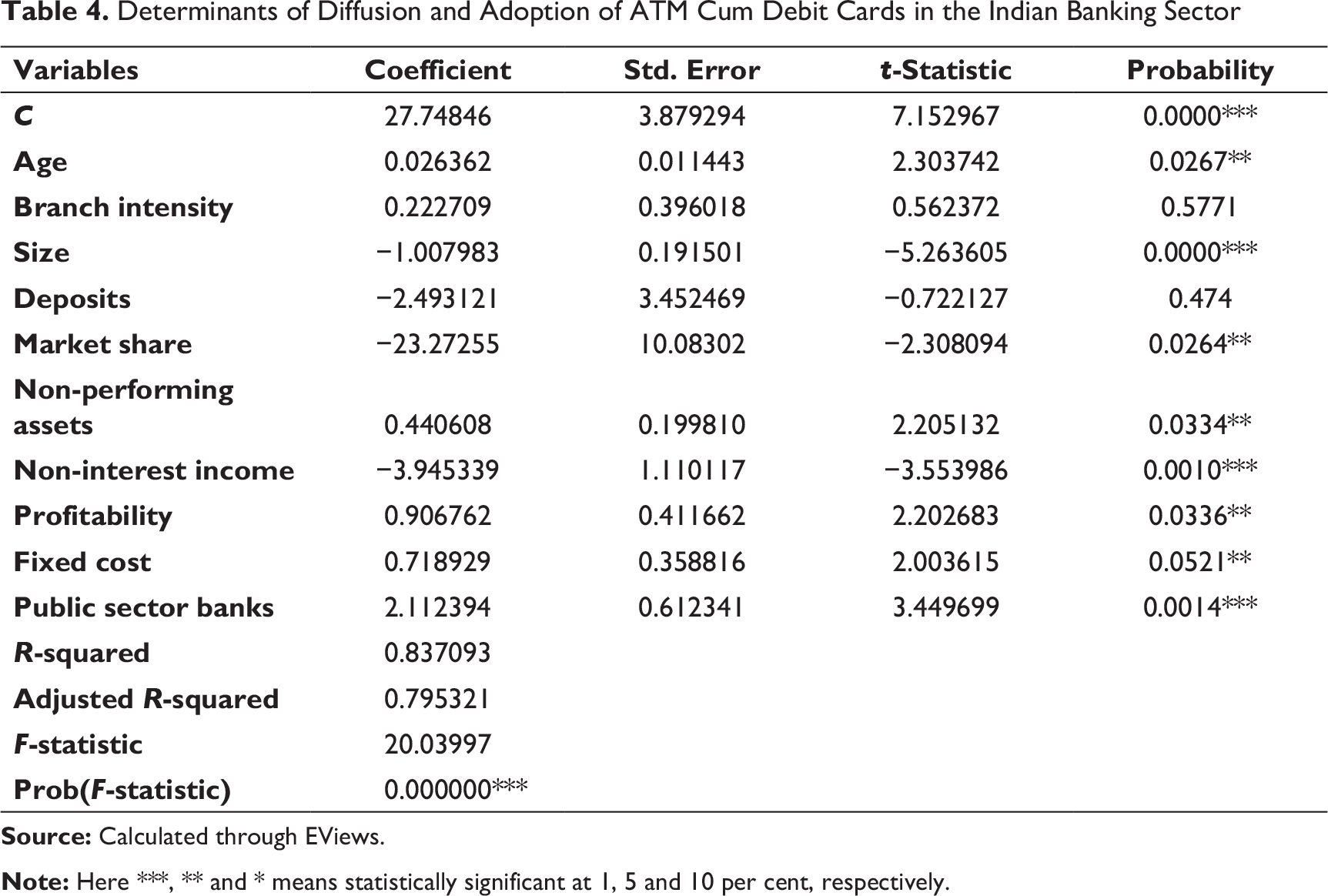

The results of the empirical model have been presented in Table 4. In the given table, F-statistics (F = 20.03, p = 0.000) is significant indicating the overall model is fit. It implies that the effect of variables cannot be assumed to be zero and have been significantly constructed to explain the diffusion of ATM cum debit cards in the Indian banks. It also means that the model is significant and better than the null model. Adjusted R-squared is calculated to measure the strength of association between dependent and independent variables. In the given model, adjusted R-squared is 79 per cent and thus having significant capacity to explain the variations caused by independent variables.

Pearson Correlation Matrix of Variables Influencing the Adoption of ATM Cum Debit Cards

Determinants of Diffusion and Adoption of ATM Cum Debit Cards in the Indian Banking Sector

The results of the regression analysis show that as the size of the bank increases, the banks tend to become more innovative and technological savvy. The value of the coefficient for variable size was found to be −1.007. It provides clear evidence that the large-sized banks took less time to adopt ATM cum debit cards. Profitability is one of the main measures to test the importance of liquidity constraints in funding the adoption of new technology. The total profits have been considered to estimate this variable. From this, it can be projected that with more profits the potential of the bank to install the new technology increases. While it may also be possible that the banks with less profits will have more urge to implement new technology so as to improve their performance and meet the competitive edge in the market. However, Corrocher (2007), Malhotra and Singh (2007) and Sullivan and Wang (2013) did not find any significant relationship between the profitability and adoption decision of the new technology.

As per the given results, profitability (b = 0.9067, p = 0.0336) has also been reported to have a significant relationship with the diffusion of ATM cum debit cards in India. The results thus show that the more profitable banks are reluctant to adopt ATM cum debit cards in India. In other words, it implies that the banks with less profit have a tendency to adopt new technology at an earlier stage so as to improve the profits in future by providing new value-added services to their customers. The findings of the study are similar to the findings of Hester et al. (2001), Corrocher (2006), Malhotra and Singh (2007), Sullivan and Wang (2008) and Saloner and Shepard (1995).

The introduction of plastic cards may have the tendency to diminish the infrastructure cost of the banks in the long run. The banks with high fixed cost may adopt the new innovation much easily so that the cost can be reduced in the future. However, in the short run, when a bank decides to install new technology, the infrastructure expenses or fixed cost of the organization may increase instantly (Andriy, 2001; Furst et al., 2002a). It gives the other viewpoint that banks who already have incurred huge infrastructure expenses may not afford to install new technology so quickly. Further, Andriy (2001) and Furst et al. (2002b) observed that a bank incurring large portion of expenses on its infrastructure, try to avoid the adoption of innovation as it can further enhance its cost in relation to fixed assets and premises. According to the results, fixed assets having a value of coefficient of 0.718 are significantly affecting the diffusion of ATM cum debit cards in India. The empirical findings of the study thus reveal that the banks with more investment on fixed assets and premises adopted ATM cum debit cards very late.

Deposits play a dual role. Deposits, on the one hand, represent the traditional source of funding for the bank while, on the other hand, it can be regarded as banks’ overall customer base. The increase in deposits can be described as a proxy of trust of the customers for the banks as they put their money into it. More the customer base of the banks and more there is the likelihood to take up the new technology. However, some of the researchers found it negatively related to the adoption of innovation. Andriy (2001) and Furst et al. (2002a) suggest that the banks which are less reliant on traditional sources of funding may have more aggressive business strategy including the adoption of new products. The findings also reveal that branch intensity (b = 2.49, p = 0.47) and deposits (b = 0.222, p = 0.577) have not contributed in predicting the determinants of diffusion of ATMs cum debit cards in India. These findings of the study coincide with the findings of Sharma (1993), Andriy (2001) and Hester et al. (2001).

Furthermore, the variable age reporting beta coefficient of 0.263 was also found to be an important determinant of diffusion of ATM cum debit cards. It signifies the experience of the bank in handling business in terms of the years since it has been incorporated. The younger banks have a tendency to adopt the innovation at an earlier stage (Arnaboldi & Claeys, 2010; Carlson, Furst, Lang, & Nolle, 2001; Crietie et al., 2009; Furst et al., 2002b; Hernando & Nieto, 2006; Malhotra & Singh, 2007; Sullivan & Wang, 2013). The results in the present study indicate that older banks take more time to adopt ATM cum debit cards as compared to younger ones.

One of the measures of the aggressiveness of the bank’s business strategy is the magnitude of non-interest-based transactions in proportion to its gross income. It has been hypothesized that banks who have greater reliance on non-traditional revenue are more likely to view new technology as a way to market fee-generating services, and are more likely to adopt innovative services as part of an overall aggressive business strategy (Arnaboldi & Claeys, 2010; Carlson et al., 2001; Crietie et al., 2009; Furst et al., 2002a; Hernando & Nieto, 2006; Malhotra & Singh, 2009). Non-interest income (b = −3.94, p = 0.0010) was found to be significantly affecting the diffusion of ATM cum debit cards in India. The banks which have more non-interest income are likely to be more diversified or modernized, and thus, would try to offer new value-added services or products to customers. The present study also reports that diversified banks have adopted ATM cum debit cards soon. The given results are in agreement with the previous researches like Corrocher (2002), Furst et al. (2002b) and Andriy (2001).

Asset quality can be estimated by the amount of non-performing assets (NPAs) of the banks. It can be considered as a proxy of credit risk also. Banks with lesser non-performing assets can be considered as efficient ones. It represents that managerial efforts put on by banks are positive and banks are efficient enough to manage its functions and funds. Efficient banks would tend to introduce new services and grow quickly. According to Furst et al. (2002a), on average, the banks having less NPAs are more efficient and safe which leads to the early adoption of technology. In other words, NPAs represent the inefficiency of the banks for handling the assets and make them unable to introduce new products. As per the results, the value of the beta coefficient for non-performing assets, that is, 0.440, was found to be negatively associated with the diffusion of ATM cum debit cards and the results are empirically highly significant too. This finding of the study is similar to the findings of Hasan et al. (2002) and Murillo (2010). It can thus be concluded that the banks having more sub-standard assets adopt the new technology at less pace.

Market share represents industry advantage of the bank. Banks having a large share in the form of deposits in the industry would have more chances to install new technology. It is thus expected that if the banks’ market is growing, the value of the investment on innovation will be more as the bank expects to capture a share of the new depositors too (Saloner & Shepard, 1995). Market share of the banks in the industry has also been widely studied by most of the researchers (Corrocher, 2002; Hasan et al., 2002; Malhotra & Singh, 2007; Murillo, 2010; Sullivan & Wang, 2013). The empirical results also found market share value of the coefficient of −23.27 as one of the encouraging factors for the diffusion of ATM cum debit cards in India. It means that the banks having more share in the industry in terms of assets have the tendency to adopt ATM cum debit cards at an earlier stage.

The ownership of the bank is also one of the main determinants which may affect the adoption decision of the bank. In general, it is the belief that the banks owned by the public sector are reluctant to adopt the new technology as compared to private sector banks. It may be due to the fact that some public sector banks are well established and experienced with a sufficient number of customers, branches and deposits and thus are less competitive, while the private sector banks are supposed to bring competition in the market by taking the risk and making the new technology readily available to the customers soon so as to raise the market potential (Bughin, 1999; Guthrie, 1999; Gourlay & Pentecost, 2002). On the other hand, it can also be depicted that public sector banks may have more potential to take risk regarding the installation of new services and products than that of private sector banks due to its strong customer base, expanded branch network and more market share.

The relationship between public sector banks and the time taken to diffuse the ATM cum debit cards have been found positive and statistically significant reporting the value of the coefficient, that is, 2.112. It means that the public sector banks took more time than private sector banks to fully adopt the technology into their system. In other words, private sector banks can be recognized as early adopters in the industry.

To conclude, the empirical findings reveal that size, non-interest income, non-performing assets, profitability, age and market share of the bank are the variables which have contributed significantly in the diffusion and adoption of ATM cum debit cards. Also, size, market share and non-interest income are positively associated with the diffusion of ATM cum debit cards, while age, profitability, fixed cost and non-performing assets are found to have a negative association with the diffusion.

Conclusion

The empirical results regarding the determinants of diffusion and adoption of ATM cum debit cards show that private sector banks were eager to adopt new technology rapidly as compared to public sector banks. Also, the size of the bank plays an encouraging and dominant role in the adoption decision. It depicts that the banks which are comparatively larger in size and possess more assets have the capacity to innovate at a greater pace. Market share as an industry advantage also plays a significant role in taking decision regarding the adoption of cards by banks. It positively and significantly affects the diffusion and adoption of ATM cum debit cards. It can be finally said that banks take advantage of their industrial competence and thus try to be more innovative. Other remarkable results report that the more diversified banks, which earn non-interest income fetched by modern services and products, have more propensity to adopt plastic cards.

Deposits of the bank enhance the likelihood of the banks to adopt plastic cards. Notable results have been observed in the case of the age of the bank. Younger banks are found to be keen to adopt ATM cum debit cards. Profitability has also shown noteworthy results. In the case of ATM cum debit cards, the less profitable banks were found to adopt it sooner. NPAs as a measure of credit risk also reported a significant impact on the adoption decision only in case of ATM cum debit cards. Apart from it, another variable, that is, fixed cost, has been found to have a significant and negative impact on the adoption of ATM cum debit cards. As the installation of ATMs involves huge cost, only the banks with less infrastructure investment were found to adopt ATM in their system. Last but not least, branch intensity representing the geographical network of the banks has not influenced the diffusion and adoption of ATM cum debit cards.

Implications of the Study

The results of the study are reliable and authentic in the sense that data have been collected from authentic sources and further the tests conducted for the empirical analysis are best suited accordingly to the objectives stated. The current study is expected to be of great use to the regulators, commercial banks, other financial institutions, bank customers and other service providers. The study has also analyzed the various determinants which affect the decision of banks regarding the diffusion and adoption of plastic cards. Thus, a comprehensive model has been developed which can assist the bankers to check the rate of success of upcoming innovation within the industry. The present study may help the regulators to frame policies and guidelines while introducing new technology in the industry which are best suited to customers as well as bankers.

Recommendations and Limitations of the Study

The present study found that the adopter banks of plastic cards had a comparatively larger share in the market. Hence, in order to enjoy industry advantage in the long run, the banks must try to expose themselves in the market by adopting new products and services earlier. Also, non-interest income of the banks was found to be significantly affecting the diffusion of plastic cards in India. Thus, the findings of the study recommend that the banks should try to diversify themselves to adapt to the changes in the industry. The results also suggest that the banks must try to reduce the non-performing assets so as to improve its asset quality, which ultimately leads the bank to be more innovative. The adoption of plastic cards has helped the banks to reduce its labour cost too. So, the banks should try to shift from the traditional banking system to a modernized one as soon as possible.

The sample of the study was limited to the scheduled commercial banks only. The co-operative banks offering plastic cards were not considered in the sample of the study. The other limitation is that foreign sector banks have not been considered while analyzing the determinants of diffusion of ATM cards by banks due to non-availability of data. Due to non-availability of some data from published reports, other published documents and websites of the selected banks; the study relies upon the responses of officials of some of the banks for getting the information regarding their adoption pattern. The information can be biased.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.