Abstract

According to a recent survey by McKinsey and Company, the Indian manufacturing sector is expected to touch US$ 1 trillion by 2025.This study analyses the impact of the announcement of cash dividends on the stock price returns of the manufacturing companies listed on Bombay Stock Exchange using event study methodology. Further, it explores whether the US financial crisis recession impacted average abnormal returns (AARs) in the period of study. The empirical results show that cash dividend announcements have positive AARs. Overall, the results lend support to the signalling and informational content hypotheses of dividends. The paired samples t-test indicates a significant difference in the mean values of AARs in the pre-and post-recession phases, highlighting the impact of recession.

Introduction

The corporate payout policy involves a trade-off between distributing and retaining earnings. The payout policy is important as it is closely related to and influences the other financial and investment decisions of the company. Hence, formulating a sound and prudent payout policy is most likely a challenging task for any firm. Cash dividends are probably the most important form of payout policy and a method of delivering value to shareholders. They convey a positive signal about the company to the investors and have been described as visible and qualitative indications of the corporate payout policy (Asquith & Mullins, 1983). Empirical work has shown that the market generally reacts to cash dividend announcements (Aharony & Swary, 1980; Aharony & Dotan, 1994; Bajaj & Vijh, 1995; Michaely, Thaler & Womack, 1995). However, empirical evidences have documented mixed results. Such an anomaly is defined in literature as the ‘dividend announcement effect’, or ‘the information content hypothesis’, or ‘the dividend signalling hypothesis’.

Various hypotheses have been put forward to explain the rationale for distributing cash dividends. Perhaps, the relationship between dividends and a firm’s share price is perhaps best explained by three major hypotheses: the information-signalling, the free cash flow, and the dividend clientele hypotheses. According to the information content hypothesis, dividends convey information regarding future prospects of the firm. The concept of information content of dividends was introduced by Lintner (1956) and Miller and Modigliani (1961) and was subsequently formalized by Bhattacharya (1979), John and Williams (1985), and Miller and Rock (1985) as a signalling theory. Numerous studies have supported the informational content of dividend hypothesis (Aharony & Dotan 1994; Lang & Litzenberger, 1989; Pettit, 1976; Woolridge, 1983). Cash flow hypothesis is based on agency theory as developed by Jensen (1986). The agency problem represents the separation of ownership and control of firm. According to the free cash flow hypothesis, management is reluctant to payout dividends as they want an unrestricted free cash flow in the firm. Therefore, cash dividend can be used a monitoring and disciplined mechanism over the management, thereby lowering agency cost (Easterbrook, 1984; Jensen, 1986; Jensen & Johnson, 1995). The dividend clientele effect hypothesis has emerged from different tax preferences by the investors as some investors prefer earnings to be paid out as a dividend and other prefer earnings to be retained in the firm. This tax preference by investors was formalized as the tax clientele effect by Miller and Modigliani (1961) and Black and Scholes (1974). Among the numerous studies in literature, the strongest support in explaining the market reaction to cash dividend announcements is the signalling hypothesis (Woolridge, 1983).

Although the impact of cash dividend announcements has been examined extensively, its impact in the manufacturing sector (especially in India) is relatively ignored. Further, the US financial crisis has been reported to be a significant event not only in the US but globally. Hence, the uniqueness of the study is in analysing the pre-and post-recession abnormal returns accruing to the firms (if any) in the manufacturing sector of BSE 500 indexed companies. The purpose of the paper is to examine the impact of cash dividend announcements and through that the signalling and information effect associated with such announcements in the Indian corporate enterprises.

For better exposition, this paper is divided into seven sections: Section 1 contains the introduction. Section 2 reviews the pertinent literature. Section 3 presents the research gaps and discusses the rationale of the study. Section 4 contains the objectives and the research hypotheses. Section 5 describes the scope and research design. Section 6 presents and analyses the results. Section 7 contains concluding observations and implications of the study.

Literature Review

Literature is rife with studies on various aspects of the dividend decision. Numerous research studies have been conducted to measure market response to announcement of cash dividends and have analysed shareholders value creation globally. The influential work by Ball and Brown (1968) and Beaver, Clarke, and Wright (1979) using event study was extended by many others (Aharony & Swary, 1980; Kalay & Loewenstein, 1985; Woolridge, 1983). Several empirical studies have investigated the informational content of dividend announcements. The impact of dividend announcement has also been tested on various other stock markets of the world with mixed results (see Akbar & Baig, 2010, on Karachi stock exchange; Capstaff, Klaeboe, & Marshall, 2004 on Oslo stock exchange; Hossain, Siddiquee, & Rahman, 2006, on Dhaka stock exchange; Kaleem & Salahuddin, 2006, on Lahore stock exchange; Lyroudi, Dasilas, Ginoglou, & Hatzigayos, 2007, on Athens stock exchange; Odabasi, 1998, on Istanbul stock exchange, etc.).

The research evidences by Gonedes (1978) and Watts (1973) reported that unexpected dividends provided little information to the market. However, some studies conducted later concluded that unexpected dividend changes produced significant announcement effects (Aharony & Dotan, 1994; Asquith & Mullins, 1983; Dyl & Weigand, 1998; Michaely et al., 1995).

Considerable research shows that there is a positive relationship between stock prices and dividend changes (Asquith & Mullins, 1983; Below & Johnson, 1996; Benartzi, Michaely, & Thaler, 1997; Denis, Denis & Sarin, 1994; Dhillon & Johnson, 1994; Lonie, Abeyratna, Power, & Sinclair, 1996; Nissim & Ziv, 2001; Urooj & Zafar, 2008; Yilmaz & Gulay, 2006). Their results were consistent with earlier empirical studies from the US, the UK, and the other developed markets. These empirical evidences support the use of dividends as signalling mechanisms with positive returns implying that investors take this event as good news (Aamir & Shah, 2011; Baker, Dutta, Gandhi, & Saadi, 2007; Dasilas, Hughes, 2008; Kale, Kini, & Payne, 2012; Koch & Sun, 2004; Lyroudi, & Ginoglou, 2008; Sylvester, 2015). Despite this general finding, some mixed results remain. In contrast, studies have also documented that cash dividends have no discernible association with stock returns and this is consistent with dividend irrelevance arguments. These studies confirm that changes in cash dividends have little incremental value (Basse, 2013; Benartzi et al., 1997; DeAngelo, Deangelo, & Skinner, 1992; Kadioglu, 2008; Qudah & Badwai, 2015; Peterson, 1996). Past studies have also indicated that an announcement of cash dividend increase (decrease) was accompanied with a rise (fall) in share prices and no change in share prices when dividends were not changed. Similarly, when a firm announces dividend, or omits such a payment, these announcements have significant effect on the share prices (Michael et al., 1995).

Indian Evidences

There is a paucity of empirical studies examining the dividend signalling hypothesis in the Indian context especially in the manufacturing sector. Chander, Sharma, and Mehta (2007) studied the stocks of the Bombay Stock Exchange (BSE) and found positive average abnormal returns (AARs) around and after the dividend announcement and negative returns prior to the dividend announcements. Similar results were reported by Mallikarjunappa and Manjunatha (2009). Lukose and Rao (2010) found significant wealth effects around dividend changes, proposed by the signalling models. The study of Taneem and Yuce (2011) focused on the information content of the dividend and observed favourable reaction toward companies that increased their dividends and negative toward companies that decreased their dividends. The results were consistent with empirical findings by Sharma (2011) and Kumar and Raju (2013) where cash dividend announcements conveyed a positive and stronger future outlook for the company. The findings also documented that dividend announcements possessed signalling property. Differing with the above results, few studies also reported absence of signalling effect of dividend increase/decrease announcements (Chen, Hsiang & Huang, 2009; Elfakhani, 1995; Savita, 2014; Sharma & Pandey, 2014) did not find any evidence to support the no signalling effect of dividend increase/decrease along with financial results announcement on the share prices of companies.

The literature review indicates (to the best of our knowledge) that there is no in-depth study (covering the pre-and post-recession period) showing the impact of cash dividend announcements on returns to the shareholders of listed corporate enterprises engaged in the manufacturing sector in India.

Research Gaps and Rationale for the Study

Considering the role of manufacturing sector in driving the overall growth of the economy and ultimately the stock markets, research in the Indian context has relatively neglected this area. Further, while reviewing the earlier studies, it was observed that these studies had some major limitations with respect to study period, sample size, sample characteristics, and methodology used. Further, it has also been noted that these studies have not isolated the announcement effect of dividends from other announcements which occurred on the same day of dividend announcement. Correspondingly, only a few studies have examined the impact of ‘pure’ cash dividend announcements (Section 5.4) especially in Indian context (Chander et al., 2007; Sharma, 2011; Sharma & Pandey, 2014). This is perhaps the first attempt (to the best of authors knowledge) to analyse the pre-and post-recession impact of US financial crisis on cash dividend announcements in India. An analysis of this nature (to the best of authors’ knowledge) has not previously been undertaken. This study is a modest attempt to fill these research gaps.

The era of liberalization, privatization, and globalization has intensified competition for the firms. The finance managers of Indian companies are increasingly becoming proactive in formulating dividend policy which can maximize the wealth of the shareholders. The empirical evidences in literature support the notion that managers ‘listen to the market’ since corporate events and changes in corporate policies are sensitive to market reactions. With this view point, the objective of the study is to gain insight into the cash dividend announcement effects and how it influences the risk-return profile of the investors. This, then, constitutes the rationale of the study.

Objective and Research Hypotheses

The objective of the present study is to examine the stock price behaviour of Indian stock markets on and around cash dividend announcements. This study is a hypothesis-testing research study. The following null hypotheses have been formulated to achieve these objectives:

H1: There is no AAR during the event window due to announcement of cash dividends. H2: There is no cumulative average abnormal return (CAAR) during the event window due to announcement of cash dividends.

Further, the impact (if any) of recession on the returns is analysed.

Research Design

Scope of the Study

The study is limited to BSE 500 index companies of the BSE based on their market capitalization. These companies represent nearly 93 per cent of the total market capitalization on BSE and cover 20 dominant sectors of the economy. The scope of the study is limited to 236 companies engaged in the manufacturing sector. 1 This paper analyses cash dividend announcements for manufacturing firms listed under the BSE 500 index.

The Indian capital markets present a unique case in the study of cash dividend announcements. According to the various survey reports, the next two decades belong to India, and the country is well on its way to become the most attractive destination for international investors. India has been ranked as the fourth most competitive manufacturing nation compared to China, US, and Germany. Further, the Global Manufacturing Competitiveness Index of 2013 has positioned India as the second manufacturing nation after China, by 2018. 2 Unlike many other emerging stock markets that focus heavily on one or two industry sectors, the Indian stock market provides investment opportunities across a wide range of sectors. The manufacturing sector in India has undergone various phases of development over time. It is witnessing a wave of growth. The progress of the manufacturing sector directly affects and sets the overall tone of the other sectors of the economy. This is the reason for the chosen sample.

Event Study Methodology

Event study methodology is one of the most popular research methods to measure the event’s economic impact by observing security prices around an event. Event studies help in predicting how the security will perform in response to the announcement of an event. The event can have either a positive or negative effect on the value of the security. The most successful application of event studies in finance have been around corporate events such as mergers and acquisitions, splits, stock dividends, bonus shares, amalgamation etc. With this background, the impact of cash dividend announcements has been studied using event study methodology (Bowman, 1983; Brown & Warner, 1985; Mackinlay, 1997; McWilliams & Siegel, 1997; Peterson, 1989). The stock returns behaviour around cash dividend announcements is likely to enable researchers to analyse the informational content and the applicability of signalling hypothesis in India. The rationale of using this methodology lies in assessing the economic impact by observing security prices around the event over a relatively short time period (Mackinlay, 1997). The present study is carried out within the framework of this literature, analysing differences in information conveyed by cash dividend announcements.

The event study methodology is a widely employed methodology to estimate abnormal returns (Brown & Warner, 1985; MacKinlay, 1997). It involves defining the event of interest, the event window, the estimation window, and the estimation model (Bowman, 1983). The methodology uses ‘market model’ for calculating the expected (normal) return. The difference between the daily return and expected return on a particular day is called ‘abnormal return’.

5.2.1. Event of Interest

The event of interest in this study is the announcement of cash dividend. The announcement date for the purpose is defined as the first official statement on cash dividends made by the executive board of the sample firms.

Event Window

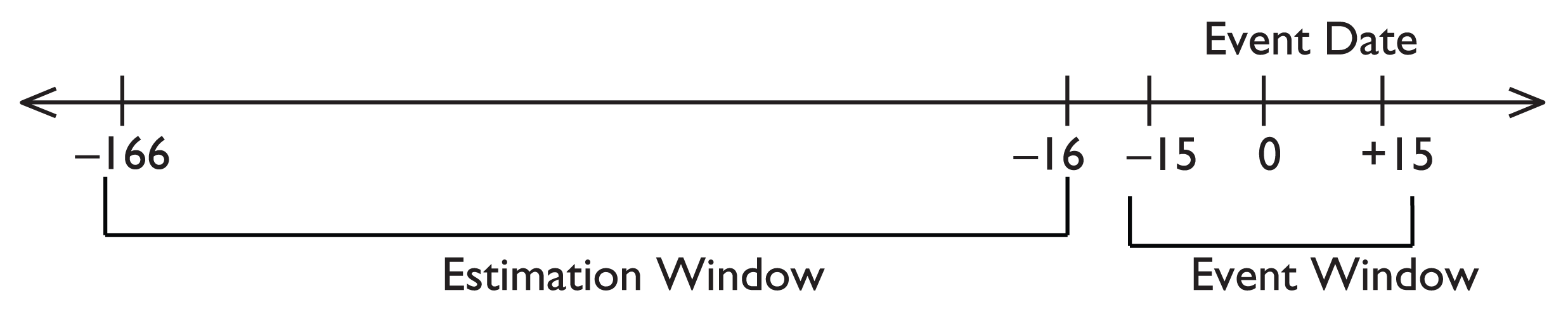

The event window examined is 31 days, that is, 15 days prior to the announcement date (AD–15) to 15 days after the announcement date (AD+15) along with the announcement day itself. The announcement day (AD) is denoted as day zero. To conduct a more in-depth analysis, the event windows of varying periods (less than 15 days as well as greater than 15 days) have also been used.

Estimation Window

An estimation window is the period used for estimating the expected returns. For the present study, the estimation window is from the day –166 to the day –16 (form 16 to 166 days prior to the event window), thus comprising 150 trading days. This ensures that the estimates of the normal return are not influenced by event-related returns. Figure 1 depicts the event window and estimation window.

The estimation model is used to estimate expected returns. The value weighted market index—BSE 500 has been used for regression. The regression equation is given as per equation 1:

where α and β are the estimated parameters, Ri,t is the expected return on stock i at time t, Rm,t is the corresponding return on the BSE 500 index, and Ei,t is the error term. The abnormal return (AR) for each day for each firm is then obtained as per equation 2:

The abnormal return for all the firms on each day of the event is then aggregated and averaged to obtain the AAR. Given N for the number of the companies, the AAR as per equation 3:

To ascertain the accumulated impact of the event during a particular time period, CAARs are calculated. The CAAR is defined as the sum of daily AARs for the pre-specified period starting at t1 through time t2, also called the event window (t1, t2), given by equation 4:

The standard deviation is estimated by the time series of AARs given by equation 5:

where

and

The test statistic for AAR on day t during the event period and for CAAR for the event window (t1, t2) is given by equations 6 and 7, respectively:

The cash dividend announcements for the period of 10 years (1 April 2003 to 31 March 2013) were collected from Prowess® database maintained by the Centre for Monitoring Indian Economy (CMIE) and from BSE website. The other secondary sources used to substantiate any missing data were the websites of Money Control, Economic Times, and the Capitaline® database. The entire set of data has been analysed using Statistical Package for Social Sciences (SPSS®) and Microsoft’s Excel® spreadsheets. To study the trend of abnormal return and its implications, measures like mean, median, standard deviation, skewness, kurtosis, minimum, and maximum abnormal returns have been computed.

The period of the study is of particular importance because of the recession (originating due to the American financial crisis) that impacted the world economy toward the second half of 2008. (The United Nations Council on Trade and Development, [UNCTAD]) 3 . The 10-year time period is divided into two sub-periods/phases: the first five years, with effect from 1 April 2003 to 31 March 2008 (for brevity referred to as 2003–2008) are referred to as Phase 1 and the next five years, with effect from 1 April 2008 to 31 March 2013 (for brevity referred to as 2009–2013) are referred to as Phase 2.

Description of Sample Characteristics and Sample Selection Criteria

There were 236 companies which constituted manufacturing sector (Table 1) under the BSE 500 index. Out of these, the announcement data were not available for eight companies, thereby reducing the sample size to 228 companies. The constituents of the manufacturing sector (classification as per the CMIE Prowess® Database) are provided in Table 1.

Composition of the Sample Companies

Composition of the Sample Companies

The study evaluates the impact (if any) of ‘pure’ cash dividend announcements. For the purpose, ‘pure’ announcements implies those dividend announcements around which certain other announcements should not have taken place during the chosen event window (listed as points 1 to 4). Therefore, event windows with the effect of ‘contaminating’ events are excluded. Contaminating events can include announcement of merger, announcement of a new product, announcement of unexpected earning etc. Any of these events might have an impact on the share price of these firms during an event window. Hence, it becomes imperative to exclude these events to have credibility of the empirical findings. Hence, the announcement is included in the sample only when the following criteria are met as suggested by other studies (Mackinlay, 1997; McWilliams & Seigel, 1997):

The company must have been traded on the BSE for two years prior to the announcement of cash dividend. The shares on which the cash dividends are announced are ordinary common shares and the listed firms are non-financial firms. The shares of each constituent company should have been traded for at least 181 days and their daily price information should be available. There should have been no announcements of stock dividends and stock splits, bonus issue and share repurchase mergers, acquisitions, amalgamation, joint venture, capital investment, substantial orders from prestigious customers, or other such financial events during the event window. Some companies provide this information to BSE expecting a positive change in the stock prices of the company. Such events would not be considered for the analysis. There should have been no announcements of financial results during the event window.

Starting from initial population of 2,347 cash dividend announcements, sample selection reduce the data set to 605 announcements made by 228 companies

Empirical Results

Price Reaction Results

Table 2 presents the relevant data related to abnormal returns during the study period of the sample companies. It contains AAR, median abnormal returns (MAR), and CAAR and their corresponding t-statistic values around the 31 days event window. It also describes the characteristics of these returns in terms of standard deviation, minimum, maximum, skewness, and kurtosis. MAR is a return separating the higher half of a sample from the lower half during the event window.

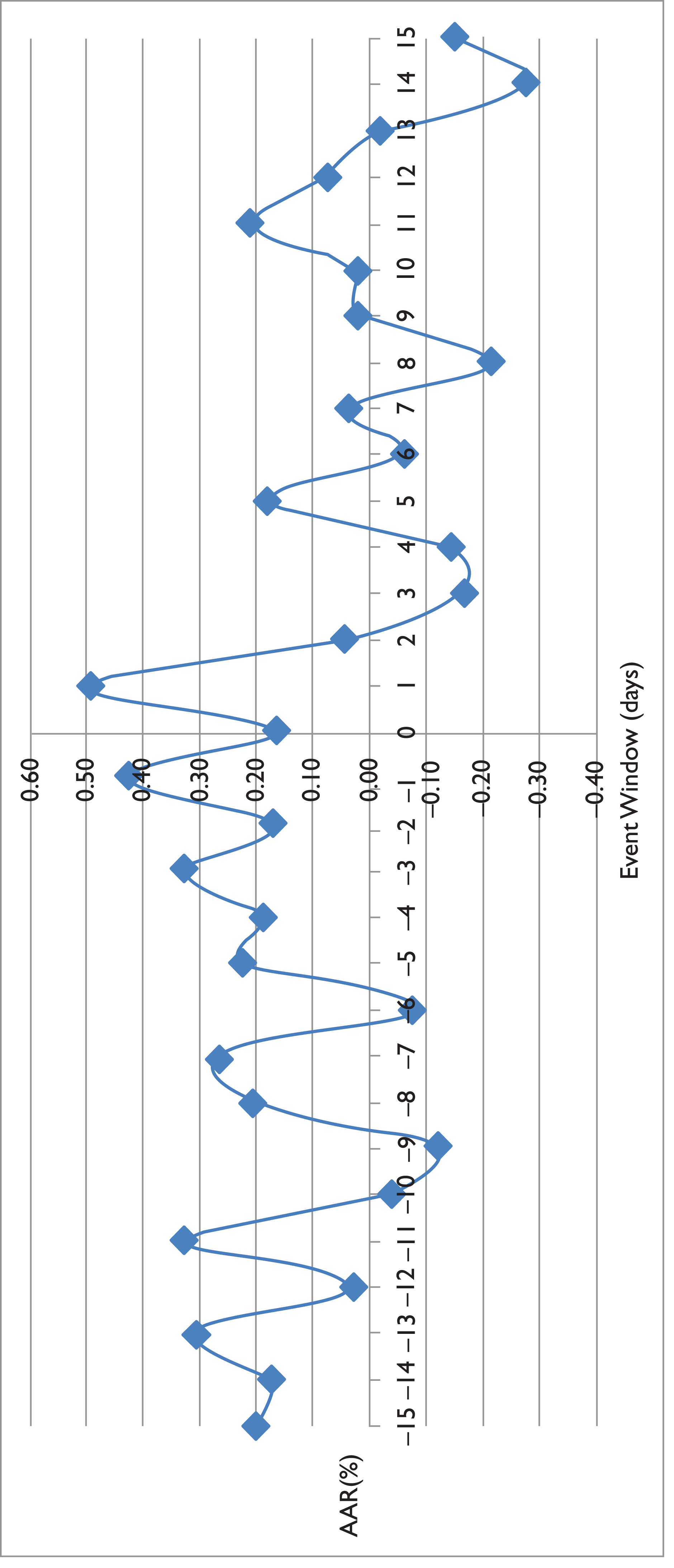

The results indicate that the announcements of cash dividend are beneficial to shareholders in terms of providing abnormal returns. The AARs are within the range of –1 to +1 per cent for most of the days. AAR on announcement date (AD) and one day before (AD–1) and after (AD+1) announcement is positive which depicts the positive reaction of investors to the dividend announcement.

The maximum AAR of 0.67 per cent can be observed one day after the announcement day (AD+1). It is a significant return for the investor (at 1 per cent significance level). Thus, it is evident from Table 2 that hypothesis (H1), namely there are no abnormal returns to the shareholders of manufacturing companies on the announcement day is rejected at 1 per cent significant level. In operational terms, it implies that there are significantly different announcement effects on the stock prices of the sample companies. It is pertinent to note that the AAR falls on the seventh day post-announcement of the cash dividends. This drop in AAR may be attributed to ex-dividend date associated with the announcement of cash dividends, when a stock price usually drops by the amount of the expected dividend.

Standard deviation varied significantly across the sample during the event window indicating high degree of volatility within the sample. Skewness and kurtosis figures report that the positive abnormal returns are small and short lived. Based on statistics contained in Table 2, it is reasonable to conclude that cash dividend announcements significantly create short-term wealth on the announcement day to the shareholders. The mean returns through out the window have a normal distribution, tested through one-sample Kolmogorov–Smirnov test. In addition, Figure 2 graphically depicts the value of AAR corresponding to each day of the event window during the ten year time period (2003–2013). It presents the trend of AAR and provides support to our findings.

Average Abnormal Return (AAR), Median Abnormal Return (MAR) and Cumulative Average Abnormal Return (CAAR) and their Corresponding t-statistic Values on and around Cash Dividend Announcements during the Period 2003–2013

Average Abnormal Return (AAR), Median Abnormal Return (MAR) and Cumulative Average Abnormal Return (CAAR) and their Corresponding t-statistic Values on and around Cash Dividend Announcements during the Period 2003–2013

*Significant level at 1 per cent.

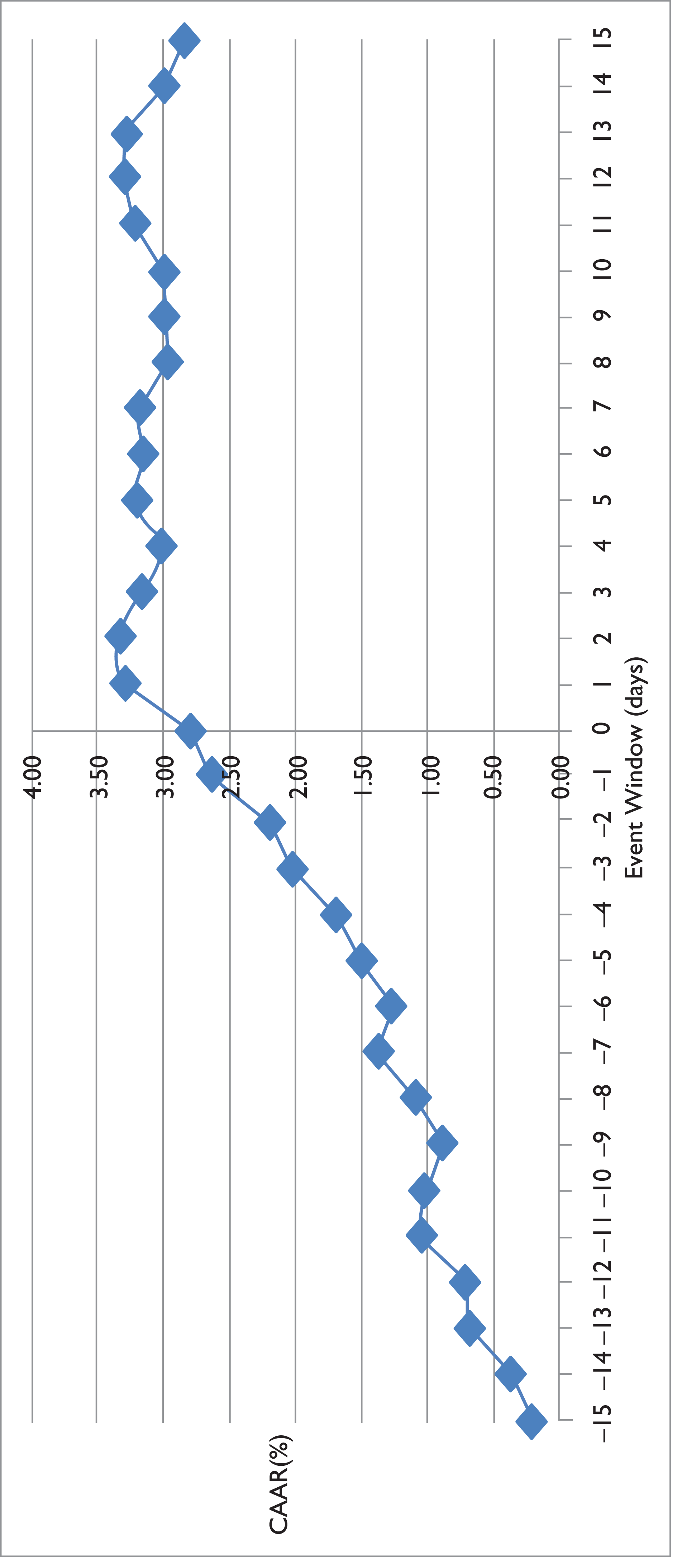

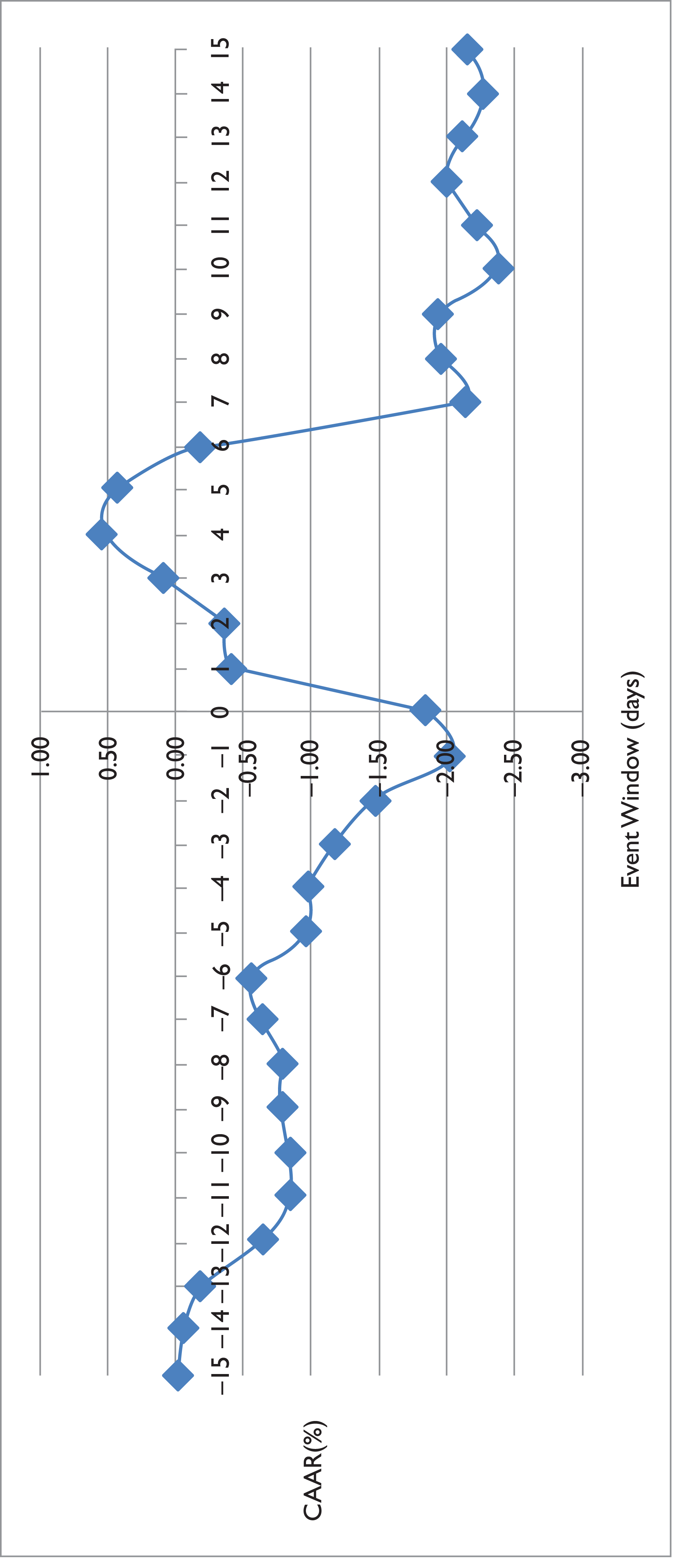

All CAAR values are positive post the event window period; in operational terms, it implies that the investors are likely to benefit during post-announcement period at any given day of the window. The results pertaining to the sample stocks during the study period in this regard are reported in Table 2. The probable reason for such a pattern of returns is that the investors tend to buy the share due to dividend signalling to earn potential abnormal returns. The value of CAAR is highest on the day following the announcement day (AD+1). As a result, hypothesis (H2), namely, there are no cumulative AARs to the shareholders of manufacturing companies on the announcement day is rejected at 1 per cent significant level. Figure 3 graphically depict the values of CAAR corresponding to each day of the event window. As per the Figure 3, post-announcement day (AD), CAAR value declines from its highest value, implying that it is likely to be beneficial for the investor to sell the share on the very next day from the announcement day.

For better understanding of abnormal returns, smaller event windows have been taken up. An event window of (x, y) denotes x days before the announcement day and y days after the announcement day. Table 3 presents the CAAR values and their corresponding t-statistics values for alternative smaller event windows.

The announcement effect of cash dividends around smaller windows have been measured for (–1, 0), (0, +1), (–1, +1), (+5,–5), (+2, +5), (–15, –2), (+15, +2) event windows. These event windows are used to control for information leakages and for ‘after hours’ announcements (Dasilas et al., 2008). The AAR values of 0.02 per cent on (AD–1) day, 0.11 per cent on announcement day (AD) and 0.67 per cent on day (AD+1) indicate that an investor can gain an overall CAAR of 0.78 per cent if the share is purchased one day prior to AD and sold one day after the AD. The negative returns in windows (+2, +10) and (+2, +15) show that the market absorbs the information related to cash dividends over a period of 10 days. The highest return to the investor of 1.01 has been noted in (+5,–5) event window; this window seems to be the best performing window from an investment perspective. The results show consistent incidences of cumulative abnormal returns around the dividend announcement, indicating over expectation of investors regarding dividend announcement in the information leakage phase, which had subsided considerably with new information disclosure. The incidence of t-values in this regard has further been inclined to the rejection of hypothesis (H2) namely there are no cumulative AARs to the shareholders of manufacturing companies on the announcement day is rejected at 1 per cent, 10 per cent, and 5 per cent, respectively.

Further, the status of the efficiency of the Indian stock market is also reflected in the abnormal returns as shown in Tables 2 and 3. The stock markets are able to incorporate this information in the market price of shares. The presence of abnormal returns around the announcement day indicates that the market operates in a semi-efficient state.

Cumulative Average Abnormal Return (CAAR) for Cash Dividend Announcements across various Event Windows during the Period 2003–2013

Cumulative Average Abnormal Return (CAAR) for Cash Dividend Announcements across various Event Windows during the Period 2003–2013

*, ** Significant levels at 1 per cent, 10 per cent, and 5 per cent, respectively.

For studying the impact of recession, the relevant data have been segregated into two phases: Phase 1 or the pre-recession period (1 April 2003 to 31 March 2008) contains data pertaining to first five years of the study period. Phase 2 or the post-recession period (1 April 2008 to 31 March 2013) contains data pertaining to the next five years of the study period. The impact of recession has been analysed in Tables 4 and 5.

Pre-recession Average Abnormal Return (AAR), Median Abnormal Return (MAR) and Cumulative Average Abnormal Return (CAAR) and their Corresponding t-statistic Values on and around Cash Dividend Announcements during the Period 2003–2013

Pre-recession Average Abnormal Return (AAR), Median Abnormal Return (MAR) and Cumulative Average Abnormal Return (CAAR) and their Corresponding t-statistic Values on and around Cash Dividend Announcements during the Period 2003–2013

*, ** Significant levels at 1 per cent and 5 per cent, respectively.

Post-recession Average Abnormal Return (AAR), Median Abnormal Return (MAR) and Cumulative Average Abnormal Return (CAAR) and their Corresponding t-statistic Values on and around Cash Dividend Announcements during the Period 2003–2013

*, **Significant levels at 1 per cent and 5 per cent, respectively.

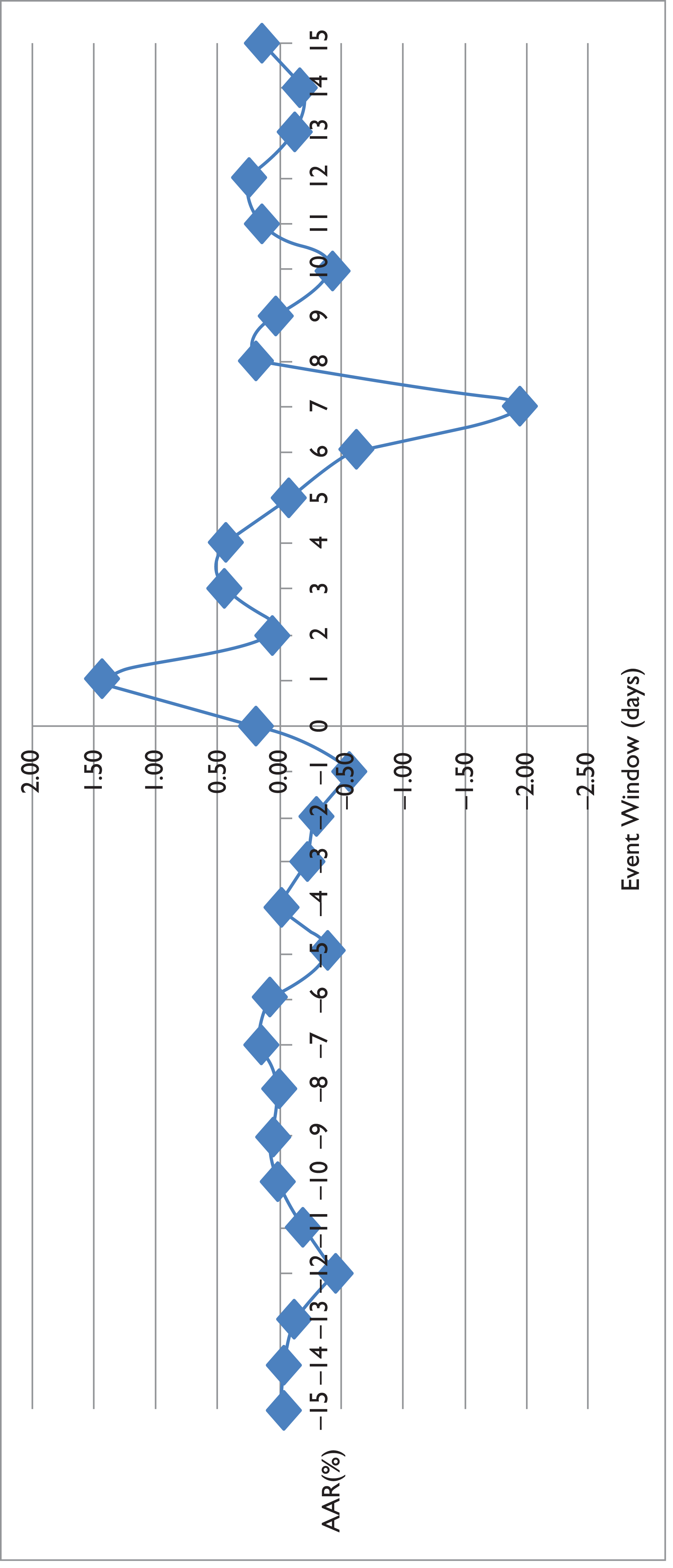

In addition, Figures 4, 5, 6, and 7 exhibits the stock price reactions to the announcement of cash dividends during pre-and post-recession period, depicting the values of AAR and CAAR corresponding to each day of the event window giving credence to our findings.

The patterns of returns have brought to light classic dichotomy of over expectation regarding dividend announcement in pre-recession period and under reaction after the post-recession period. The impact has been significantly different for the Indian stock market compared to the other developed markets.

The findings are notable as the post-recession abnormal returns decreased compared to the pre-recession period. The stock market has shown a negative impact of the recent global financial meltdown. This outcome tends to support the notion that dividend reductions convey negative information to the public which results in a subsequent fall in stock price. This decrease was statistically significant as per the paired t-test (Table 6).

Paired Samples Test for Pre-and Post-recession during the Period 2003–2008 and 2009–2013

The results are in conformity with the Indian Budget Report, which states that the manufacturing sector in spite of being a dominant sector in the economy witnessed a decline in growth to 2.7 per cent in 2011–12 and 1.9 per cent in 2012–13 compared to 11.3 per–cent and 9.7 per cent in 2009–10 and 201011, respectively. 4 However, since 2010–2011, it is observed that there has been an increase in abnormal returns which is perhaps the indication that the sector is recovering (Ernst & Young, 2012).

The paper builds on the existing literature indicating that cash dividend announcements provide abnormal returns to the investors. The evidence from the Indian stock market suggests that the market reacts positively to the announcement of cash dividends. Overall, the positive and significant abnormal returns around the announcements are in accordance with the signalling hypothesis and consistent with other empirical evidences (Aharony & Dotan, 1994; Denis & Sarin, 1994; Michaely et al., 1995).

As per the findings, AARs is the highest after one day from the announcement day. Further, such returns fall significantly as the market incorporates the information over the next two days. The best performing event window is (+5,–5). The results are consistent with the semi-strong efficiency form of market due to abnormal returns on the day of announcement (AD) as well as a day before (AD–1) and after (AD+1) the announcement.

Another significant finding is that the recession impacted the abnormal returns over the period of study. The returns decreased in a statistically significant manner in the post-recession indicating that the market returns were affected adversely.

The findings may prove useful for redesigning (if required), of the dividend policy keeping in view the analysis, results and discussions presented. They can be helpful for investors and investment managers in understanding the behaviour of the market with regard to dividend announcement. The results may also be useful to the regulators in understanding the information in the capital markets. The study also provides an opportunity to check the applicability of dividend theories developed in academia with regard to the Indian capital market.