Abstract

Investing in advertising, research and development (R&D) and human resource management and development (HRMD) enabled firms to achieve competitive advantage and improve profitability. Indian economy witnessed the event of ‘Demonetization’ in November 2016 that created short term cash shortage. The study aimed at understanding the relationship of advertising, R&D and HRMD intensities on firm performance (proxied with return on assets). The effects of demonetization on these variables were explored. Financial data of listed Indian firms, over the years 2014–2019 was collected from CMIE Prowess database for the analysis using fixed effects panel-data regression. Results indicated significant positive relationship between R&D and advertising intensity with firm’s performance pre-demonetization, while reduced effect post-demonetization. HRMD intensity had a negative relationship pre as well as post-demonetization on firm’s performance. The results provided insights for managers and decision-makers on the impact of cash resource allocation on R&D, HRMD and advertising expenditures in creating firm value.

Keywords

Introduction

Indian economy, one could argue, witnessed two significant events in the last five years, between the years 2015 and 2020. First was the event of demonetization, which happened in November 2016 (Kulkarni & Tapas, 2017; Uke, 2017). The second event was the rollout of goods and services tax (GST) carried out on 1July 2017 (Kumar et al., 2019; Mali, 2016; Shekhar, 2019; Singh, 2017). Emerging economies like India required a special treatment as its business landscape was viewed as unique (Bhattacharyya, 2011; Chittoor & Ray, 2007; Gaur et al., 2014; Singla & George, 2013). These events could be characterized as dynamic, chaotic and complex (Bhattacharyya et al., 2011; Midthanpally, 2017).

Indian economy had traditionally followed the erstwhile Soviet Union (USSR) style of five-years planning based centralized form of economic governance (Geall & Pellissery, 2012; Jalan, 2004; Kapila, 2008; Misra & Puri, 2011). However, Indian economy confronted a major foreign exchange crisis in the year 1991 (Basu, 2004). In the year 1991, Government of India (GoI) rolled out the policy of liberalization, privatization and globalization (popularly abbreviated as LPG) (Basu, 2004). Prior to this event, most Indian businesses were substantively regulated by the government, including manufacturing capacities, industrial and market licenses (Kapila, 2008). Subsequent to the year 1991, with the advent of LPG policies, the role of government in granting industrial and market licenses were abandoned (Basu, 2004; Jalan, 2004; Misra & Puri, 2011). There was also expansion of the Indian equity market, inflow of venture capital, Foreign Institutional Investments and Foreign Direct Investments (Banerjee, 2013; Khan & Banerji, 2014; Sinha, 2011). Given these underlying conditions, Indian private sector, increased its footprints due to which Indian economy became more vibrant (Bhattacharyya et al., 2020a; Deb & Mukherjee, 2008; Samal, 1997). Indian economy, along with the likes of the economies of China, Brazil and Russia was christened as emerging economies (Hoskisson et al., 2000). One could argue that Indian economy did well because of the sectorial growth of services industries (Arora & Athreye, 2002; Kochhar et al., 2006). Furthermore, subsequent to the year 1991, the Indian private sector became outward and export oriented (Basu, 2004; Bhattacharyya & Choudhury, 2017; Jalan, 2004; Kapila, 2008). One could argue that as the restrictions on capital investments inward and outward were reduced, so Indian firms invested both in Indian market as well as global markets (Bhattacharyya et al., 2020b; Chittoor & Ray, 2007; Gaur et al., 2014; Singla & George, 2013). Indian firms competed with foreign players which entered India post 1991, as many factor input commodity markets and others became global (Bhattacharyya & Deepak, 2012; Dicken, 2007; Jalan, 2004). Indian firms also financially performed well in certain foreign markets (Chandra & Sastry, 1998; Kochhar et al., 2006). Indian economy grew at an average growth rate of around 6–7% over the last three decades which was more than the previous four decades of growth of around 3–4% annually (Jalan, 2004; Kapila, 2008; Kumar, 2016; Misra & Puri, 2011). Therefore, one could tautologically argue that the Indian economy, between the years of 1991 till 2019, did well because of increased privatization, globalization, increased output and export-oriented focus.

Demonetization was announced by the GOI on 8 November 2016, voiding all the extant ₹500 and ₹1,000 INR currency legal tenders (Kulkarni & Tapas, 2017; Uke, 2017). The government also announced the issuance of new ₹500 and ₹2,000 INR currency legal tenders in exchange for the demonetized currency legal tenders (Mali, 2016; Singh, 2017). The demonetization event implementation resulted in a cash shortage, which resulted in reduced purchases made by consumers (Raychaudhuri, 2017; Uke, 2017). Some argued that the process of demonetization had an adverse impact on the informal and unorganized sector (Ghosh, 2017; Roy, 2019). However, the positive arguments for demonetization towards the economy were regarding demonetization enabling consumers to switch to digital payments (Aggarwal & Gupta, 2019; Bhukuth & Terrany, 2019; Verma et al., 2019) and reduced scope of the proliferation of shadow economy, which often acted as a drag in the formal economy growth (Tagat & Trivedi, 2020). GoI policymakers did significant thinking about the fact that the Indian economy was beset with institutional voids (Manikandan & Ramachandran, 2015). Furthermore, it was also being carried in large proportion as shadow economy (Chaudhuri et al., 2006). The size of the shadow economy of India was around 17–18% (Medina & Schneider, 2018; The Association of Chartered Certified Accountants, 2017). To reduce the impact of the black-market on Indian economy, GoI decided to take away with the highest denomination of currency legal tenders. Generally, hoarding of cash was done with higher denomination currencies. Demonetization had been practiced earlier when government carried it out in the year 1946 (by British Government in pre-independent India) and in the year 1978 (Singh, 2017).

Given such realities, it would be pertinent to understand how the demonetization event had affected Indian firms’ profit/sales, return on assets (RoA), research and development (R&D) intensity, advertisement intensity, human resource management and development (HRMD) intensity. To ascertain this, the authors had undertaken both correlation and regression analysis with independent variables as R&D intensity, advertising intensity, HRMD intensity and the dependent variable as firm profit/assets ratio. The authors undertook this through the application of econometric tools (Mali, 2016; Singh, 2017). The authors had collected data for this study for the last six financial years (between the years 2014 and 2019) from CMIE Prowess database. The authors for analysis used fixed effects panel-data regression. For the Indian context, research was scarce regarding how this event (demonetization) had impacted the parameters mentioned. The insights derived from this study would aid managers and decision-makers in optimizing resource allocation into the value creation and value appropriation activities before, during and after such a chaotic event. So, the authors were interested in studying this researchable gap.

Literature Review

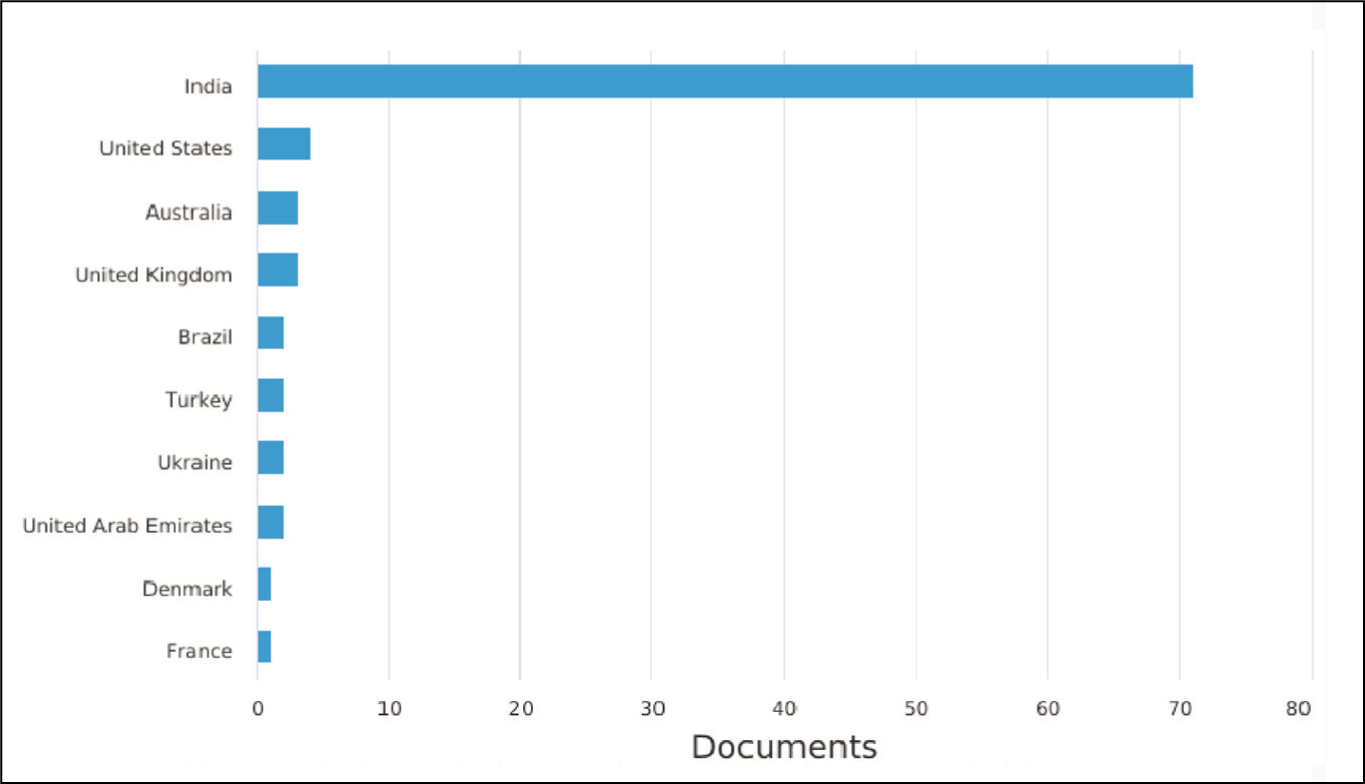

In this section, the authors presented the literature review of relevant extant studies. For this, the authors selected articles from journals listed in the ‘Scopus’ databases. Figures 1–3 depicted the statistics collected through the search query in the ‘Scopus’ database using the keyword ‘demonetization’. Around 81 journal articles and conference papers had been published on the topic in ‘Scopus’ listed journals. Most of the research work had been carried out in India. This was tautological, because demonetization as an event (in the recent history of the world) occurred only in one big economy, that being India. So, Indian researchers were most interested in this topic. This was evident from Figure 1.

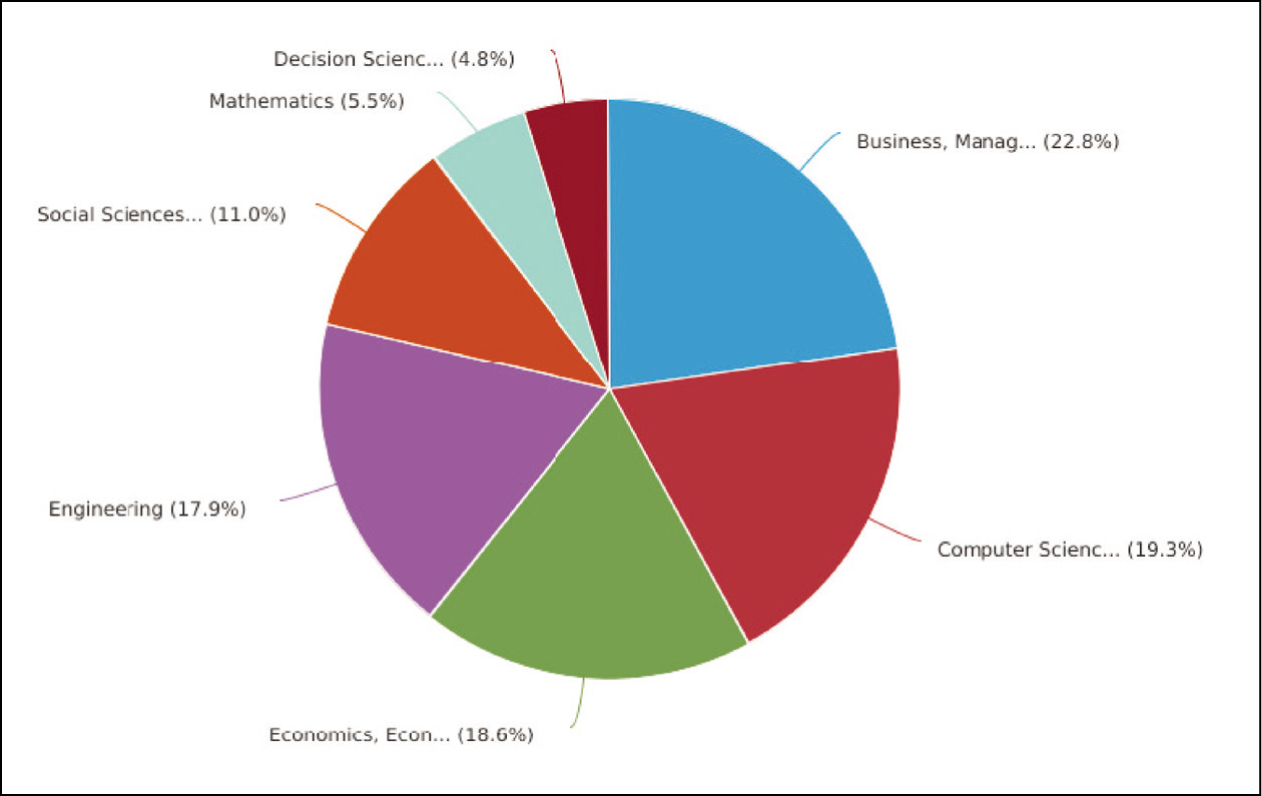

Figure 2 depicted that the field of demonetization had a majority of studies from the business and management domain. This was because demonetization as an event affected businesses and management of firms.

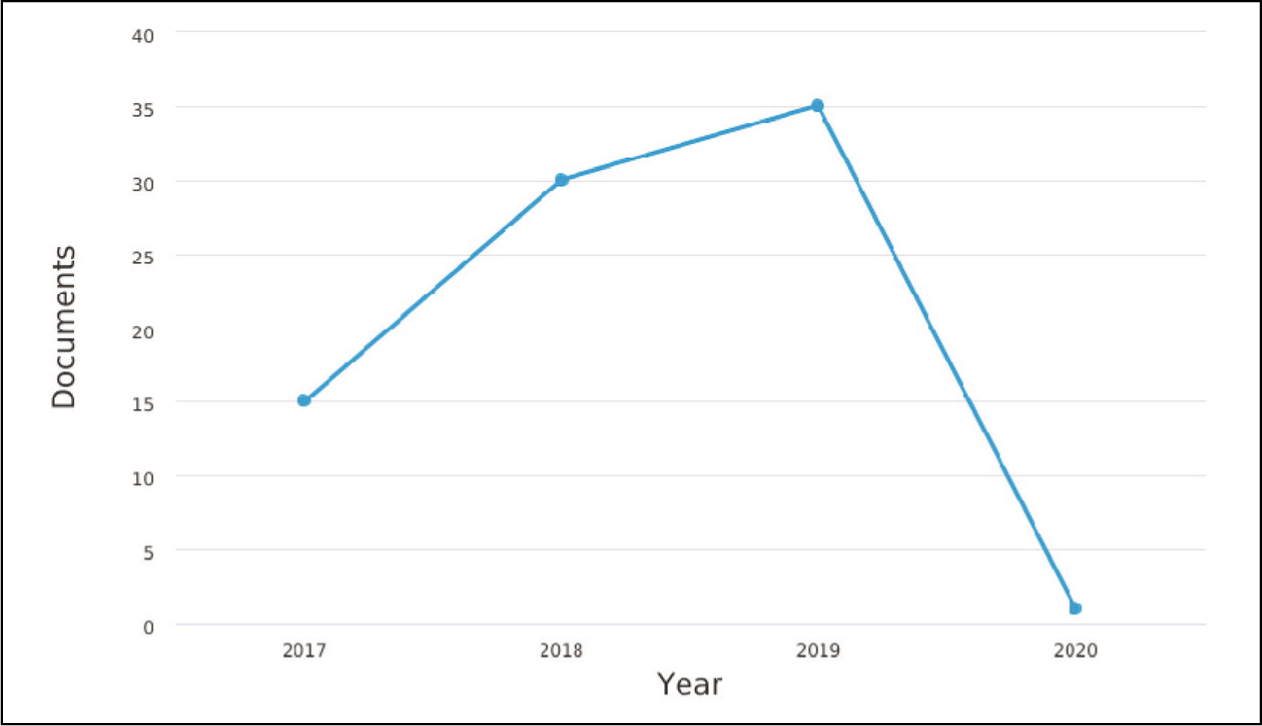

Figure 3 depicted that the field of demonetization as a field of study gained interest from the year 2017.

Researchers picked interest in the event of demonetization post the year 2016. These articles had focused on the push towards digital payments, effects of demonetization on different sectors and social media analysis. However, there was scarcity of investigations in terms of the effects of demonetization on firm performance and the three intensities mentioned earlier, which were important determinants of firm action and performance.

Cash has been considered as key strategic assets for firms in carrying out operations as well as towards spending on innovation projects (Kim & Bettis, 2014; Russo, 1991). Holding excessive cash reduced financial friction and helped firms towards investing in high-risk and high return projects (Brown & Petersen, 2011; Russo, 1991). However, very high level of firm cash position could also increase opportunity costs and lower returns (Lee & Powell, 2011; Martínez-Sola et al., 2013). It was observed that firm managers often tended to accumulate more cash and liquid assets, whereas reduced investing in growth opportunities and innovation during crisis periods such as during the Dot.Com bubble or the sub-prime mortgage crisis (Jalilvand & Kim, 2013). Also, firms that maintained higher liquidity levels in the pre-crisis period performed better during the crisis period than those firms’ with shortage of cash (Garcia-Appendini & Montoriol-Garriga, 2013). Null and Pathak (2019) had found that Indian firms, on average, tended to keep higher levels of cash during crisis periods compared to other times and corporate cash holding for business group firms was lower than that of standalone firms.

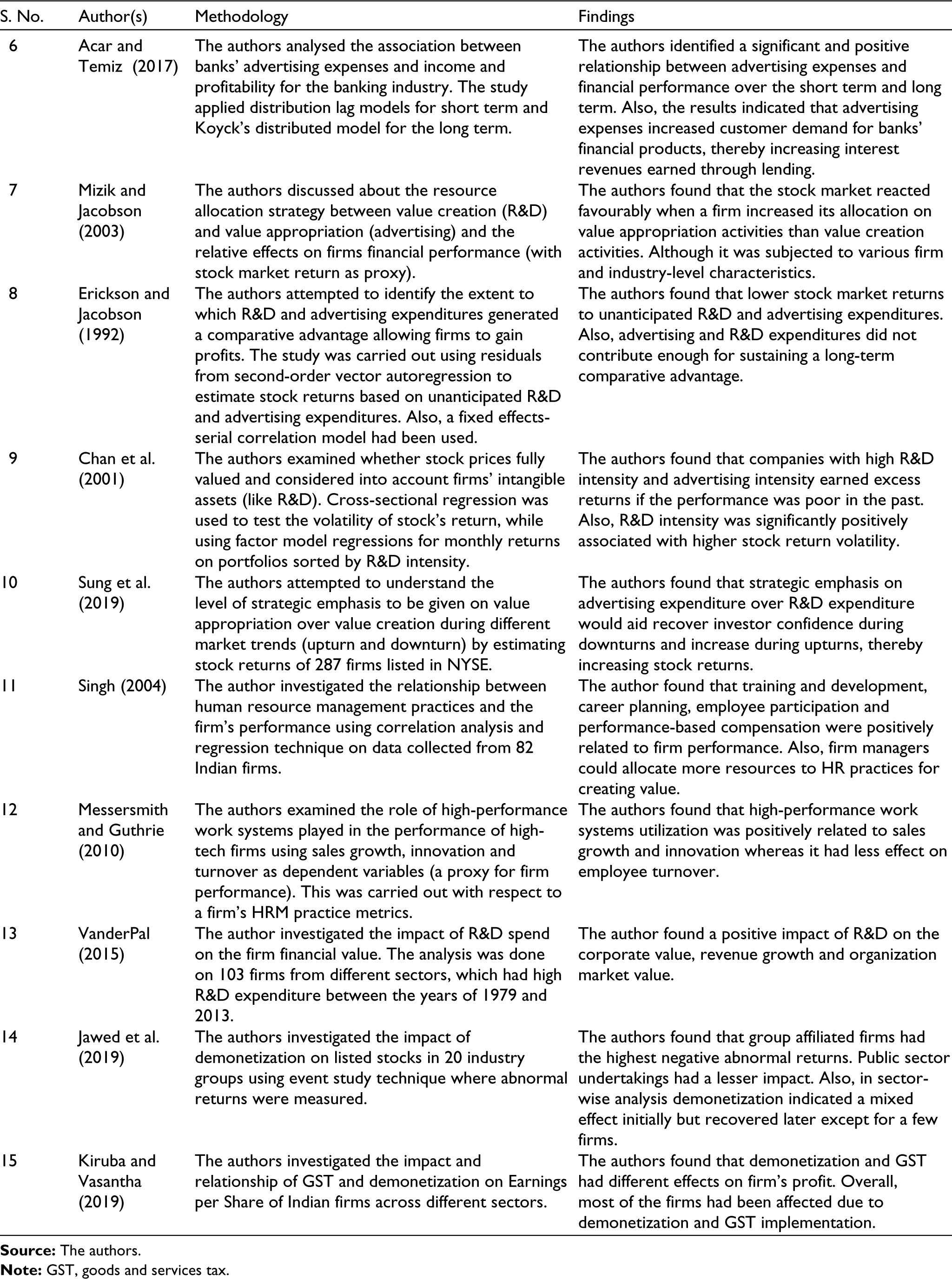

Event study has been a popular technique used in understanding the effect of an event on a firm by measuring the abnormal returns subsequent to the event period against the performance of the firm stock in the listed exchange (Corrado, 2011; Yalla et al., 2020). The market model was considered while employing the technique in order to nullify market-wide effects (Ball & Brown, 1968; Fama et al., 1969). The technique had been utilized in various domains of research (Cichello & Lamdin, 2006; Gong, 2009; Johnston, 2007; Roztocki & Weistroffer, 2009; Yalla et al., 2018;). Another technique used was regression-based event study, in which the non-overlapping event windows were treated using dummy variables and therefore estimated the effect based on the coefficients (Pynnonen, 2005). Regarding the literature study on demonetization, the authors studied the articles from ‘Scopus’ indexed journals search. The literature review was initially based on the study of the article title, abstract and keywords. Subsequently, the authors narrowed down the literature review study based upon relevance, context and immediacy parameters to focus on 15 articles for in-depth analysis. The findings and methodology of 15 relevant articles for this study had been tabulated in Table 1.

Literature Review

Based on the literature review study, it was of importance to understand the changes in the relationship post demonetization. Based on the literature review, the authors did not find studies exploring the effects of demonetization on the Indian economy specifically from the business firm’s standpoint and the impact of demonetization on the relationship of advertising, R&D and HRDM intensities on firms’ performance. These intensity ratios have been considered as independent variables, because in this era of technology driven business, spending on R&D (Cooper, 2019; Tan & Zhan, 2017; Viete & Erdsiek, 2020), human resources (Becker & Huselid, 2006; Wang et al., 2012) and advertising and market building (Oh et al., 2017; Tajvidi & Karami, 2017) were critical elements in determining firm performance. Thus, the authors investigated the effects of advertising intensity, R&D intensity and human resource intensity on firm’s performance in the Indian business context. This was because these intensity (ratios) variables have been viewed as significant as independent variables in past literature (Andras & Srinivasan, 2003; Ho et al., 2005; Nair & Bhattacharyya, 2019; Peng et al., 2018; Sridhar et al., 2014; Sung et al., 2019; VanderPal, 2015).

When a firm had an extant base of products and services it was important to educate the customers in the market regarding the benefits of the firm offerings (Aguirre et al., 2015; Jha & Bhattacharyya, 2018; Shareef et al., 2019). It was well established in the marketing literature that advertisement often helped build customer awareness, product service recall amongst customers and finally manifested towards increased purchase (Pavlou & Stewart, 2000; Thompson & Malaviya, 2013). This finally resulted in increase in revenue for the firm. The spending on advertisement helped a firm improve its performance in the industry (Oh et al., 2017; Tajvidi & Karami, 2017). Thus, the following hypothesis was formulated:

H1a: Advertising intensity has a positive effect on firm performance.

Firms spending on R&D expenditure aided both new product development and ongoing product developments to develop new products or improve existing products (Cooper, 2019; Tan & Zhan, 2017). This would benefit the firm in the long run. Generally, firms invested significantly in new technologies for improved firm performance in the long run (Lee & Grewal, 2004; Nayak et al., 2021; Pinna et al., 2018). In the present-day context this entailed investments in emerging technologies like cloud technologies, automation, machine learning capabilities and such others to create business value in organizations (Martínez-Caro et al., 2020; Nayak et al., 2019; Verma & Bhattacharyya, 2017; Viete & Erdsiek, 2020). This would have a positive effect on the future earnings of the firm. Thus, the following hypothesis was formulated:

H1b: Research and development intensity has a positive effect on firm performance.

Human resources in an organization have been viewed as strategic resource from a classical Resource Based View point of perspective (Becker & Huselid, 2006; Jha & Bhattacharyya, 2017a; Raduan et al., 2009). This stemmed from the fact that human resources applied capabilities worked on an array of varied organizational resources including technology capabilities to create value (Jha & Bhattacharyya, 2017b; Liu et al., 2009; Mueller, 1996). Human resources integrated and steered organizational resources to generate firm gains (Becker & Huselid, 2006). Thus, organizations had to engage in training and development activities to develop the strategic capabilities of human resources (Sparrow & Pettigrew, 1987; Wang et al., 2012). Adequate and timely training and learning and development initiatives of human resources would help a firm gain better performance (Becker & Huselid, 2006; Wang et al., 2012). Thus, the following hypothesis was formulated:

H1c: Human resource intensity has a positive effect on firm performance.

The implementation of demonetization was expected to induce a short-term shock, which would have resulted in a cash shortage, thereby reduced purchases by consumers. This event and process was further expected to create an adverse impact on Indian business and economy. When short-term shocks were induced, firms tended to safeguard the revenues for short-term and meet analyst expectations than invest in R&D, advertising and HR development expenditure thereby affecting the sustainability in the long term. In the past, during economic crisis, several firms had reduced R&D and innovation activities during downswing and increased the investment subsequently to leverage the benefits during upswing (Cincera et al., 2012). The authors were motivated to understand how it had affected the three intensities post demonetization, so the following hypothesis was formulated:

H2: Post demonetization, advertising intensity, R&D intensity, and HR Intensity had a weaker impact on firm performance.

Research Methodology

Data Collection

The data required for the study was collected from Prowess database (product maintained by Centre for Monitoring Indian Economy Pvt Ltd), which contained financial statement data of listed and unlisted Indian companies. The dataset consisted of six-year panel data financial statement variables of Top 1,000 companies (ranked by Market Capitalization as on 31st March 2019) listed in National Stock Exchange for the fiscal years between 2014 and 2019. The variables included net profit, total assets, sales, R&D expenditure, salaries & wages expenses, staff training and welfare expenses, total assets, total liabilities (excluding shareholder’s equity), current assets and current liabilities. Banking, financial services and insurance industries were excluded from the sample. Similarly, companies with missing data in the key variables under discussion were also excluded. Also, the firms with zero R&D and advertising expenditure were not considered in the study. About 189 firms’ data were finally retained, resulting in 1,134 firm-year observation units. Ratios were then computed using the variables. R&D intensity, advertising intensity and HR intensity exhibited high skewness and kurtosis. Log transformation was applied to the three variables so that the variables were under acceptable limits as prescribed for such studies (Strike et al., 2006).

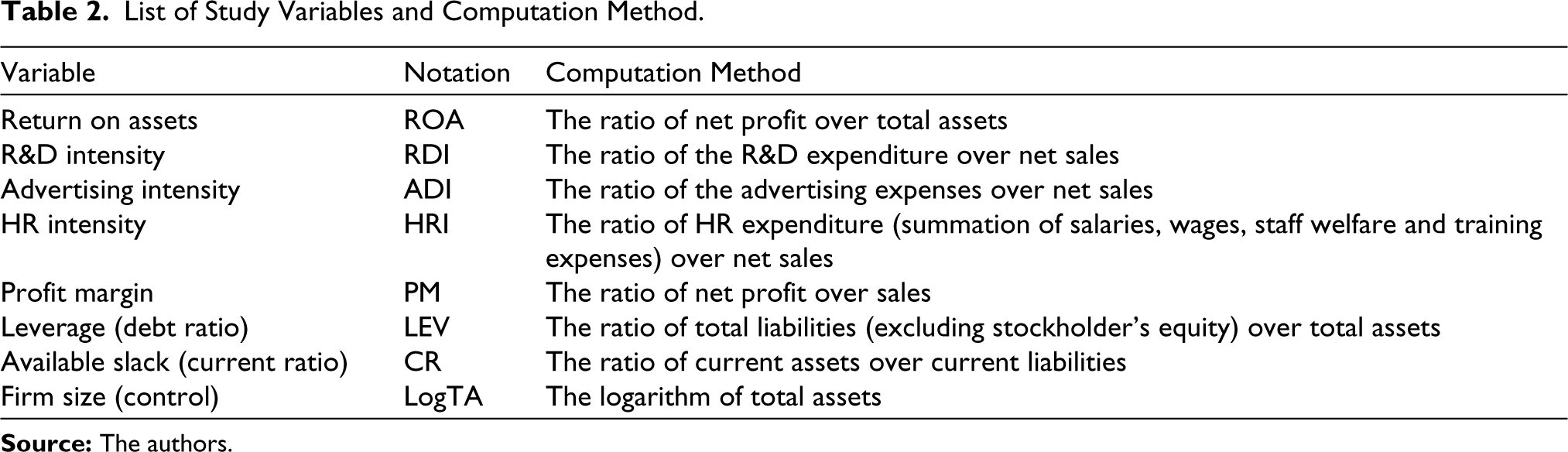

The RoA ratio was chosen as a proxy for firm performance as advocated by Eng and Keh (2007). The three intensity ratios were considered as independent variables for the study. There were several control variables included in the model. Net profit margin, leverage, available slack resources and firm size were added as control variables as prescribed for such studies (Ho et al., 2005; Lee, 2018; Peng et al., 2018). The net profit margin was known to affect the spend on R&D, advertisement and human resources by the firm (Naik et al., 2014). The debt ratio was chosen as a proxy for the firm’s leverage. The ratio of current assets over current liabilities was chosen as a proxy for available slack resources. Firm size was considered as a control variable as practiced. The logarithm of total assets was used as a proxy for the firm size. The notation and computation method of variables used in the study have been listed in Table 2.

List of Study Variables and Computation Method

Data Analysis

The model Equation (1) was built to test hypotheses H1a, H1b, H1c and H2, where θn were the corresponding coefficients. A fixed-effects panel data regression was selected over the random-effects model after performing the Hausman specification test (Woutersen & Hausman, 2019). A fixed-effects model accounted for both heteroscedasticity and autocorrelation---- was prescribed as the desired model to test while considering firm or individual-specific effects (Baltagi, 2008). Fixed-effects within group model was utilized to obtain the estimators by using mean corrected values thereby removing the unobserved effects which were constant over time. The fixed-effects model assumed strict exogeneity. This consisted of the demeaned error terms, which were uncorrelated with the demeaned covariates after averaging over the time period (Gardiner et al., 2009). Furthermore, there was absence of lagged-dependent variables among the regressors (Gardiner et al., 2009). The event study was carried out by splitting the data sets into pre-demonetization and post-demonetization. The coefficients of the equation were compared to understand the effects of the event on the dependent variable, which was firm performance.

where ‘i’ denotes firm i, ‘t’ denotes the year and ε denotes error.

Variable inflation factors were computed to determine the presence of multicollinearity. The values of these were all less than two (which was in turn well within the limit of 10), indicating the absence of multicollinearity (Draper & Smith, 1998).

Research Findings

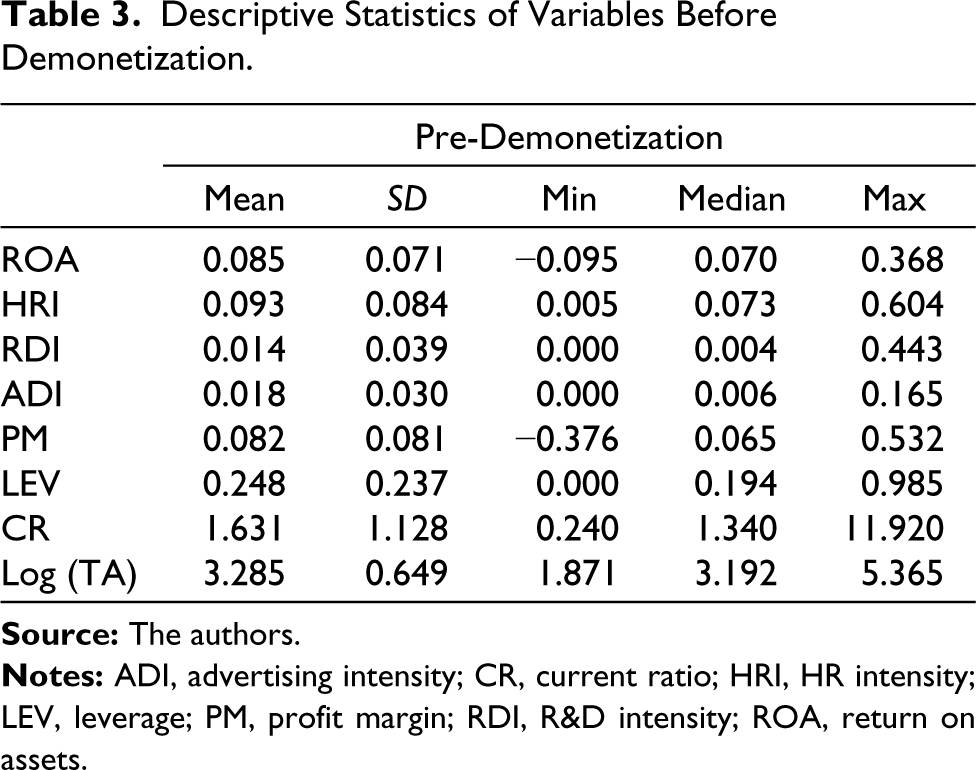

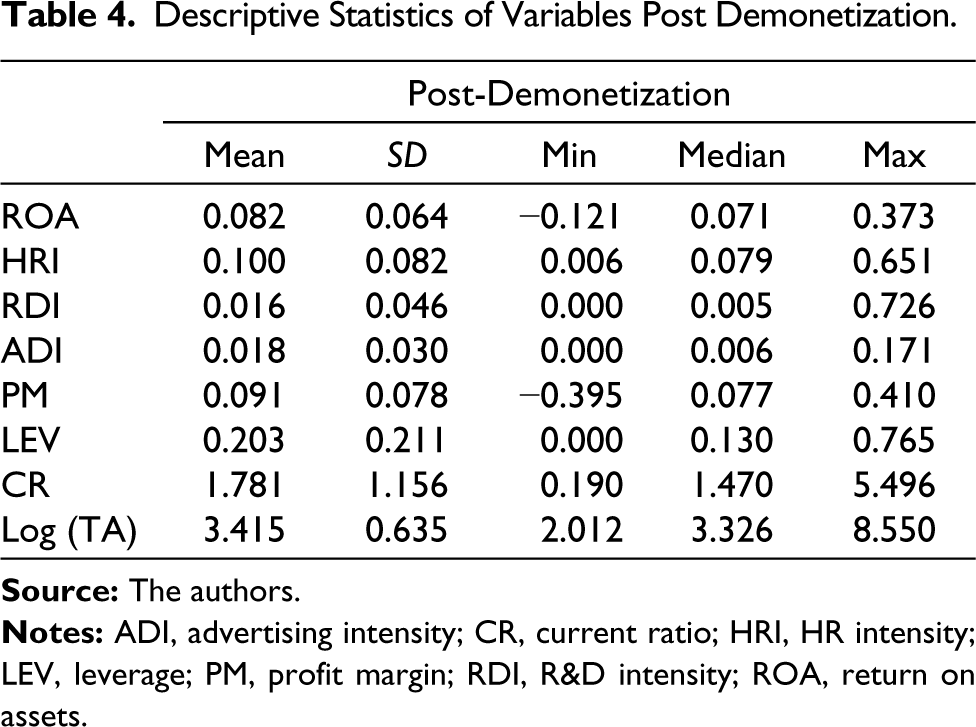

Descriptive statistics regarding pre-demonetization and post-demonetization phases has been presented in Tables 3 and 4, respectively. It was observed that the mean values of the R&D intensity and advertising intensity were 1.6% and 1.8%, respectively, while HRDM intensity was 10%. It was also interesting to note that firm mean current ratio was 1.631 during pre-demonetization phase and the mean had increased later further to 1.781 post-demonetization. The increased value indicated the emphasis of firms’ liquidity component. All the three intensities mean values had increased or remained constant. This indicated further spending by the firms on these aspects, although these reflected weaker effect on RoA.

Descriptive Statistics of Variables Before Demonetization

Descriptive Statistics of Variables Post Demonetization

Table 5 presented the Pearson correlation matrix. It was observed that there was a significant positive correlation between advertising intensity, control variables (net profit margin and current ratio), and RoA. Firm leverage had a negative relationship with RoA indicating lesser the ratio value, the better being the firm performance. The R&D intensity and HR Intensity were not significantly correlated with RoA at p < .05 (**). There was a weak correlation between the intensity ratios.

Pearson Correlation Matrix

*p < .1; **p < .01; ***p < .001.

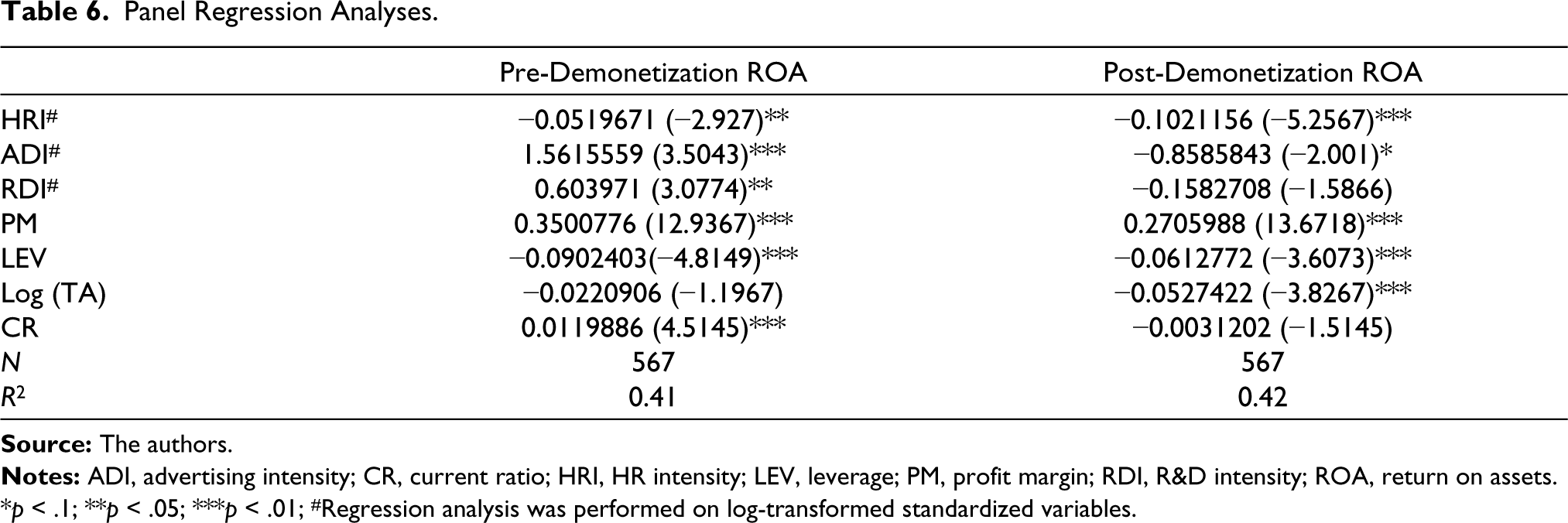

Table 6 illustrated the panel regression analysis results. Coefficients, t-values (in parenthesis), and significance levels were listed. The coefficient of HR intensity was negative pre-demonetization (θ1 = −0.0519 and t = −2.927) as compared to post-demonetization. While it was higher in the latter period (θ1 = −0.1021 and t = −5.257). R&D intensity had a positive influence on RoA (θ3 = 0.6039 and t = 3.077), while it was insignificant post-demonetization. Advertising intensity had positive effect before demonetization (θ2 = 1.5615559 and t = 3.5043), though it had reduced effect post-demonetization at significance level (p < .1). It must be noted that firm size (proxied by the logarithm of total assets) was significant (p < .01) post-demonetization.

Panel Regression Analyses

*p < .1; **p < .05; ***p < .01; #Regression analysis was performed on log-transformed standardized variables.

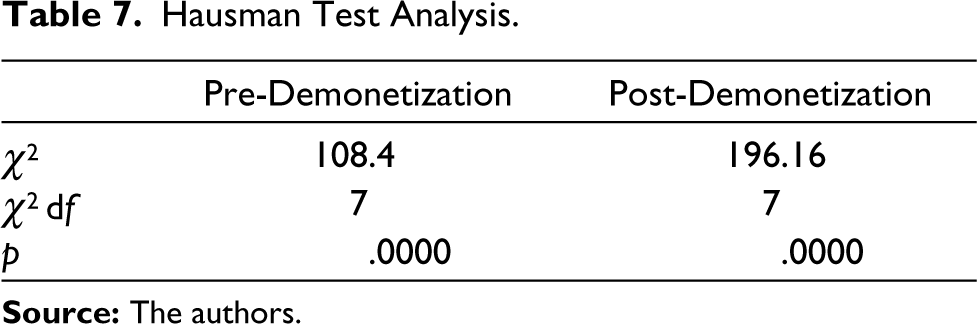

To determine the appropriate model between fixed-effects and random-effects panel-data regression, Hausman specification test (also called Durbin–Wu–Hausman test) which was most frequently used to check the validity of the random-effects assumption (Woutersen & Hausman, 2019) was applied. This was regarding the conditional independence between group-specific intercepts and covariates. The null hypothesis of Hausman test was that the estimators (fixed-effects and random-effects) did no differ substantially. When null hypothesis was rejected, the random-effects were possibly correlated with one or more regressors, therefore, fixed-effects model were chosen (Woutersen & Hausman, 2019). Table 7 indicated the results of Hausman test for both the pre-demonetization and post-demonetization panel models. The results indicated that the probability of obtaining the estimated χ2 value of 108.4 and 196.16 would be practically zero (<0.05). Therefore, the null hypothesis was rejected, and fixed effects panel-data regression model was preferred over random effects.

Hausman Test Analysis

Discussion and Conclusion

In this research study, the authors considered the effect of advertising intensity, R&D intensity and HR intensity on firm performance as well as the impact of demonetization on these three intensities. It was found that there was a negative relationship between HRDM intensity and firm performance. Therefore, the hypothesis—Human Resource Intensity had a positive effect on a firm’s performance and was rejected. While the hypothesis—Post-Demonetization, Advertising intensity, R&D intensity and HR Intensity had a weaker impact on firm’s performance (H2) and were all supported. It was also observed that R&D intensity indicated a positive relationship with firm performance, signifying the need for a firm to invest in R&D efforts and to innovate continually. While R&D intensity effected firm performance post-demonetization was insignificant, this partially supported the hypothesis that R&D intensity had a positive effect on a firm’s performance and H2. Advertising intensity also had a positive and significant effect before demonetization. This supported the hypothesis that advertising intensity had a positive effect on firm performance and reduced effect post demonetization, thus supporting hypothesis H2.

In this research, it was found that R&D intensity was significant and positive before demonetization. It was of low significance post-demonetization as the impact of R&D on short term profitability was low. This was in line with the findings in the literature (Andras & Srinivasan, 2003; Ho et al., 2005; Peng et al., 2018). It was also found that HR intensity was negatively correlated with firm’s performance contrary to the positive relationship (Singh, 2004). Advertising intensity had a significantly positive effect on the firm’s performance. This matched with the findings reported in the literature previously (Acar & Temiz, 2017; Andras & Srinivasan, 2003; Peng et al., 2018; Peterson & Jeong, 2010; Sridhar et al., 2014; Sung et al., 2019).

Firm decision-makers and managers were usually focused on short term profitability and maximizing shareholder value (Bhattacharyya & Thakre, 2021). Therefore, managers focused spending on resources that would have a higher impact on current quarter or year earnings. This approach could affect long term firm potential earnings due to less spending on resources focusing on such opportunities. This study findings would aid key stakeholders in better decision making to optimally balance the spend on human resources (including learning and development), R&D (for long term gains) and advertising (for short term profitability). Sustainability also could be ensured by leveraging innovation. Focus on advertising would create brand value while investing in R&D and human resources would create firm value. The findings would also aid managers to appropriately scale up or reduce the investments post demonetization based upon the effects of returns of an individual firm. Managers should also ensure that they planned and mitigated risks during such events.

Indian government’s demonetization initiative had the policy level perspective of reducing the impact of the shadow economy through the removal of high denomination legal tenders. The study results indicated that slack financial resources were an essential component of an economy or, more importantly, of firms. This was because slack financial resources provided firms the ability to undertake secondary but vital functions like R&D, increasing market share through advertisement, developing organizational talent base through human resource development initiatives. The impact of demonetization in the short run reduced the availability of cash or liquidity in the Indian economy. This was of much significance to firms that were of small size or already in liquidity distress. The results indicated the impact of demonetization on advertising, R&D and HRMD intensities. So, in the future, when policymakers would be shaping events like demonetization, they should think of long-term implications. This should focus on how to smoothen out the impact of such events on firms that were small or medium in size by revenue or number of employees. This study context provided a significant scope for future research on studying the impact of such events, specifically on small and medium-sized enterprises. Policymakers should not only think about the long-term impact but also heed to the requirements of businesses in the short-term. The study analysed financial data from multiple sectors. The data of only such firms which had reported or spent on advertising, R&D, human resource development and management were considered. Therefore, firms that did not have spending in any of the above three areas were omitted in the study. Although individual firm effects were considered, sector-wise effects were not considered due to less sample size available for study. The effects were estimated on annual financial data as quarterly data was not available for the parameters. The lag effects of the return on investments in the mentioned areas on the firm performance were not considered as only three financial years of data post demonetization was available. The non-linear relationship between the dependent and independent variables was not investigated in this study. Future studies could focus on these aspects. This research work should help set a datum for further studies in investigating the lag effects and non-linear relationships for events such as demonetization, especially for large emerging economies.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.