Abstract

The purpose of this study is to empirically investigate the vindication of the savings-led growth hypothesis for the Malaysian economy with the long-run TYDL version of the Granger causality test—Toda and Yamamoto (1995) and Dolado and Lütkepohl (1996). This study used the quarterly sample from 1970:Q1 to 2008:Q4. The recursive regression procedure will also incorporate into the TYDL causality test to measure the stability of the savings-led growth hypothesis in the long-run. Our empirical results support that the savings-led growth hypothesis is a long-run phenomenon and stable over time. Therefore, the Malaysian dataset supports the endogenous growth theory.

JEL Classification: C22, E21, O16

INTRODUCTION

Are high-savings countries growing faster? Logically, to achieve economic growth, one must invest. To encourage investment, one should save. Therefore, savings may play an important role in the process of economic growth and development. The role of savings in economic growth has long been debated and many empirical studies have been conducted to examine the vindication of the savings-led growth hypothesis. In general, two famous groups of economic thought explained the savings-led growth hypothesis. Harrod (1939) and Domar (1946) were the first group of economists that systematically modelled the role of savings in economic growth. They claimed that the speed of economic growth depends on the ability to save, as a high savings rate will increase the rate of investment and hence trigger economic growth. Solow (1956) added that although savings was an important source for economic growth through its impact on capital formation, it does not affect economic growth in the long-run because of the assumption of diminishing returns to scale and because technological progress is assumed to be exogenous. Therefore, the neoclassical growth economists believed that savings-led growth is just a transitory or short-run phenomenon rather than an endless process. Ironically, the endogenous growth theory proposed by Romer (1986) argued that technological progress is determined endogenously and the production function is subject to increasing returns to scale. Moreover, savings are required to finance technological progress. Therefore, the endogenous or new growth theory articulated that savings-led growth is a long-run phenomenon.

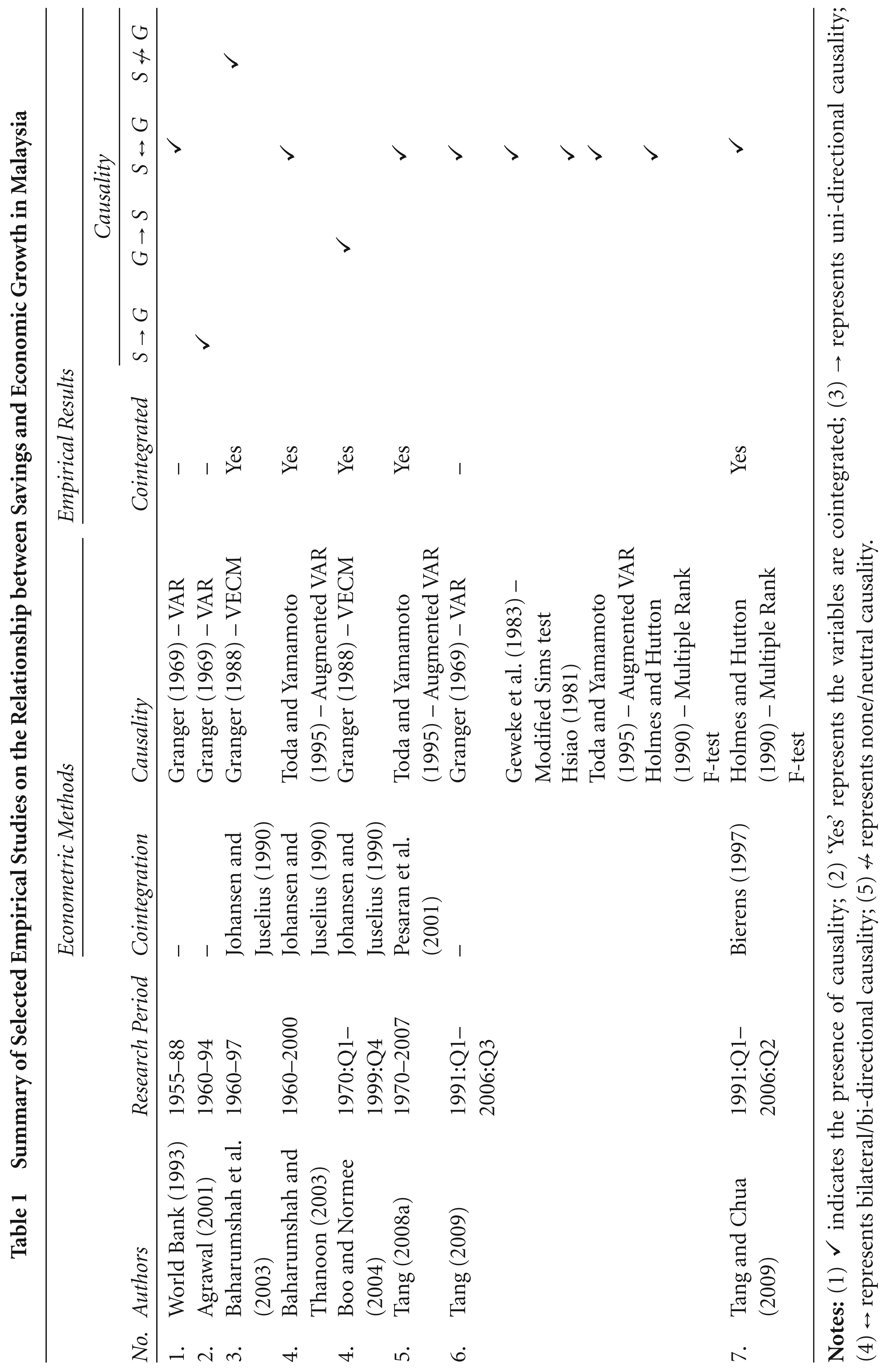

Given the policy relevance and the controversy among growth theorists, many researchers have empirically investigated the validity of the savings-led growth hypothesis in developed and developing economies. For this reason, it is implausible for the present study to comprehensively review all the relevant studies within the ambit of this article. The objective of this study is to review some empirical studies pertaining to the causal relationship between savings and economic growth in the Malaysian economy. A summary of the preceding studies on the subject is reported in Table 1. In general, Table 1 shows that existing research efforts failed to provide clear evidence for the savings-led growth hypothesis. The vindication of the savings-led growth hypothesis is of concern because it is directly related to the formulation and implementation of appropriate growth policy. If savings-led growth is a long-run phenomenon as indicated by the endogenous growth theory, enhanced savings may be a potential long-run stimulus for economic growth policy. Otherwise, alternative growth policies should be implemented to achieve sustainable economic growth in the long-run.

Summary of Selected Empirical Studies on the Relationship between Savings and Economic Growth in Malaysia

Summary of Selected Empirical Studies on the Relationship between Savings and Economic Growth in Malaysia

Notes: (1) ✓ indicates the presence of causality; (2) ‘Yes’ represents the variables are cointegrated; (3)

Using annual data from 1955 to 1988, World Bank (1993) attempted to investigate the causal relationship between savings and economic growth within the bi-variate vector autoregression (VAR) framework. The study found that savings and economic growth Granger-cause each other. In another study, Agrawal (2001) performed an empirical analysis on seven Asian economies with the residuals-based cointegration and Granger causality tests. In the case of Malaysia, the study found that savings and its determinants are stationary at different orders. Therefore, the residuals-based cointegration test cannot be used to examine the presence of a long-run equilibrium relationship. For this reason, the above authors assumed that savings and its determinants for Malaysia are not cointegrated. Therefore, the Granger causality test based on the first difference VAR framework was used to examine the causality between savings and economic growth. The authors found uni-directional causality running from savings to economic growth. On the contrary, Baharumshah et al. (2003) and Boo and Normee (2004) used the multivariate Johansen and Juselius (1990) cointegration and Granger causality tests to examine the relationship between savings and its determinants. They found that savings and its determinants for Malaysia are moving together in the long-run; therefore, the Granger causality test within the vector error-correction model (VECM) was used to examine the direction of causality between savings and economic growth.

Contrary to earlier studies and also to the growth theories, Baharumshah et al. (2003) found no causality between savings and economic growth, while Boo and Normee (2004) observed that economic growth Granger-causes savings in Malaysia instead of the opposite. However, Baharumshah and Thanoon (2003) re-investigated the long-run causal relationship between savings and economic growth in Malaysia using the Toda and Yamamoto (1995) causality approach. They found that savings and economic growth in Malaysia is a bi-directional causality in the long-run. Furthermore, Tang (2008a) proposed to incorporate the modified dependency ratio into the savings–growth relationship for Malaysia. In addition to that, the author also used a relatively new cointegration test developed by Pesaran et al. (2001)—the bounds-testing approach to examine the presence of a long-run relationship between savings and its determinants. The TYDL developed by Toda and Yamamoto (1995) and Dolado and Lütkepohl (1996) was used within the augmented-VAR system to verify the causal relationship between savings and economic growth in Malaysia. The authors observed that savings and its determinants are cointegrated and the TYDL Granger causality test implied bilateral causality between savings and economic growth over the sample period of 1970 to 2006. The causality result is consistent with the finding of the World Bank (1993) and Baharumshah and Thanoon (2003), but contradicted earlier studies. Recently, Tang (2009) attempted to investigate whether the causal inference between savings and economic growth in Malaysia is sensitive to the particular causality tests employed to ascertain the causal relationship. To achieve the objective of his study, the author employed five different causality techniques, namely, the Granger (1969), Geweke et al. (1983), Hsiao (1981), Toda and Yamamoto (1995) and Holmes and Hutton (1990) causality approaches. Interestingly, the author found bilateral causality between savings and economic growth regardless of the causality technique employed. The author concluded that causality methods do not influence the causality results. Similarly, using quarterly data from 1991:Q1 to 2006:Q3, Tang and Chua (2009) also detected bilateral causality between savings and economic growth in Malaysia with the Holmes and Hutton (1990) causality test.

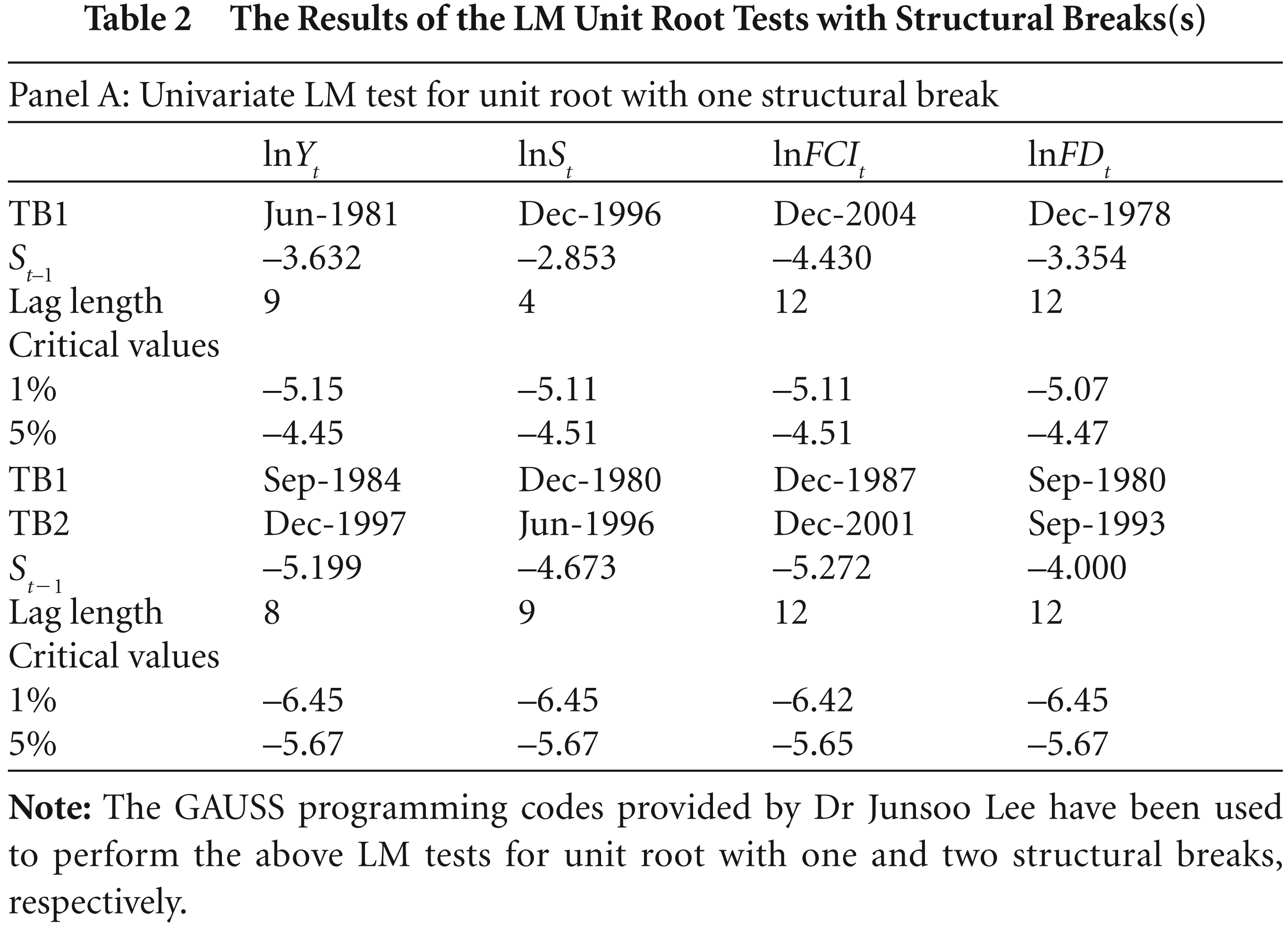

Motivated by the paradoxical empirical evidence presented above, this study attempts to re-investigate the existence of the savings-led growth hypothesis for the Malaysian economy from 1970:Q1 to 2008:Q4. It differs from the earlier studies in at least three dimensions. First, none of the Malaysian studies has taken into consideration the effect of structural break(s) in the unit root tests. Perron (1989) pointed out that the conventional unit root tests such as Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) may be biased when the time series pertain to structural change. Therefore, apart from using the conventional unit root tests, we also apply the Lagrange Multiplier (LM) unit root tests with one and two structural breaks developed by Lee and Strazicich (2003, 2004) to fill the detected gap. This is because the ADF-type structural break(s) unit root tests (e.g., Lumsdaine and Papell, 1997; Zivot and Andrews, 1992) tend to select the incorrect breakpoints (see Lee and Strazicich, 2001). Second, we employ the TYDL Granger causality test within the augmented-VAR system to ascertain the direction of causality in the long-run. Nevertheless, Hacker and Hatemi-J (2006) found that the MWALD test statistics bias rejected the null hypothesis of non-Granger causality. Therefore, a correction has to be done to avoid this bias. Following Hacker and Hatemi-J (2006), we employ the leveraged bootstrap simulation approach to yield robust causality test results. Finally, this study contributes to the empirical literature by testing the persistency or the stability of the savings-led growth hypothesis by incorporating the recursive regression procedure into the TYDL Granger causality test as suggested by Tang (2008b). To the knowledge of the author, no study has analysed the stability or persistency of the savings-led growth hypothesis using the recursive causality procedure. The stability of the savings-led growth hypothesis is of concern because it is an important criterion for modelling appropriate growth policies. If the causal relationship is unstable, the macroeconomic policy initiatives that encourage savings may be less effective in stimulating economic growth in the long-run.

The remainder of this study is organised as follows. In the next section, we provide an overview of savings in Malaysia. In Section 3, we will briefly discuss the econometric techniques used in this study. Section 4 reports the source of data and empirical findings of this study. Finally, the concluding remarks of this study will be presented in Section 5.

Malaysia is a small open economy located in the Southeast Asian region. According to Tang (2008a), Malaysia has the second highest savings rate among countries in the ASEAN region. Figure 1 provides the savings rates (i.e., domestic savings, private savings and public savings) as a percentage of GDP in Malaysia from 1970 to 2008. It can be seen that savings rates in Malaysia increase over the analysis period. On average, domestic savings, private savings and public savings are approximately 35 per cent, 19 per cent and 11 per cent of GDP, respectively. In addition, domestic savings reached its peak at 42 per cent of GDP in 1996. However, the savings rate dropped to 31 per cent in 1997 due to the Asian financial crisis that hit the Malaysian economy. The crisis triggered a massive outflow of foreign capital and also caused the depreciation of Malaysian currency. Hence, savings rates in Malaysia dropped drastically from 42 per cent to 31 per cent of GDP.

Based upon the plots, we observe that the behaviour of domestic savings in Malaysia is more likely to be correlated with private savings than public savings, especially before 1990. Specifically, private savings in Malaysia contributes around 15 to 20 per cent of GDP. However, public savings contributed less than 10 per cent of GDP in Malaysia, especially during the 1970s and 1980s. Nonetheless, since the 1990s, the contribution of public savings increased to approximately 15 per cent of GDP in Malaysia. With respect to the increase in public savings, Ang (2009) noted that such an increase is achieved due to cutting of public consumption rather than increase in taxes in Malaysia. In summary, both private and public savings are the main sources of savings in Malaysia and they are equally important in contributing to total domestic savings in the economy.

LM Unit Root Tests with Structural Break

In this section, we discuss the LM unit root test with one and two structural breaks introduced by Lee and Strazicich (2003, 2004). The Model C and Model CC for one and two structural breaks LM unit root tests will be estimated. This is because Sen (2003) noted that Model C and Model CC typically performed better than the other models. Therefore, we estimate the following model to determine the order of integration with one and two structural breaks.

Here,

TB1 and

This study uses the Granger causality test proposed by Toda and Yamamoto (1995) and Dolado and Lütkepohl (1996)—TYDL to verify the long-run causality direction between the candidate variables

Where k is the optimal lag length for the VAR system determined by AIC. Even though Toda and Yamamoto (1995) noted that the maximum order of integration for the economics series are commonly at either I(1) and I(2) process, according to simulation results produced by Dolado and Lütkepohl (1996) the performance of

From Equation (2), the null hypothesis of

From the above notation, the augmented-VAR(p) model together with the constant term (b) can be expressed compactly as below:

The estimated

where T is the total number of observation and p is the lag length in the augmented-VAR system. Nevertheless, it is noteworthy to point out here that the additional lag order, that is,

Next, the residuals-based bootstrapping approach is adopted to compute the critical values for the MWALD test with the empirical distribution. Following Davidson and MacKinnon (2004), 1000 times of bootstrapping will be performed to yield the leveraged bootstrap critical values. As a common interpretation for statistical inferences, the null hypothesis of non-Granger causality is rejected if the computed MWALD test statistic is greater than the bootstrapped critical values. 1

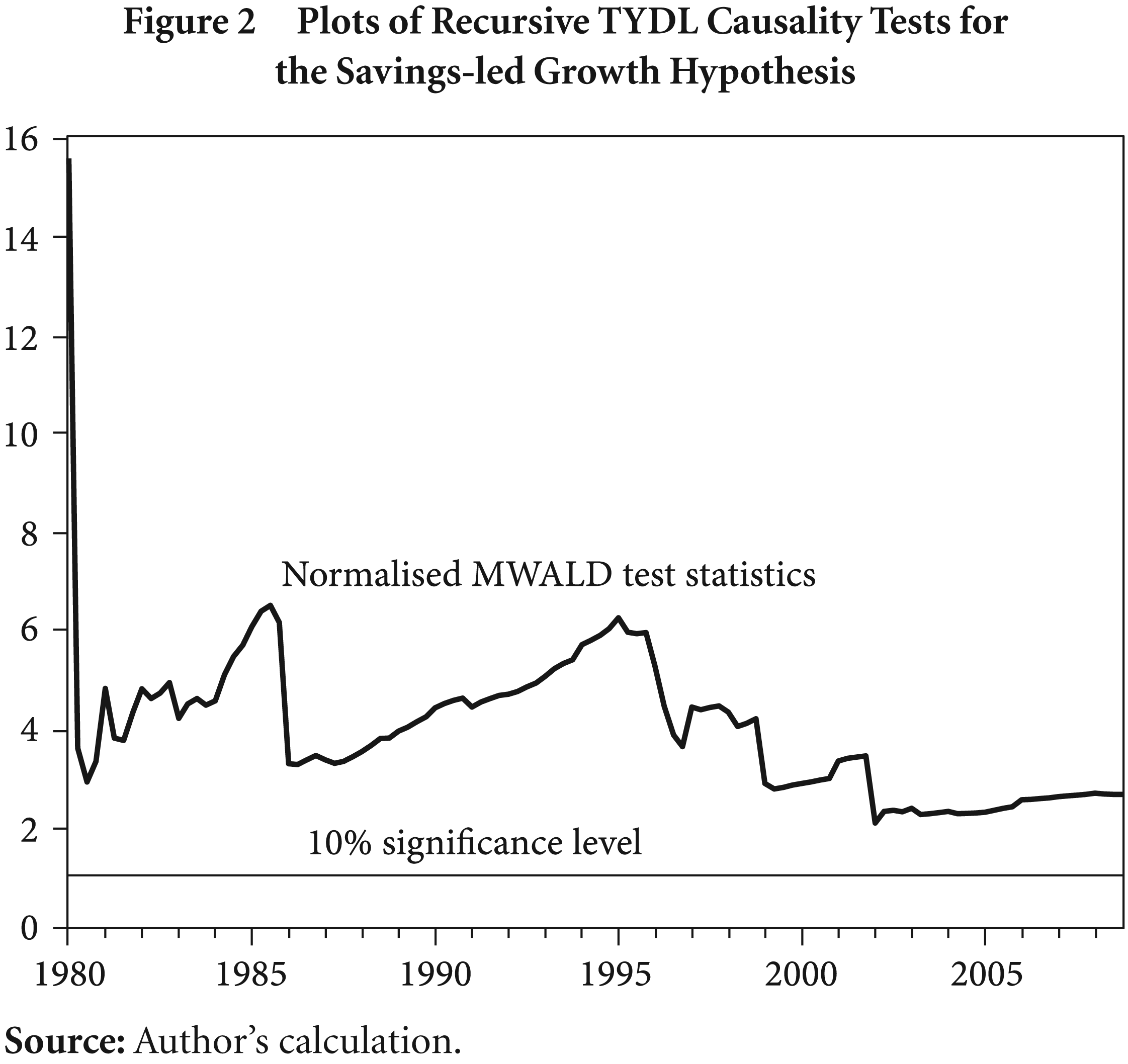

This section will briefly discuss the estimation procedure for the recursive regression-based TYDL causality test. The idea of the stability of the causal relationship was raised by Tang (2008b). His study noted that the causal relationship may be not be stable owing to frequent changes in the global economy and the political environment. In this regard, Tang (2008b) proposed recursive regression-based causality tests to examine the stability of the causal relationship. The major advantage of this recursive causality test is that it can be used to examine the volatility or fluctuation of the causal relationship over time. In other words, we can visually inspect the stability of the causal relationship over the analysis period. The recursive regression-based TYDL causality test can be conducted by first estimating the augmented-VAR system with the initial sub-sample of T observations. Then, a new observation will be added at the end of the sub-sample without deleting the first observation (i.e., T + 1). The causality test will be performed for each sub-sample. For interpretation, the computed MWALD statistics will be normalised by the 10 per cent

EMPIRICAL RESULTS

Source of Data

This study examines the savings-led growth theories for Malaysia within a multivariate framework. It uses the Gandolfo (1981) interpolated quarterly data from 1970:Q1 to 2008:Q4 for real gross domestic product (GDP), real gross domestic savings (GDS), real foreign capital inflows (FCI), and a financial development indicator proxy of the ratio of M2 money to GDP. The interpolated data was used in this study to increase the statistical test power and avoid the size distortion problem (Zhou, 2001). The raw data for interpolation were extracted from the World Bank’s World Development Indicators (WDI) and Bank Negara Malaysia’s Monthly Statistical Bulletin. All data were transformed into the natural logarithm form. The analyses in this study were conducted with GAUSS 9.0 and Eviews 6.0 software.

Unit Root Tests Results

According to time series econometric literatures, the regression results may be spurious if the variables are non-stationary (Granger and Newbold, 1974; Phillips, 1986). Thus, it is interesting to examine the order of integration for each variable to avoid spurious correlation problems. Although the TYDL version of the Granger causality test does not require pre-testing of the unit root, the unit root test result can shed some light on the order of

To ascertain the order of integration, we begin by applying the conventional ADF and PP unit root tests. Interestingly, the conventional unit root test results suggest that the variables under investigation

The Results of the LM Unit Root Tests with Structural Breaks(s)

The Results of the LM Unit Root Tests with Structural Breaks(s)

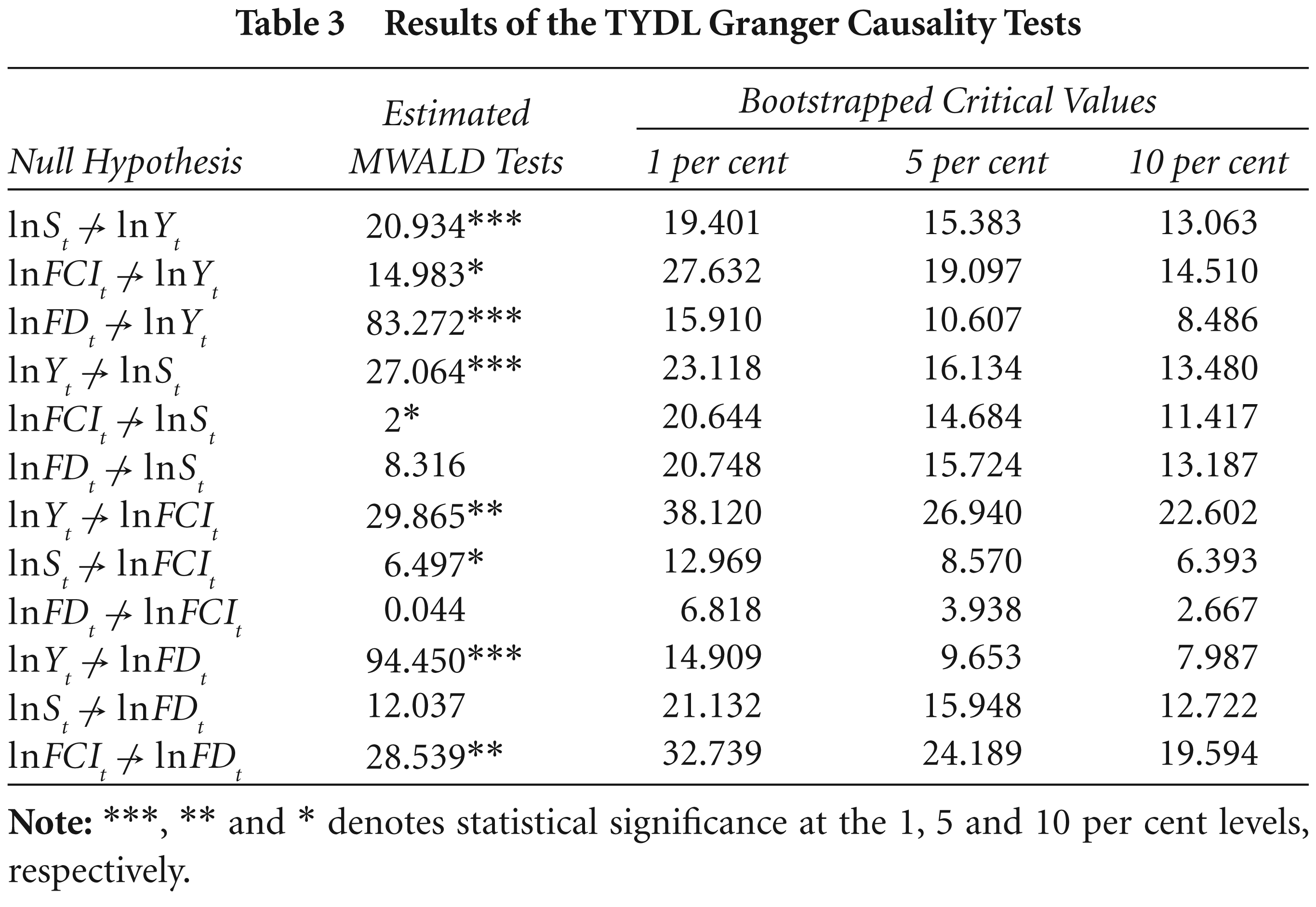

In this section, the long-run causal relationships between the candidate variables

As opposed to the neoclassical growth theory, our empirical results indicate that the savings-led growth hypothesis is a long-run phenomenon. In other words, the Malaysian dataset supports the endogenous growth theory. This is not an unexpected result as Malaysia is the second-highest savings economy among the Association of Southeast Asia Nations (ASEAN), which has attracted large amounts of foreign direct investment that will simultaneously enhance technological progress (see Aghion et al., 2009). Therefore, the discovery of a savings-led growth hypothesis in the long-run is plausible. Indeed, this is consistent with our causality result that savings Granger-causes foreign capital inflows. Towards a knowledge-based economy (K-economy), expenditure on education and health as a proportion of total government development expenditure in Malaysia (i.e., human capital investment) increased steadily during the period from 1970 to 2007.

Results of the TYDL Granger Causality Tests

Results of the TYDL Granger Causality Tests

During the decade 1981–90, the proportion of total expenditure on education increased from 7 per cent to 15 per cent, while that on health rose from 1 per cent to 4 per cent. The proportion of expenditure on education further increased from 13 per cent in 1991 to a peak of 35 per cent in 2002. This implied that the Malaysian government has recognised the importance of human capital investment in stimulating economic growth and development. According to Romer (1986), an increase in the investment in human capital will enhance the labour force and capital productivity and efficiency, because human capital is not subject to diminishing returns. Meanwhile, savings is a prerequisite for human capital investment; hence savings Granger-causes economic growth in the long-run.

Although we have observed strong evidence to support vindication of the savings-led growth hypothesis in the long-run, the causal relationship may not be stable over time, so we also examine the stability of the savings-led growth hypothesis with the recursive regression-based TYDL Granger causality tests. In order to implement the recursive regression-based causality test, we have to decide the initial sample size for estimation. To serve the purpose of long-run causality and also to avoid the size distortion problem, we begin the estimation with a ten-year sample (i.e., 40 observations). For interpretation, the computed MWALD statistics for each sample (i.e., T + 1) will be normalised by the 10 per cent

The aim of this study is to empirically examine the vindication of the savings-led growth hypothesis for Malaysia within a multivariate framework through the TYDL Granger causality test. The sample period for the study was from 1970:Q1 to 2008:Q4. With the TYDL Granger causality evidence, we conclude that the savings-led growth hypothesis for Malaysia is valid in the long-run. Importantly, the recursive regression-based TYDL causality test also affirmed that the savings-led growth hypothesis is valid and stable over the sample period. These findings are in tandem with the new growth theory that increases in savings will affect capital accumulation and thus stimulate economic growth in the long-run.

Although the findings of this study affirmed that savings is necessary, it is not a sufficient condition for economic growth. To effectively promote economic growth, available savings in Malaysia must be mobilised and channelled into productive investment. Since most of the available saving deposits are in financial institutions, we advise decision-makers to promote financial development and liberalisation in order to free available resources and channel them into productive sectors for investment. Moreover, priority should be given to export-oriented and manufacturing industries because they are the best examples of productive industries that gain foreign exchange earning and create more employment opportunities in the country. In doing so, the available savings in Malaysia can be effectively utilised and Malaysia’s long-term economic growth can be sustained.

Footnotes

Acknowledgements

The author would like to thank an anonymous reviewer for his/her valuable comments and suggestion on the earlier draft of this research paper. In addition, the author would like to thank Soo Yean Chua for his valuable comments and suggestions on an earlier draft of this manuscript. The author would also like to express his appreciation to Lee Junsoo and Abdulnasser Hatemi-J for sharing their programming codes to perform the econometric analysis. I am solely responsible for errors (if any), views and conclusions.