Abstract

This article examines the existing synergy between financial inclusion and human development in Indian states during the post-liberalisation periods (1993–2015). Using both principal component analysis and panel data regression models, first, the impact of financial inclusion on human development is measured. Second, the reverse causality from human development to financial inclusion is estimated to know whether human development should be a pre-condition for ensuring greater financial inclusiveness in Indian states. It is found that financial inclusion has a positive and statistically significant impact on human development, along with other control variables such as social sector expenditure, per capita state gross domestic product and capital receipt. However, the lack of urbanisation (measured by the percentage of rural population) has a negative and significant impact on the process of human development in Indian states. On the other hand, since human development has also a significant reverse causal connection with financial inclusion, it is argued that ensuring financial inclusion through urbanisation measures would not only improve the level of human development in Indian states, but it would also sustain the process of inclusive development in itself due to the existing feedback loop with the later.

Keywords

Introduction

Although Indian economy has been passing through a high growth trajectory during the post-liberalisation (1991) periods (Adeel-Farooq et al., 2017; Chandrasekhar & Pal, 2006; Kotwal et al., 2011), its global ranking of human development is still remaining very low. Though incidence of poverty declined massively (Chauhan et al., 2016; Planning Commission, 2012), a large sections of Indian population (rural poor and socially marginalised groups including women) still lack access to basic financial products and services (Kapoor, 2014; Lenka & Sharma, 2017; Sharma & Chatterjee, 2017). According to Sen (2001), availability and easy access to finance has a very significant effect on economic entitlement. Thus, excluding a person from the formal financial system yields an inherent negative value for the individual, and it also led the individual to face other kinds of deprivation, thereby limiting further basic living opportunities (Sen, 2001). Hence, it is important to examine, whether, low level of human development is an outcome of the lack of financial inclusion in Indian states. If yes, then to what extent?

In this context, it is important to note that previously both the Government of India (GoI) and the Reserve Bank of India have under-taken several initiatives to improve the situation and to help achieve a higher level of human development through greater financial inclusion. The first initiatives of financial inclusion in India could be traced back to the nationalisation of banks in 1969. Furthermore, during the pre-liberalisation period both RRBs (in 1975) and NARARB (in 1982) were established. But the financial sector reforms undertaken during 1991 was a paradigm shift in the functioning of India’s financial market in general and the banking sector in particular. Firstly, the period of financial reform faced the withdrawal of social banking policy. The social banking policy or bank licensing policy was started in 1977 to spur banking outreach in rural areas. In order to provide basic banking facilities to the rural unbanked people, commercial banks were instructed to open four branches in rural areas in order to operate one branched in urban area. However, the withdrawal of social banking system during this period erupted a big debate among the economists and policymakers, as it was believed to have poverty reduction impacts (see Burgess & Pande, 2005).

Moreover, during post-liberalisation periods many foreign and private banks were also welcomed to operate in the Indian market. With the operation of these banks, it was expected that outreach and penetration of banking service would increase in India. Similarly, the rise of microfinance institutions and self-help groups (SHGs) were considered as an unprecedented trend in India, which immensely helped linking the members of the SHGs with formal sector banking (Jung, 2008; Muthu, 2021).

Similarly, during the post-2000 periods, a number of pro-financial inclusion policy initiatives were initiated by the formal banking system in India. Such policies include the formation of financial inclusion committee, implication of Know Your Customer norms, introduction of no-frill account, Direct Benefit Transfer scheme, and the Pradhan Mantri Jan Dhan Yojana (PMJDY), etc.

Despite these initiatives, about 37% of the total population is still excluded from the formal financial system in India (Sharma & Chatterjee, 2017). Is this poor financial inclusion an outcome of the low level of human development in India? This article examines the interlinkages between financial inclusion and human development in Indian states to come out with better policy outcomes that would help sustain the process of inclusive development in India.

This article is organised into six sections. The second section provides a brief discussion on the theoretical connections between financial inclusion and human development, while the third section reviews past studies and outlines the research gaps and contributions of this study. Fourth section explains the data, methodology for the construction of financial inclusion and human development indicators, and econometric tools used for the empirical estimation. Fifth section provides the empirical results and discussion. Finally, sixth section concludes the article along with a discussion on policy implications.

Linkages Between Financial Inclusion and Human Development

One of the major objectives of human life is to have healthy and peaceful life. Hence, every human being chooses to have a healthy life, to be educated and to enjoy a decent standard of living. Since, it is expected that the extension of basic financial services through financial inclusion will directly assist to attain good health, education and a decent standard of living to the individuals, which will ultimately improve the human capability or human development (Figure 1). Professor Amartya Sen has defined human development as the process of expanding human capability. Sen’s concept of ‘Capability’ and ‘Functioning’ refers to the overall wellbeing of an individual through the availability of broad range of opportunities (Sen, 1990). The word ‘functioning’ indicates to the actual realisation of a set of capabilities by the individuals. Functions are the active realisation of one or more capabilities, that is, beings and doings that are the outgrowths or realisation of capabilities (Sen, 1990). In other words, capability is a combination of multiple functioning that is feasible to attain by the individuals. Therefore, providing a safe and affordable formal financial service is always considered as effective policy instrument to ensure a multiple functioning to individuals which ultimately produces a better level of human capability.

Similarly, it could be argued that poor people use their financial services to attain two main outcomes for improving their wellbeing, that is, (a) building resilience and (b) capturing opportunities (Belayeth et al., 2019). Building resilience refers to individual’s ability to prepare against the future adverse economic shocks. In this case, the availability of the formal financial system at an easy and affordable manner provides a chance to the poor to save money in order to save their family from unforeseen economic hardships. Whereas ‘capturing opportunities’ refers to individual’s ability to seize investment opportunities that improve their livelihood conditions (Swamy, 2019), with the easy accessibility of credit from the formal financial system, people can devote a chunk of that credit on improvement of their skill through acquiring better education and training, for obtaining decent jobs in order to gain more well-being in life.

A Brief Review of Past Studies

The relationship between financial inclusion and various dimensions of development has been well studied by the researchers. Past studies (Anwar et al., 2016; Chibba, 2009; Hussaini et al., 2018; Inoue, 2011, 2018; Kablana & Chhikara, 2013; Kim, 2016; Meager, 2019; Mookerjee & Kalipioni, 2010; Neaime & Gaysset 2017; Park & Mercado, 2017; Williams et al., 2017; Zhang & Posso, 2019) have found that financial inclusion plays a crucial role in the process of poverty reduction, and bridging the gap between rich and poor through lessening income inequality.

Moreover, a few other cross-country studies (Matekenya et al. 2020; Nanda & Kaur 2016; Ofosu-Mensah Ababio et al. 2019; Peria & Shin 2020; Qureshi & Xiong 2018; Sarma 2008; Sarma & Pais 2011) have found that financial inclusion has played positive role in improving human development. Similarly, in Indian subcontinent, some researchers have also tried to look after the interrelationship between financial inclusion and human development. Researchers like Kuri and Laha (2011) conducted a study among the Indian states and union territories (UTs) taking the time period from 1993 to 2004, to know the impact of financial inclusion on human development. The findings of the study show that an inclusive financial system enables the progression of human development through addressing the basic distortions in the level of human development. Gupta et al. (2014) conducted a study among the 21 major states to know the relationship between financial inclusion and human development. The result of the study shows that a positive correlation exists between these two variables. Similarly, recently Nanda and Kaur (2017) conducted a study with 25 states and 4 UTs of India to measure the relationship between financial inclusion and human development among the Indian states. The result of the study indicates that financial inclusion is high among the states like Delhi, Goa and Chandigarh throughout the period of the study. The study further reflects that southern region of the country has done extensive progress in financial inclusion. And states from North-East region are performing poor in terms of financial inclusion. With relation to financial inclusion and human development, the study shows that financial inclusion is an imperative policy measure to ensure human development.

From our journey of literature review, it is observed that amongst all the studies that have been conducted between financial inclusion and human development in the Indian states, either these studies are directed to examine the convergence between these two variables or to see the correlation between these two variables. There is dearth of studies showing the cause-and-effect relationship between these two variables. Furthermore, these studies calculated both the financial inclusion index and human development index through the distance-based approach given by UNDP, using limited components from financial access and human well-being indicators.

However, the current study differs from the earlier studies mainly in three ways. Firstly, this study uses a far wide range of indicators for constructing both the Financial Inclusion Index (FII) and Human Development Index (HDI). Secondly, unlike earlier studies, here the study uses principal component analysis (PCA) method to construct both the indexes. Thirdly, this study not only empirically examines the impact of financial inclusion on human development, but also examines the reverse causality from human development to financial inclusion. Hence, the policy measures derived from this study would be more useful.

Model Specifications, Variable Selection and Econometric Methods Used

On the Construction of Financial Inclusion Index

Previous studies (Arora 2010 1 ; Chakravarty and Pal, 2013 2 ; Gupte et al., 2012; Sarma, 2008 3 ) have mainly used either the analytical and hierarchical process or the axiomatic approach to compute financial inclusion index. Although these methods were quite appealing at times, but due their faulty and limited weighting mechanisms these methods were criticised for their effectiveness (see Lenka & Barik 2018).

To overcome these deficiencies, this study relies on the PCA 4 method. PCA not only allows to include a large number of indicators, but it also uses a unique and unbiased method of assigning weights to various indicators. In this study, we have used six financial access indicators to construct a single holistic financial inclusion index. The secondary data on these six indicators have been collected from the Scheduled Commercial Banks. These include (a) number of bank branches in proportion to 1,000 population (BB); (b) number of bank employees as the ratio of bank branches (BE); (c) deposit bank accounts in proportion to 1000 population (DBA); (d) credit bank account in proportion to 1000 population (CBA); (e) amount of deposit as the percentage of state GDP (DEP); and (f) amount of credit as the percentage of state GDP (CRE).

We first calculate the factor scores (weights) through their eigenvalues. Then factor score (weights) of each variable is calculated, and multiplied it with the respective original variable. Unlike, other methodologies, PCA assigns equal weight to every variable (Kendall 1939; Lenka & Barik 2018). Finally, we add them together to get the single value of the composite index for ith state for a particular time period t. Hence, for constructing a single index of financial inclusion, the following formula is used:

By expanding this equation, it can be expressed as

Here, FII i is the financial inclusion index; Wi is the weight of the factor coefficient, X is the respective original value of the component, and p is the number of variables used.

Finally, FII for all Indian states is calculated using these below cited variables

Here, the financial inclusion index for all the Indian states is calculated by adding together the entire factor scores (weights) and their respective original values. FII i is the financial inclusion index of ith state and W1, W2, …, W6 are the weights of different factor scores.

Computation of Human Development Index

In the UNDP methodology, 5 HDI is calculated using three important dimensions of development, namely. health, education, standard of living. While computing the HDI, first three separate indices for each of these aspects of development are calculated, and then the geometric mean of these indices is finally considered as HDI. For computation of health and standard of living indices, indicators like life expectancy at birth and per capita GNP are used. Whereas in the case of education index, three separate indicators, namely literacy rate, mean years of schooling and expected years of schooling are used with proper weights assigned to each of these indicators (UNDP, 1990). According to Santos and Alkire (2011), due to paucity of data on these indicators, this methodology is sometimes modified in case of developing countries. But studies like Lai (2003), Nguefack-Tsague et al. (2011) and Mylevaganam (2017) have used the PCA to compute HDI. According to these studies, arbitrary equal weighting of the three components by treating human development as a latent concept imperfectly captured by its three component indices. Hence, weights based on PCA correlation matrix are better because practically it assigned same weights each of the indicators used.

To avoid the above cited problem, we have used PCA method to calculate HDI 6 for 28 Indian states. The procedure to calculate state level HDI is the same like that of the calculation of FII. 7 The study uses nine indicators of human development covering three dimensions. The three dimensions are heath, education and standard of living. For the first dimension (i.e., health), the study considers five indicators such as infant mortality rate (IMR), death rate (DR), birth rate (BR), early health good (EHG) and ailment to total population (ATP). Similarly, for education dimension, the study has considered literacy rate (LIT), mean year of schooling (MYS) and expected year of schooling (EYS). For the third dimension (i.e., standard of living), the study has considered monthly per capita consumption expenditure (MPCE).

Finally, for calculating HDI for a particular state, the study follows the below given equation.

Here, after adding together all the factor scores (weight) with their original value, we get the final HDI score for each state. The term HDI i is the human development index of ith state, t is the time period, and W1, W2, …, W9 are the weights of different factor scores.

Econometrics Tools Used

Since, we have an unbalanced 8 panel data for 28 Indian states (23 years from 1993 to 2015). The study here runs one panel regression estimation with five different econometric models (i.e., fixed effect (FE), random effect (RE), panel corrected standard error (PCSE), feasible generalised least square (FGLS) and Hausman–Taylor panel regression (HTR) model. Reginal dummy (Reg-Dum) variables are also used as control variables to capture the impact of various regional characteristics on human development. Based on geographical location of states, Indian subcontinent is divided into six zones (i.e., Central Region, Eastern Region, Northern Region, North-East Region, Southern Region and Western Region). Hence, to capture six regional effects, the study has considered five dummies (to avoid the dummy variable trap). Finally, the following econometric model is specified to empirically examine the determinants of human development.

Model Specification

In the above model, the term HDI it is the composite index of all human development indicators for ith states at time period t, and here it is used in the dependent variable side. Similarly, in the independent variable side, the term FII refers to the composite index of financial inclusion indicators for ith states at time period t. The term Z it refers to the vector of four control variables, namely the log of social sector expenditure (SSE), per capita state gross domestic product (PCSGDP), rural population (R_POP) and the log of capital receipt (CR) for each state at the time period t. The term Reg_Dum it refers to the zonal dummies that have been considered to capture the zonal effect on human development. And finally, the term εit indicates the error term.

On Estimation Procedures

Before running the regression models, the study provides the summary statistics of the variables used in the regression analysis (see Table 1). First, we run FE and RE models, and based on the result of the Hausman test, an appropriate estimated (between FE and RE) result is interpreted. Furthermore, in order to remove the problem of autocorrelation and heteroscedasticity in the used data, the study uses PCSEs and FGLS for checking the robustness of the results, as both PCSEs and FGLS are not sufficient to solve the issue of endogeneity or any potential problem of variables omission. To overcome this problem, the study applies the Hausman–Taylor regression (RE_HTR) model and re-estimates the results (see Table 3). Finally, to check the possible reverse causality from human development to financial inclusion, we have estimated Pairwise Dumitrescu–Hurlin panel Granger causality tests (see Table 5).

Summary Statistics.

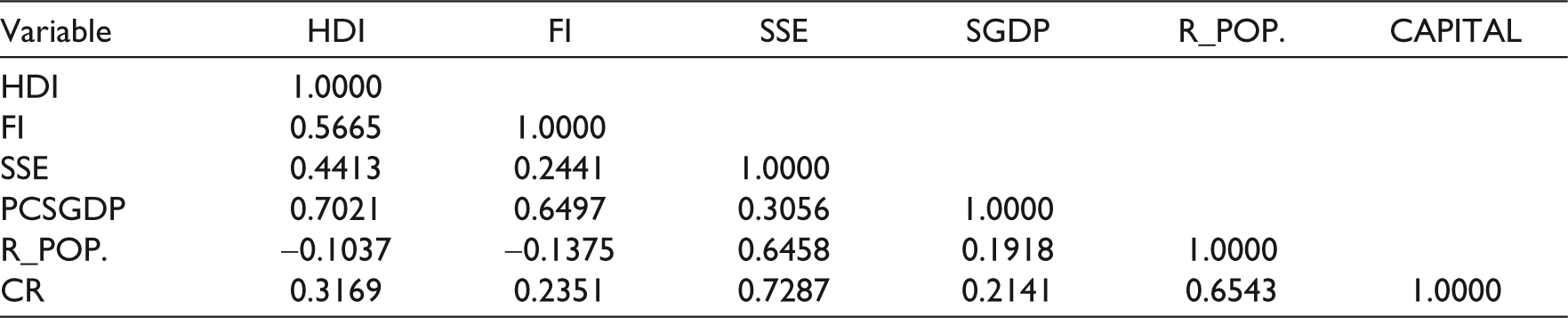

Correlation Matrix.

*, ** and *** imply statistically significant levels at 10%, 5% and 1%, respectively.

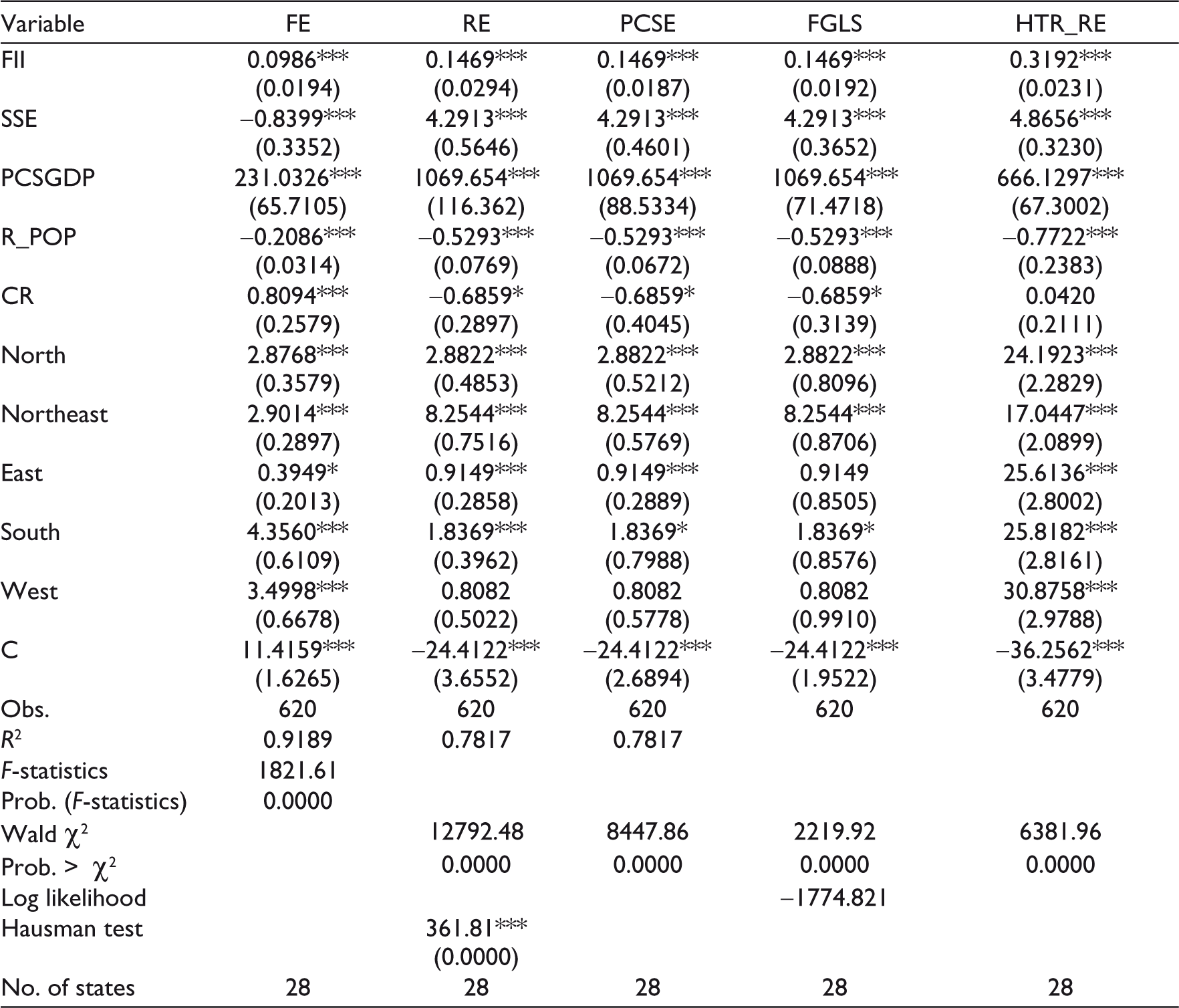

Regression Results of Financial Inclusion and Human Development-Dependent Variable: Human Development Index (HDI).

Empirical Results and Discussions

At the outset, we find a positive and statistically significant correlation (see Table 2) between financial inclusion and human development. Moreover, we find that other control variables such as the SSE, PCSGDP and CR have a positive correlation with HDI. However, we find a negative correlation with human development and R_POP. That means people have a number of socio-economic problems (e.g., illiteracy, lack of employment opportunities and low per capita income). Hence, the higher presence of socio-economic problems among the rural people can negatively hamper the progress of human development.

Our main variable (i.e., financial inclusion) has statistically significant and positive impact on the dependent variable (the composite index of human development). Moreover, we have also found statistically significant impact of other four control variables on the human development. While SSE, PCSGDP and CR have reflected statistically positive estimates, percentage of R_POP has produced a statistically negative estimate. This result is not only consistent with our theoretical argument, but it also supports the findings of studies in other countries, such as Lai (2003), Nguefack-Tsague et al. (2011) and Mylevaganam (2017).

Since financial inclusion has positive and significant impacts on human development, it can be argued that ensuring a higher level of financial inclusion is going to improve the status of human development in Indian states. The empirical finding depicts that across the five model’s specification, our positive results for financial inclusion on human development remain same (see Table 4). This result is consistent with the findings of Datta and Singh (2019), Kuri and Laha (2011), Laha (2015), Matekenya et al. (2020), Nanda and Kaur (2016, 2017), Ofosu-Mensah Ababio et al. (2019), Peria and Shin (2020), Qureshi and Xiong (2018) and Raichoudhury (2016).

Our findings support the hypothesis that financial inclusion could work as prominent means to improve the human development condition among the Indian states. This finding could be understood through the development made by the public sectors banks by extending their financial products and services across the Indian states. There is no doubt that over the years, specifically the post-2000 period has witnessed tremendous growth in banking outpost (Barik & Sharma, 2019), starting from the expansion of bank branches to the rural hamlets, providing credit to the priority sectors and including poorer section of people through easy banking process. Hence, the results demonstrate that financial inclusion captured by various indicators of financial availability, accessibility and usability would have helped the individuals to spend more on their health, education and consumption. That means with the expansion of more credit, and the increase in saving, the individuals are expected to promote their expenditure in areas that improve human development, such as education, food consumption and healthcare.

Furthermore, access to credit can also lower unemployment and raise income level by encouraging business start-up among the individuals. Fulfilment of various socio-economic goals is also linked with the process of human development improvement. Hence, providing more employment and boosting income can also assist the individuals to spend more on their capabilities that help to boost the overall human development process.

Furthermore, the reason for the positive impact of SSE is that the post-liberalised Indian has seen tremendous growth in the SSE. Every year, both the central government and various state governments are spending huge amount of money for the well-being of the general citizens. Over the years, the government has realised that one of the major roles of a democratic government is to improve the quality of life of the people, which can be carried out by incurring public expenditure in areas of health, education and other social services (Agarwal, 2015). The public spending on health and education are always considered as the merit goods which have positive externalities. Correspondingly, the market sources have failed to provide the basic amenities like health and education to the poorer section of people. As a result of this, government intervention through public expenditure has become an indispensable requirement for the well-being of people. It is always assumed that when the government expand its public expenditure, this helps to improve the human development condition of the states. Hence, our empirical result supports the hypothesis and depicts that SSE has positive and significant impact on the human development condition of the 28 Indian states.

Similarly, as expected, the PCSGDP has positive impact on human development. It is quite obvious that with the rise in income levels, people will tend to spend more on basic consumption goods up to a threshold level (following angels’ law), but the share of spending on healthcare, and education will start rising. This has positive implication on enhancing their human development condition. Statistically positive coefficient of CR implies that with rising capital inflow, the state economy is likely to improve the human development condition of the state through various public expenditures.

However, our control variable ‘R_POP’ is showing a negative and significant effect on human development. That means the presence of higher percentage of rural people (an indicator of lack of urbanisation) can hamper the process of human development. As it is known that India’s rural area lacks better education and healthcare facility, low literacy, and less income, hence, the greater presence of rural population can hinder the improvement in human development condition in the Indian states.

Finally, our regional dummies indicate that our reference categories (i.e., the central region) lack in term of human development. Although all five region dummies have statistically positive coefficients, the absolute value of the Eastern region and North-East region is relatively smaller, whereas the coefficients of Southern and Western region are relatively higher. This clearly reveals that interregional differences and disparities of human development in India. Hence, for reducing this disparities of human development, financial inclusion should be given topmost priority in the states of these backward regions.

On Casual Connections

The constant credit cash flow through financial inclusion can assist to raise income and reduce poverty. Similarly, credit can also encourage the individuals to invest on their various developmental activities like building housing/toilet, spending money on better education, healthcare, acquiring new working skill and on other activities which improves the well-being of the individuals. On the other hand, rise in income and level of human development can equally inspire the people to participate in formal banking activities like saving, deposit, withdrawal, etc. Hence, both the variables can cause each other by nature. Therefore, this study attempts check the feedback loop between financial inclusion and human development. In order to materialise the above cited objective, the study used Pairwise Dumitrescu–Hurlin Panel Granger Causality test. Before moving towards Pairwise Dumitrescu–Hurlin Panel Granger Causality test, the study checked the stationarity of the data through applying Im–Pesaran–Shin and Fisher-type test for the period of 1993–2015 and found that both variables FII and HDI are not stationary in level as well as in first difference (Table 4).

The causality result suggests a bidirectional relationship between them (Table 5). That means there exists a synergic connection between financial inclusion and human development, which indicates that both financial inclusion and human development cause one another. That means the process of financial inclusion not only helps to improve the human development base of the states, but it is also positively being influenced by the level of improved human development conditions of the states. Hence, policies that ensure higher level of human development would also help achieve greater level of financial inclusion and inclusive development in Indian states.

Unit-Root Test.

Pairwise Dumitrescu–Hurlin Panel Granger Causality Test Between Financial Inclusion and Human Development.

Concluding Remarks

An easy and affordable access to finance works as a productive means to enhance the condition of human well-being by encouraging the individuals to spend money on their developmental activities like expenditure on health, education, sanitation, housing, employment creation, etc. Understanding the significance of financial accessibility in human life, this study endeavours to empirically examine the impact of financial inclusion on human development in Indian states during the post-liberalisation period. Moreover, it examines the feedback loop between financial inclusion and human development, to come out with better policy outcomes that help the process of inclusive development in India. To construct the state-wise indexes of financial inclusion and human development, PCA method is used. Furthermore, this study uses FE, RE, PCSE, FGLS and HTR-RE regression models to empirically verify the influence of financial inclusion on human development. The empirical findings of this study depict that financial inclusion has a positive and significant effect on human development. That means the process of financial inclusion has played an important role for improving human development condition among the Indian states in the post-liberalised period. Similarly, our results from control variables show that SSE, PCSGDP and CR have positive effect on human development whereas R-POP has a negative impact on human development. Furthermore, Pairwise Dumitrescu–Hurlin Panel causality results illustrate that a reverse causal connection also exists from human development to financial inclusion, reflecting a synergic connection between the two. Hence, to achieve long-run inclusive development and to improve the level of human development, financial inclusion should be given top most priority in Indian states.

Limitations and Scope for Future Research

Like any other studies, this study has certain limitations. Observing Indian economy from the post-liberalisation time period, it cannot be denied that over the years, Indian economy has witnessed some major policy changes in the country. In this context, researchers (like Barik and Sharma, 2019; Lenka & Sharma, 2017) have confirmed that the process of financial inclusion has witnessed a rapid growth from post-2000 onwards. Similarly, the implication of Pradhan Mantri Jan-Dhan Yojana in 2014 has also significantly helped to boost the financial inclusion in India (see Nimbrayan et al., 2018; Singh et al., 2021; Verma & Garg, 2016). Hence, from this point of view, it is always a matter of inquiry that how these policies have impacted the process of financial inclusion and human development in various Indian states? In order to find out the appropriate answer for this question, any study applying structural break methodology can be more useful. However, this study has not used the structural break methodology here; therefore, the study recommends any further study using the structural break methodology can provide us more information in this regard.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.