Abstract

Corporate investment efficiency may be determined by changes in overinvestment and/or underinvestment. Prior studies showed that national culture dimensions affect firm investment efficiency. However, they failed to address whether overinvestment or underinvestment is the effective mechanism to transmit these effects. With a research data of 280,092 year-firms from 44 countries, we find that national culture affects corporate investment efficiency through underinvestment. Individualism and masculinity are positively related to investment efficiency while uncertainty avoidance and power distance are negatively related to investment efficiency.

Introduction

Modigliani and Miller (1958) posited that corporate investment is only driven by investment opportunities in a perfect business environment. However, the real world has many market frictions. Therefore, corporate investment tends to deviate from its optimal level (Chen et al., 2017). According to agency theory, managers tend to expropriate shareholders through investment decisions (Hope & Thomas, 2008; Jensen, 1986; Jensen & Meckling, 1976; Masulis et al., 2007). Their self-interest motive may reduce corporate investment efficiency (Chen et al., 2017; Jiang et al., 2011; Tran, 2019; Xie, 2015). In addition, managers’ self-interest motive is governed by shared values, belief systems, rules and patterns in their countries. As a result, many prior studies showed that national culture affected corporate investment and investment efficiency around the world (Choi, 2020; Kashefi-Pour et al., 2020; Li et al., 2021; Yan et al., 2021; Zhang et al., 2016). Nevertheless, these studies have not addressed whether national culture affects investment efficiency through overinvestment or underinvestment. Therefore, this article is conducted to fill this research gap.

Shapira (1995), Baird and Thomas (1985) and Bluhm and Krahnen (2014) found that managers’ investment decisions were based on their risk-taking behaviour. Moreover, Ashraf et al. (2016) and Mihet (2013) documented that national culture significantly determined corporate risk-taking. However, we argue that corporate managers’ over investment in unprofitable projects is less affected by their risk management policy, since this behaviour is conducted deliberately and intentionally. When managers are less willing to take risk under the impact of national culture, they tend to decrease their investment in profitable projects rather than unprofitable projects. Therefore, national culture influences corporate investment efficiency mainly through the channel of underinvestment.

In line with Fazzari et al. (1987), Baker et al. (2003), McLean et al. (2012) and Chen et al. (2017), we measure investment efficiency by the sensitivity of corporate investment to investment opportunities. National culture is proxied by four cultural dimensions (i.e. individualism, uncertainty avoidance, power distance and masculinity) from Hofstede et al. (2010). With a sample of 280,092 observations from 33,947 firms across 44 countries, we find that individualism and masculinity are positively related to investment efficiency. In addition, uncertainty avoidance and power distance negatively affect investment efficiency. Remarkably, the effects of these cultural dimensions are transmitted mainly through underinvestment.

This article contributes to the literature of national culture and corporate finance as follows. First, it provides empirical evidence for the effect of national culture on corporate investment efficiency. Kutan et al. (2020) showed that the relationship between national culture and investment efficiency was rather scarce. Second, it shows the effective channel through which national culture affects corporate investment efficiency. Zhang et al. (2016) found the effect of culture on investment efficiency, but they failed to show whether overinvestment or underinvestment was the effective transmission channel. The rest of this article includes four sections. The second section presents the extant literature and research hypotheses. The third section describes research models and research data. The fourth section reports regression results. The fifth section presents robustness checks. The sixth section provides main conclusions.

Literature Review

National Culture and Corporate Decisions

According to Williamson (2000), an analytical framework of institutional analysis consists of four interrelated levels. Level 1 is informal institutions (e.g., culture and religion) that are deemed as the most fundamental. Level 2 is formal institutions that are constrained by Level 1. Level 3 includes governance structures on contracts. Level 4 is decisions to allocate resources like firm investment decisions. As a factor in Level 1, culture indirectly affects corporate investment decisions through formal institutions in Level 2. Besides, it may have a direct impact on firm investment when formal institutions fail to control incomplete contracting problems (Shao et al., 2013).

Culture influences corporate decisions through investors’ views and managers’ views. First, corporate decisions are determined by investors’ views and preferences since firms cater to investors (Chen et al., 2015). According to Kumar et al. (2011), religion-induced gambling beliefs affect investors’ portfolio choices. Shu et al. (2012) showed that religious beliefs played an important role in risk-taking practices. Besides, Chui et al. (2010) found that differences in cultural values are associated with momentum profits. However, the manager mechanism tends to be more effective since firms’ financial decisions are mainly at managers’ discretion (Bae et al., 2012). Despite the globalization of business environment, national culture still influences corporate financial decisions directly through managers’ views and indirectly through firm- and country-specific features (Li et al., 2013).

Farooq et al. (2020) showed that national culture determined firms’ financial performance through their financial decisions across 13 Asian economies. Li et al. (2013) found that culture measures influenced corporate risk-taking via their impacts on manager’s decisions and nations’ formal institution in 35 countries. Mourouzidou-Damtsa et al. (2019) also found that national cultural values also influenced bank risk. Illiashenko and Laidroo (2020) documented that individualism negatively affected bank risk-taking across 56 countries. Shao et al. (2010) used Schwartz’s culture dimensions to investigate how culture values affected dividend policy in 21 countries from 1995 to 2007. Their findings showed that conservatism and mastery were positively and negatively associated with dividend payouts, respectively. Bae et al. (2012) found that Hofstede’s culture dimensions (i.e., individualism, long-term orientation and masculinity) had negative effects on corporate dividend decisions across 33 countries over the period 1993–2004. Aggarwal and Goodell (2014) showed that uncertainty avoidance and masculinity negatively affected firms’ access to finance. Moreover, Dority et al. (2019) documented a negative relationship between masculinity and private credit access in 70 countries over the period 2005–2014. Chen et al. (2015) argued that national culture influenced the precautionary motive of corporate cash holdings. With a sample of 27,801 firms from 41 countries over the period 1989–2009, they showed that individualism and uncertainty avoidance were negatively and positively related to cash levels. Besides, several previous studies also found significant impacts of national culture on firm leverage (Chui et al., 2002), corporate innovation and growth (Gorodnichenko & Roland, 2010), access to bank credit (Mishra & Tripathi, 2017), banks’ earnings management (Kanagaretnam et al., 2011) and bank’s dividend policy (Zheng & Ashraf, 2014). Recently, Yan et al. (2021) showed that Confucian culture increased corporate R&D expenditure.

National Culture and Investment Efficiency

Although many prior studies showed the effects of market frictions on corporate investment (Boubakri et al., 2013; Chen et al., 2006, 2011; Jiang et al., 2011), there have been relatively few studies investigating the relationship between national culture and investment decisions. In a pioneer study, Shao et al. (2013) analysed how individualistic culture affected corporate investment. They argued that individualism was dominant in most cultural paradigms and relevant to managers’ risk-taking behaviour. Managers in countries of high individualism were more willing to take risk; therefore, they preferred long- to short-term investment. With a sample of 146,275 firm-year observations during the period from 1997 to 2009 across 18 countries, Zhang et al. (2016) documented that individualism was positively related to corporate investment bias while uncertainty avoidance and masculinity were negatively associated with corporate investment bias. Moreover, Kashefi-Pour et al. (2020) examined how national culture affected the relationship between corporate investment and cash flow across 24 OECD countries from 1990 to 2017. They found that uncertainty avoidance, power distance and masculinity had positive effects on investment–cash flow sensitivity while collectivism had a negative effect. Furthermore, Li et al. (2021) showed that individualism, uncertainty avoidance and masculinity increased corporate investment efficiency through improving corporate social responsibility performance in 12 Asia-Pacific countries between 2006 and 2016. Choi (2020) documented that firms in countries of high individualism, low masculinity and high indulgence had more investment in R&D projects. Yan et al. (2021) also found that Confucian culture tends to increase R&D expenditure of Chinese private firms.

The extant literature showed that corporate investment decisions were determined by corporate risk-taking behaviour (Baird & Thomas, 1985; Bluhm & Krahnen, 2014; Shapira, 1995). Mihet (2013) used a research data of 50,000 firms from 400 industries across 51 countries and found that individualism was positively related to corporate risk-taking. Nevertheless, uncertainty aversion and tolerance for hierarchical relationships were negatively related to corporate risk-taking. In addition, Ashraf et al. (2016) documented that banks in countries of low individualistic culture, high uncertainty avoidance and high power distance engaged in more risk-taking. According to agency theory, due to the separation of corporate control and ownership, managers are likely to use firm resources to overinvest in unprofitable projects (Jensen, 1986; Jensen & Meckling, 1976). Unprofitable projects are deliberately and intentionally conducted by managers to expropriate shareholders; therefore, they are less influenced by managers’ risk-taking behaviour. If national culture makes corporate managers less willing to take risk, they are more likely to decrease corporate investment in profitable investment opportunities than to decrease their overinvestment in unprofitable projects. A decrease in corporate investment in profitable investment opportunities results in lower investment efficiency (González, 2018). When national culture affects firm investment efficiency mainly through the channel of underinvestment, cultural dimensions affect investment expenditure and investment efficiency in the same direction.

According to Hofstede (2001), people in societies of high individualistic culture are more self-confident. After reviewing a large number of cultural experiments and surveys, Markus and Kitayama (1991) also found that people in countries of high individualism were overconfident. They believed that they were more capable than the average person. In addition, Chui et al. (2010) showed that individualism score positively affected momentum trading profit across countries. Breuer et al. (2014) found that individualism was connected with overconfidence and over-optimism. Ashraf et al. (2016), Mihet (2013) and Shao et al. (2013) documented that individualism was positively related to corporate risk-taking. Zhang et al. (2016) also found a positive relationship between individualism and corporate investment bias. Therefore, we hypothesize that firms in countries of low individualism tend to reduce corporate investment in profitable projects. This makes their investment efficiency lower.

Uncertainty avoidance is the degree of threat that members of a specific cultural group feel when they are in unknown or ambiguous conditions. This feeling is, among other things, unveiled by a need for predictability (Hofstede, 2001). People in countries of high uncertainty avoidance consider uncertainty as a continuous threat. Therefore, they are more risk-averse (Li et al., 2013). Mihet (2013), Ashraf et al. (2016) and Zhang et al. (2016) also found that uncertainty aversion culture negatively affected corporate risk-taking. We hypothesize that firms in countries of high uncertainty avoidance culture tend to decrease corporate investment in profitable projects and thus their investment efficiency is lower.

In addition, power distance is defined as the extent to which less powerful members of a specific cultural group accept and expect the equality of power dissemination (Hofstede, 2001). It also characterizes highly stratified societies that value conformity higher than independence. People in high power distance societies tend to accept a hierarchical order and need no justification of power inequalities (Kumar et al., 2019). When powerful people have more privileges than powerless people, they have latent conflicts and rarely trust each other (Hofstede, 2001). However, in low power distance countries, they have latent harmony and more trust to each other. Prior studies in psychology showed a significant relationship between trust and risk-taking (Das & Teng, 2004; Growiec & Growiec, 2014). Mihet (2013) found supporting evidence for the negative relationship between power distance and corporate risk-taking. Consequently, we hypothesize that firms in countries of strong power distance culture tend to reduce corporate investment in profitable projects and thus their investment efficiency is lower.

In addition, Hofstede (2001) and Bae et al. (2012) posited that people in high masculinity countries focussed more on independence, outcomes and performance. Masculinity indicates how tough values (e.g., assertiveness, success and competitiveness) dominate a society and thus visible achievement and earning money are preferred (Hofstede, 2001). Performance-driven managers are more willing to take risk and thus have higher incentives to exploit investment opportunities (Bae et al., 2012). Therefore, we hypothesize that firms in countries of high masculinity experience higher investment efficiency.

Methodology

Data Source

Firms in our data are from countries suggested by La Porta et al. (2006). Financial information is obtained from Compustat database. In line with Bates et al. (2009), we consider R&D expenditure as zero if it is unavailable. Following prior across-country studies, we eliminate observations that are not suitable for subsequent analysis: (a) observations have negative total assets or negative book equity; (b) observations belong to utilities industry and financial sector (Fama & French, 2001); (c) firms have several issues of common stocks (Ferris et al., 2009) and (d) observations fail to have information from consolidated financial statements (Mahajan & Tartaroglu, 2008). Finally, we obtain a research sample with 280,092 firm-years from 33,947 firms across 44 countries during the period 2002–2018.

Empirical Model

In line with Fazzari et al. (1987), Baker et al. (2003), McLean et al. (2012) and Chen et al. (2017), we use an investment model to investigate the effect of national culture on investment efficiency. Corporate investment is proxied by total capital expenditure and R&D expenditure. Investment efficiency is proxied by the sensitivity of corporate investment expenditure to investment opportunities.

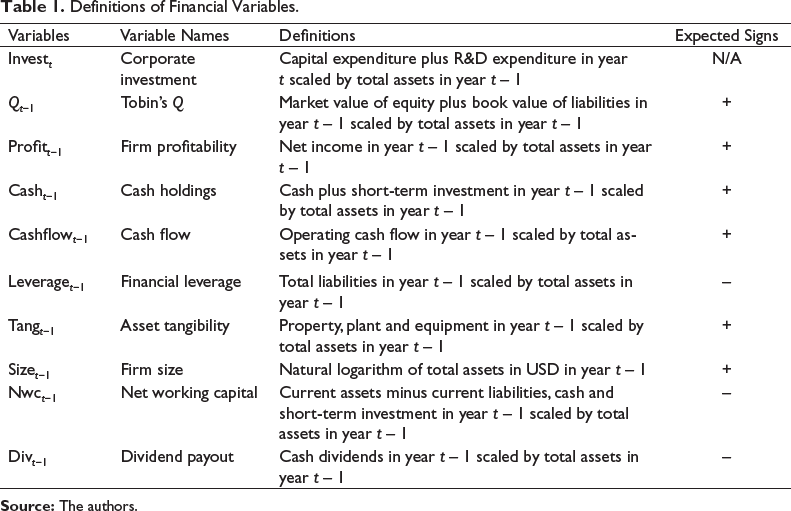

where Invest i,j,t is corporate investment of firm i in country j in year t. Qi,j,t−1 is Tobin’s Q of firm i in country j in year t − 1. IND, UAV, PDI and MAS are Hofstede’s cultural dimensions including individualism, uncertainty avoidance, power distance and masculinity, respectively. Each interaction between Tobin’s Q and a cultural dimension is employed to investigate the effect of national culture on firm investment efficiency. F_control is a vector of firm-level control variables including firm profitability, cash holdings, operating cash flow, financial leverage, asset tangibility, firm size, net working capital and dividend payout. Firms with high profitability, cash holdings and cash flow have more resources. Therefore, they are more likely to increase their investment (Chen et al., 2017). In line with pecking order theory suggested by Myers and Majluf (1984), firms with lower leverage, high tangibility and large size incur lower costs of external financing and thus they may raise their investment. Net working capital is an alternative of cash holdings. Dividend payment reduces corporate cash reserves. Consequently, firms with higher net working capital and dividend payout tend to have lower corporate investment. C_control is a vector of country-level control variables, namely, shareholder protection, creditor protection, private credit, market capitalization, GDP per capita and GDP growth. Definitions of financial variables are presented in Table 1.

Definitions of Financial Variables.

Analysis

Descriptive Statistics

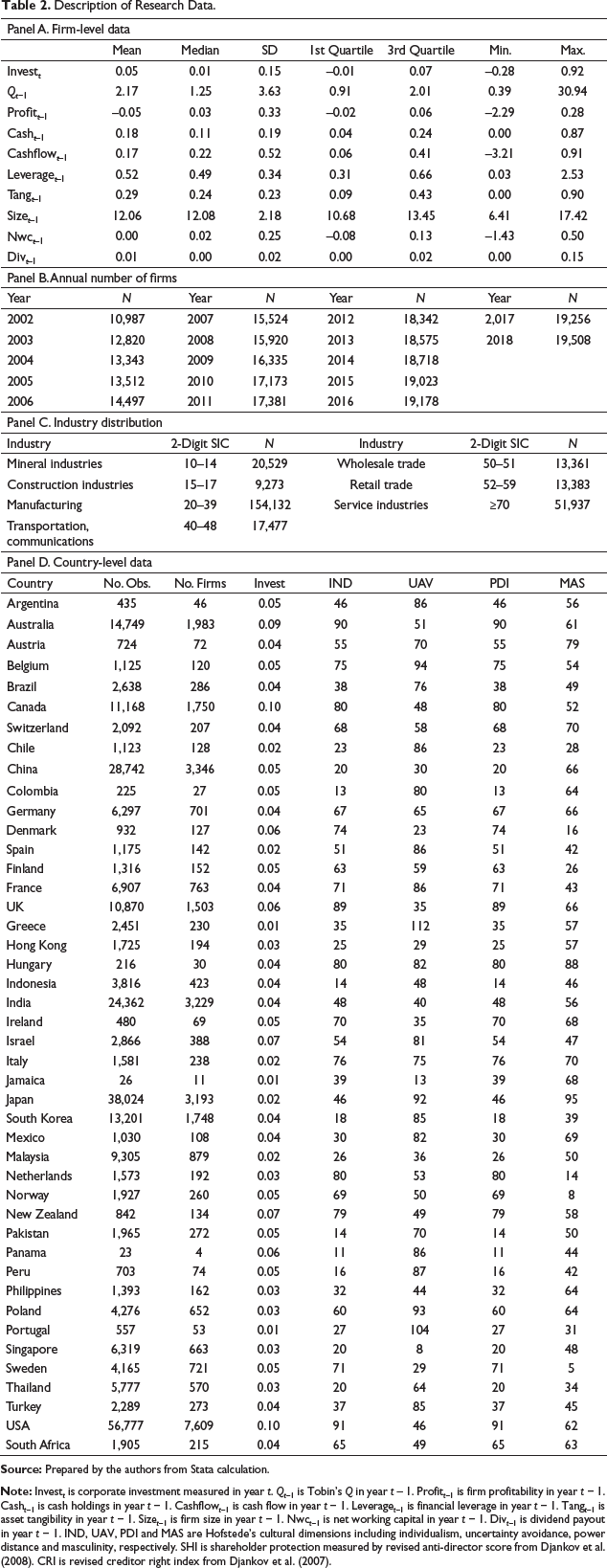

Table 2 presents description of research data. We winsorize all financial variables at 1% to eliminate outliers’ effects. Panel A shows descriptive statistics of financial variables. Corporate investment varies considerably from –0.28 to 0.92. Its mean is 0.05. Tobin’s Q also fluctuates significantly from 0.39 to 30.94 and has an average value of 2.17. Panel B illustrates that the annual number of firms tends to increase gradually over the research period. There are 10,987 firms in 2002 and 19,508 in 2018. Furthermore, panel C shows that manufacturing is the largest industry (154,132 firm-years), followed by service and mineral with 51,937 and 20,529 firm-years, respectively. The smallest industry is construction with only 9,273 observations. In addition, panel D reports country-level data. US firms provide the largest number of observations with 56,777. Colombia constitutes the smallest percentage of firm-years in the sample with only 225 observations. This imbalance is also present in prior cross-country studies regardless of data source.

Description of Research Data.

Regression Results

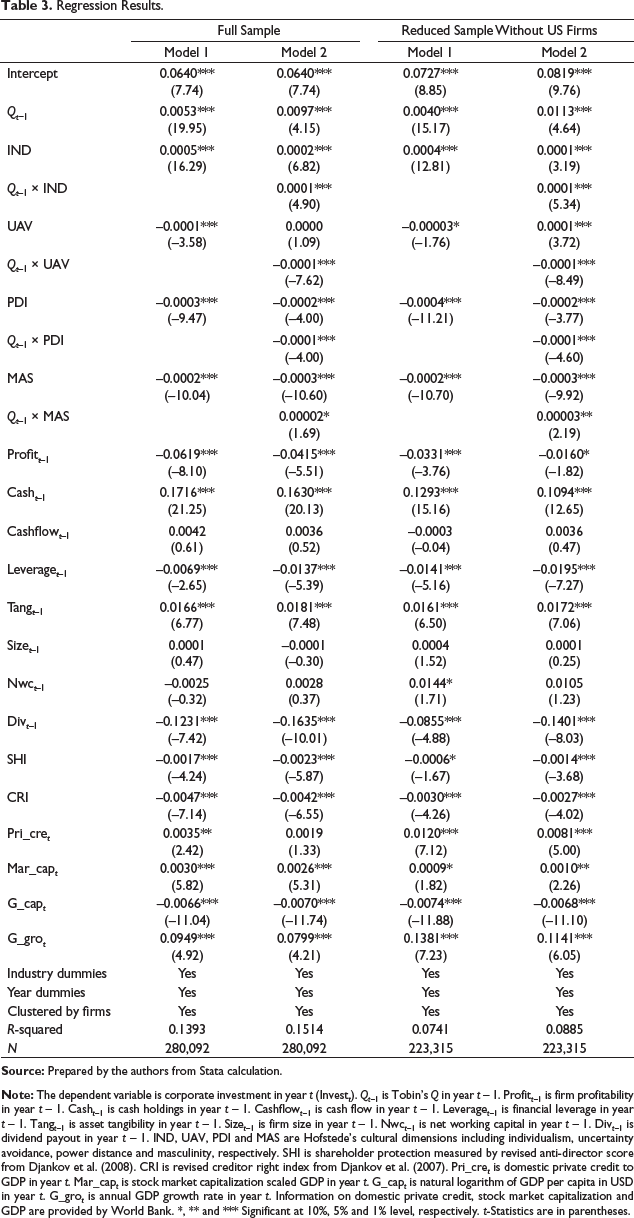

Table 3 presents results of pooled ordinary least squares (OLS) regression to analyse how national culture affects corporate investment decisions. Regression results for the reduced sample without US firms are also presented as robustness checks. Models 1 and 2 are used to investigate the effects of national culture on corporate investment and investment efficiency, respectively. In model 2, we use interactive terms between Tobin’s Q and cultural dimensions to investigate the relationship between national culture on corporate investment efficiency. In line with Shao et al. (2013) and Zhang et al. (2016), we find that individualism is positively related to both corporate investment and investment efficiency. Corporate managers in societies of high individualism are more self-confident (Breuer et al., 2014; Chui et al., 2010; Hofstede, 2001) and thus they are more willing to take risk. When firms engage in more risk-taking, they may increase their investment in unprofitable and/or profitable projects (González, 2018). An increase in corporate investment in unprofitable (profitable) projects leads to higher (lower) corporate investment efficiency. According to agency theory, corporate managers deliberately and intentionally overinvest in unprofitable projects to serve their personal benefits (Jensen & Meckling, 1976). Therefore, corporate risk-taking policy less influences corporate overinvestment and individualistic culture influences corporate investment efficiency mainly through the underinvestment channel.

Regression Results.

In addition, we find that uncertainty avoidance index is negatively associated with corporate investment in model 1. The coefficient of the interaction between uncertainty avoidance index and Tobin’s Q is also negative in model 2. Therefore, uncertainty avoidance culture negatively affects both corporate investment and investment efficiency. People in high uncertainty culture are risk-averse (Hofstede, 2001; Li et al., 2013). Hence, managers in countries high uncertainty avoidance are less willing to take risk and thus their firms have lower investment. Due to agency problem, when firms engage in less risk-taking, managers tend to reduce more investment in profitable projects instead of overinvestment in unprofitable projects. Consequently, they experience higher investment efficiency. These findings do not only provide supporting evidence for Zhang et al. (2016), but also provide additional knowledge on the way national culture determines corporate investment efficiency. We show that underinvestment is the effective transmission channel.

Moreover, consistent with Ashraf et al. (2016) and Mihet (2013), we also find that power distance negatively affects corporate investment and investment efficiency. Power distance culture reduces trust between people and thus they are willing to take risk (Das & Teng, 2004; Growiec & Growiec, 2014; Mihet, 2013). Accordingly, managers in high power distance countries tend to reduce corporate investment. Due to agency problem, corporate underinvestment is higher and thus investment efficiency is higher. Besides, our research findings show that the impact of masculinity on corporate investment efficiency is positive. Managers in high masculinity countries focus on success and competitiveness and visible achievement (Hofstede, 2001). Therefore, they are more willing to take risk to exploit profitable investment opportunities (Bae et al., 2012). This makes corporate investment more efficient.

Furthermore, in line with Modigliani and Miller (1958), we find that investment opportunities positively affect corporate investment. Besides, firm profitability is negatively related to corporate investment. This finding is opposite to our expected result; however, it can be explained by agency theory. Managers of high profitability firms are less likely to take risk due to their career concerns (Amihud & Lev, 1981; Hirshleifer & Thakor, 1992; Jensen & Meckling, 1976). Consequently, their firms have lower investment. Besides, we find that cash holdings are positively related to corporate investment. Firms with high cash holdings are more flexible to seize emerging projects, hence their investment expenditure is higher (Bates et al., 2009; Opler et al., 1999). Firms paying more dividends have lower corporate investment since dividend payment reduces their cash holdings. Moreover, financial leverage and asset tangibility negatively and positively affects corporate investment, respectively. These findings are consistent with pecking order theory (Myers & Majluf, 1984). Firms with lower leverage and high asset tangibility have better access to external funds with lower costs; therefore, they tend to increase their investment expenditure. In addition, we find that creditor protection is negatively related to corporate investment. This can be explained that firms in countries of strong creditor rights are controlled more strictly by creditors and thus they are less flexible to make investment decisions.

Robustness Check

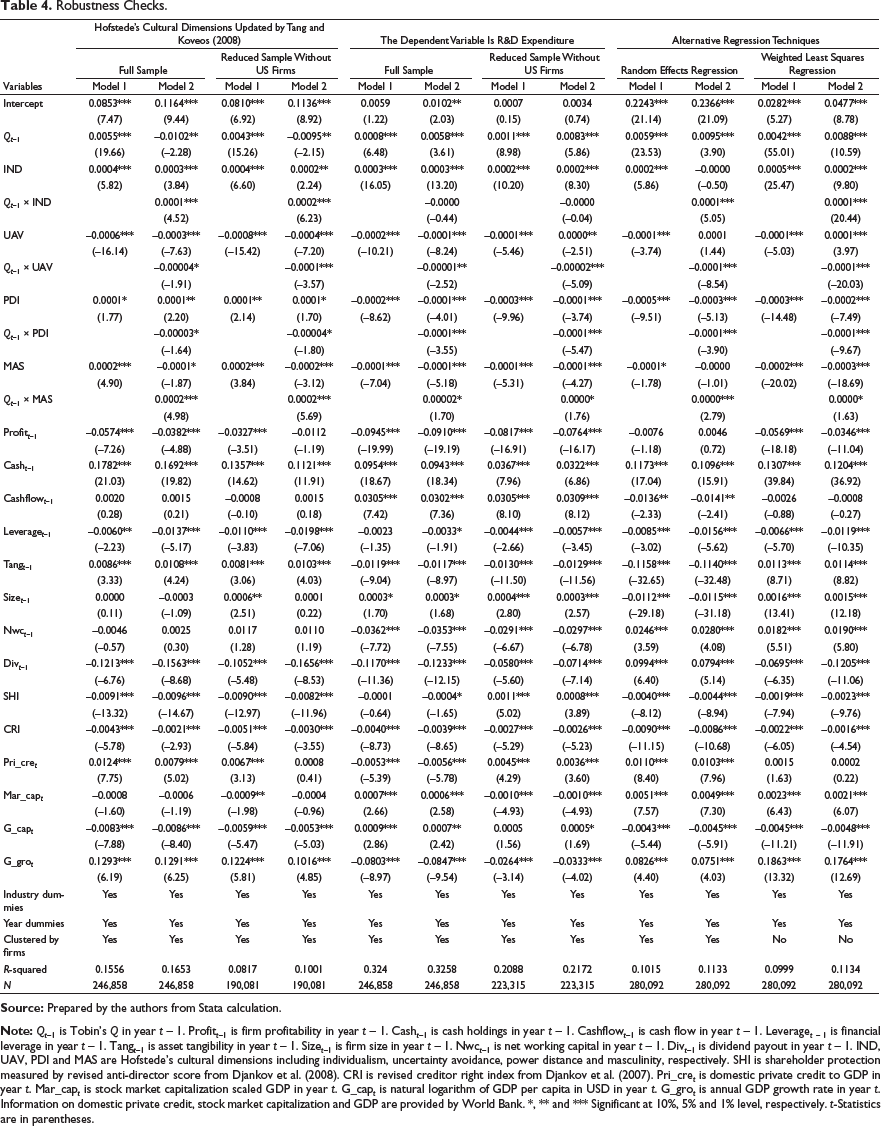

In order to ensure the consistency of our findings, we conduct the following robustness checks. First, we replace Hofstede’s original cultural dimensions by Hofstede’s updated dimensions from Tang and Koveos (2008). Tang and Koveos (2008) posit that apart from reflecting institutional traditions, cultural values should also manifest economic conditions of a nation. Therefore, they modify Hofstede’s original dimensions based on changes in national economic conditions. Second, following Chen et al. (2017), Shao et al. (2013) and Xiao (2013), we use R&D expenditure as an alternative dependent variable. Third, we use two alternative estimation approaches including random effect regression 1 and weighted least squares regression. 2 All regression results presented in Table 4 show that the effects of national culture on investment efficiency remain unchanged.

Robustness Checks.

Conclusion

Corporate investment efficiency may be determined by changes in overinvestment and/or underinvestment. Prior studies showed that national culture dimensions affected corporate investment efficiency. However, they failed to address whether overinvestment or underinvestment is the effective mechanism to transmit these effects. With a research data of 280,092 year-firms from 44 countries, we find that national culture affects corporate investment efficiency through underinvestment. Hofstede’s individualism and masculinity positively influence investment efficiency while uncertainty avoidance and power distance negatively influence investment efficiency. Our robustness checks with a reduced sample, updated cultural dimensions, R&D investment and various regression techniques also show that these findings are stable.

This article contributes to the literature on culture and finance as follows: First, the effects of national culture on both corporate investment and investment efficiency imply whether overinvestment or underinvestment is the transmission channel. When a cultural dimension affects corporate investment and investment efficiency in two opposite directions, an increase in investment efficiency is caused by a decrease in overinvestment. However, when a cultural dimension affects corporate investment and investment efficiency in the same direction, a decrease in investment efficiency is caused by a decrease in underinvestment. Second, we document that national culture influences investment efficiency mainly through the changes in underinvestment.

Managerial Implications

Corporate managers deliberately over-invest in unprofitable projects in order to build their empire; therefore, their risk management policy is ineffective in these projects. When a cultural dimension makes managers less (more) willing to take risk, they tend to decrease (increase) their investment in profitable projects rather than their overinvestment in unprofitable projects. In addition, our research findings also provide important implications for international investors and managers of multinational corporations. They should take national culture into consideration when conducting investment strategies and seeking joint-venture partners abroad. Moreover, corporate managers should have deep analysis of cultural environment to take advantage of cultural factors in their firms’ investment efficiency.

Study Limitations and Future Research

This study has two limitations as follows. First, cultural dimensions may be outdated. They were measured many decades ago while shared values and beliefs in our societies have changed significantly. Therefore, our results may be biased due to this problem. Second, we fail to measure investment efficiency in different ways due to data inavailability. Consequently, future studies may have better results and implications if they use updated cultural dimensions and various approaches to measure investment efficiency.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.