Abstract

Studies are being conducted to measure the impact of corporate social responsibility (CSR) on different dimensions of performance of the firm. Therefore, it becomes imperative to measure CSR activities undertaken by the firms. The measures used to assess CSR range from quantitative to perceptual; hence, the study proposes to present an analytical profile of various methods used to measure CSR. The article reviews studies that span over the time period from the 1980s to 2016 to determine the relationship between CSR and performance of the firm. Various measures of CSR used in studies are broadly categorized as rating-based measures, financial measures, perceptual measures, and disclosure-based measures.

The study revealed that perceptual and rating-based measures are the most commonly used measures. Also, it has been found that the operationalization of CSR using these two measures has been used in the studies that are conducted mainly in developed countries. However, disclosure of CSR and expenditure made on social responsibility can be more comprehensive measures as they are more objective in nature and are not influenced by the biases. Also, expenditure on CSR can be a useful measure while conducting a cost-benefit analysis of CSR activities performed by the organizations.

Keywords

Introduction

Corporate social responsibility (CSR) is gaining importance worldwide (Yelkikalan & Köse, 2012). It has developed as a concept and is defined by several national and international bodies and researchers, in different ways (Frederick, 1960; Freeman, 1983; Osuji, 2011; Sprinkle & Maines, 2010).

Commission of the European Communities (2002) states that “Being socially responsible means not only fulfilling legal expectations, but also going beyond compliance and investing ‘more’ into human capital, the environment and the relations with stakeholders” (p. 6). These definitions of CSR reflect a very broad spectrum of CSR.

CSR has been recognized as an extension of corporate governance because organizations are expected to operate within the ethical and legal norms of the society (Parente & Machado Filho, 2016). Social responsiveness is a vital dimension of the reputation of the firm among stakeholders (Fombrun & Shanley, 1990). At the time of crisis, organizations may utilize CSR in order to maintain the trust of the stakeholders (Davis, 1973; Fehre & Weber, 2016). Corporate social performance attempts “to offer a managerial framework to deal with CSR and simultaneously, an attempt to measure CSR” (Valor, 2005, p. 193). Waddock (2004, p. 9) states that corporate citizenship refers to “the strategies and operating practices a company develops in operationalizing its relationships with and impacts on stakeholders and the natural environment.” Thus, corporate citizenship, corporate social performance, and CSR are used interchangeably in studies, but CSR is superior to them due to its normative orientation (Valor, 2005). The scope of the present paper is to review CSR and its measures.

Strategic implications of CSR for the firms have been realized by organizations as well as scholars. As per Porter and Kramer (2011), the companies must create shared value, that is, addressing the needs and challenges of the society along with profit-making for long-term growth and development. The concern of firm toward society generates intangible resources such as human capital, reputation, innovation, etc. that boost the performance of the firm Surroca et al. (2010). The augmented support of stakeholders due to CSR activities enhances the reputation of the firm (Chen & Wang, 2011). The engagement of firms in CSR activities benefit the firms in terms of higher sales volume, increased productivity, greater access to capital, reduced operating costs, enhanced brand image, greater customer loyalty, and better financial performance (Rettab et al., 2009; Said et al., 2009). Shukla et al. (2019) assert that strategic and ethical motive of firms reflected through their CSR activities positively impacts the purchase intention of consumers.

Thus, several studies are being conducted to measure the influence of CSR on different dimensions of performance of the firm. So to ascertain the implications of social responsibility on the firm’s performance, CSR needs to be measured. But the measurement of CSR is an issue as it is a qualitative aspect, and different procedures are used to quantify it (Tsoutsoura, 2004). The use of different measures of CSR in previous researches to study the impact of CSR on the financial performance of the firm has been indicated as one of the major causes of variation in results by researchers (Griffin & Mahon, 1997; Orlitzky et al., 2003).

The present study attempts to evaluate the different measures of CSR used in prior researches and develop an analytical framework. The articles reviews studies that span over the time period from the 1980s to 2016 to determine the relationship between CSR and performance of the firm. This time period was chosen, as in the 1980s, CSR was realized as an opportunity for businesses (Drucker, 1984) and several types of research were conducted to study its implications on the performance of the firm. The studies reviewed are obtained from different online databases.

Measures of CSR

“CSR is a multi-dimensional construct with behavior ranging across a wide variety of inputs (e.g. investment in pollution control equipments), internal behavior or processes (e.g. relationship with customer) and outputs (e.g. community relations and philanthropic programs)” (Waddock & Graves, 1997, p. 304). Walker (2010) conducted a systematic literature review of studies on corporate reputation and found that measurement of corporate reputation is a tight spot. Studies on CSR show that varied measures for CSR are used. Some of these measures are based on ratings, whereas other are derived from perceptions of various stakeholders including employees. The paper begins with grouping various measures into four categories on the basis of similarity of method and scope. These categories are rating-based measures, financial measures, perceptual measures, and disclosure-based measures.

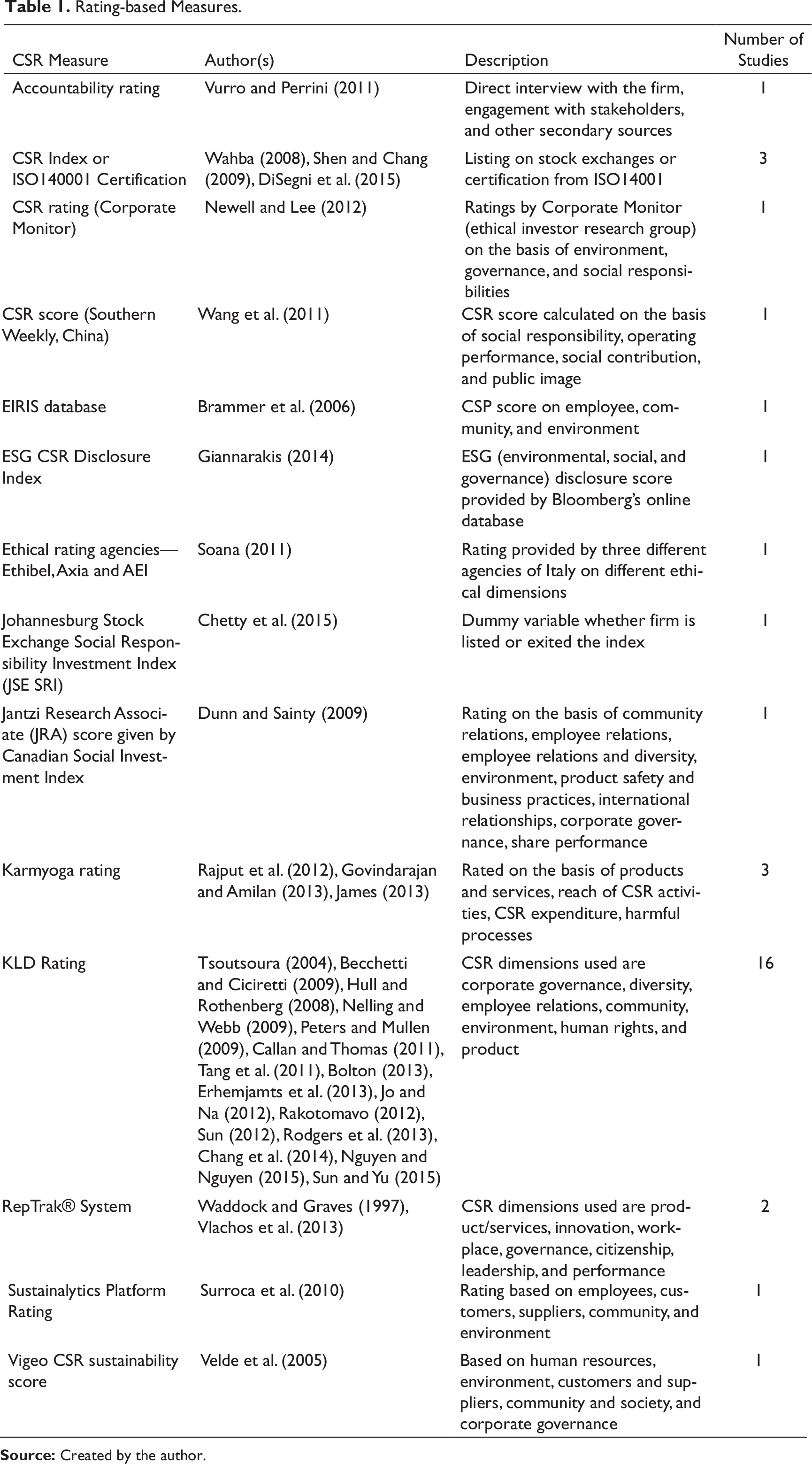

Rating-based Measures

The review of literature exhibits that the rating given to the firm by different agencies, on the basis of their involvement in philanthropic practices, community development, use of ethical business practices, has been used as a proxy for CSR. CSR ratings or scores are developed on the basis of information provided by firms in their reports, which is further supplemented with the information obtained by agencies through third parties, direct interview of stakeholders, etc. (Vurro & Perrini, 2011). Also, the listing of a firm on DowJones Sustainability Index (Wahba, 2008) as well as certification by well-known agencies such as ISO 140001 for their environmental and other CSR-related dimensions (DiSegni et al., 2015) are considered as CSR measures in this category. However, in this case, CSR variable is a binary variable with value 1, if the firm is certified or listed; otherwise, value is 0.

Rating-based Measures.

Table 1 exhibits different rating-based measures that have been used in previous studies being reviewed in alphabetical order of the rating used. The rating-based measures, such as KLD rating and RepTrak® System, are widely used measures of CSR found across studies. “KLD assigns a qualitative indicator zero/one score to CSR strengths and CSR concerns for rating purposes on an annual basis, with CSR strengths representing positive social performance and CSR concerns indicate negative social performance” (Chang et al., 2014, pp. 215).

RepTrak® System is based on the perception of stakeholders across seven dimensions of the firm that indicate the reputation of the firm among stakeholders (Fombrun et al., 2015). Porter and Kramer (2006) criticized rating-based measures due to variations in the criteria used in the ranking system as well as weights allocated to them.

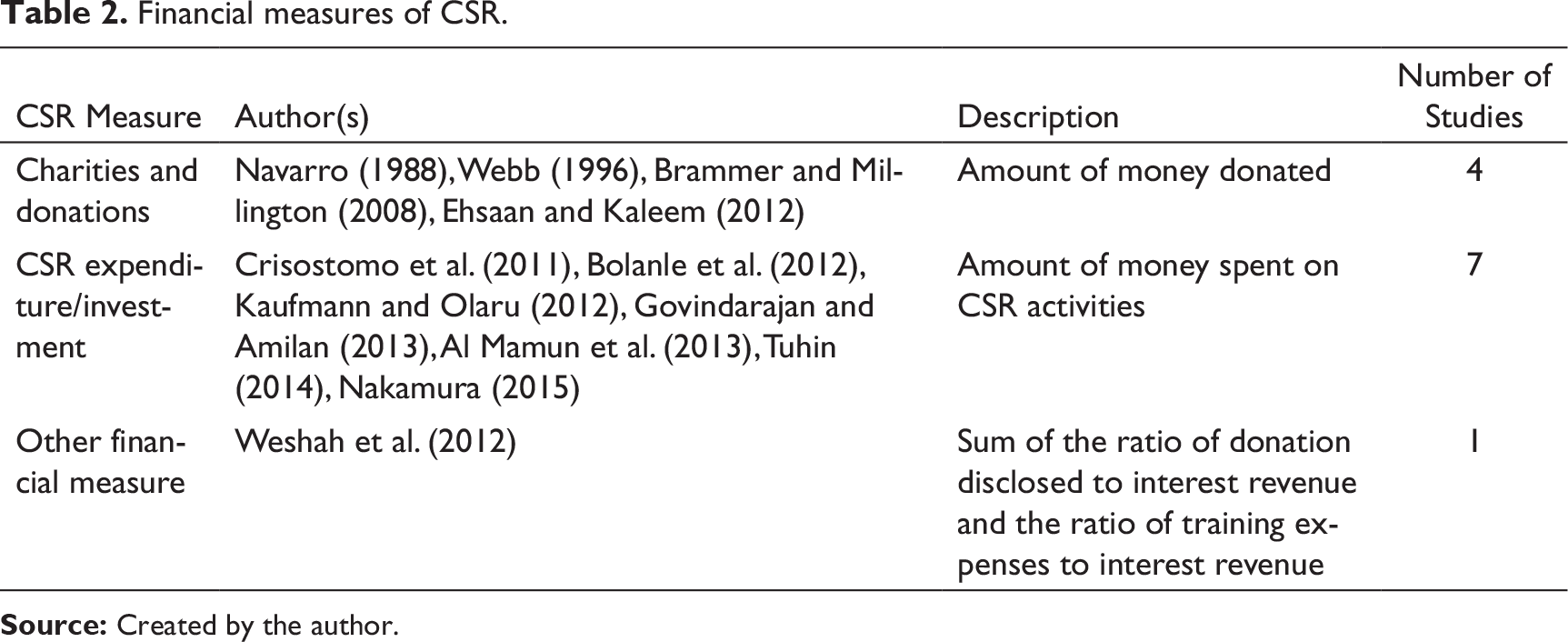

Financial Measures

Financial measures are quantitative in nature. These measures include the amount of money given away for charities and donations or expenditure made by firms on CSR activities. Table 2 lists such financial measures of CSR used in studies in alphabetical order.

Financial measures of CSR.

Table 2 indicates that, in this category, most of the studies reviewed used expenditure made on CSR activities as measure of CSR.

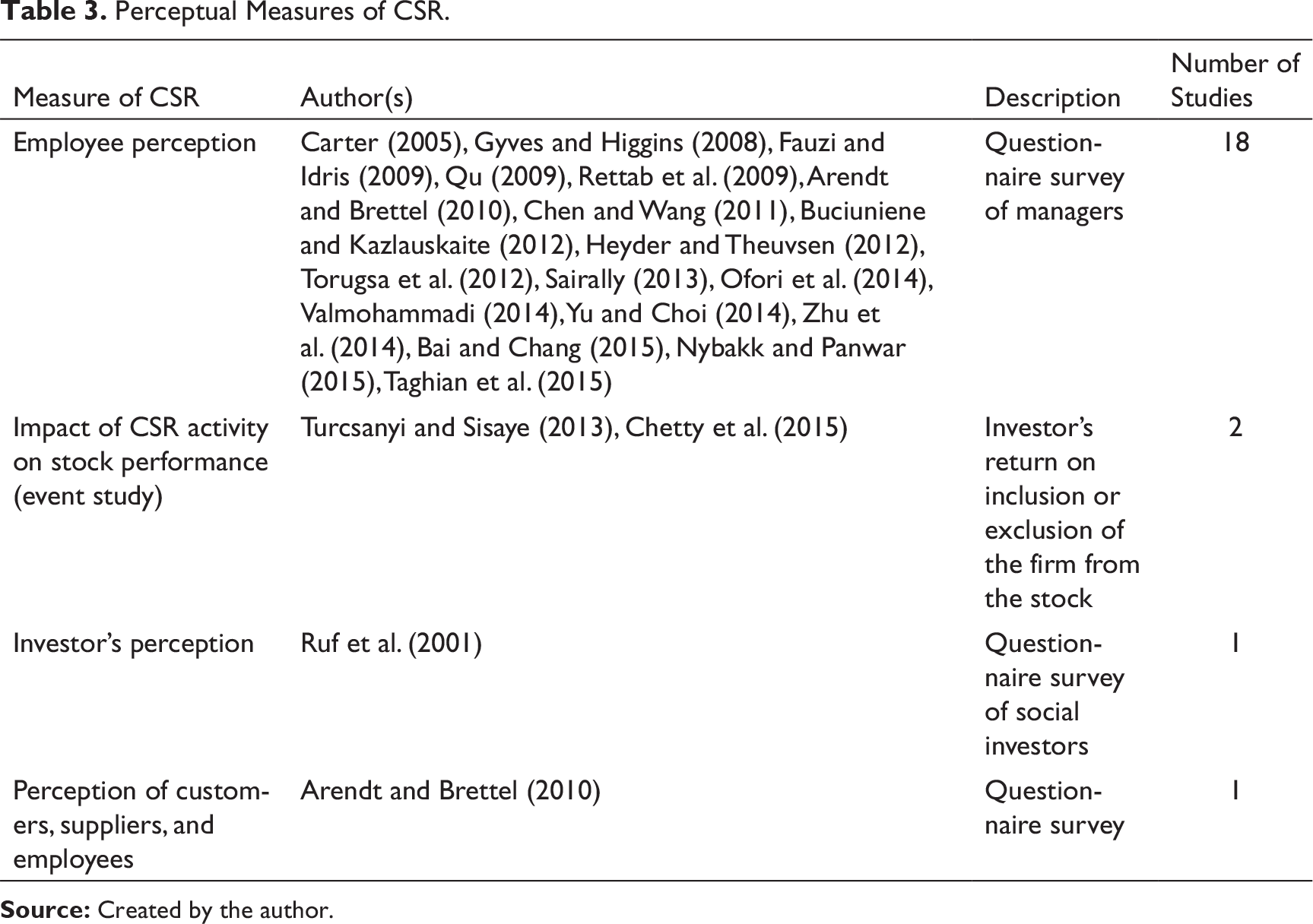

Perceptual Measures

Perceptual measures evaluate the CSR performance of firms on the basis of the perception of stakeholders. These measures include the perception of employees, customers, and investors obtained using various research instruments such as a questionnaire. These measures also include event study, that is, a study of the perception of stakeholders after some CSR event such as entry or exit from a socially responsible index (Chetty et al., 2015). Several perceptual measures used in previous researches are illustrated in alphabetical order in Table 3.

Perceptual Measures of CSR.

As evident from Table 3, employee perception is revealed to be one of the most commonly used perceptual measure of CSR in previous pursuits reviewed in the study.

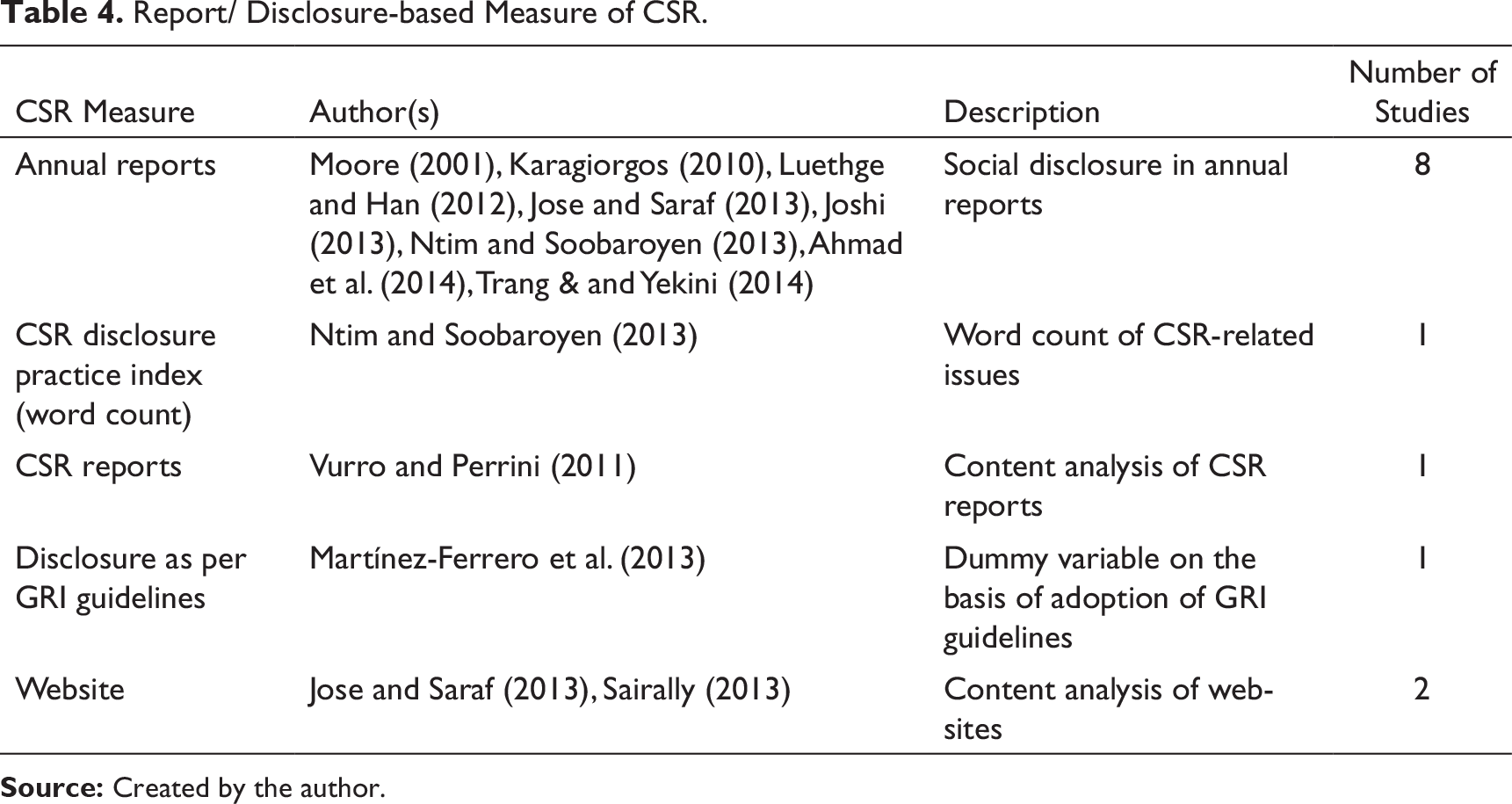

Report- or Disclosure-based Measure

Report- or disclosure-based measure of CSR relies on social responsibility information disclosed by firms through several documents such as an annual report, website, and exclusive CSR reports. In this case, CSR is quantified using content analysis of information related to social responsibility activities disclosed by firms in various reports. Content analysis can be defined as “a systematic, replicable technique for compressing many words of text into fewer content categories based on explicit rules of coding” (Montabon et al., 2007, p. 1002). It includes word count (Ntim & Soobaroyen, 2013) and frequency of sentences (Luethge & Han, 2012) related to CSR in the report. It also incorporates the disclosure of CSR activities of firms as per standard guidelines set by reputed agencies such as Global Reporting Initiatives (GRI; Martínez-Ferrero et al., 2013). Table 4 depicts different types of such measures used in studies.

Report/ Disclosure-based Measure of CSR.

It can be seen in Table 4 that information related to CSR, present in annual reports, is considered to be most relevant for assessing the performance of firms in previous studies.

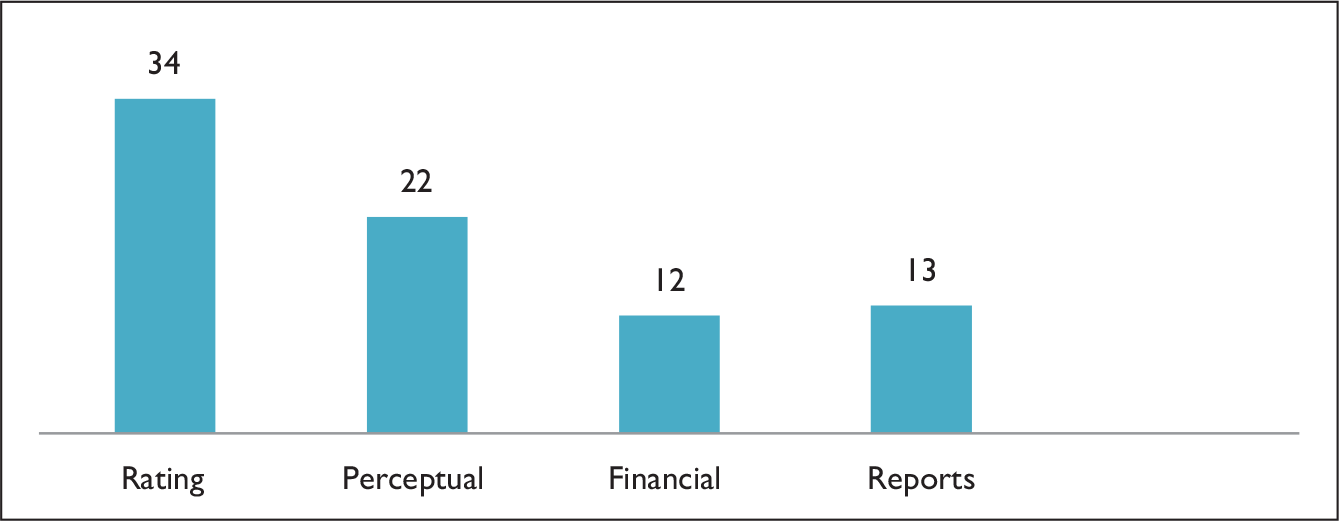

Figure 1 illustrates the different measures of CSR used in prior studies that are given in Tables 1, 2, 3, and 4.

It is demonstrated in Figure 1 that rating-based measures of CSR are the most commonly used measures followed by perceptual, financial, and report measures in descending order. However, evaluation of different measures led to the conclusion that rating-based and perceptual measures are highly subjective in approach. On the other hand, the financial measures can objectively measure the CSR activities as well as their impact on the firm’s performance. At the same time, CSR disclosure leads to perception and image building of the firms.

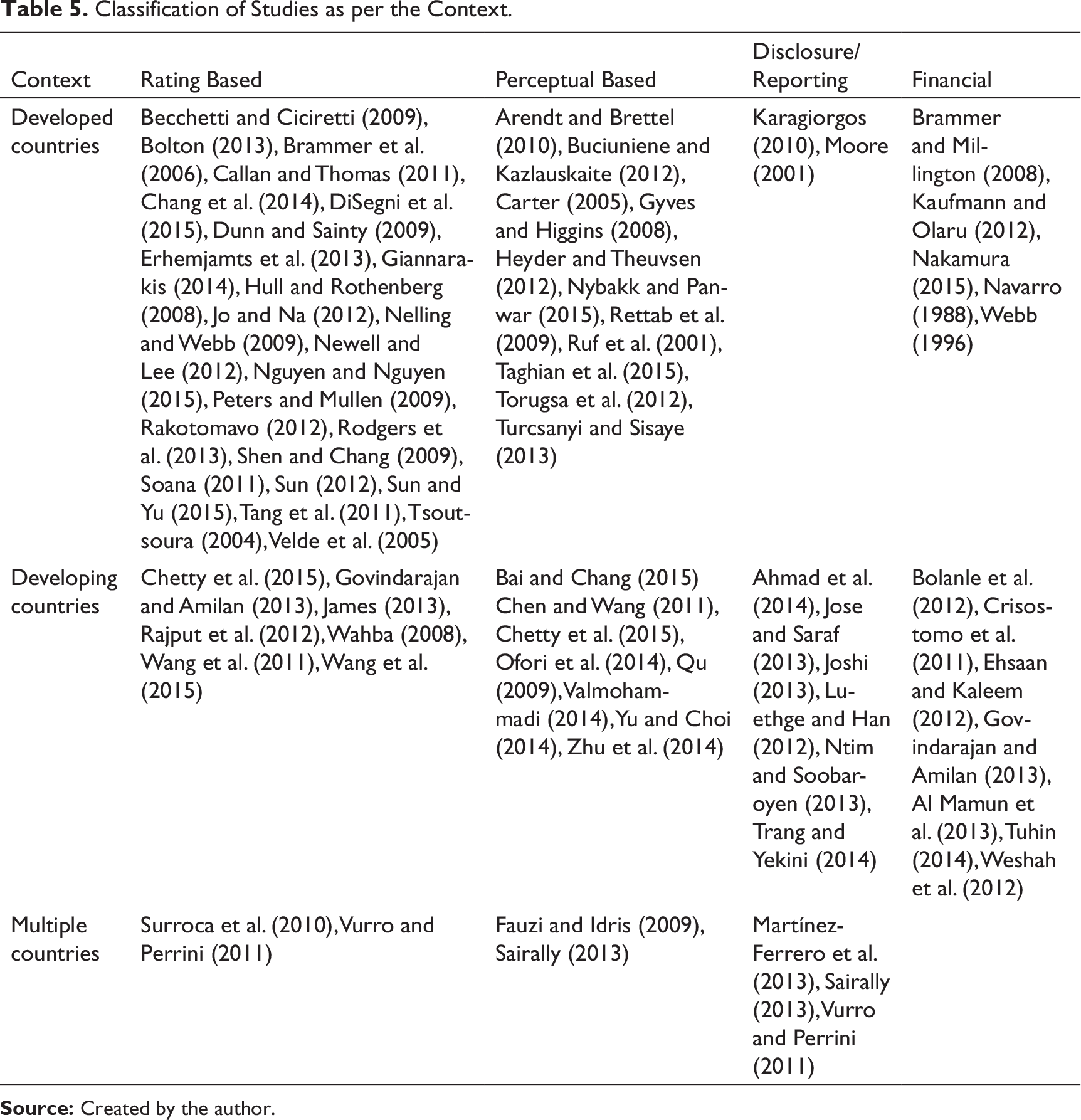

The measures of CSR are also classified on the basis of the context, that is, developed, developing, or multiple countries (more than one country), to provide insights on the type of measures used and the type of country where research is conducted. This classification of studies on the basis of context of study is presented in Table 5.

Classification of Studies as per the Context.

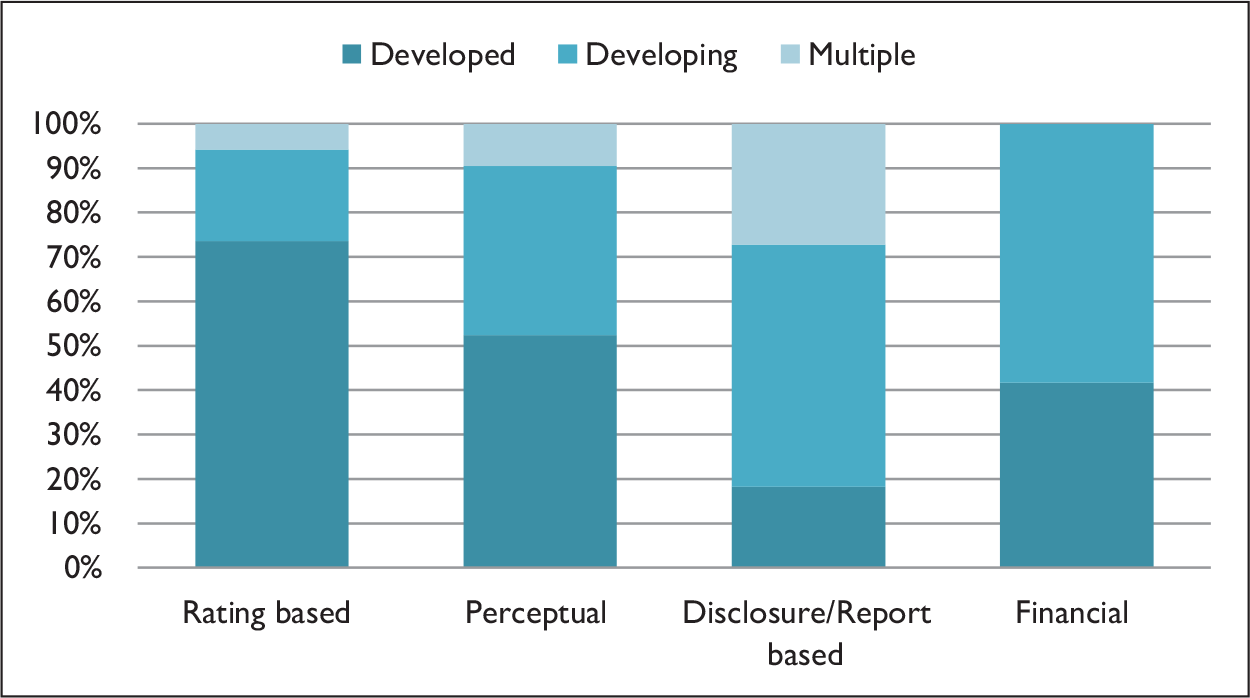

Figure 2, drawn using Table 5 data, indicates that majority of the studies that used rating-based and perceptual-based measures are conducted in developed countries where CSR is a well-developed concept. But disclosure-based and financial measures are found to be more prevalent in developing countries where CSR is still a new concept.

From Figure 2, it can be envisaged that CSR expenditure and CSR disclosures as measures have been underutilized. CSR expenditure provides the basis for a cost-benefit analysis of social responsibility activities performed by firms. It is quantitative in nature and reflects the actual efforts made by firms for the welfare of society. Further, Crisostomo et al. (2011) posit that CSR activities of the firm do not enhance the profits unless they are well communicated to the stakeholders. This makes CSR disclosure an equally relevant measure. Therefore, with an objective of highlighting the significance of the two measures, it is attempted to present a detailed account of CSR expenditure and CSR disclosure for evaluating social responsibility of firms, in the following sections. For the sake of presentation donations, charities and similar activities have also been included in CSR expenditure and any information on CSR activities undertaken whether from company sources or other publications are included in the disclosure. These two measures separately and jointly provide a tool for comparison and evaluation of CSR profiles.

Expenditure as a Measure of CSR

Kaufmann and Olaru (2012) suggest that expenditure on CSR activities is the preferred measure of CSR while determining impact of CSR on satisfaction of stakeholders. CSR expenditure is the amount of money spent in carrying out CSR activities. It determines the extent to which a firm is actually involved in CSR activities not merely paying a lip service to it.

Barnea and Rubin (2010) assert that managers of the firm overspend on CSR activities if their ownership in the firm is low to enhance their personal image termed by the authors as “warm-glow effect” (p. 71). This study also found that firms with a large amount of debt are short of cash, and, hence, they do not spend heavily on CSR. Thus, expenditure on CSR could be a source of conflict among stakeholders. Rakotomavo (2012) found that the investment in CSR activities is highly contagious to profits and earned equity of the firm. Firms with higher earned equity tend to be more socially responsible. Cheng et al. (2013) further complemented the results by stating that expenditure on CSR depends on managerial ownership and governance as “improvements in managerial incentives and governance lead to a reduction in firm goodness” which implies that “managers overspend on goodness because they wish to do good with other people’s money” (pp. 26, 27).

Level of CSR expenditure is also discovered to depend on the financial slack, a company possesses as it is revealed in a research (Hong et al., 2012) that “goodness spending is much more sensitive to financial slack than is the case for capital and research and development expenditures” and also that “such goodness expenditures are not core to the firms’ themselves but are plausibly interpreted as off-sets” (pp. 26, 27). It was further investigated by Harrison and Coombs (2012) that available slack with firms though has a positive effect on corporate spending but “board composition, professional investment fund ownership, and CEO stock ownership all weakened the relationship between available slack and community investment” (p. 418).

As an example, a study on Coca-Cola by Ogola and Dreer (2012) revealed that CSR spending is affected by its market share as firms strategically use CSR to gain benefits in the regions where their market share is medium because “there are more chances for the company to capture and penetrate the market” and “maybe there is fierce competition that the company has problems staying in them so they become more aggressive in their CSR spending” (p. 2244).

Suriya and Sudtasan (2014) categorized the relationship between sustainable profits and CSR expenditure into four categories, namely, frozen area, warm-glow area, decayed area, and charitable area. In the warm-glow area, a firm has to spend more on CSR activities, and gains are seen in the long run; in frozen area, the sustainable profitability of the firm increases without much increase in CSR expenditure. The charitable area is marked with a large amount of CSR expenditure with no profits, and in decayed area, neither CSR expenditure nor profits exist. The study suggests determining the location of the firm with regard to the state where profits are steady and thus amend policies to reach that status.

Webb (1996) showed that CSR expenditure by organizations results in “stock of goodwill” and “the stocks of goodwill would diminish to zero if no further expenditures were made to charitable organizations” (p. 408).

Realization of strategic benefits such as an increase in the corporate image has inspired large firms to enhance their expenditure on CSR activities (Ogola & Dreer, 2012). Berner in 2005 indicated that large companies disclosed substantial spending in CSR initiatives “that is, Target’s donation of $107.8 million in CSR represents 3.6% of its pre-tax profits, General Motors’s donation of $51.2 million represents 2.7% of its pretax profits, General Mills’ donation of $60.3 million represents 3.2% of its pre-tax profits, Merck’s donation of $921 million represents 11.3% of its pre-tax profits, and Hospital Corporation of America’s donation of $926 million represents 43.3% of its pre-tax profits”. However, Lys et al. (2015) assert that positive impact of expenditure on CSR activities of the firm “is more likely due to the signaling value of CSR expenditures rather than positive returns on those investments” (p. 70), as expenditure on CSR activities is made by firms in anticipation of better future prospects.

Disclosure as a Measure of CSR

Reporting of CSR activities is well-established in developed countries, as asocial responsibility model has a strategic orientation and considers stakeholder’s perspective (Guthrie & Parker, 1990; cf. Deegan & Rankin, 1997). Blacconneire and Northcut (1997) found that firms which provide extensive environmental information are positively perceived by investors to be abiding by rules and regulations and are less prone to regulatory cost. Deegan and Rankin (1997) found that environmental information presented in the annual reports of the firms is useful for shareholders and managers with oversight task, but accounting information is of prime importance.

CSR disclosure is transparent communication of CSR activities of firms to its stakeholders (Orlitzky et al., 2003). Habek and Wolniak (2015) define CSR reporting as “the provision of useful information for external and internal stakeholders on the economic, environmental and social results achieved by an organization” (p. 560). Haque and Azmat (2015) have proposed disclosure of eight dimensions of CSR that include labor rights, occupational health and safety, environment, fair pay, social welfare/work –life balance, legal aspects, fair trade, and gender issues for a labor-intensive industry.

Cormier and Maignan (1999) determined several aspects that impact environmental disclosure by firms. These aspects comprise financial condition, that is, a firm with more financial resources reports more environmental information. Another set of factors that positively impact environmental disclosures include dependence on the capital market, trading volume, and the risk involved in the firm’s operations. Also, the impact of a firm’s actions on the environment determines environmental disclosure.

Mohd Ghazali (2007) found that the ownership structure of the firms determines the extent of CSR disclosure. Firms which are privately managed show lesser concern for CSR communication, while firms that are owned by the government reveal more CSR information. Giannarakis (2014) states that the board commitment to CSR along with profitability and firm size positively impacts disclosure of CSR practices. However, increased financial leverage is a constraint on the extent of CSR disclosure. Muttakin and Subramaniam (2015) established that the corporate governance structure of the firm impacts the reporting of social responsibility activities. Social responsibility of firms is positively influenced by ownership and the number of independent directors on board of the company. Muttakin et al. (2015) in a study on Bangladesh firms posited that the extent of CSR disclosure is positively influenced by the presence of foreign directors on the board, profitability of the firm, and its size while the presence of female directors reduces it.

Giannarakis et al. (2014) stress that the firm in highly polluting industry, which takes measures to reduce its negative impact on society, highly discloses CSR information in order to build the image of a responsible corporate citizen and minimizes regulatory cost. It is evidenced in Javaid et al. (2016), that firms in polluting industry such as oil and gas disclose more information while the firms belonging to the textile industry that has a major stake in the economy of the nation, discloses less information on CSR.

Khemir and Baccouche (2015) establish that international orientation of a firm as well as the political associations of the firm influences its disclosure of CSR practices positively.

Dhaliwal et al. (2012) suggest that disclosure of CSR information supports financial disclosure and leads to more accurate forecast for firms. Blomback and Scandelius (2013) assert that the incorporation of heritage identity of the firm in CSR reporting enhances the image of the brand. Ling and Sultana (2014) established that as the number of signal breach increases, the management is more concerned with CSR disclosure to assure the stakeholders of functions of the firm. Lu et al. (2015) state that high-quality reporting of CSR activities increases the reputation of the firm as through reporting of these activities a firm attempts to meet the societal expectations.

Crisostomo et al. (2011) established that the benefits of the cost involved in CSR activities are only realized when a firm exists in an environment that is well aware of it. Organizations use standalone reports on CSR to flaunt their social performance in market (Mahoney et al., 2013) because CSR disclosure sends positive signals to different stakeholders and provides valuable information about the firm. Thus, CSR disclosure is considered essential for firms to retain the confidence of stakeholders (Fatma et al., 2014; Perez & del Bosque, 2014). The content presented in CSR reports is an indicator of a firm’s performance (Malik, 2015). Social resilience theory proposed by Zahller et al. (2015) states that organizations which voluntarily disclose their CSR performance are perceived as trustworthy and credible and are, therefore, not affected by external incidents that are alarming for industry and beyond the control of the firm.

A study on Islamic financial institutions by Aribi and Gao (2011) found that the disclosure of CSR information in annual reports is affected by Islamic beliefs. Content analysis of CSR reports of China by Gao (2011) revealed that government-owned firms in China being politically sensitive addressed most of the social issues while non-government owned enterprises were more concerned toward the interest of the stakeholders. In a study in Malaysia by Haji (2013), it was affirmed that, initially, the size of the board had significant influence only on the extent to which CSR information is disclosed but after policy changes related to CSR, it influenced the quality of CSR disclosure also. Thus, CSR disclosure is influenced by the external environment such as social and political in which a firm operates.

Kilic (2016) has set up that the firms that are highly visible in society due to their large size and listing on multiple exchanges communicate more about their CSR activities. Gallego-Alvarez and Quina-Custodio (2016) found that size of the firm is one of the important determinants of CSR disclosure, but leverage impacts the economic dimension of the disclosure, and listing of a firm on Dow Jones Sustainability Index (DJSI) and common law have considerable influence on disclosure of environmental information. It was established that a firm’s size along with the existing trends and vogues positively affects the communication of CSR activities by the firm.

Rahdari and Braendle (2016) affirm that the perception of users that disclosure is comprehensive is more important as compared to simply reporting CSR activities as per the established reporting framework. Dias et al. (2016) emphasize that firms that are in close proximity with consumers focus on CSR disclosure to build their reputation. Firms with large family ownership disclose less, while those owned by the government disclose more CSR information.

The review of the extant literature on CSR disclosure sufficiently supports the argument that it is an important measure and has a far-reaching effect on the performance of the firm, especially in a long-term perspective. Therefore, it is worthwhile to utilize this measure for evaluating CSR of firms at large.

Evaluation and Comparison of Different Measures of CSR

Table 5 provides a summary viewpoint in order to facilitate the choice of appropriate measure for a particular context.

The rating-based measures are found to employ different methods as well as different dimensions of CSR to obtain the CSR rating of the firm. Kinder, Lydenberg, and Domini (KLD) rating uses corporate governance, diversity, employee relations, community, environment, human rights, and product dimensions of CSR for calculating CSR score, while RepTrak® System evaluates CSR score on the basis of product/services, innovation, workplace, governance, citizenship, leadership, and performance. The selection of stakeholder or CSR dimensions for the evaluation of the score also depends on the nation where the study is carried out. These measures can be subjective and vary with the method used to calculate score as well as accuracy of the information (Balabanis et al., 1998). It can be concluded that the reputational index and rating-based measures can be effectively applied in situations where awareness and adoption of CSR are well in place and all stakeholders, including consumers, understand the impact of CSR practices. Such ratings may be used especially in economically advanced countries, where CSR awareness is relatively high.

Questionnaire-based surveys or interviews of employees, customers, and other stakeholders are used for developing perceptual measures. The source of input for such measures is found to impact the results in favor of those stakeholders whose perception is used for developing the measure. The employee perception can be inclined toward labor and employee dimension of social responsibility while ignoring other important dimensions such as environment, community. Perceptual measures have all those limitations that are found in opinion-based methods, such as respondents’ biases as well as researchers’ biases. A prerequisite of these measures is that the respondent should be fully aware of the CSR concept and practices. Therefore, these measures may be used where the objective is to evaluate the impact of CSR on any one of the stakeholders and also the awareness of the stakeholders about CSR is high. Therefore, these measures are also prevalent in developed economies.

Financial measures (refer Table 2) used in studies comprise CSR expenditure and donations given away by organizations. CSR expenditure is the expenditure of firms on activities that are not related to its operations rather concerned with society (Crisostomo et al., 2011). These measures employ an objective approach to quantify CSR. These measures provide a concrete account of the involvement of firms in CSR activities in terms of budget allocations and actual expenditure. Financial measures quantify the CSR activities of a firm as in many countries the mandatory requirement for CSR is expressed in terms of a proportion of annual turnover. This makes it possible to compare the impact of CSR expenditure on a firm’s financial performance. Therefore, it is proposed that CSR expenditure is a suitable measure for conducting a cost-benefit analysis of CSR. It is the responsibility of the board of directors to allocate budget for CSR activities; hence, financial measures shall be a reflection of good governance as well. Thus, it is an appropriate measure for developing economies where CSR is in a naive stage.

Modern business is largely based on communication. Therefore, disclosure/report-based measures depend on the revelation of social responsibility activities by firms. Since CSR disclosure is in terms of activities carried out on various accounts, the method adopted to measure CSR disclosure is content analysis. It is also a subjective measure where the firm itself is providing details of CSR activities in the annual reports or other documents. However, the content analysis provides objectivity to the outcomes. “Content analysis yield insights that would otherwise be impossible to obtain through questioning” (Maphosa, 1997, p. 184). These measures can be used to assess the inclination as well as the involvement of firms toward CSR activities. The limitations of these measures are that these can be adopted only when firms report their CSR activities on a regular basis and also when the activities so disclosed are the ones actually converted into reality. This measure of CSR, as shown in Figure 2, is more applicable in developing countries where communication of CSR is more important to enhance the awareness level of CSR among stakeholders.

Conclusion and Recommendations

The present article provides a critical review of available measures of CSR used in previous studies ranging from 1960 to 2016. It is observed that researchers’ concerns have not changed over the period, irrespective of country/industry context. All the CSR measures used in studies are categorized into four categories, namely, CSR rating-based scores, perceptual measures, financial measures, and reporting/disclosure-based measures on the basis of the method employed to measure them.

Review of studies reveals that most commonly used CSR measures are rating-based and perceptual measures, which are commonly used in developed countries where CSR is a well-recognized concept. But these measures are subjective in nature and can be biased toward a particular stakeholder whose perception is studied. On the other hand, a few studies utilize financial measures such as CSR expenditure that can provide a more objective picture of social involvement of firms. It can be a better measure for a cost-benefit analysis of CSR activities. Further, CSR reporting or disclosure is also an important measure because firms are expected to disclose their CSR activities to stakeholders (Rao & Tilt, 2016). To conclude, it can be said that CSR expenditure can be used effectively for evaluating CSR profile of the company as a single measure as well in combination with other measures.

However, it would be presumptuous to say that the research is free of any limitations. It is primarily a literature review, and although efforts have been made to cover a large number of studies, still it is possible that some important studies might have been left out albeit unintentionally. Thus, future research can be taken up to further refine the framework.