Abstract

This study explores the research on Environment, Social and Governance (ESG) investments, which have emerged as a feasible way to strike a balance between sustainability, responsibility and profitability. The article employs bibliometric technique to analyse 161 articles published on ESG investments after 2007 in Scopus database. The data were analysed using VOS viewer. There was a sudden surge in publications is ESG investments after COVID pandemic. Seven clusters emerged out of bibliographic coupling; ESG risk and return, preferences for ESG investments, ESG investments under shocks, usage of ESG information, influence of ESG rating and determinants of ESG investment. The study provides insights into the evolution of ESG investing over time and across organizations and countries. The results indicate that ESG investments provide an alternative way to manage risk-reward trade-off. The study presents the prominent countries, institutions, sources, authors and cited articles in the area of ESG investments. The findings will be beneficial for investors and policymakers interested in ESG investments.

Introduction

The world of investment has evolved from the value investing approach of Benjamin Graham through the modern portfolio theory of Harry Markowitz to the present socially responsible investing. Environment, Social and Governance (ESG) has attracted the attention of institutions and investors. The inclusion of ESG factors in the investment process has gained momentum as investors explore to enhance the sustainability of their investments (Belyaeva et al., 2020). The emergence of ESG investing represents a shift from traditional investment approaches that prioritized financial returns to a more balanced approach that incorporates both financial and non-financial factors (Belyaeva et al., 2020).

The adoption of ESG investing has been driven by a growing recognition of business operations’ impact on society, the environment and governance as part of their corporate social responsibility (Freeman, 1999). The stakeholder theory considers that the primary objective of a firm is to provide benefits to stakeholders (Freeman, 1999). ESG investing began as an ethical and religious aspect to exclude certain specific industries having an adverse impact on health, societal harmony and the environment in the 1920s. However, it gained momentum in the 1970s when the public investments started focusing on responsible investments. Environmental disasters such as the Exxon and Bhopal gas tragedy in the 1980s brought the importance of environmental hazards to the forefront.

The United Nations support for the establishment of the principles of responsible investing (PRI) in 2005 further accelerated the growth of ESG investing. The PRI initiative calls on investors to integrate ESG into the investment process, thereby enhancing the sustainability of the financial system. Investors rely on ESG scores to help them assess the suitability of corporate actions on societal norms (Suchman, 1995). ESG has been presented before United Nations as a sustainable development strategy (Lee & Kim, 2022).

ESG investing has been found to provide an alternative way to manage risk-reward trade-offs, with research suggesting a positive association between financial performance and ESG scores, firm value and stakeholder expectations for corporate accountability through ESG disclosures (Friede et al., 2015; Fatemi et al., 2015; Gold & Heikkurinen, 2018). Firms focus on maintaining social legitimacy as a strategic objective (Lai et al., 2016). In fact, good performance on ESG parameters enhances the reputation of a firm, shields it from negative news (Minor & Morgan, 2011) and helps it recover from controversy (Kim et al., 2018; Marsat et al., 2022). However, concerns have been raised about ESG investing, with some researchers suggesting that excessive expenditure on social activities based on personal considerations can decrease shareholder value and adversely affect the financial condition (Dorfleitner et al., 2020).

The crisis of 2008 has highlighted the significance of governance in financial institutions (Mele et al., 2017). The ESG disclosures and scores provide useful information for investors to take conscious decisions to contribute for ultimate good (das Neves & Vaccaro 2013). Amel-Zadeh and Serafeim (2018) observed that ESG is used for screening of investments, but negative screening was found to have no significant benefits. ESG mutual funds give better returns in periods of crisis and underperform in normal times. The asymmetric bias is prominent in funds that use positive screening (Nofsinger & Varma, 2014).

ESG stocks have gained prominence in equity portfolios globally (Daugaard, 2020) due to significant rise in investments in ESG stocks (Gao et al., 2021). ESG investments are constrained by opaqueness of ESG ratings and inconsistent disclosure requirements (Balp & Strampelli, 2022). Factor investing during uncertain times needs understanding of ESG (Díaz et al., 2021). There is no consistency in findings on ESG investment returns. Plastun et al. (2022) found that traditional portfolios returns are not significantly different from ESG portfolios in emerging and developed economies. Kwak et al. (2022) found that ESG had no significant effect on fund flow, fund volatility and sensitivity asymmetry. Halbritter & Dorfleitner (2015) investigated ESG returns in US market between 1991 and 2012 and found no significant difference in portfolios with low and high ESG rating. Jain et al. (2019) compared ESG indices with global indices for five-year period between 2013 and 2017. The study found traditional indices performance was at par with ESG index.

Kilic et al. (2022) however noticed that ESG had positive correlation with traditional investments in developing countries, but negative correlation in developed economies. Prospect theory supports an inverse association between economic resource and corporate social responsibility activities (Chari et al., 2019). ESG investments differential returns from traditional returns need to be investigated. ESG is adopted by firms as a branding strategy (Lee et al., 2022).

Due to the recent increase in research interest in ESG investments, bibliometric analyses are needed to gain insights into ESG investment research conducted in recent years. Gao et al. (2021) examined the bibliometric analysis of ESG governance. Khan (2022) performed bibliometric analyses of ESG disclosure and its impact on firm performance. Liao et al. (2021) conducted bibliometric analyses on corporate social responsibility and ESG. The bibliometric research on ESG was done by Senadheera et al. (2022) to explore themes emerging out of ESG. Growing interested on ESG as a sustainability approach leads to the relevance of evaluating bibliometric analyses on ESG investments. Pu et al. (2023) examined the implications of the knowledge economy for ESG. There is a gap in bibliometric analyses on the research of ESG investments.

There are multiple approaches and dimensions of ESG investments. The practitioners and researchers have realized the significance of ESG. In light of growth in literature on ESG, the current study makes an attempt to review the published literature using bibliometric methodology. Bibliometric approach is useful to analyse emerging themes when there is large literature base (Donthu et al., 2021). Park & Jang (2021) examined ESG models and proposed a country-specific model for South Korea. It was found that institutional investors give priority to governance and environmental factors over social factors. This study employs bibliometric techniques to analyse 161 articles published after 2007 in the Scopus database to provide insights into the evolution of ESG investing over time and across organizations and countries, identifying the leading countries, organizations, journals, authors and cited articles in the area of ESG investments.

The present study attempts to answer the following research questions (RQ).

RQ1. What is the trend of publication in ESG investments?

RQ2. Which are the major themes in ESG investment research?

Research Methodology

The study employs bibliometric method to explore the literature on the topic of ESG investment on Scopus database. Bibliometric has emerged as a method of analysis in various fields (Ellegaard & Wallin, 2015). Scopus database was selected as it is the most comprehensive database of research articles (Norris & Oppenheim, 2007). The Scopus database has 60% higher coverage as compared to Web of Science database (Comerio & Strozzi, 2019). The search was done using keywords: ‘ESG investing’, ‘ESG investments’, ‘ESG investment’ and ‘ESG Funds’. The search led to 317 documents. The documents in English language were included for further process. Total 315 documents were obtained in the first stage of exclusion, after excluding one article in Russian and one article in Korean language. The type of document was used as the second exclusion criteria. Editorial (2), review (16) and conference review (1) were excluded. Articles (252), books (7), book chapter (20), conference paper (17) were included. Total 296 articles were extracted after the second stage of exclusion. In the third stage of exclusion, a one-to-one screening was done to exclude articles not directly associated with ESG investments. A total of 135 articles were excluded in the third stage of exclusion. After the third stage of exclusion, 161 articles were selected for bibliometric analysis. The date of search was 11 April 2023. The query used for search was TITLE-ABS-KEY (“ESG investing” OR “ESG investments” OR “ESG investment” OR “ESG Funds”) AND (EXCLUDE (LANGUAGE, “Korean”) OR EXCLUDE (LANGUAGE, “Russian”)) AND (EXCLUDE (DOCTYPE, “re”) OR EXCLUDE (DOCTYPE, “ed”) OR EXCLUDE (DOCTYPE, “cr”)). The present study employs bibliometric analysis to explore the literature on ESG investments, categorizing and understanding the evolution of literature on sustainability, responsibility and profitability. The bibliometric analysis is conducted using VOS viewer, a software tool that is designed to analyse and visualize bibliometric data. The software is used to generate co-citation and bibliographic coupling maps, which are used to identify the key themes and clusters in the literature on ESG investments. The relationships between the different constituents of research are examined through science mapping. Science mapping comprises of analysis of citations, co-citations, co-authorship, co-word analysis and bibliographic coupling (Donthu et al., 2021).

Results

This section presents the trends of publications on ESG investments, the leading countries, universities, organizations and journals, and authors engaged in research on ESG investment. We also examine five science mapping using citation analysis, co-occurrence analysis, co-citation analysis, co-author analysis and bibliographic coupling to gain insight into the impact and relation between papers, authors and themes of research in ESG investments.

Citation Analysis

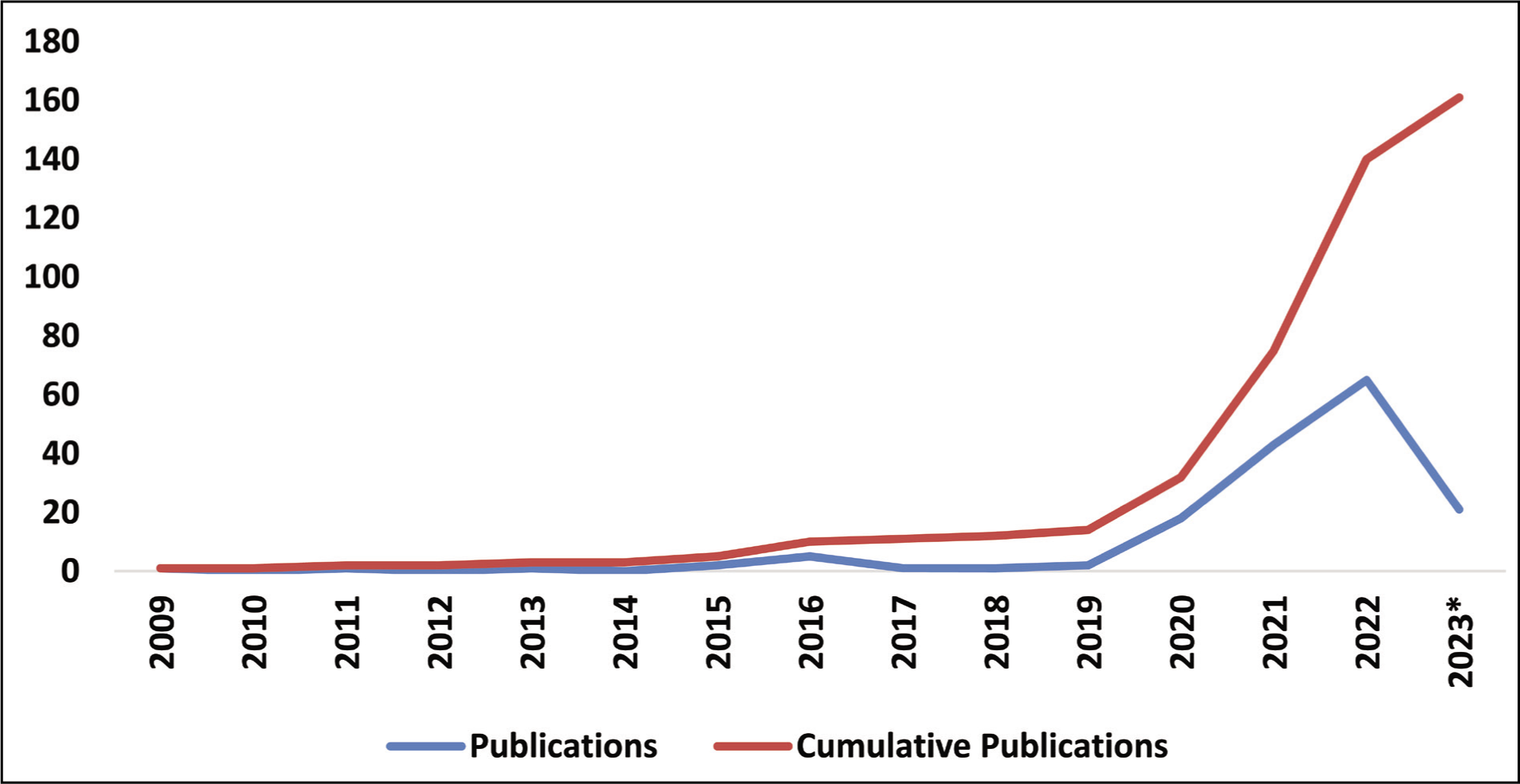

Citation is considered as a benchmark of the impact of the scholarly work (Dzikowski, 2018). The citation is a reflection of the acceptance and significance of the article (Ding & Cronin, 2011). Figure 1 depicts the trends of publications on ESG investments. The financial crisis of 2008 has highlighted the need for sustainability of the investments. ESG investment attracted the interest of the researchers towards ESG investments. The ESG investments research remained stagnant between 2009 and 2019, with hardly one publication in a year, except in 2016 which witnessed five publications. There is sharp increase in the number of publications after the onset of COVID pandemic. Only two articles were published in 2019, while 2021 and 2022 witnessed 43 and 65 article publications, respectively. In 2023, 21 articles have been published till 11 April 2023. Majority of papers have come in previous 3 years. The recent surge in publications highlights the significance of ESG investments. Thus, it needs to be explored further.

Year-wise Trends of Publications on ESG Investments.

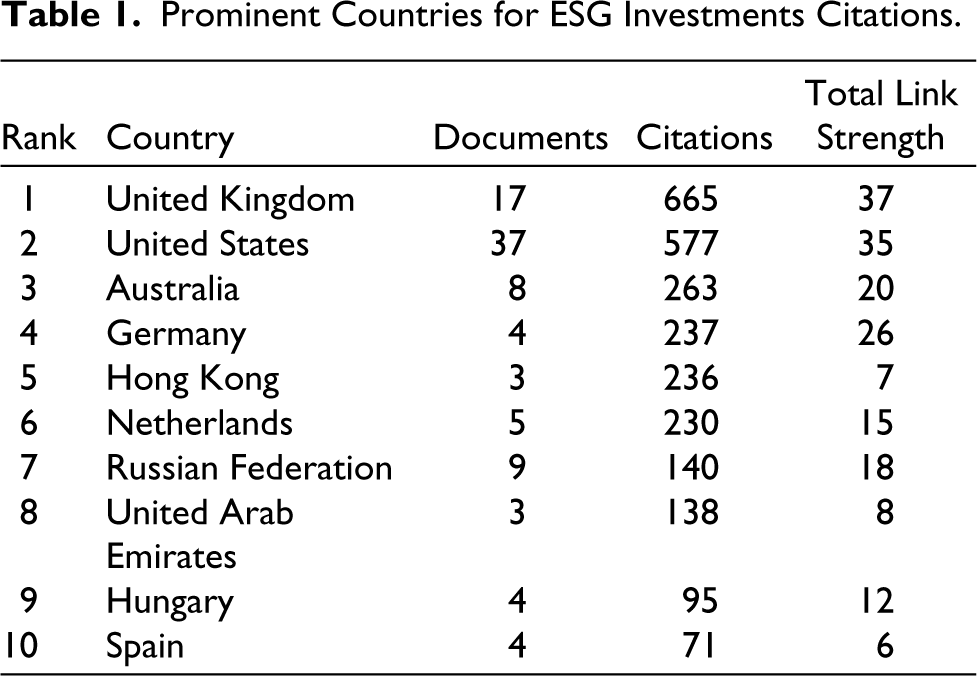

The prominent countries for research on ESG investments are depicted in Table 1. The countries were screened with a threshold of minimum 1 document and 10 citations. Out of 46 countries, 24 met the criteria. The top countries in ESG investments research citations are the United Kingdom with 665 citations from 17 articles followed by the United States with 577 citations from 37 articles. Other contributions have come from Australia, Germany, Hong Kong, Netherlands, Russian Federation, United Arab Emirates, Hungary and Spain with less than 10 publications but with more than 70 citations. In number of articles published, China is second with 23 articles and 46 citations. Italy has 13 articles with 69 citations. India ranks fifth in number of articles with 11 articles and 13 citations. The research on ESG investments is concentrated in the developed economies in terms of citations. But the research interest in China and India highlights the spread of research interest in emerging economies.

Prominent Countries for ESG Investments Citations.

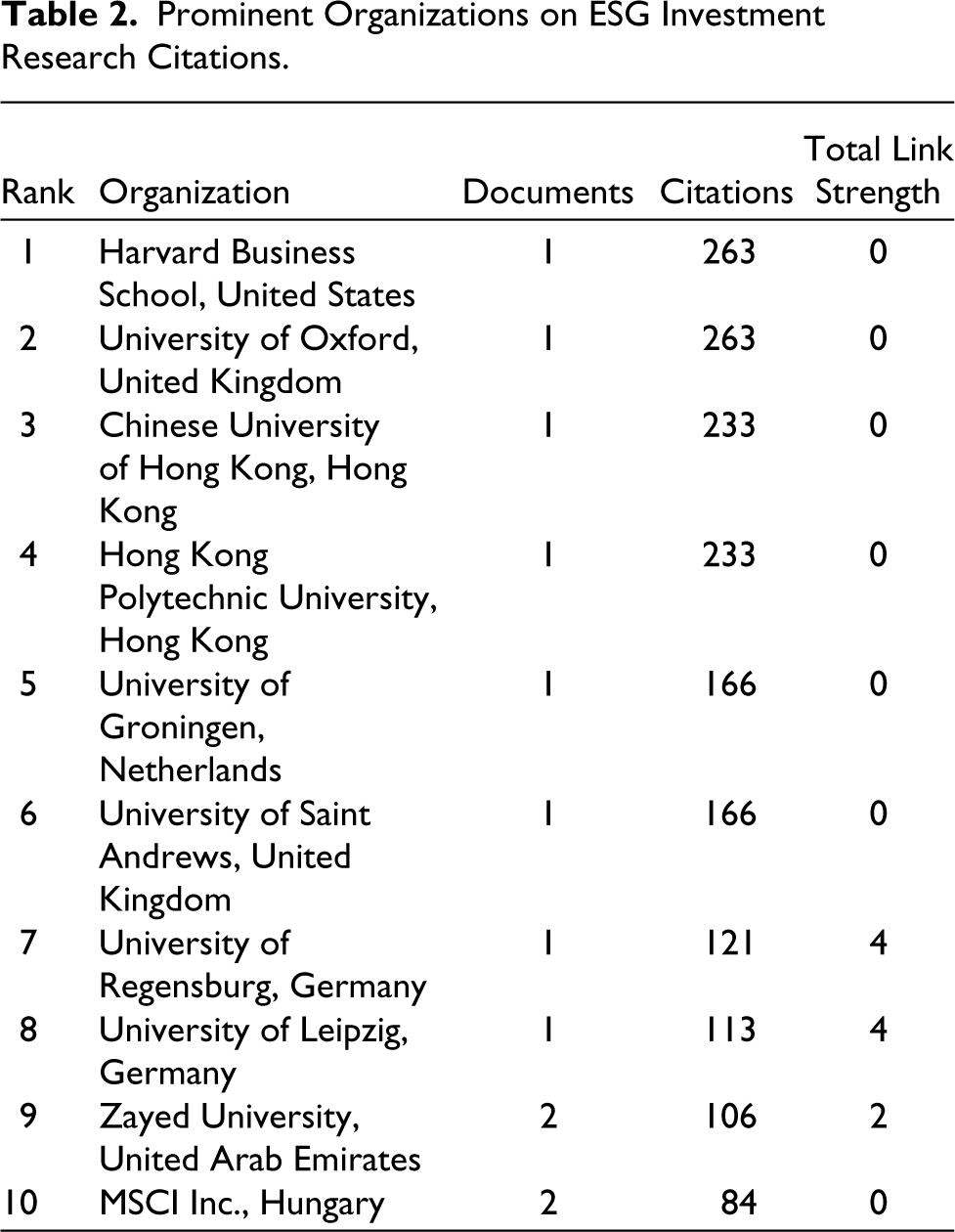

The prominent organizations are shown in Table 2. Out of 318 organizations, 24 met the threshold of minimum 1 publication and 40 citations. Out of 24, only 6 organizations were connected. Harvard Business School and University of Oxford lead with 263 citations followed by Chinese University of Hong Kong and Hong Kong Polytechnic University with 233 citations. There is no significant difference in number of publications of the organizations. The poor link strength shows that there is lot of scope for further research on ESG investments by enhancing the collaborations among organizations across the world.

Prominent Organizations on ESG Investment Research Citations.

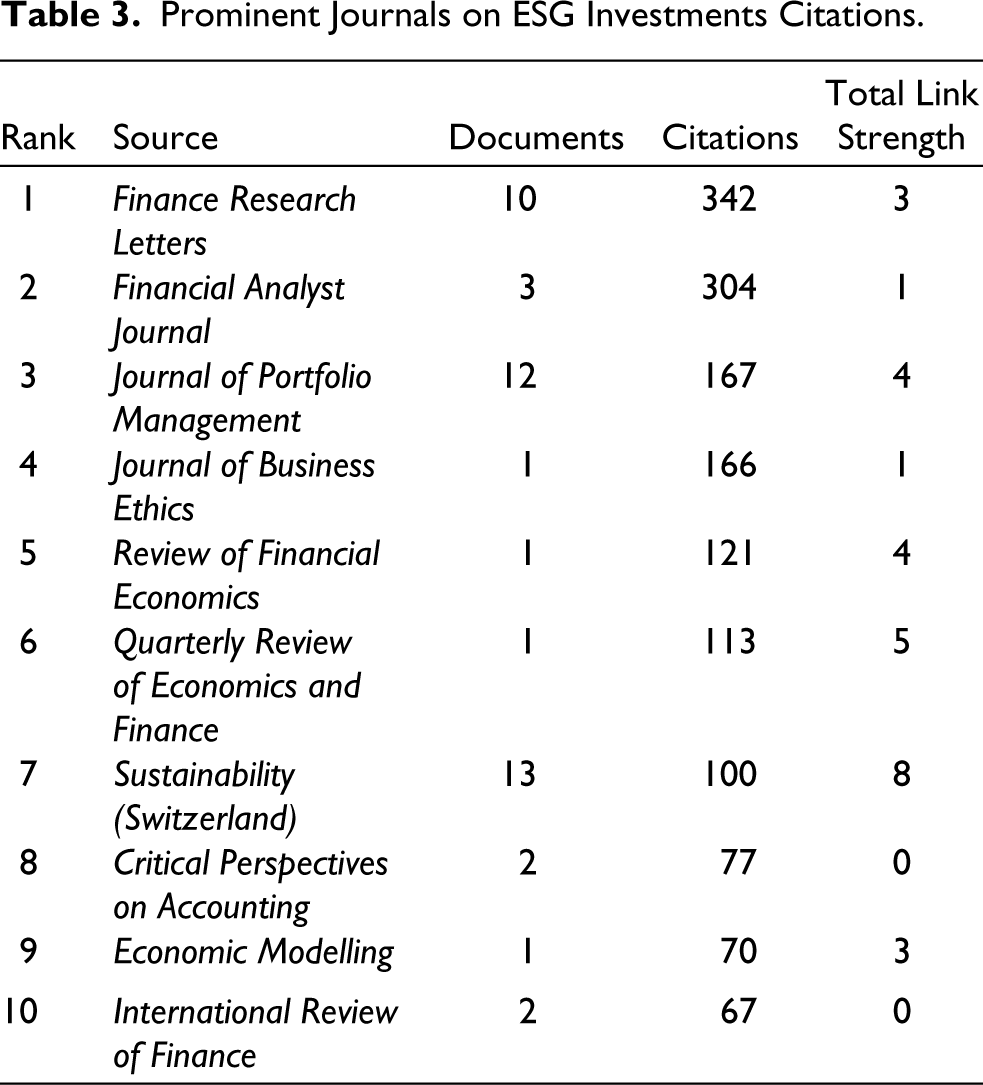

The prominent journals on ESG investment are depicted in Table 3. Out of 97 organizations, 16 met the threshold of minimum 1 document and 30 citations. Finance Research Letters is the prominent journal with 342 citations and 10 publications, followed by Financial Analyst Journal with 304 citations and 3 publications. Sustainability (Switzerland) has highest publications (13) followed by Journal of Portfolio Management (12).

Prominent Journals on ESG Investments Citations.

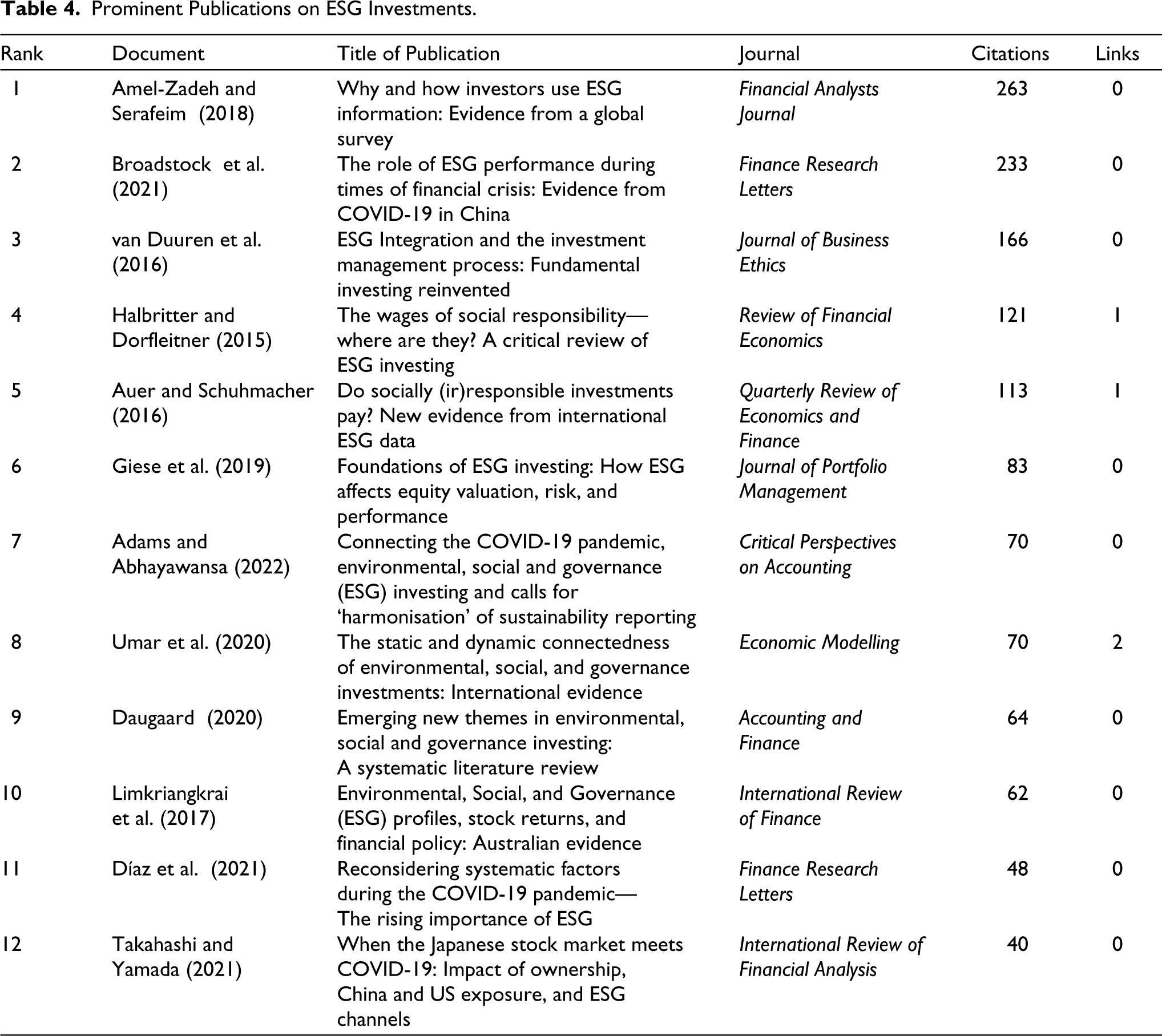

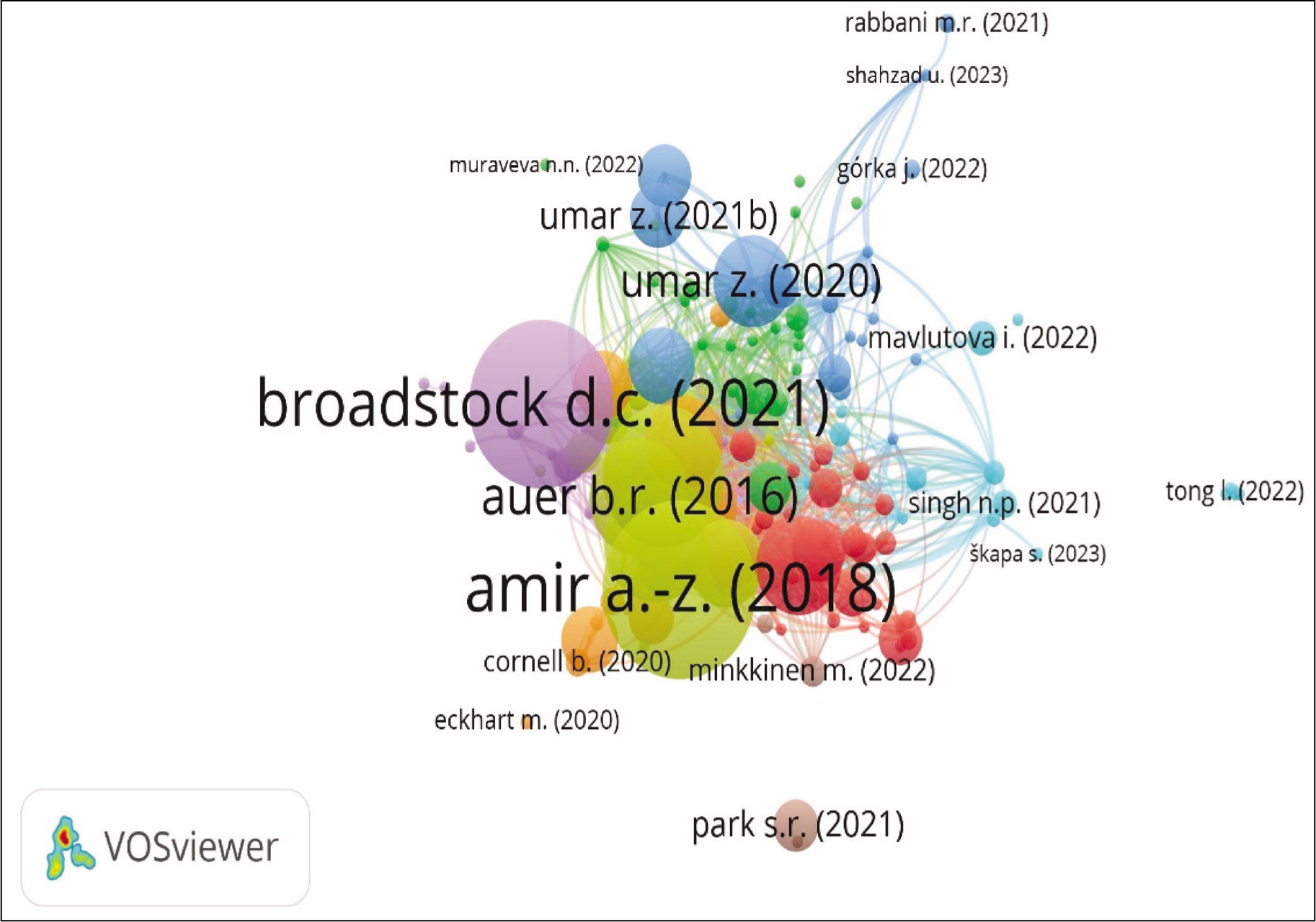

Prominent authors are shown in Table 4. Out of 370 authors, 28 met the threshold of minimum 50 citations. Out of 161 authors, 12 authors have more than 40 citations. Umar is the prominent author with three publications and 138 citations on ESG investments. Amel-Zadeh and Serafeim are prominent authors with their article ‘Why and how investors use ESG information: Evidence from a global survey’ having 263 citations. The article of Broadstock et al. (2021), titled ‘The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China’ has 233 citations. Article titled ‘ESG Integration and the Investment Management Process: Fundamental Investing Reinvented’ by Van Duuren et al. (2016) has 121 citations, followed by ‘Do socially (ir)responsible investments pay? New evidence from international ESG data by Auer and Schuhmacher (2016) with 113 citations.

Prominent Publications on ESG Investments.

Co-citation Analysis

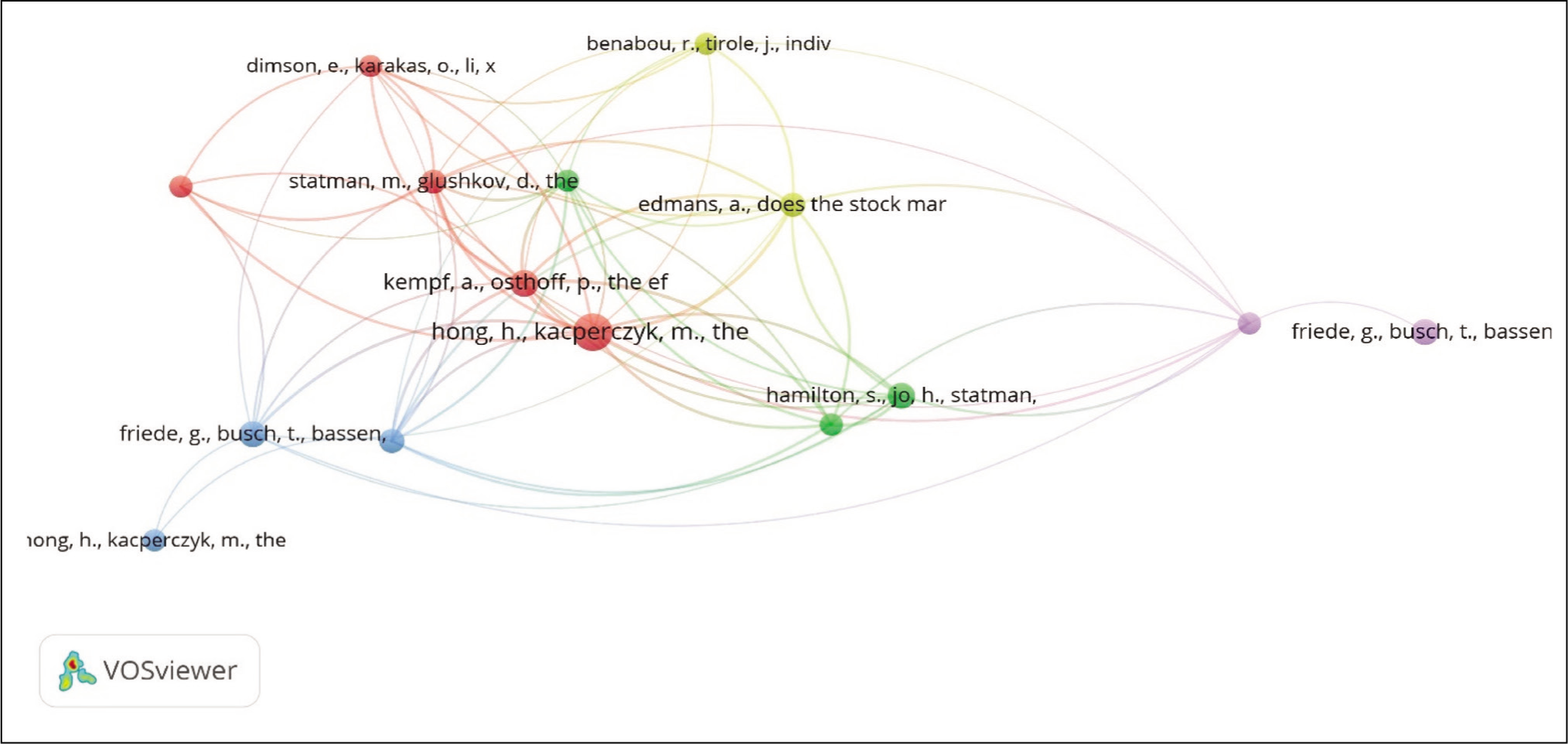

Co-citation analysis evaluates the citation strength of an article by examination of citation of group of papers, signifying research themes (Hjorland, 2013). Intellectual structure (Rossetto et al., 2018) and underlying themes are revealed by co-citation analysis (Liu et al., 2015). Co-cited papers signify association with a specific subject domain or theme (Small, 1973). It also exhibits the relation between themes, keywords and researchers (Pilkington & Liston-Heyes, 1999). However, co-citation analysis ignores the papers which are new or different from the thematic area. Co-citation analysis has been done using a threshold of six citations. Co-citation map is shown in Figure 2. Out of 7,107 references, 15 references met the criteria of 6 citations. Size of node indicates number of citations. Hong and Kacperczyk received maximum 17 citation with a link strength of 42, followed by Kempf and Osthoff with 9 citations and link strength of 40.

Co-citation Map of ESG Investments.

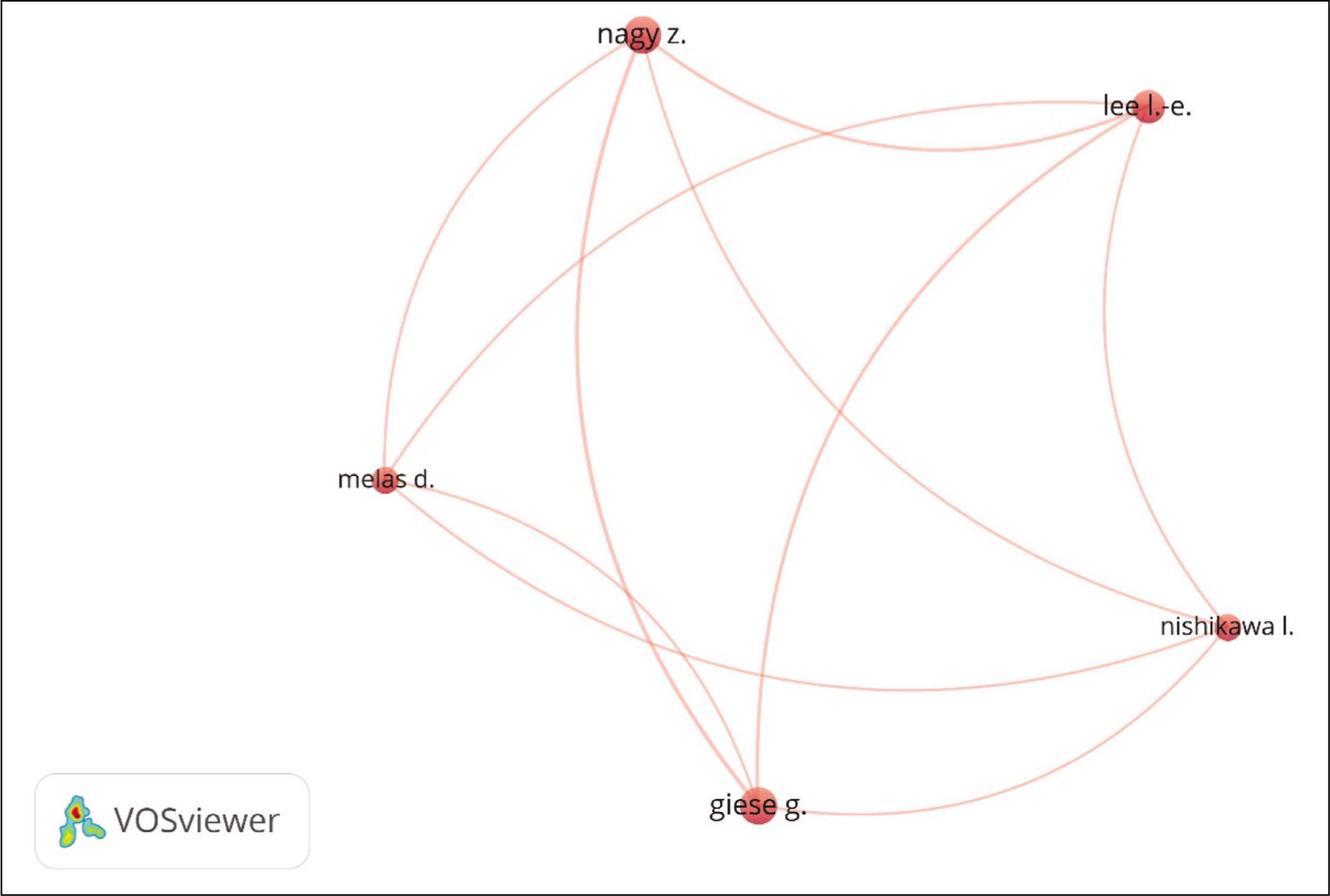

Co-authorship Analysis

Co-authorship analysis is done in VOS viewer using a threshold of minimum 2 publications and 10 citations of an author. Out of 370 authors, 27 met the criteria. Out of 27 authors, only 5 authors were connected. Full counting method was used for the analysis. The co-authorship map for authors is depicted in Figure 3.

Map of Co-authorship for ESG Investments.

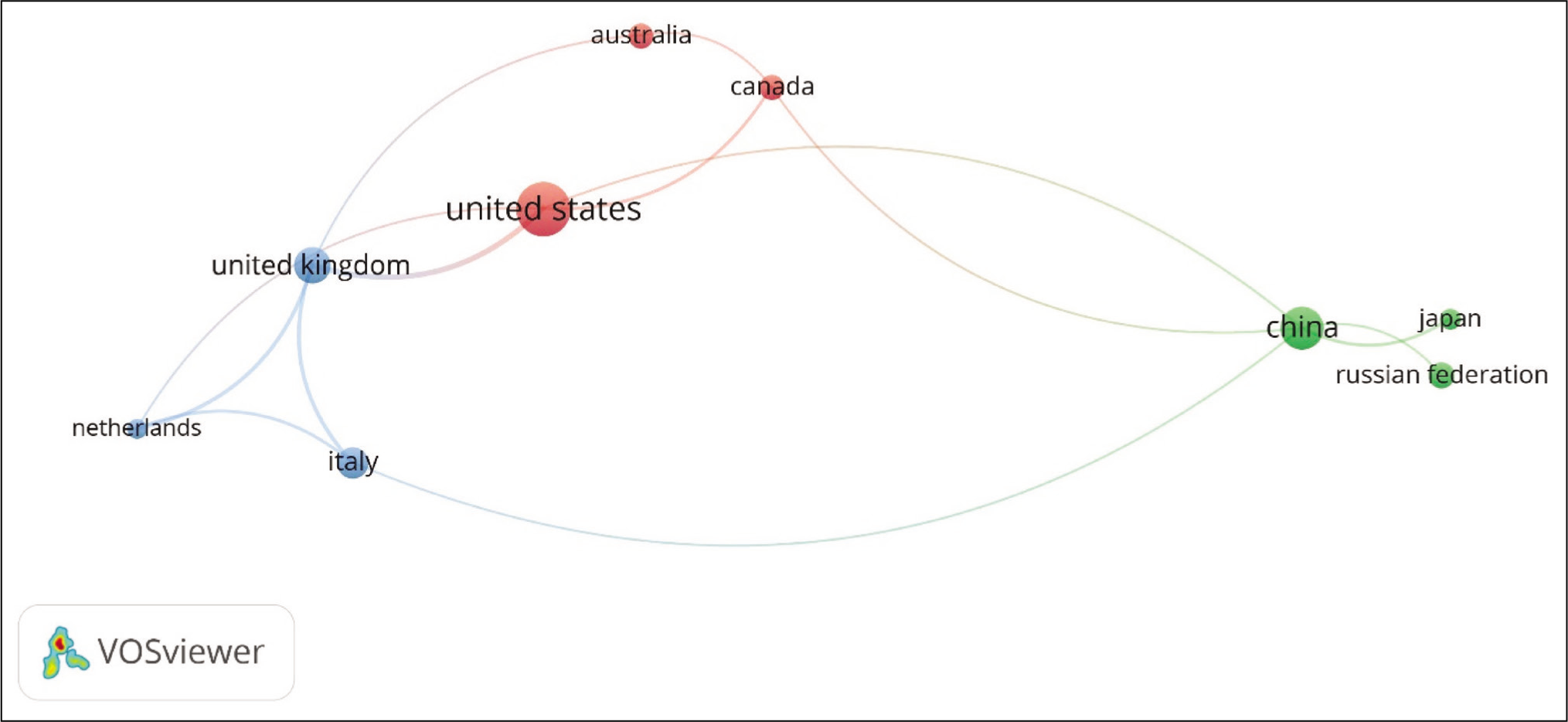

Out of 49 countries, 10 countries met the threshold of minimum 5 publications and 15 citations. Out of 10, 9 countries were connected with each other. The research on ESG investments is concentrated in developed economies as shown in co-authorship map of countries in Figure 4.

Map of Co-authorship of Countries for ESG Investments.

Co-occurrence Analysis

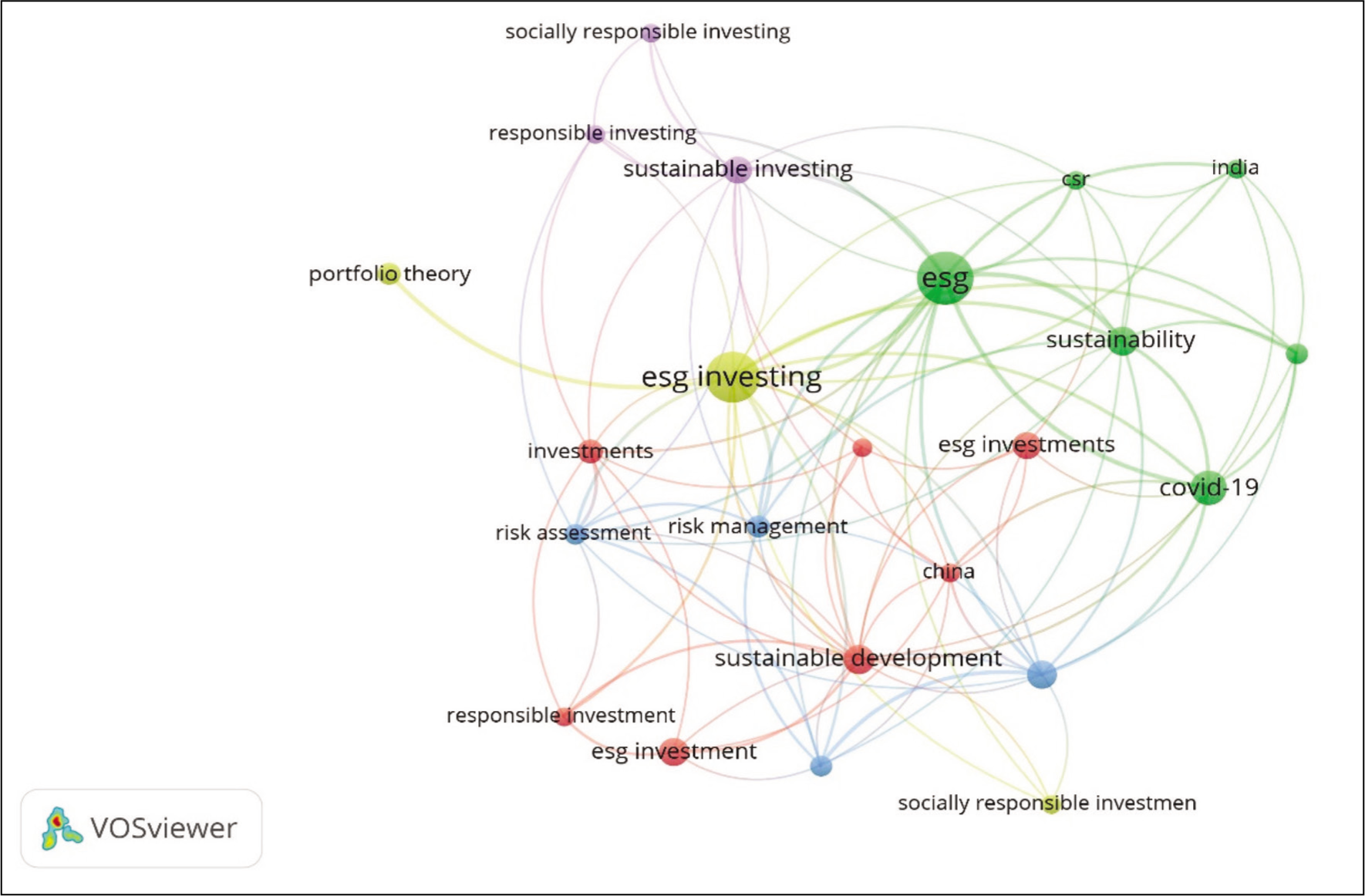

Co-occurrence analysis examines the frequently occurring phrases in the publications under considerations (Su & Lee, 2010). The co-occurrence is done using a threshold of minimum five occurrences. Out of 659 keywords, only 23 met the threshold. Full counting method was used for the analysis in VOS viewer. The co-occurrence map is shown in Figure 5. The keyword ESG has occurred 38 times, ESG investing has occurred 35 times, COVID-19 has occurred 16 times, sustainability and sustainable development has occurred 12 times each. ESG investment and investment has occurred 11 times each. ESG investments and sustainable investing has occurred 10 times each. Investments has occurred eight times, and portfolio theory and risk management has occurred seven times.

Co-occurrences Map of ESG Investing.

Bibliographic Coupling

Bibliographic coupling is a method of science mapping which assumes that any two research publications sharing common references are focused on same content (Weinberg, 1974). It shows similarity in publications of different authors based on similarity of references (Gu et al., 2021). Bibliographic coupling was done using VOS viewer, with documents as the unit of analysis. The map of bibliographic coupling is shown in Figure 6.

Map of Bibliographic Coupling on ESG Investment.

Cluster #1: ESG Risk and Return

Cluster 1 is the largest cluster with 30 articles. It is depicted in red colour. The cluster is focused on ESG risk and return. Giese et al.’s (2019) article is highly cited article in the cluster. Giese et al. (2019) investigated the linkage between ESG information and performance and valuation of companies. It was found that ESG information gets transmitted through systematic risk profile and idiosyncratic risk profile to performance and valuation of a company. Kim & Li (2021) recommended the integration of ESG for portfolio construction to lower the risk and maximize the returns. It was found that governance and social factors were more prominent as compared to environmental factors. Chen & Musalli (2020) recommended an ESG investment framework that provides optimal results of alpha and sustainability. The major types of ESG investing were characterized by the authors. A quantitative methodology for designing ESG efficient framework was proposed when the sustainability values and alpha objectives are not aligned.

Cluster #2: Impact of ESG Ratings

The cluster 2 is the second largest cluster with 24 publications. Shanaev and Ghimire (2022) examined the impact of ESG rating change on returns of US stocks for a period of five years from 2016 to 2021. The rating upgrade provides insignificant and inconsistent positive returns, while a rating downgrade provides significant negative returns. de Zwaan et al. (2015) investigated the perception of pension fund managers towards ESG investing. It was found that pension fund managers are interested in ESG investing. The lack of clarity about approach of fund house towards ESG investing is a constraint. Governance issues were found to be more prominent than social and environmental issues.

Cluster #3: Preferences for ESG Investments

Cluster 3 has 21 publications. Cornell (2021) investigated investor preferences for ESG investments. It was found that ESG preference reduces the cost of capital. ESG delivers social benefits but higher returns for investors is not certain. Adams & Abhayawansa (2022) examined the harmonization of sustainability reporting standards in light of increasing ESG investments. It was found that the needs of different stakeholders of ESG information have been ignored and there is overestimation of the expertise of IFRS. Przychodzen et al. (2016) investigated the motives of fund managers for ESG investing. It was found that ESG investing is used as a risk mitigating tool. Abhayawansa and Tyagi (2021) evaluated differences in ESG ratings of various agencies. It was observed that there is lack of transparency and understanding on ESG constructs. It was recommended that investors should prefer to use ESG constructs themselves rather than relying on ESG ratings of other agencies.

Cluster #4: ESG Investments Under Shocks

Cluster 4 comprised of 20 items. Umar et al. (2020) investigated the impact of shocks on ESG investments. It was found that under shocks, the contagion spreads from developed markets to emerging markets. Umar et al. (2021a) examined impact of COVID-19 pandemic on ESG investments. It was argued that ESG investments provide benefits of diversification and can mitigate the downside risk during global shocks. Umar et al. (2021b) investigated the influence of media coverage on ESG investments during COVID pandemic. It was observed that the effect was different in different geographies. Geographical diversification is useful for hedging. Díaz et al. (2021) examined the role of ESG for explaining returns of different industries. The authors developed ESG factor by using the spread between low and high quartile ESG ratings. It was found that ESG factor can explain the returns of industry in addition to Fama–French model.

Cluster #5: Usage of ESG Information

This cluster was made up of 20 publications. Amel-Zadeh and Serafeim (2018) investigated the rational and manner in which investors use ESG information. It was found that negative screening is not much beneficial. Returns on investment is influenced by full integration and engagement. Van Duuren et al. (2016) examined the usage of ESG information by asset managers globally. It was found that asset managers use ESG information for negative screening and red flagging to manage risk. ESG investing was found to be similar to conventional investing. The asset managers from US and European region have different perception about ESG. Auer and Schuhmacher (2016) investigated the outcomes of ESG investments across geographical territories. There were no significant differences in outcomes of active and passive stock selection on ESG criteria across all territories. The investors in US and Asia Pacific obtained ESG returns at par with market returns. Investors in Europe have accepted premium payment for socially responsible investing. Halbritter and Dorfleitner (2015) also found no significant outcomes from adoption of ESG investments as compared to traditional investments.

Cluster #6: Influence of ESG Rating

The cluster comprised of 18 publications. Broadstock et al. (2021) found that high ESG portfolios lag behind low ESG portfolios in performance. Horn (2023) evaluated the influence of ESG rating on idiosyncratic risk. It was found that ESG rating reduces the idiosyncratic risk. Bofinger et al. (2022) found that overpricing of funds is associated with higher ESG rating. D’Apice et al. (2021) observed that under conditions of reliable ESG rating, sustainability disclosures provide benefits for SRI funds.

Cluster #7: Determinants of ESG Investment

The cluster #7 was made up of 17 publications. Aich et al. (2021) investigated the determinants of ESG investments. It was observed that disasters and need for mitigating risk have led to surge in ESG investments. The trend of ESG investments will continue after the end of disaster. Mavlutova et al. (2021) found that income, education and investment experiences influence ESG investments. Silvola & Landau (2021) argued that desire to beat the markets influence investments in ESG. There is a need to overcome the limitations of bi-objective mean variance model by multi-objective portfolio optimization model (Xidonas & Essner, 2022). Zeidan (2022) examined 13,000 messages of finance professional and found that ESG is not a sufficient condition for fund managers. Poor quality of ESG data, transaction costs, strategy space are barriers for ESG investing.

Discussion

Sustainability of returns from investment has gained prominence with disruptions caused due to global shocks. Traditional approaches of investment have been questioned (Woods & Urwin, 2010). PRI have been instrumental in the development of alternative approaches of investment which incorporates sustainability issues. Sudden rise in publications on ESG investment after the onset of COVID highlights the significance of sustainability and responsibility in investments. ESG has become a broader theme with 1,336 publications in Scopus in 2022. ESG investment is emerging as an upcoming area of research within the ESG umbrella. There is need to explore ESG beyond the regulatory issue and unearth the different aspects of risk–return, investor preferences of retail and institutional investors from developed and emerging economies. US and European countries lead the research on ESG investments. Developed financial markets, wealth and political settings are driving ESG investments in these territories (Daugaard & Ding, 2022).

There is a difference in citations of the different academic institutions, but no significant difference in number of publications. Nine Universities have more than 100 citations. Except Zayed University, MSCI-Hungary, all top 10 cited universities have only 1 publication on ESG investments. Harvard Business School and University of Oxford are the prominent institutions with 263 citations. Sustainability (Switzerland) is the prominent journal with 13 publications, followed by Journal of Portfolio Management with 12 and Finance Research Letters with 10 publications. Amel-Zadeh and Serafeim (2018) are the prominent authors. The authors examined the usage of ESG information in a global survey. Broadstock et al. (2021) have examined the role of ESG during COVID crisis. Co-citation and co-authorship indicate the lack of collaboration between authors and institutions on ESG investment research.

Most frequently occurring keywords were ESG and ESG investing. Third most frequently occurred keyword was COVID-19. The surge in publications after the onset of COVID pandemic has implications for fund managers. Traditional portfolio management approaches ignore the significance of sustainability. COVID has highlighted the significance of ESG investment as a viable alternative worth exploring by fund managers. Bibliographic coupling has been used to extract the emerging research themes. Seven themes were identified by bibliographic coupling.

The largest cluster was focused on risk–return on ESG investments. Unless there is convincing evidence of superior returns on ESG, fund managers will not integrate ESG in the investment process. ESG rating emerged as the second research theme. ESG rating has created more confusion among fund managers and investors, due to lack of consistency and transparency. There is need to develop ESG rating framework that produces consistent results. Third cluster was focused on preferences for ESG investment. The role of ESG has been limited to an exclusion tool, rather than an approach for delivering superior returns. The fourth cluster was dedicated for role of ESG under shocks. Financial crisis and shocks have become more frequent. Traditional investment models need to be examined with ESG philosophy to develop approaches to integrate shocks in the investment process. Fifth cluster was focused on usage of ESG information. There are divergent findings on the usage of ESG information. Further studies are needed to develop clarity of the utility of ESG information. Sixth cluster was focused on influence of ESG ratings. The ESG ratings reliability needs to be further explored. The seventh cluster was dedicated on determinants of ESG investment. Desire to mitigate risk and earn superior return influences ESG investments. But lack of clarity on ESG ratings and consistency of superior returns have limited the integration of ESG into investment management by fund managers.

Conclusion

The study adopted bibliometric analysis to explore the field of ESG investments using Scopus database and VOS viewer. The major contribution of research publications came from developed economies, with the US being the leading country with 37 articles, followed by the UK with 17 articles. However, BRICS economies have also shown interest in ESG investments with China, India and Russian Federation having published 23, 11 and 9 articles, respectively. The crisis of 2008 and COVID have highlighted the vulnerability of the financial system amid rising concerns for people and planet. There has been a sudden rise in publications on ESG investment after COVID pandemic. A total of 78% publications on ESG investment in Scopus database have been done in period between 2020 and 2022 after the onset of COVID. ESG investment is being examined along with socially responsible investing and sustainable investing by the researchers.

ESG investment has been accepted as a mechanism for negative screening to red flag potential investments to be excluded in the portfolio. In practice, fund managers are finding it challenging to integrate ESG into investment practice due to lack of transparency in ESG ratings, ESG disclosures, ambiguity in ESG constructs. The bibliographic coupling categorized the current research in ESG investments into seven themes: ESG risk and returns, impact of ESG rating, preference for ESG investments, ESG investments under shocks, usage of ESG information, influence of ESG investments and determinants of ESG investment. There is no consistency in superiority of ESG portfolio returns over traditional portfolios. Some studies find ESG portfolios to outperform traditional portfolios while other find no significant differences.

The study contributes in the research on ESG investments. The study highlights the development in research on ESG investment publications trend and contributions of countries, organizations, journals and authors. The study presents the major research themes in ESG investments. These research themes will be useful for researchers for further investigations. The study had few limitations. The study was done using Scopus database. Therefore, the findings may not be generalizable to other databases or to the broader literature on ESG investments. Additionally, the study is limited to articles published in English, which may result in a bias towards research conducted in English-speaking countries. Future studies may broaden the search using other databases. Comparative study can also be done on performance of ESG funds across low-, middle- and high-income countries to unearth differences in trends. The findings would help investment professionals and policymakers to make better and more sustainable approaches for investments, especially in emerging economies where there is a gap in research on ESG. Collaboration among universities can also be encouraged for further research on ESG investments.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.