Abstract

The reshoring trend has gained momentum among manufacturing companies, which increasingly decide to relocate their production activities back to their home country. In this article, we explore the relationship between the motivations guiding the decision to reshore and the companies’ shareholder value. Particularly, taking an eclectic paradigm perspective, we aim to understand whether the motivations driving the companies’ decisions to reshore explain changes in the shareholder value. Empirically, we built an ad-hoc database based on 370 reshoring decisions involving the USA as a reshoring destination and announced in the 10-year time window ranging from 2009 to 2018. Our results highlight that resource seeking, market seeking and strategic asset seeking motivations positively affect the share price of the companies, while there are no market reactions when companies repatriate their activities because of efficiency-seeking motivations. This study extends previous literature offering explanations about how changes in the companies’ share price depend on the different reshoring motivations (i.e., efficiency seeking, resource seeking, market seeking, and strategic asset seeking motivations) pursued by the reshoring companies. Moreover, this study offers important implications for managers of companies undertaking reshoring decisions.

Introduction

During the last three decades, offshoring, that is, the location of a portion of the operations function to a foreign and usually low-wage country, has been considered one of the most important strategies for manufacturing companies (Boffelli et al., 2020; Nassimbeni et al., 2018). Recent evidence, however, highlights that an ever-increasing number of companies such as Apple, General Electric, Whirlpool and Ford, are announcing the return of their offshored production back to their home countries (Piatanesi & Arauzo-Carod, 2019; Wan et al., 2019). Such a reverse trend has been labelled in literature with different terms (e.g., reshoring, back-shoring, back-reshoring and homeshoring) but ‘reshoring’ seems to be the most commonly used one.

Reshoring is defined as a voluntary corporate strategy regarding the home-country’s partial or total re-location of (in-sourced or out-sourced) production (Fratocchi et al., 2014, p. 56). This strategy has been recently fostered by several factors, such as changes in the global economic conditions, home government policies, new production technologies and the demand for sustainability, which are calling companies to reconsider their location decisions (Barbieri et al., 2018; Wan et al., 2019).

As the reshoring trend has gained momentum among manufacturing companies, this strategy has gradually attracted the attention of scholars (Boffelli & Johansson, 2020; Stentoft et al., 2016; Wiesmann et al., 2017). The reshoring literature has paid most of the attention to the determinants of reshoring and, in particular, to the motivations why companies engage in the re-location of their production activities (Dachs et al., 2019; Ellram, 2013; Tate et al., 2014). This literature highlights that the decision to reshore may be driven by several different reasons, such as remaining close to customers, resolving quality issues related to the offshored production and taking advantage of collaborations with local partners (Ellram, 2013; Vanchan et al., 2018). However, while the extant reshoring literature has deeply enhanced our understanding of the different reasons behind the repatriation of business operations, scant attention has been devoted to exploring the implications related to such motivations. In this context, some scholars have addressed, for example, how the drivers to repatriate the production influence the geographical location of the reshored activities in the home country/region (Di Mauro et al., 2018; Wan et al., 2019). Some others have investigated whether different reshoring drivers have diverse implications across different industries (Joubioux & Vanpoucke, 2016; Martínez-Mora & Merino, 2014; Zhai et al., 2016). Moreover, Ancarani et al. (2015) have investigated how the motivations for the relocation from offshored countries to the home country affect the duration of the offshoring activities. Finally, Johansson and Olhage (2018) have addressed the relationship between the strategic motivations for relocation and the performance outcomes of companies.

Alongside, these already investigated effects of reshoring motivations, we reason that also the financial implications associated with such motivations deserve to be explored. To the best of our knowledge, so far, only Brandon-Jones et al. (2017) have investigated the financial implications related to reshoring. Particularly, by assessing how the reshoring decisions affect the shareholder wealth, authors indicate that reshoring decisions result on average in positive abnormal stock returns (Brandon-Jones et al., 2017). However, the authors disregarded considering that reshoring decisions may be guided by different motivations. Thus, in this explorative study, we aim to further investigate the relationship between reshoring decisions and shareholder value to understand whether the diverse motivations leading companies to repatriate their production differently affect their share price. Deepening the comprehension of the effects that different motivations have on shareholder values may provide theoretical insights about the financial consequences of implementing a reshoring strategy and enable companies to better evaluate the reshoring decision for securing the wealth of their shareholder.

We grounded this study on the eclectic paradigm (Dunning, 1998) by considering that when engaging in the reshoring decision-making, companies may pursue four kinds of motivations: resource seeking, market seeking, efficiency seeking and strategic asset seeking motivations. Then, building on the results of previous research on shareholder value (e.g., Alexandridis et al., 2017; Eckert et al., 2010; Mani & Luo, 2015; Ni et al., 2014; Perryman et al., 2010), we explore how the four kinds of reshoring motivations can explain changes in the share price of the company. Empirically, we built an ad-hoc dataset based on 370 reshoring announcements considering a 10-year time window, from 2009 to 2018. We gathered data from different secondary data sources including newspapers and magazines, press releases, companies’ websites, the website of the Reshoring Initiative, Yahoo! Finance and the Compustat databases. Then, we performed an event study and an econometric analysis.

This article offers important theoretical and managerial contributions. First, our study suggests that the stock market reaction depends on the different reshoring motivations declared by companies. Particularly, this research extends the previous study of Brandon-Jones et al. (2017) offering explanations about how changes in the companies’ share price depend on the different reshoring motivations (i.e., efficiency seeking, resource seeking, market seeking and strategic asset seeking motivations). Moreover, the results of this study extend previous literature investigating the effects of reshoring motivations (e.g., Ancarani et al., 2015; Di Mauro et al., 2018; Johansson & Olhager, 2018; Martínez-Mora & Merino, 2014; Wan et al., 2019; Zhai et al., 2016) highlighting that resource seeking, market seeking and strategic asset seeking motivations positively affect the share price of the companies. While it seems that, there are no market reactions when companies engage in reshoring activities because of efficiency seeking motivations. In addition, earlier research investigating conditions and determinants of the effect of various decisions (e.g., M&A, alliance and recall decisions) on the companies’ share price suggests that the stock market reacts differently to the diverse motivations behind these decisions (e.g., Alexandridis et al., 2017; Eckert et al., 2010; Ni et al., 2014; Perryman et al., 2010). Thus, this article contributes to the literature investigating the relationship between companies’ decisions and shareholder value suggesting that the reshoring announcements affect shareholder value. Finally, this study attempts to offer some practical implications to managers taking their reshoring decisions and advise them about the effect that different reshoring motivations have on the shareholder value.

Literature Background

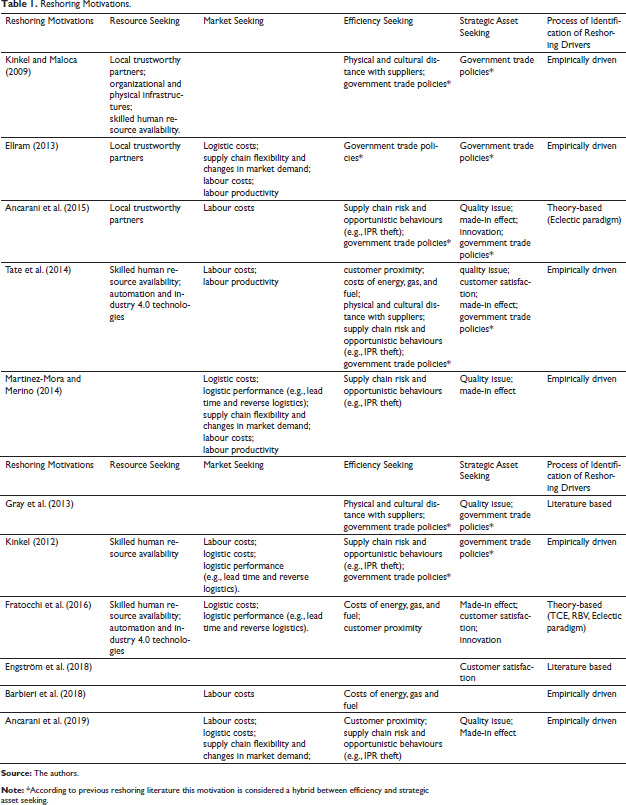

Previous scholars have largely discussed the reshoring outcomes highlighting the main benefits deriving from such a relocation decision. For example, the decision to reshore may avoid intellectual property thefts, which are usually more common in offshore countries such as China (Ellram, 2013). Moreover, reshoring may enable companies to better manage their production capacity and inventory, reducing the risk of production excesses and stockouts (de Treville & Trigeorgis, 2010; Tate et al., 2014). Relocating the production closer to the customers, reshoring may also enable companies to respond faster to changes in the customer demands (Ellram, 2013). In addition, reshoring could lower the risk of product-quality defects, which may result in a higher magnitude of product recalls (Bruccoleri et al., 2019). Since reducing the distance between design and manufacturing units, bringing back operations to the home country could also increase the company’s innovation rate (Tate et al., 2014). Furthermore, reshoring is likely to reduce communications and transportation costs (Porter & Rivkin, 2012). Finally, companies may also take advantage of marketing benefits associated with being able to claim that products are produced in the home country (Ancarani et al., 2015). Reshoring literature highlights how companies pursue different motivations when deciding to relocate their production activities back to the home country to reach such benefits. Specifically, some previous scholars addressing the reshoring motivations have embraced Dunning’s ‘eclectic paradigm’ perspective (Dunning, 1998) to explain why companies decide to repatriate their activities. Following these scholars and leveraging their clusterization (Ancarani et al., 2015; Fratocchi et al., 2016), we consider that reshoring drivers can be grouped into four main categories, that is, resource seeking, market seeking, efficiency seeking and strategic asset seeking motivations.

Broadly speaking, resource seeking motivations are related to some drivers related to the differences between the resources located in the home country and those in the offshore country (e.g., Ancarani et al., 2015; Dunning, 1998; Ellram, 2013). For instance, since it is difficult to establish a reliable raw material supply network in the offshore country, some scholars suggest that companies repatriate the production to rely on local partners, which are generally more trustworthy than those in the hosted country (Kinkel & Maloca, 2009). Also, some other scholars point out a critical gap between the organizational and physical infrastructures needed to run a company and those offered by some offshored countries (e.g., Mexico), which often leads companies to bring back home their production activities (Benstead et al., 2017; Kinkel & Maloca, 2009; Moore et al., 2018). Furthermore, scholars suggest that companies decide to reshore because they are concerned about the availability of some key resources such as skilled human resources, automated machinery and industry 4.0 technologies, which are severely limited in the offshored countries when compared to the home country (Ancarani & Di Mauro, 2018; Tate et al., 2014).

Considering the market seeking motivation it is possible to identify several other drivers why companies engage in the reshoring activities that mainly concern labour and logistic factors (Ancarani et al., 2015; Barbieri, 2019; Dunning, 1998; Ellram, 2013). Particularly, some studies suggest that companies reshore their activities to streamline their supply chain and make it more flexible and less costly (Kinkel et al., 2007; Martínez-Mora & Merino, 2014). In addition, companies may decide to reshore to reduce costs related to their reverse logistics activities caused by supply chain disruption events (Dong et al., 2018). Moreover, reshoring decisions can be driven by changes in the customers’ demand. This imposes companies to be more flexible to respond to the new conditions on the logistic structure as, for example, lower lead times are easier to observe when producing in the home country (Kinkel & Maloca, 2009; Martínez-Mora & Merino, 2014). Finally, some other studies argue that a driver of repatriating the production is the difference in the labour productivity between home and offshored countries (Bailey & De Propris, 2014; Tate et al., 2014). Particularly, these studies advance that, although the reshoring decision may lead to higher labour costs in the home country, it also results in higher labour productivity per output compared to the hosted country (Ellram, 2013).

Moving on to efficiency seeking motivation, previous literature mentions several other reshoring drivers that mainly consider production-cost-related factors (Ancarani et al., 2015; Dunning, 1998; Ellram, 2013). For example, some researchers highlight that a prominent driver to pursue the reshoring strategy is the possibility to reduce costs related to both excess of production and stockouts (Bailey & De Propris, 2014; de Treville & Trigeorgis, 2010; Tate, 2014; Tate et al., 2014). Being close to the customers, indeed, companies can postpone the production until they have a better estimate of the demand, thereby eliminating the safety stocks and reducing the inventory costs (de Treville & Trigeorgis, 2010; Porter & Rivkin, 2012). Other production costs that drive the need to reconsider the companies’ location decisions are the costs of energy, gas and fuel that, for example, in the USA are lower than in many offshoring countries (Porter & Rivkin, 2012; Tate, 2014). Finally, some other researchers suggest that companies may reshore their production to reduce the physical and cultural distance with their suppliers. Thereby reducing supply chain and opportunistic behaviour risks and the associated costs for negotiating, monitoring and enforcing transactions (Bailey & De Propris, 2014; Gray et al., 2013; Martínez-Mora & Merino, 2014; Tate, 2014). For example, reshoring could lower the risk of intellectual property theft, which tends to be more common in offshore locations as, for example, in China or India (Jagadeesh & Sasidharan, 2014; Kinkel, 2012).

Last, exploring the category of strategic asset seeking motivation it is possible to list some other drivers concerning the possibility for companies to protect and access valuable assets, and to take advantage of synergies associated with the presence in their home country (Ancarani et al., 2015; Dunning, 1998; Ellram, 2013). For instance, scholars highlight that one of the most important drivers to repatriate the production is solving quality issues in the offshore country (e.g., Bailey & De Propris, 2014; Martinez-Mora & Merino, 2014; Tate et al., 2014). The low-quality level characterizing the production in the offshored countries, indeed, leads companies to face product recall issues that damage the brand reputation of their companies (Bailey & De Propris, 2014; Tate, 2014). Some other scholars also suggest that customer satisfaction is a driver for companies taking a step back in their manufacturing location decisions (Engström et al., 2018; Tate et al., 2014). In fact, by relocating the business to the home country companies could meet customers’ demands more accurately and offer them more customizable products, so increasing their satisfaction (Engström et al., 2018). Moreover, scholars advance that a reason for reshoring is the opportunity for companies to benefit from the so-called ‘made-in’ effect (e.g., Fratocchi et al., 2016; Martínez-Mora & Merino, 2014; Tate et al., 2014). Such a strategic effect is a key driver in consumers buying behaviour and it has emerged as particularly relevant in those industries in which the perceived quality of the products is influenced by the production location (e.g., fashion industry), and in those industries with a long-standing reputation (e.g., Italy) (Fratocchi et al., 2016). In addition, some other scholars reason that another strategic asset seeking driver to reshore is innovation. These scholars suggest that reducing the geographical and cultural distance between the design and the manufacturing units allows companies to improve their innovation rate (Mcivor, 2013; Moretto et al., 2019; Tate et al., 2014). Finally, a further critical driver is related to the home country’s government policy that regulates trade (e.g., tax advantages and subsidies), which can voluntarily incentivize companies to repatriate their production activities to favour the local economy (e.g., Ancarani et al., 2015; Tate et al., 2014).

Reshoring Motivations.

Conceptual Development

In this section, we explore the determinants of shareholder values due to the reshoring activities. Earlier research investigating the determinants of shareholder value has studied the effect of different kinds of companies’ decisions (e.g., M&A, alliances, foreign direct investment and recall decisions) on the share price (Alexandridis et al., 2017; Arend, 2004; Campa & Hernando, 2004; Das et al., 2003; Eckert et al., 2010; Mani & Luo, 2015; Ni et al., 2014, 2016; Perryman et al., 2010; Zhao et al., 2013). Some scholars suggest that M&A decisions driven by the possibility for firms to leverage synergistic benefits between the acquiring and target companies positively affect the shareholder value (e.g., Alexandridis et al., 2017). Focusing on the relationships between alliances and shareholder value, previous literature suggests that market reactions to alliance announcements depend on different driving motivations (e.g., Das et al., 2003). For instance, some studies show that the market reacts negatively to alliances that focus on product activities (Mani & Luo, 2015). Other researchers advance product recall announcements motivated by major hazards have a more negative effect on the shareholder value since they are likely to receive substantial attention from the media entailing severe consequences on the companies’ reputation (e.g., Ni et al., 2016). Moreover, focusing on the role of the CEO, it may be expected a negative market reaction whether the CEO leaves the company to take up another job or due to health reasons (Perryman et al., 2010). Finally, some scholars highlight that the effect of investing in a foreign country depends on whether the strategic motive is resource seeking or market seeking (Barbopoulos et al., 2014). Thus, from this previous research, it emerges that the stock market reacts differently to the diverse motivations that guide companies in undertaking these decisions.

In line with the reasoning of previous research investigating the determinants of shareholder value, we propose that the reshoring motivations may determine different market reactions. As such, taking together the reshoring literature investigating the reshoring motivations under the eclectic paradigm perspective, we explore how the four main reshoring motivations (i.e., resource seeking, market seeking, efficiency seeking and strategic asset seeking) affect the shareholder value.

Hence, we aim to explore the following proposition:

Proposition: Reshoring motivations can explain changes in the shareholder value of the company.

Methodology

Data and Sample

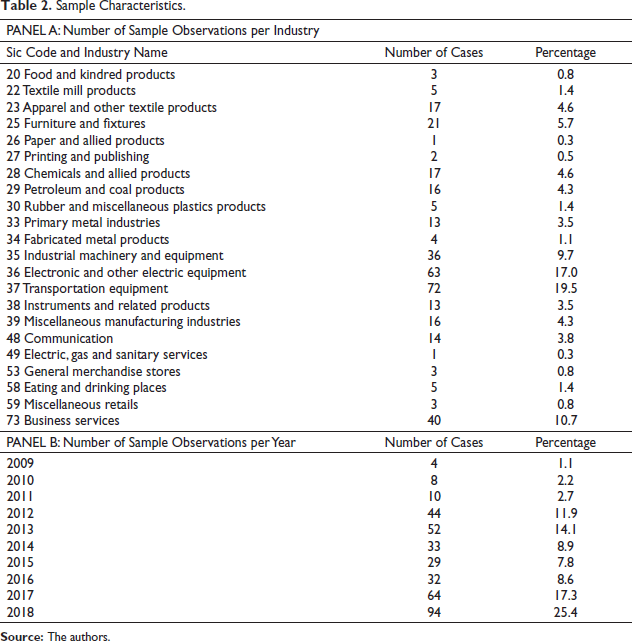

To analyse the relationship between reshoring motivations and shareholder value, we built a unique database using secondary data from different sources. Specifically, the database used in this study was created through the following steps. First, we collected data about the reshoring announcements retrieved from the Reshoring Initiative, a database largely used by previously reshoring scholars (e.g., Brandon-Jones et al., 2017). Leveraging such a database, we were able to collect data about the reshoring decisions announced in the 10-year time window ranging from 2009 to 2018. Particularly, we only focus on those reshoring decisions involving the USA as a reshoring destination. Second, two of the authors searched for a timestamp for the earliest public announcement of each reshoring decision of the database from sources, for example, Dow Jones, Associated Press and PR Newswires. If we were not able to retrieve the time stamp for a reshoring announcement, we excluded that reshoring decision from our database. We leverage such a condition to align calendar dates to event dates (e.g., Brandon-Jones et al., 2017). Third, two of the authors independently carried out a content analysis on the announcements to extract all the necessary information as the reshoring motivations and the offshore location from which the companies moved their operations (e.g., Ancarani et al., 2019). Considering the reshoring motivations, in less than 5% of cases, the two authors provided different interpretations of data sources. In these cases, a third author was involved, and all the data sources were reviewed again until an agreement was reached. Whether the agreement has not been reached because of critical inconsistencies among the multiple sources considered, the reshoring case has been excluded from the database. Focusing on the offshore locations, we imposed the condition that a reshoring announcement must mention the offshore location from which the firm moved its production activities. Such a condition allows us to weed out from our final database all those announcements that mainly pertain to manufacturing expansions or factory openings, rather than to manufacturing relocation decisions (e.g., Brandon-Jones et al., 2017). Furthermore, if a company has reshored its business activities from two different host countries such a reshoring announcement has been accounted as two different observations in our database (e.g., Ancarani et al., 2015). Then, since we need to collect data about the share price of the reshoring companies, we excluded from the database all those reshoring initiatives carried out by companies whose stock price data was not available on the Yahoo! Finance database for the full year before the announcement date of the reshoring and until two trading days after the announcement date (Brandon-Jones et al., 2017). Finally, we used the compustat database to include economic and financial data about the reshoring companies.

Sample Characteristics.

Measures

Concerning the dependent variable, we operationalized the shareholder value as a continuous variable measuring the abnormal return (AR) of the reshoring companies (e.g., Brandon-Jones et al., 2017). By assessing the shareholder value through the abnormal stock return, we leverage the efficient market hypothesis suggesting that stock prices capture the full effect of companies’ decision to reshore in a relatively short period surrounding its announcement, that is, the event window (Fama, 1970). Before calculating the AR for the reshoring companies we identified the event window of interest, whose lengths should be as narrow as possible to minimize possible estimation bias (Mcwilliams & Siegel, 1997). In line with the previous study of Brandon-Jones et al. (2017), we use a one-day event period by leveraging stamp information on the reshoring announcements and adjusting, whether necessary, calendar dates into event dates. Particularly, in those cases when the reshoring announcement has been made before 4:00 p.m. EST on a trading day, we use that calendar day as the event date. Conversely, when the announcement has been made after 4:00 p.m. EST on a trading day, or at any time on a non-trading day, we set the event date to the following trading day. This adjustment procedure allows us to incorporate the information contained in announcements made during a period of stock market closure in the stock price as of the subsequent trading day. Thus, we were able to leverage a 1-day event period referring to the announcement date t as day 0.

Then, we computed the abnormal stock return as the actual stock return minus the normal return expected when the reshoring had not been announced. Specifically, for each reshoring company i on day t, the AR is equal to:

where Rit and E(Rit) are actual and expected normal stock returns, respectively. To calculate the expected normal return, we used an OLS market model regression, with the S&P500 value-weighted stock market index as a proxy for the market portfolio. Moreover, we considered an estimation period of 200 trading days ending 10 trading days before the announcement date (e.g., Brandon-Jones et al., 2017). In particular, the market model regression equation for a focal reshoring company i is equal to:

where Rmt is the day t return on the market portfolio, εit is a zero-mean disturbance term, and αi and βi are the two parameters of the market model (Campbell et al., 2012).

Then, we define the expected normal stock return for the focal reshoring company i on day t as follows:

where

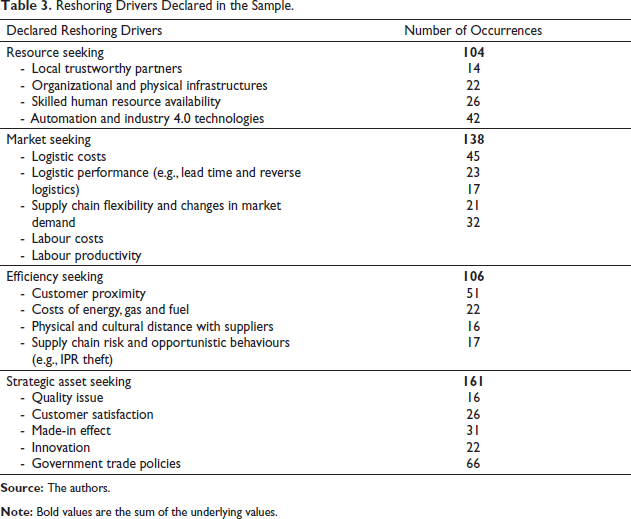

Reshoring Drivers Declared in the Sample.

Strategic asset seeking and market seeking motivations are prominent. Particularly, the most frequent reshoring driver is related to government trade policies (i.e., tax advantages and subsidies). Resource seeking and efficiency seeking motivations are less frequent. The less common driver for reshoring in our sample, concerns the possibility to leverage on local trustworthy partners compared with those in the host locations. To assess the classification of the reshoring motivations within the four eclectic paradigm categories of Dunning (1998), we computed the internal reliability of the four dummies by using a confirmatory factor analysis (CFA). The CFA’s results highlight that the category resource seeking has a factor loading equal to 0.69; the category market seeking has a factor loading equal to 0.78; the category efficiency seeking has a factor loading equal to 0.73; the category strategic asset seeking has a factor loading equal to 0.67. Since all the eclectic paradigm categories have factor loadings greater than 0.6, there is evidence for the reliability of the individual dummies (Hair et al., 2006).

Since the companies’ shareholder value could also be affected by other factors than the reshoring motivations, we included some other control variables in our model related to the operating performance and value of the reshoring companies (Flammer, 2015). Particularly, we control for the following companies’ financial and economic measures; net profit margin, return on equity (ROE), leverage, advertising on sales, return on asset (ROA) and cash flow on sales. Moreover, we control for the size of the company measured as the value of the company’s total asset. Due to the skewness of some data, we used the logarithm of the variable. In addition, we add the binary variable manufacturing, for controlling whether the reshoring company is a manufacturer (i.e., SIC codes 20–39) or a service company (i.e., SIC codes 48, 49, 53, 58, 59 and 73) (Brandon-Jones et al., 2017). Finally, we also add some control variables related to the attributes of the reshoring activity. Particularly, we add the count variable reshored products to control for the number of products associated with the reshoring activity as reported in the reshoring initiative database. Finally, we also controlled for the effect played by that the country from which the company has reshored its activities by using five dummies, that is, ‘China’, ‘India’, ‘South East Asia’, ‘South America’ and ‘Europe’.

Analysis and Findings

Event Study

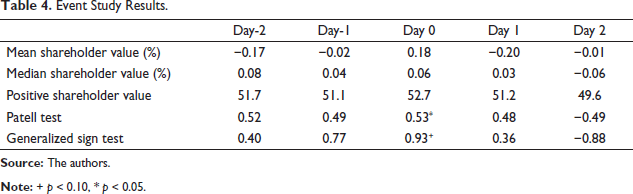

We use two different tests (i.e., the Patell test and the generalized sign test) to assess the significance of the variable shareholder value, which measures the AR. The Patell test weighs each AR estimate with an estimate of the variance of the residual stock returns (Patell, 1976). The generalized sign test is a nonparametric test, which leverages the fraction of positive AR for each company over the estimation period (Cowan, 1992).

Event Study Results.

Econometric Analysis

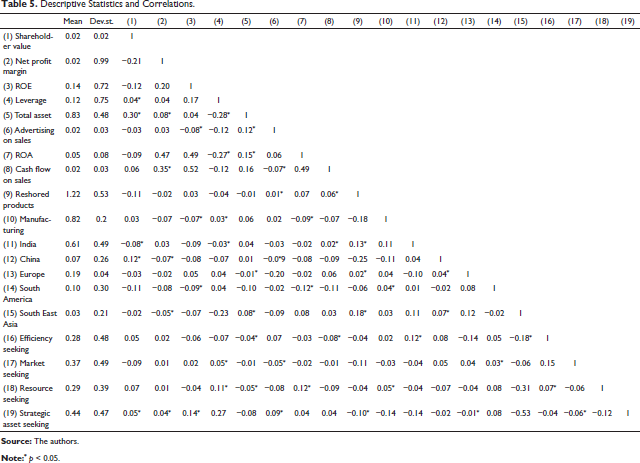

Descriptive Statistics and Correlations.

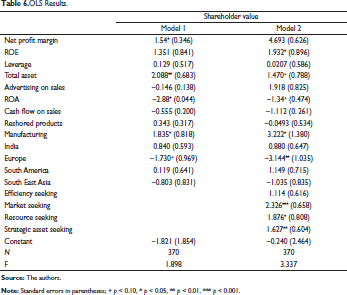

OLS Results.

Starting with the control variables model 1 suggests that net profit margin and total asset have a significant and positive effect on the shareholder value. In turn, the ROA has a significant and negative impact on the share price variation of the reshoring company. Furthermore, the results show that the control variable manufacturing has a significant and positive coefficient, suggesting that the reshoring announcements from manufacturing companies have a positive effect on the shareholder value compared to service companies. Finally, the dummy variable ‘Europe’ has a significant and negative effect on the shareholder value, meaning that reshoring the production activities from this country harms the share price of the company compared to repatriating the production from ‘China’, used as a baseline category.

Considering the dependent variables related to the reshoring motivations, we focus on model 2. The results show that market seeking, resource seeking and strategic asset seeking have a significant and positive coefficient meaning that, when the company’s decision to reshore is related to the possibility to leverage local high-quality labour and resources, to improve the companies’ logistic processes, or to access valuable assets, the share price of the company increases. Finally, the results reveal that efficiency seeking does not have a significant effect on the shareholder value, suggesting that there is no stock market reaction when a company decides to reshore for reducing its production costs.

Discussion and Conclusions

Our empirical investigation showed that the reshoring motivations are relevant to explain the effect of the company’s decision to reshore on changes in the share price. In what follows, we discuss our results and summarize them in a set of propositions.

Behind the reshoring strategy concerning resource seeking motivation, our results show a positive effect on the shareholder value. When a company decides to reshore its production activities for resource seeking motivations, one of its objectives is repatriating the production to leverage the availability of workforce and human resources that is more skilled and qualified in the home country than that in the foreign country (e.g., Tate et al., 2014). The human resources of a company are valuable since they constitute a determinant of the company’s competitive advantage (Wright et al., 2001). Particularly, the value of a company’s human resources reflects the skills and capabilities embodied in people and it affects the companies’ future cash flows (Hamel & Prahalad, 1994). Thus, by leveraging human resources with higher skills and capabilities in the home country, the company brings the market to think that it will be able to generate higher cash flows. If shareholders expect positive incremental cash flow, there will be a positive effect on the company’s share price (Becker et al., 1997).

In addition, another objective when repatriating the production according to resource seeking motivations is to count on a network of suppliers that is more reliable in the home country than that built in the offshored locations (e.g., Kinkel & Maloca, 2009). The performance of a company critically depends on the established network of suppliers since it affects the quality of products and their availability, the time to market for new product development, and the responsiveness and resilience of the company’s supply chain (Lambert & Schwieterman, 2012). Relying on suppliers located in the offshored countries, which are characterized by inadequate public infrastructures, more exposure to natural disasters and associated with a higher incidence of major accidents, companies face higher supply chain uncertainties that may undermine their cash flows (Abe & Ye, 2013; Klibi et al., 2010). As such, bringing the production at home to build a more reliable local supply network can lead the market to foresee that a company will be able to generate higher cash flows in the future, so generating gains for the company’s shareholders (Klibi et al., 2010).

Finally, companies can reshore their production to rely on resources such as advanced digital technologies in the home country (e.g., Ancarani & Di Mauro, 2018). Advanced digital technologies, such as automated machinery, big data and the internet of things, provide companies with great opportunities to sustain their competitiveness (Bender et al., 2018). Indeed, these technologies lower the total production costs of a company by both reducing the necessary labour input and shifting the ratio between capital and labour inputs in favour of the capital ones (Dachs et al., 2019). Consequently, moving the production to the home country to leverage advanced digital technologies strengthens the company’s ability to generate higher future cash flows, so generating gains for the company’s shareholders (Bender et al., 2018).

Considering the market seeking motivations for reshoring, our results suggest that such motivations may cause market predictions of positive changes in share price for the focal company. Reshoring for market seeking motivations, a company longs to improve its logistic performance (e.g., Kinkel et al., 2007; Martínez-Mora & Merino, 2014). Logistics performance reflects the location decisions of a company and it is usually associated with measures such as logistics costs (Bogataj et al., 2011). Particularly, logistics costs, such as transportation costs and costs related to reverse logistics activities (i.e., activities related to the flow of products from their place of consumption back to their place of production), impact the cash flows of the company by critically affecting the final price of the product to the customers (Novack et al., 1992). Consequently, relocating the production at home to reduce logistic costs can lead the market to predict higher company ability in generating positive incremental cash flows in the future and gains for shareholders (Mihi Ramírez, 2012).

Another market seeking motivation that brings companies to undertake the reshoring decision is the aim to have a more flexible supply chain to adapt to changing customer demands (Kinkel et al., 2007). Changes in the customers’ demand impose companies to fast adapt their logistic structure to new conditions, for example, prescribed lower lead times (Martínez-Mora & Merino, 2014). Lead times have a critical effect on the company’s cash flow since they may imply additional costs in the form of penalty and customer discounts whether the company is not able to deliver the product on time and need to delay their shipping (Sirias & Mehra, 2005). Since, lower lead times are easier to observe when producing in the home country, repatriating the production activities of a company brings the market to think that it will increase their future cash flows (Kinkel & Maloca, 2009; Kinkel et al., 2007). Hence, leading the market to foresee positive incremental cash flow, there will be a positive effect on the company’s shareholder value.

Furthermore, when a company decides to reshore its production activities for market seeking motivations, another of its objectives is to benefit from higher labour productivity typical of the home country (e.g., Bailey & De Propris, 2014; Tate et al., 2014). Labour productivity is a key indicator of the workforce performance of a company and it has been defined as the total output divided by the labour inputs (Datta et al., 2005). Consequently, leveraging on a higher level of labour productivity in the home country increases the company’s ability to produce the same level of output with a lower level of input, so generating higher future cash flows. Expecting positive incremental cash flow leads to positive changes in the shareholder value (Becker et al., 1997).

Finally, our results highlight that also pursuing strategic asset seeking motivations can cause a shareholder value gain. Consider, for example, the case of a company that decides to reshore its production activities to increase the level of customer satisfaction by meeting customers’ demands more accurately or offering them more customized products (e.g., Engström et al., 2018). Customer satisfaction plays a critical role for businesses in providing and maintaining a competitive advantage (Anderson et al., 2004). Particularly, higher customer satisfaction should lead to higher cash flow by pushing customers to purchase more products, recommending the acquisition of products to other potential customers and enabling the company to charge higher prices (Bolton, 1998; Narayandas, 1998). Thus, by relocating the production to the home country to foster the customers’ satisfaction, the company brings the market to think that it will be able to generate higher future cash flows, so increasing the company share price (Gruca & Rego, 2005).

Additionally, by repatriating the production following strategic asset seeking motivations, a company attempts to resolve quality and safety issues that can arise when manufacturing in the offshored country (e.g., Bailey & De Propris, 2014; Martinez-Mora & Merino, 2014; Tate et al., 2014). Quality issues refer to the likelihood that a product does not perform as projected while safety issues denote the probability that the product may harm the consumers (Ni et al., 2016). Both quality and safety issues strongly damage the reputation of the company, which in some cases has to recall its products undermining its cash flows (Kim et al., 2019; Ni et al., 2016). Then, solving these quality and safety issues by relocating the production at home allows the company to signal higher quality of its products, strengthen its reputation and increase its cash flows (Hsu & Lawrence, 2016). As such, the market may positively evaluate this relocation leading to an increase in the company’s share price (Kim et al., 2019; Ni et al., 2016).

Moreover, when a company decides to reshore its production activities for strategic asset seeking motivations, another objective is to take advantage of the ‘made in effect’ (e.g., Fratocchi et al., 2016). The ‘made in effect’ influences the products’ evaluation by customers, who generally develop positive buying attitude toward those products manufactured in the home country (Grappi et al., 2018). Customers perceive that the quality of the products made in the home country is higher compared to the quality of products manufactured in a foreign country (Grappi et al., 2019). Consequently, relocating the production for being able to declare that the product is made at home, brings the market to think that the company will be able to generate higher cash flows, so raising the company share price (Bharadwaj et al., 2011).

Additional insights emerge from the non-significant effect of efficiency seeking motivations on the shareholder value. According to this result, the stock market seems not to be influenced by the companies’ reshoring motivations related to production-cost-related factors as, for example, the aim to improve the inventory management or reduce the cultural distance with the network of suppliers (Bailey & De Propris, 2014; De Treville & Trigeorgis, 2010; Kinkel & Maloca, 2009; Martínez-Mora & Merino, 2014; Tate, 2014). Different reasoning can advance to explain such a non-significant result. For example, a possible explanation may be found in the market reaction to counteract decisions. The most frequent reason that leads companies to offshore their production activities in a host country is the reduction of costs and productivity of labour (Di Mauro et al., 2018; Gylling et al., 2015; Kinkel & Maloca, 2009). Offshoring is indeed a strategy that allows companies to reduce their labour costs while increasing productivity by benefiting from scale advantages and profiting from the lower-wage workforce (Farrell, 2004; Roza et al., 2011). Thus, repatriating the production for the same reasons that have previously pushed them to move the activities offshore, the market may reason that companies are reshoring to correct previous misjudgements (Kinkel & Maloca, 2009). For example, the companies may need to reshore the production because they have disregarded to consider the unanticipated costs associated with the implementation of the offshoring strategy (Larsen et al., 2013). Thus, the market may be disoriented by these counteracting companies’ decisions and lose confidence in companies’ decisions. In such a circumstance, since the market does not trust the decisions made by the company, it may prefer to wait for some proven effect of the reshoring decision and does not react to the reshoring announcement.

Implications of the Research

Theoretical Implications

The results of this article offer important theoretical contributions to previous literature. First, our empirical analysis has highlighted that the reshoring motivations may have critical financial implications for companies engaging in the repatriation of their business activities. Grounding on the eclectic paradigm perspective (Dunning, 1998) and building on the results of previous research on shareholder value (e.g., Alexandridis et al., 2017; Arend, 2004; Barbopoulos et al., 2014; Campa & Hernando, 2004; Das et al., 2003; Eckert et al., 2010; Mani & Luo, 2015; Ni et al., 2014; Perryman et al., 2010; Zhao et al., 2013), we showed how the motivations that drive the companies’ decision to reshore can also explain changes in the shareholder value. This result enriches previous literature exploring the relationship between reshoring and financial performance (i.e., Brandon-Jones et al., 2017). So far, this literature has neglected to consider that reshoring initiatives may be guided by different motivations, such as resource seeking, market seeking, efficiency seeking and strategic asset seeking motivations (e.g., Ancarani et al., 2015). From previous research, it emerges that the stock market reacts differently to the diverse motivations that guide companies in undertaking several strategic decisions such as M&A, alliances, foreign direct investment and recall decisions (e.g., Alexandridis et al., 2017; Barbopoulos et al., 2014; Mani & Luo, 2014; Perryman et al., 2010; Zhao et al., 2013). Thus, we add to previous contributions provided by Brandon-Jones et al. (2017) suggesting that changes in the share price of the reshoring companies depend also on the reshoring motivations declared in the reshoring announcements. This is because the motivations behind the decisions guide the expectations that shareholders have on the company’s future cash flows.

As such, the results extend previous literature investigating the implications related to different reshoring motivations (e.g., Ancarani et al., 2015; Di Mauro et al., 2018; Johansson & Olhager, 2018; Martinez-Mora & Merino, 2014; Wan et al., 2019; Zhai et al., 2016) highlighting that the reactions of the stock market to the companies’ reshoring decisions depend on why companies repatriate their business activities. As recognized by previous literature, when deciding to reshore, companies may pursue different motivations (Ellram, 2013), which have different implications for the companies. For example, some studies have investigated how reshoring motivations influence the geographical location of the reshored activities (e.g., Di Mauro et al., 2018; Wan et al., 2019). Among these studies, for instance, Di Mauro et al. (2018) argue that specific reshoring motivations influence the companies’ decision to distinguish between backshoring and nearshoring. These authors suggest that the strategic asset seeking motivation related to the ‘made in’ effect discourages companies from nearshoring while favouring the relocation of the manufacturing activities back to the proper home country. Moreover, some other studies have addressed the motivations for reshoring, investigating whether such motivations have a different impact in different industries (e.g., Joubioux & Vanpoucke, 2016; Martinez-Mora & Merino, 2014; Zhai et al., 2016). In this context, the motivation analysis conducted by Zhai et al. (2016) suggests that reshoring motivations have the same implications across different industries. Companies operating in different industries undertake the reshoring decision pursuing the same motivations. Moreover, Ancarani et al. (2015) have revealed how different reshoring motivations impact the duration of offshoring activities. They particularly propose that reshoring due to quality-related motivations and the ‘made-in’ effect are associated with shorter offshoring duration. Finally, Johansson and Olhager (2018) have verified that different reshoring motivations related to costs, market and competencies influence the operational performance of companies in terms of logistic costs and product quality. Hence, this study adds to prior literature investigating the motivations to reshore suggesting that beyond the geographical location, the industry implication, and the duration of offshoring activities, motivations to reshore have financial implications for the companies undertaking such a strategy. Particularly, resource seeking, market seeking and strategic asset seeking motivations have a positive effect on the share price of the companies, while efficiency seeking motivations do not entail market reactions. This has allowed providing reshoring literature with some propositions that may orient future reshoring literature in further exploring how the motivations that lead companies to relocate their production activities bask to the home country, determine the companies’ shareholder wealth.

Third, this article contributes to earlier research investigating the effect of companies’ decisions (e.g., M&A, alliances, foreign direct investment, recall decisions and board composition) on the shareholder value (e.g., Alexandridis et al., 2017; Eckert et al., 2010; Mani & Luo, 2014; Ni et al., 2014; Perryman et al., 2010). Particularly, previous literature suggests that stock markets react differently to companies’ decisions depending on the company’s motivations behind these decisions (Alexandridis et al., 2017; Arend, 2004; Campa & Hernando, 2004; Das et al., 2003; Eckert et al., 2010; Mani & Luo, 2015; Ni et al., 2014, 2016; Perryman et al., 2010; Zhao et al., 2013). For example, regarding the M&A some scholars suggest that an M&A pursued to leverage synergistic benefits between the acquiring and target companies has a positive effect on shareholder value (e.g., Alexandridis et al., 2017). Some other scholars show that M&A that aims at diversifying the two partners’ line of business tend to be more associated with poor shareholder value than M&A focused on a unique and shared line of business (Campa & Hernando, 2004). Regarding the decisions to ally, some studies show that the market reacts negatively to alliances that aim to develop new products (Mani & Luo, 2015; White & Lui, 2005) while other studies show a positive reaction when companies ally to set technical standards (Arend, 2004; Axelrod et al., 1995). Taking into account the recall of the product, prior literature asserts that the different effects of such an announcement on the stock market may be explained by several reasons (Chen et al., 2009; Ni et al., 2014). For example, some researchers suggest that the effect of the product recall on the shareholder value depends on whether the recall of the product is government-initiated or manufacturer-initiated (e.g., Chen et al., 2009). Some other researchers advance that product recall announcements motivated by a major hazard such as customer injuries have high negative effects on the shareholder value since these kinds of announcements are likely to receive substantial attention from the media, entailing severe consequences on the companies’ reputation (e.g., Ni et al., 2016). In sum, previous literature investigating the effect of companies’ decisions on the shareholder value has mainly focused on the effect of decisions such as M&A, alliance, foreign direct investments and management changes on share price disregarding also investigating the effect of the decision to reshore the production. Thus, this article contributes to this literature by suggesting that the decision to reshore influences the share price of the company and that it depends on the motivations that push companies to undertake the decision to repatriate their production activities.

Practical Implications

This study also offers some suggestions for managers undertaking the decision to repatriate their production activities to the home country. This study advises managers that the stock markets recognize the benefits associated with the reshoring decision. More particularly, the results of this article suggest to managers that the stock markets care about the motivations that push companies to engage in the reshoring activities. Rewarding reshoring decisions, which the companies claim to have taken it to leverage local high-quality labour and resources, improve their logistic processes and access to valuable assets. In turn, the reshoring strategy does not determine market reaction in terms of share price or whether companies undertake this decision for efficiency motivations. Since pursuing efficiency is the major reason for offshore, whether companies repatriate their production activities to reduce the production costs, may induce the stock market to interpret this decision as a correction to previous misjudged offshoring decisions.

Limitations and Suggestions for Future Research

While the present article provides a useful analysis of reshoring motivations and their implications on the companies’ share price, we acknowledge it is not exempt from limitations. Considering the nature of the data, the heterogeneity of sources used to collect data about the reshoring motivations (i.e., articles collected by the reshoring initiative dataset) carry the risk that such motivations may be ascribed to the judgments and the interpretation of commentators (Ancarani et al., 2015; Zhai et al., 2016). Future research may overcome this limitation by collecting primary data and conducting, for example, a survey asking companies the motivations that have pushed them to repatriate their business activities. Moreover, the sample of companies we used in this article only includes companies that have reshored their business activities disregarding to also include those companies that have previously offshored their production but have not reshored. Thus, to provide a clearer understanding of the relationship between motivations for reshoring and shareholder value future studies should compare the financial implications of both these two kinds of companies. In addition, the offshoring decisions in our sample are limited to USA companies. While the reshoring phenomenon has been much more limited in other parts of the world than in the USA, it could be critical for future studies to extend the investigations including for example European companies for transferring the results derived from the present article to other countries. Furthermore, regarding the dependent variable used in the study to assess the financial implications associated with reshoring, considering the share price of the companies, our propositions cannot be extended to non-publicly quoted firms. Thus, future research can consider alternative measures for assessing the shareholder value of companies such as sales and return on assets. Finally, our analysis focus on short-term stock price reactions. This approach is justified by the efficient market hypothesis suggesting that stock prices capture the full effect of companies’ announcements immediately (Fama, 1970). However, evidence of under-reaction or over-reaction to companies’ announcements has been proven by previous studies (Edmans, 2011). Hence, to address this further issue future research should analyse long-term stock market reactions to reshoring decisions.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.