Abstract

Australia has one of the highest per capita carbon emissions, and its energy sector contributes significantly to the country’s carbon emissions. Renewable energy and climate change call for a shift from fossil fuels to low-carbon technologies for energy production. Policies aiming to reduce carbon emissions are perceived by many people as leading to higher living costs, but changes in energy policies can also lead to economic gains in the presence of revenue recycling. This article applies a computable general equilibrium approach to study the effect of energy tax in the Australian economy. Four different scenarios of green tax reform (GTR) are simulated to test the employment double dividend (EDD) potential. All four scenarios simulate changes in energy tax and one of four tax revenue recycling policies including (a) value added tax reduction, (b) payroll tax reduction, (c) goods and services tax (GST) reduction and (d) a mixture of all three recycling policies. The results show strong EDD potential of GST and payroll tax reduction when used along with energy tax in a revenue-neutral GTR approach. The study also presents a comparison of an optimal EDD inducive policy design between the European and Australian GTR approaches.

Introduction

Globally, Australia ranks 18th in total energy consumption (EIA, 2017a) and 7th in per capita energy consumption (The World Bank, 2015). Only 6 per cent of its energy is produced using renewable sources, and the rest comes from coal (32%), petroleum and other liquids (38%), and natural gas (24%) (EIA, 2017b). With a population of 25.28 million (ABS, 2019), Australia accounts for 1.08 per cent of global CO2 emissions (Muntean et al., 2018) and ranks very high on per capita CO2 emissions (The World Bank, 2019). Electricity generation is the highest source of emissions, accounting for 33.1 per cent of total emissions, followed by stationary energy (19.3%), transport (18.8%) and agriculture (12.7%) (Department of the Environment and Energy, 2019). These statistics imply that the prime cause for Australia’s high emissions is an overdependency on coal, especially brown and black coal, which has very high emissions intensity, along with the use of other fossil fuels in energy production. A significant reduction in emissions is possible by substituting coal for other renewable or even non-renewable energy (for example, LNG) (Hardisty et al., 2012). The Australian Government, through the Paris Agreement, is committed to reduce its emissions to 26–28 per cent on 2005 levels by 2030 (Australian Government, 2015a) which is complimented by a renewable energy target (RET) of 23.5 per cent of Australia’s electricity generation being from renewable sources by 2020 (Australian Government, 2015b). This target has been met and is currently being reviewed, with state and territories having more ambitious targets in place.

Climate change and associated temperature variability and extremes have a myriad negative consequences for Australia’s economy, including the wheat industry (Howden & Jones, 2004), livestock systems (Howden et al., 2008), wine industry (Webb et al., 2008), avifauna (Chambers et al., 2005), wool industry (Harle et al., 2007), broadacre crops (Anwar et al., 2015) and aquaculture (Doubleday et al., 2013). The increasing frequency of severity of natural disasters such as bushfires (Lucas et al., 2007), droughts (Nicholls, 2004) and floods (Whetton et al., 1993) can also be linked to carbon emissions and climate change. Despite all scientific evidence, the general population has had a mixed reaction to policies aimed at curtailing emissions (Akter & Bennett, 2011), and, while the majority see a threat in climate change, many also fear the economic costs of taking steps to mitigate it (Lowy Institute, 2019). Australia’s political environment is divided over climate change issues, and the political influence on mitigation policy is evident as Australia is the first developed country to annul carbon tax (Taylor & Hoyle, 2014). Therefore, robust public support for emission reduction measures is needed to gain bipartisan political willingness. We argue that such support requires not only environmental awareness but also additional economic benefits for the general population.

The theoretical framework of this article is predominantly based on the double dividend (DD) hypothesis and the optimal taxation theory. The optimal taxation theory suggests that a tax system should be designed in a way that maximizes social welfare. The literature on whether the contemporary tax system is optimised or not is divided; however, according to Mankiw et al. (2009), optimal taxation is an ongoing process, meaning there is room for further optimisation. It is also accepted that, in the presence of negative externality (e.g., carbon emissions), Pigouvian taxes can make the tax system more efficient (Cremer et al., 1998). DD hypothesis, on the other hand, argues that taxing industrial and household activities that pollute the environment, and then recycling the tax revenue back to the economy through a reduction of other distortionary taxes (e.g., labour tax), can be beneficial for the environment and can also reduce the welfare cost of taxation (Tullock, 1967). These are known as the primary dividend (environmental dividend) and secondary dividend (economic dividend), and this whole process of reducing distortionary taxes for the environmental taxes is known as green tax reform (GTR). One branch of the DD hypothesis focuses on employment as the second dividend, which is also known as the employment double dividend (EDD) (Pearce, 1991).

Prior to the introduction of the carbon tax on 1 July 2012 by the Gillard Government, and also following introduction of the tax, numerous studies were conducted to assess the effectiveness and consequences of the tax, including CGE models prepared by the Australian Treasury (2011). This article differs from the existing literature as it examines whether the European or non-European GTR approach is optimal for Australia in yielding EDD. Europe has been a forerunner in economic research on GTR and also in implementing different GTR policy mixes. The rest of the world followed Europe’s footsteps, and a multitude of policy mixes are tested in different regions using simulation studies. The differences in optimal GTR policies for EDD between European and non-European countries are outlined by Maxim and Zander (2019) and Maxim et al. (2019). This article examines the two GTR approaches, applying them to an Australian context, to see which policy mix has the highest positive effect on employment. We postulate that both emissions reduction and creating employment will be two pressing concerns in the foreseeable future. Based on the current trend, we predict that local and international pressure to reduce emissions in Australia will continue to mount and the government will be forced to enact stricter pricing on CO2 emissions. At the same time, due to a rise in artificial intelligence and automation (Arntz et al., 2016), coupled with the possibility of a slowdown in the global economy (Cashin et al., 2017), maintaining employment levels will be a challenging task. Also, employment creation will be needed to absorb the negative consequences of emissions-based taxes on employment in the fossil fuel sector. Therefore, a GTR policy-driven EDD can be a highly practical remedy for tackling both challenges.

The findings of our article will aid policymakers in understanding which GTR approach is most effective in the Australian context. Unlike other simulation studies, this study only focuses on the employment effect and offers a prescription on suitable tax recycling policy after examining the European and non-European approaches. The article is organised as follows: Section 2 presents a review of existing literature on simulation studies, based on the Australian economy; Section 3 provides a description of the model, database used and the simulation designs; Section 4 presents the simulations results; and Section 5 provides conclusion and policy implications.

Previous Studies

The earliest studies on the effect of any form of carbon pricing were done using the ORANI model made by the Centre of Policy Studies (CoPS), Australia. ORANI is a static single-region CGE model that has been used for multiple policy decisions in Australia and also in many other parts of the world (see Kilimani et al., 2015; Pui & Othman, 2017; Van Heerden et al., 2006; Yusuf, 2008). It was effectively used to assess the effect of tariff reduction and trade liberalisation in Australia, along with other major policy contributions. The earliest reported simulation study on carbon pricing in Australia is R. A. McDougall (1993a). The author used an extended version of the ORANI model with detailed modelling of the energy sector. The database used for the study was created from the 1986–1987 input-output (IO) tables. The results showed that carbon pricing would hinder the competitiveness of trade-exposed industries due to the hike in input cost, and an overall reduction of employment by 1.2 per cent, compared to the baseline scenario. In a subsequent study R. A. McDougall (1993b) employed the ORANI-E model where the author tested the effect of carbon tax, energy tax and fuel tax using the same database as the previous study. The study reported that both carbon and energy taxes are efficient in curbing the emissions, but not the fuel tax.

CoPS then developed an improved model based on the Monash Multi-Regional Forecasting (MMRF) model, called MMRF-Green. This model was specifically designed to test various aspects of environmental taxation on the Australian economy. The key feature of this model is its ability to analyse the effect of carbon emissions trading, and it was used in studies such as Adams (2007) and Australian Treasury (2011). Unlike ORANI or ORANI-E, MMRF-Green is a dynamic multiregional model. The results of the simulation studies conducted by the Australian Treasury are very optimistic in showing a major reduction in carbon emissions without any economic slump. However, one of the major weaknesses of the results generated by the Australian Treasury is that the simulation design was very complicated and numerous models were employed to generate the simulation results.

A more recent study is that of Meng et al. (2014), which examines the impact of carbon tax on households and industries and finds a subtle negative impact on employment ranging from –0.6 to –1.7 per cent across various industries. According to Meng et al. (2013), the impact of carbon tax will be a reduction in emissions, coupled with a mild contraction of the overall economy.

All the studies conclude that implementing any form of carbon pricing could result in a noticeable reduction in carbon emissions. However, its impact on economic growth and employment is mixed. Also, the existing literature on simulation studies concerning Australia is focused on emissions and economic growth with limited attention to employment. There is no study dedicated towards testing the EDD hypothesis in Australia or what combination of tax and revenue recycling leads to the most optimal result.

Data and Methods

ORANI-G Model

Since the study’s purpose is to assess the effectiveness of two different GTR approaches, and not to forecast the performance of the economy inter-temporally, we opt to use a static CGE model. The applied model is based on the ORANI-G model (Horridge et al., 2000), which is a single-country multisector comparative static model. The model is primarily developed based on the Australian economy using all the neoclassical assumptions, such as constant return to scale, cost minimisation for producers and utility maximisation for households.

In this model, the Australian economy is segregated into 37 industries that can produce 37 different goods and services. The model also includes one government, one representative investor, one representative household and 97 different occupations, with the demand side of the model consisting of producers, households, government, investment, exports and stocks. The primary database of the model is aggregated from the Australian Input-Output Tables 2012–13 (ABS, 2015). The ORANI-G compatible database used in this study is compiled by the CoPS, Australia. There are 114 industries and 114 commodities in the original IO tables, which are aggregated into 37 different industries and commodities.

All the behavioural parameters of agents in the model are adopted from the original ORANI-G model (Horridge, 2003), including the primary factor substitution elasticity, Armington elasticity, labour elasticity (elasticity between different types of labours) and export demand elasticity. However, we make one key modification in the original model by including value added tax (VAT), which is not modelled in ORANI-G. We included an alternative for the VAT in the model using the following equation:

Here, delV1PTX(i) is change in production tax in industry i; PTXRATE(i) is the rate of production tax in industry i; delV1PRIM(i) is change in total factor input to industry i; V1PRIM(i) is total factor input to industry i; and delPTXRATE(i) is change in the rate of production tax in industry i.

In the original model, the interim tax rate on a specific industry is represented by the variable t. This is an endogenous variable in the model and, therefore, we could not shock this directly in our simulations. Variable t is represented by the following equation:

Here, f0tax_s(c) is the general sales tax shifter and ftax_csi is the uniform percentage changes in the power of tax for intermediate usage, investment, household usage, export and government usage separately. We add an additional shifter ftax_si(c) which represents uniform percentage changes in the power of tax by commodity and modified the equation as following:

By keeping ftax_si(c) exogenous, we managed to control the shock on interim tax rate t indirectly. This allowed us to calibrate the tax on petroleum and coal products.

The energy tax rate we used in our simulations was influenced by the work of De Mooij and Bovenberg (1998) where they found 10 per cent energy tax in a GTR to be EDD inducive. We made some additional adjustments and used a rate of 11.3 per cent in all our simulations.

To ensure the tax revenue neutrality, we used a trial and error approach. For each different scenario, we adjusted the revenue recycle until the additional tax revenue generated from energy tax is fully recycled through the reduction in revenue from another tax.

Scenarios

One of the key assumptions of our study is that the primary dividend or environmental dividend of GTR, which is measured through the reduction of CO2 emissions, is a stylized fact and will always be achieved in the presence of any form of environmental tax. This nexus between environmental tax to internalise the external cost of pollution and reduction of emissions has been proven time and again (see Anger et al., 2010; Bosquet, 2000; Maxim et al., 2019; Patuelli et al., 2005). Therefore, our simulations of scenarios are more focused on the second dividend or the employment dividend.

We outlined the GTR characteristics of European and non-European studies based on the works of Maxim and Zander (2019) and Maxim et al. (2019) that highlight the effectiveness of VAT reduction, payroll tax reduction and reduction of mixed taxes in yielding EDD. We designed four different simulations to test different approaches of GTR and observed the impact on employment. For all four simulations, we used an energy tax, which we incorporated in the model by adding shifters f1_tax si(c) – f5_tax si(c). Using the shifters, we calibrated the tax on petroleum and coal products for five agents on the demand side of the model, including producers, investors, household and export. However, regarding tax revenue recycling, we used four different revenue recycling policies: (a) VAT reduction, (b) reduction of payroll tax, (c) reduction of other taxes and (d) a combination of all three different recycling policies. For all four simulations, tax revenue neutrality was ensured, meaning the additional tax raised from energy tax was fully recycled back to the economy.

Simulation 1. In our first simulation, we employed VAT reduction as the tax revenue recycling method. According to Maxim et al. (2019), one of the key differences between European and non-European approaches in yielding GTR-driven EDD is that VAT reduction is an EDD-inducive tax revenue recycling policy in European countries, whereas, in non-European countries, it is counterproductive. We designed the first simulation to measure the impact of GTR, where energy tax revenue gets recycled through a reduction of VAT in the Australian economy. The nexus between VAT reduction and a possible employment effect is slightly devious. A reduction of VAT can effectively lower the price level, which then can cause a downward push on nominal wage. However, if the elasticity of wage to price level is high, then it can cause the real wage to go down and positively impact employment levels.

Simulation 2. Reduction of labour tax is well documented in the literature as an effective tax revenue recycling method in creating EDD (see Bosquet, 2000; Maxim et al., 2019; Patuelli et al., 2005). In the simulation studies conducted in European countries, it is referred to as employers’ social security contribution. A reduction of labour tax, in theory, makes labour cheaper to the employers and, therefore, can positively influence employment levels. In the Australian context, this tax is predominantly known as the payroll tax. Paying an additional payroll tax on top of the wage makes the real wage higher from the employers’ perspective. A reduction of that, however, effectively is the same as a reduction of the real wage from the standpoint of employers (Pisauro, 1991). Payroll tax or any form of labour tax is not originally modelled in the ORANI-G. We have used a reduction of real wage as a proxy for the reduction of payroll tax as a tax recycling policy. Also, in our model, revenue neutrality was ensured by keeping the increase in tax revenue from energy tax equal to the reduction in the total labour wage bill caused by the reduction in real wage.

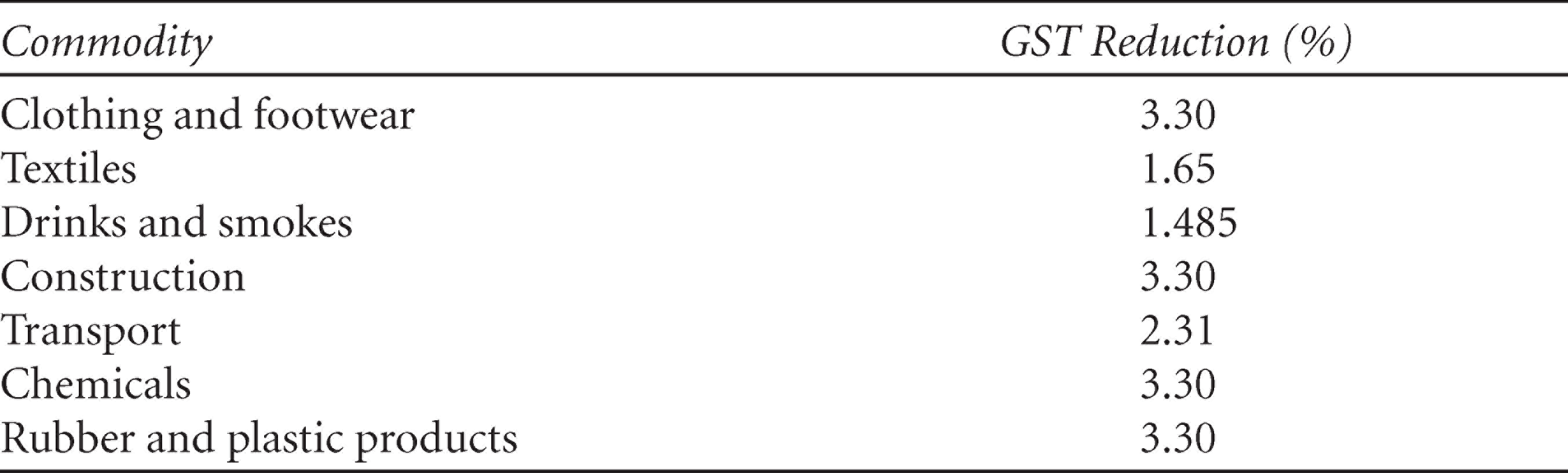

Simulation 3. Reduction of ‘other taxes’ is reported to be another EDD-inducive tax revenue recycling policy used by both European and non-European countries (Maxim et al., 2019). The idea stems from the work of Van Heerden et al. (2006), where food tax reduction was employed in the simulation as a tax revenue recycling method in South Africa. The simulation results reported this tax revenue recycling method to have a positive impact on employment. The underlying economic reason behind this is that the reduction of tax on a necessary consumption, such as food, reduces the overall expenditure of the household, which is effectively similar to an increase in the real wage from the household’s perspective. This increases the opportunity cost of leisure and, therefore, may positively influence employment levels (McConnell & Strand, 1981). A higher real wage also has a positive impact on aggregate demand and, therefore, may influence employment levels (Bhaduri & Marglin, 1990). In the Australian context, we test this by reducing the goods and services tax (GST) on goods and services frequently consumed by the household. The list of the goods and services is presented in Table 1.

Simulation 4. In the last simulation, we use a mixed tax recycling approach where we employed all three revenue recycling policies mentioned above. The revenue-neutral GTR is designed using an increase in energy tax and a reduction in VAT, payroll tax and GST.

Model Closures

For all the simulations, we used a constricted short-run closure where we kept capital stock fixed, but level of employment endogenous. We also used the Euler method in running all the simulations. Revenue neutrality was ensured in all the simulations.

We applied an energy tax of 11.3 per cent on the use of petroleum and coal products for household, investment, producers and export. The tax revenue is then recycled through a uniform 0.5 per cent reduction of VAT across all industries. The target tax and tax revenue recycling figures are calibrated to ensure revenue neutrality.

For the second simulation, we applied the same 11.3 per cent tax on energy which was recycled back through 0.8 per cent reduction of payroll tax across all industries and all occupation groups.

We employed a reduction of GST on seven commonly used goods or services consumed by a household to recycle the energy tax revenue. The GST reductions are given in Table 1.

In the final simulation, we used a mixed recycling approach including a VAT reduction of 0.11 per cent, payroll tax reduction of 0.13 per cent and various GST reductions on seven goods and services presented in Table 2.

Rate of Reduction of GST Across Various Goods and Services

Rate of Reduction of GST Across Various Goods and Services

Rate of Reduction of GST Across Various Goods and Services in Mixed Recycling Approach

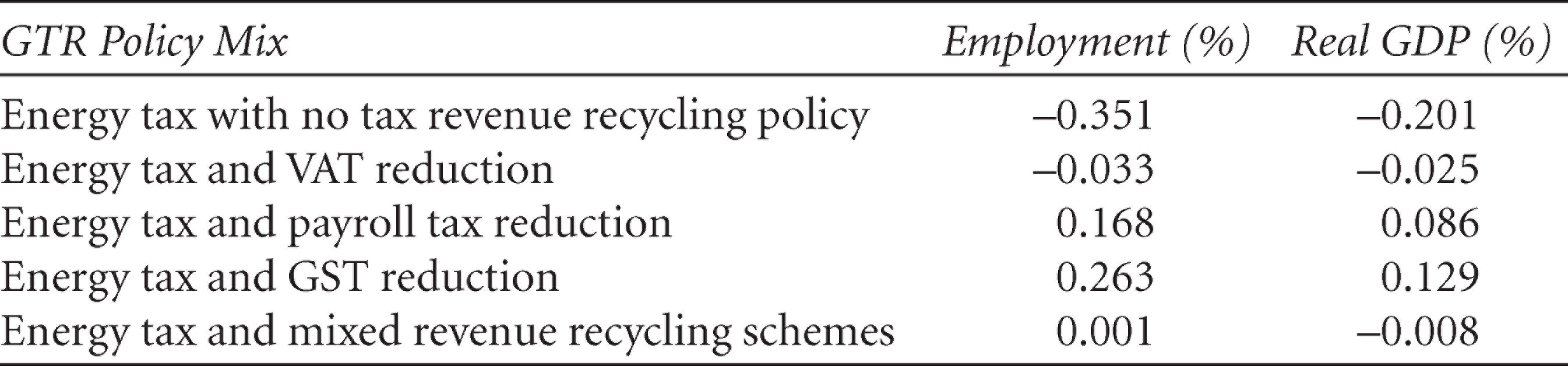

When energy tax is used as a standalone policy without any revenue recycling scheme, it causes the employment level to go down by –0.351 per cent. Table 3 presents the effect of energy tax on employment in the presence of four different revenue-neutral GTR schemes.

Effect of GTR Policy Mixes on Employment and Real GDP

Effect of GTR Policy Mixes on Employment and Real GDP

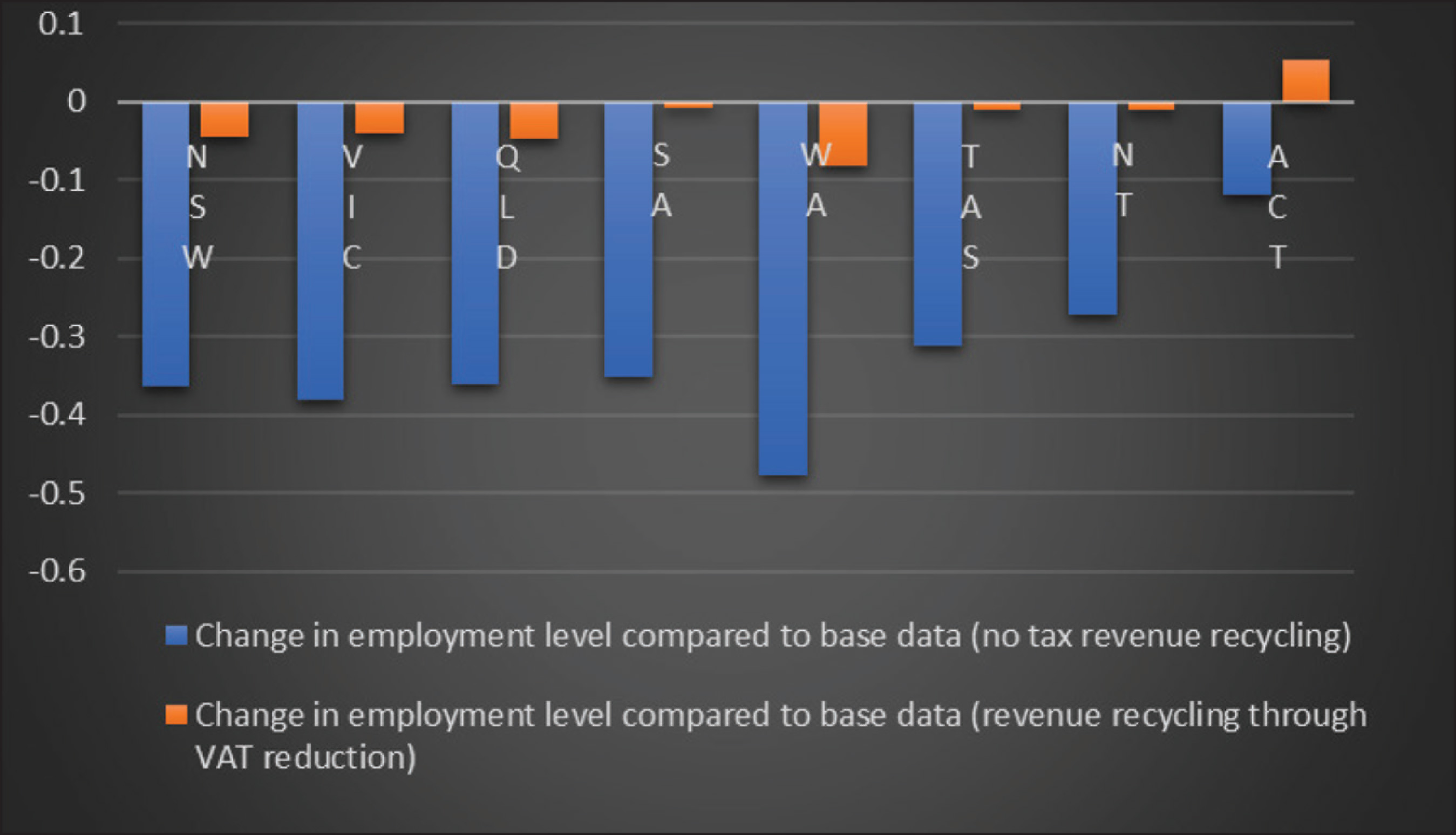

The results of the first simulation showed that the use of petroleum and coal products on which the energy tax was imposed went down by 3.148 per cent compared to the baseline scenario. The regional decompositions of employment changes are presented in Figure 1. The decomposition of employment by region and industry showed that the adverse effect of energy tax on employment is noticeable in the agriculture and mining sector. Only in the ACT did the VAT reduction has EDD potential and proved to be an effective revenue-recycling policy. ACT however has a dominant service sector with very little presence of agriculture and mining. This explains why this GTR approach is employment-inducive in the ACT but fails to create EDD in other regions. This also suggests that the Australian optimal GTR design for EDD is more towards the non-European policy designs than the European ones.

A reduction of payroll tax improved employment in Australia by 0.168 per cent compared to the baseline scenario. Additionally, it had a subtle positive impact on real GDP which went up by 0.086 per cent compared to the baseline. These results are in line with the existing literature (Maxim et al., 2019; Patuelli et al., 2005). We also found that the sale of petroleum and coal products went down by 3.03 per cent.

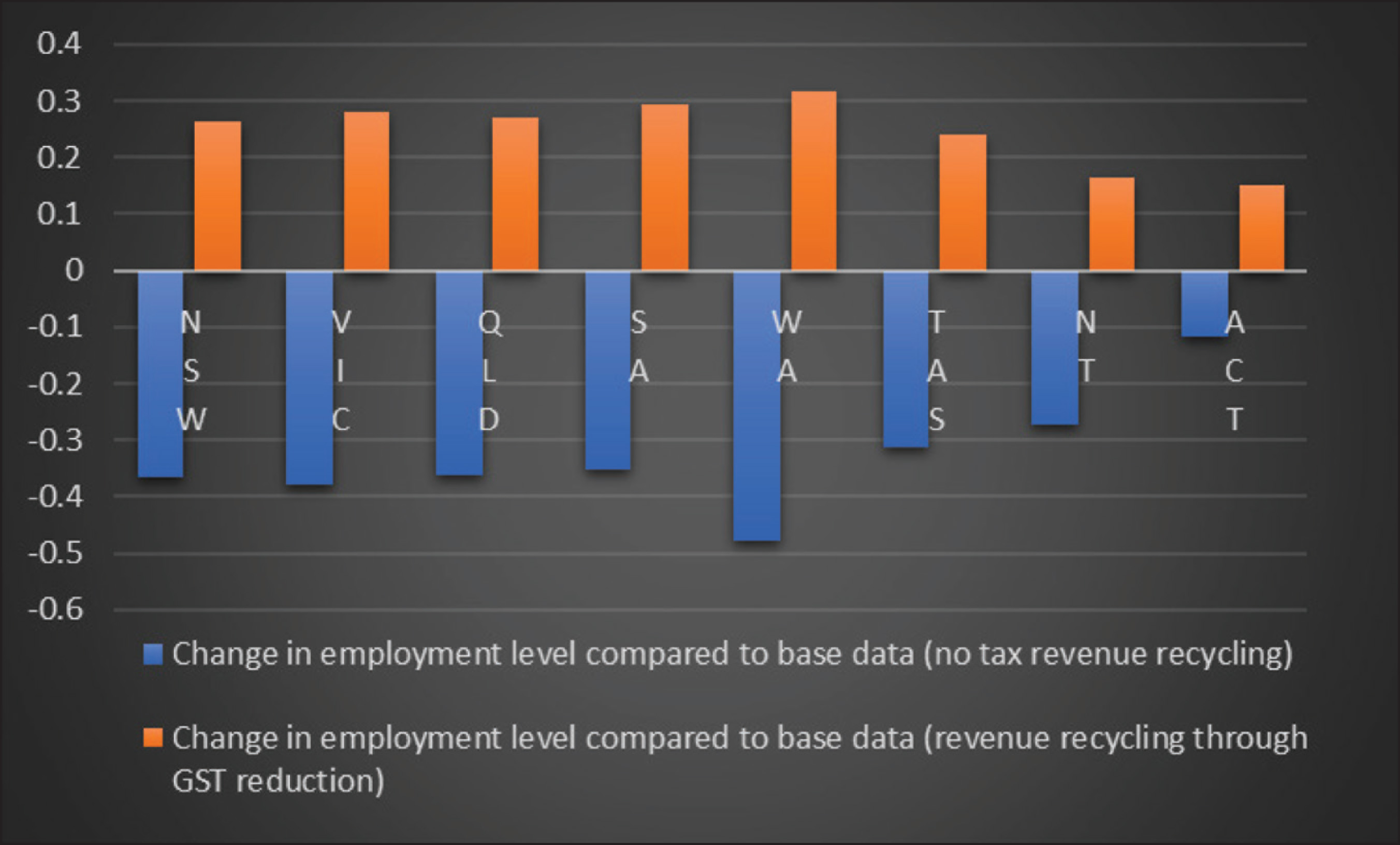

Figure 2 presents the regional decomposition of the employment changes. EDD potential was observed in all the regions, but the highest employment effect is observed in SA. The economy of SA is predominantly powered by agriculture, manufacturing and mining industries. All these industries are labour intensive, which explains a payroll tax reduction having a major impact on employment in SA.

The results of Simulation 3 showed an employment growth and real GDP growth of 0.263 per cent and 0.129 per cent, respectively, compared to the baseline scenario. This is a major finding because the existing literature on GTR in Australia concentrates on recycling through a lump sum payment (Meng et al., 2013, 2014; Meng, 2012). But a tax reform consisting of energy tax and a reduction of GST to yield EDD is a novel approach. More so, the fact that a reduction in GST has a stronger EDD potential than a reduction of payroll taxes is also an interesting finding. This GTR policy mix causes the sale of coal and petroleum products to go down by 2.902 per cent compared to the baseline scenario. Regional decomposition showed that WA had the highest EDD potential, followed by SA (Figure 3).

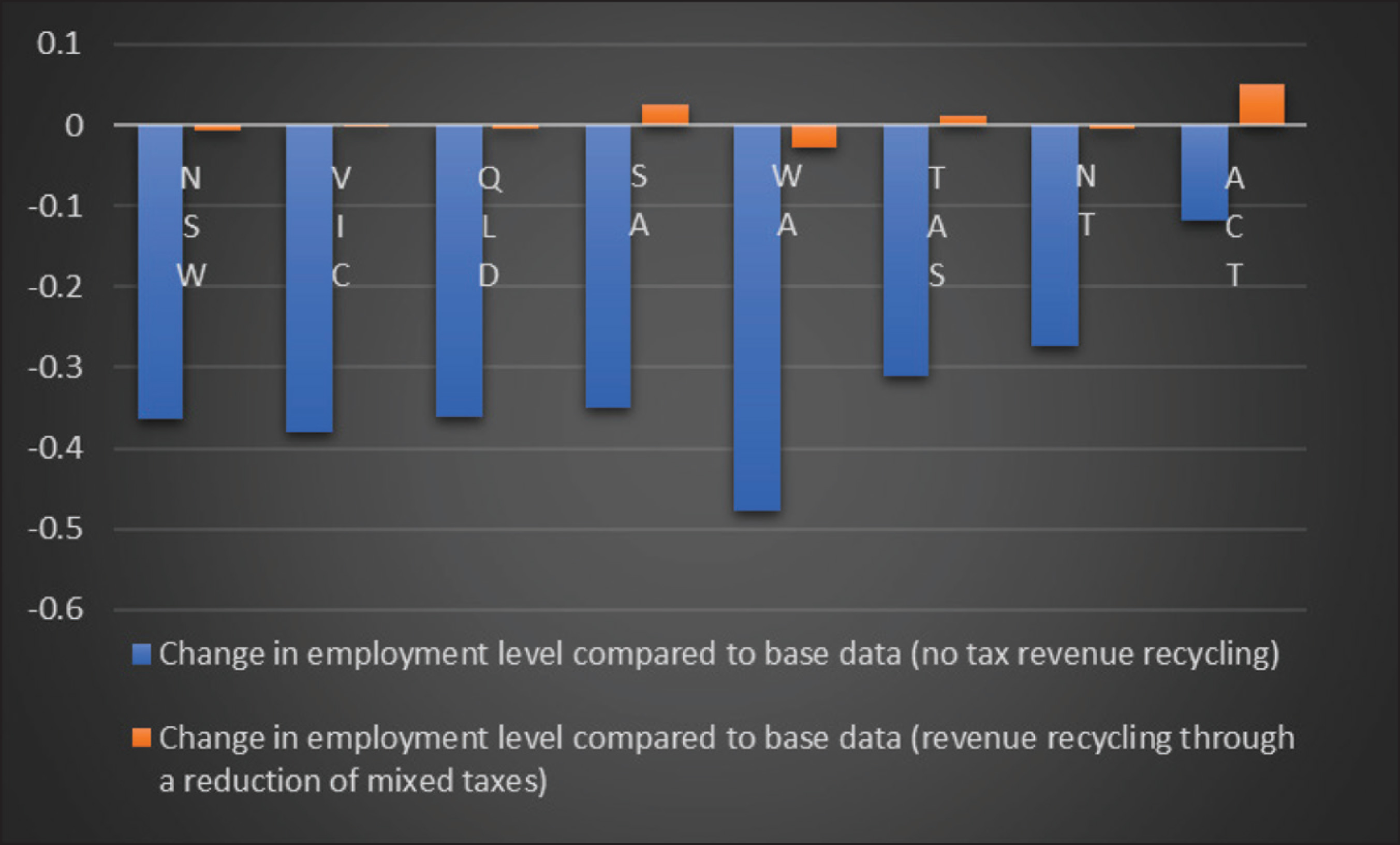

The mixed recycling approach consisting of VAT, payroll tax and GST reduction failed to create any noticeable EDD with a negligible negative impact on real GDP. It showed potential in covering up the negative effect of a standalone energy tax policy on employment. The consumption of petroleum and coal went down by 3.106 per cent, showing strong potential in achieving the environmental dividend.

The regional decomposition exhibited weak EDD potential in SA, TAS and ACT (Figure 4). More so, even though it is employment neutral, this GTR approach is likely to reach out to a larger portion of the economy by offering reductions of VAT, payroll tax and GST, all at the same time. Such a property can be politically beneficial in rendering the GTR policy more acceptable to a wider group of people.

Study Limitations

ORANI-G is a top-down CGE model and, therefore, the regional employment decompositions can be improved by using a bottom-up CGE model, such as MMRF-green or by a hybrid top-down CGE model (Higgs et al., 1988). Nevertheless, our study gives a primary breakdown of employment driven by GTR across regions. The other limitation of our study is that ORANI-G is a static model, so an intertemporal decomposition of the employment effect is not possible. Also, the impact of GTR on employment in the long run could not be measured through our simulation. Future researchers can test our findings using a dynamic model to obtain a more accurate intertemporal breakdown of employment in both the short and long terms.

Conclusions

This article presents a CGE analysis of four different types of tax revenue recycling schemes to test the EDD potential of GTR in Australia. It aimed to identify whether the European GTR policy design is optimal for Australia in yielding EDD.

We employed an energy tax in the model and find evidence for EDD in two of our tax revenue recycling approaches, which are payroll tax reduction and GST reduction. We argue that the employment dividend is needed to face future challenges that can hinder employment levels and also make any tax-based emissions reduction approach be politically acceptable. The employment potential of emissions reduction goes beyond the employment effect that comes from GTR, if investment in renewable energy projects is included, as such projects are labour intensive (see Lehr et al., 2008; Lehr et al., 2012). Future studies may investigate the combined employment effect of GTR and renewable energy projects to ascertain the true employment potential of the decarbonisation of energy systems in Australia.

The two salient features of our study are the EDD potential of GST reduction in a GTR context and the contrast between European and Australian employment response to GTR. The effect of GST reduction as a form of revenue recycling in Australia has been studied by Sajeewani et al. (2015) to measure its effect on income distribution, and they reported the positive effect GST reduction has on real GDP. Our results complement their findings by demonstrating the EDD potential of GST reduction when used along with energy tax in a revenue-neutral GTR context. Our simulation results show that in a revenue-neutral GTR, both GST and payroll tax reduction can annul the negative impact of energy tax on employment. One of the political reasons that causes apathy towards any form of carbon pricing in Australia is the negative impact it can inflict on employment. Meng et al. (2014) exhibits through simulations how the proposed carbon tax adversely affects employment. A GTR that can nullify that adverse impact can certainly make any tax-based approach to reducing CO2 emissions politically feasible. Additionally, our results show that a revenue-neutral GTR with either GST or payroll tax reduction as the revenue recycling policy not only has EDD potential but can also yield a triple dividend by positively influencing GDP (Bovenberg & van der Ploeg, 1996). This finding is in line with the existing literature of a GTR-induced triple dividend (Maxim, 2020).

The triple dividend potential of payroll tax reduction lies in the substitution between capital and labour. A tax on energy puts pressure on energy-intensive industries to reduce energy consumption. Energy and capital being complementary factors of productions in the short run (Finn, 1983), such tax is likely to reduce the overall output. However, a subsequent reduction in the labour tax can make labour cheaper relative to capital and hence induce higher employment. In the presence of a certain degree of substitution between capital and labour, this higher use of labour can recover the loss in output that is caused by the energy tax. And in the presence of unused factors (i.e., high unemployment rate), this tax reform mechanism can effectively create a higher demand for labour, leading to greater overall factor endowment and subsequently higher output. A reduction of GST reduces the distortionary effect this tax has on the economy and hence the real GDP improves.

Furthermore, the extensive meta regression analysis of Maxim et al. (2019) reveals that the key difference in European and non-European GTR effectiveness lies in the employment response to VAT reduction. Our study finds VAT reduction to be a hindrance to EDD in Australia, which is contrary to the employment response to GTR in Europe. Policymakers therefore should keep this in consideration when designing GTR policy mixes and maintain this caveat before following in Europe’s footsteps.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.