Abstract

The study examines the moderating and mediating effect of corporate social responsibility (CSR) disclosure and CSR expenditure on the association between listed firms’ financial performance and gender diversity. There are 80 listed firms with 800 firm-year observations from 2010 to 2019 that qualified for the study using the Indian stock market. The first finding shows a negative association between financial leverage and gender diversity. The second finding shows that the implementation of CSR disclosure hurts the improvement of gender diversity. The third finding shows that CSR expenditure improves gender diversity of listed firms in an emerging market. The fouth finding shows that CSR expenditure positively mediates the negative association between financial leverage and gender diversity. The fifth finding shows that CSR disclosure does not mediate the association between financial performance (return on assets, price to book ratio and financial leverage). The sixth finding shows that CSR expenditure negatively moderates the negative association between return on assets and gender diversity.

Introduction

The purpose of this study is to examine the moderating and mediating effect of corporate social responsibility (CSR) disclosure and expenditure on the association between financial performance and gender diversity. Very few studies have examined gender diversity from the general workforce perspective (Pedrini, 2018). The enactment and acceptance of sustainable development goals in 2015 (Sustainable Development Goals, 2019) allows firms to contribute to the sustainable development agenda by addressing minority issues, including gender diversity. The transferability of this agenda into a local firm perspective makes CSR and sustainability meaningful (Mun & Jung, 2018). In addition, an understanding and implementation of gender diversity gives a firm an implied advantage of having a wide range of resources and skills which has a competitive edge over other non-practicing firms in the industry (Sahoo & Lenka, 2016). The study uses the Indian context as the testing ground because the World Bank and the United Nations data on India show a weak growth of women employment (Annette, 2018). However, firms are making the efforts for improving gender diversity by communicating through CSR disclosure and incurring a continuous expenditure in CSR activities (Usman & Amran, 2015). The effectiveness of CSR disclosure and CSR expenditure to promote gender diversity lacks in-depth study. On the basis of the points mentioned above, this study uses the social role theory to examine the moderating and mediating effect of CSR disclosure and expenditure between financial performance and gender diversity of listed firms in India.

There are studies on gender diversity and financial performance with mixed results from both developed and developing economies (Chieh Hsu & Lawler, 2019; Chih-shun Hsu et al., 2016; D’Amato, 2017; Darmadi, 2013; Kravitz, 2003; Mínguez-Vera & Campbell, 2007; Solakoglu & Demir, 2016). Likewise, there are associations between gender diversity and CSR disclosure (Grosser & Moon, 2005; Lauwo, 2018; Setó-Pamies, 2015; Yasser et al., 2017).

This study provides a link between gender diversity and firm performance, and gender diversity and CSR (Chadwick & Dawson, 2018; Elsharkawy et al., 2018; Grosser & Moon, 2005; Jadiyappa, et al., 2019; Setó-Pamies, 2015). However, there are no studies that examined financial performance as factors on gender diversity. Also, no studies have examined the moderating and mediating effect of CSR disclosure and CSR expenditure between financial performance and gender diversity. Accordingly, this study investigates the moderating and mediating effect of CSR disclosure and expenditure on the association between financial performance and gender diversity. There are 80 listed firms (800 firm-year observations) out of 131 firms on the India stock market from 2010 to 2019 that practise sustainability reporting and have information on gender diversity.

The study contributes to the existing knowledge in two ways. First, our study findings extend previous studies on board gender diversity and financial performance (Chieh Hsu & Lawler, 2019; D’Amato, 2017) by investigating the financial performance and gender diversity of all employment levels in the firm. Second, our study uses CSR proxy by either CSR disclosure or CSR expenditure as mediating and moderating variables to examine the association between financial performance and gender diversity.

Literature Review and Hypothesis Development

Theory

Social role theory explains why there is a high disparity in women’s employment in the workplace in emerging economies. Social role theory is a social psychology theory that refers to gender disparities and social behavioural similarities. Thus, the actions of men and women typically promote and perpetuate the division of labour through socialization and the creation of gender roles leading to social roles (Eagly, 1978; Eagly & Wood, 2016). Similarly, the community and the society stereotype women to be the weaker vessel which also cause the high disparity of women employment in the workplace (Eagly & Wood, 2012). The importance of social role theory application mentioned in many gender studies (Franke et al., 1997; Harrison & Lynch, 2005) causes this study to examine the moderating and mediating effect of CSR expenditure and CSR disclosure between financial performance and gender diversity in an emerging economy.

Gender Diversity

There are studies on gender diversity and financial performance with mixed results from both developed and developing economies (Chieh Hsu & Lawler, 2019; Chih-shun Hsu et al., 2016; D’Amato, 2017; Darmadi, 2013; Kravitz, 2003; Mínguez-Vera & Campbell, 2007; Solakoglu & Demir, 2016). Some of the studies showed that gender diversity did not influence firm’s performance (Unite et al., 2019) and included is a study in the Indian context which showed no association between board gender diversity and financial and social performance (Sanan, 2016). Nonetheless, most of the studies concentrate on middle-management, top-management diversity, female CEO or women on board composition (Chadwick & Dawson, 2018; Elsharkawy et al., 2018; Jadiyappa et al., 2019) but with little reference to the magnitude effect of gender diversity in all levels of employment (Pedrini, 2018). There are, however, some limited studies that examined women employment and performance (Kravitz, 2003; Tsou & Yang, 2019). For example, in a US study, Kravitz (2003) showed that 49% of the total workforce was female and the findings from the study showed a positive association between gender diversity and firm performance in retail, wholesale and service industries (Kravitz, 2003). Another study in China investigated the effect of gender workforce composition on firm productivity of Chinese manufacturing firms. The findings showed that the higher the female workers, the lower the productivity contribution (Tsou & Yang, 2019). However, the reverse, where factors such as financial performance can cause an increase or decrease in the gender diversity of the entire workforce which is consistent with the advocators of sustainable development goals (Sustainable Development Goals, 2019) lacks scholar attention.

Hypotheses Development

Financial Performance

Evidence from previous studies shows a positive correlation between financial performance and gender diversity in a Chinese study (Sial et al., 2018), but statistically testing the effect of financial performance on the gender diversity of the whole workforce is lacking. Also, there are no current studies in an emerging economy context. The study’s findings suggest that female directors have a significantly larger positive impact in high-performing firms relative to low-performing firms (Conyon & He, 2017). India’s context is not left out, and studies showed that women directors have a positive and statistically significant association with firm performance (Jyothi & Mangalagiri, 2019). Still, the authors did not examine the reverse, creating a research gap for this study in an emerging economy context that examines gender diversity for the whole firm, consistent with sustainable development goals (Sustainable Development Goals, 2019). The role of social role theory has, in many previous studies, contributed in explaining the increase and decrease in gender diversity (Franke et al., 1997; Harrison & Lynch, 2005). Even though different studies attribute some factors responsible for the increase or decrease in gender diversity, there are no studies that examined the effect of financial performance (return on assets (ROA), price to book ratio (PBR) and financial leverage (FL)) on gender diversity. We employ different performance measures to observe how other measures impact gender diversity (Solakoglu & Demir, 2016). Given that there is a positive correlation between financial performance and gender diversity (Conyon & He, 2017), we perceive that financial performance will positively influence gender diversity. Therefore, we propose a conditional statement which states that:

H1a: ROA has a positive and statistically significant association with gender diversity of listed firms in an emerging economy H1b: PBR has a positive and statistically significant association with gender diversity of listed firms in an emerging economy H1c: FL has a positive and statistically significant association with gender diversity of listed firms in an emerging economy

Moderating and Mediating Effect of CSR Disclosure and Expenditure

Firms use CSR disclosure to communicate social performance to shareholders and stakeholders and among what is communicated is gender diversity (Usman & Amran, 2015). The impact of CSR disclosure to communicate gender diversity effectively to stakeholders remains fluid. Sometimes CSR cannot address different class conflicts, thereby neglecting some women in the pursuant CSR strategies in a capitalist market (Lauwo, 2018). Nonetheless, CSR is currently the best method to capture gender diversity (Lauwo, 2018). A literature review also showed a positive correlation between financial performance and gender diversity (Conyon & He, 2017). Gender diversity is a sustainable development goal agender (Sustainable Development Goals, 2019) pursued by governments and firms. Firms contribute by making it a corporate strategy reflected in its integrated report (Adams et al., 2016). Although CSR and gender diversity correlate, the moderating and mediating effect of CSR disclosure on gender diversity is yet to be examined by researchers. In a study, we found that CSR managers only push for gender diversity in upper management (Mun & Jung, 2018), leaving lower management and the entire women workforce deficit. We study this work further and examine all levels of women in employment. Evidence from the literature showed a positive association between gender diversity and CSR disclosure (Amorelli & García-Sánchez, 2020). Still, the reverse has received no attention, especially in the context of India. Previous studies also examined the mediating effect of CSR disclosure on the association between corporate governance and financial performance (Machdar, 2019). Therefore, we perceive in this study that CSR disclosure positively influences gender diversity, given that a firm has an excellent financial position. We expect the mediating and moderating CSR disclosure variable to strengthen the relationship between financial performance and gender diversity to improve women employment in the workplace. Therefore, we propose the hypotheses which state:

H2a: CSR disclosure moderates the association between financial performance and women employment. H2b: CSR disclosure mediates the association between financial performance and women employment H2c: CSR disclosure improves gender diversity of listed firms in an emerging market

CSR expenditure is the amount a firm commits to undertake CSR activities and the total cost captured in firms’ sustainability report (Geetika & Shukla, 2017; Nakamura, 2015). Previous CSR investment and expenditure studies covered an association with economic performance (Nakamura, 2015), expected dividends of stockholders (Rakotomavo, 2012), and financial performance (Malik et al., 2019). However, no current studies examined CSR expenditure as a proxy to CSR on gender diversity. Even though previous studies examined gender diversity and CSR disclosure (Setó-Pamies, 2015), no researchers have examined CSR investment on gender diversity. Therefore, we take CSR research further and examine first CSR expenditure on gender diversity and second examine the moderating and mediating effect of CSR expenditure between financial performance and gender diversity. Therefore, we propose the hypotheses which state:

H3a: CSR expenditure moderates the association between financial performance and gender diversity H3b: CSR expenditure mediates the association between financial performance and gender diversity H3c: CSR expenditure improves gender diversity of listed firms in the emerging markets

Research Design and Methodology

Data and Sample

The study based on 80 listed firms in Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) from 2010 to 2019, falls in the criteria of voluntary and mandatory reporting on CSR in sustainability reports. The companies in BSE and NSE reflect the current availability of data from emerging economies on the firm. The study period is between 2010 and 2019 because of the voluntary and mandatory CSR law passed in 2009 and 2013, respectively (Ministry of Corporate Affairs, 2013). Green Clean organization and Sustainability outlook, reports on all firms in India that submit sustainability reports (BRR and Sustainability Report Tracker for Listed Companies, 2017; Green Clean Guide, 2011). The details of the firms under study are in Table A1. Data are from each firm web page. Specific financial and non-financial information is from chairman reports, corporate governance reports, sustainability reports and stand-alone audited financial statements ending 31 March every year.

Model Specification

To examine the financial performance, CSR (CSR disclosure and CSR expenditure) and gender diversity, we specify the following economic models:

Mediating Regression

This study applies a panel regression to test the proposed hypotheses. CSR disclosure and CSR expenditure can be a mediator variable if it meets the conditions specified by Baron and Kenny (1986). First, a significant association between financial performance and gender diversity; second, a significant association between CSR (CSR disclosure and expenditure) and gender diversity; and finally, a significant association between financial performance and CSR. The testing of the mediating variable effect using Baron and Kenny (1986) is consistent with previous studies (Xie et al., 2019).

Hierarchical Regression Model

The hierarchical regression model is used in this study and is consistent with existing studies (Xie et al., 2017, 2019). CSR represents CSR disclosure and CSR expenditure in this study. A variable is a moderating variable when the interactive variable of ‘CSR × financial performance’ is significant (Baron & Kenny, 1986) is associated with the dependent variable of gender diversity. Moderating variable strengthens the association between two variables (Baron & Kenny, 1986) in a study. Hence we test to see if the moderating variable of CSR enhances the relationship between financial performance and gender diversity. The rationale for introducing the moderating variable is because there is no variable moderating effect of CSR (CSR disclosure and CSR expenditure). Data analysis process includes the following steps. In the first step, we enter the independent variable, financial performance. In the second step, we add the moderating variable of CSR (CSR disclosure and CSR expenditure). Finally, we add the interactive variable of combined CSR and financial performance.

The subscript i represent the cross-section of the firm and t represents the period for equations.

Dependent Variable

GDIVit defines the dependent variable, which is the ratio of women in employment to the total workforce. Different studies have measured gender diversity using total women on the board as a percentage of overall board size (Amorelli & García-Sánchez, 2020; Mun & Jung, 2018) and this study expands the ratio to cover the entire women in employment.

Independent Variable

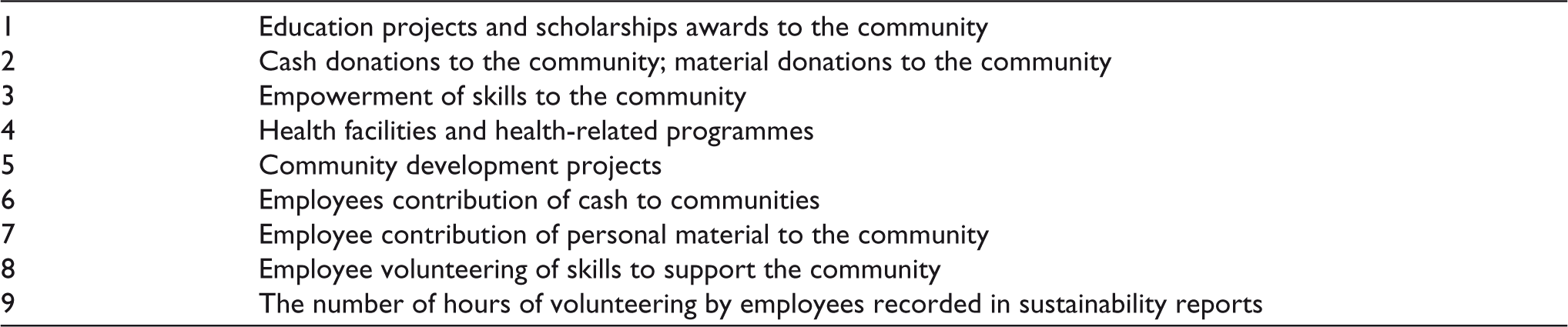

CSRit is an independent variable in this study made up of CSR disclosure and CSR expenditure. CSR disclosure is a proxy for social performance which covers nine variables, and each is assigned one if present and zero otherwise. The computed score of each firm equals the maximum possible outcome divided by the total count of all categories. The measurement approach is consistent with other research studies (Kamel & Shahwan, 2014; Shahwan, 2015; Shahwan & Hassan, 2013). The details of the variables are shown in Table A2. CSR expenditure is the amount a firm commits to undertake CSR activities and the total cost captured in the sustainability report of firms (Geetika & Shukla, 2017; Nakamura, 2015). The CSR expenditure converted into a natural logarithm to remove outliners. Perfit in this study covers ROA, PBR and FL. PBL measures a firm’s market capitalization to its book value (Foye & Mramor, 2016). It is calculated as PBL is equals to current share price divided by book value per share (assets-liabilities/total shares outstanding). FL measures the ratio of total liabilities to total assets which measures the leverage of the firm (Clarkson et al., 2008; Cormier et al., 2011; Mishra & Suar, 2010). ROA is the ratio of natural logarithms of net income over total assets. The choice of ROA affects the firm ability to replace its investment in fixed assets (Graves & Waddock, 1994; Qui et al., 2016).

Control Variables

CTRL it represents the control variables, which include firm size, the board size, independent directors, growth sales and year effect. Board size is the total of directors serving on the board and mostly shows the positive significance and independent directors are outside directors on the board (Inoue & Lee, 2011). Firm size measures a firm’s capacity to undertake CSR activities and calculated as the natural logarithm of the firm’s total assets (Clarkson et al., 2008; Mishra & Suar, 2010). Sales growth is the natural logarithm of sales of the current period to the previous period multiplied by 100%. It is included as a control variable to reduce the impact of substantial sales revenue of firms (Luo & Bhattacharya, 2006). Year indicator dummy represents the timing effect and uses a dummy variable in the model to control the year effect (Qui et al., 2016).

Methodology

We applied descriptive statistics, hierarchical regression and mediating regression models to test H1–H3 of the study, and analysed with Stata 15.0. The study uses a panel regression test to determine the choice between pooled ordinary least squares (OLS), fixed effect (FE) and random effect.

Panel Regression Test

A poolability test (pooled OLS versus fixed effect) and Hausman test are used to determine the model appropriateness between FE and pooled OLS regression and also between random effects (RE) and FEs (Baltagi, 2005; Hausman, 1978). A null hypothesis is where pooled OLS is appropriate and p-values are not significant at a 1% level of significance. The poolability test using F-test under gender diversity shows F(79,713) = 260.22 and is significant at 1% (p-value = 0.000), hence pooled OLS rejected. Using a Hausman test to choose between FE and RE, the p-value is 0.015, which is significant. Therefore, FE is appropriate for gender diversity. The poolability test using F-test under CSR expenditure and CSR disclosure shows F(79,713) = 13.19 and is significant at 1% (p-value = 0.000), hence pooled OLS rejected. Using a Hausman test to choose between FE and RE, the p-value is 0.000, which is significant. Therefore, FE is appropriate for CSR expenditure and disclosure.

Empirical Results and Discussions

The empirical analysis of the study presented in Tables 1–6. The next section shows descriptive statistics and correlation analysis, while subsequent section shows the regression results of the study.

Descriptive Statistics and Correlation Matrix

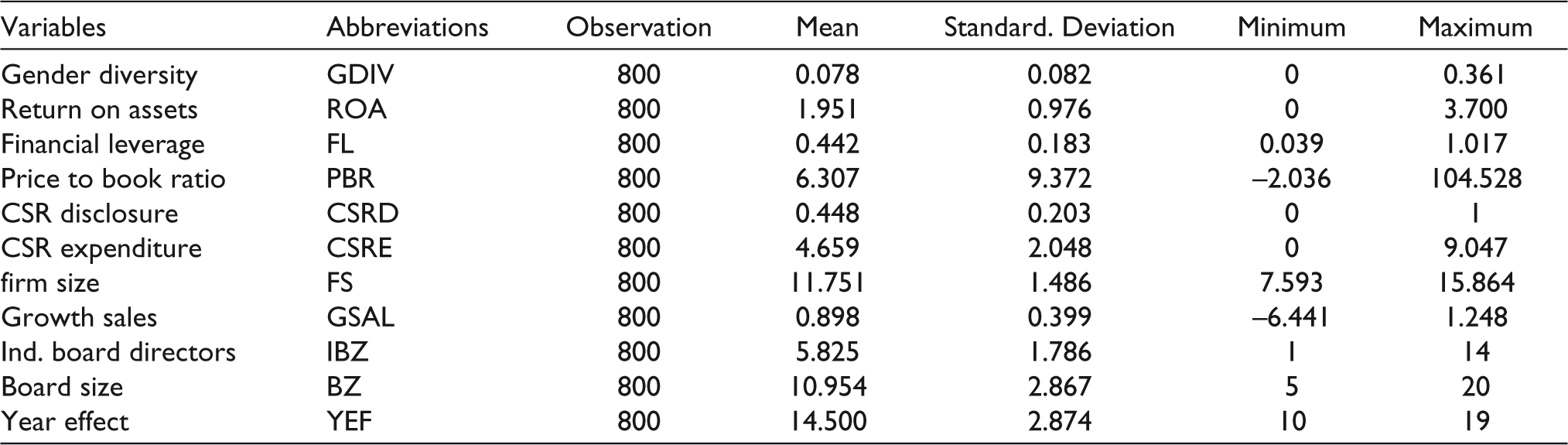

Table 1 presents the descriptive statistics of variables. Gender diversity is the ratio of women employees to the total workforce of a firm. Gender diversity has an average mean of 0.078, which shows that 7.8% of the entire workforce are women covering all employment levels in the firms. The financial performance measures ROA, PBL and FL. The average mean of ROA is 1.951 and deviates from mean by 50.02% and has uneven distribution. PBL average mean is 6.307, and the mean deviation is high, with an uneven distribution among the firms. FL has an average mean of 0.442, which indicates that 44.2% of the capital structure is financed by debt. CSR expenditure has a mean of 4.659 and standard deviation of 2.048 with a deviation of 43.96%. It is an indication that CSR expenditure is not even among firms under study. CSR disclosure has an average mean of 0.448, representing 44.8% of the firms under study display a form of disclosure to stakeholders and shareholders.

Descriptive Statistics

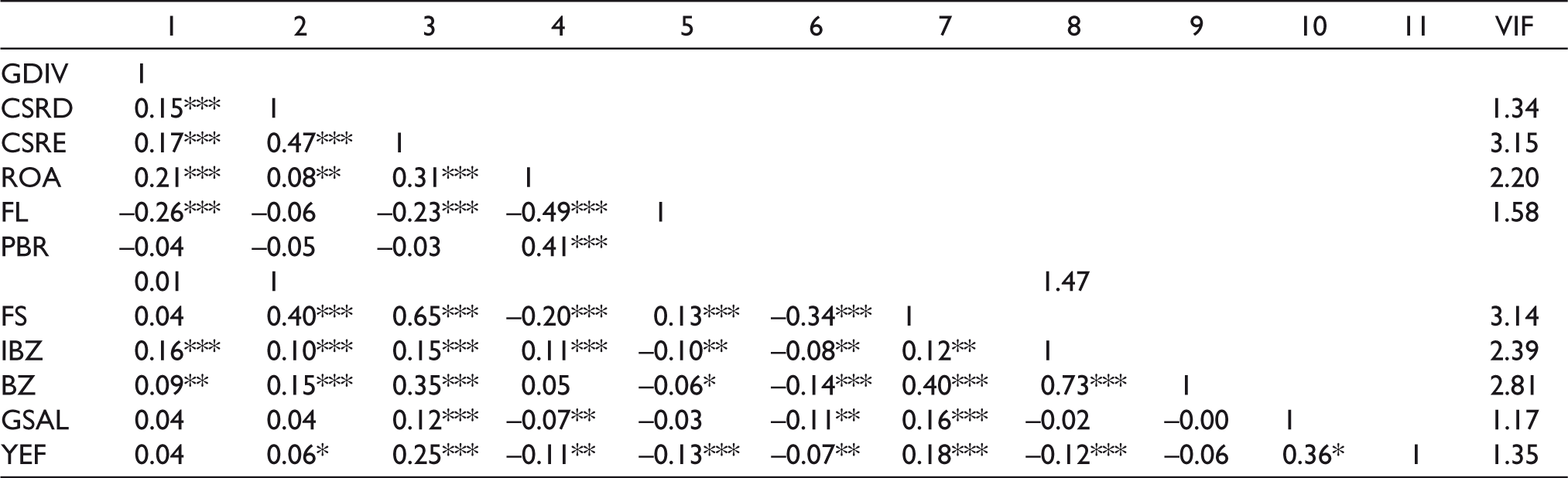

Table 2 shows the correlation matrix of the variables under study. The results show that gender diversity has a positive and weak correlation with ROA but negatively correlates with PBL and FL. Gender diversity also has a positive and weak correlation with CSR (CSR disclosure and CSR expenditure). The largest significant coefficient among the variables is 0.73, and is below the threshold of 0.80, creating no multicollinearity (Dougherty, 2017). In addition, multicollinearity test using a variance inflation factor showed no problem of multicollinearity.

Correlation Matrix and Variance Inflation Factor

Regression Results

Panel Regression

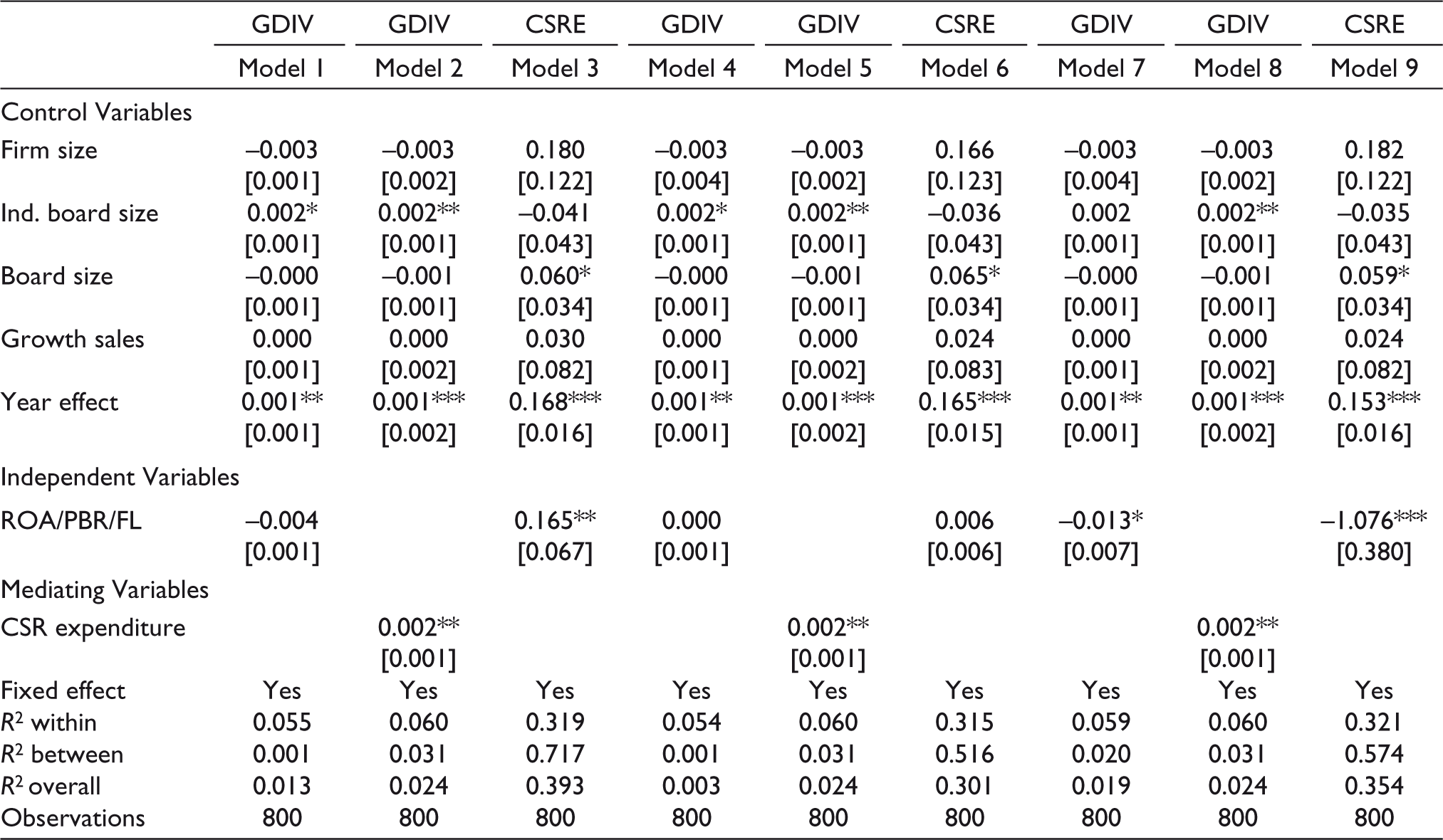

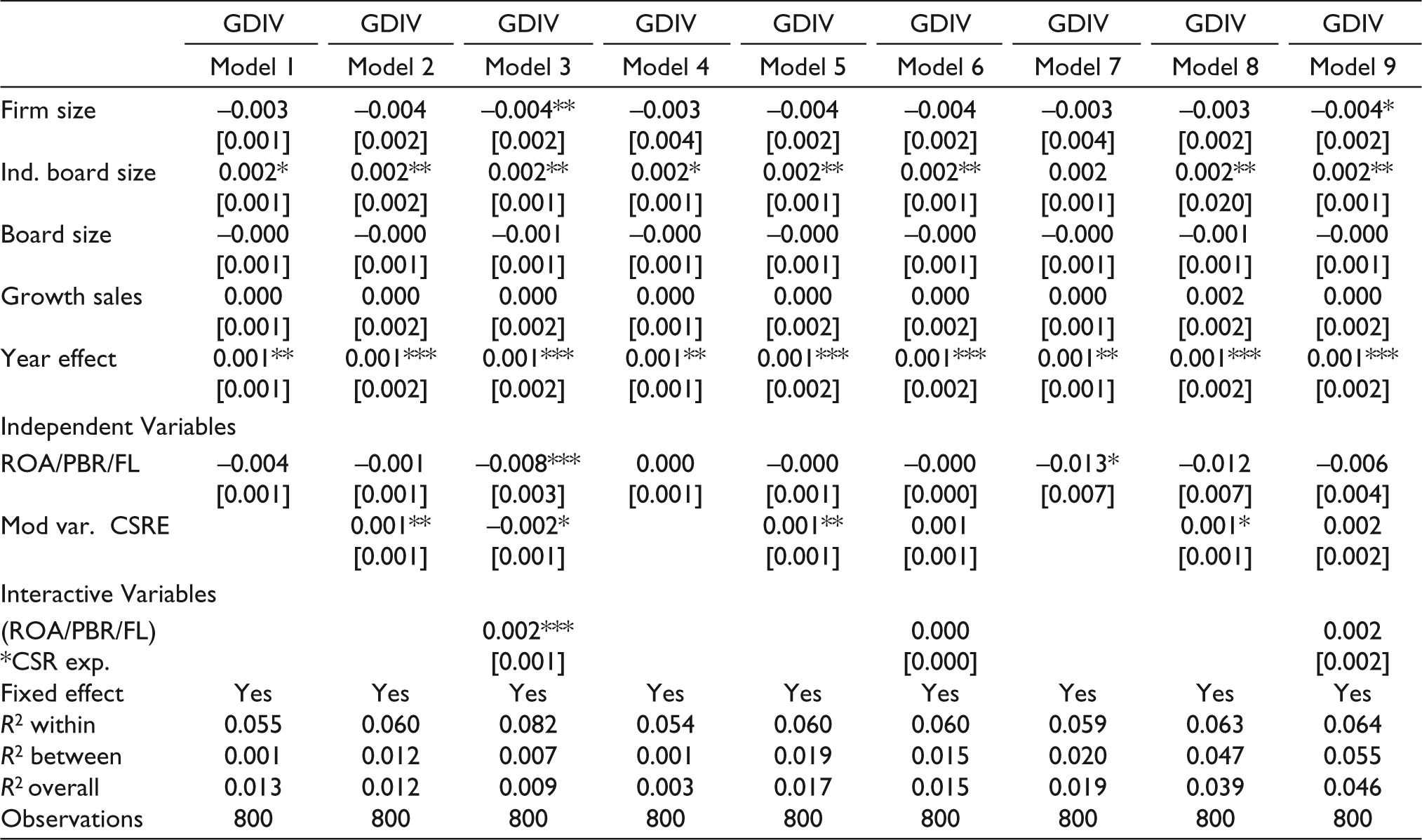

H1a, H1b and H1c state that financial performance (ROA, PBL and FL) has a positive and statistically significant association with gender diversity of listed firms in an emerging economy. Model 1 from Table 3 shows no association between ROA and gender diversity. Model 4 also shows no association between PBL and gender diversity. However, Model 7 shows a negative, statistically significant association between FL and gender diversity. Thus, FL (β = –1.076***) has a 1% (***) level of significance with gender diversity. H1c is supported, but there are no previous studies on financial performance and gender diversity to compare and contrast. However, previous studies showed a positive correlation between financial performance and gender diversity (Conyon & He, 2017). The FL ratio indicates that the firm uses debt to finance its assets and operations, which has risk consequences. Similarly, through social role theory, authors also argue that women engagement has associated risk (Eagly & Wood, 2012). The negative association suggests to investors and shareholders that the firm’s capital structure is significant to influence women employment. Therefore, an increase in leverage reduces women employment by firms in India because it is perceived that women contribution is weak to generate enough revenue (Tsou & Yang, 2019; Unite et al., 2019) to meet the firm’s interest payments and to finance firm operations and assets.

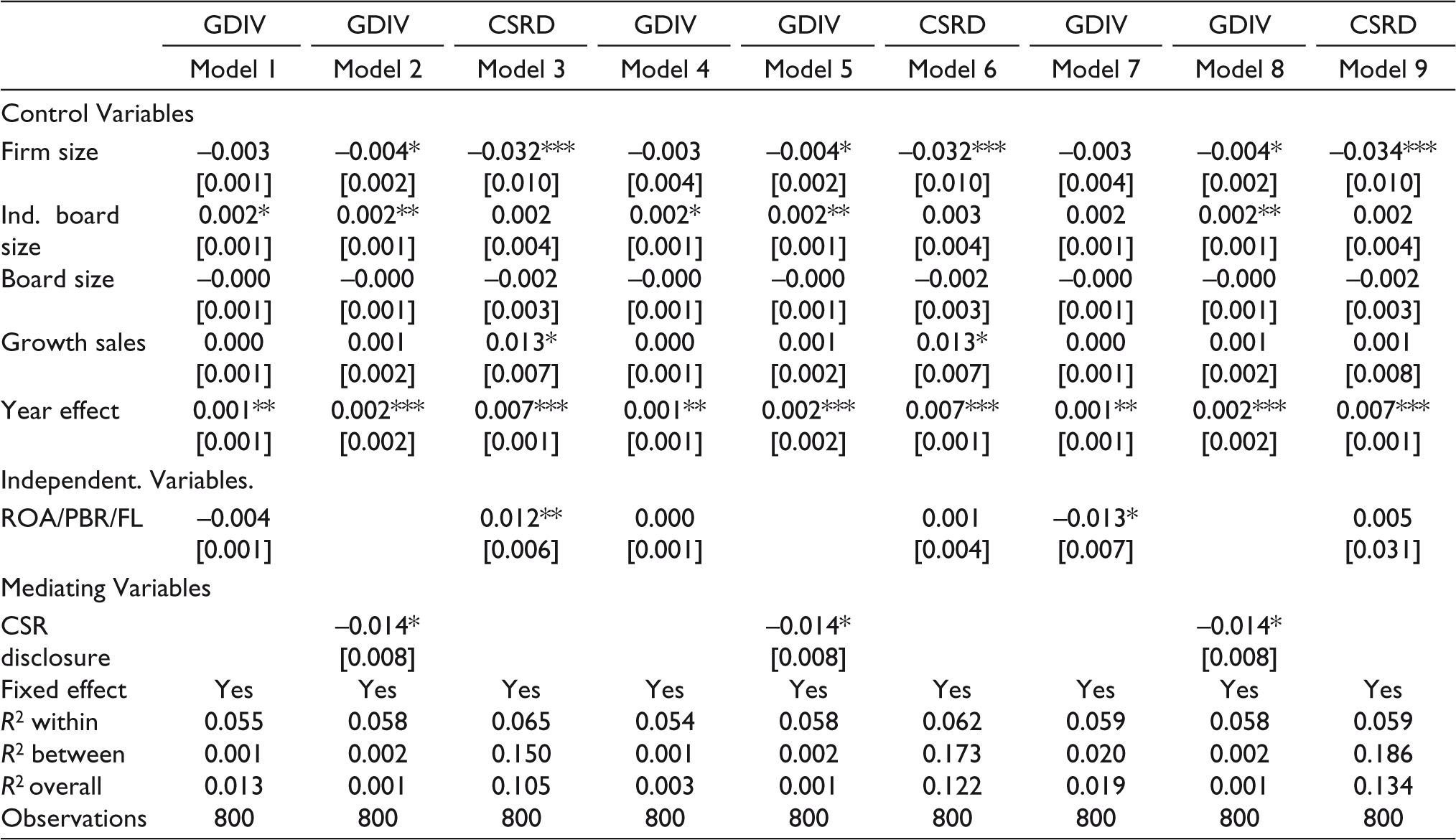

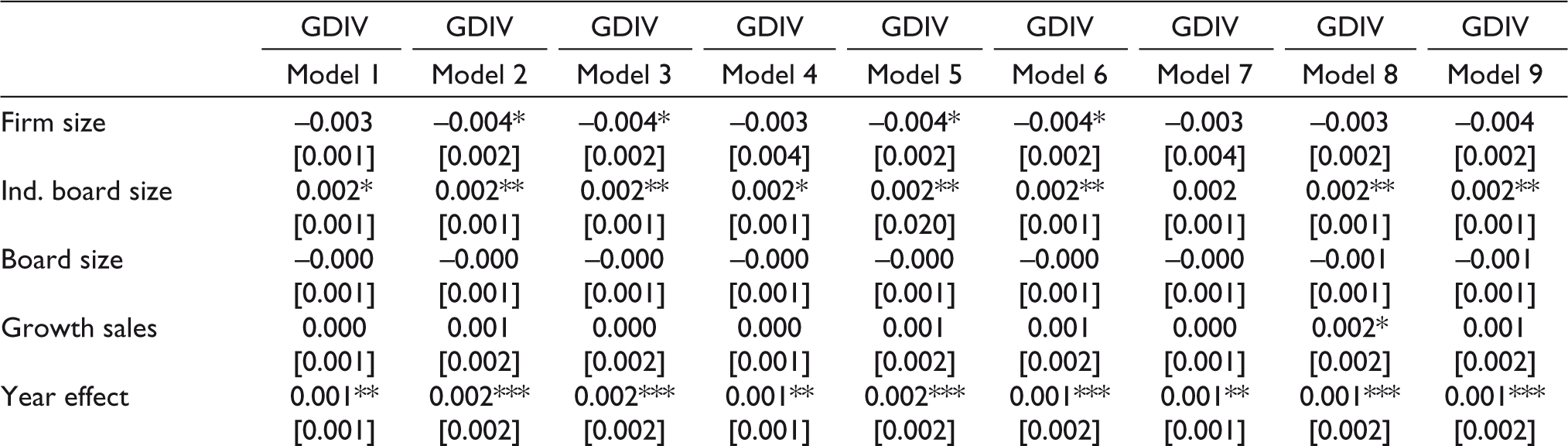

H2c states that CSR disclosure improves gender diversity of listed firms in an emerging market. Model 2 from Table 4 shows a negative statistically significant association between CSR disclosure and gender diversity. Thus, CSR disclosure (β = –0.014*) has a 10% (*) level of significance with gender diversity. H2c is supported, but it is perceived that CSR disclosure does not address different class of women in employment (Lauwo, 2018), causing dissatisfaction in users of the sustainability reports. Too much emphasis placed on only the gender diversity of top management and board size. The social role theory of division among male and female seems to have relevance in the gender diversity of the entire workforce compared to the board of directors who are decision-makers. The proportion of women in the general workforce are more than women in top management, but there is a low production contribution from general women employment (Tsou & Yang, 2019). The perception of weak contribution may be why the low relevance of total gender diversity to sustainability reports. The neglect of lower levels of women employment is supported by the argument that CSR managers only push for gender diversity in upper management (Mun & Jung, 2018), leaving lower management and women workforce deficits. H3c states that CSR expenditure improves gender diversity of listed firms in an emerging market. Model 2 from Table 3 shows a positive, statistically significant association between CSR expenditure and gender diversity. Thus, CSR expenditure (β = 0.002**) has a 5% level of significance with gender diversity, but the beta coefficient is weak. H3c is supported, and we see that an expenditure item on gender diversity communicates better than disclosing the levels of gender diversity in a firm which is inconsistent with the actions of CSR managers (Mun & Jung, 2018).

Mediating Effect of CSR Expenditure

Mediating Variable Regression

Table 3 shows the regression results of the CSR expenditure as a mediating variable. The results of Model 8 in Table 3 show that CSR expenditure is positively related to gender diversity and positively mediates the negative association between FL and gender diversity. Hence, H3b is supported. It is suggested that there is a complementary effect from a firm that spends money on CSR activities in the relationship between FL and gender diversity than firms that do not have expenditure item of CSR activities in its annual reports. Thus, CSR expenditure mitigates the negative association between FL and gender diversity. Table 4 shows the regression results of the CSR disclosure as a mediating variable. However, the CSR disclosure only meets two out of the three conditions mentioned by Baron and Kenny (1986). Therefore, H2b is not supported as a mediating variable. We can deduce that CSR disclosure does not improve the relationship between financial performance (ROA, PBL and FL) and gender diversity of listed firms in India. Therefore, it can be argued that CSR disclosure is defective in communicating the actions of firms in the area of gender diversity of the entire workforce (Mun & Jung, 2018).

Mediating Effect of CSR Disclosure

Hierarchical Regression Results

The results align with the conditions for a moderating variable predictor (Baron & Kenny, 1986). Table 5 shows that CSR expenditure hurts the relationship between ROA and gender diversity. Thus, H3a is supported because CSR expenditure negatively moderates the negative association between ROA and gender diversity. The quest of a firm to achieve asset recovery competes with women’s employment and the spending on CSR worsens the situation, making firms with CSR objectives less attractive than non-CSR firms towards the improvement in gender diversity. Therefore, the assumption and argument that a firm that undertakes CSR activities helps increase gender diversity is not supported in this study. It rather confirms CSR concept is not appropriate to address gender diversity because CSR cannot resolve different class conflicts, thereby neglecting some women in the pursuant CSR strategies in a capitalist market (Lauwo, 2018). Table 6 also shows that CSR disclosure moderates the association between PBR and gender diversity. Therefore, H2b is supported because CSR disclosure negatively moderates the positive and statistically significant association between PBR and gender diversity. We see that firms with improved market capitalization are perceived to employ women in an Indian context, and CSR disclosure is significant to influence the relationship.

Hierarchical Regression: Financial Performance, CSR Expenditure and Gender Diversity

Hierarchical Regression: Financial Performance, CSR Disclosure and Gender Diversity

Conclusion

The purpose of this study is to examine the moderating and mediating effect of CSR disclosure and expenditure on the association between financial performance and gender diversity. Data over the period allow this study to apply descriptive statistics, panel regression, hierarchical regression and mediating variable regression for the period 2010–2019 using the Indian stock market as a testing ground. CSR is proxy by CSR disclosure and CSR expenditure, and results from the study shows a positive and moderate correlation between CSR disclosure and CSR expenditure. The first finding shows a negative association between FL and gender diversity. The negative association suggests investors and shareholders that the firm’s capital structure is significant to influence women employment. Therefore, an increase in leverage reduces women’s employment by firms in India because it is perceived that women’s contribution is weak to generate enough revenue to meet the firm’s interest payments and finance firm’s operations and assets. The second finding shows that the implementation of CSR disclosure hurts the improvement of gender diversity. CSR disclosure does not address different class of women in employment (Lauwo, 2018), causing dissatisfaction in users of the sustainability reports. The social role theory of division among male and female seems to have relevance in the gender diversity of the entire workforce compared to the board gender diversity who are decision-makers. The proportion of women in the general workforce are more than women in top management and the low production contribution from general women employment (Tsou & Yang, 2019) may be the reasons for low relevance of total gender diversity to users of sustainability reports. The third finding shows that CSR expenditure improves gender diversity of listed firms in an emerging market. It is suggested that an expenditure item on gender diversity communicates better than disclosing the levels of gender diversity in a firm which contravenes the actions of CSR managers (Mun & Jung, 2018). The foruth finding shows that CSR expenditure positively mediates the negative association between FL and gender diversity. It is suggested that there is a complementary effect from a firm that spends money on CSR activities in the relationship between FL and gender diversity than firms that do not have expenditure item of CSR activities in its annual reports. Thus, CSR expenditure mitigates the negative association between FL and gender diversity.

The fifth finding shows that CSR disclosure does not mediate the association between financial performance (ROA, PBL and FL) and gender diversity. CSR disclosure only meets two out of the three conditions mentioned by Baron and Kenny (1986). We can deduce that CSR disclosure is defective in communicating the actions of firms in the area of gender diversity of the entire workforce. The sixth finding shows that CSR expenditure negatively moderates the negative association between ROA and gender diversity. The quest of a firm to achieve asset recovery competes with the employment of women and the spending on CSR worsens the situation making firms with CSR objectives less attractive than non-CSR firms towards the improvement in gender diversity in listed firms. Finally, CSR disclosure negatively moderates the positive and statistically significant association between PBR and gender diversity. We see that firms with improved market capitalization are perceived to employ women in an Indian context, and CSR disclosure is significant to influence the relationship.

Implication, Limitation and Future Direction of the Study

The previous assessment of gender diversity issues is limited to top management and gender diversity on the board, but this renders the sustainable development goal ineffective. A rethink of the relationship between gender diversity and financial performance for the entire workforce must be pursued by listed firms if there is a desire to contribute to sustainable development’s global objective.

The philosophy of CSR as the best system to communicate and improve minority issues are wholly not correct and is better for firms to show an item of expenditure on CSR than to use CSR disclosure with the ultimate intention of drumming up support for an improvement in gender diversity. This study’s discovery makes unlisted firms more attractive in improving gender diversity than large firms listed on the stock market.

The maximization of CSR manager’s efforts towards the improvement in gender diversity in upper management needs reassessment and inclusion of all levels of women employment which is consistent with international laws and sustainable development goals out doored in 2015 on gender diversity in all levels of employment in the firm.

The social role theory is also expanded to include FL, RAO and CSR disclosure which seems to affirm the disparity between women and men in employment through its negative association with gender diversity of listed firms in an emerging economy. However, CSR expenditure and PBR adds value to the improvement of gender diversity. Based on the aforementioned, firms’ management must be careful in designing strategies for gender diversity improvement, especially when the firms seek to use CSR disclosure to communicate to stakeholders and investors.

The study provides a new dimension in the study of gender diversity in the workplace. However, the use of a single country with listed firms with sustainability reporting may present a limitation to the study. Therefore, future studies can look at different countries in single research to improve the study’s generalization in the context of gender diversity.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

List of Variables for the Measurement of CSR Disclosure

| 1 | Education projects and scholarships awards to the community |

| 2 | Cash donations to the community; material donations to the community |

| 3 | Empowerment of skills to the community |

| 4 | Health facilities and health-related programmes |

| 5 | Community development projects |

| 6 | Employees contribution of cash to communities |

| 7 | Employee contribution of personal material to the community |

| 8 | Employee volunteering of skills to support the community |

| 9 | The number of hours of volunteering by employees recorded in sustainability reports |