Abstract

The integration of the world economies is responsible for an increase in the number of cross-border mergers and acquisitions (M&A), together with the growing participation of companies from emerging countries in this type of investment. However, the area studies focus their analyses on the determinants, antecedents and profitability of the companies, leaving the effects of this type of business on the operational risk of the companies involved as a gap to be explored. To fill it, we used panel data regressions to identify the relationship between cross-border M&A and the operational risk of companies. The results indicate that acquiring companies based in emerging economies are the ones that suffer the most significant impacts on this type of business. As the implication, this study serves as a basis for the decision-making of the managers of the acquiring companies, being able to identify the risks of this activity and the ways of preventing them.

Introduction

The volume of cross-border mergers and acquisitions (M&A) has been growing in recent times. In the year 2017, this type of business represented 36 per cent of the M&A performed worldwide (Morgan, 2017). According to Erel, Liao, and Weisbach (2012) the reason for cross-border M&A is conceptually the same as domestic M&A, competitive advantages and consolidation and growth of the company. However, cross-border M&A adds additional concerns to companies that make such an investment, such as the synergistic effects between assets, real and potential competitors, as well as increased complexity and expenditures for being in markets with characteristics different.

Factors such as institutional distance and differences in accounting, economic and legal standards are responsible for the increased difficulties, costs and risks of cross-border M&A compared to domestic M&A (Chari & Chang, 2009; Erel et al., 2012; Kogut & Singh, 1988; Yang, 2015). These factors have been discussed in the literature, and several studies have demonstrated how the theme develops over the years, especially in developed countries (Chari & Chang, 2009; Kogut & Singh, 1988).

One of the possible explanations for the majority of the research focussed on companies from developed economies may be the fact that these companies were ahead of the companies of emerging economies about the level of Direct Foreign Investment and, consequently, the number of M&A. However, it can be seen that, over time, companies from emerging economies have increased their participation in this type of investment. So much so that cross-border M&A can be characterized as the primary strategy of entry into the global market for this type of company (Dikova, Sahib, & Van Witteloostuijn, 2010; Erel et al., 2012; Kogut & Singh, 1988; Yang, 2015). Some authors explain this increase from globalization and increasing economic integration between countries (Erel et al., 2012; Yang, 2015).

Yang (2015) states that in addition to the increased participation of companies from emerging economies, there has also been an increase in the number of studies on the subject. The vast majority focus their efforts on understanding the investment flows and quantity of M&A undertaken. As well as in identifying the determinants, antecedents and profitability of the companies involved (Dikova et al., 2010; Erel et al., 2012; Kogut & Singh, 1988; Yang, 2015).

Thus, there is a gap in the literature regarding the understanding of the relationship between cross-border M&A and the risk of the companies involved, particularly operational risk, which is related to possible losses with inadequate systems and controls, management and human error. More specifically, the operational risk is the risk arising from the execution of a company’s business functions. The Basel II defines operational risk as the risk of loss resulting from inadequate or failed internal processes, people and systems, or from external events (Sun & Chang, 2011). The only study found on the subject was conducted by Mandelker (1974) and listed the variations in risk and return of companies to M&A events. However, despite its contribution, the author analyses only the specific case of North American companies.

In order to fill this gap, the effects of cross-border M&A on the operational risk of acquiring companies will be explored, considering the differences between the intrinsic characteristics of firms in developed economies and those in emerging economies. In order to do so, the following question is addressed: What are the impacts of cross-border M&A on the operational risk of companies from developed economies that acquire companies from developed and emerging economies?

The overall objective is to verify how intrinsic cross-border M&A factors affect the post-acquisition operational risk of developed economies engaged in acquisitions with target companies from emerging and developed economies. To that end, companies from the emerging economies were those belonging to Latin America and as developed economy companies those belonging to North America, specifically companies from Canada and the USA.

The main contribution of this research is to foment the discussion on cross-border M&A involving companies from developed and emerging economies and their specificities. The study is a precursor in analysing the effects of such investments on the operational risk of acquiring companies by comparing those that buy targets from developed economies with those from emerging economies.

The rest of the article is organized as follows. The second section presents the review of literature and the research hypotheses while the third section handles the methodology. The fourth section presents and discusses the empirical findings and their interpretation. Lastly, managerial implications and conclusion are contained in the fifth section.

Literature Review

Mergers and acquisitions have been pursued by companies as an important growth strategy (Ranju & Mallikarjunappa, 2019). Domestic and cross-border M&A happen for a common reason, gaining synergy (Erel et al., 2012). In other words, companies carry out this type of investment when, from the acquirer’s perspective, there is an expectation of creation or gain in value. For Liu and Qiu (2013), M&A participating companies, whether domestic or cross-border, performed better than non-participants. Also, acquiring companies perform better than acquired ones, and cross-border M&A are more profitable than domestic ones.

In contrast, some authors (Erel et al., 2012; Narayan & Thenmozhi, 2014; Yang, 2015) state that cross-border M&A have higher levels of complexity than domestic ones, since there are differences between countries, their cultures, legislation and other factors that contribute to the increasing difficulties of integration between the parties. Some of these differences have been studied through the analysis of the institutions present in each country (Dikova et al., 2010; Kogut, 1988; Yang, 2015).

In the present study, starting from Yang (2015), institutional distance is used to capture the differences between the countries of acquiring companies (developed economies) and target companies (emerging economies) in the development of formal institutions. This is because, although emerging economies have undergone a profound institutional transformation, firms in these markets remain distinct from developed market institutions (Wan, 2005).

A greater institutional distance between the country of the acquiring company and the target firm’s nation suggests an increase in the acquirer’s risk due to a lack of knowledge of local business institutions and shops (Contractor, Lahiri, Elango, & Kundu, 2014). In other words, the higher the institutional distance, the greater the uncertainty about the availability of the resources necessary to maintain the acquirer’s operating activities (Contractor et al., 2014). As a result of this, the firm has been able to adapt to the needs of the target firm in order to meet the needs of the target firm (Chen & Hennart, 2004; Contractor et al., 2014; Demirbag, Ng, & Tatoglu, 2007). This context gives rise to the first hypothesis of this research.

H1: Institutional distance is positively related to the operational risk of the acquiring company at the time of acquisition.

In addition to studies that deal with the differences between the countries in which firms invest, some authors have analysed the relation between the companies’ operational performance (Heron & Lie, 2002; Servaes, 1991), past experience (Haleblian, Kim, & Rajagopalan, 2006; Levitt & March, 1988) and the M&A event.

Using Tobin’s Q as a metric for the company’s operating performance, Servaes (1991), observed that acquiring firms obtain higher returns by acquiring companies that have lower Tobin Q’s. Heron and Lie (2002) used a different proxy, the market to book ratio, but the results were similar. Thus, the literature has demonstrated the existence of a positive relationship between the firm’s market value and its post-acquisition performance.

Although there were no studies that correctly verified the effects of market value or firm’s operational performance on its post-acquisition operating risk, the proportional relationship between risk and return is a consensus in finance (Markowitz, 1952). Therefore, it is possible that the increase in the value of the company has a positive effect on the operational risk after the acquisition. Also, it is believed that this effect is more significant in cases where the acquiring company comes from a developed economy nation and the target of an emerging economy. Thus, the following hypothesis is postulated here:

H2: The firm’s market value is positively related to the operational risk of the acquiring company at the time of acquisition.

Levitt and March (1988) present an organizational learning interpretation that is based on the premise that organizations make decisions and carry out actions focussed on objectives, based on a pre-established routine and a history of actions past. In this sense, Haleblian et al. (2006) argue that a company’s chance of acquiring an acquisition increases when its experience in this type of event also increases, especially if the performance in the previous acquisition is positive.

However, successive acquisitions can increase company size and diversity, especially when companies from developed economies acquire companies from emerging economies (Aktas, Bodt, & Roll, 2013). This increases the integration costs and the operational risk of the firm. This argument leads to the third hypothesis of this research.

H3: The operating risk of the acquiring firm is positively influenced by its experience in acquisitions (volume of acquisitions).

Objective

The objective for this article is to verify how intrinsic cross-border M&A factors affect the post-acquisition risk of developed economies engaged in acquisitions with target companies from emerging and developed economies.

Methodology

Data Source and Sample Frame

The companies that comprise the sample of this research are non-financial publicly held companies based in developed countries that have acquired companies from other developed countries and emerging countries. The data required for the empirical tests were collected from the Thomson Eikon Database as well as the financial and market information about the sample companies.

In order to form the sample of acquiring companies, the businesses codified as mergers or acquisition of controlling interest were selected and concluded in the period between 1 January 1996 and 31 December 2017. Following the literature on the topic, among the companies identified, we retain an acquisition only if the acquirer owns less than 50 per cent of the target firm prior to the bid, is seeking to own more than 50 per cent of the target firm and owns more than 90 per cent of the target firm after the deal completion (Bena & Li, 2014).

The data needed to calculate the institutional distance were taken from the World Bank’s online database. The data correspond to six indicators that seek to capture the perceptions about the quality of the formal institutions, policies and governance of the countries to which they refer (Kaufmann, Kraay, & Mastruzzi, 2011). The six indicators are voice and accountability, political stability and absence of violence/terrorism, government effectiveness, regulatory quality, rule of law and control of corruption.

The voice and accountability indicator is linked to people’s participation in politics, freedom of speech and print, ultimately being related to democratic values. Political stability and absence of violence/terrorism are related to the perception of political stability and political risk. The indicator called government effectiveness relates to the perceived quality of public services and public policies in the country.

The regulatory quality indicator is linked to government actions, regulations and legislation that favour and promote private sector development. Rule of law represents the perception of the quality of laws, combating crime, violence, terrorism and guaranteeing rights, especially the right to property. Finally, we have the control of corruption linked to the perception of the state’s ability to control and suppress corrupt practices (Kaufmann et al., 2011). The methodology used to convert the six indicators into the institutional distance measure is presented in the section on independent and control variables.

Model Variables

Dependent Variable

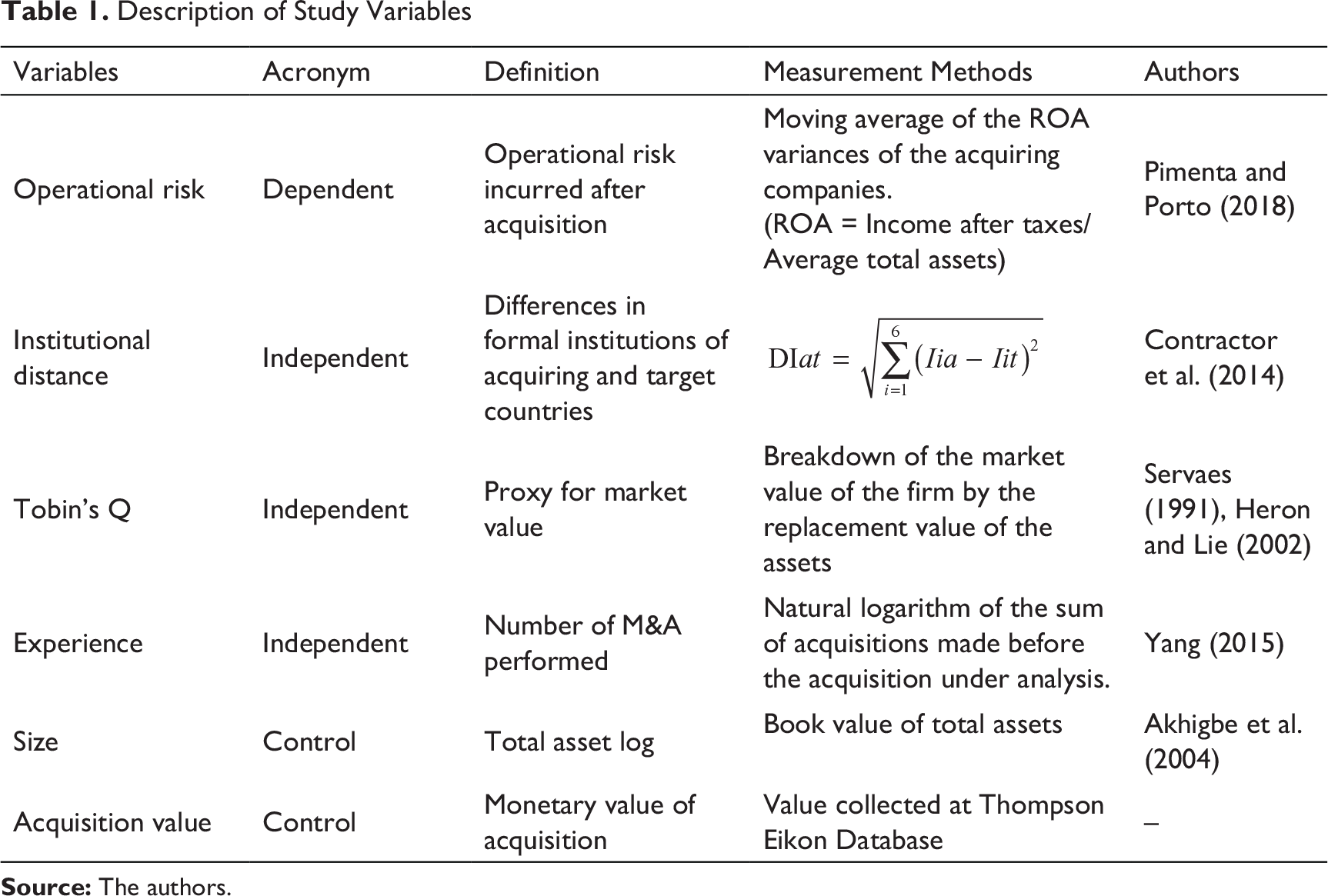

The dependent variable of this study is the operational risk (RISK) incurred by the company after an acquisition. Along with capital market measures of risk, accounting operational measures of historical fluctuations in an income stream are among the most common risk measures employed in strategic management research, such as the return on assets (ROA) variance and the return on equity (ROE) variance (Miller & Bromiley, 1990; Sun & Chang, 2011). In this article, we chose ROA variance as an operational risk indicator due to its potential for representing the interests of organizations stakeholders (Alghifari, Triharjono, & Juhaeni, 2013). Return on assets was measured by dividing income after taxes by average total assets.

In longitudinal studies, the measure of risk as variance in returns may pose problems if the risk measure spans multiple stages of the business growth. Such risk measures will fail to differentiate different environmental contingencies. An alternative approach would be to design a refined measure of risk based on fewer years’ data (Chang & Thomas, 1989). Thus, our dependent variable is calculated by three period moving average of the variances of the ROA of the acquiring companies and aims to capture the uncertainties and volatility of the company’s performance under analysis after the acquisition.

Independent and Control Variables

The independent variables of the present study are institutional distance, capitalization of actions and experience. Institutional distance seeks to capture the differences in the formal institutions of the acquiring and target countries, and the greater this distance, the greater the differences between countries. Its calculation is based on the Contractor et al. model (2014), which follows below in Equation (1):

where DIat is the institutional distance between the acquiring country ‘a’ and the target country, ‘t’. Iia represents the value of the ‘i’ indicator for the acquiring country and Iit the value of the ‘i’ indicator for the target country.

The second independent variable is Tobin’s Q. It will serve as a proxy for market performance (Heron & Lie, 2002; Servaes, 1991). Tobin’s Q was measured based on the division of the firm’s market value by the asset replacement value (Fu, Singhal, & Parkash, 2016).

The experience, in turn, captures the number of M&A made previously by the same acquiring company. This variable will be measured by the natural logarithm of the sum of acquisitions made before the acquisition under analysis (Yang, 2015). The control variables are the size of the company and the value of the acquisition. The firm size was measured by the logarithm of the total assets (Akhigbe, Madura, & Whyte, 2004).

Already the value of the acquisition is the one collected in Thompson Eikon Database. Table 1 presents the description of the variables used for analysis, as well as the authors who have already used the same metrics in their empirical investigations.

Empirical Model

Description of Study Variables

The first is composed of acquiring companies from developed countries, and the target of countries with economies also developed. The second one is made up of acquiring companies from countries with a developed economy and targets from countries with an emerging economy. Also, the square term of the experience variable will be inserted into the regressions so that evidence can be found on the relationship between increased M&A experience and corporate risk.

Before starting the estimation of the models, tests were carried out to verify their suitability. The first tests indicated the presence of heteroscedasticity (Breusch–Pagan test) and autocorrelation (Wooldridge test). As a way to overcome these problems, robust standard errors grouped at the firm level were applied. The variance inflation factor (VIF) of the predictor variables of the models was also calculated. In none of the cases did the results indicate the presence of multicollinearity.

As a way of minimizing possible problems of omitted variables, considering the heterogeneity not observed, it was chosen to estimate the models with fixed effects. To confirm the suitability of this choice, the Hausman test (1978) was used.

Significant test results (p-value < 0.00) allowed us to reject the null hypothesis and accept that the fixed effects model is more appropriate since there is strong evidence that the firm-specific effects in the random effects model are correlated with the explanatory variables (Pimenta & Porto, 2018). The regressions were estimated for each study group, according to the basic model presented in Equation (2).

Where

Analysis of Results

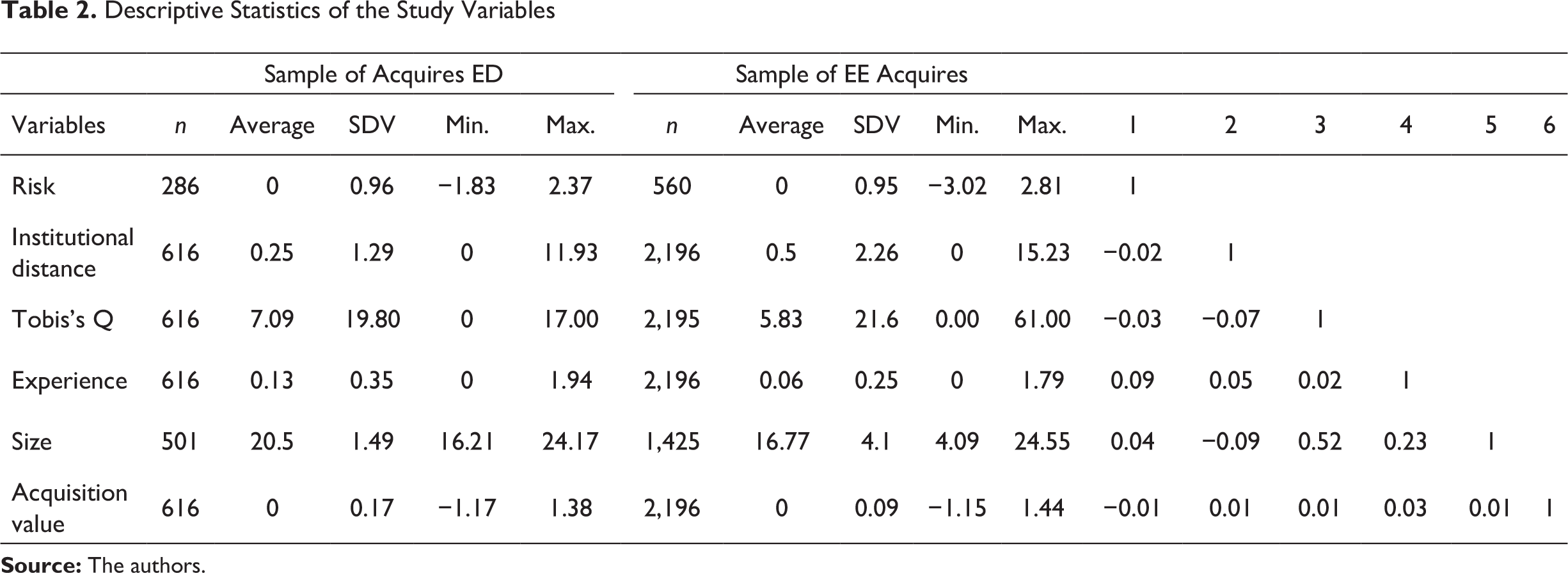

Table 2 presents the descriptive statistics and the correlations of the variables involved in the study. Attention is drawn to the averages of stock capitalization and company size since it is observed that companies located in emerging economies have lower values when compared to the averages of companies located in developed economies. We can see values around 1.22 times higher, which was already expected given the distinct development between both markets.

Another aspect that requires attention is the difference between the means of the experience variable. There is an average value of 0.13 when referring to companies from developed economies compared to 0.06 when referring to companies from emerging economies, more than double. Given that this variable measures the amount of M&A made by the acquirers, we can say that the acquisitions of companies from developed economies are twice as large as the acquisitions of companies from emerging economies.

Descriptive Statistics of the Study Variables

Regressions with Dependent Variable Risk Without the Square Term of the Experiment

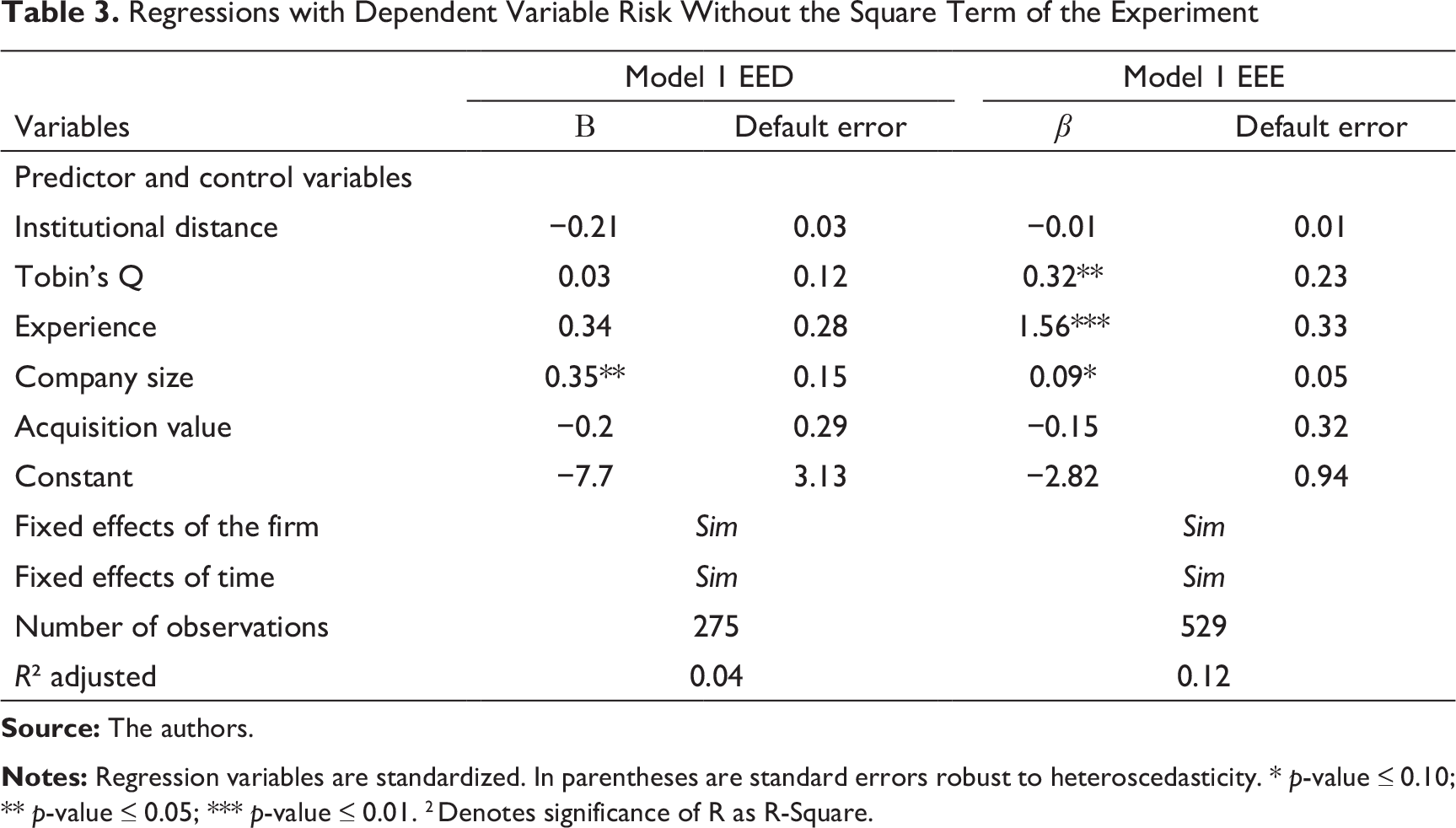

In this first example, the case is verified for a sample of investment firms that bought other companies with the same information. There is a total of 275 notes and a coefficient of explanation of about 4 per cent, with the coefficient of the company size variable being the only significance (p-value ≤ 0.05). However, it is observed that for a sample of economy companies, which capture the economy companies in which the 1 per cent, 5 per cent and 10 per cent dosages were constituted, respectively.

The coefficient of the institutional distance variable was not significant to none of the density analysis to the analysis, but one of the fronts of this research is not sustained. The probabilities of obtaining the largest or the largest variable value of participation rate, higher or lower than the higher and lower level of risk. Also, the number of specimens increased to 529, and the coefficient of explanation of the model tripled from 4 per cent to 12 per cent.

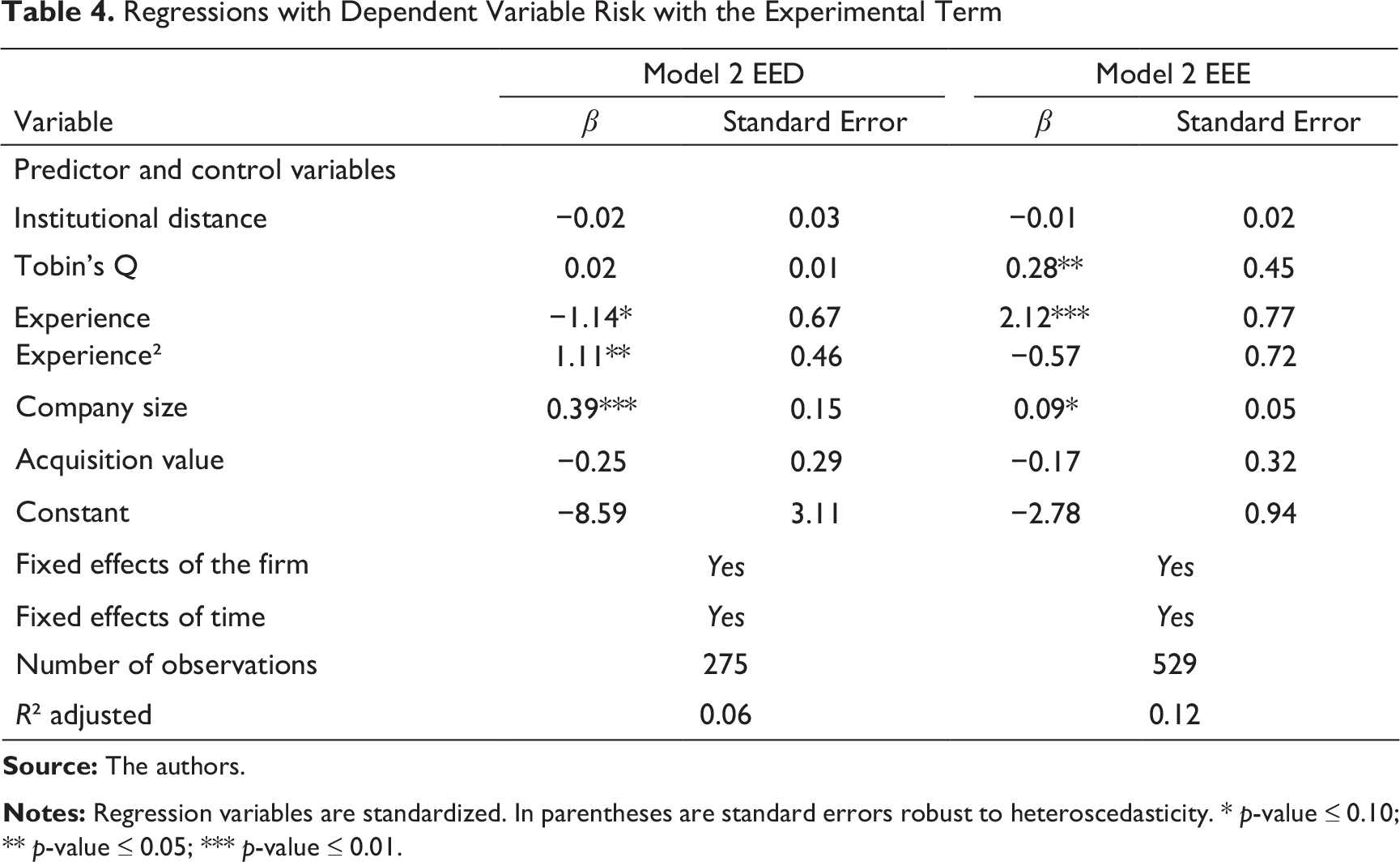

Regressions with Dependent Variable Risk with the Experimental Term

The number of observations remained constant, but the R² value increased from 4 per cent to 6 per cent. In this way, we can affirm that the experiment variable 2, besides improving the explanation power of the model, seems to be more adequate for the sample of developed economies than the experience variable, since it allows the statistical validation of H3. Figure 1 shows on the left side the relationship between M&A experience and risk when companies located in developed countries acquire a company also located in a developed country. Already on the right side shows the graph illustrating the relationship between risk and experience variables when companies located in developed countries acquire a company located in an emerging country.

Figure 1 graphically shows that the relationship between risk and the number of acquisitions (experience) is positive. In other words, the higher the number of acquisitions, the greater the risk of the acquiring company. However, although it is true, the relationship is not perennial, since once the acquirer has already made a certain number of acquisitions, it is perceived that the risk presents a stagnation and then a long fall.

It is observed that the curve differs drastically from that related to companies from developed economies. The difference is due to the fact that in the first moment it is verified that the realized acquisitions seem to reduce the risk of the acquirers, but after a certain number of acquisitions the risk increases without showing any sign of stabilization or fall.

Discussion of Results

As shown by Yang (2015), the institutional distance was related to the level of participation acquired during M&A. However, after performing the tests, the variable did not present a statistically significant relationship with the risk of the acquiring company. It is believed that the reason for this is the methodology used to measure such variables.

Tobin’s Q as a proxy for operational performance shows the positive effect of the increase in the Tobin Q of the companies that acquire emerging economy targets is offset by the increase in the company’s risk, whereas, when the target is economically developed, as well as the acquirer, the effect does not appear to exist.

As far as the experience is concerned, in both samples of acquired companies, this variable had a significant coefficient, thus supporting H3. However, from a graphical analysis of the relationship between risk and M&A experience, it was found that there are distinctions in the relationship type when changing the samples.

For the sample of companies from developed economies, it is verified that the relationship between the variables is positive at the beginning, but from a given number of acquisitions, it becomes negative. It is believed that the reasons for this can be found in the organizational learning memory literature in which authors present results that corroborate this (Haleblian et al., 2006; Levitt & March, 1988; Peng & Fang, 2010).

According to Levit and March (1988) results, companies can learn from their experiences, feeling increasingly apt to engage in new events like those earlier. Therefore, it seems plausible to argue that when companies make acquisitions frequently, the volatility in their performance becomes smaller and smaller, this is because with each new acquisition these companies also acquire experience, and the uncertainties of the activity become smaller and smaller.

The same analogy cannot be extended to the sample of companies from emerging economies, and the reason for this lies in the curve presented in Figure 1. Initially, the realization of an acquisition implies a reduction of risk, but then a sharp inversion of the relationship between the variables, and there is no evidence that the experience of these companies can reduce the volatility in their performance, that is, the risk.

Conclusion

The present study examined how the intrinsic factors of cross-border M&A affect the post-acquisition risk of developed economies engaged in acquisitions with target companies from emerging and developed economies. It is believed that this work was a pioneer in many aspects of its construction, since it is mainly focussed on the dynamics of emerging markets and their interactions with developed markets, besides seeking to analyse variables that are not very well covered in M&A literature, such as the case of operational risk, of the differences between the cultures of the countries and their formal institutions, which can generate a new approach within the M&A literature.

Since organizational learning theory does not seem to be able to be applied to acquisitions of companies from emerging economies as the acquisitions of companies from developed economies are applied, we have a new horizon for new research, especially within the behavioural approach of companies involved in M&A. New metrics for the calculations of cultural and institutional distances can still be tried in future works since the methodologies used here did not result in significant coefficients.

It is hoped that new methodologies can be developed to allow unrealized results to be found in future work, such as the relationship between experience and risk of acquiring firms in emerging economies. Finally, it is hoped that the results obtained will contribute to the development of cross-border M&A studies, fostering discussion and analysis of the issue in emerging countries, thus making possible a better understanding of these markets.

Managerial Implications

A M&A in corporate environment have an effect in companies with long term perspectives. Specially, when these events are cross-border M&A increase concerns in companies that make this kind of investment because the significant risk involved. In this sense, our results show empirically that when USA and Canadian companies buy other companies from countries with similar economies, post-event operational risk is significantly reduced.

Footnotes

Acknowledgements

This article was a collaborative effort of all the authors. The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions that have greatly improved the quality of this article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.