Abstract

This study integrates the research on corporate political strategy and corporate governance. Using the agency theory perspective, this study examines how corporate governance mechanisms such as institutional ownership, insider ownership, and long-term executive compensation affect a firm’s political strategy approach. This study proposes that an agency problem may occur between owners and managers in regard to firms’ approach to corporate political strategy. Since a relational approach to corporate political strategy, such as establishing a government relations office in Washington, DC, requires significant resource commitments without guaranteeing a favorable policy change, shareholders might be reluctant to approve such an approach. In a sample of 3,417 U.S. manufacturing firms, over 5 years of data, the results show that institutional ownership and insider ownership are negatively associated with firms’ propensity to engage in a relational approach to political strategy.

The increasing effect of government policies on the competitive environment of firms has contributed to firms’ involvement in political activity. Since government policies greatly affect a firm’s cost of doing business in some industries, the extent to which a firm pursues a political strategy is recognized as one of the most important decisions in a firm’s nonmarket strategies (Hillman, Keim, & Schuler, 2004). Prior research suggests that corporate political strategy (CPS) is influenced by a variety of firm (Hillman, 2003; Hillman & Hitt, 1999; Oliver & Holzinger, 2008), industry (Hansen, Mitchell, & Drope, 2005), and issue-related factors (Getz, 1993) among other factors (Getz, 2002). Although these studies imply that such factors do matter, they implicitly assume that CPS is determined by managers whose interests are aligned with those of investors. However, recent research strongly indicates a divergence of interests in CPS between managers and owners. This research not only indicates that returns on political investments are questionable but that shareholders are concerned about such activities (Aggarwal, Meschke, & Wang, 2012; Coates, 2011). Due to the opaque and uncertain nature of CPS (see Hart, 2004, for a review, and also Snyder, 1992), shareholders will face information asymmetries when assessing the effectiveness of their portfolio firms’ political activities, and executives of such firms may engage in riskier and short-term strategic choices as well as focus on personal managerial benefits. Aggarwal, Meschke, and Wang (2012), Coates (2011), and Hadani (2011) all report the same negative association between different forms of institutional ownership and firms’ political activities. Under existing law, firms are not required to report their political strategies to their shareholders (Bebchuk & Jackson, 2010). In recent years, shareholders have become more vigilant regarding firms’ political activities, and demand that public companies make their political contributions and lobbying activities more transparent (Bernstein, 2008). For example, JP Morgan Chase & Co’s shareholders required that the company disclose how and why it uses company money to engage in political action at their annual meeting in 2006 (Tambe, 2006). Hence, there is growing evidence indicating a possible divergence of interests between managers and owners when deploying firm resources to pursue CPS.

However, studies that support a negative association between firm ownership and CPS have not distinguished between different types or approaches to firms’ political strategies; they assume a uniform effect of governance mechanisms (such as ownership) on firms’ political strategies. In this context, Hillman and Hitt (1999) differentiate between relational and transactional forms of CPS. Transactional CPS reflects firms’ engagement in CPS only when firms feel there is a need or an issue that matters to them or that requires attention but not otherwise. Relational CPS reflects firms’ continuous and long-term interactions with policy makers so when or if the need arises the firm can utilize its already existing CPS (Hillman & Hitt, 1999). The two approaches represent very different forms of CPS and different views of CPS: one is more reactive and thus may represent a late response to political contingencies and the other is more proactive and long-term oriented. For example, to pursue higher involvement in public policy, firms establish government relations offices in Washington, DC. Having such offices indicates a firm’s willingness to allocate significant and continuous resources. It also reflects, at least theoretically, a firm’s ability to monitor policy making more effectively and closely (Hillman & Hitt, 1999) in a way that may avoid agency conflicts with hired lobbyists (i.e., Kersh, 1986). Thus, unlike a more transactional or short-term approach to political strategy, relational CPS, in particular having a Washington, DC office, may actually enhance shareholder value. Yet, existing research exploring the effects of ownership on CPS has not looked at how firm owners react to this unique type of CPS; much of the existing research has looked at ownership’s effects on political action committee (PAC) or lobbying expenditures that may at least partiality reflect nonrelational CPS (Hadani, 2007).

This article is built on the premise that firms’ propensity to engage in relational CPS depends on their corporate governance structures. Specifically, this article examines the effects of institutional investors, insider ownership, and executive compensation on firms’ tendency to pursue a relational approach. Drawing on agency theory arguments (Jensen & Meckling, 1976), this study argues that while there may be benefits associated with a relational approach to CPS, owners may also be wary of it due to the continuous nature of resource investments it requires without a clear return on such investments (Hart, 2004; Lowery, 2007). Hence, it is plausible that a relational approach can be more prone to agency problems.

This study makes two main contributions. First, it takes an agency theory perspective to CPS approach. Although previous studies that draw on agency theory assumptions (Getz, 1993; Mitnick, 1993) contribute to our understanding of CPS, research on the possible agency problems in CPS approach is relatively new and emerging. Though studies have began looking at an agency theory interpretation of CPS (Aggarwal et al., 2012), they have not looked at specific aspects of CPS approaches. This study adopts an agency theory perspective which suggests that improved corporate governance mechanisms will minimize the divergence of interests between managers and owners with respect to CPS approach.

Second, this study contributes to the corporate governance research. Prior research on ownership structure has largely neglected the impact of ownership structure on nonmarket strategies. Most ownership structure research has focused on market-oriented strategies such as diversification, innovation, international expansion, and research and development (R&D) investments (see Gerhart, Rynes, & Fulmer, 2009, for a review). Yet, other studies have indicated that nonmarket strategies have important implications for firm performance and shareholder value (Boddewyn, 2003; Bonardi, Holburn, & Bergh, 2006; Hillman, Zardkoohi, & Bierman, 1999; Shaffer, Quasney, & Grimm, 2000; Vogel, 1996). This study, therefore, argues that ownership structure also influences firms’ nonmarket strategies. Different owners have divergent interests and ownership stakes in a firm, giving them different preferences toward nonmarket activities.

The rest of the article is organized into four more sections. The next section discusses why ownership structure affects firms’ CPS approach. The subsequent section explains the development of testable hypotheses. The next section explains the methods for this study. To examine these hypotheses, this study uses a sample of 3,417 firms in the U.S. manufacturing industry between 1998 and 2002. The final section discusses the findings and their implications for future research.

Theoretical Background

Corporate Political Strategy Approach

CPS plays an important dual role—as both a significant competitive resource for firm performance and an investment with uncertain outcomes—in the strategy formulation process. Although there are different views on CPS, there seems to be an agreement in the literature that CPS decisions are one of the significant decisions in strategy formulation. As a result, CPS may be of interest to senior executives (Hart, 2004). Griffin and Dunn (2004) find that senior executives’ commitment is critical in allocating additional resources for political strategy. There is disagreement on whether these commitments are beneficial. Prior literature on CPS diverges on whether political strategies have intended effects on firm performance. An extensive body of research views political strategy as an investment with positive outcomes for firm performance and argues that firms engage in political strategies to control their nonmarket environment. For example, Getz (2002) finds that CPS results in less dependence on government action and reduces environmental uncertainty. Salorio, Boddewyn, and Dahan (2005) assert that political strategy can be a source of rent-creating competitive advantage that should be integrated with economic and organizational strategies. In addition, a number of empirical studies indicate that CPS positively affects firm performance. Hillman, Zardkoohi, and Bierman, (1999) find that linkages with the government, such as having a firm representative to serve in a political capacity, positively affect firm value. Shaffer, Quasney, and Grimm, (2000) find that firms (in the airline industry) engaging in political strategies are more likely to experience above-normal performance. By studying the number of ex-politicians on the board of directors, Hillman (2005) also indicates that political connections positively affect firm performance.

However, another stream of research is skeptical about the impact of CPS on firm performance. Scholars highlight the uncertainty of the immediate impact of political strategy on legislative processes and their consequent financial returns (Baron, 1995; Getz, 2002; Rehbein & Schuler, 1999). Also, scholars note that the actual impact of political strategy on market-oriented strategies is indirect, since political strategy returns are primarily derived via the possible consequences of legislative outcomes on market-oriented strategies and firms’ competitive environments (Hillman & Hitt, 1999). Several studies also argue that political contributions do not deliver the expected benefits and have minimal impact on changing public policy (Aggarwal et al., 2012; Gordon & Hafer, 2005). Moreover, collective action problems (Olson, 1965) may occur; namely, the industry as a whole may share the benefits of a single firm’s successful lobbying for the passage of a favorable regulation without incurring the cost of lobbying. In addition, policy makers may be inclined to maintain political status quo (Baumgartner, Berry, Hojnacki, Kimball, & Leech, 2009). Even though firms use a variety of political strategies to change existing public policies, the efforts to change an existing policy orientation could fail (Lowery, 2007).

The efficacy of CPS may depend on its type or strategic approach. The level of influence and involvement the firm will pursue when engaging in CPS is one of the first decisions a firm must make in formulating its political strategy. Hillman and Hitt (1999) provide a parsimonious model of political strategy approach where they distinguish between transactional and relational approaches to CPS. Having government relations offices in Washington, DC is a very common tactic of relational approach (Hillman & Hitt, 1999). Companies such as Comcast, General Electric, Motorola, and Credit Suisse, for example, have offices in Washington, DC that engage in lobbying. The existence of these offices indicates that some firms are acutely concerned about the influence of government; they incur the cost of having full-time representation in Washington, DC. Establishing a Washington office indicates a long-term interest and a higher level of involvement in public policy formation. Lobbying and PAC contributions, however, are deemed common tactics of the transactional approach; studies show that firms use lobbying tactics when the need arises (Lowery, 2007; Schuler, Rehbein, & Cramer, 2002). Firms hire lobbyists for specific purposes or specific areas of expertise. PACs are seen as complementary to lobbying because PACs provide access to politicians (Schuler et al., 2002).

Following Hillman and Hitt (1999), this study argues that these political strategy approaches differ in several ways. First, although a transactional approach includes a short-term horizon and is made on an issue-by-issue basis, a relational approach is long-term oriented and made on a continuous basis(Hillman & Hitt, 1999). Establishing and maintaining government relations offices imply that firms are willing to use their resources to incur the cost of having these offices so that they can utilize these offices over a long period of time. Second, this study argues that these approaches require different resource commitments. The decision on political strategy approach can be perceived as a strategic decision where firms make trade-offs between resource commitments to either a relational or a transactional approach. Compared to a transactional approach, a relational approach may require more significant resource investments that allow firms to continue their relationships with policy makers over time. Having full-time staff in government relations offices indicates a substantial investment whereas hiring outside lobbyists for a specific issue involves relatively lower levels of investments, since firms can terminate external lobbying contracts much more easily and without significant costs compared to shutting down a Washington, DC presence.

Third, this study posits that relational approach requires heavy and long-term investments with potential higher returns as long as firms maintain their relationships with policy makers over time. Firms’ relations with policy makers may enable them to affect public policy, which spurs firms’ continued economic survival (Hillman & Hitt, 1999). Nevertheless, firms may not receive favorable policy outcomes despite their efforts. Scholars have indicated the strong momentum in Washington toward maintaining the status quo (Baumgartner et al., 2009) as well as the inherent uncertainty of the policy-making process (Keim, 2001; Lowery, 2007) even for those who consistently interact with policy makers (Kersh, 1986, 2002; Smith, 2000). This study, therefore, asserts that though relational CPS provides firms with greater control over their political environments by having full-time representation in Washington, DC (and the potential for higher long-term returns), relational CPS also represents greater risks and longer payback periods.

Thus, pursuing a relational approach to political strategy has important implications for shareholders and managers. This study proposes that investors and managers may have different preferences and interests in the CPS approach. This divergence may culminate in an agency problem that encompasses the propensity of managers to pursue agendas that may conflict with shareholders’ interests and preferences (Jensen & Meckling, 1976; Coates, 2011). Recent research has described potential differences between managers and shareholders with respect to political spending, implying an agency problem between managers and shareholders (Aggarwal et al., 2012). Coates and Wilson (2007) find a negative relationship between trade associations’ political activities and average returns on stock markets. Their findings indicate that such political activities are associated with an inefficient allocation of resources. Coates (2011) finds that firms with strong corporate governance practices which empower shareholders engage in less political activity, and firms that engage in political activity generate less shareholder value. He also reports that CEOs of politically active firms may extract higher private rents and seek post corporate employment as politicians; private benefits may overshadow long-term corporate interests. Mathur and Singh (2011) argue that CPS could be reflective of agency conflict due to two reasons. First, senior executives may undertake political strategies that will boost short-term firm performance at the cost of long-term shareholder value maximization. Second, senior executives might invest their firms’ resources in political strategies in the pursuit of personal interests, such as political connections and positions, promoting political ideologies and preference; thus they waste firms’ resources which will not yield shareholder value (see also Aggarwal et al., 2012). Consequently, this study argues that ownership structure affects how owners and managers perceive the firm’s investments in CPS, and this effect has important implications for how firms make decisions regarding their political strategy approach.

Hypotheses Development

Institutional Ownership

Institutions such as pension funds, mutual funds, insurance companies, and foundations nowadays own about 70% of the largest 100 firms in the United States (Heineman & Davis, 2011). A large body of literature suggests that institutional investors could influence management in two ways (Daily, Dalton, & Cannella, 2003; David, Hitt, & Gimeno, 2001; Dharwadkar, Goranova, Brandes, & Khan, 2008; Neubaum & Zahra, 2006). First, due to their large percentage shareholdings institutional investors have a significant influence over security trade. Since they can exit their equity positions, they can directly impact the market price of stocks. As a result, they have significant leverage in negotiations with management. Second, institutional investors hold substantial voting rights. As investors with significant voting rights, they can exert power and influence management’s strategic decisions to protect their own interests. Thus, institutional investors have both the incentive and ability to influence strategic decisions made by management. These large, concentrated owners are believed to have a long-term interest in the firms they invest and act like stewards of corporate resources (Connelly, Tihanyi, Certo, & Hitt, 2010; Musteen, Datta, & Herrmann, 2009; Heineman & Davis, 2011).

Another important stream of research which investigates the value of CPS argues that political strategy lowers shareholder value (Coates, 2011) and signals agency problems in the organization (Aggarwal et al., 2012; Gordon & Hafer, 2005). According to Gordon and Hafer (2005), although corporations expect to influence public policy, empirical research fails to show a definitive relationship between CPS and policy change. The complexity of the political marketplace (Baumgartner et al., 2009) and its uncertain nature (Smith, 2000) attest to this dynamics; firms may assume CPS is effective when it is not (Hart, 2004; Kersh, 1986). In fact, CPS might be viewed as a way to satisfy the managements’ need to participate in politics (Ansolabehere, de Figueiredo, & Snyder, 2003).

Drawing from these two streams of literature, this study argues that institutional investors may either prefer or oppose relational CPS. On the one hand, investors may prefer a more long-term approach to CPS because of its potential for creating stable relationships with policy makers or monitoring abilities over the long term (Hansen, 1992). A relational approach, especially maintaining a Washington, DC office, provides firms the ability to cultivate intimate relationships with policy makers who have been on relevant committees and assess the reliability of policy makers (Kroszner & Stratmann, 2005). Also, firms’ long-term relationships with policy makers may impel them to act sympathetically toward these firms and develop policy positions that could favor these firms (Kroszner & Strahan, 2001). Thus, in theory, a relational approach can help the firm learn about policy makers’ agendas and changes in the policy-making process that can help the firm deal with political dependencies.

On the other hand, institutional investors might be reluctant to approve a relational approach to CPS since these investments represent long-term commitments, such as establishing a Washington, DC office and have uncertain outcomes. First, once a firm undertakes their political activity through the establishment of a Washington, DC office that office will have powerful incentives to continue its operations and to justify its existence even if it is not necessarily successful. Second, though a relational approach has the potential for higher returns, the significant resource investments in relational approach also have greater risks. For example, considerable uncertainty is embedded in firms’ relational approach as their efforts may not succeed in terms of securing desired or preventing threatening legislation or regulation (Lowery, 2007).

This study proposes that the information asymmetry between institutional investors and managers regarding the value and long-term effects of CPS may contribute to institutional investors’ reluctance for relational CPS as well. Information asymmetry between institutional investors and managers is deemed a prominent source of agency problems (Eisenhardt, 1989; He & Wang, 2009). Managers of politically active firms presumably possess far more information than institutional investors about the public policy environment (Blumentritt, 2003; Epstein, 1969). Institutional investors’ lack of firm-specific information with regard to the uncertain process of creating value from CPS (i.e., Snyder, 1992) may deter them from supporting firms’ investments in relational CPS. Even though managers undertake a political strategy with the intention of creating favorable policy environment for the firm’s operations, institutional investors may not see managers’ efforts as value maximizing. Institutional investors could view political strategy as pursuit of a pet project by managers, which is unrelated to shareholder interest (Coates, 2011). Indeed, according to a survey conducted by the Center for Political Accountability (2006), 73% of shareholders believe that CPS is pursued to advance the personal political interests of managers rather than the firm’s interest.

Also, institutional investors may perceive that they are more vulnerable to agency problems in the context of relational CPS as there is no legislation requiring disclosure of political strategy to shareholders and shareholder approval of the firm’s political strategy (Bebchuk & Jackson, 2010). Although firms must disclose their PAC and lobbying expenses as required by law, they are exempt from reporting the resources allocated to other types of CPS, such as establishing, operating, and maintaining a Washington, DC office, which involves a significant resource cost. In other words, engaging in relational CPS increases CPS costs substantially. Yet, it also likely increases information asymmetry between mangers and owners. In fact, Gardberg and Schepers’s (2011) study indicates that firms that engage in political activities the most disclose the least information about their political activities. Given the disparity between costs and actual returns, investors may experience higher information asymmetry especially with regard to relational CPS; making it a less attractive strategy for them. Although institutional investors are not directly involved in the CPS decisions, their monitoring and influence could affect managers’ decisions regarding CPS approach as it has been documented for market oriented strategies (Dharwadkar et al., 2008). Thus, even though relational CPS may have potential for future firm payoffs, this study proposes a negative association between institutional ownership and relational approach to CPS. Accordingly:

Hypothesis 1: Firms with higher levels of institutional ownership are less likely to use a relational approach to corporate political strategy.

Insider Ownership

According to agency theory (Eisenhardt, 1989) several incentive mechanisms help mitigate agency problems by aligning the objectives and interests of owners and managers. Insider ownership is considered to be an important incentive mechanism to establish improved corporate governance. (Beatty & Zajac, 1994; Gomez-Mejia, Larraza-Kintana, & Makri, 2003; Zajac & Westphal, 1994). Insider ownership encourages managers to act in a way that benefits both themselves and firm’s shareholders. When key executives have significant ownership in their firms, they are more likely to favor investments that maximize shareholder value (Wright, Kroll, Krug, & Pettus, 2007). Their significant control of a firm’s stock induces them to focus on investments that will maximize shareholder value.

Extending the above arguments to CPS approach, this study proposes that firms with higher levels of insider ownership are less likely to engage in relational CPS, in particular establish a Washington, DC office. According to Aggarwal et al. (2012), firms with good corporate governance practices are less likely to make large donations to political activities. In a similar vein, this study argues that executives’ higher equity ownership will more likely to deter them from making significant amounts of resource commitments that might not maximize shareholder value. Establishing a Washington, DC office is a costly and continuous investment for firms. When their personal wealth is closely linked to shareholder value, insiders will be less likely to make investments that are not closely linked to better returns. Thus, even though executives with significant equity ownership may acknowledge the potential long-term positive outcomes of a relational approach to their firm, they may still be reluctant to support relational CPS. Accordingly:

Hypothesis 2: Firms with higher levels of insider ownership are less likely to use a relational approach to corporate political strategy.

Executive Compensation

Drawing from agency theory, researchers have suggested that long-term executive compensation is another corporate governance mechanism that can alleviate agency problems (Jensen & Murphy, 1990; Westphal & Zajac, 1994). Long-term executive compensation represents a prominent mechanism to ensure the proper alignment of the interests of managers with those of owners (Eisenhardt, 1989; Gomez-Mejia & Balkin, 1992). Although short-term compensation consists of a base salary and short-term incentives, long-term compensation entails stock options, restricted stock grants, deferred compensation benefits, and long-term accounting-based incentive plans (Dalton, Hitt, Certo, & Dalton, 2007). Prior research indicates that short-term compensation encourages managers to maximize a firm’s short-term performance and hinder their interest in taking risks and making long-term commitments (Gerhart et al., 2009). However, long-term compensation spurs managers to pursue long-term oriented strategies and invest in activities that enhance long-term firm performance (Datta, Musteen, & Herrmann, 2009; Wiseman & Gomez-Mejia, 1998).

In the context of this article, firms that compensate executives with longer-term incentives are expected to be less likely to undertake a relational approach to CPS. According to agency theory (Jensen & Meckling, 1976), incentive mechanisms such as long-term compensation might curb executives’ desire to pursue actions that might benefit themselves while jeopardizing shareholder value in the long run. Establishing a Washington, DC office might provide executives with immediate visibility and political capital while failing to deliver desired policy changes in the long run. Executives must consider the potential costs and benefits of relational approach that may indirectly impact firm performance in the long term. The effectiveness of executive compensation depends on the extent of tying the behavior of executives to the interests of their shareholders. Long-term compensation impels executives to consider long-term success of their firms and their shareholders; thus, they make decisions that are consistent with shareholders interests. Accordingly, long-term executive compensation can mitigate an agency problem. Aggarwal et al. (2012) find that firms with less abnormal executive compensation—an indicator of good corporate governance—engage in less CPS. Since it is difficult to directly link a relational CPS to firm performance (Ansolabehere et al., 2003; Hart, 2004; Lowery, 2007), executives should be less inclined to invest in a resource-intensive and uncertain relational approach. Accordingly:

Hypothesis 3: Firms with long-term executive compensation are less likely to use a relational approach to corporate political strategy.

Method

Sample

The empirical analysis was carried out in the manufacturing industry (SIC code=2000–3990) in the United States during the period 1998-2002. The manufacturing industry is a particularly interesting setting for this study due to several characteristics. For example, manufacturing firms have allocated a substantial amount of resources to a variety of corporate political strategies in decades (Center for Responsive Politics, 2012). Also, there has been an increased role of government in regulating the environment of the manufacturing industry such as trade agreements (Rehbein & Schuler, 1999). This study focuses on the time period between 1998 and 2002 due to the significant changes in the campaign finance law. The Lobbying Disclosure Act of 1995 requires firms to disclose money spent on lobbying activities. Shareholders now have access to their firms’ spending on lobbying activities. Also, the Bipartisan Campaign Reform Act of 2002 that contains many substantial and technical changes to the federal campaign finance law was signed. Due to these developments, shareholders have become more vigilant and have started demanding more transparency on corporate political strategies. The underlying rationale for gathering time series data is that a longer time frame allows us to better understand the relationship between corporate governance and relational CPS by eliminating possible time specific biases.

To construct the sample, several sources have been used. The data for firm financial information came from the COMPUSTAT database. These data were supplemented with information from the publication “Washington Representatives” (2009) that is used to measure the dependent variable, COMPUSTAT’s ExecuComp which provides information about executive compensation, and Thomson Financial Network that is used to construct the measures of ownership. After merging all databases, the sample consisted of 6,843 observations, encompassing 3,417 firms.

Measurements

Dependent variable: Consistent with prior research (Hillman & Hitt, 1999), the authors measured a firm’s relational approach to CPS with having a government relations office in Washington, DC. Establishing a Washington, DC office indicates that firms are willing to incur a higher cost of relational CPS with the intention to build intimate relationships with policy makers and obtain legislative favors. The dependent variable is a dummy that takes 1 if a firm has a Washington, DC office, and 0 otherwise (Lenway & Rehbein, 1991).

Independent variables: This study tests the effects of institutional ownership, insider ownership, and executive compensation on CPS approach. Institutional ownership is the percentage of ownership held by the institutions such as banks, mutual funds, insurance companies, pension funds, university endowments, investment banks, etc. Insider ownership is measured as the percentage of ownership held by the top management team and board of directors of the firm (Johnson & Greening, 1999). Executive compensation can be divided into two broad categories: current compensation and long-term income. Long-term income consists of pensions, profit sharing, stock options, and long-term incentive plans (David, Kochhar, & Levitas, 1998; Mahoney & Thorne, 2005). Long-term compensation is measured as long-term income (including the total value of any restricted stock granted, the net value of options exercised, long-term incentive pay-outs, and other annual compensation) divided by total income of an executive.

Control variables: Several variables that might affect firms’ tendencies to pursue a relational approach were controlled. Previous research has showed that organizational slack affects firms’ decision to invest in CPS (Grier, Munger, & Roberts, 1991; Lenway & Rehbein, 1989; Rehbein & Schuler, 1999). Organizational slack is calculated as equity in earnings divided by total sales. We also controlled for firm size since larger firms tend to invest more in CPS. Firm size is measured as the natural logarithm of total assets (Schuler, 1996). Another important variable that has been shown to affect CPS is past firm performance (Hillman, 2003). Past firm performance is the average of return on assets in the past three years as net income divided by total assets. Following prior literature, we controlled for leverage since it affects firms’ tendencies to invest in CPS (Schuler, 1996). Leverage is calculated as total long-term debt over total assets. Prior literature tested the relationship between R&D intensity and CPS (Hart, 2003). R&D intensity, calculated as R&D expenditures over total sales, is controlled. Industry and year dummies are used to avoid any seasonal and industry effects.

Results

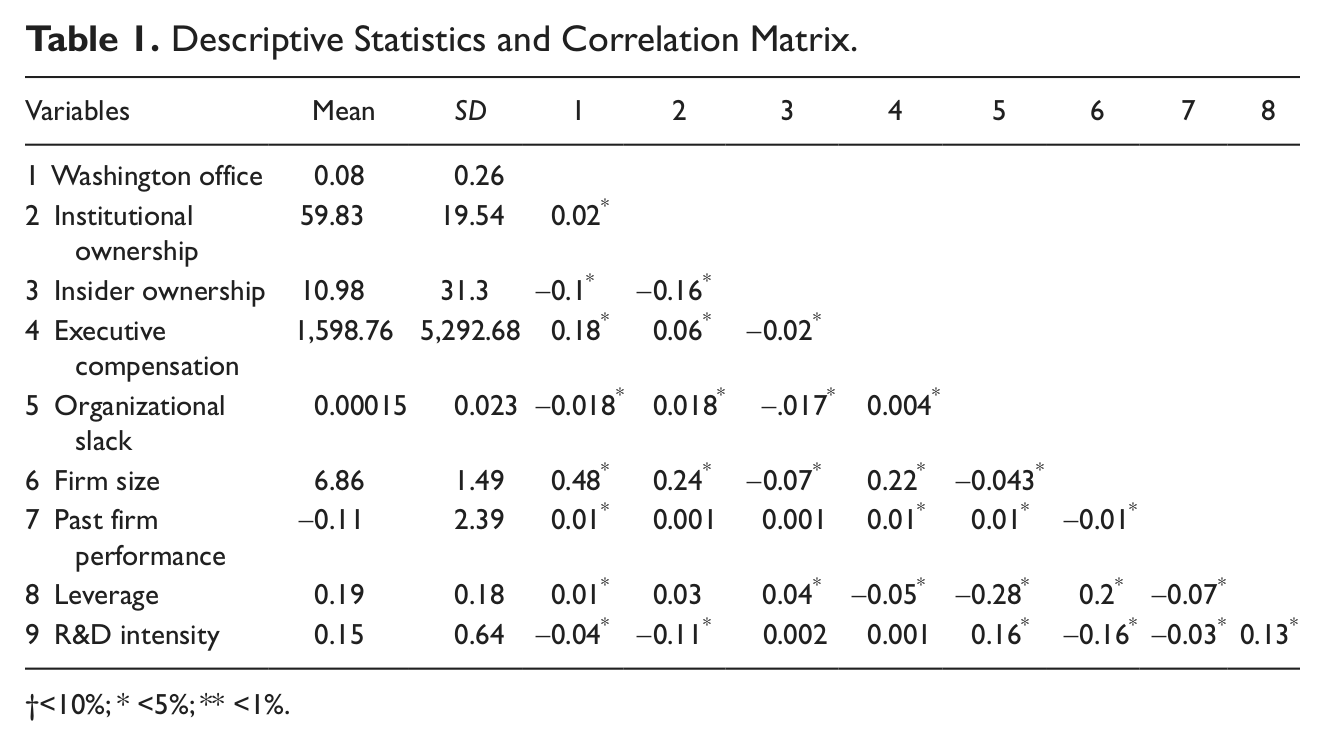

Hypotheses are tested using logistic regression. Table 1 reports the descriptive statistics and pairwise correlations. As seen in the correlation matrix, there are strong correlations between the variables. To rule out any multicollinearity problems, variation inflation factor (VIF) for each variable is calculated. The mean VIF is 1.48 for the model that is much lower than the threshold point of 10.

Descriptive Statistics and Correlation Matrix.

<10%; * <5%; ** <1%.

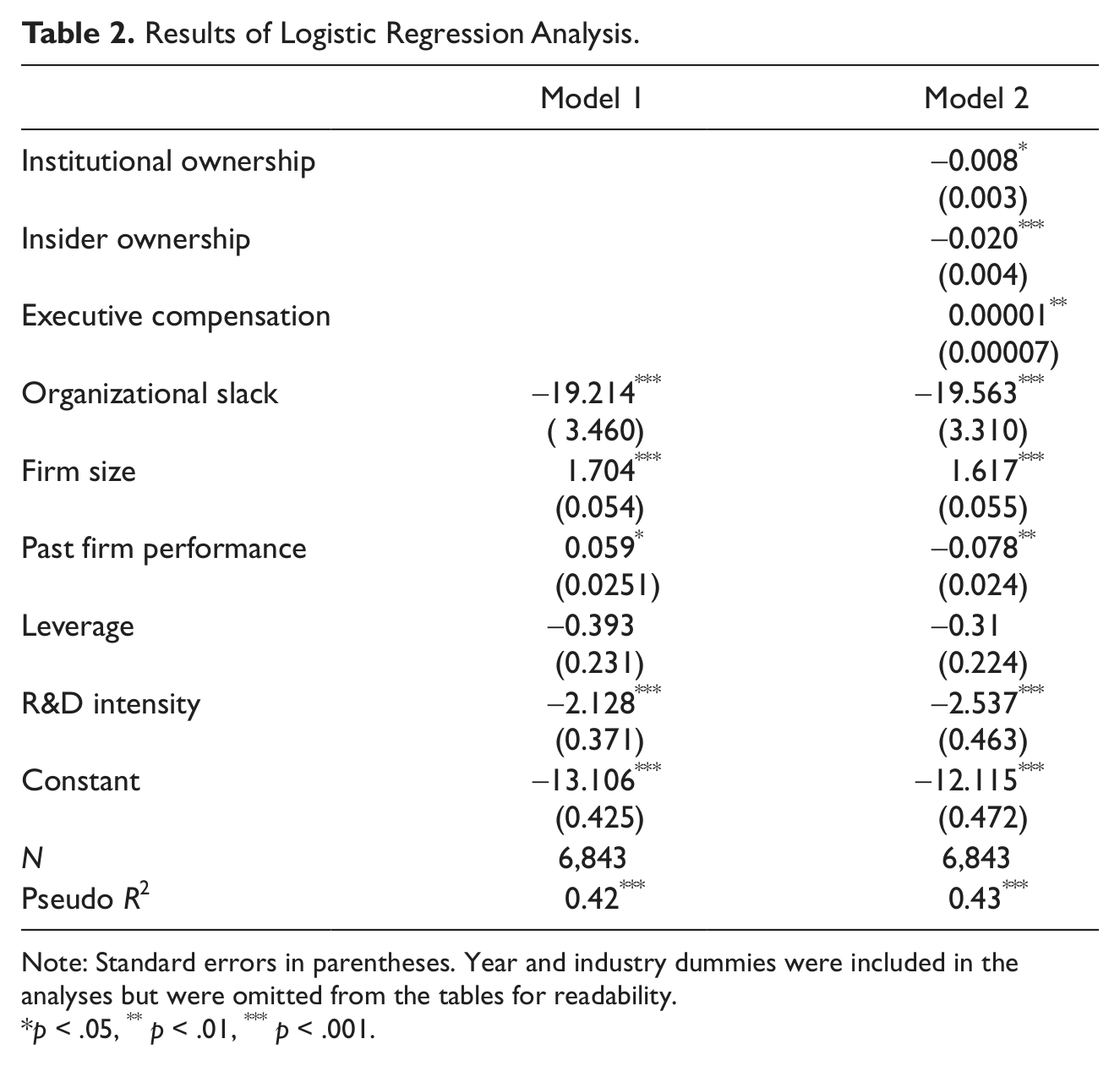

Table 2 reports the results of the logistic regression. We first entered the control variables and then the main effects. Hypothesis 1 predicts that firms with higher levels of institutional ownership are less likely to pursue a relational approach to CPS. According to Model 2 of Table 2, the coefficient of this variable is negative and significant (p < .05), supporting Hypothesis 1.

Results of Logistic Regression Analysis.

Note: Standard errors in parentheses. Year and industry dummies were included in the analyses but were omitted from the tables for readability.

p < .05, ** p < .01, *** p < .001.

Hypothesis 2 suggests that firms with higher insider ownership are less likely to pursue a relational approach to CPS. According to Model 2 of Table 2, the coefficient of this variable is negative and significant (p < .001), providing support for this hypothesis.

Finally, Hypothesis 3 predicts that firms with higher levels of executive compensation are less likely to pursue a relational approach to CPS. Contrary to what this study predicts, executive compensation variable is positive and significant (p < .01).

Some of the control variables are also strongly related to the relational CPS. Firm size and past performance have positive and significant effects, while organizational slack and R&D intensity have negative and significant effects on the firms’ propensity to pursue a relational CPS. The negative relationship between organizational slack and relational CPS shows that firms having slack resources may opt to allocate their resources to market-oriented strategies rather than long-term-oriented CPS. Similarly, the negative relationship between R&D intensity and relational CPS could indicate that firms with less R&D intensity engage in more political action as they view political action as a substitute for investment in R&D (Aggarwal et al., 2012).

To ensure the robustness of the findings, additional analyses were run. Hadani (2007) used soft money contributions as a proxy for relational CPS arguing that firms make these contributions with the intention of having long-term relations with political parties. Also, soft money contributions are aimed at a national party, not a federal candidate, and represent a more stable institution (Hadani, 2007). To test whether the hypotheses would hold true, additional analyses were run using soft money contributions as dependent variable. The results were consistent with the original findings.

Discussion

This study aims to understand how ownership structure affects a firm’s tendency to pursue a relational CPS by building on the CPS and corporate governance literatures. The results corroborate that ownership structure affects a firm’s political strategy approach. Specifically, the findings indicate that firms with higher institutional and insider ownership are less likely to pursue a relational CPS. From a theoretical perspective, these findings support the basic predictions of agency theory, suggesting that firms with improved governance structures are less likely to engage in a relational CPS that might adversely affect shareholder value. Contrary to the expectations of this article, the findings indicate that firms with higher levels of long-term executive compensation are more likely to engage in relational CPS. One possible reason could be that executives’ tenure might affect their perception of relational CPS. Despite the uncertainty of relational CPS outcomes, longer tenure of executives might affect their decision to support relational CPS as it may seem beneficial on a long-term basis (i.e., Coates, 2011). Future research can examine the moderating effects of executive tenure on the relationship between executive compensation and relational CPS. Another reason may be related to the risk characteristics of stock option compensation, in comparison to stock ownership. Unlike stock ownership, stock options reflect asymmetric risk, offering upside wealth potential with limited downside risk (Sanders, 2001). Thus, executives may view the potential returns of relational CPS as justified—their stock price may go up but is less likely to go down; they have nothing to lose, equity compensation wise. The same cannot be said for stock ownership that not only have immediate income effects but also that can go down or up in real economic terms (Sanders, 2001).

The majority of past research implicitly assumes that the interests of managers are aligned with those of owners in regard to the choice of CPS. However, recently, scholars have explored whether political spending can be a source of agency problems. Most notably Aggarwal et al. (2012) and Coates (2011) argue that corporate political spending adversely affects shareholder value. This study extends this stream of research by taking a more fine-grained approach and focusing on relational CPS arguing that the scale and scope of establishing a Washington, DC office might induce conflicts of interest between managers and owners. This article also focuses on different aspects of good corporate governance indicators such as institutional ownership, insider ownership, and long-term compensation.

In addition, this study contributes to the research on corporate governance by suggesting that ownership structure influences nonmarket strategies. Prior research on corporate governance examines the relationship between ownership structure and various market strategies such as diversification, innovation, mergers and acquisitions, etc. (Connelly et al., 2010). The findings suggest that nonmarket strategies have important implications for perceived shareholder value or lack thereof; understanding the relationship between ownership structure and nonmarket strategies is therefore critical. This study brings these different research streams together by examining the role of ownership structure on CPS approach.

However, this study is not without limitations. First, the sample is based on the manufacturing industry and the results may not be applicable to firms’ CPS in other industries. Future research should examine the research question in different industry settings such as finance, utility, service, etc. Second, there is no distinction between different types of institutional investors. Recent studies indicate that different types of institutional investors have different preferences for firm strategies (Connelly et al., 2010). Future research should incorporate different categories of institutional investors such as pension funds, mutual funds, banks, insurance companies, etc. into firms’ political strategy approach. Future research should also address potential moderating effects. It is plausible that several corporate governance variables such as board characteristics, CEO compensation, and industry structure may also moderate the relationship between ownership structure and political strategy approach. Finally, future research might go beyond the scope of our study and explore multiple agency conflicts in CPS. For example, future studies might address the pursuit of political strategy by the firm and its institutional investors.

In conclusion, this study contributes to the understanding of how firms make decisions pertaining to their political strategy approach. The agency perspective proposed here suggests that firms’ ownership structure such as institutional ownership, insider ownership, and executive compensation affects their approach to CPS. This research aims to shed light for future research in understanding of corporate governance mechanisms and political strategy.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.