Abstract

The objective of this study is to investigate the determinant factors of mobile wallet users’ continuance intention in Indonesia. It integrates technology continuance theory (TCT) with perceived security. Mobile wallet has been received well by Indonesian; however, the sustainability of the business is challenged by several issues, such as fierce competition, security concern, the practice of burning cash and low switching costs. Although the study of continuance intention of using information systems has caught scholars’ attention, the application of TCT in the study received little attention. This study used a questionnaire for data collection and convenience sampling for selecting the respondents. The total number of respondents in this study is 240 respondents and the data was analyzed using partial least square (PLS)-structural equation modelling (SEM). The result showed that perceived usefulness, satisfaction and attitude had a direct relationship with continuance intention, while the relationship between perceived security and continuance intention was insignificant. Perceived usefulness and perceived security were the predictors of satisfaction and attitude. This study also found that satisfaction influenced attitude. This study contributes to the study of Information systems and the use of TCT in understanding users’ continuance intention. The theoretical and practical implications, as well as future studies, are discussed.

Keywords

Introduction

Nowadays, people have a strong dependency on smartphones and the internet to complete their daily tasks. As a result, more smartphone-based service innovations are invented to assist people in completing their tasks effectively and efficiently. The mobile wallet is one of the innovations in the financial technology sector that facilitates mobile payment by using a smartphone as a device. It offers users an easy and convenient way of financial transactions without time and location limitations and connects all users’ financial transactions from various sources (Talwar et al., 2020). Moreover, users use mobile wallets to pay monthly bills, purchase goods online and pay for online riding services.

Indonesia is one of the countries that has accepted mobile wallets as one of the modes of mobile payment. It is among the six countries in Southeast Asia with the highest usage of mobile payment in Southeast Asia (Pricewaterhousecoopers, 2019) and the level of mobile wallet awareness reaches 82.7% (VOI, 2021). The Central Bank of Indonesia (Crisanto, 2021) reported a 38.62% growth in mobile money transactions between 2019 and 2020 and the transaction value is projected to reach US$83,520 million by 2025 (Nurhayati-Wolff, 2021)

However, mobile wallet service providers face several challenges to further sustain their business. First, the market fierce competition, according to (CIPS Indonesia, 2020) there are 51 mobile wallet service providers in Indonesia. Crisanto (2021) reported that Indonesia has a 270 million population with 50% of them still unbanked. This shows a large opportunity for mobile wallet service providers to ripe in. Second, low retention rate due to low switching costs; with many providers in the market and low switching costs, users can switch from one provider to another (Sasongko et al., 2021). Zhou (2014) asserted that low switching costs lead to low user retention. While the sustainability of technology-based service providers depends on user retention that actively uses the service (Bhattacherjee et al., 2008). Third, the practice of burning cash by offering sales promotions leads to a company incurring a loss of almost US$10 per user on US$3 revenue (Mittal & Mitra, 2020). Four, security concerns, the habit of using cash and fear of being scammed are among three Indonesian’s user’s concerns to use a mobile wallet (Statista, 2021). Many scholars (e.g., Chen & Li, 2017; Khayer & Bao, 2019; Nguyen & Simkin, 2017; Parnell et al., 2018) stated that security concerns and fierce competition may result in the discontinued use of a service. Accordingly, this study addresses the challenge related to users’ security concerns to users’ continuance intention (CI) to use the mobile wallet.

Continuance usage intention is the user’s willingness to keep using a technology-based service/product after adoption (Bhattacherjee, 2001). Intention to continue using occurs in the post-adoption stage where users have interacted with the service and resulted in having a higher level of belief, attitude and knowledge about a service (Lee & Kim, 2020). As a result, differences in users’ behaviour between the pre-adoption stage and post-adoption stage may exist that later affect their future behaviour (Khayer & Bao, 2019). Moreover, Lee and Kim (2020) showed that users use different criteria to decide for each adoption stage. Therefore, it is imperative to examine the determinant factors that influence users’ decision to continue using the mobile wallet, particularly when the success of the business lies in the continuance of using the service (Alghamdi et al., 2018; Bhattacherjee et al., 2008; Gao et al., 2015). However, the study in the mobile wallet context that focused on the post-adoption stage is still limited (Alhassan et al., 2020; Gupta et al., 2020a; Khayer & Bao, 2019; Oertzen & Odekerken-Schröder, 2019). Hence, this study aims to investigate the determinant factors of mobile wallet users’ continuance usage intention.

Yan et al. (2021) conducted a systematic literature review on the CI study and concluded that there are two models frequently used in the study like technology acceptance model (TAM) and expectation confirmation model of information system (ECM-IS). Both theories have different views on what shapes users’ CI. TAM focuses on attitude as the central construct that connects users’ beliefs (i.e., Perceived usefulness [PU] and ease of use) with behaviour intention (Davis et al., 1989). While ECM views satisfaction acts as the connector (Bhattacherjee, 2001). However, according to Foroughi et al. (2019), users’ continuance use depends on both satisfaction and attitude. Further, the cognitive model (COGM) theorizes that CI is based on satisfaction and attitude (Oliver, 1980). Therefore, the weakness of TAM and ECM is not integrating satisfaction and attitude into one model.

Technology continuance theory (TCT) is a theory that predicts users’ willingness to keep using the technology-based service/product by integrating satisfaction and attitude into one framework (Liao et al., 2009). The theory proposed that users’ CI is built on the users’ PU of the products/service, their satisfaction after interacting with the product/service, and their favourable attitude toward the product/service (Liao et al., 2009). Although TCT has higher explanatory power than the two popular models (i.e., TAM and ECM), an improvement of TCT by applying it in different contexts and settings is still possible (Liao et al., 2009). Veeramootoo et al. (2018) asserted the importance of combining, and/or extending theories in understanding the behaviour of IS users in every stage of adoption. In addition, modifying and revising a model are claimed to be a requirement in a specific application of Information technology.

Literature shows that some studies have modified, and/or extended the TCT with other theories or variables to suit the research setting. For example, Khayer and Bao (2019) conducted a study aimed to examine the CI of Alipay users by integrating TCT with context-awareness theory. Abdul-Halim et al. (2021) applied TCT to study about CI of mobile wallet users in Malaysia by extending the constructs with price benefit, trust, habit and operational constraints which are used to measure the direct relationship with CI. While Foroughi et al. (2019) extended the TCT by adding self-efficacy and channel preference to measure mobile banking users’ continuance use. Daragmeh et al. (2021) studied the continuance used of mobile wallet users during the Covid-19 pandemic by combining the health belief model (HBM) and TCT into one framework.

However, TCT has never integrated with perceived security (PS), most scholars applied TAM (Chawla & Joshi, 2019; Ogedengbe & Abdul-Talib, 2020; Patel & Patel, 2018; Shankar et al., 2018), ECM (Kumar et al., 2018; Lim et al., 2019; Ogedengbe & Abdul-Talib, 2020; Prakash et al., 2021) and diffusion theory (Abu Salim et al., 2021; Shao et al., 2019). Integrating PS in TCT is essential in enhancing the understanding of mobile wallet users’ CI. Garrouch (2021) stated that when a service is related to financial transactions and personal data, PS is one of the important variables that influence users’ decisions to use the service. It affects users’ evaluation of the service (i.e., satisfaction, dissatisfaction) and their decision to continue using the service (Susanto et al., 2016). It also reflects the quality of mobile wallet services (Kapoor et al., 2020). Hence, this study modifies the TCT by adding PS into the framework to better understand the CI of mobile wallet users.

Subsequently, the novelty of this study is applying TCT to study mobile wallet CI by integrating PS into the model. This study enriches the use of TCT as the theoretical foundation in studying information system CI. It also contributes to providing some strategies based on the study’s findings to the mobile wallet service providers in retaining current users. Moreover, the article is organized as followed, the following section is the literature review and hypothesis development of the study. Then, it is followed by a description of the research method, the result as well as the discussion and conclusion. Finally, this study’s limitations and future studies are presented at the end of this article.

Literature Review

Technology Continuance Theory (TCT)

TCT is developed by Liao et al. (2009) as an improvement of two widely used theories in IS continuance studies TAM (Davis et al., 1989) and ECM-IS (Bhattacherjee, 2001). Liao et al. (2009) criticized that the models strongly rely on one central construct to explain user behaviour in IS. They criticized TAM for relying on attitude as the determinant of user behaviour and ECM on satisfaction. Further, they asserted that attitude and satisfaction play important roles in affecting behaviour intention in each user lifecycle. Therefore, TCT is built by integrating the COGM, TAM and ECM-IS into one model (Liao et al., 2009). It consists of six elements, such as PU, perceived ease of use, confirmation, satisfaction, attitude and CI (Liao et al., 2009). Moreover, the integration of satisfaction and attitude in one framework as the central construct of TCT is the distinctive point of the theory that differs it from the other two models (Liao et al., 2009)

However, this study removes perceived ease of use and confirmation from the model. According to Alkhowaiter (2020), perceived ease of use has the lowest effect on user behavioural intention. More studies also found an insignificant relationship between perceived ease of use and CI (e.g., Cheng et al., 2019; Foroughi et al., 2019; Garrouch, 2021). According to Gilani et al. (2017), perceived ease of use is irrelevant to study in the post-adoption stage since users are already familiar with the service. Hence, this study adopts the simple version of TCT that only consists of satisfaction, attitude and PU.

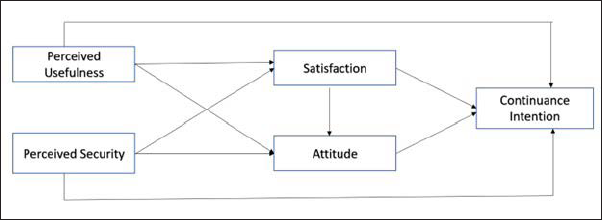

This study proposes that users are willing to continue using the mobile wallet when they perceived it as useful in helping them to complete their tasks and a secured service to store their data and perform financial transactions. Subsequently, the favourable perception of usefulness and security leads them to form satisfaction and a positive attitude toward using the service that influences their decision to continue using the service. Moreover, previous studies have applied TCT to understand users’ CI in various contexts, such as mobile taxi booking apps (Weng et al., 2017), mobile banking (Foroughi et al., 2019), bike-sharing apps (Cheng et al., 2019) and mobile wallets (Abdul-Halim et al., 2021; Gupta et al., 2020b; Khayer & Bao, 2019).

Perceived Usefulness (PU)

PU reflects consumers’ belief in information technology products/services (Susanto et al., 2016). It acts as the determinant of consumers’ intention to adopt the technology (Wang et al., 2020) and reflects the degree of a consumer’s belief that using a particular system will contribute to performance improvement (Davis et al., 1989). Subsequently, in this study, PU is used to examine the degree of mobile wallet users’ belief that using mobile wallets improves their performance in conducting online financial transactions.

PU is one of the forms of users’ expectations regarding the performance of IT products/services (Abdul-Halim et al., 2021; Ogedengbe & Abdul-Talib, 2020; Wei et al., 2021). It is also considered a reflection of the utilitarian aspect of pre-adoption and post-adoption (Talwar et al., 2020). In the context of mobile wallets, users expect that using the mobile wallet will help them in doing their daily tasks and remove the pain of using the conventional method of payment. Accordingly, the confirmation of the user expectation in the pre-adoption stage will result in a favourable view as useful in the post-adoption stage (Liao et al., 2009).

Some studies have been conducted on the effect of PU on satisfaction, attitude and CI. For example, Nguyen et al. (2021) measured the role of PU on satisfaction and CI in the context of mobile banking chatbots and found that users’ perception of the usefulness of the service in helping them complete the task contributed to their satisfaction and CI. Similar findings were also found in other studies with different contexts, such as Li and Fang (2019) in the context of mobile branded apps, Cheng et al. (2019) in bike-sharing apps, Rahi and Abd. Ghani (2019) in internet banking, and Sasongko et al. (2021) in mobile wallets. Moreover, users’ perception of the product/service’s usefulness shapes their attitudes toward the product/service. The relationship has been empirically proven by some researchers (e.g., Abdul-Halim et al., 2021; Chatterjee et al., 2018; Cheng et al., 2019; Oertzen & Odekerken-Schröder, 2019). Hence, this study hypothesizes that PU has a direct relationship with satisfaction, attitude and CI.

Perceived Security (PS)

Perceived security is related to the ability of service providers in creating a secure system for users when using the service. It is defined as users’ perception of the security of financial services in performing financial transactions and maintaining users’ privacy (Kapoor et al., 2020; Patel & Patel, 2018; Sharma et al., 2018).

PS is the result of the cognitive process conducted by the users when evaluating the security procedures of the service (Lim et al., 2019). This process results in the belief of the users that the services have provided a secure system (Gupta et al., 2020b). Subsequently, this positive belief will impact users’ emotional responses and behaviour toward the service (Lim et al., 2019).

Some scholars have investigated satisfaction and CI as the outcomes of PS. For example, Prakash et al. (2021) studied the effect of PS on satisfaction in digital contact tracing apps and found that users’ perception of the app’s security determines their satisfaction with the app. In the context of mobile wallets, PS was also found to affect users’ satisfaction (Gupta et al., 2020b; Kumar et al., 2018; Singh et al., 2017), users’ intention to continue using the service (Abu Salim et al., 2021; Aggarwal & Rahul, 2018; Garrouch, 2021; Merhi et al., 2019; Shao et al., 2019) and attitude (Chawla & Joshi, 2019; Fan et al., 2018). Hence, this study hypothesizes that:

Satisfaction

Oliver (1980) defined satisfaction as the function of expectation and disconfirmation. The process of satisfaction starts with the cognitive evaluation of the adoption experience by comparing the expectation of the performance in the pre-adoption with the actual performance after adoption (Babin & Mitch, 1998; Bagozzi, 1991). Subsequently, satisfaction is gained after users’ expectation is met which lead to the emotional response of the users regarding the future adoption of the product/service (Babin & Mitch, 1998; Bagozzi, 1991). Hence, users’ satisfaction with mobile wallets depends on whether the actual performance of the mobile wallet meets users’ expectations.

According to COGM (Oliver 1980) when users are satisfied with the product/service, they will formulate a favourable attitude toward the product that led them to have a post-purchase intention. Vahdat et al. (2020) stated that satisfaction is the easiest way to reach a favourable attitude toward a brand. Numerous studies have confirmed that satisfaction is the antecedent of attitude (Daragmeh et al., 2021; Foroughi et al., 2019; Khayer & Bao, 2019; Rahi et al., 2021; Raman & Aashish, 2021). Satisfaction also has an immense effect on continuance usage intention (Alghamdi et al., 2018; Cheng et al., 2019; Foroughi et al., 2019; Hepola et al., 2020; Mouakket, 2018; Yang, 2021). This finding shows that satisfied users will develop a favourable attitude that later affects their willingness to continue using the service. Accordingly, this study’s hypothesis is as below:

Attitude

There are different perspectives among scholars related to satisfaction and attitude, some scholars perceive satisfaction and attitude as different constructs, while others view them as similar (Foroughi et al., 2019). Satisfaction relies heavily on experience that lasts for a short time, while attitude is more lasting and goes beyond all preceding experiences (Liao et al., 2009). Moreover, Fishbein and Ajzen (1975) defined attitude as an ‘individual’s positive and negative feeling about performing a target behavior’.

According to Cheng et al. (2019), users who have a favourable attitude toward the product will be more prone to accept and use it again. It indicates that when users have a favourable attitude toward mobile wallets, they will continue using the service. Previous studies have confirmed the effect of attitude on continuance usage intention. For example, Weng et al. (2017) found that attitude has a higher contribution to affecting continuance usage intention of mobile taxi booking app users than perceived risk, satisfaction and PU. Similar findings were found in other research settings, such as mobile banking (Foroughi et al., 2019; Rahi et al., 2021), mobile bike-sharing (Cheng et al., 2019) and mobile wallets (Abdul-Halim et al., 2021; Daragmeh et al., 2021; Khayer & Bao, 2019) as well as mobile payment (Raman & Aashish, 2021). Therefore, this study hypothesizes that:

Research Method

To collect the primary data, this study designed a structured questionnaire consisting of two parts. The first part of the questionnaire is the personal information of the respondent aiming to develop a demographic profile of the respondent. In this part, this study asked about respondents’ age, income, gender, occupation, education and duration of using a mobile wallet. The second part is related to the construct of the model aimed to analyze the relationship between them. The measurement of the construct was built by adapting from previous studies. To measure PU, this study adapted the measurement from Venkatesh and Davis (2000) which consisted of five items. PS consisted of three items, adapted from Garrouch (2021). Satisfaction was measured using three items adapted from Khayer and Bao (2019). Attitude is measured with three items adapted from Schierz et al. (2010). Three items adapted from Bhattacherjee (2001) were used to measure CI. Overall, this study has 17 items to measure the proposed model. The measurement scale used in this study is a 7-point Likert scale anchored from (1) strongly disagree to (7) strongly agree. Subsequently, using a google form, the questionnaire is designed to be easily distributed to the respondent of this study using an online platform such as Whatsapp.

Moreover, the respondent of this study is mobile wallet users selected using the convenience sampling method due to the unidentified population. This study has collected 240 responses which are more than the requirement suggested by Hair Jr et al. (2019). They suggested multiplying the number of items with a number ranging from five to ten to decide the appropriate number of responses required for a study.

Accordingly, the data is analyzed using a partial least square-structural equation model (PLS-SEM). Following the suggestion of Hair et al. (2019) to use PLS-SEM when the study’s objective is to assess an extended version of an established theory. Subsequently, the measurement model and hypothesis testing results were generated from SmartPLS 3.0.

Result

The total respondent in this study is 240 respondents dominated by females (54.6%) with a range of age 18–22 years old (33.8%) followed by 23–27 years old (22.1%). Most respondents have graduated high school (35.8%) and university (32.1%) with occupations mostly college students (37.1%) and civil servants (32.5%). The majority of the respondents have a range of income of less than one million Indonesian Rupiah (27.5%) to more than one million to two million Indonesian Rupiah (14.6%). Moreover, Most of the respondents are long-time users of mobile wallets since they have used the service for more than 3 months (89.2%). Table 1 illustrates the detailed version of the demographic profile of this study’s respondents.

Demographic Profile.

Measurement Model

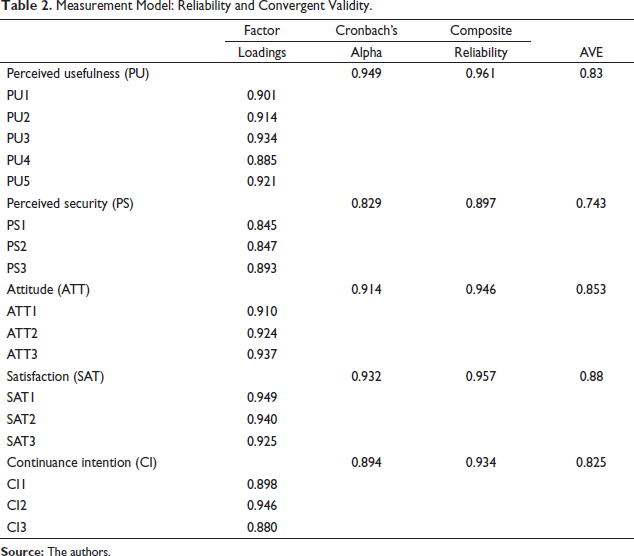

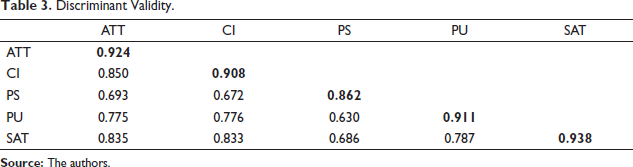

This study follows the suggestion of Hair et al. (2019) on the process of measurement model assessment for reflective construct. The first step is evaluating the indicator loading, the recommended value for indicator loadings is greater than 0.708. Then, evaluating the internal consistency reliability using the composite reliability (CR) value, the CR value above 0.70 is satisfactory. The third, measuring the convergent validity using average variance extracted (AVE). The acceptable value of AVE is higher than 0.5 to indicate 50% of its items variance explained by the constructs. The fourth, measuring discriminant validity which in this study is evaluated using Fornell and Larcker’s (1981) criteria. They stated that to confirm the discriminant validity of the constructs, the square root value of AVE (the diagonal values must be above the correlations among the variable (the off-diagonal values).

Table 2 shows the measurement model related to internal consistency reliability and convergent validity. It shows that factor loading values are greater than 0.708 which means all the instruments have a satisfactory factor loading. The CR value of each construct is more than 0.70 indicating that the constructs have established internal consistency reliability. Finally, all the constructs have an AVE value greater than 0.5 meaning that the convergent validity is confirmed. Table 3 shows the result of discriminant validity. It illustrates that all constructs have a higher square root AVE value (as seen in bold) than the correlations among the variables. It means that the latent variable in this model is distinctive from other variables.

Measurement Model: Reliability and Convergent Validity.

Discriminant Validity.

Structural Model

The result of measurement model has shown a satisfactory result; therefore, it is qualified to evaluate the structural model. Hair et al. (2019) suggested that the evaluation of the structural model should include the coefficient of determination (R2), the predictive accuracy of the path model (Q2), the path coefficients, effect size (f2) and variance inflation factor (VIF).

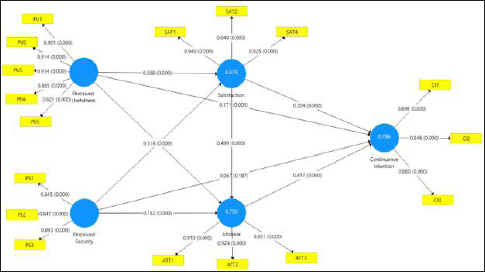

The value of the coefficient of determination (R2) shows the explanatory power of the model (Shmueli & Koppius 2011 cited in Hair et al., 2019). Hair et al. (2019) classified R2 into three groups, 0.75 (substantial), 0.5 (moderate) and 0.25 (weak). As seen in Table 4, this model has 75% explanatory power in explaining attitude, 67.9% in explaining satisfaction and 78.6% in explaining CI. In conclusion, the R2 values of the research model of this study range from moderate to substantial.

Coefficient of Determination (R2) and Predictive Accuracy (Q2).

The predictive accuracy (Q2) value is generated from the blindfolding procedure. Hair et al. (2019) stated that for a model to be meaningful it must have a Q2 value greater than zero. Table 4 shows that the Q2 value of this study is higher than zero which means the research model’s predictive accuracy is confirmed.

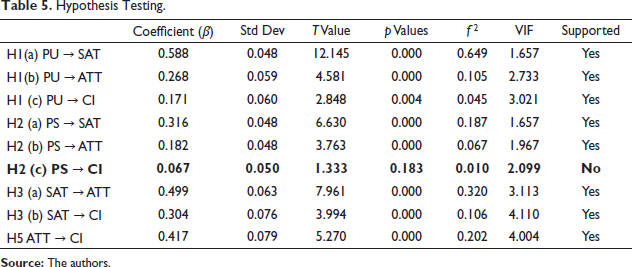

Hypothesis testing involves evaluating the significance of the path coefficient conducted by employing bootstrapping procedure with 5,000 sub-sample. The result shows (see Table 5) that out of nine hypotheses tested in this study, only hypothesis H2 (c) is rejected (as seen in bold), which is a hypothesis on the relationship between PS and continuance intention (CI). The largest coefficient in the eight accepted hypotheses was in H1 (a), the relationship between PU and satisfaction (SAT) (β = 0.588, p < 0.000), and the smallest coefficient was in H1 (c) the relationship between PU and CI (β = 0.171, p < 0.005). To evaluate the presence of bias resulting from collinearity issues in the result, this study conducted a VIF test. Hair et al. (2019) stated that collinearity issues existed when the VIF value is five or above. As seen from Table 5 all hypothesis tests have VIF lower than five indicating the abstain of collinearity issues between the variables.

Hypothesis Testing.

Hair et al. (2019) suggested assessing the effect size (f2) to learn the effect of removing a particular predictor construct from the model on the R2 value of the endogenous constructs. Cohen (1988, as cited in Hair et al., 2019) stated that the f2 value is range from small (0.02), medium (0.15) to large (0.35). Table 5 shows that PU has a small effect size on CI. While the removal of PS on CI does not have any effect on the explanatory power of CI. Regarding the effect size of satisfaction (SAT) and attitude (ATT) on CI, ATT has a large effect on CI while SAT has a medium effect. This indicated that removing ATT from the CI model will affect the explanatory power of CI significantly.

Discussion and Conclusion

This study aims to investigate the determinant factors of CI of mobile wallet users by applying a simplified version of the TCT. It consisted of four main components, such as PU, satisfaction, attitude and CI. The integration of PS into the model aims to enrich the understanding of mobile wallet users’ CI. Although this study used the simplified version of TCT, the results show that it has 78.6% explanatory power in explaining the CI of mobile wallet users. Thus, the model offers a solid theoretical foundation for the research model.

This study examines four predictors of CI, such as PU, PS, satisfaction and attitude. The result of this study found that the determinant factors of CI are PU, satisfaction and attitude. The significant relationship between PU and CI is aligned with previous studies (e.g., Foroughi et al., 2019; Garrouch, 2021; Gilani et al., 2017; Gupta et al., 2020b; Sasongko et al., 2021; Susanto et al., 2016). This shows that when users perceived using the mobile wallet as beneficial, they will continue using the service.

The direct effect of satisfaction on CI is consistent with previous studies (e.g., Alghamdi et al., 2018; Cheng et al., 2019; Daragmeh et al., 2021; Foroughi et al., 2019; Hepola et al., 2020; Mouakket, 2018; Yang, 2021). This finding indicated that users’ satisfaction with the overall performance of mobile wallets influences their willingness to continue using the service. The direct relationship between attitude and CI is also supported by Abdul-Halim et al. (2021) who found that attitude influences the CI of mobile wallet users in Malaysia. Other studies (e.g., Daragmeh et al., 2021; Foroughi et al., 2019; Khayer & Bao, 2019; Rahi et al., 2021; Raman & Aashish, 2021; Weng et al., 2017) also generated similar results. This shows that the favourable attitude of users toward mobile wallets can affect their intention to continue using them. Moreover, among the four predictors, the attitude has the strongest effect on the CI of mobile users reflecting the importance of creating a favourable attitude of users toward the service.

While this study found that PS does not have any direct influence on the continuance use of the mobile wallet. It is supported by Maqableh et al. (2021) who conducted a study on Facebook users. They found that PS has an insignificant relationship with the continued use of Facebook. In a different study context, Lim et al. (2019) found that PS does not affect users’ CI in using mobile fintech payment services.

Regarding the predictor of satisfaction and attitude, this study found that PU and PS play a role in influencing users’ satisfaction and attitude toward the mobile wallet. The finding of PU as the predictor of satisfaction is aligned with the study of Handarkho et al. (2021) who conducted a study in the context of mobile payment. In the context of mobile commerce, Marinković et al. (2020) found that PU has the strongest effect on satisfaction. Similar findings are found in the study of Nguyen et al. (2021), Li and Fang (2019), Gilani et al. (2017), Rahi et al. (2021), as well as Singh et al. (2017). Moreover, the finding on the relationship between PU and attitude is confirmed by Abdul-Halim et al. (2021), Cheng et al. (2019) and Gilani et al. (2017). This shows that when mobile wallet service providers have provided services that benefit the users, users will be satisfied and have a positive attitude toward the service.

Previous studies have confirmed the finding of this study on the relationship between PS and satisfaction. For example, Prakash et al. (2021) found that PS influences users’ satisfaction with the digital tracing app. Abu Salim et al. (2021), Aggarwal and Rahul (2018), as well as Kumar et al. (2018), are some previous studies that supported the finding. This indicated that mobile wallet users will be satisfied when the mobile wallet security measures met their expectations. It also showed that to influence users’ continued use of the mobile wallet, the mobile wallet must have a security system that met the users’ expectations.

Moreover, this study also found that a favourable PS contributes to creating a favourable attitude toward mobile wallet services. This shows that although in the pre-adoption users have security concerns toward the service, the concern is diminished after the users experience the service and learn that the providers have provided several security measures to protect users’ financial transactions and personal data. Accordingly, this effect on their post-adoption attitude resulted in them having a positive attitude toward the service. Lim et al. (2019) stated that for a mobile wallet to be accepted positively by users it should provide a secure system for users to perform their financial transactions. This finding is supported by Chawla and Joshi (2019) who found that PS is the antecedent of the attitude of mobile wallet users in India.

This study also investigated the influence of satisfaction on attitude and found that satisfaction influences attitude. This finding is aligned with the COGM (Oliver, 1980) which stated satisfaction is the predictor of attitude. It is also in line with (Foroughi et al., 2019) and (Rahi et al., 2021). This indicated that to create a favourable attitude of users on the mobile wallet, the users first must satisfy with the overall performance of the service.

Implication

Theoretical

This study provides some contribution to the Information System study. First, it enriched the literature by focusing on post-adoption user behaviours and applied a simplified version of the TCT. Based on this study’s result, the integration of PS into the model resulted in high explanatory power (i.e., 78.6%). Proving that the model is applicable to understanding mobile users’ CI. Second, PS is found to have no direct relationship with CI, but it has a direct relationship with satisfaction and attitude. This indicates that PS is irrelevant when studying users’ CI of using mobile wallets but significantly relevant in studying users’ satisfaction and attitude toward using the mobile wallet. Finally, this study confirmed that PU, satisfaction and attitude are imperative to influence users’ CI with attitude as the most important component among the three. It also confirmed that satisfaction and attitude are two distinct constructs where satisfaction plays as the predictor of attitude.

Practical

A mobile wallet is a financial innovation where users’ acceptance is imperative to influence users’ intention to use the service. This study has identified that attitude plays an important role in influencing users’ CI to use mobile. Therefore, improving the attitude of mobile wallet users to the service is imperative. Based on the empirical evidence of this study, users’ attitude is influenced by PU and PS. Therefore, it is suggested to focus on providing features that are beneficial for the users and improve the service’s security measures. The PU of mobile wallets can be achieved in several ways, first, by increasing the number of merchants, both online and physical merchants. Second, providing a peers-to-peers payment that not only connected users to the bank account but also other mobile wallet service providers. Finally, adding a feature where users can make an automatic payment for their monthly bills may enhance users’ experience in using the service. Regarding the PS, the mobile wallet service providers must handle it with care, if the services have many layers of protection, it may affect users’ experience. Moreover, not only does perceive usefulness and security affect attitude but it is also found to influence users’ satisfaction. This study found that user satisfaction leads to users’ CI using mobile wallets. The finding highlights the importance of creating beneficial features and mobile wallet security systems to influence users’ CI.

Limitation and Future Studies

Despite having a contribution theoretically and practically, this study has some limitations. First, most respondents are long-term users of mobile wallets, so the finding of this study represents the view of long-term users. Therefore, for future studies, it is suggested to examine the determinant factors of CI for short-term users (i.e., less than 3 months). Second, this study does not hypothesize mediation and moderator effects. Therefore, for future studies, it is suggested to investigate the mediation role of satisfaction and attitude in the relationship between users’ belief and their intention to continue using the mobile wallet. Future research should investigate the moderation effects of income, gender and duration of usage. Finally, this study introduces a simplified version of TCT with the integration of PS. Accordingly, integrating other constructs into the model, such as trust, perceived quality, or perceived value could generate an interesting outcome.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The work is supported by Universitas Syiah Kuala (Grant number: 211/UN.1.2.1/PT.01.03/PNBP/2022).