Abstract

In October 2013, Mahboob Ali Shah Manager Financial Services Planning Telenor Pakistan (TP) needed to make decisions on the future of Mobile Accounts Sales officers (MASOs). TP had two businesses, i.e., GSM (96 per cent revenue contribution in TP 2012 sales) and financial services offering (4 per cent revenue contribution in TP 2012 sales) under the brand name of EasyPaisa.

TP launched EasyPaisa in 2009 with a view to reach out to the unbanked segment (60 million people). By 2012, EasyPaisa had a brand awareness of 80 per cent with the largest footprint of 36,000 EasyPaisa shops. Mobile accounts (MAs) were introduced in 2010 which could be operated only by Telenor sim and; hence, offered a great opportunity for TP to attract and retain customers for continual usage of its complete offerings.

TP developed an elaborate go to market strategy (direct as well as indirect) to reach its customers effectively. Territory Sales Supervisors (TSS) has been the focal contact point between TP and their franchises since the launch of GSM services in 2005; however, as TP increased their offerings in the realm of financial services and offered diverse services such as MAs it became difficult for TSS to focus on MA and other financial services products whereas ironically MA contributed only (5 per cent) in KPI of TSS.

At the same time, selling of MAs required different selling process as opposed to selling GSM services to franchisees and subsequently to retailers. Due to this change in the selling process, highly successful TSS had not been able to achieve sales targets for MA.

In order to achieve corporate objectives for MA sales, Mahboob needed to make a choice from among different possible options for MASO’s expansion to achieve this year’s target of 350,000 MA, out of which until now he could achieve only 224,000.

Discussion Questions

What is the current sales strategy of TP? Does TP need to change its current sales strategy to adapt to the changing market dynamics? If yes then kindly propose a way forward and critically analyse its implications on TP’s business.

What are the differences between Over the Counter (OTC) & MAs? Why are MAs important for TP in changing the business environment?

Elaborate on the current Sales approach of Telenor Pakistan, what is changing in the environment?

Why Territory sales supervisors (TSS) are not successful in selling MAs specifically? Will you label them as Hunters or Farmers?

How important is the role of retailers in TP go to market strategy, what are different approaches TP is using to retain them? Why retailers are not successful in selling MAs?

Why and how TP launched MASOs?

Discuss Pros And Cons of Proposed Options for MASO’s Future

During the first week of October 2013, Mr Mahboob Ali Shah Manager Financial Services Planning Telenor Pakistan (TP) while sitting in his office took a deep breath as he was planning the fate of newly launched (June 2013) sales team; ‘Mobile Accounts Sales officers’ (MASOs). MASOs were solely managed by franchisees and were recruited to sell MAs only. MAs had strategic importance in the dynamic competitive horizon of financial services offered by TP, and any decision regarding MASO’s would have significant long-term consequences not only for financial services division but also for TP.

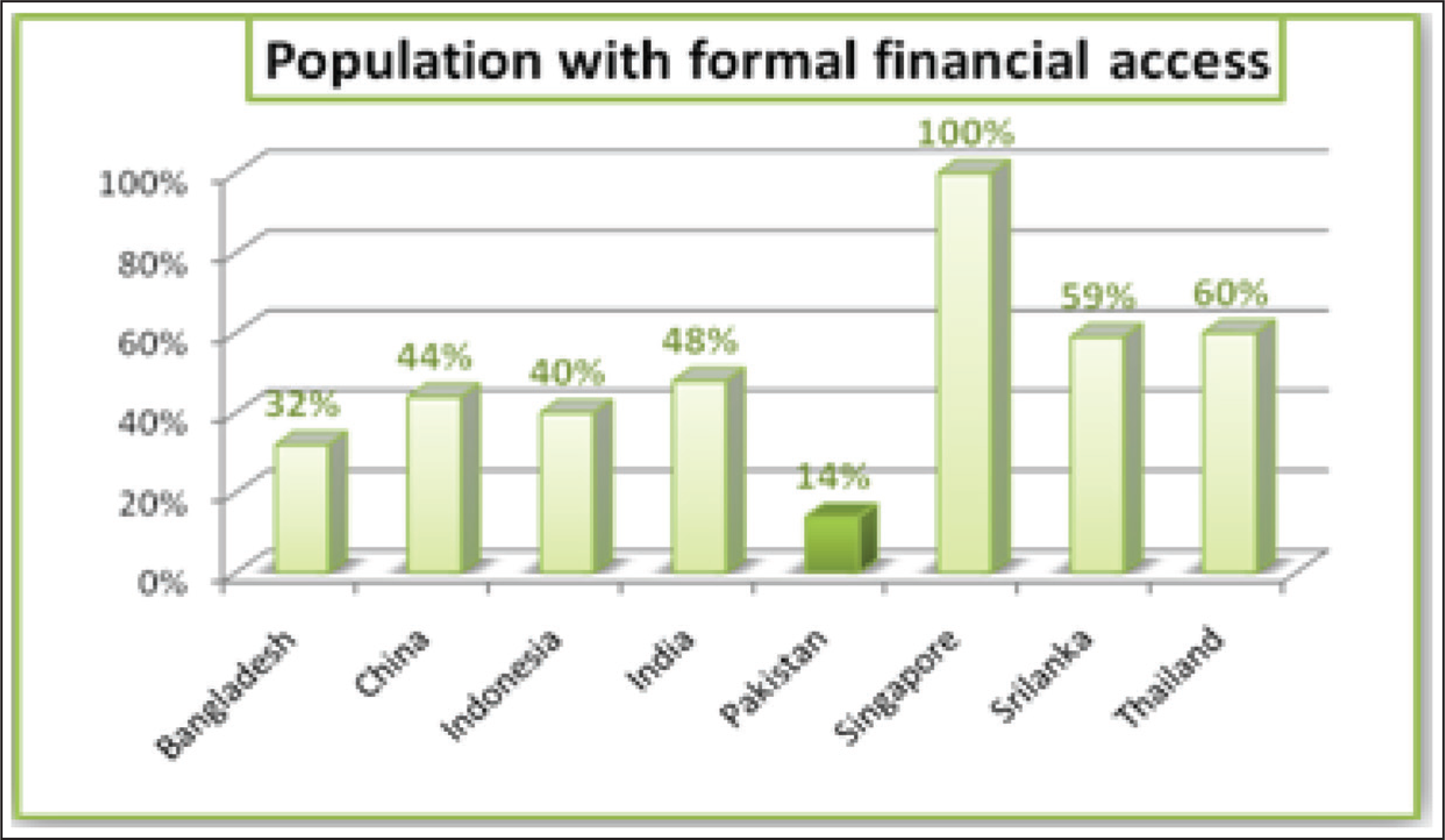

In 2012, TP reported revenue of PKR 85 Billion, it was divided into two business units; GSM (96 per cent revenue) and Financial services (4 per cent revenue). Financial Services were launched in late 2009 under the brand name of EasyPaisa which was an instant success. In 2009, only 14 per cent of the population had formal financial access (Figure 1). EasyPaisa opened an array of opportunities for TP to capitalise on its existing GSM business channel structure.

Fierce competitive intensity and perpetual price wars were the main highlights of the telecom industry in Pakistan. Pakistan had some of the lowest call rates in the world while it had the second highest levels of taxation in the world. The squeeze on margins that came with fierce competition and high levels of taxation meant that for companies to grow profitably, innovation through value-added products was the way forward. Cellular mobile operators could increase average revenue per users (ARPUs) through additional non-voice services such as mobile banking. 1 TP looked forward to amplifying its financial services business to diversify its product portfolio and develop an alternative source of revenue.

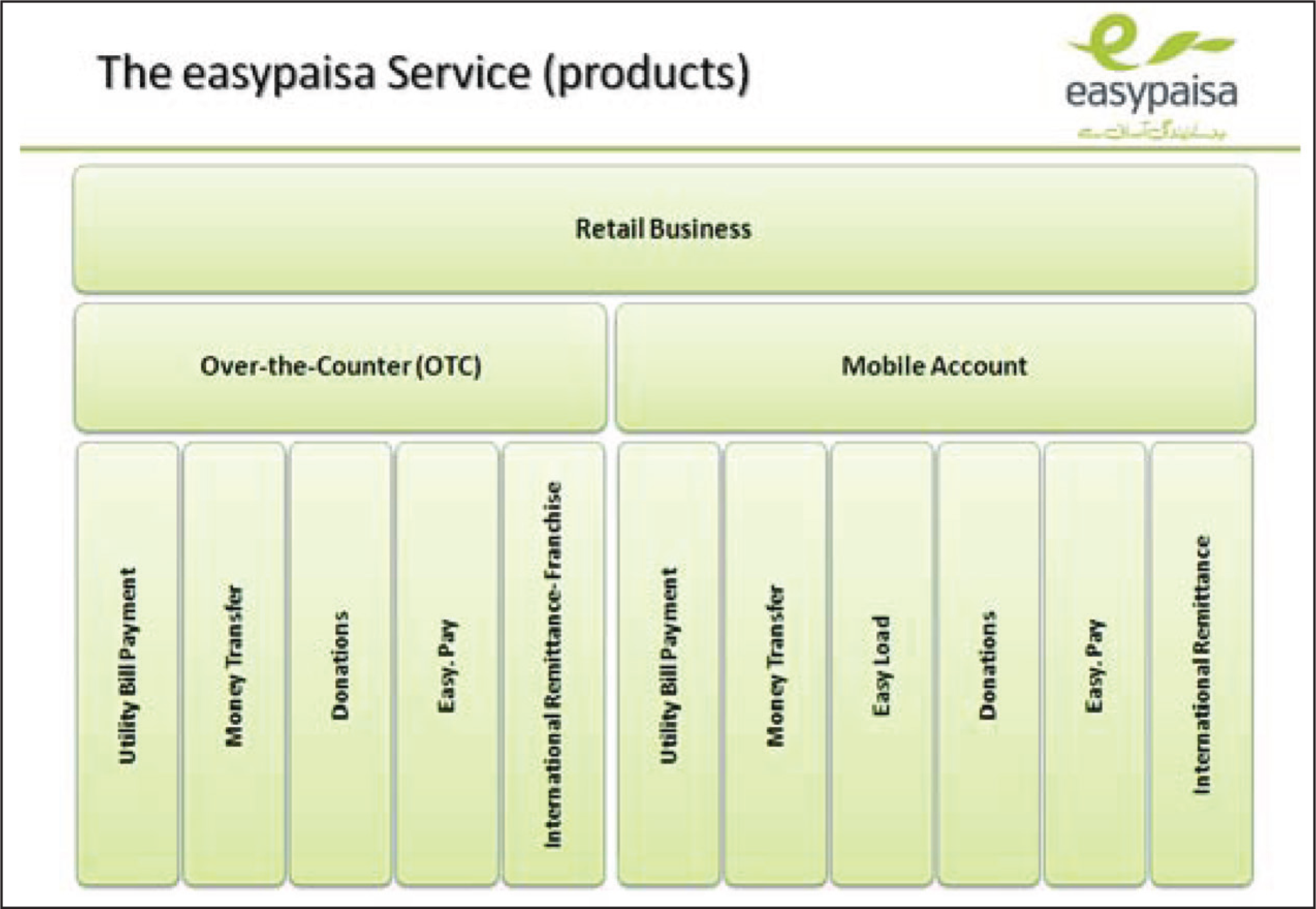

EasyPaisa offered two products; i) OTC (Transaction from one CNIC 2 to another CNIC without a need of MA wallet) ii) MAs 3 (Figure 2). Revenue mix of 2012 from these two products was 90 per cent from OTC and 10 per cent from MAs. Due to the unique nature of MA attributes, they warranted a different selling approach and skill set from TP’s highly effective selling machine; therefore, TP had to build a new salesforce for selling MAs.

MASO’s experiment proved to be successful, in its first four months the number of MAs increased by 113 per cent (105,000 to 224,000). Fifty per cent of September 2013 sales were generated by MASOs. Strategic objectives of financial services business stated a target of 350,000 MAs in 2013. The same target was also a qualifier for Melinda Gates foundation next aid instalment of USD 6.5 million (Bill & Melinda Gates Foundation, 2015). Melinda Gates foundation aimed to improve financial inclusiveness in Pakistan, where the population was severely underbanked. Also in a fiercely competitive market, it was imperative to develop incremental sources of revenue, MAs were considered to be a major source of incremental revenue for TP. TP also wanted to maintain its first mover’s advantage in the financial services category. Hence MAs success was critical for TP to remain competitive in Pakistan’s Telecom industry in the longer run.

To amplify sales of MAs and achieve the targets set for 2013 Mahboob had the following options:

Increase the number of current MASO’s for accelerated penetration, Maintain the same number of MASOs but focus on enhancing their skills and related control system, or Develop a sophisticated in-house sales force managed by TP to focus on the institutional and corporate customers only in addition to current franchisee managed MASOs.

Each option had its own advantages and challenges. Mahboob wondered how to decide and what option to select.

Company Background

The public company that started out in 1855 as the ‘The Royal Electric Telegraph’ was later called Telenor. The company had gone from being a governmental institution, focussed on telegraphy to become a global shareholding company, offering some of the most advanced telecommunication technologies and services in the world. Telenor Group was one of the world’s largest mobile operators with 148 million mobile subscriptions, operating in 13 international markets. Telenor was amongst the top 500 global companies by market value (Financial Times Global 500, 2015). By 2012, it had 32,900 employees worldwide with revenue of NOK 101.7 billion. 4

TP 100 per cent owned by the Telenor Group, acquired GSM license in 2004 and began commercial operations on March 15, 2005. By 2012, TP’s investment in Pakistan reached USD 749, with a total subscriber base of 21 million and market share of approximately 22 per cent (GSM Association, 2015), making it Pakistan’s second largest mobile operator at that time.

TP acquired 51 per cent shares of Tameer Microfinance Bank in November 2008. In 2009, it launched ‘EasyPaisa’ and became Pakistan’s first telecom operator to partner with a bank which offered mobile financial services across Pakistan. By 2012 TP created 2,800 direct and more than 25,000 indirect jobs with a network of over 200,000 retailers, franchises and sales & service centres, thus, providing a means of livelihood to a large number of people.

EasyPaisa Launched in 2009

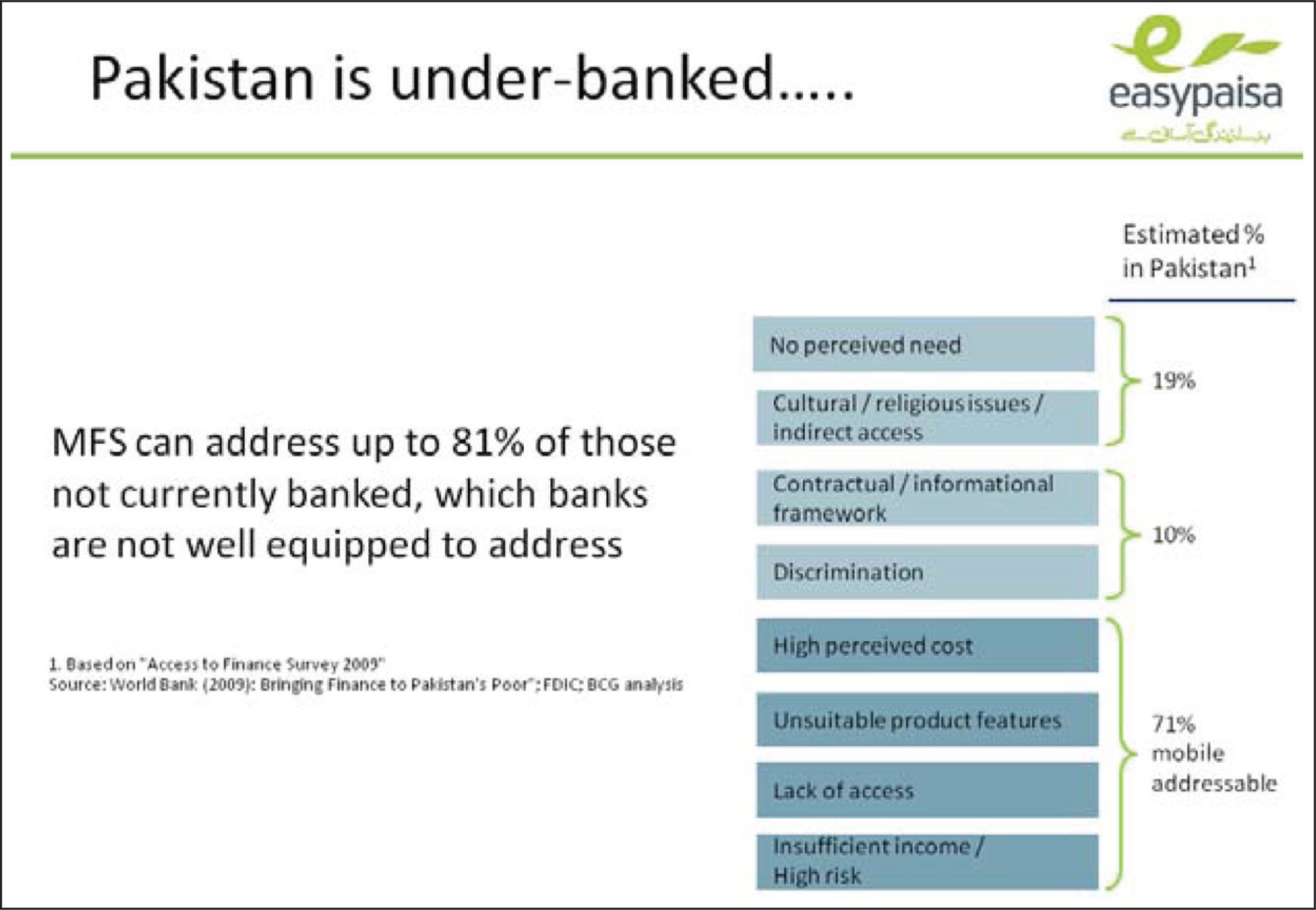

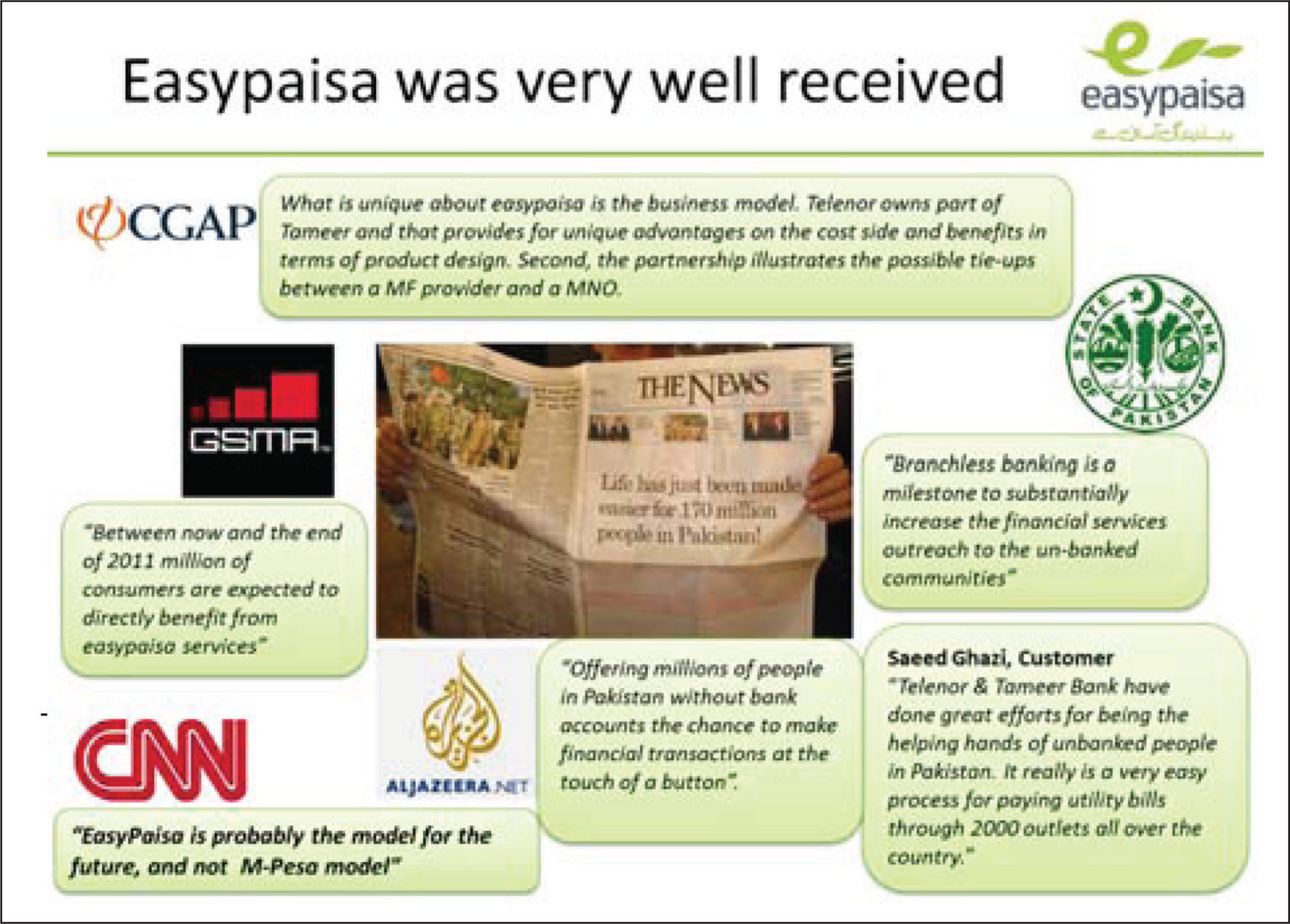

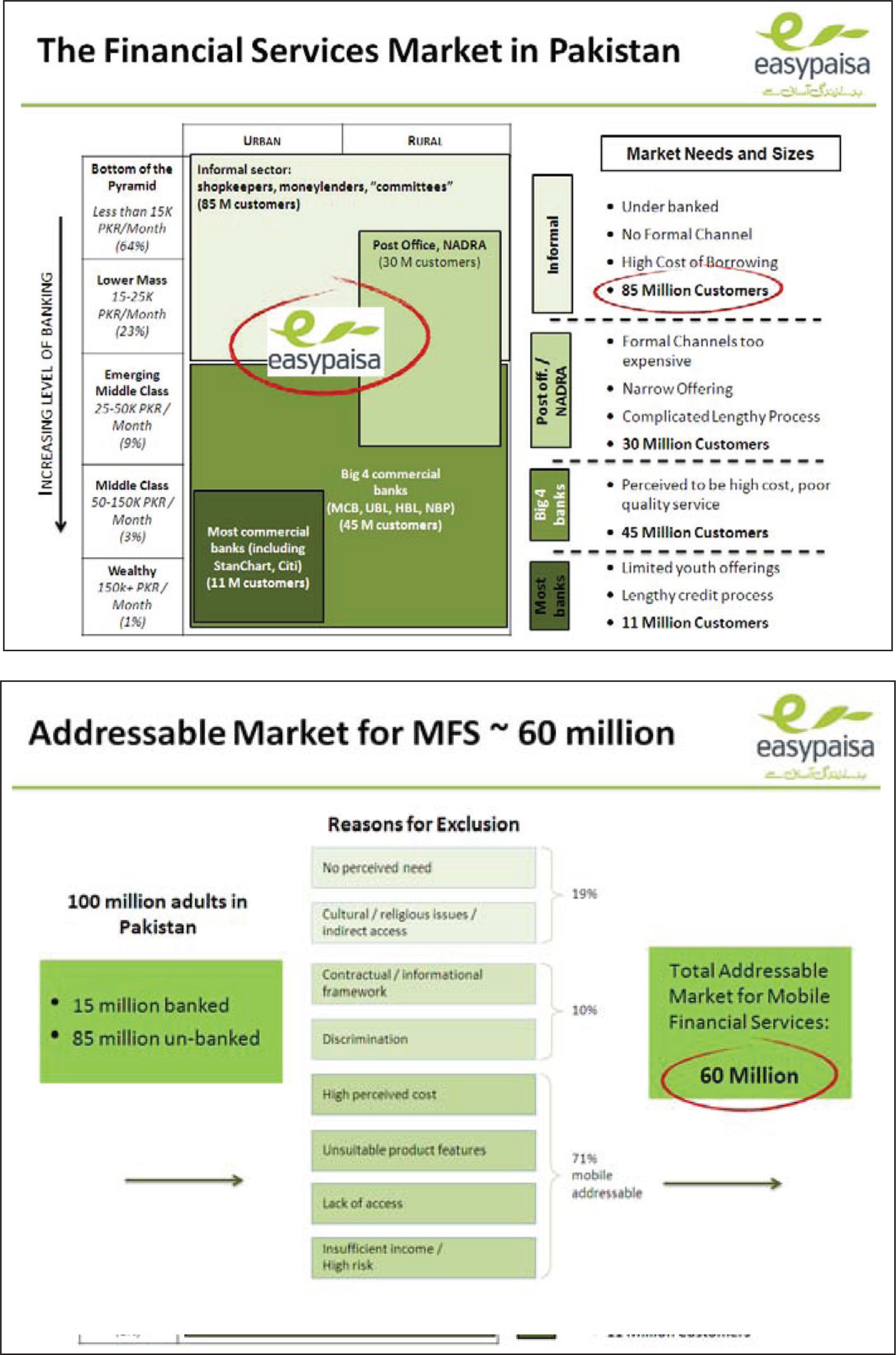

TP launched its financial services under the brand name of EasyPaisa in 2009. EasyPaisa offered financial services to 71 per cent of Pakistan’s unbanked population which was unbanked due to the reasons highlighted in Figure 3. EasyPaisa’s value proposition was to offer basic financial services in a reliable and convenient way. By the end of 2012, EasyPaisa established itself as a preferred brand (more than 80 per cent brand awareness) with the largest network of 36,000 EasyPaisa shops in 750 cities. 60 million transactions were conducted in 2012. In the same year, EasyPaisa was ranked 3rd largest mobile money service in the world by CGAP. 5 EasyPaisa was well received by many local and foreign bodies. (Figure 4).

Subsequently, EasyPaisa launched MAs under its brand name in 2010. MAs worked as complete bank accounts that could be operated from any mobile phone with a Telenor sim

6

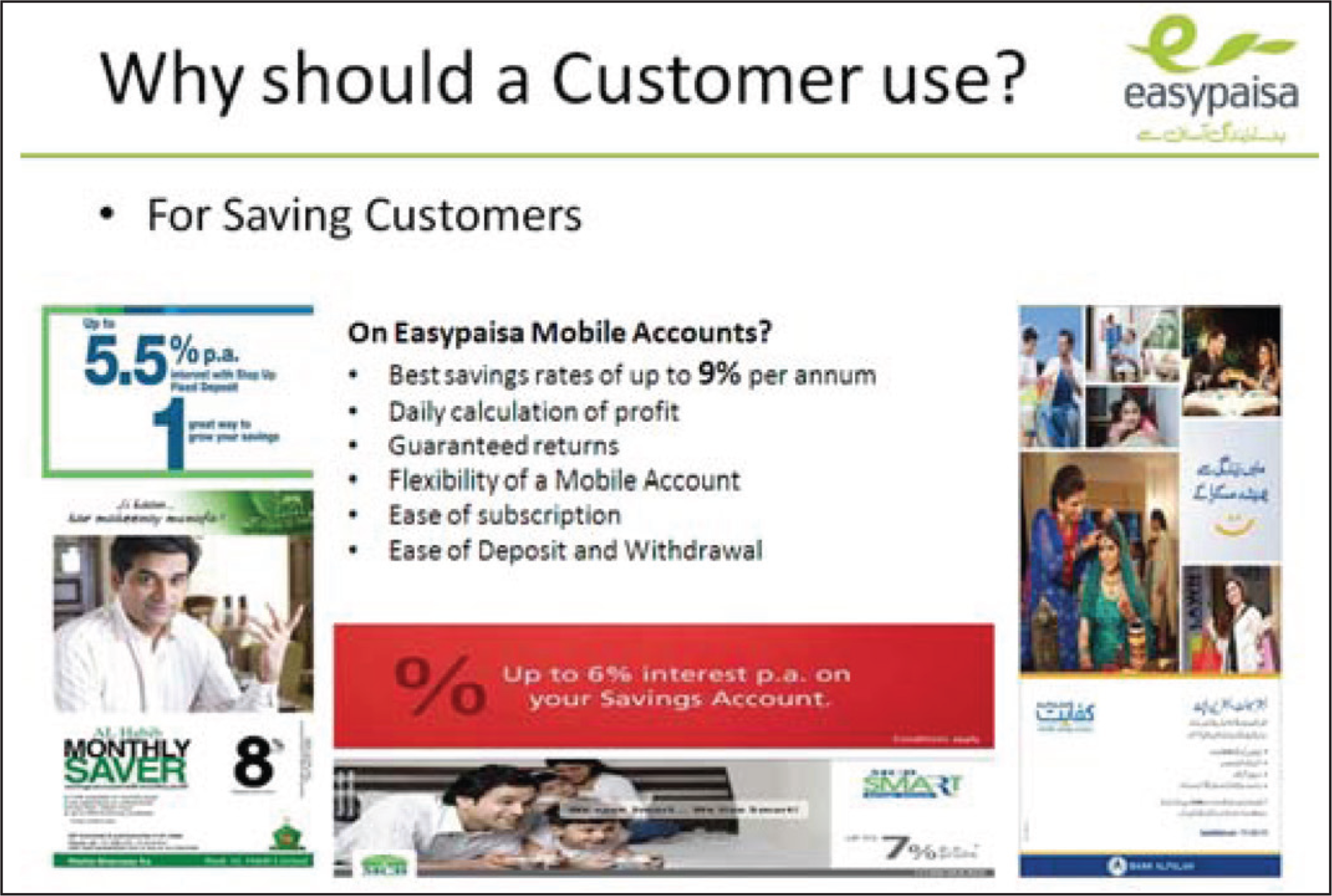

card. As many customers (22 per cent of the industry) were already using Telenor sim card; therefore, it gave TP the following additional advantages: i) Reduced customer churn ii) Increased GSM ARPU and at the same time provided customers unmatched convenience and savings. MAs offered savings and insurance (Figure 5) on top of all services already available at OTC

In the financial services industry, due to rampant regulatory violations and frauds, State Bank of Pakistan (SBP) 7 was expected to further tighten already stringent regulations around OTC banking (traditional banking) in near future, making it difficult for a layman to open a bank account; hence, MAs became an important source of increasing financial inclusion in the country. MAs offered several benefits to all the stakeholders (customers, telecom companies and indirect channels). For TP, it increased the GSM sales, reduced churn and increased switching cost for the end consumer. For retailers it lowered cash management burden with increased convenience and savings, lastly, customers got convenience since it was considered to be the most convenient bank account ever to open in Pakistan as account opening in Pakistan entailed lengthy paperwork.

Vice President Financial Services of TP Mr Roar Bjaerum believed that time had come when the industry needed to progress from the OTC business model to MAs due to obvious benefits that MAs offered for all the stakeholders. MAs were considered a strategic necessity for TP due to their obvious benefits over OTC models.

Pakistan Demographics and ARPU

Pakistan’s estimated population in 2012 was 183.5 Million with a growth rate of 2 per cent (Ministry of Finance, Government of Pakistan, 2015). Urbanisation was 37 per cent (World Bank, 2015b) with a population density of 232 per sq. km of land area (World Bank, 2015a).

Monthly ARPU of TP’s Market Vis a Vis Other Countries Having Telenor Footprint in 2012 (Telenor, 2015)

The low ARPU of Telenor’s Pakistan market shows the high potential that Telenor can tap into by offering a diverse range of value-added services.

Financial Services Market in Pakistan

Financial services market in Pakistan offered great potential for organisations to tap banked and unbanked customers, according to one estimate total addressable market for mobile financial services was 60 million individuals (Figure 6).

The first quarter of 2013 witnessed a 16 per cent increase in the number of branchless banking transactions. Five per cent of Pakistani households were mobile money users; however, only 0.3 per cent had registered MAs (State Bank of Pakistan, 2015). It indicated the potential available for corporations to pursue the market of the MA. Mostly opened MAs were not active, only 0.32 million out of 1.4 million accounts (22.86 per cent) were active in the first quarter of 2013; therefore, it was necessary for organizations to enhance the number of active MAs. MAs were active either because of disbursements made by the government (social welfare disbursement) or salary disbursements by private organizations.

Competition

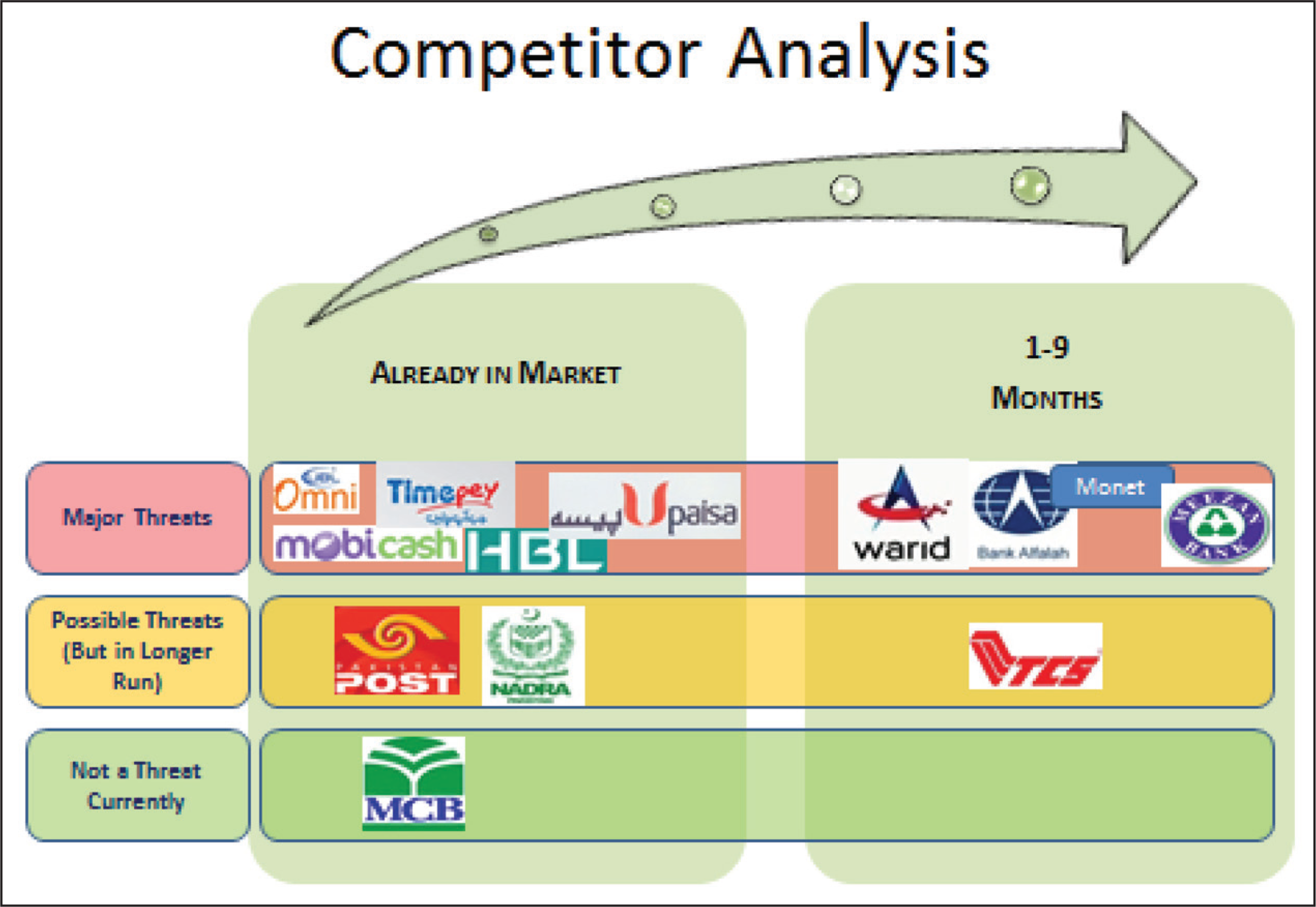

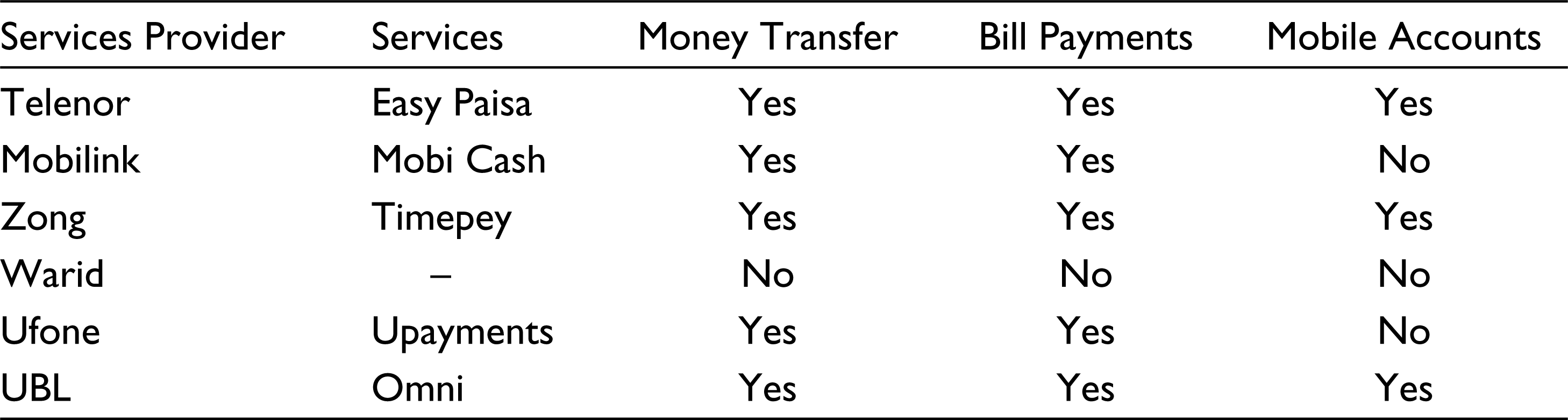

Over the last five years, financial services had become one of the leading value-added services in Pakistan’s telecom landscape. Mobilink started financial services under the name ‘Mobicash’ in 2012 in collaboration with Waseela Bank (major sponsor was Mobilink). Zong in collaboration with Askari bank launched financial services under the brand name ‘Timepey’ in December 2012. ‘UBLOmini’ was launched in 2010 under the flag of United Bank Limited. Other competitors included ‘U-Paisa’ by U-fone, EasyPaisa maintained its first mover advantage. The large retailer base developed over the years was TP’s point of differentiation. But new entrants like Mobicash and Upayments were aggressively poaching existing EasyPaisa retailers. This led to a decline in market share for TP and an increase in market share for competitors. (Figure 7)

TP Sales Organization

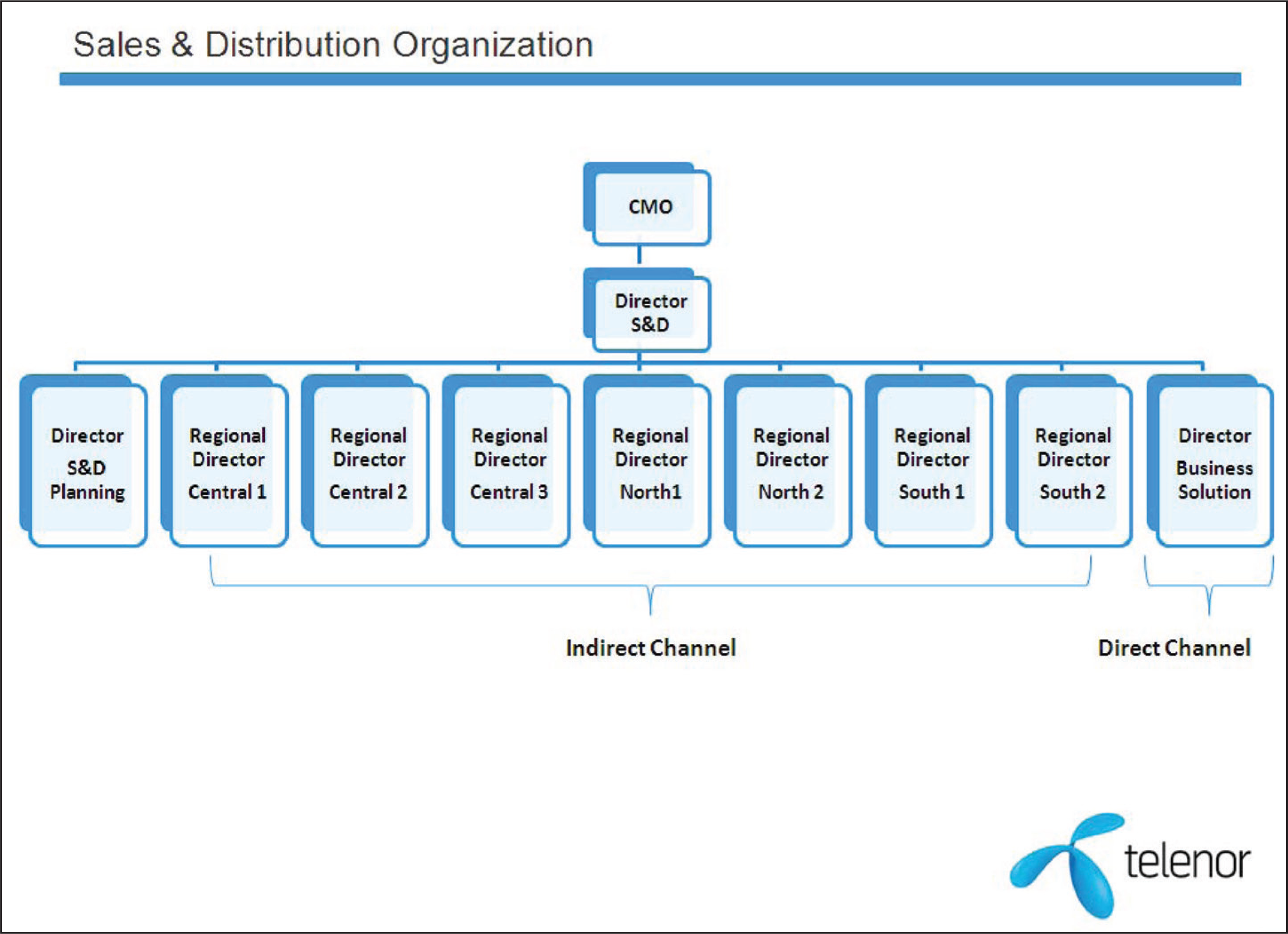

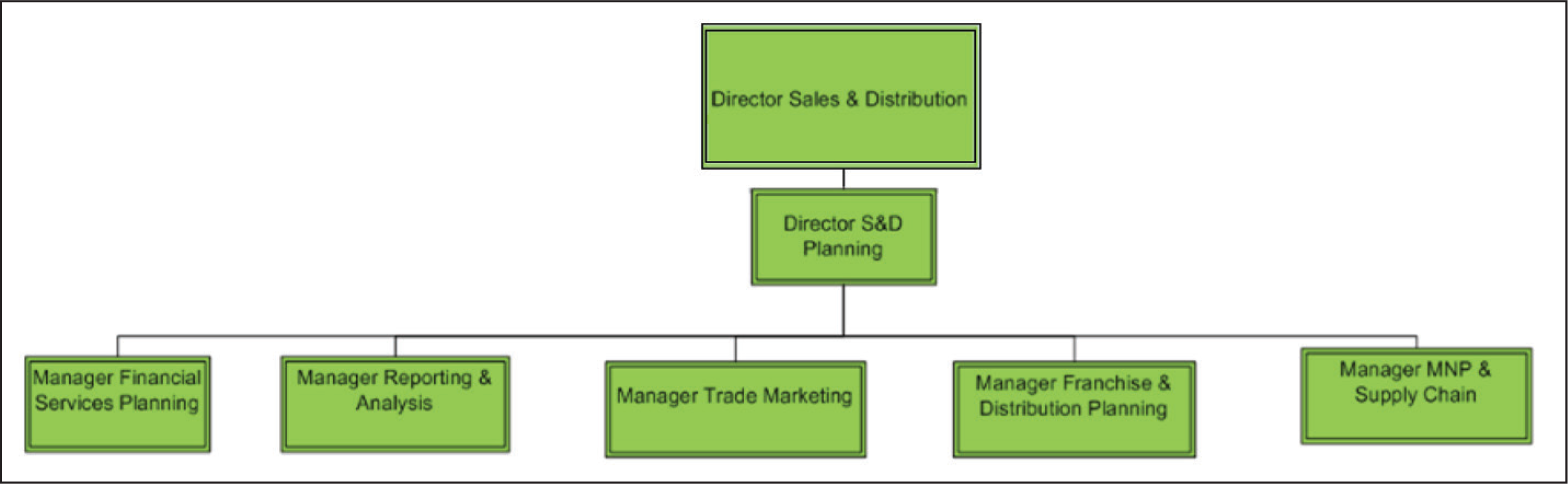

TP sales and distribution organization comprised of a direct and indirect channel (Figure 8). Director sales & distribution planning function provided support across both channels in a number of areas such as trade marketing and distribution planning (Figure 9).

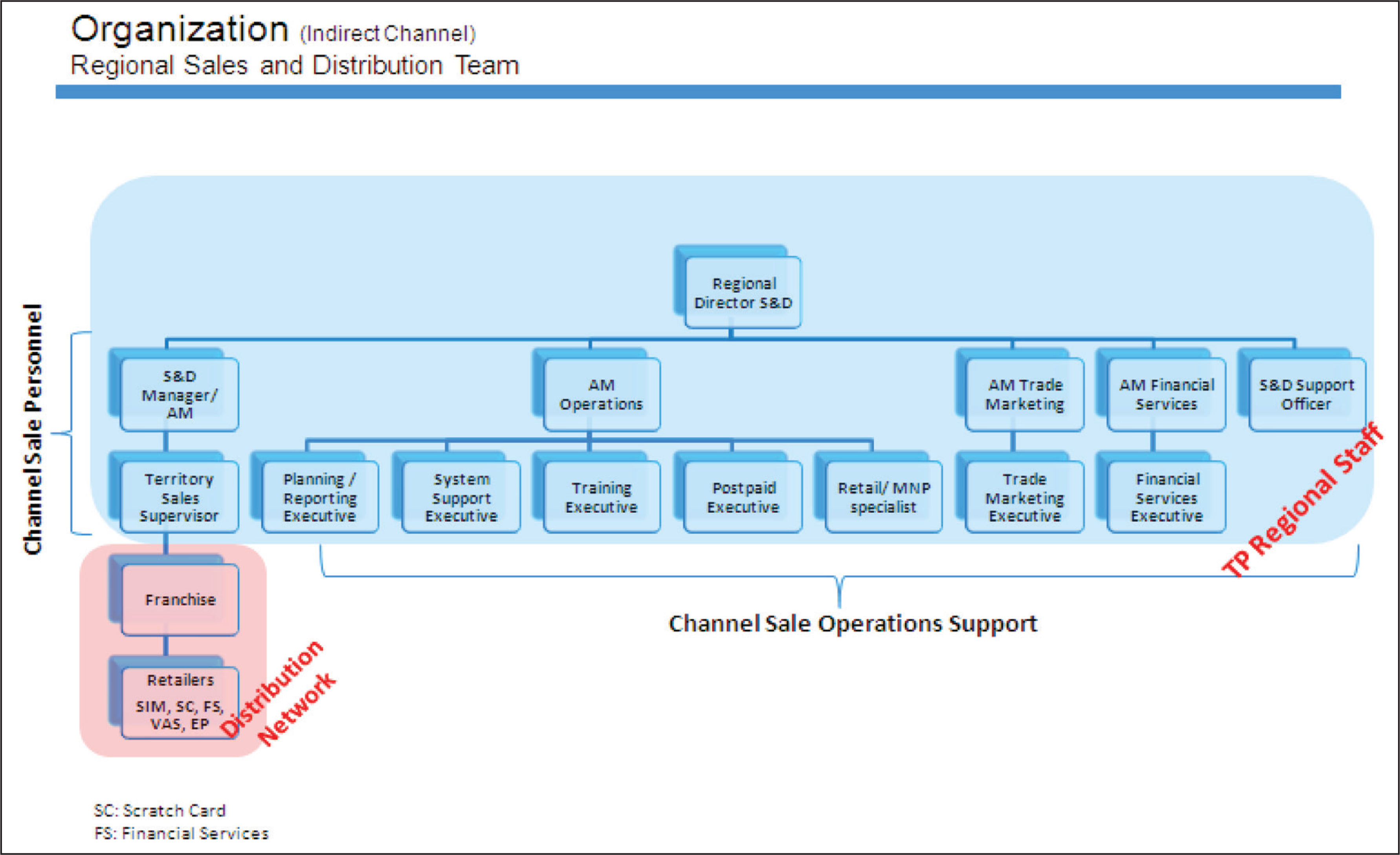

Indirect Channel

The indirect channel was divided into seven geographic regions, every region was managed by one regional director (Figure 10) who was solely responsible for the region’s performance. In any given region, there was an average of fifteen TSS, this number could vary based on the size and future potential of the region.

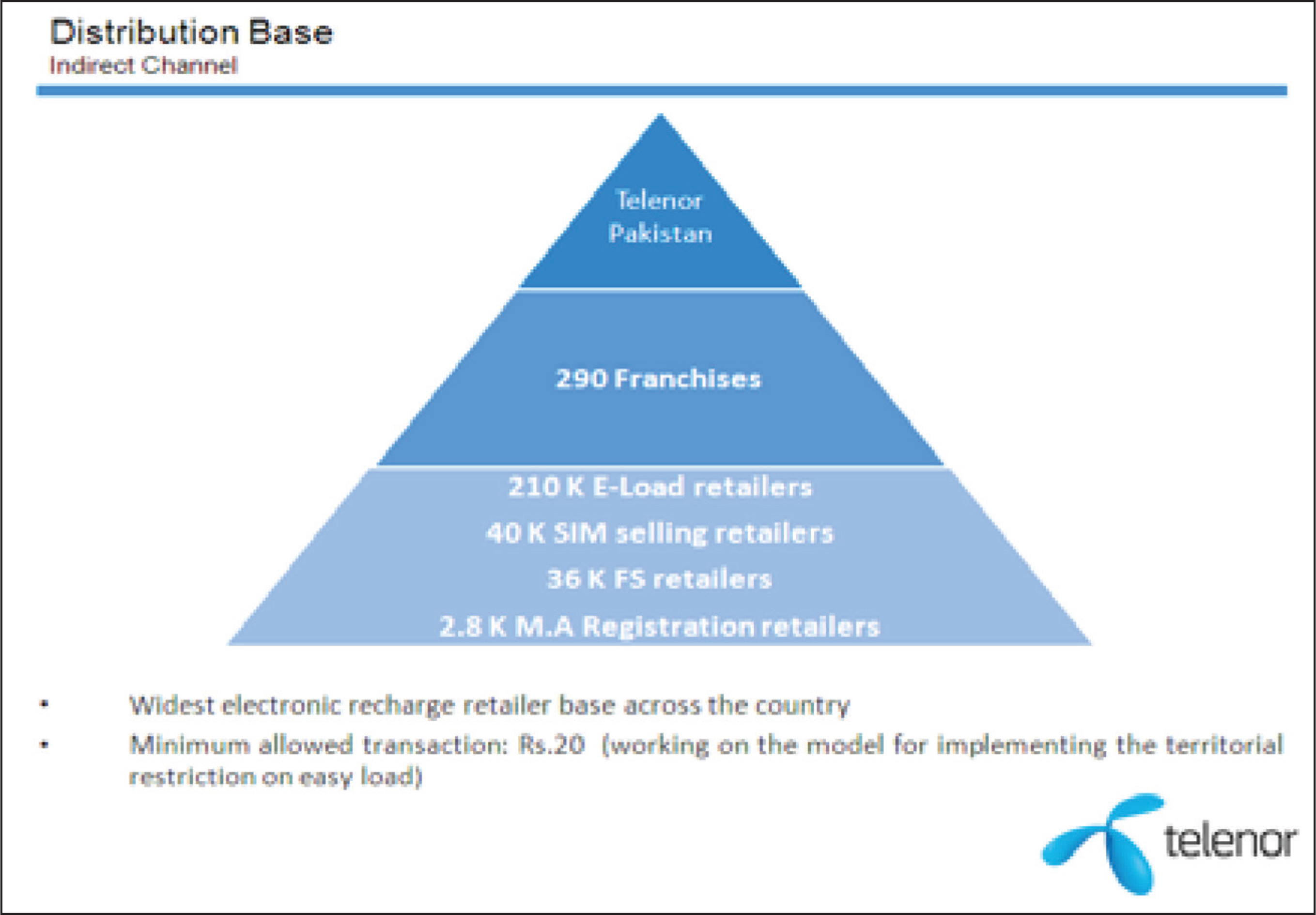

Over the years, TP had developed a large distribution base across the country (Figure 11), at top of the pyramid there were 290 franchises, these franchises served the retailers in their respective territories. Such a large distribution base remained one of the competitive advantages for TP as it could not be replicated by the competition easily.

Territory Sales Supervisors

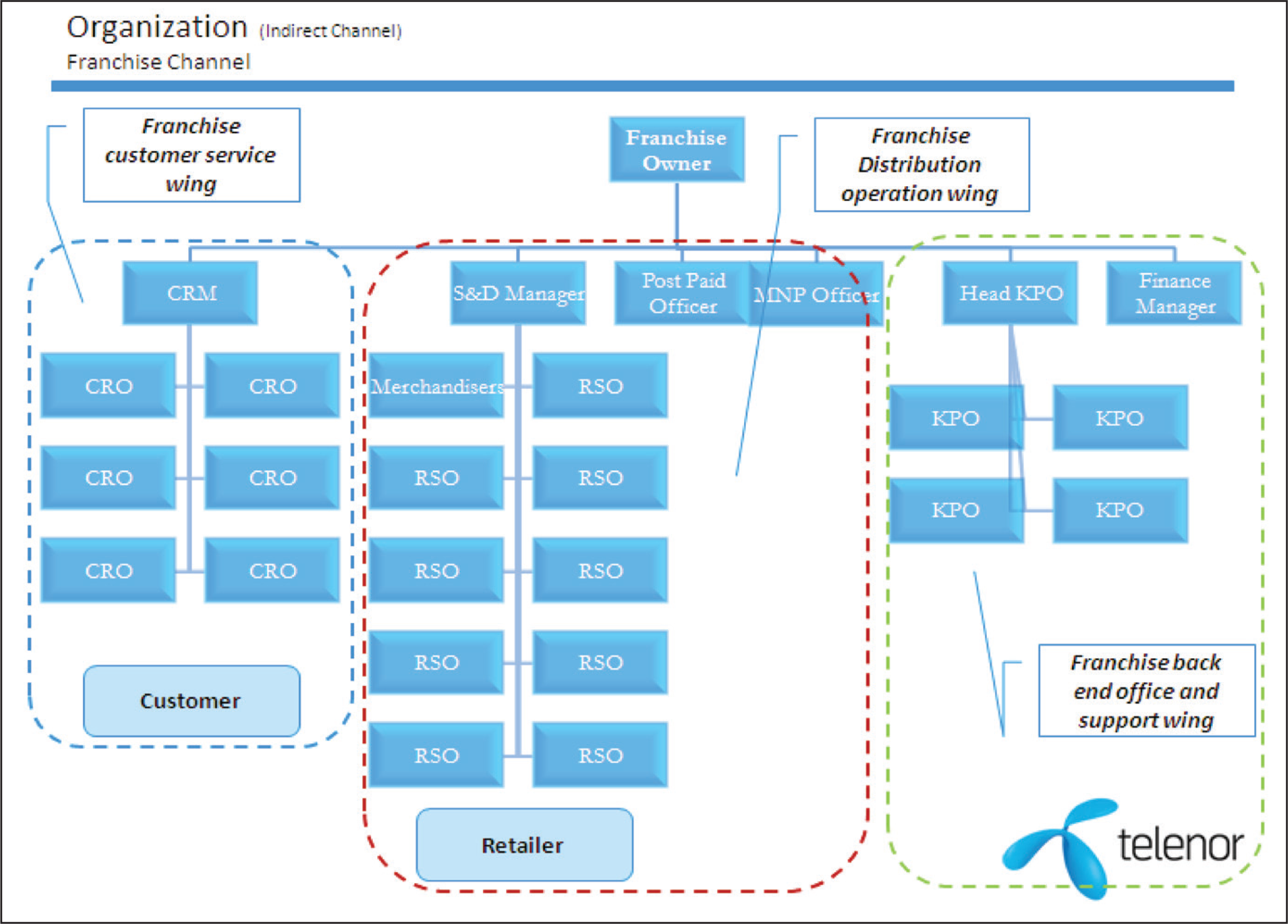

TSS was the main point of contact for franchisee from TP and was involved in the day to day management of franchise operations.

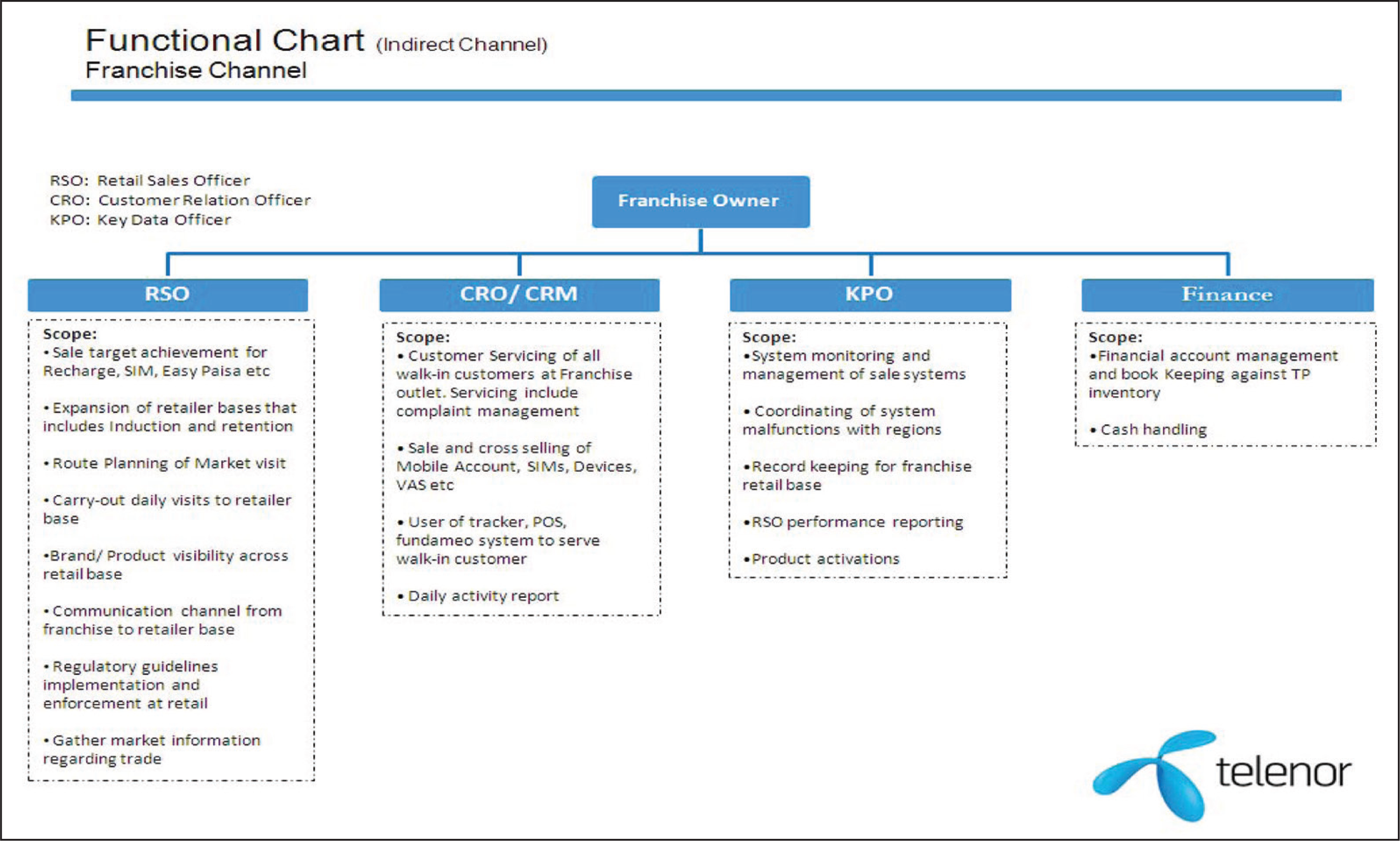

There were 115 TSS in TP. Average TSS had a work experience of four to five years in sales with a bachelor’s degree (sixteen years of education). The job description of TSS is given in (Figure 12). Franchise organizational and functional charts are displayed in (Figure 13A and 13B) respectively, retail sales officer visited around 40 retailers daily and was responsible for the availability and sales of Telenor’s complete portfolio.

Key performance indicators for TSS are described in (Figure 14). There was a debate among TSS about last two KPIs (earlier it was the responsibility of operations team) as to whether TSS had any control over these objectives or not.

Compensation

TSS compensation structure comprised of fixed and a variable component, around 22 per cent of salary was variable. It was necessary for any TSS to achieve 90 per cent sales on an aggregated basis to secure this 22 per cent variable portion. TSS could achieve an additional 50 per cent incentive when each individual KPI achieved 100 per cent. There was no incentive for the incremental performance above 100 per cent achievement.

Retailer (Agents) Management

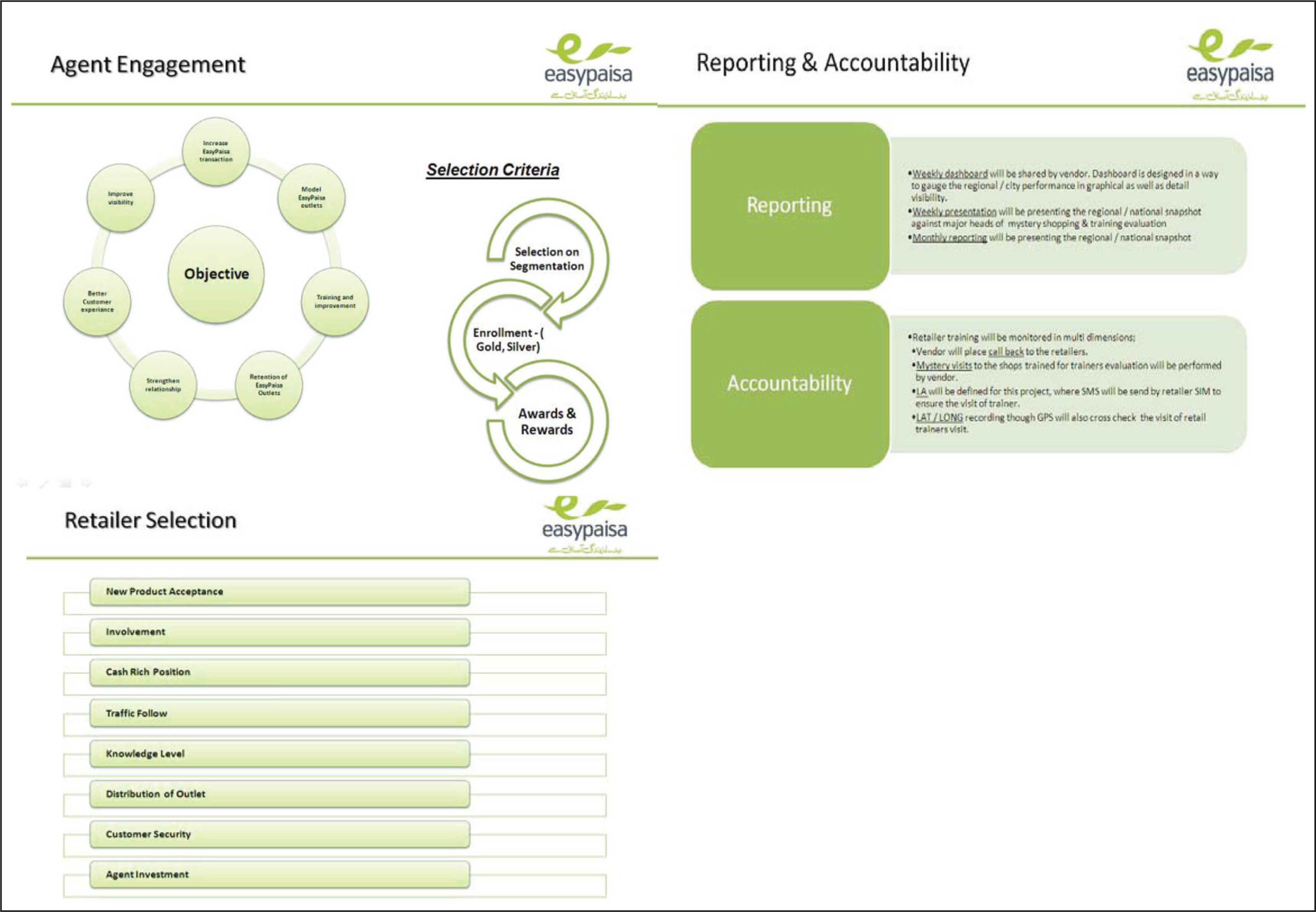

At the base of the pyramid, 36,000 financial services retailers played a critical role in terms of delivering value to customers. It was necessary to make sure that retailers were being managed well. TP EasyPaisa team devised a thorough process for retailer management from selection to continual training (Figure 15).

Retailers played an important role in influencing customer’s decision for using service of any particular company, mostly customer was indifferent (low involvement decision) to which company retailers actually used to transfer their funds. After the emergence of competition, the first target for the competition was to poach EasyPaisa retailers to make them their agents as well. According to an estimate, around 45 per cent of retailers were using funds transfer facilities of multiple service providers and competition successfully poached EasyPaisa retailers by offering better commissions. To minimize this trend, EasyPaisa initiated several projects which focussed (merchant loyalty program, merchant training program and cash management programs) on retailer loyalty.

Due to increased competition, easier approach for new players was to focus on current agents of TP instead of developing new retailers. A price war also started in the telecom financial services sector. Such circumstances resulted in decreased margins for companies in the OTC business.

Direct Channel

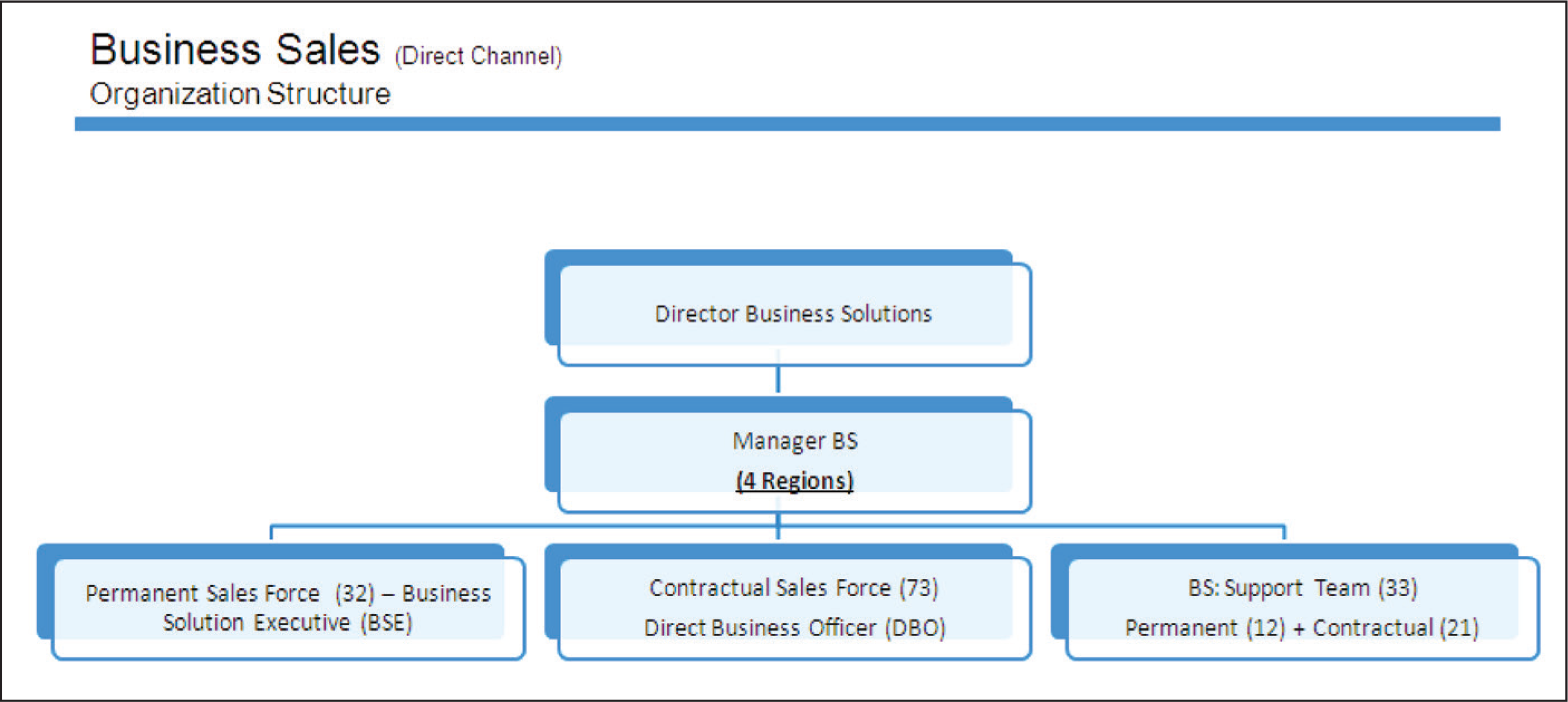

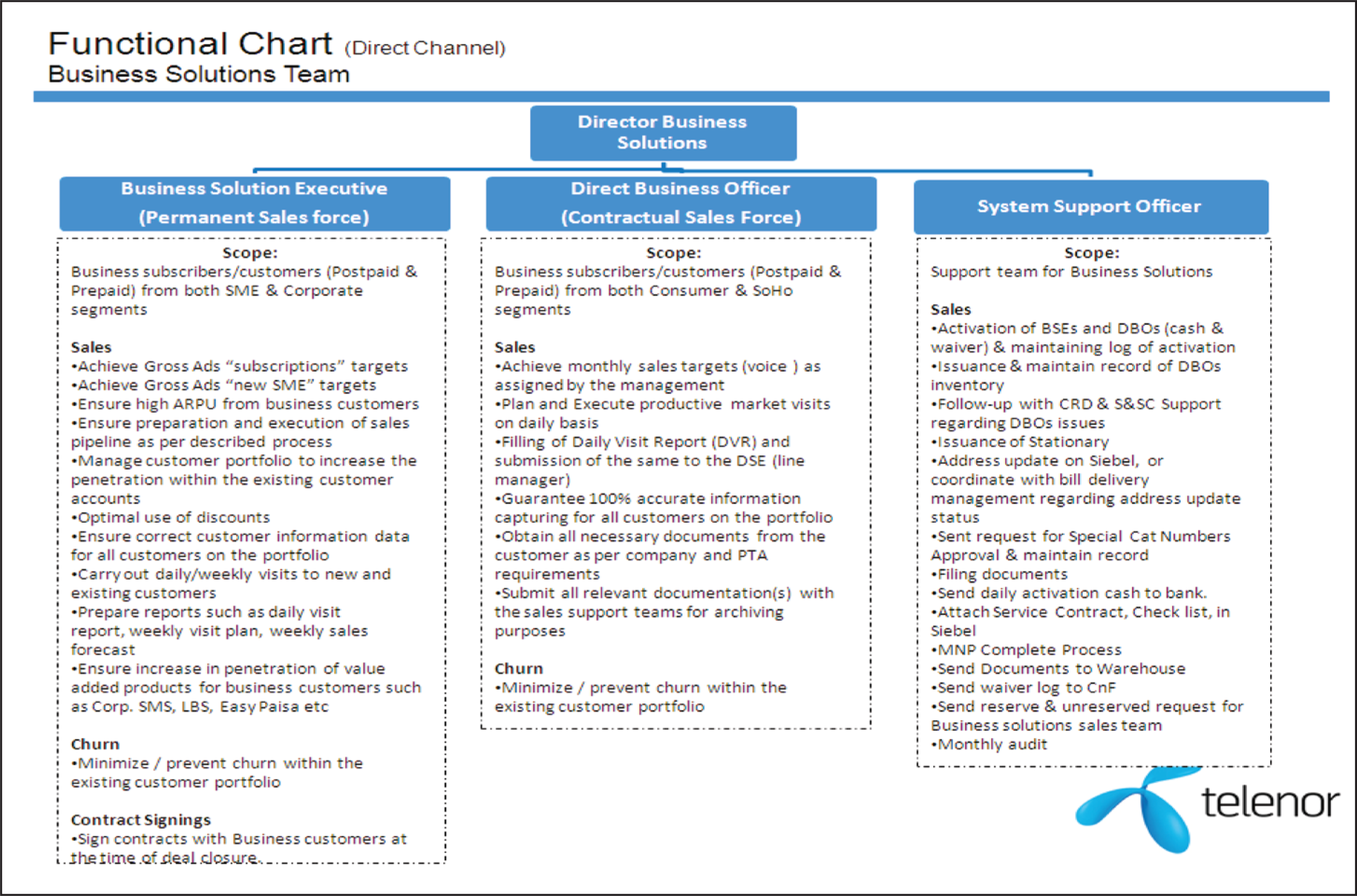

It comprised of business solution direct sales team of TP (Figure 16A). The primary focus of this sales team was to target the value segment (institutional and corporate customers). This sales force demonstrated B2B sales approach to manage complex decision-making unit (DMU) of institutional customers. Scope and job description of business solution team is described in Figure 16B.

Issues in Mobile Account Selling

Financial services carried a weight age of 15 per cent in total KPI’s of TSS. This 15 per cent was further divided among three products: i) Utility bill payments, ii) MAs and iii) Direct remittances. Due to the arduous nature of MAs selling process which required numerous cold calls and frequent visits to new customers, TSS ignored MA and focussed more on KPI with the highest weight (35 per cent): secondary recharge (easy load scratch cards). Incentive mismatch for TSS was one of the causes of sluggish sales of MA.

To sell MAs as opposed to OTC services substantial effort by the agents (retailers) was required. Typically, it took around 25 minutes to explain product features and usage instructions to a prospective customer. Since a majority of EasyPaisa retailers were engaged in other businesses such as grocery store, tobacco shop, etc., it was not in their interest to spend time on selling MAs, as they could earn more income by investing the same time in other fast-moving products. Limited interest in MA selling from existing OTC retailers was another reason for sluggish sales of MA.

The MA offered services of a complete bank account; therefore, to open MA compliance from the SBP was required. There were only 2,800 MAs registered retailers against the total of 36,000 EasyPaisa retailers. Limited footprints of MA registration points also resulted in low sales of MA.

EasyPaisa launched OTC services before MA in Pakistan, as opposed to other countries in the world where MAs were launched before OTC services. This was due to the strict regulations of SBP which required lengthy paperwork for account opening, whereas for money transfer only CNIC of the customers was required. CNIC availability was not an issue in Pakistan; therefore, TP management chose to enter in financial services with EasyPaisa OTC services.

Mobile Accounts Sales Officer Evolution

The unique features of MAs warranted a different selling approach as compared to current sales and distribution infrastructure TP. It was agreed that due to different products attributes, MA required a push as opposed to a pull strategy to sell. To achieve these objectives MASO’s structure was devised in April 2013. It had the following objectives:

To have a mobilized field force in the franchise channel, To increase the number of direct selling agents of MAs, and Develop a sales force which had direct interaction with customers; to educate and guide them for MA usage.

Salesforce was responsible for active MAs and ensured continual usage by customers and minimized idle MAs.

Sales Process: (JD)

MASOs interacted with customers in several ways. Primarily they found their customers through cold calls, door to door visits, visits to small and medium offices and leads collected through the retail channel. On a typical call, MASOs told customers about product features, benefits and addressed all customer queries. Every MASO was given a special handset with an application installed in it to complete all requirements to open an MA at the point of sale. It decreased confusion which the customer experienced prior to MASO’s visit where they had to go to appropriate Telenor/retailer premises and the retailer was unable to explain the product features due to lack of time.

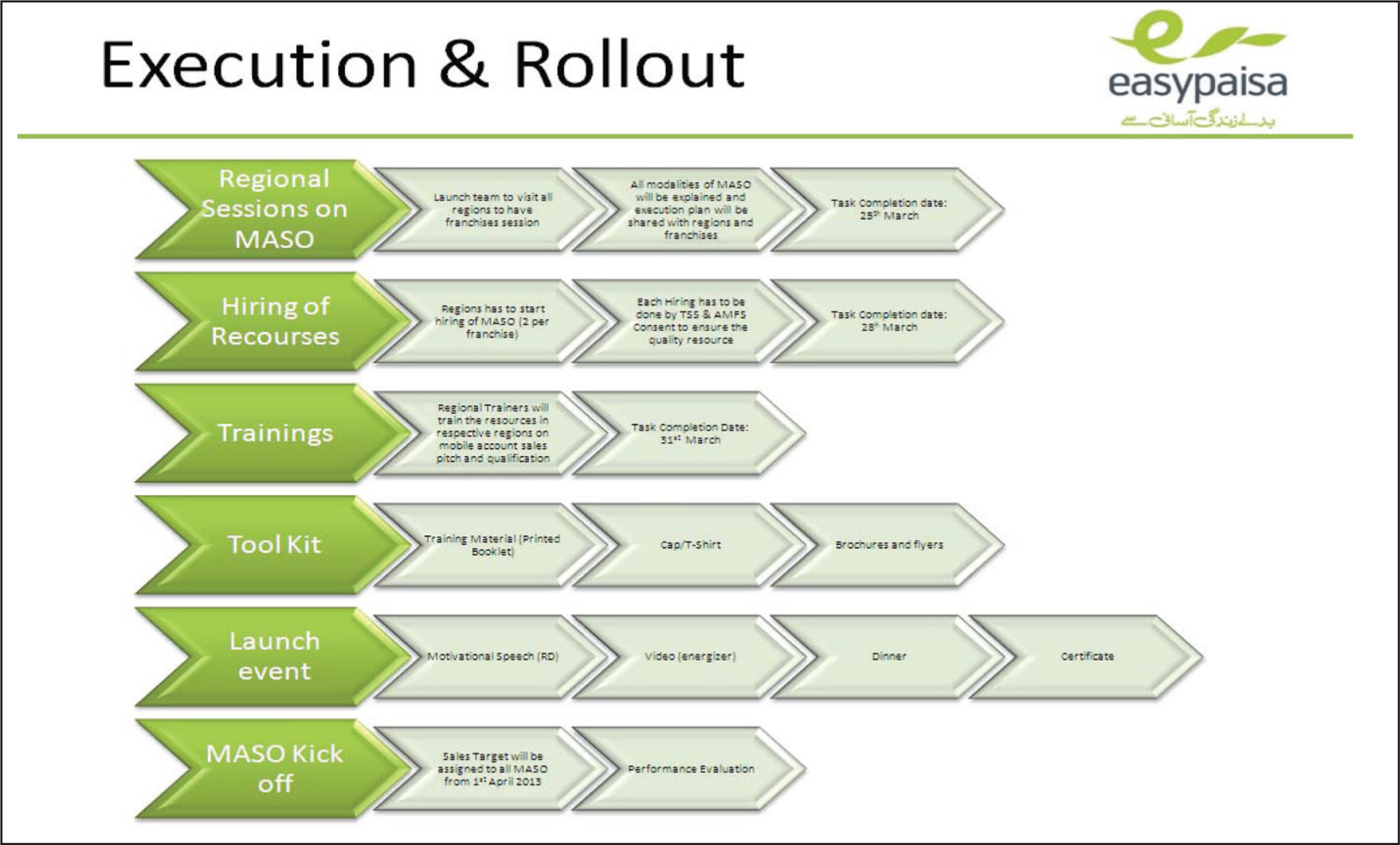

Rollout Plan for MASO

After approval of MASO’s plan by management in the first quarter of 2013, detailed execution and rollout plan was prepared (Figure 17). The objective of this plan was to ensure flawless execution of MASO’s nationwide.

Structure

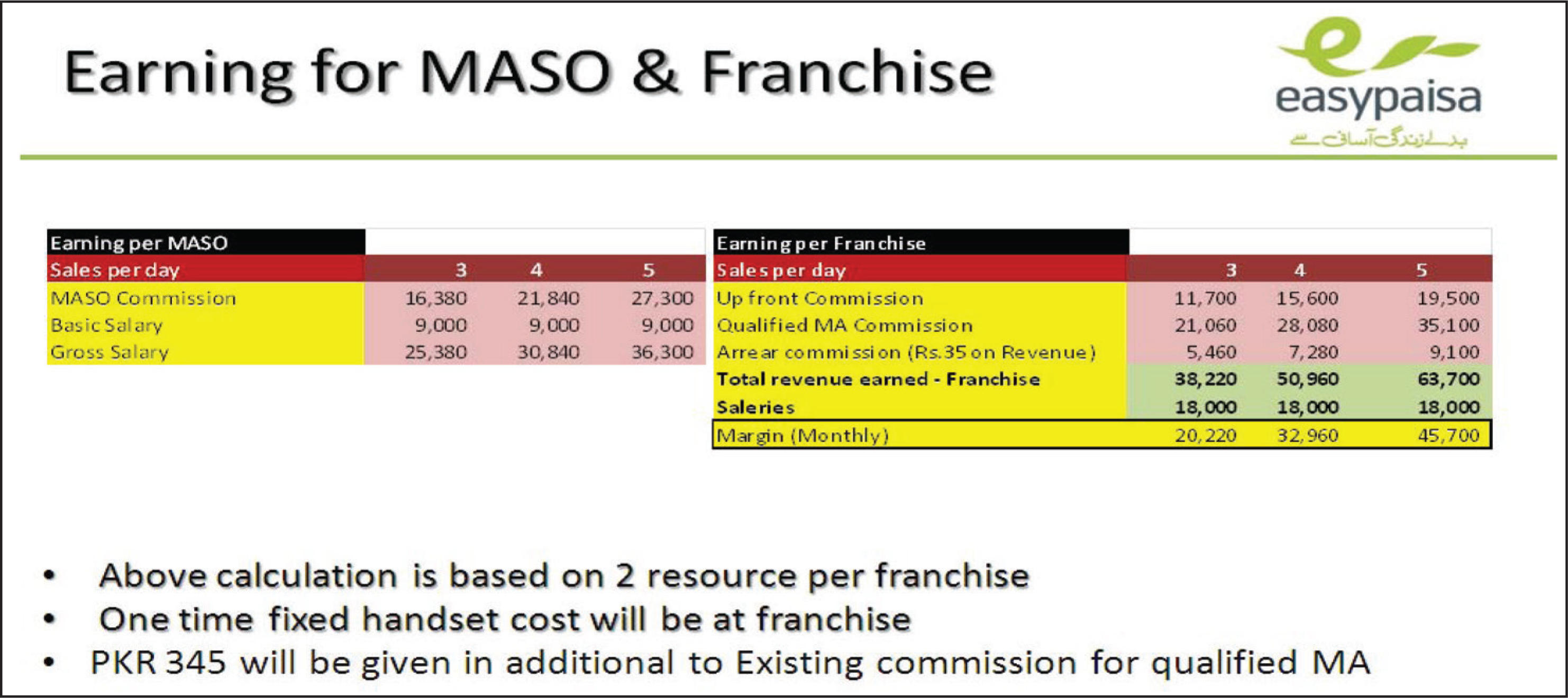

Two MASOs were hired initially per franchise, the number could vary based on the geographical location of the franchise and the willingness of the franchise as each MASO increased the fixed cost of the franchise. But the initial decision of two MASOs per franchise was made after a thorough sensitivity analysis performed by TP (Figure 18). TSSs were primarily responsible for the hiring of their franchisees MASO.

Skills

Average qualification of MASO was intermediate 8 with two years of general experience. Primarily MASOs demonstrated hunting 9 characteristics with a sole focus on selling MAs. MASOs initially targeted the prepaid segment of GSM business without any elaborate segmentation plan. Training of MASOs was carried out by regional trainers initially when they were hired. Additional trainings were to be conducted if there was any change in the product features or any new product was offered. All the trainings were carried out by the existing regional trainers; hence, it did not entail any incremental cost.

Compensation

MASOs were on the franchisee pay role, with an average fixed salary of PKR 9,000 per month. On registration of each MA, MASO became eligible for PKR 30. MASO could earn PKR 150 after two transactions in 2 distinct months on the same MA. To reduce churn, major part of the variable compensation was tied to transactions in the account sold. Sensitivity analysis for MASO‘s and franchisees earning is attached (Figure 18).

Results in First Four Months

MASO’s performance in the first four months was commendable. They sold 105,000 active MAs in these four months. The monthly break up of these sales is given in Table 3.

Financial Services by Telecom Companies

Monthly Sales Data

MASOs found the job very challenging as it involved going out in the field and convincing people to use MAs.

One of the MASO commented:

We have to do lots of cold calling to several types of people and most of the time our effort goes to waste because when it comes to money, people are conscious about it and they are not ready to trust us; therefore, it is very difficult to stay motivated in the field.

MASO’s turnover was high (25 per cent as compared to the 15 per cent industry benchmark). Reason for high turnover was the nature of the product which was relatively new and required tons of effort to sell. With the rollout of MASO’s TSSs were happy as a portion of their KPI was being achieved by MASOs.

A TSS commented:

MASO’s have made my life much easier. Now I don’t have to worry about mobile accounts targets in my KPI, which although had a small percentage but required a lot more effort and time. Now I have dedicated resources to work on mobile accounts and I can focus more on my core KPI’s.

The franchise was also happy as he was making more money (see Figure 18) whereas the retailer had some concerns as he believed that the sales of OTC services might go down as more and more people start using MAs.

Way Forward

MASO experiment was a great success as MAs sales in the first four months demonstrated a substantial increase of 113 per cent. However, the following options were being considered by TP about future of MASOs.

To achieve 2013 strategic objective of 350,000 MAs, one option was to increase the number of MASOs. Keeping in view the performance of MASOs in the first four months, one could safely assume that an increase in the number of MASOs would result in more active MAs. With increased MASOs, franchises could get an opportunity to make more money as the MA brand got established. Bill and Melinda Gates foundation donation (USD6.5 million) instalments were also linked with the 350,000 active accounts target; hence, increased MASOs could contribute to achieving this target.

There were also concerns with regards to the quality and control of MASOs. End customers considered MASOs as Telenor representatives but Telenor exercised very little control on the selling efforts and behaviours of MASO as they were employees of the franchise. There were quite a few franchises who made good profits on MASO; however, some of the franchisees were not convinced by the effectiveness of MASO business model and it could take time to make business sense for them.

Another option under consideration was to maintain the current number of MASO’s while at the same time focus on building their skills so that service expectations could be met. It was expected that well-trained MASO demonstrated good relationship skills with customers and could increase their usage of MAs on a continual basis. It could increase ARPU for Telenor and subsequent earnings for franchises. It could also provide an opportunity for those franchisees who struggled to get returns from their investment.

On the other side, while maintaining the existing number of MASOs there was little hope for TP to achieve their business objectives and commitments with international stakeholders. Keeping in view the fierce competition in the telecom industry, if there was a delay in acquiring more MAs it could easily result in losing share to competition as well.

TP managed salesforce for value segments (institutional and corporate customers). TP was evaluating an option to appoint MASO’s on its payroll to serve the value segment. TP planned to upgrade the average profile of MASOs and bring it to the level almost like business support executives. Proposed upgraded MASO’s planned to cater to the

This approach could make it possible to sell MAs to banked segment (corporate as well as individuals) of the market which looked for convenience in these services. It could also provide much more control over the efforts of MASO’s but a thorough cost and benefit analysis had to be done.

It was 7 p.m. on the office clock and Mahboob was still thinking about which one of these three options he should recommend to the top management. Albeit enormous uncertainty was associated with these decisions but one thing was crystal clear that whatever decision was taken regarding MASO’s future, it would have serious long-term consequences for the financial services business of TP.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.