Abstract

While cross-border acquisitions by emerging economies are increasing over time, a significant percentage of deals are withdrawn before completion. By integrating the ‘organizational learning lens perspective’ with the ‘signalling lens perspective’, this study aims to investigate deal-specific, firm-specific and country-specific factors that can increase the likelihood of deal completion. The analysis is based on 16 years of data from a prominent emerging economy: India, from 2005 to 2021. A binary logistic regression model is used to understand the determinants of deal completion. Additionally, standard event study methodology is deployed for a particular firm-specific determinant (market reaction to deal announcement) to develop a proxy for the variable. Our findings indicate that factors which enhance learning during the acquisition process and communicate strong and positive signals to build trust between the acquirer and target positively impact the completion of announced acquisitions. Specifically, we report that acquisitions using cash as the payment method and those that receive positive market reactions at the time of acquisition announcement exhibit a higher likelihood of completion. In contrast, the prior failure experience of the acquirer has a detrimental impact on the likelihood of deal completion. The empirical results have important implications for improving the success of cross-border deals from emerging nations.

Introduction

Globalization has seen a notable transition over the past few years, with several firms from emerging economies expanding overseas. The countries once known as foreign direct investment destinations are now expanding aggressively in the global marketplace as hosts of foreign investments (Zhou et al., 2016). Even in the Indian context, companies have responded to the global competitive pressures by repositioning themselves through extensive corporate restructuring activities (Kar & Kar, 2021). The increase in corporate restructuring activities in particular has been in the form of Cross-Border Acquisitions (CBAs) and has contributed a significant share to the global economic growth (Bhagat et al., 2011; Deng & Yang, 2015; Rani et al., 2015).

The acquisition of Jaguar and Land Rover by Tata Group (India) in 2008, Lenovo’s takeover of IBM’s computer business in 2005 and Vale’s acquisition of Canadian mining company Inco in 2006 are just a few examples of notable landmark deals completed by companies from emerging countries. There are many reasons why emerging market multinational enterprises (EMMEs) prefer to enter foreign markets via CBAs; for example, to have speedier access to critical resources like brands and technology, to escape institutional and market flaws in domestic markets and to avoid the latecomer disadvantage in the international arena (Lebedev et al., 2015; Luo & Tung, 2007). The expansion of assets and research and development capabilities through the acquisition of foreign enterprises (Hege et al., 2014) or the utilization of the complementarity of the two businesses (Gubbi et al., 2010) are other reasons why EMMEs pursue these transactions.

Despite the growing popularity of CBAs as a mode of internationalization, the ultimate success, survival, performance and long-term implications of deals from emerging economies still need to be determined. Every announced merger and acquisition (M&A) deal is subjected to completion risk as there is some probability of deal abandonment associated with the deal. The closing risk is particularly vital in emerging market contexts as a significant percentage of M&A deals announced by acquirers from these economies fail to complete (Hawn, 2021; Zhou et al., 2016). Popli and Kumar (2016) checked cross-border deal cancellations by acquirers from eight emerging economies between 1992 and 2012 to support this argument. They concluded that, on average, 25% of disclosed M&A transactions fail to complete after the public announcement. The rate of deal abandonment in emerging economies is high compared to developed countries like the United Kingdom and the United States (Kim & Song, 2017). Withdrawing an announced deal is costly as it not only attracts penalties but can also cause proprietary damage to the acquiring firm. For instance, a company’s strategic moves might be disclosed to competitors at the time the agreement is announced. Furthermore, abandoning a deal before completion has a detrimental impact on the acquiring firm’s reputation and credibility as well (Luo, 2005).

Despite the higher abandonment rates in emerging economies, factors impacting deal completion have received limited academic attention and largely remain unexplored (Kumar & Sengupta, 2021; Sun et al., 2012). Additionally, studies in the existing literature suggest that there is a pertinent need for policymakers to establish transparent merger completion processes because the regulatory environments of the acquirer and target nations are fundamentally different. This is necessary for prevention of unnecessary delays in negotiations and deal abandonments (Liang et al., 2017). The current study attempts to fill this gap by exploring the determinants of acquisition completion in a prominent emerging economy: India.

In this study, we blend the ‘organisational learning lens perspective’ with the ‘signalling lens perspective’ to examine the effects of three kinds of factors (deal-specific, firm-specific and country-specific factors) on the likelihood of deal completion. The empirical analysis is carried out on 228 CBAs by Indian acquirers between 2005 and 2021. The study’s conclusions offer recommendations for the stakeholders of acquiring and target company. Based on the findings of the study, the stakeholders can formulate strategies to lower the likelihood of abandonment, establish transparent processes for merger completion and save valuable resources and time. This study thus contributes to resolving a real-world business problem related to the collapse of announced CBA deals before completion.

The rest of the article is organized into the following sections: Theoretical lens, Literature Review and Hypotheses Development highlights the theoretical foundations of the study, Data & Methodology describes the empirical approach, Results tabulates the findings, Robustness Tests validates the findings, and Discussion and conclusion section concludes.

Theoretical Lens, Literature Review and Hypotheses Development

Theoretical Lens

Initially focused on the completion rate of domestic and cross-border M&As out of developed economies, the investigation into deal completion has more recently expanded to include outbound cross-border M&As of the emerging nations (Kumar & Sengupta, 2021). Distinct from outbound M&As from developed markets, the market for corporate control poses additional challenges for EMMEs, which places them at a competitive disadvantage in the global economy (Jain et al., 2018). As evidenced by the synthesis of influential publications in the cross-border M&A literature, Li et al. (2021) posit that complex ownership and board structure of the firms, limited presence in the international arena and the lack of prior international deal exposure contribute to the disadvantage faced by firms from the emerging economies. These challenges subsequently exacerbate the information asymmetry problems between the acquirer and target and have a detrimental impact on the negotiation and completion process.

In view of these issues, researchers have attempted several models and constructs to theorize the completion of outbound M&As initiated by EMMEs. Despite these attempts, there remains a need to conduct more studies using rigorous theories and methodologies in the emerging market setting to understand the factors impacting merger failure (Reddy et al., 2015). Drawing upon the ‘organizational learning lens perspective’ and the ‘signalling lens perspective’, this study thus attempts to plug this gap by examining the influence of three categories of factors (deal-specific, firm-specific and country-specific) on the likelihood of completion for deals announced by acquirers from India—a prominent emerging economy.

Organizational Learning Lens and Acquisition Completion

To cope with the challenges of the CBA process, effective organizational learning is necessary for the acquisitions to be completed successfully. As acquirers face more uncertainty and unfamiliarity in the host nation, they will rely on learning as a resource to help them navigate these difficulties. However, organizational learning is not a standalone resource; it depends on the acquirer’s internal capabilities and competencies as well as the external circumstances (Zhou et al., 2016). The learning process therefore may get enhanced or hindered by the interaction of internal and external influences.

Greater institutional, political, economic, legal and cultural differences between the acquirer and the target, for example, might function as an external barrier and impede cross-border learning, which can have a detrimental effect on the likelihood of deal completion. In contrast, acquirers who have conducted successful acquisitions in the past might internalize these lessons and apply them to subsequent acquisitions for increased synergistic gains (Jain et al., 2018). In a similar vein, this study investigates the influence of several factors combined under three categories (deal-specific, firm-specific and country-specific) that can enhance or hinder the process of learning and, as a result, differently affect the outcome of deal completion.

Signalling Lens and Acquisition Completion

EMMEs, who are still relatively new to the global markets, attempt to overcome their latecomer disadvantage in technological and managerial capabilities by growing inorganically through acquisitions (Lebedev et al., 2015). Considering this background, to establish legitimacy, EMMEs would want to convey signals (information) to firms in target nations that their internationalization endeavours can be trusted.

Drawing from the seminal work of Michael Spence, weak indicators can alter the signalling firm’s credibility and serve as action cues for the market players (Spence, 1973). Consistent with this school of thought, we contend that certain factors can serve as positive signals of the acquiring firm’s commitment to cooperate and successfully secure the deal. For example, using cash to settle the deal represents the acquiring firm’s belief in the valuation of the target company (Huang et al., 2016). It, therefore, sends a strong signal indicating the acquirer’s commitment to successfully complete the deal with the target firm. However, there may also be the factors that can send negative signals to the target firm’s shareholders and shake their confidence in the deal’s potential. As in the case of stock market reaction to deal announcement, if the market reaction to the deal at the time of the announcement is unfavourable, it indicates the lack of investor confidence in the prospects of the deal (Jain et al., 2021). This can send a negative signal to the target firm and can thus deter the likelihood of deal completion.

As theoretical constructs, ‘organizational learning lens’ and ‘signalling lens’ work in tandem with each other and are not independent concepts. Effective organizational learning by the acquirer during the acquisition process not only contributes to building competitive advantage but also signals enhanced commitment and effort on the acquirer’s part to build trust with the target firm. In contrast, an obstruction to learning, regardless of internal or external factors will communicate negative signals to the target firm and may have heterogeneous impact on the outcome of deal conclusion. Grounding our arguments in these integrated theoretical constructs, we therefore develop the hypotheses to be tested for the empirical analysis in the following sections.

Deal-specific Determinants of Acquisition Completion

Zhou et al. (2016) report that the percentage of ownership acquired in the target company can influence the cooperation and understanding between the parties to the M&A transaction. For agreements with greater percentages of stake sought, target companies may be more ready to provide comprehensive corporate information during the private-takeover stage.

1

Considering the ‘organizational learning lens perspective’, this is a positive indicator as the supply of increased information will enhance the acquirer’s ability in making well-informed decisions. The increased learning will also reduce the information asymmetry between the acquirer and target, which is thought to be a primary cause of deal abandonment (Kim & Song, 2017). Additionally, a sizable ownership share also signals to the target business about the acquirer’s commitment and interest in securing the deal and contributing to the growth of the firm’s shareholders and the host economy. In lieu of the positive signals, the target business may get motivated to make more concessions to close the deal even if there are negative changes in the external environment during the public-takeover phase

2

because of disturbances in the host nation. We hypothesize that, considering the preceding arguments:

H1: Greater percentage sought by the acquirer increases the likelihood of deal completion.

In addition to ownership acquired, another deal-level factor that can impact the likelihood of deal completion is the payment method utilized to finance the transaction. Muehlfeld et al. (2007) report that M&A transactions can be completed using cash, company stock or a combination of both. The use of cash as a method of payment has several advantages. For instance, Fishman (1989) suggests that acquirers using cash signal have greater confidence in the valuation of the target company and indicate that the acquirer is adequately prepared to absorb any risk arising from overpayment. The use of cash will also enable the acquirer to ward off competing bids, as the competing bidders would need to incur higher charges to match or exceed the bid.

Furthermore, Shimizu et al. (2004) report that compared to stock payment, cash payment has the advantage of quick settlement and thorough ownership transferal. In contrast, a stock offer negotiated during the private-takeover period considering the market value of the acquiring and target companies can lead to contention. Any market fluctuation following the deal announcement can impact the perspective of both parties, making it difficult to arrive at a common agreement. Owing to the increased negotiations following the market fluctuations in the valuation of the stocks, there can arise a situation that the target business finds it difficult to cooperate with the acquiring firm. This lack of cooperation can impede the process of learning as it may be challenging for the acquiring firm to obtain additional information from the target and engage in further negotiations for deal conclusion.

Furthermore, target shareholders are likely to prefer cash vis-à-vis stock as payment method in CBAs as stock offered by acquiring firm is listed on a foreign exchange, thereby exposing the target shareholders to additional risk (Huang et al., 2016). Based on the above discussion, we hypothesize that:

H2: Use of cash as a payment method increases the likelihood of deal completion.

Firm-specific Determinants of Acquisition Completion

The firm’s prior experience can help in the completion of M&As by helping to manage the challenges that arise during the public-takeover phase. The learning-curve effect due to experiential learning has been established in the literature to positively affect firm’s performance (Levitt & March, 1988; Yelle, 1979). Previous experience with M&A can be categorized as success or failure. Successful experiences can add to the repository of information available to a company and make it better prepared in terms of negotiations and strategy preparation (Zhou et al., 2016). Owing to the advanced knowledge base and enhanced learning, firms with successful experiences are more likely to navigate the crucial and interdependent tasks in the M&A process with greater ease (Zhou et al., 2023). Furthermore, prior experience not only facilitates the development of organizational routines but also signals the acquirer’s ability to encounter obstacles with persistent efforts through deploying the advanced knowledge base, thereby reinforcing the likelihood of successful deal completion.

In contrast to successful experiences, failure to complete M&A deals indicates gaps in the acquirer’s existing knowledge and skill set and the need for the acquirer to re-evaluate its strategic intentions. Moreover, learning from failures is relatively difficult, and the returns are quite uncertain (March, 1991). Learning from previous failure experiences is further complicated by the contextual complexities of the M&A transactions. In a recent study examining the impact prior failure has on the likelihood of deal completion, Zhou et al. (2023) notes that a sufficiently large number of failures are needed (more than 6) to draw significant learnings from these experiences. However, as EMMEs are relatively new in their internationalization endeavours with most firms having two decades or lesser experience (Hawn 2021; Zhou et al., 2023), these firms may not undergo such large number of failures to produce a positive learning effect. Furthermore, it can be argued that even if EMMEs are inclined to apply the learnings from prior failure experiences, they may not possess the requisite international knowledge needed to learn from failures in the cross-border context (Hastings & Hastings, 2014). Past failures may also serve as negative signals impacting the credibility of the acquiring firm’s intentions. Based on the above arguments, we, therefore, propose that:

H3a: Prior successful M&A experience increases the likelihood of deal completion. H3b: Prior failure M&A experience decreases the likelihood of deal completion.

Another important firm-level determinant that can impact the outcome of deal-completion is the stock market reaction received by the acquiring company at the time of the deal announcement. EMMEs engage in CBAs to gain future synergistic benefits from the deal. The share price of the acquiring firm responds at the time of the deal announcement, expressing the market’s perspective of the deal. Many studies on CBAs consider acquirer returns as an important signal to assess the value-creation potential of the deal. However, there is a dearth of conclusive evidence in the literature that acquirers from emerging economies extract information from acquisition announcement returns when making deal-closing decisions.

According to the managerial learning hypothesis, stock prices are an important information source for operational decisions (Pereira da Silva, 2021; Xie et al., 2022), as the aggregated information provided in stock prices gives stakeholders access to knowledge that they are oblivious to or ignore. If the market judges the acquisition favourably, it will provide stakeholders confidence and ease their worries about the EMMEs expansionary efforts.

Current studies in this field, such as those by Tanna et al. (2021) and Luo (2005), provide inconsistent outcomes, and the results of their investigation are not based on acquisitions from emerging economies. The findings of Tanna et al. (2021) do not support Luo’s (2005) conclusion that market reaction predicts whether the acquiring company would complete the transaction. Their conclusions suggest that deal completion decisions are unaffected by the deal announcement returns. Given the contradictory outcomes in the available literature, we investigate the association between announcement returns and deal completion. Thus, we hypothesize:

H4: Positive announcement return to the acquisition announcement increases the likelihood of deal completion.

Country-specific Determinants of Deal Completion

Along with deal-specific and firm-specific variables, country-level factors are likely to increase the closing risk associated with M&A deals. Doidge et al. (2007) have even suggested that differences across countries are more relevant than inter-company differences within a country. From the perspective of ‘organizational learning’, the work of Jain et al. (2021) suggests that greater cultural disparity between the acquirer and target nation hinders effective learning and causes difficulty in knowledge transfer, thereby creating more hurdles for the acquirers to consummate the deal. As distance is an external influence impacting cross-border learning, greater variation can make the acquirer misunderstand or overlook crucial information and make it challenging to process unexpected changes during the acquisition process.

The findings of Dikova et al. (2010) indicate that the likelihood of deal completion is adversely influenced by the country distance between acquiring and target nation. Similarly, Zhou et al. (2016) reveal that larger legal and regulatory distance between the acquirer and target country increases unfamiliarity and hinders learning, contributing to increased completion risk. Another dimension of country distance captured by Zhang et al. (2017) relates to the economic freedom distance between acquiring and the target nation. The study’s findings indicate that the economic freedom of the acquirer’s parent country plays a significant role in deal completion. It even offsets the detrimental effect of institutional quality in the acquirer’s home country. Another strand of literature suggests that cultural and institutional variables may not have an impact on the completion rate of announced deals as these variables would have been factored in at the time of target selection and deal initiation (Alexandridis et al., 2021; Fong et al., 2019; Lawrence et al., 2021). However, it is possible that managers negotiate and conduct transactional due diligence even after deal announcement whereby greater differences in the institutional and cultural environment can obstruct the successful completion. Based on the foregoing discussion, the impact of cultural and institutional differences on deal completion is not straight-forward. Therefore, the current study examines the effects of institutional and cultural distance between the acquiring and target nations on deal completion and hypothesize that:

H5: Greater institutional distance between acquiring and target country decreases the likelihood of deal completion. H6: Greater cultural distance between acquiring and target country decreases the likelihood of deal completion.

Data and Methodology

Sample Selection Criterion

For our analysis, we extracted the list of cross-border transactions (1519) announced by Indian firms from April 2005 to March 2021. The deal details were obtained from the Bloomberg® terminal. We started the sample in 2005 since the outbound Indian M&As exhibited an upwards trend during this period (Col & Sen, 2019).

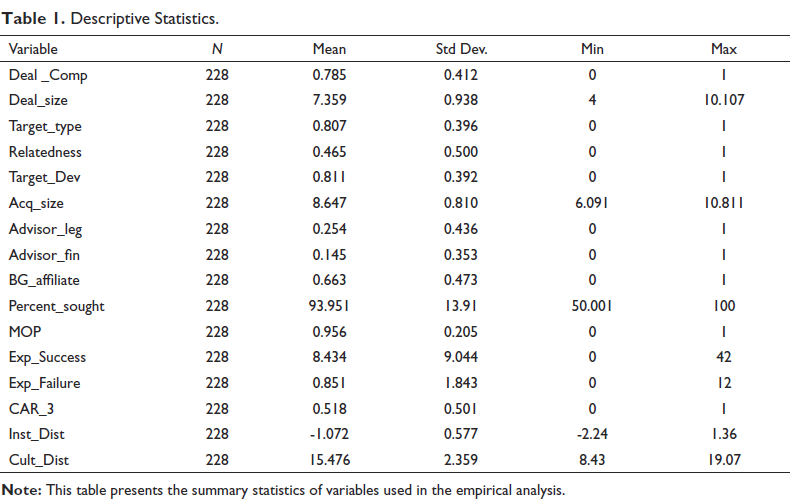

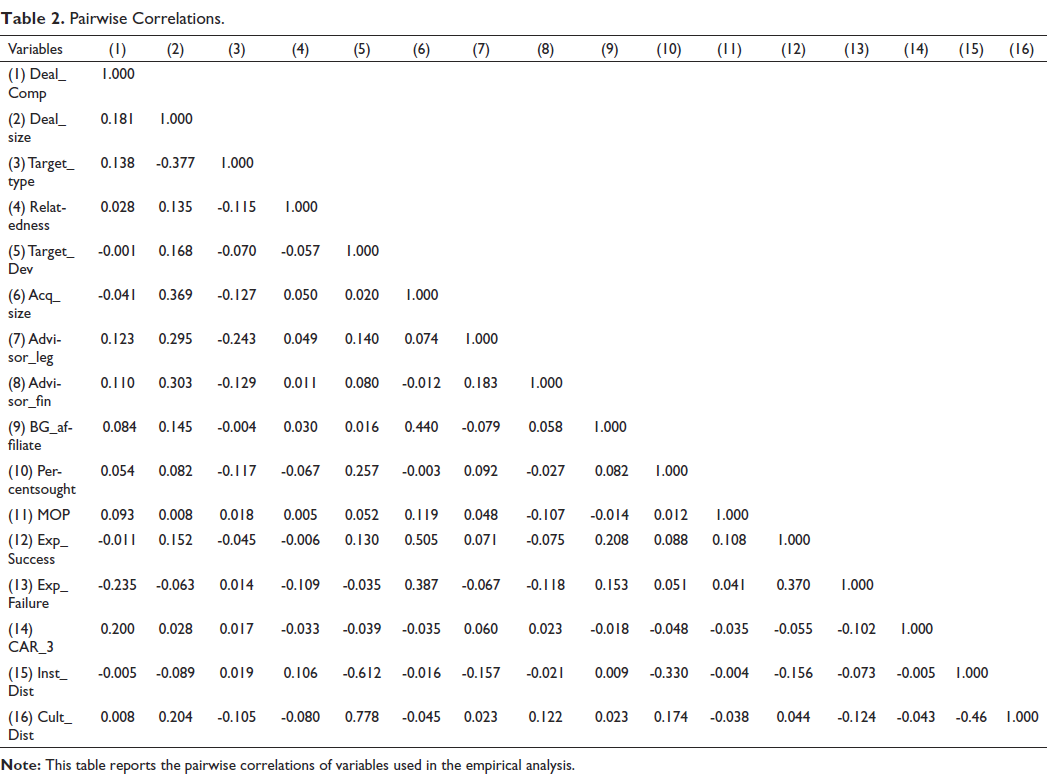

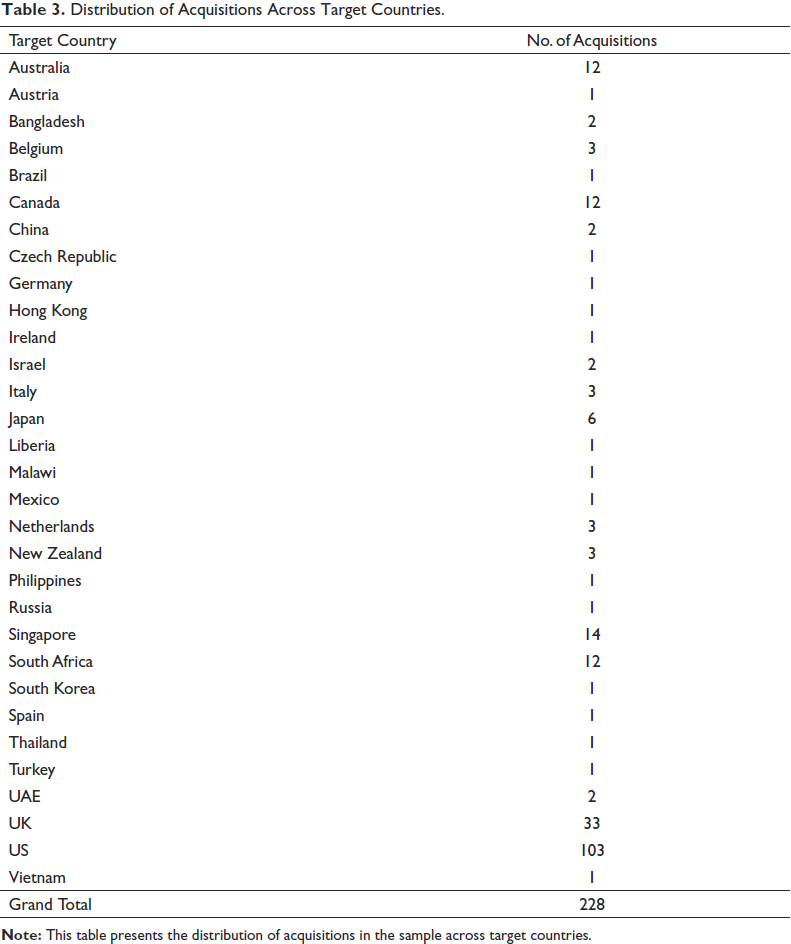

The dataset was filtered to include only those deals announced by a single acquirer where the deal value was available, the consideration/payment was made in cash or stock and where the acquirer took a majority stake in the acquisition. This reduced our sample to 504 deals. The deals were then cleaned to remove any event with missing information that could not be obtained from other sources/hand collected. The final dataset consists of 228 deals with a complete set of controls and explanatory variables. The summary statistics and pairwise correlation matrix for all variables used in the empirical analysis are presented in Tables 1 and 2, respectively. Further, the distribution of acquisitions across target countries is reported in Table 3.

Descriptive Statistics.

Pairwise Correlations.

Distribution of Acquisitions Across Target Countries.

Variables

Dependent Variable

The current study’s dependent variable is the deal completion status which is coded as 1 for completed deals and zero otherwise. All deals which had the status of intended, intent withdrawn and pending were assigned as not completed. The dependent variable is consistent with earlier studies examining the factors that influence deal completion (Fuad & Gaur, 2019; Hawn, 2021; Lim & Lee, 2016).

Explanatory Variables

Percent sought is the ownership stake sought by the acquiring company at the time of the deal announcement. We proxy method of payment as a dummy variable with a value of 1 if the deal is financed in cash and zero otherwise. The number of completed transactions by the acquirer prior to the announcement of the focal deal is a measure of the acquirer’s prior M&A success. The acquirer’s overall number of failed transactions prior to the focal deal is used to calculate the acquirer’s prior M&A failure history. For ascertaining the market reaction to deal announcements, we calculate cumulative abnormal returns (CAR) to shareholders using the standard event study methodology deployed extensively in finance and strategy literature (Brown & Warner, 1980, 1985; Kothari & Warner, 1997). We follow studies in existing literature (Bhagat et al., 2011; Ranju & Mallikarjunappa, 2019) that use the market model to calculate abnormal returns as follows:

where Rit is the expected return to firm i and Rmt is the return of the reference market index on which the firm is listed (BSE Sensex) on day t. The security-specific parameters, that is, αi and βi, are obtained using ordinary least squares regression (OLS) of Rit on Rmt over the 90-day estimation period (120 days to 30 days before the merger announcement). We then aggregate the announcement returns over the event window (+1, –1) to arrive at the CAR. Based on this calculation, we develop a dummy variable taking the value of 1 if the CAR to the acquirer is positive and zero otherwise.

The country-specific variables capturing institutional and cultural distance have been computed using the International Country Risk Guide published by the PRS Group and Hofstede’s dataset, respectively. Following the work of Lawrence et al. (2021), the institutional distance between the acquirer and target country is captured as the average of differences between government stability, investor profile, internal conflict, external conflict, military in politics, democratic accountability, corruption, law and order and bureaucracy index. Cultural distance on the other hand is measured as

Control Variables

In accordance with prior research in the domain of CBAs by EMMEs (Fuad et al., 2021; Jain et al., 2018, 2021), we control for the impact of the following variables:

Deal size, which is proxied as the log of deal value. Target type, indicating the listing status of the target company as private or public (1,0). Industry relatedness, indicating whether or not the target and acquirer are part of the same industry group (1,0). Target development status, indicating whether or not the target is based in a developed country (1,0). Acquirer size, which we proxy as the log of sales made by the acquirer in the financial year preceding the acquisition announcement. Legal advisor, indicating if the acquirer has hired legal counsel for the underlying transaction (1,0). Financial advisor, indicating if the acquirer has hired investment bankers for the underlying transaction (1,0). Business group affiliation, indicating if the acquirer is affiliated with a business group or is a standalone firm (1,0).

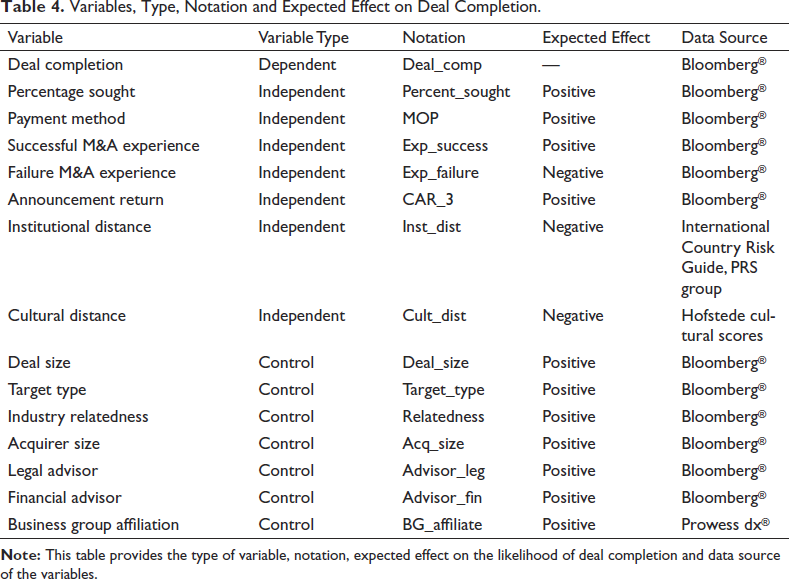

Table 4 summarizes the variables along with the expected effect on the likelihood of deal completion.

Variables, Type, Notation and Expected Effect on Deal Completion.

Methodology

To estimate the completion likelihood of M&A deals, we run the following binary logistic regression model:

Where Pi is the probability that transaction i will be completed, αi is the constant term, β1-7 are the coefficients of interest and β8-15 represent the vector of coefficients of control variables. The analysis of the above regression model is done at the deal level.

Results

The outcomes of logistic regression are reported in Table 5.

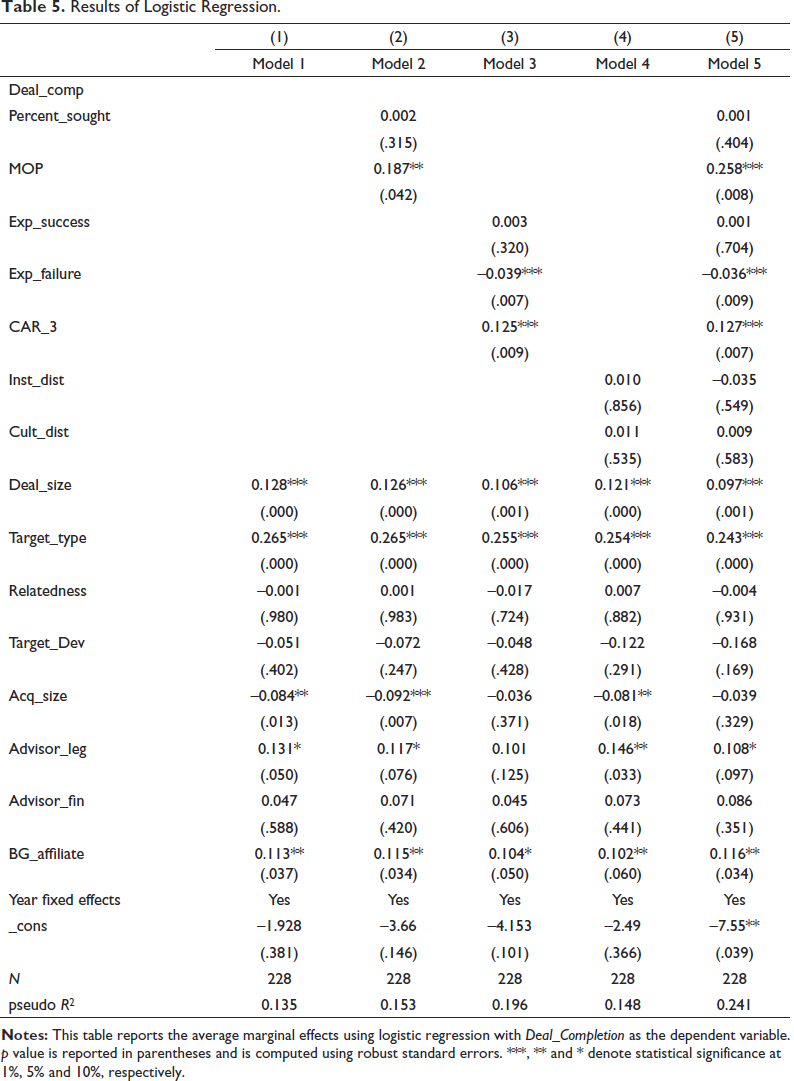

Results of Logistic Regression.

Model 1 includes all control variables. Model 1 indicates that deals with greater value have a higher likelihood of deal completion (β = 0.128, p < .01), signifying that in deals with bigger size the acquiring and target company cooperate with better understanding to successfully secure the deal. Further, acquiring private target companies increases the likelihood of completion (β = 0.265, p < .01). The results suggest that compared to private firms, the diverse nature of public ownership requires increased diligence and coordination and therefore impacts the completion likelihood negatively. The empirical analysis also reveals that hiring legal counsel positively influences the likelihood of deal completion (β = 0.131, p < .10), suggesting that acquirers benefit from the legal advisors’ skill, expertise and experience. Additionally, the results attest to the importance of being affiliated with business groups. Although there is an ongoing debate in the extant literature about business groups being ‘heroes’ or ‘villains’ owing to conflicting results regarding the benefits and costs of group affiliation (Aggarwal et al., 2019; Claessens et al., 2000; Khanna & Yafeh, 2007; Popli et al., 2017), our study attests the positive benefits derived from group affiliation. Affiliated firms have advantages over standalone firms in sourcing critical resources, such as information and capital, which are needed for the successful execution of the deals. Consistent with the benefits of affiliation, our results indicate that acquirers associated with business groups exhibit a higher likelihood of deal completion than standalone acquirers (β = 0.113, p < .05). Overall, the findings of Model 1 are in consonance with the results reported by Kim and Song (2017), Fuad and Gaur (2019) and Lawrence et al. (2021).

In Model 2, we include deal-specific variables. Even though the coefficient of ownership stake sought is in the expected direction, the results are not statistically significant. We, therefore, do not find support for Hypothesis 1. However, our findings echo the importance of using cash to finance the deals as discussed in the existing literature. Deals financed with cash exhibit a higher likelihood of completion (β = 0.187, p < .05). Cash payments are not only simple but also offer the advantage of high-speed settlement and complete transferral of ownership. They signal acquirer’s confidence in the deal’s value-creation potential. The findings align with the predictions of Hypothesis 2.

Model 3 investigates the impact of firm-specific variables. Our results support Hypothesis 3b as firms with higher failure experience demonstrate a lower likelihood of acquisition completion (β = –0.039, p < .01). The findings are consistent with the work of Zhou et al. (2016) and Zhou et al. (2023), indicating that prior failure experience has an adverse impact on the likelihood of subsequent completion as there are gaps in the existing knowledge base of the acquirers that need to be plugged to ensure success. However, we do not find support for Hypothesis 3a. Further, we report that deals with positive announcement returns exhibit a higher likelihood of completion (β = 0.125, p < .01). Hence, Hypothesis 4 is supported. The results align with the managerial learning hypothesis suggesting if the market’s assessment of the deal is positive, it provides confidence to the stakeholders regarding the deal’s value-creation potential and thus increases the likelihood of completion.

Model 4 tests the effect of country-specific determinants. We do not find support for Hypotheses 5 and 6. The results are concurrent with the findings of Lawrence et al. (2021), suggesting that country-specific determinants are more important at the time of target selection and deal initiation and not during the public-takeover phase involving deal completion. Model 5 is a complete model including all variables. The results of Model 5 are in line with the reported findings.

Robustness Tests

As is evident from Table 3, our sample is dominated by acquisition of targets from the United States (45%). To ensure that our results hold across all markets and are not specific to acquisitions from one target nation, we repeat our analyses after excluding 103 transactions conducted in the United States. The results on the alternative sample are reported in Table 6. Even though the size and significance of the effects vary slightly, the findings related to our variables of interest largely continue to hold. Model 10 which reports all variables continues to support the predictions of Hypotheses 2, 3b and 4. The results indicate that any specific subsample of deals does not influence the findings of this study.

Robustness Results (Without US Deals).

Discussion and Conclusion

Theoretical Implications

Our study contributes to the body of knowledge on the factors impacting acquisition completion in the context of CBAs announced by EMMEs. We extend the ‘organizational learning lens perspective’ in the context of acquisitions by showing that factors that enhance learning during the acquisition process positively influence the likelihood of deal completion.

Amongst the deal-specific factors, we report that deals settled using cash report a higher completion rate. Cash as a payment method indicates the acquirer’s confidence in the deal’s potential. Given the acquirer’s confidence, the target is willing to share additional information with the acquiring firm, contributing to increased learning and robust negotiations, thereby positively impacting deal completion. Further, firm-specific factors also reinforce the ‘organizational learning lens perspective’. Our results indicate that past failure experience is detrimental to the success of acquisition completion. Given the significant uncertainty, unfamiliarity and complexity involved in the CBAs, the results underscore how challenging it is for acquirers to learn from past failed experiences. The results also suggest that acquirers with past failures must enhance internal skills and learning competencies to compensate for their past errors. Next, we report that a positive reaction to the acquisition announcement is associated with increased completion probability. The results again align with the ‘learning lens’ perspective as the aggregated information provided in stock prices (market’s reaction) gives stakeholders of both the acquiring and target firm access to knowledge from the perspective of stock market investors that they are oblivious to or ignore.

Furthermore, our results viewed through the ‘signalling lens perspective’ suggest that acquirers from emerging nations should communicate strong and positive signals to build trust with businesses from target nations. The empirical analysis attests that signals indicating the acquirer’s commitment to the acquisition process positively impact the completion of announced acquisitions. Using cash to settle the deal signals the confidence of the acquirer in the valuation of the target company and hence increases the likelihood of deal completion. Similarly, positive market reaction following the acquisition announcement assures the stakeholders about the deal’s potential and is thus associated with increased completion likelihood. In contrast, past failures serve as negative signals indicating the gaps in the acquiring company’s existing knowledge base, negatively impacting deal completion.

Limitations and Suggestions for Future Research

Although our study advances knowledge on the factors that influence deal completion, it is not free from limitations. First, the study is focused on acquisitions from only India. Future studies can also consider other emerging economies to broaden the analysis. Second, even though the association between the market reaction and deal completion is positive, the relationship may be contingent on other factors such as the legal and regulatory distance and corporate governance indicators (country-level as well as firm-level). It would be interesting to analyse if the relationship between market reaction and deal completion gets modified after accounting for these factors. Third, future studies can proxy the country-specific determinants using other measurements available on the World Bank databases. Finally, following the study of Singla (2019), future studies can also segregate the industry effects from country effects and examine if the determinants of completion hold across multiple industries.

Conclusion

Despite the vast amount of money and resources spent on CBAs, there remains ambiguity regarding the success of these deals (Renneboog & Vansteenkiste, 2019). Acquisitions announced by emerging market acquirers lack legitimacy in foreign markets and face more challenges compared to their developed market counterparts (Bartlett & Ghoshal, 2000; Hawn, 2021; Hymer, 1976; Zaheer, 1995). Stakeholders assume certain disadvantages with the expansionary activities of emerging economy firms because of the uncertainty associated with the political, cultural and economic background of these countries.

Considering this background, the present study, by examining deal-specific, firm-specific and country-specific determinants on CBAs by Indian acquirers, makes several contributions to the existing literature. First, the findings of the study will help the stakeholders in emerging markets manage the abandonment risk more effectively. As evidenced by our findings, acquirers in emerging economies should focus on factors that increase learning during the acquisition process and consequently signal positive cues to the target nations. Specifically, using cash as payment method to settle the deals and incorporating the market’s assessment of the deal potential, positively impact the likelihood of completion. Further, acquirers with prior failure experience should be cautious with their expansionary activities and are advised to plug gaps in their existing knowledge and skill sets. Acquirers with previous failure experience are suggested to mitigate the effect of information asymmetry and address the legitimacy concerns of the target companies more effectively.

Further, by investigating the impact of announcement returns on acquisition completion, this study adds to the growing literature demonstrating the relationship between financial markets and firm-decision making (Bond et al., 2012; Tanna et al., 2021; Xie et al., 2022). Our analysis indicates that compared to deals that received negative market reaction from the shareholders at the time of deal announcement, deals receiving favourable reaction exhibit a higher likelihood of deal completion. This indicates that the market’s assessment about the deal’s potential is crucial in alleviating concerns regarding the expansionary activities of EMMEs. A positive assessment from the market provides confidence to the stakeholders of both the acquiring and target firm and thus motivates them to conclude the deal successfully. Finally, the insights derived from our work can be extended to other methods of cross-border internationalization by emerging market firms. We hope that this work will stimulate more interest in investigating the performance of acquisitions by emerging market firms at different stages of the M&A process.

Footnotes

Acknowledgement

The authors are grateful to the journal’s anonymous referees for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.