Abstract

Abstract

Ensuring effective and fair determination of executive compensation is complex, though equally essential for protecting the interests of shareholders and in creating long-term corporate value. The present study attempts to unravel the perceptions of executives and investors in terms of the determinants on which executive compensation ought to be based in the context of corporate India. The main research instrument is a quantitative questionnaire through which the responses of 74 top executives and 55 investors have been examined. Results highlight statistically significant mean differences in the perception of executives and investors with regards to the determinants of executive compensation. Further, the underlying dimensions representing pay determinants vary for executives and investors with the former regarding corporate governance and human capital as important, while the latter emphasising on the primacy of ownership and leverage. The article offers valuable insight as it proposes a comprehensive set of determinants of executive compensation by integrating multiple theoretical perspectives.

Introduction

Over the years, the senior executive rewards landscape has evolved significantly in India. Executive pay in India has seen a compound annual growth rate of approximately 13 per cent to 14 per cent in comparison with 1 per cent to 3 per cent across most Western economies over the last decade (Aon Hewitt, 2016). There also exists a widening disparity in pay levels, particularly between the middle and senior management (Gill, 2014), as well as across various industry sectors (Willis Towers Watson, 2016). Ensuring the retention of key talent remains among the top concerns due to heightened talent mobility (Mercer, 2014). Given the current imbalance between supply and demand for executive talent in India, the ‘C-suite’ compensation package is expected to rise even further.

Recognising the burgeoning pay differentials, questions are being raised on whether double-digit pay increases are truly supported by growth in revenue and profits. Past research affirms that even though executive compensation is set against a background of market forces, these forces rarely result into optimal contracting outcomes (Hirshleifer, 1978; Rajan & Zingales, 2001). These results are qualitatively similar to the inferences that currently exist in the literature for the impact of horizontal agency costs on executive pay, as in India (Chakrabarti, Subramanian, Yadav, & Yadav, 2011). Thus, the issue arises as to what determines the executive compensation. Executive compensation as it relates to shareholder value is important in view of two reasons. First, executive compensation is the most cited measure within the business and related social sciences literature (Gomez-Mejia, 1994). Second, this variable is one of the salient elements in nearly all corporate governance models (Felton, 2004).

Until very recently, studies in executive remuneration have been exclusively associated with the developed countries. Yet the concern regarding executive compensation level and structure is possibly equally important in transitional and emerging economies (Kato & Long, 2006; Luo, 2014). Focusing on India, the rapid stock market growth in the last decades has led to a transformation in the underlying institutional infrastructure, with corporate governance reforms progressing faster than in many other emerging market economies (Armour & Lele, 2009). This growth brings with it an acute need to understand factors that influence compensation of Indian executives. There are preliminary indicators of what could possibly be the determinants of executive compensation. However, there is lack of knowledge about what the key stakeholders perceive as important factors in determining executive compensation. The present article aims to fill this research gap, as it attempts to unravel the perceptions of executives and investors in terms of the determinants on which executive compensation ought to be based in the context of corporate India.

The institutional context in India is important in two ways. First, the ownership structure of India’s publicly traded companies is characterised by high concentration of shareholding and control structures (Gill & Kaur, 2015; Gollakota & Gupta, 2006). In addition, listed companies in India are often controlled by families holding large shareholdings with presence at both the levels of management and board (Bertrand, Mehta, & Mullainathan, 2002; Gill & Kaur, 2015; Jaiswall & Firth, 2009). Over the years, the compensation packages of professional executives have been robust so as to attract and retain the right talent (Barclays Wealth, 2012). However, the commission-focused compensation is peculiar to India, with dominant shareholders in executive directorial positions being paid exorbitantly (Balasubramanian & George, 2012). Second, due to increasing public investment, the question of protecting non-controlling shareholders has been prominent while developing and implementing a corporate governance model in India (J. Sarkar & S. Sarkar, 2000). According to the recent report of the World Bank (World Bank, 2017), India ranks thirteenth and ahead of many developed countries when it comes to protecting minority shareholders. Further, the Indian legal framework has been fairly stringent in matters related to executive compensation. The Indian corporate background, thus, provides an interesting yet uncharted research platform to examine how executives and shareholders view executive compensation.

The article aims to make significant contribution to the existing literature. First, using rigorous analytic techniques, it seeks to examine the determinant factors in executive compensation based on survey data. Most papers on determinants of executive compensation depend solely on publicly available data from listed companies (Cole & Mehran, 2016). Further, surveys of executives and investors carried out by most consultancy firms lack theoretical and econometric foundations (Groshen, 1996). Second, to the best of our knowledge, difference between the perceptual view of executives and investors in factors determining executive compensation has not been explored in the context of transitional and emerging countries. 1

One other study (see Fleming & Schaupp, 2012), in the US context, examined the differences between the perception of determinant factors in executive compensation through a survey for a sample of top executives and shareholders.

Theory and Hypotheses

The level and structure of executive compensation has attracted significant interest from both economists and academicians over the years. However, the mainstream compensation studies in developed countries may not likewise apply to emerging markets due to differences in market, institutional and corporate structure (Bertrand & Mullainathan, 2001). The literature relevant to the present article includes prominent determinants of executive compensation as proposed by various theoretical viewpoints and established by recent empirical evidence from emerging and developing economies.

Perceptions on Executive Compensation

Executive compensation has been explained in the light of various theoretical standpoints emanating from the theory of the firm (Coase, 1937). The basis underlying these contractual theories is the separation of residual claimants and the decision control agents (Foss, 2008). This thereby suggests that the shareholders will focus on maximising their wealth, while executives’ focus will rest on optimising their growth trajectory. Thus implying that while shareholders will place greater importance on the firm performance, managers, on the other hand, will seek to place greater emphasis on personal, human capital measures. There is sufficient evidence to show that Indian executives value personal growth at work (Singh-Sengupta, 1997). It is therefore expected that there would be divergence between the perception of executives and investors on executive pay model as well. Formally, this leads to the following hypothesis:

H1: There are differences in the perception of executives and investors with regards to the determinants of executive compensation.

Determinants of Executive Compensation

Consistent with prior theory and empirical work, it is expected that executive pay is generally determined by economic and institutional factors, including corporate performance, governance mechanisms, corporate characteristics and human capital as the major determinants of executive compensation. We hypothesise that these factors shape preferred compensation designs.

Finding its genesis in agency theory, the predominantly established determinant of executive compensation is the performance of the firm. This theory broadly asserts that when managers act in a self-serving manner, in the context of dispersed share ownership, suboptimal contracts would result in executive compensation which is insensitive to corporate performance (Jensen & Meckling, 1976). Such suboptimality can also arise under concentrated ownership with the controlling shareholders obtaining private benefits in the form of higher compensation irrespective of firm performance at the expense of minority shareholders (Abdullah, 2006; Chang, 2003; Claessens & Fan, 2002; Liu & Lu, 2007). Further, the identity of the controlling shareholder also affects executive compensation (Cordeiro, He, Conyon, & Shaw, 2013; Firth, Fung, & Rui, 2006; Sun, Zhao, & Yang, 2010; Unite, Sullivan, Brookman, Majadillas, & Taningco, 2008). Though mixed empirical evidence exists, bulk of the studies report performance as a primary determinant of compensation. Therefore, we pose the following:

H2 (a): Corporate performance is a significant determinant of executive compensation.

A growing body of literature casts doubt over the effectiveness of corporate governance mechanisms in emerging economies (Ball, Robin, & Wu, 2000; Gibson, 2003; Kim, Lee, & Shin, 2017; Van Essen, Van Oosterhout, & Carney, 2012). Generally, the owner-controlled firms are believed to be more vigilant than manager-controlled firms (Carney & Gedajlovic, 2002; Chen & Kao, 2016), resulting in lower explicit incentive pay contracts (Ramaswamy, Veliyath, & Gomes, 2000). However, some other studies have found that chief executive officer (CEO) compensation is positively related to the proportion of promoter/owner holdings, especially in the presence of diffused institutional ownership (Chakrabarti et al., 2011; Gallego & Larrain, 2012). A number of empirical studies also suggest higher monitoring intensity (Firth et al., 2006) and lower pay levels for firms with large blockholders (Jaiswall & Bhattacharyya, 2016; Lee, 2014). Other than owners, board of directors also act as a monitoring mechanism for controlling the self-interest-driven agent. Lower level of board control, thereby, implies a higher salary for the CEO (Lin, 2005). In a similar vein, the CEO also serving as the board chair has, often, been associated with unjustified rewards influenced by CEO’s heightened control and discretion (Conyon & He, 2016; Li, Moshirian, Nguyen, & Tan, 2007; Veliyath & Ramaswamy, 2000). Further, the presence of directors holding multiple board appointments has frequently been matched with inadequate check on the management, thereby leading to a higher executive pay (Jackling & Johl, 2009). CEO pay–performance sensitivity is higher with greater proportion of non-executive independent directors (Ghosh, 2006), and companies having the compensation committee in place (Lee, 2014). Taken together, the findings support agency theory and its offshoot, the ‘positivist’ approach, suggesting that corporate governance structures influence executive compensation leading to the following hypothesis:

H2 (b): Corporate governance processes play a significant role in determining executive compensation.

It is generally acknowledged that contingency factors, primarily organisational and institutional environment, play an important role in containing the opportunistic tendency of top executives to pursue their self-interest overlooking the long-run growth of the company (Gomez-Mejia & Wiseman, 1997). Specifically, the level of executives’ pay is significantly higher in certain industries (Ding, Akhtar, & Ge, 2006), and increases with growth and diversification (Ghosh, 2006). Generally, executives of large firms might demand a higher pay because of the need to maintain a pay differential, the complexities of the job, the requirement for more human capital and greater organisational complexity (Bhattacherjee, Jairam, & Shanker, 1998; Li et al., 2007; Mengistae & Xu, 2004). Evidence also shows interesting links among sensitivity of executive pay to debt (Ho, Lam, & Sami, 2004; Wen, Rwegasira, & Bilderbeek, 2002). Theoretically, leverage has an impact on the optimal design of managerial compensation (T. John & K. John, 1993). Consequently, the risk that the company faces also determines the level and structure of executive pay (Jaiswall & Firth, 2007). A number of studies have also considered the institutional context while looking into the impact of specific corporate governance characteristics on executive compensation (Chen & Kao, 2016; Varma, 1997). In summary, a more complete understanding of compensation contracting involves examination of firm characteristics resulting in the following hypothesis:

H2 (c): Company-specific characteristics are important determinants of executive compensation.

Managerial resources, defined as the abilities and skills of managers, contribute significantly to the bundle of corporate resources which create resource-based rents (Pandher & Currie, 2013). In addition, executives’ professional network outside the firm is also a highly valued resource providing better access to strategic information (Baeten, Balkin, & Van den Berghe, 2011; Maloa, 2018). This value is reflected in the hefty pay packages offered to entice executives with superior managerial abilities (Adithipyangkul, Alon, & Zhang, 2011). In general, older (Gallego & Larrain, 2012), highly qualified executives, with long tenure fetch more in the labour market (Chen, Ezzamel, & Cai, 2011). Further, executive stock ownership also determines managerial pay since it provides a direct link between CEO and shareholder wealth (Sheu & Yang, 2005). However, due to the peculiarity in the institutional set-up specific to emerging economies, divergent results have often been observed (Kang & Payal, 2010). Notwithstanding, keeping the increasing demand for managerial talent in the labour market into perspective we assume that:

H2 (d): Executive-specific heterogeneities account for varied levels of compensation to the executives.

In general, discerning the basis of determining executive pay is of paramount importance. This assumes special importance in the wake of criticism of executive pay being unidirectional, without regard of corporate performance. Further, the findings of a large body of research indicate that more than one theory might be needed to explain the nuances of executive compensation. In the Indian context, however, little is known about the epistemological perspective that forms the basis for structuring executive compensation. The results established in this article attempts to addresses this research gap.

Research Design

Respondent Demographics

Respondents of the study comprised of universe of executives that serve on the board of directors and communities of investors in India. A total of 74 executives and 55 investors participated in the survey. The ‘executives’ comprise of managers having past or present experience in top managerial positions. The investor communities comprise of brokers, financial/security analysts, investment advisors and other investors. As such, this group of respondents comprise of individuals who are well educated and have necessary skills and knowledge to make well-informed financial decisions. For simplicity, the entire group is referred to as ‘investors’.

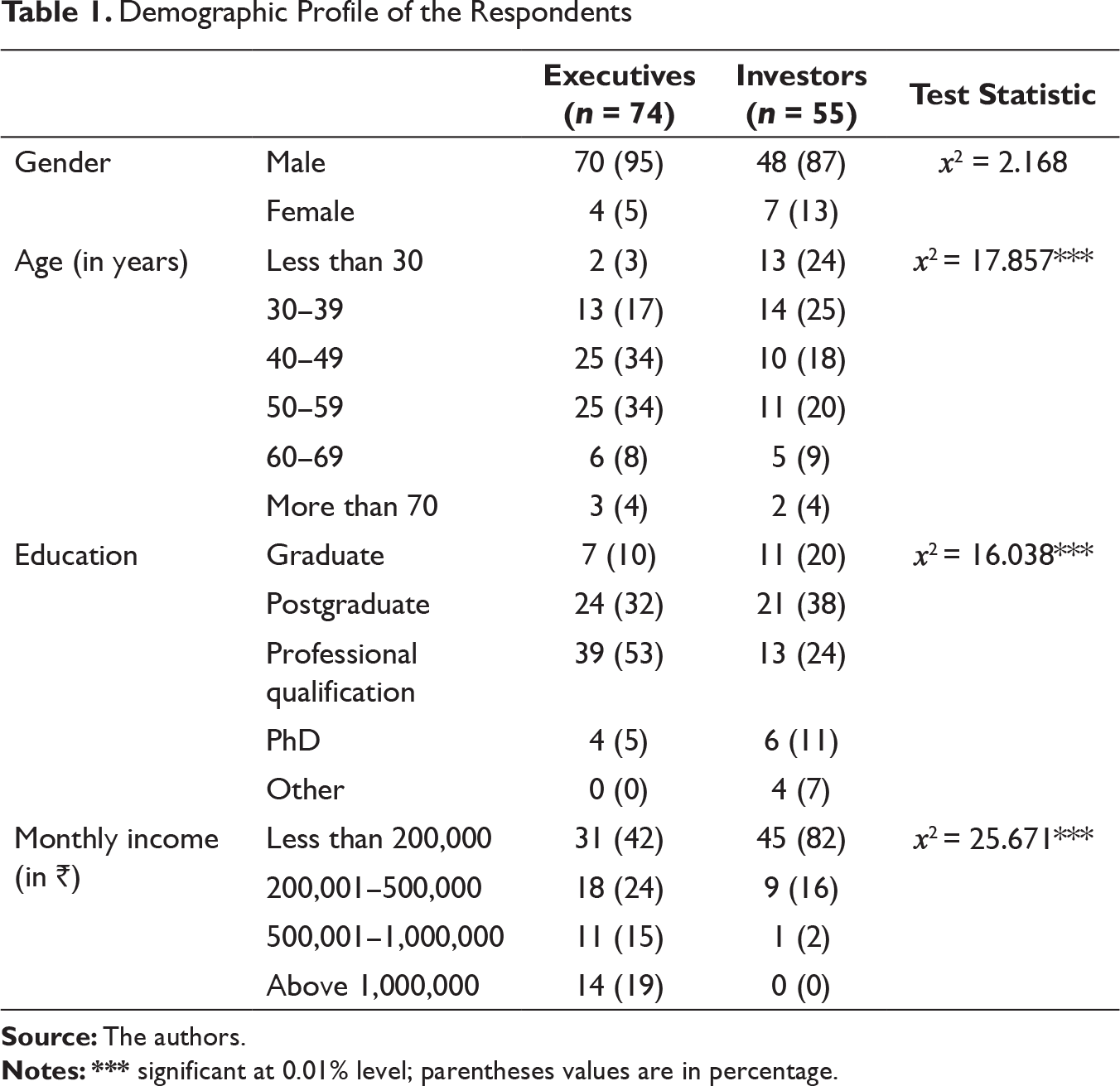

A brief demographic profile of the executives and investors is presented in Table 1. It can be observed that there were significant differences between executives and investors in terms of age (χ2 = 17.857; p < 0.01). Additionally, executives were more professionally qualified than the investors (χ2 = 16.038; p < 0.01). A further significant difference was that the bulk of investors (98%) had monthly income below 500,000 ₹ vis-à-vis executives (χ2 = 25.671; p < 0.01). However, executives were not significantly different from investors in terms of gender, with majority of them being males.

Demographic Profile of the Respondents

Development and Administration of the Survey Instrument

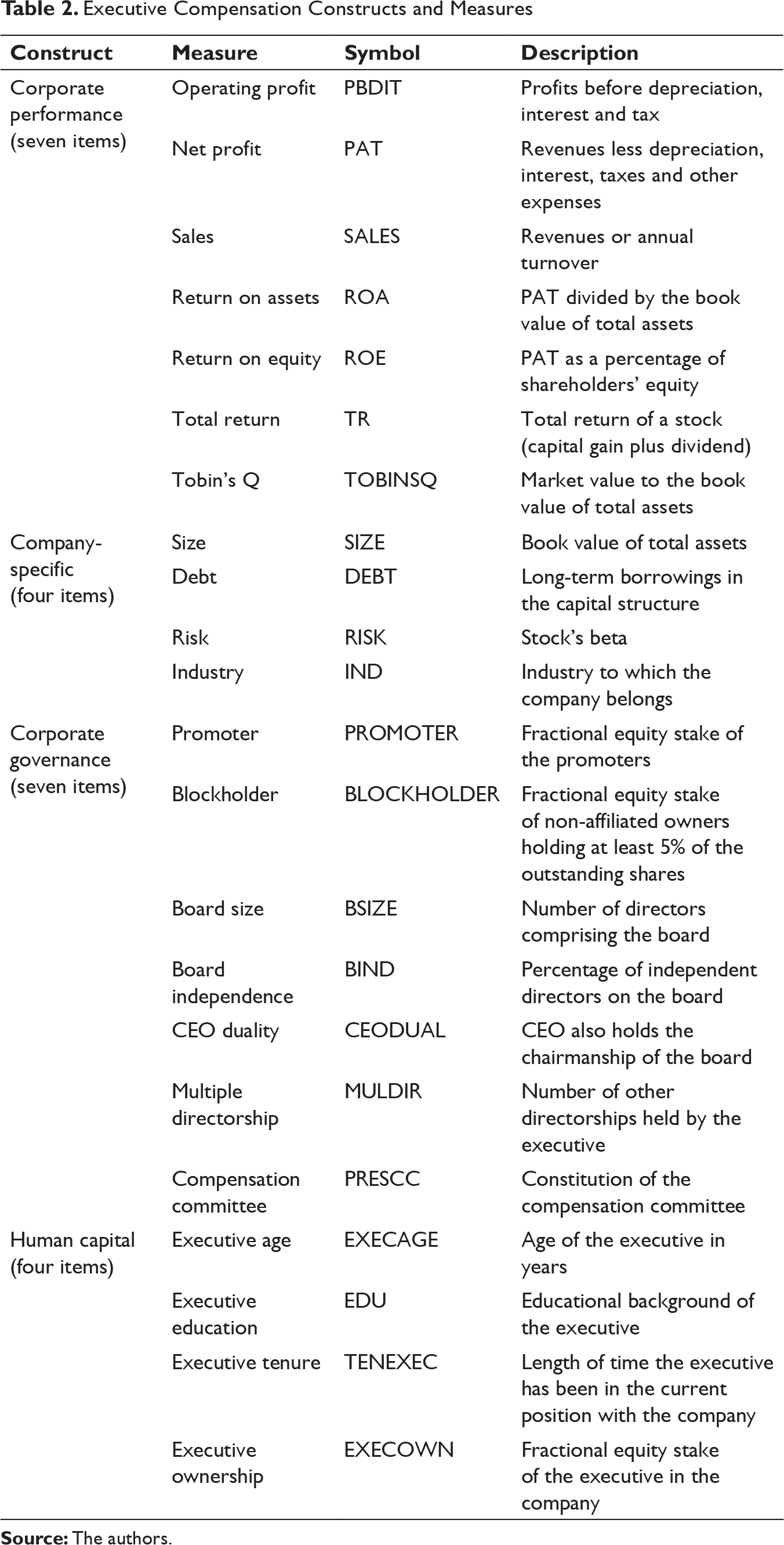

The survey instrument aimed at identifying the perceived determinants upon which executive compensation ‘ought to be’ based. Though, executive compensation may be determined on the basis of a large number of measures, the most pertinent ones keeping in mind the premeditated objectives of the study have been adopted. Based on extensive review, 22 measures were identified as plausible compensation determinants. Table 2 presents these measures with their respective connotations. These measures reflect four compensation constructs covering corporate performance, company-specific characteristics, corporate governance and human capital.

A series of actions were taken in order to establish the validity and reliability of the survey instrument developed for the purpose of the study. First, a panel of two experts verified the said instrument. Second, the questionnaires were pretested on experienced researchers and potential respondents for content, design and comprehension. Accordingly, the survey instrument was used to conduct beta tests to seek feedback from academic researchers (ion aimed at obtaining a general opinion of the respondents on various aspects of executive compensation, for example, relative importance of investors (‘say-on-pay’) and other stakeholders in setting executive compensation, composition of compensation classes and the level of compensation disclosures. The third section measured demographic statistics.

Executive Compensation Constructs and Measures

The final survey was administered using two mechanisms. First, an online survey was emailed to 1,263 members of communities for executives and investors on a professional networking site. 2

World’s largest growing professional networking platform, LinkedIn, was used for conducting the online survey. Using the ‘find a group’ option, relevant groups were identified for executives (namely, India CEOs Club, CFO Forum India, India Leadership Network) and investors (namely, Fundamental Stocks—Investing in Indian Equity Markets, Technical Analysis India, India Investor Network, Indian Stock Market Professionals, Indian Stock Market Investor & Traders). Thereafter, profiles of active group members were scanned for educational qualification, professional experience and premeditated research criteria.

Examples include a 10 per cent investor response rate reported by McCahery and Sautner (2012) and an 11 per cent executive response rate by Graham, Harvey, and Puri (2013)

Pilot Sample: Mean Subscale Score and Coefficient Alpha†

Results of ANOVA

Data Analysis and Methodology

To unravel the perception of executives and investors with regards to the determinants of executive compensation, independent analyses were carried out for two separate subsamples, each corresponding to executives and investors. First, the one-way analysis of variance (ANOVA) using the general linear model was invoked to investigate differences in perception for each of the 22 measures. Second, cluster analysis was applied to identify measures perceived as important determinants of executive pay and, further, to explain the differences in perceptions. More specifically, this technique has been applied in order to group the respondents, rather than the variables. Such classification or grouping has been done using K-mean clustering algorithm. 4

Similar methodology has been applied in governance literature by Kaplan and Strömberg (2003) and Gillan, Hartzell, and Starks (2011).

Factor analysis has been used to aid the development of appropriate constructs determining executive pay. To ascertain the underlying dimensions representing determinants of executive compensation for executives and investors and discern their perceptual differences, the principal axis factor analysis approach has been used on the subsamples. 5

Research has demonstrated that common rules of thumb regarding sample size in factor analysis are not valid or useful, see, for example, Costello and Osborne (2005).

Results and Discussion

Perception of Executives vis-à-vis Investors on the Determinants of Executive Compensation

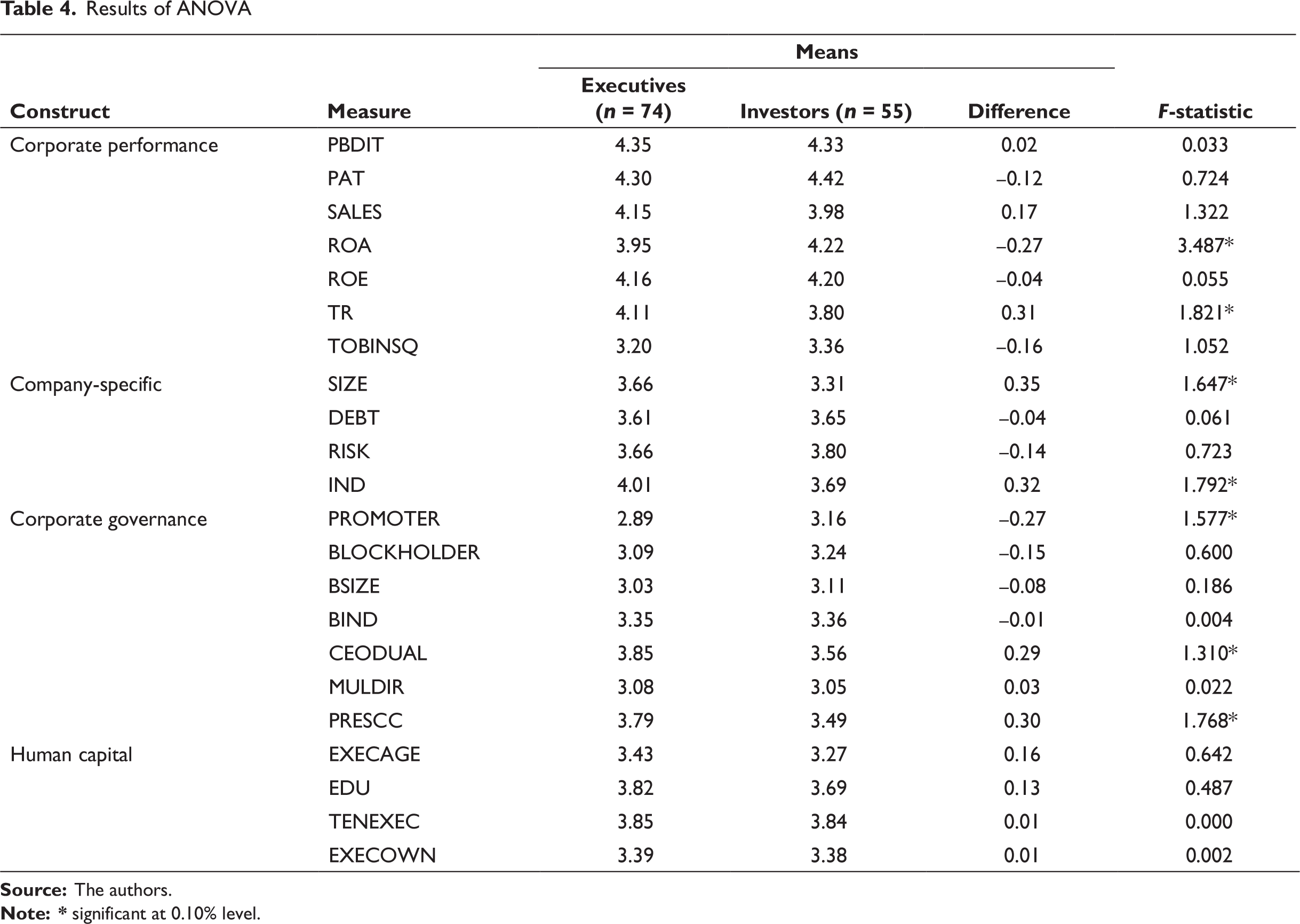

In order to analyse the perceptions of executives in comparison with those of investors, one-way ANOVA using the general linear model has been invoked. The ANOVA test reveals statistically significant differences between responses of executives and investors on the four compensation constructs along with the results of F-test (cf. Table 4). No significant difference can be observed with regards to human capital construct although the average values for various measures are higher for executives than those for investors. Of the 22 compensation measures, difference in perception at 10 per cent level of significance was found for seven measures. The mean scores of executives relative to investors are statistically higher for total return (mean difference = 0.31; F = 1.82), size (mean difference = 0.35; F = 1.65), industry (mean difference = 0.32; F = 1.79), CEO duality (mean difference = 0.29; F = 1.31) and compensation committee (mean difference = 0.30; F = 1.77). As posited in literature, executives consider compensation to be linked to both stock prices and governance structures, especially the role of CEO duality and compensation committee. These results are in concurrence with a meta-analysis proving that stronger boards are able to establish better link between firm performance and CEO compensation (Van Essen, Otten, & Carberry, 2015). Further, the findings highlight that the market for executives is rather segmented with company size and industry as important determinants of executive compensation. It is reasonable to expect that executives should be paid for firm size and industry affiliation, which reflects the complexity of the job (Gomez-Mejia, Berrone, & Franco-Santos, 2010).

On the other hand, mean scores for investors were significantly higher for return on assets (mean difference = 0.27; F = 3.49) and promoter (mean difference = 0.27; F = 1.58), thereby indicating some support for Hypothesis 1. This shows that investors relate pay more to accounting-based performance and promoters’ shareholding. Theoretical research and circumstantial evidence suggests that the level of monitoring is higher for owner-controlled firms leading to improved performance (Hölmstrom, 1979; Mazur & Salganik-Shoshan, 2017). In family firms, the family CEOs receive lower compensation vis-à-vis professional CEOs, although their pay tends to be more insulated from risk (Gomez-Mejia, Nuñez-Nickel, & Gutierrez, 2001). This is specifically true for India wherein most of the companies are in the dominant control of the family (Bertrand et al., 2002; Khanna & Yafeh, 2007).

For identifying the underlying dimensions that represent the determinants of executive compensation, factor analysis of the 22 compensation measures has been conducted. Analysis of the executives subgroup yielded six factors with eigenvalues greater than one explaining 54.19 per cent of the total variance (cf. Table 5—Panel A). As evident from the first factor (1), executives seem to recognise the significance of corporate governance by assigning highest importance to the variables CEO duality, blockholder, board independence, multiple directorship and board size. The executives seem to support the view that the level and composition of compensation is affected by the quality of internal corporate governance mechanisms, namely monitoring by board of directors and blockholders, thereby corroborating positivist agency theory (Conyon & He, 2012; Eisenhardt, 1989; Lin, 2005; Słomka-Gołębiowska & Urbanek, 2016). The second factor (2), comprising size and executive tenure, supports the conjecture that more experienced executives may be associated with large companies. Reflecting equity efficiency (return on equity and total return) and operating efficiency (net profit and sales), two factors (3 and 4) are loaded by the corporate performance dimension. The fifth factor (5) loading on executive age and executive education points towards the pertinence of personal attributes for the executives for setting executive pay. In addition to the second factor (2), this factor shows that executives associate pay with their personal characteristics (Humphery-Jenner, Lisic, Nanda, & Silveri, 2016), thus supporting the resource-based theory that firm-specific human capital is highly rewarding for executives (Sturman, Walsh, & Cheramie, 2008). The preference placed on this determinant factor indicates that executives are willing to capture a portion of these resources by way of compensation and private benefits (Pandher & Currie, 2013). The sixth factor (6) is loaded by debt and risk, reflecting executives’ preference for a higher pay for bearing more risk.

Summary of Rotated Component Matrix Determining Executive Compensation for Executives (n = 74) and Investors (

n

=55)

From the investors sub-group, an initial six-factor solution was obtained which explains 51.32 per cent of the total variance as shown in Table 5—Panel B. The corporate governance dimension along with a loading of 0.701 on the company-specific dimension predominates the first factor (1). The factors promoter, debt and blockholder points towards the importance investors assign to the role of ownership structure and leverage in determining executive pay. The results for investors suggest that they believe that the nature of ownership control and creditors’ ability to monitor the debt contracts influences executive pay. Besides promoter ownership, they acknowledge the supervisory role of debtholders as well as blockholders in aligning pay to performance. Such holders derive their power from the size of their investment (debt or equity) in the company (Crespí-Cladera & Gispert, 2003). In concurrence with developed countries (Balsam, Boone, Liu, & Yin, 2016), the present results also underline the fact that investors do recognise the role of ‘say on pay’, especially that of non-affiliated owners, in exerting isomorphic pressure on compensation issues even in the emerging economy of India. Similarly, the second factor (2) loaded by multiple directorship, board size and CEO duality, reflects the pertinence of board structure as an agent-monitoring mechanism. Comprising return on equity and return on assets, the third factor (3) is loaded by the corporate performance dimension revealing investors’ preference for increasing the responsiveness of pay to performance. The fourth factor (4) is loaded by the company-specific dimension. Clubbing risk and industry, Factor 4 shows that investors consider the role of company- and industry-specific risk to be significant in pay determination. Investors’ concern for market risk and industry-wide norms, thus, accentuates the role of contingency theory in pay determination. The fifth factor (5) is focused on two human capital variables executive tenure and executive age. Indicating the importance of company size in determining pay, the sixth factor (6) loading on size and sales reveals company size as an important executive compensation determinant.

As can be observed, multidimensional factors underlying the compensation determinants for executives are fewer than those for investors. Executives, for instance, have five factors loaded on a specific compensation construct, while for investors there were only four. Even though the underlying compensation constructs were comparable for executives and investors, the factor loadings were not on corresponding compensation measures. For instance, Factor 3 and Factor 5 for both executives and investors were ordered on the corporate performance and human capital constructs, yet not totally loaded on like measures. Further, certain divergence in the factor loads have also been highlighted. It was observed that executives have relatively high loadings on certain compensation measures, namely board independence (0.703) on the corporate governance construct as well as total return (0.790) and profit after tax (0.648) on the corporate performance construct; while the same are insignificant for investors. The results reflect that the underlying dimensions representing determinants of executive compensation vary for executives and investors. Overall, the results suggest that there exists a general difference among executives and investors in discerning the determinants of executive pay supporting Hypothesis 1.

Framework for Executive Compensation Determination

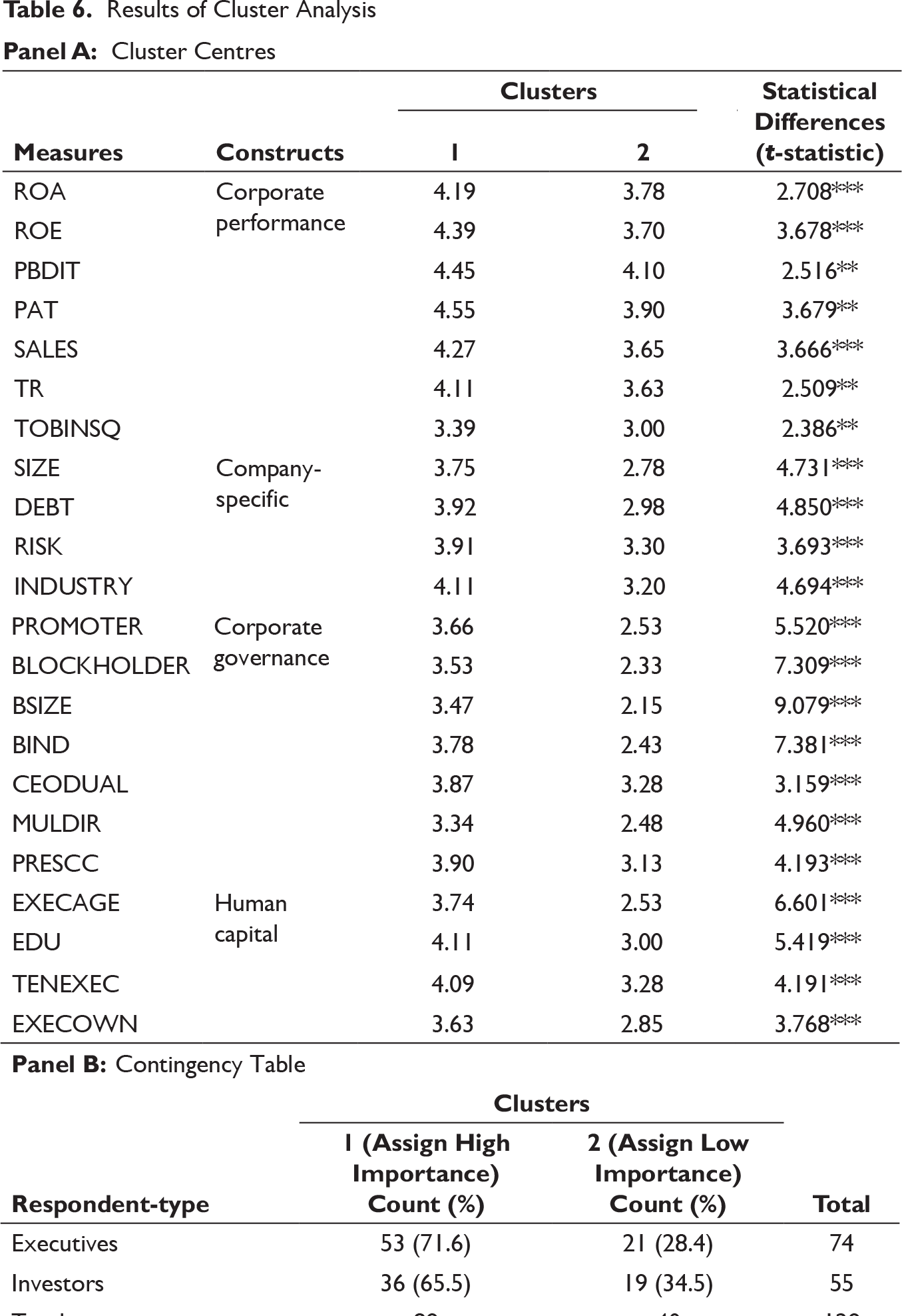

For analysing the perceived importance of selected measures as pay determinants and thereby establishing perceptual difference, cluster analysis has been conducted. The results for cluster analysis have been presented in Table 6—Panel A. The centroids of the two-group cluster solution suggests a cluster comprising of respondents who assign high importance to all the compensation measures (Cluster 1, comprising 89 respondents) and another with respondents who assign low importance to these measures (Cluster 2, comprising 40 respondents). An independent samples t-test shows that the difference between the centroids of two clusters is statistically significant at 1 per cent (p < 0.01) for all the measures except some of the corporate performance measures (operating profit, net profit, total return and Tobin’s Q) which are significant at 5 per cent (p < 0.05). This shows that a vast majority of the respondents, that is, 89 out of 129, support the contention that a multitude of determinants influence executive pay, thereby extending support for Hypotheses 2(a) through 2(d). Establishing the pertinence of the constructs, the results further suggest a framework comprising significant determinants for designing compensation contracts for top executives.

It can moreover be observed from the contingency table that a higher percentage of executives (72%) vis-à-vis investors (66%) consider these measures highly important in determining executive pay (Table 6—Panel B). This, therefore, extends support for Hypothesis 1 explicating perceptual differences between executives and investors.

Results of Cluster Analysis

Conclusion

Corporate governance literature asserts that the conflict of interest between executives and shareholders might be mitigated through a correctly designed executive compensation package (Bebchuk & Fried, 2003; Carter, Marcus, & Tehranian, 2016; Conyon, 2006; Thévenoz & Bahar, 2007). In depth, knowledge of the perceived determinants is, hence, instrumental in designing suitable pay packages for the executives. Though more than 300 studies have explored the issue of top management compensation (Lin, 2005), the nature of research has primarily been archival. The present article, therefore, endeavours to conduct a primary survey so as to discern the perception of Indian executives and investors on the determinants of executive compensation.

The study provides valuable insights on the conception of executive pay. First, there are statistically significant mean differences in the perception of executives and investors on seven measures determining compensation. Further, the results of cluster analysis show that a multitude of determinants influenced executive pay with disproportionately higher number of executives in the cluster group assigning higher importance to the same. Second, the underlying dimensions representing determinants of executive compensation vary for executives and investors. On applying factor analysis, it was observed that executives regard corporate governance and human capital as more important determinants. However, investors consider the strength of pay–performance relationship to be contingent on the role played by both ‘insiders’ and ‘outsiders’. Although a host of deterministic factors influence pay, the results put forth by bivariate and multivariate analyses corroborate that there are subtle perceptual differences between executives and investors with regards to these factors. Overall, the application of multiple and combined theoretical perspectives rather than a mono-theoretical view presents an appropriate and adequate epistemological underpinning to these empirical findings. 6

Similar conclusion has been drawn by Edmans, Gabaix, and Jenter (2017).

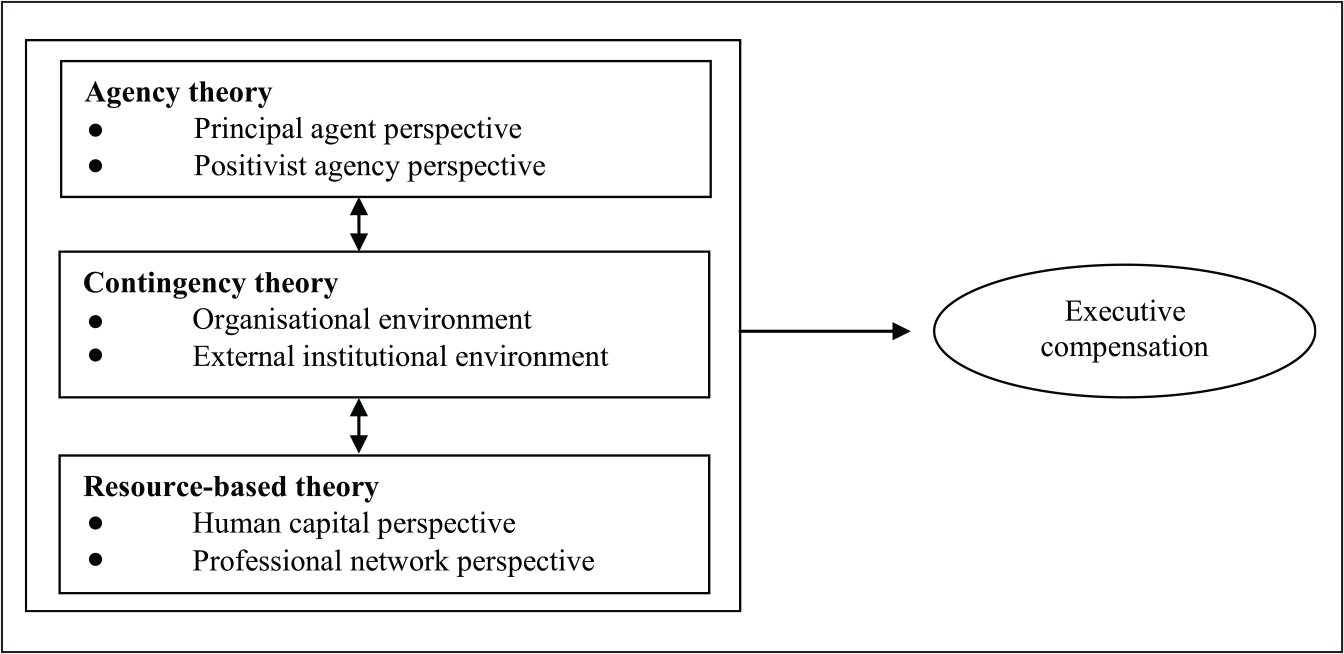

Thus, as evident, both Indian executives and investors are predisposed to relate pay to performance as the traditional economic theory and compensation literature typically suggests (Coombes & Watson, 2000; Firth, Fung, & Rui, 2007; Raithatha & Komera, 2016). In general, the results are also consistent with other surveys on top-management compensation that have used executives and/or investors as respondents in testing the generalisability of agency theory (Fleming & Schaupp, 2012; Kay, 2008). However, in contrast to the Western world, investors in India apparently realise the influence of promoter-owners on the corporate compensation practices. Notwithstanding the stringent legal environment, they look to alternative mechanisms for disciplining errant executives. Further, the inter-domain determinants of executive pay are quite realistic and rational, evidencing that individuals exhibit different orientations within a given context as shown in Figure 1. The article, thus, corroborates that there exists difference in what executives and investors perceive to be the determinants of executive compensation, evidencing the significance of intermediation in the Indian context.

Past research relating to determinants of executive compensation has been generally associated with regimes wherein ‘say-on-pay’ policies have not yet become an accepted aspect of corporate governance. In India, compensation policies and limits are approved and may be altered by shareholders. Thus, findings of the present study should be interpreted carefully due to the following limitations. First, an attempt has been made to deduce perceptual intent based on survey results. Second, a more rigorous analysis involving larger and more diverse sample would have allowed for higher level of generalisability. Lastly, the present survey solicits responses on various compensation measures based on archival research.

Regardless of these limitations, the study is pertinent in the present context given the growing public criticism and practitioners’ concern towards rising executive pay in many emerging economies. This survey is the first of its kind conducted with respect to an upcoming market. It reviews empirical evidence of executive compensation for these economies, highlighting its peculiarities and contributions to the vast body of Western literature by unravelling the complexities in determination of executive pay by putting forth a multi-theoretical perspective. The results of the study significantly contribute to the existing literature in the following ways:

First, whilst majority of the compensation studies relied solely on data from publicly traded companies, this has not, in practice, resulted in actual advancement of the field of study (Cole & Mehran, 2016; Tosi Jr & Gomez-Mejia, 1989). Moreover, the surveys conducted by most consultancy firms fall short of a strong theoretical orientation and econometric foundation, thereby not capturing a holistic view of the pay setting scenario. Whereas, the present study has examined the determinant factors in executive compensation based on survey data using strong theoretical arguments by applying advanced analytical techniques.

Second, to the best of the researcher’s knowledge, difference between the perceptual view of executives and investors in factors desired to determine executive compensation has not been explored in context of transitional and emerging countries.

The study provides valuable insight into the dilemma faced by the two key stakeholders, that is, the executives and investors, as apparent in the discernment of executive compensation in India. The results show that executives and investors approach pay issues from very different perspectives. It is only by examining the differences in the disposition of these key stakeholders that an attempt can be made to address issues around setting executive compensation (Garen, 1994).

Third, in the wake of criticism of executive pay being unidirectional, without regard of corporate performance, discerning the basis of determining executive pay assumes paramount importance. In the Indian context, however, lack of knowledge or epistemological underpinnings to the expectations and processes within which executive compensation is structured and set constitutes the real problem. The findings of the survey have addressed this gap in literature and extended understanding on two fronts—the relative disposition of executives and investors to the determinants of executive compensation as well as the underlying dimensions representing pay determination in the context of corporate India.

Lastly, the survey results clearly highlight that no single theory completely explains the executive pay determination, which suggests a need to apply amulti-theoretical approach. This study uses survey data, which may provide policymakers and regulators with salient information necessary to make future regulatory changes in the realm of corporate governance. The findings of the study would also be useful to practitioners and academicians as it provides first-hand evidence about the perceptual view on determinants of compensation in the Indian context.

The present article is a step towards analysing the predisposition of executives and investors. The fact that investors show pay-for-performance sensitivity suggests that corporates need to initiate reversal of controversial pay practices and work towards better disclosure of performance related pay policies. Ultimately, companies that are responsive to shareholders’ expectations and engage in a dialogue with them are most likely to succeed in the emerging Indian and global business environment. Additionally, it is equally important to anticipate the expectations of management in response to the changing market and industry trends as regards pay. It is, therefore, important to reconcile these distinct interests as the market continues to shape the executive pay paradigm (Kay, 2008). Future research can be extended to apply larger samples and other stakeholders. Further, research initiatives can be built around other factors, such as political, social, cultural, behavioural, etc., as plausible determinants of executive compensation. Finally, the present study is in the context of India wherein compensation policies and limits are approved by shareholders. Future research could critically appraise the impact of law and key pay reforms in determining compensation. Such extensions may enable better appreciation into indigenous factors influencing executive compensation and the reasons for the pervading gap in the perception of executives and investors.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.