Abstract

This study examines the effects of corporate governance mechanisms on climate change disclosure in Bangladeshi-listed banks. The corporate governance mechanisms used in the study were board size, board meetings, board independence, audit committee size, audit committee independence and audit committee meetings. A climate change disclosure index (CCDI) was developed to assess the sample banks’ climate change disclosures. From 2013 to 2018, data on climate change disclosures and corporate governance mechanisms were collected from the annual reports of all 30 listed banks. Employing a feasible GLS (FGLS) model for panel data, the findings demonstrated that increasing audit committee meetings, independent directors on the board and audit committee size positively and significantly increased climate change disclosures of listed banks in Bangladesh. Unlike prior climate change research on listed banks in Bangladesh, this study has included the audit committee attributes and the sponsor-directors’ ownership as determinants of climate change disclosures. This research offered a novel viewpoint on the significant positive impact of sponsor-directors’ ownership on climate change information disclosure. These findings have practical implications for governments, regulatory authorities, investors, green groups and other organisations working on climate change issues in the country.

Introduction

Nowadays, the biggest threat to businesses is climate change (CNN, 2020; Intergovernmental Panel on Climate Change [IPCC], 2014), regardless of whether they are in developed or developing countries. This harms people’s livelihoods, society, culture and health throughout the world (Meng et al., 2014). It threatens world economic progress, durable growth and the eradication of poverty (IPCC, 2013). According to Kintisch (2009), emissions are skyrocketing, sea-level rise forecasts are greater than projected and climate consequences are becoming more common throughout the world. The United Nations Framework Convention on Climate Change (UNFCCC, 2014) forecasted a lack of water and food and higher health risks for thousands of people in developing nations.

Bangladesh is a developing country. Climate change has a more significant impact on the business environment in Bangladesh than in other developing countries due to its geographical location and an increasing population that causes deforestation and intensive agricultural activities. Global factors, such as the massive industrialisation of developed countries that give rise to carbon emissions, are also partly to blame. Climate change has increased the severity of extreme weather events, threatening the agriculture sector, which employs 45% of the workforce (Gogoi & Kakakhel, 2014). Moreover, Bangladesh attained the ninth position among the most affected countries in the world based on the adverse outcomes of climate change, such as death toll, absolute loss of purchasing power parities and loss of per unit GDP (Eckstein et al., 2019). The country has been experiencing numerous severe climatic events, such as floods, riverbank erosion, salinity intrusion, cyclonic storm surges, droughts and waterlogging, which cause massive loss of life and economic assets. Consequently, it damages infrastructures and adversely impacts the lives and livelihoods (e.g., shortage of food, edible water, energy and health security) of people in different parts of the country, particularly destitute people in the coastal region (Abedin et al., 2019; Adnan et al., 2020; Hoque et al., 2019). These shreds of evidence reveal that Bangladesh is one of the world’s most vulnerable countries as a result of climate change.

Environmental damage and climate-related risks have a considerable impact on the stability of financial institutions, notably banks and insurance firms (Dikau & Volz, 2019). Banks’ business models are adversely affected due to the greater variability of climate change resulting from drought to an increasingly warmer climate (Flood, 2017; Weber & Kholodova, 2017). While banks do not directly contribute to the massive pollution and increased carbon emissions that cause climate change, they do fund the industries that are mainly responsible for the environmental damage (Boston Common Asset Management, 2015). Several large industries, for example, power, steel, textiles, paper, chemicals, cement, fertilisers and other industries, rely on banks for funding (Adeleke & Naim, 2017). These industries’ production and economic activities indirectly pollute the environment (Bangladesh Bank, 2011). Thus, these businesses are massively responsible for creating polluted wastewater, causing environmental damage, raising emissions and severely affecting climate change (Sharmin, 2016).

This study focuses on the impact of corporate governance mechanisms on climate change disclosures in the banking sector in Bangladesh for several reasons. First, Bangladesh Bank, the country’s central bank, recognises the negative environmental impact on the financial sector and the economy as a whole (Rahman, 2013). Consequently, it introduced the ‘Environment Risk Management Guidelines (ERM)’ and ‘Green Banking Guidelines’ in 2011 in order to protect banks and financial institutions from the undesirable outcomes of climate change and environmental degradation (Bangladesh Bank, 2011). Second, stakeholders, particularly shareholders and depositors, seek to safeguard their investments from the negative impact of climate change. For example, shareholders understand the adverse effect of climate change on banks’ share values and sustainability at large (Clark, 2017). They want to know how banks deal with environmental and social activities that significantly contribute to climate change. Therefore, disclosures of climate change-related information may meet the expectations of key stakeholders. Corporate governance structures influence climate change disclosures. That is, truly effective corporate governance structures and implementations are inevitable to address the current climate change issues and disclosures (Masud et al., 2018). For example, the corporate board, responsible for developing long-term business plans and overseeing the use of the company’s assets (Khan et al., 2019; Muttakin & Subramaniam, 2015), makes critical decisions on climate change disclosures. Weak corporate governance structures of banks do not ensure the disclosure of climate change information, causing investors to lose faith in banks.

Numerous studies (e.g., Amran et al., 2014; Ben-Amar & McIlkenny, 2015; Ben-Amar et al., 2017; Charumathi & Rahman, 2019; Giannarakis et al., 2018; Haque & Deegan, 2010; Omar & Amran, 2017; Ooi et al., 2019; Sullivan & Gouldson, 2017) have examined the effectiveness of corporate governance mechanisms in disclosing climate change-related information across developed and developing countries. These studies provide evidence that the governance structures of banks influence the level of climate change-related information disclosures. However, the findings may not be relevant to the banking sector in Bangladesh since the corporate governance structures, banking laws and bank management systems of Bangladeshi banks differ significantly from those of other developed and developing economies.

Despite being an important sector, researchers paid less attention to investigating the relationship between corporate governance structures and disclosures of climate change-related information in the banking sector in Bangladesh. There have been several studies conducted in this area. For example, Nurunnabi (2016) examined climate change reporting practices in Bangladesh and the market response to and corporate accountability for climate change, using a sample of 71 publicly traded firms from 2010 to 2011, of which only 8 were commercial banks. Belal et al. (2010) examined the nature of and revealed the extent of corporate environmental and climate change disclosures in Bangladesh for the year 2008. Similarly, Masuma et al. (2019) showed disclosure levels practiced by the Bangladeshi-listed 82 companies for the year 2016. These studies performed univariate analysis to determine the level of climate change disclosures. Therefore, it is still less evident from prior studies how corporate governance frameworks impact climate change disclosures in Bangladeshi-listed banks following the first implementation of ERM and Green Banking Guidelines provided by the country’s central bank. This demonstrates the gap in the literature on corporate governance and climate change disclosures in the Bangladeshi banking sector. So far, research on corporate governance and its influence on climate change disclosures has offered specific suggestions for developed economies, but the issue is whether the corporate governance structures of Bangladeshi firms have any effect on them. To the best of our knowledge, no study on the impact of corporate governance on disclosures of climate change in listed banks in Bangladesh is available. This study thus intends to examine the impact of corporate governance mechanisms on the disclosure level of climate change information in listed banks in Bangladesh.

Literature Review and Hypotheses Development

Several theories (e.g., agency, stakeholder, legitimacy and resource dependency theories) emphasise responsibility and maintaining a relationship between banks and their stakeholders through social information disclosures. Relevant prior studies were also reviewed to develop hypotheses for the study.

Board Size and Climate Change Disclosures

A corporate board is a top management body that is responsible for creating firms’ strategic plans, overseeing the effective use of firms’ assets (Jizi et al., 2014) and confirming that other major concerns are adequately managed and reported, for example, major environmental hazards (Ben-Amar et al., 2017). The inclusion of more members on a board may increase the board’s ability to oversee and contribute to creating value-adding activities (Akhtaruddin et al., 2009). A large board of directors may also assist management in other ways. For example, it makes it easier to gain access to specific talents, experiences and resources (Katmon et al., 2019). As a result, a large board provides better advice to management on various critical issues, including pollution, biodiversity and carbon emissions (Katmon et al., 2019; Masud et al., 2018). According to Chang et al. (2017), firms with large boards may be more willing to share social and environmental information in this circumstance, lowering business risks and uncertainties. Moreover, a larger board allows for more diverse decision-making and enhances monitoring authority, pushing businesses to engage in more active environmental sustainability reporting (Masud et al., 2018). This view is supported by Jahid et al. (2020), who discovered a favourable association between board size and corporate social responsibility disclosures of publicly traded banks in Bangladesh. However, Kılıç and Kuzey (2019) documented that board size had no impact on the carbon emission disclosures of Turkish nonfinancial firms. Similarly, Ahmad et al. (2017) also revealed that board size had no effect on corporate social responsibility disclosures of firms listed on the Bursa Market in Malaysia. They argued that the number of board members had little impact on developing voluntary disclosure rules for carbon emissions.

According to Ntim et al. (2013) and De Villiers et al. (2011), a large board minimises agency conflicts because more members may collaborate to represent the interests of many stakeholders. It also reduces the information asymmetry problem (Masud et al., 2018). This hypothetical relationship is supported by the empirical studies of Zaid et al. (2019), who revealed a positive impact of board size on information dissemination. They argued that bigger boards met stakeholders’ expectations of greater transparency and disclosure. Furthermore, having a larger board size assures more variety and resources (Katmon et al., 2019) to conform to social customs, demands and beliefs, thus enhancing firms’ legitimacy (Ntim et al., 2013). Masud et al. (2018) argue that legitimacy demonstrates that a larger board size benefits society and the company by promoting greater disclosures related to environmental plans and activities. Similarly, and consistent with resource dependency theory, Masud et al. (2018) contended that a larger board resulted in better environmental sustainability reporting. Based on the above discussion and empirical results, we hypothesise that:

Board Meeting and Climate Change Disclosures

According to agency theory, the frequency of board meetings represents the time capacity of the board; hence, the number of meetings reflects the amount of board activity (Hu & Loh, 2018). A sufficient number of board meetings is required for directors to make successful decisions. This is because more audit committee meetings require significant time and effort to make strategic decisions. Moreover, directors review sustainable reports and stakeholder engagement plans, among other things, at board meetings (Herremans et al., 2016). They argued that directors could effectively monitor demands and fulfil stakeholders’ requirements if there was greater involvement through board meetings. In line with the agency theory, Ahmad et al. (2017) argued that directors who attend board meetings more regularly are more likely to involve themselves for the benefit of stakeholders. According to Giannarakis (2014), the numerous board meetings allow directors to discuss and focus more on social-related matters. Consequently, all disclosures, including climate change, remain under surveillance regularly, thus ensuring climate change disclosures. In a study, Nguyen et al. (2021) provided evidence of a significant positive impact of board meetings on environmental performance and the sustainability of severely polluting industries in China. Similarly, Hu and Loh (2018), Aliyu (2018) and Agyemang et al. (2020) revealed a similar relationship between board meetings and environmental disclosures of Chinese, Nigerian and Singapore listed companies, respectively. The underlying reason is that a high frequency of board meetings improves the board’s capacity to analyse reports necessary to resolve agency problems and improve disclosure quality (Knechel et al., 2007). Chou et al. (2013) support the argument that increased board oversight and accountability reduce agency costs and information asymmetries, resulting in better disclosure quality. Thus, a board with increased meeting frequency enables the top executives to perform better business operations on climate change issues to satisfy the stakeholders in the competitive business world. The above discussion leads us to the following hypothesis:

Board Independence and Climate Change Disclosures

Board independence, defined as the percentage of independent directors to the total number of directors, plays a critical role in reducing agency problems between management and shareholders (Akhtaruddin et al., 2009). A larger number of independent directors on a board enables decentralisation of authority and responsibility and serves as a mediator between management and other stakeholders, decreasing agency conflicts (Masud et al., 2018). The presence of more independent directors on the board minimises the legitimacy gap between the company and society since they work for the firm’s stakeholders (Ntim et al., 2013). Resource dependence theory suggests that independent directors frequently provide corporations with critical skills, abilities, experience and knowledge that can aid firms in managing their external dependencies through developing stronger business relationships with key stakeholders (Mallin & Michelon, 2011). Additionally, according to stakeholder theory, a greater variety in skills, expertise, knowledge and stakeholder engagement, all of which are commonly associated with independent boards, can aid in resolving the competing interests of diverse groups of stakeholders by maintaining a balance between firms’ financial and operational goals.

Independent directors are more knowledgeable, informative, educative and experienced regarding climate change issues (Hafsi & Turgut, 2013). They improve firms’ climate change-related activities and carbon emission reports in the long run since they are believed to be immensely effective in overseeing management in terms of creating long-term value and maintaining a high level of openness (Jizi et al., 2014). Moreover, they extend sensitivity to social needs by discouraging a concentration on short-term benefits (Yunus et al., 2016). Many prior studies (e.g., Agyemang et al., 2020; Ahmad et al., 2017; Aliyu, 2018; Hu & Loh, 2018; Khan et al., 2020; Kılıç & Kuzey, 2019; Masud et al., 2018; Ofoegbu et al., 2018) found a positive effect of board independence on environmental reporting/disclosures, supporting theoretical premises. They contended that shareholders and management do not place as much pressure on independent directors as on internal directors (Hussain et al., 2018). As a result, independent directors push a company to promote a greater level of transparency and openness (Amran et al., 2014). Also, independent directors would persuade non-independent directors to give more information about the firm to stakeholders of their own will (Aliyu, 2018). Therefore, we developed the following hypothesis:

Audit Committee Attributes and Climate Change Disclosures

Audit committee attributes such as the size, independence and frequency of meetings of the audit committee, among other things, are three key corporate governance instruments. The audit committee’s attributes are intended to increase control and monitoring of management decisions as well as to report various types of information required by stakeholders (Fama & Jensen, 1983). For example, a large audit committee provides the necessary strength and diversity of skills to ensure proper oversight leads to corporate social responsibility disclosures (Buallay & Al-Ajmi, 2019; Khan et al., 2019). Consistent with the resource dependency theory, a large audit committee brings knowledge, diversified skills, wider experience and intellect to the board (Mollah et al., 2012). It is argued that using these qualities of a large audit committee and a high frequency of audit committee meetings can ensure good governance (Akter et al., 2021). Good governance of a firm reduces asymmetric information problems by disclosing information related to stakeholders’ interests, including climate change information. Habbash (2016) supported this argument and provided evidence of a significant positive association between audit committee effectiveness and environmental disclosures. Based on the theoretical and empirical literature, our study finally argues that major audit committees may contribute to a higher level of climate change disclosure among Bangladeshi-listed banks. Therefore, an attempt was made here to determine if audit committee size is associated with climate change disclosures by Bangladeshi-listed banks and we developed the following hypothesis:

As for the frequency of audit committee meetings, the Bangladesh Securities and Exchange Commission (BSEC) (2012) recommended that the Bangladeshi corporate sector hold at least four meetings in a financial year. According to Allegrini and Greco (2013), having at least four audit committee meetings in a financial year significantly affects the degree of voluntary disclosure. The higher number of audit committee meetings requires substantial time and energy to perform audit committee activities (Magembe et al., 2017). The frequent holding of audit committee meetings enhances the exchange of relevant information among directors, which significantly encourages increased monitoring and supervision of firms’ activities and improves reporting (Karamanou & Vafeas, 2005). Bryan et al. (2004) and Soliman and Ragab (2014) also argued that the audit committee’s activities, as measured by the frequency of meetings, increase the quality and quantity of disclosure. Similarly, Musallam (2018) and Appuhami and Tashakor (2017) provided evidence of a significant positive impact of the audit committee meetings on CSR disclosures. Therefore, we developed the following hypothesis regarding the relationship between the frequency of audit committee meetings and climate change disclosures:

Another attribute of an audit committee is its independence. According to the BSEC (2012), an independent audit committee refers to an audit committee consisting of non-executive directors, of whom at least one shall be an independent director of the company, except the chairman of the board. An independent audit committee facilitates the timely release of unprejudiced accounting information to key stakeholders, leading to reduced agency costs and information asymmetries (Ernstberger & Grüning, 2013; Heenetigala & Armstrong, 2011; Ntim, 2016). Consequently, firms tend to disclose accurate and adequate climate change information. Pomeroy and Thornton (2008) supported this view by documenting the positive impact of audit committee independence on financial reporting quality in emerging economies. Al-Rashid (2010) also revealed a significant positive effect of audit committee independence on corporate social reporting disclosures of banks in the GCC region. Therefore, we developed the following hypothesis regarding the independence of an audit committee and climate change disclosures:

Research Methodology

Sample Selection and Sources of Data

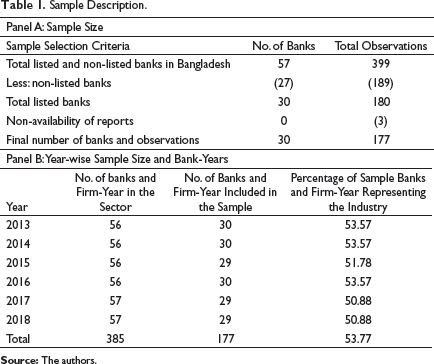

As of 31 December 2018, the banking sector in Bangladesh consisted of 57 banks, 30 of which were listed on the Dhaka Stock Exchange (DSE) (Table 1). We excluded non-listed banks from the sample because they were thought to be less regulated and accountable and thus provided less quality information. Therefore, the sample comprised 30 banks that were continuously listed between 2013 and 2018, and it included 177 firm-year observations in total after excluding three firm-year observations due to data unavailability (Table 1).

Sample Description.

We collected data on climate change and corporate governance from the annual reports, which were available on the websites of all sample banks. This is because Bangladeshi banks usually publish their yearly environmental policies, plans and actions in annual reports. We also collected or computed various financial (e.g., firm size, return on assets and leverage) and nonfinancial data (e.g., firm age, Big 4 audit firm, sponsor-directors’ ownership and institutional ownership) from the sample banks’ annual reports.

Variable Description and Measurement

Dependent Variables

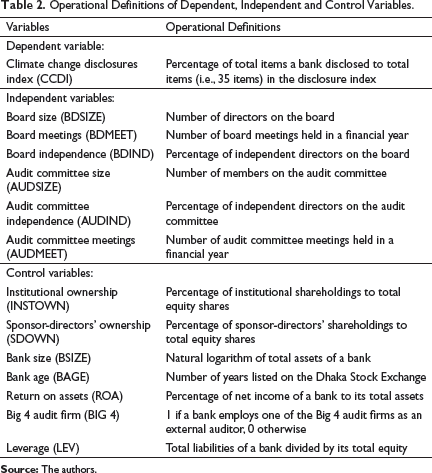

The degree of climate change disclosures is the dependent variable of the study. Following the studies of Masuma et al. (2019) and Dey et al. (2017), we developed a climate change disclosure index (CCDI) that measured the degree of climate change disclosure of the sample banks. A non-weighted binary index was developed to examine the narrative sections of the annual green banking report, corporate social responsibility report, sustainability report, directors’ report and chairman or director’s statement of each bank. If a sample bank disclosed an item selected for the study at least once, we assigned it a 1, and 0 otherwise. We selected 35 items to develop a score of CCDI for the sample banks. Consistent with the studies of Nurunnabi (2016), Kılıç and Kuzey (2019) and Masuma et al. (2019), the CCDI score was derived by dividing the climate change disclosure items disclosed by the maximum number of items that a bank might disclose. The CCDI score was calculated as:

where ci = 0 or 1, as follows:

ci = 0 if the disclosure item was not reported;

ci = 1 if the disclosure item was reported; and

t = the maximum number of climate change disclosure items a bank could disclose (i.e., 35 items).

Independent Variables

The corporate governance mechanisms, which included six different mechanisms, were the independent variables of the study. They were board size, board meetings, board independence, audit committee size, audit committee independence and audit committee meetings. Board size indicates the total number of directors on the board. The number of board meetings held each financial year is referred to as the board meetings. Board independence is meant to represent the total number of independent directors on the board. The audit committee size is referred to as the total number of members on the audit committee. Audit committee independence is meant to represent the total number of independent directors on the audit committee. Audit committee meetings refer to the number of meetings held each financial year.

Control Variables

We controlled the effect of some variables, such as institutional ownership, sponsor-directors’ ownership, bank size, bank age, return on assets, Big 4 audit firms and leverage. Following the prior studies, we predicted that these variables could impact banks’ climate change disclosures. Management is heavily influenced by institutional ownership in disclosing more information in order to please stakeholders. Institutional investors, for example, are important stakeholders that push for more corporate responsibility in terms of financial aspects as well as disclosure practices for social, environmental, community and climate change activities (Rupley et al., 2012). In our sample banks, sponsor-directors held roughly 37% of the shares on average, giving them power on the board to make strategic decisions and incentivising them to disclose more information. They play an essential role in managing, controlling, operating and disclosing environmental-related information for banks (Uddin & Choudhury, 2008). Large banks may experience greater pressure to disclose information regarding social, environmental, sustainability, carbon emissions and climate change as a result of increased exposure and public scrutiny (Ashfaq & Rui, 2019; Yunus et al., 2016). Thus, we predicted a positive relationship between bank size and climate change disclosures.

Older banks (e.g., AB Bank, City Bank, Islami Bank Bangladesh Limited (IBBL), IFIC Bank, National Bank, Pubali Bank, Rupali Bank, United Commercial Bank and Uttara Bank) are believed to have enough resources and experience to create synergy for disclosing climate change-related information. They are also expected to have extensive stakeholder networks. They, therefore, disclose various pleasant information (e.g., social, environmental and climate change-related disclosures) to preserve the relationship with their stakeholders (Alsaeed, 2006; Kang & Gray, 2011). Thus, we assumed a positive effect of bank age on climate change information. Better-performing banks, as measured by return on assets (ROA), would have greater resources to cover the expenses of collecting and reporting the information necessary for environmental disclosures (Choi et al., 2013). Furthermore, environmental disclosures may serve as a technique for establishing public confidence and legitimacy in relation to the method of profit generation (Chithambo & Tauringana, 2014). Therefore, we expected a positive correlation between ROA and climate change disclosures.

More transparency regarding social and environmental events may help to decrease potential conflicts between owners and creditors, as well as agency costs (Prado-Lorenzo et al., 2009). Banks are expected to offer voluntary disclosures to meet depositor expectations as they rely heavily on depositor funds (Rankin et al., 2011). Thus, we presumed a positive association between banks’ leverage and climate change disclosures. The Big 4 international audit firms (Big 4) have developed a set of metrics and disclosures for firms attempting to harmonise environmental, social and governance reporting internationally (Cohn, 2020). The Big 4 audit firms encourage their client companies to disclose relevant and significant environmental data (Iatridis, 2013). Prior research demonstrated that companies audited by one of the Big 4 audit firms are more likely to disclose social and environmental information than companies audited by non-Big 4 firms (Abba et al., 2018; Idowu & Çaliyurt, 2014; Welbeck et al., 2017). Therefore, we predicted a positive link between the Big 4 audit firms and climate change disclosures in listed banks in Bangladesh. Table 2 shows the operational definitions of dependent, independent and control variables.

Operational Definitions of Dependent, Independent and Control Variables.

Model Specification

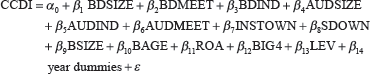

We used a panel data regression model to examine the effect of corporate governance mechanisms on climate change disclosure levels. Specifically, we employed the feasible GLS (FGLS) model to examine the effect of corporate governance mechanisms on climate change disclosure levels. This model was selected after performing the F-test (Baltagi, 1995), the Breusch and Pagan (1980) Lagrange Multiplier (B–P LM) test and the Hausman (1978) specification test. Therefore, the following regression model was employed for this study:

The above regression was run after the winsorisation of several variables. Several variables, namely, BDMEET, AUDIND, AUDMEET, BSIZE, INSTOWN and ROA, had outlier values. To reduce the influence of outliers, all of these variables were winsorised at 5% and 95%. Therefore, the top and bottom nine values of each variable affected by outliers were replaced by the 10th and 168th values, respectively.

Robustness Check

We checked the robustness of the main results by performing two more FGLS regressions with modified datasets. First, we ran a regression before the winsorisation of variables that had outliers. Second, after transforming several variables (e.g., BDMEET, AUDSIZE, AUDMEET, BSIZE, INSTWN and LEV) affected by the non-normality problem, another regression was conducted. Moreover, a number of diagnostic tests were also performed to check the goodness-of-fit model. The Pearson’s correlation test was performed to confirm the linearity of two independent variables; variance inflation factors (VIF) and tolerance (TOL) statistics tests were conducted to check for multicollinearity problems between independent variables. The modified Wald test (Greene, 2012) and the Wooldridge test (Wooldridge, 2002) were conducted to detect the existence of heteroscedasticity and autocorrelation problems.

Results

Descriptive Statistics

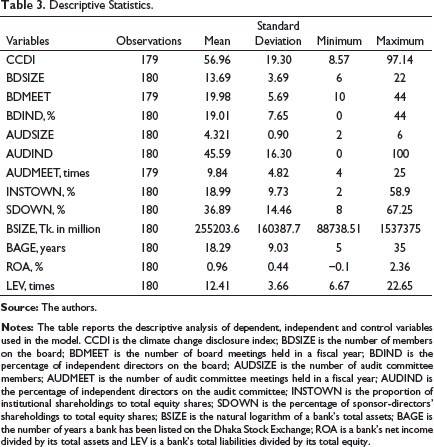

Table 3 presents the findings of the descriptive statistics. The CCDI had a mean of 56.97 and a standard deviation of 19.30, with a range of 8.57–97.14%. These results suggest that the average level of climate change-related information disclosures in the sample banks was good, with a significant variance. The average BDSIZE was 13.69, with a standard deviation of 3.69 and a range of 6–22, suggesting that board sizes varied greatly among the sample banks. The number of board meetings varied enormously across the sample banks, as the minimum BDMEET was 10 and the maximum was 44, with the average number of meetings held in the sample banks was 19.98 and a standard deviation of 5.69. BDIND had a mean of approximately 20% and a standard deviation of 7.65, with a range of 0–44%. These results suggest that non-independent directors predominated on the boards of the sample banks and that no independent directors served on the boards of some of the sample banks.

Descriptive Statistics.

The AUDSIZE mean was 4.32, with the lowest standard deviation (0.90), indicating that the audit committee size did not differ considerably across the sample banks. The mean and standard deviation of AUDIND were 45.59% and 16.31%, respectively, with a range of 0–100%. According to these figures, audit committee independence varied significantly, with some banks having 100% audit committee independence while others did not. Moving on to AUDMEET, it had a mean of 9.84, with a standard deviation of 4.82, revealing a significant variation in the number of audit committee meetings held among the sample banks.

In terms of control variables, institutional investors (INSTOWN) owned an average of 19% of the stock, with a standard deviation of 9.734. Sponsor-directors (SDOWN) had an average ownership influence of 36.89%. However, their ownership significantly varied among the sample banks, as the standard deviation of 14.46 indicated. The mean and standard deviation of bank size (BSIZE) were Tk. 255203.6 (million) and Tk. 160387.7, respectively. The average bank age (BAGE) was 18.29 years, with a standard deviation of 9.07. The sample banks’ average return on assets (ROA) was 0.96%, with a standard deviation of 0.44, indicating significant variation. The average leverage (LEV) was 12.41 times, with a standard deviation of 3.66.

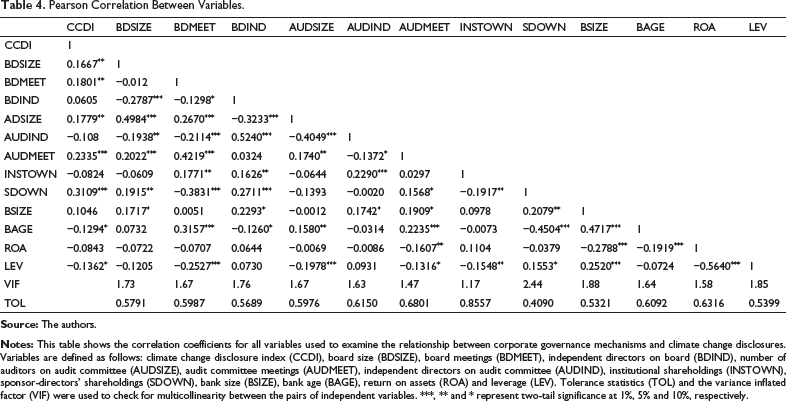

Pearson Correlation Matrix

Pearson Correlation Between Variables.

Regression Results

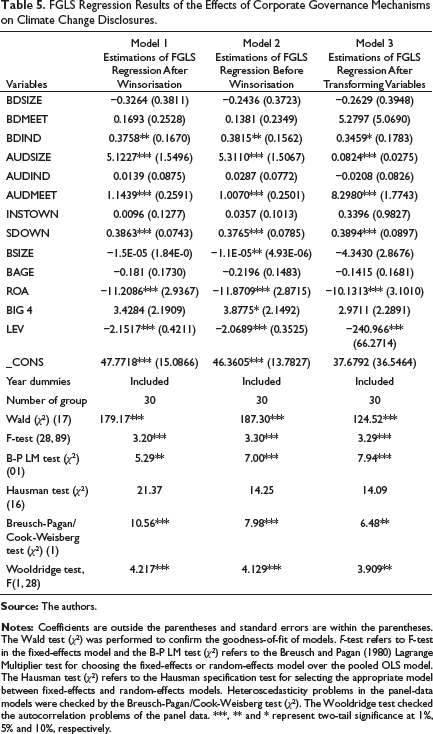

FGLS Regression Results of the Effects of Corporate Governance Mechanisms on Climate Change Disclosures.

Table 5 presents the FGLS regression results of the study. Model 1 estimates the effects of corporate governance mechanisms on climate change disclosures of Bangladeshi-listed banks using FGLS regression estimations on datasets after winsorisation. Model 2 and Model 3, respectively, estimate the effects of corporate governance mechanisms on climate change disclosures of the sample banks using FGLS regression estimations on datasets prior to winnowing and after transforming specific variables that had a nonmorality problem. These two regressions were run to test the robustness of the results of Model 1.

Model 1 shows that the regression weight of BDSIZE on CCDI is negative and statistically insignificant when all other variables are held constant. Models 2 and 3 likewise demonstrate the same result, supporting the robustness of the findings of Model 1. Therefore, all of these results reject H1. The result of testing hypothesis 2 presented in Model 1 shows that BDMEET has a positive regression weight on CCDI; however, it does not statistically significantly predict CCDI. Models 2 and 3 also confirm the robustness of the findings of Model 1. Therefore, all of these findings reject hypothesis H2. BDIND, as revealed in Model 1, provides evidence of statistically significant positive coefficients on CCDI at p < 0.05. The coefficient of 0.3758 indicates that a one-unit increase in board independence leads to a 0.3758-unit increase in CCDI. Also, Model 2 and Model 3 provide similar evidence at p < 0.05 and p < 0.10, respectively. Thus, all these results fail to reject H3.

Model 1 also reveals that the regression weight of AUDSIZE on CCDI is positive and statistically significant at p < 0.01, controlling the effect of other corporate governance variables in the model. The coefficient of 5.1227 indicates that for every one-unit increase in the audit committee size, CCDI increases by 5.1227 units. Models 2 and 3 also demonstrate a consistent result, confirming the robustness of the findings of Model 1. Therefore, the findings do not support the rejection of H4. AUDIND, as shown in Model 1, exhibits statistically insignificant positive coefficients on CCDI. Model 2 also documents the same result, confirming the robustness of the outcomes of Model 1. Model 3, however, finds that AUDIND has a statistically insignificant negative effect on CCDI. Therefore, all these outcomes reject H5. While the regression weight of AUDMEET on CCDI is positive and statistically significant at p < 0.01, as reported in Model 1. The coefficient of 1.1439 suggests that CCDI increases by 1.1439 units for every one-unit increase in audit committee meetings. Models 2 and 3 also demonstrate a similar relationship, confirming the robustness of the outcomes of Model 1. These results, therefore, support H6.

Moving on to the effect of control variables on CCDI, all models provide a statistically insignificant positive regression weight of INSTOWN on CCDI, while BAGE has a statistically insignificant negative regression coefficient on CCDI. Model 1 provides credible evidence that SDOWN has a statistically significant positive weight on CCDI at p < 0.01. The coefficient value suggests that a one-unit increase in sponsor-directors’ ownership would increase the climate change disclosure index by 0.3863. Model 2 and Model 3 also provide consistent results with Model 1, confirming the robustness of the findings. As evident in Model 1, ROA and LEV have statistically significant negative coefficients on CCDI at p < 0.01. The coefficients of −11.2086 and −2.1517 indicate that for every one-unit increase in ROA and LEV, CCDI decreases by −11.2086 and −2.1517 units, respectively. Model 2 and Model 3 both agree that the findings of Model 1 are sound. Finally, BSIZE and BIG 4, as shown in Model 1, demonstrate statistically insignificant coefficients on CCDI. Model 3 also supports similar results. However, Model 2 suggests that BSIZE has negatively and statistically significantly predicted CCDI, while BIG 4 has positively and statistically significantly predicted CCDI, contradicting the outcomes of Model 1.

Discussion

Three models were employed to investigate the effects of corporate governance mechanisms on climate change disclosures of Bangladeshi-listed banks. Model 1 is the base model of this study, while estimations of Model 2 and Model 3 confirm the robustness of Model 1. Therefore, we mainly depended on the results of Model 1 as the baseline for discussion.

Our study documented that independent directors had a significant positive impact on the climate change disclosures of listed banks in Bangladesh. This finding suggests that Bangladeshi-listed banks with more independent directors on their boards are more likely to respond positively to climate change disclosures. This result is consistent with those of Masud et al. (2018), Kılıç and Kuzey (2019), Agyemang et al. (2020), Ahmad et al. (2017), Aliyu (2018), Ofoegbu et al. (2018), Khan et al. (2020) and Hu and Loh (2018). As with Hussain et al. (2018) and Amran et al. (2014), the positive association can be explained by the fact that independent directors are not susceptible to the same level of pressure from stockholders and management as internal directors. As a result, they urged banks to promote a greater level of accountability toward climate change disclosures. The favourable relationship also supports the premise of the agency theory that the predominance of independent directors on a board reduces agency conflicts by ensuring a decentralisation of authority and duty, as well as serving as a mediator between management and other stakeholders. Consequently, independent directors may have motivated internal directors to disclose climate change information. This result also confirms the argument of the stakeholder and legitimacy theories that banks with more independent directors on their boards benefit society by inducing them to disclose more information about their environmental plans, policies and activities.

We revealed that the size of the audit committee had a positive impact on the disclosure of climate change information. This finding demonstrates that a larger audit committee of Bangladeshi-listed banks can motivate bank management to disclose climate change information. This finding is consistent with the arguments of Buallay and Al-Ajmi (2019) and Khan et al. (2019), who suggest that a bigger audit committee has adequate strength and diversity of knowledge to guarantee effective monitoring that leads to corporate social responsibility disclosures. Theoretically, the result also supports the arguments of the resource dependency theory that a large audit committee brings knowledge, diversified skills, wider experience and intellect to the boards. These qualities of a large audit committee ensure good governance that reduces asymmetric information problems by disclosing climate change information. We also found that audit committee meetings were positively associated with climate change disclosures. This finding implies that an increase in the number of audit committee meetings causes bank management for Bangladeshi-listed banks to report climate change information. This finding confirms the contention of Karamanou and Vafeas (2005) that a greater number of audit committee meetings promotes the exchange of relevant information among directors, which, in turn, encourages a greater level of monitoring and supervision of firms’ activities, thereby increasing the climate change reporting process.

Consistent with Kılıç and Kuzey (2019) and Ahmad et al. (2017), we revealed that the size of the board of directors had no effect on climate change disclosures by Bangladeshi-listed banks. The result indicates that the number of directors on a board plays an insignificant role in disclosing voluntary climate change information. This insignificant relationship between board size and climate change disclosures is contrary to the premise of both the legitimacy theory and the resource dependency theory. Similarly, the research results revealed that board meetings had no significant impact on climate change disclosures of listed banks in Bangladesh. This result suggests that the high frequency of board meetings has little effect on directors’ discussions and attention to stakeholders’ interests and societal issues. As a result, all disclosures, including climate change, are not consistently monitored, resulting in a failure to ensure climate change disclosures. This inference is inconsistent with the agency theory. This result is also inconsistent with those of Nguyen et al. (2021), Hu and Loh (2018), Aliyu (2018) and Agyemang et al. (2020). Furthermore, we found that the independence of the audit committee of listed banks in Bangladesh had no contribution to their climate change disclosures. This result contradicts the idea that an independent audit committee promotes the timely disclosure of fair accounting information to major stakeholders, thereby reducing agency costs and information asymmetry.

Among the control variables, the sponsor-directors’ ownership of listed banks in Bangladesh was shown to positively influence climate change disclosures, demonstrating that a large share of the sponsor-directors’ ownership encourages bank management to disclose climate change information enormously. This result has important implications, in that, in Bangladesh, the sponsor-directors own a large proportion of a bank’s equity shares, on average 36.89% revealed in this study, as founding members and thus have power and influence over the board (Hossain et al., 2020). Therefore, they forced bank management to proactively pursue climate change strategies and offer stakeholders more climate-related information. This conclusion is surprising because most enterprises in Bangladesh, including banks, are family-owned and the sponsor-directors of these firms often prioritise their profit maximisation over wealth maximisation for all stakeholders, owing to their self-motivation and lack of diversification. Nonetheless, they encourage bank management to adopt climate change plans and report climate-related information.

Contrary to expectations, the return on assets and leverage of listed banks in Bangladesh were found to have a negative impact on climate change disclosures. The result related to the return on assets suggests that banks with high performance are reluctant to disclose climate change information. A possible explanation is that banks that are financially performing well are unaware of stakeholder pressures. This negative attitude contradicts the resource dependency and stakeholder theories in the sense that resourceful banks are not motivated to reveal climate-related information since they are less likely to act in the best interests of stakeholders. This attitude might be detrimental to banks’ future reputations among pressure groups and regulatory authorities. The negative relationship between leverage and climate change disclosures is also surprising. This is because banks with higher leverage indicate that they have a high volume of core deposits. However, the result suggests that they are reluctant to provide climate change disclosures to depositors, who are one of the key stakeholders. Finally, institutional ownership, bank size, bank age and the Big 4 audit firms do not contribute to disclosing climate change information.

Conclusion

Bangladesh is one of the world’s most susceptible and severely impacted countries as a result of global climate change. At present, researchers, governments, lawmakers, businesses and civil society are paying more attention to the climate change issue. An empirical research gap exists regarding the effects of corporate governance mechanisms on climate change disclosures in listed Bangladeshi banks. Therefore, in this study, we aim to look into the impact of corporate governance mechanisms on climate change disclosures of listed banks in Bangladesh.

The findings demonstrate that increasing audit committee meetings, a higher proportion of independent directors on the board and the audit committee size positively and significantly influence the disclosures of climate change information of listed banks in Bangladesh. However, board size, frequency of board meetings and audit committee independence are not regarded as contributory corporate governance mechanisms to climate change disclosures.

The findings of this study add to the body of knowledge about the relationship between corporate governance mechanisms and climate change disclosures. Governments, regulatory bodies, investors, green groups and other bodies working on climate change problems may put pressure on banks to reveal more information in order to reap the benefits of climate change data. The audit committee attributes have been employed in very few studies as a factor in climate change information disclosures when it comes to board characteristics. Therefore, our study adds to the current literature by demonstrating a favourable relationship between audit committee meeting frequency and climate change information disclosures. Prior climate change research has seldom included the ownership of sponsor-directors as a consideration in determining whether or not to disclose climate change-related information, and this is particularly true in Bangladesh. However, our study provided a unique perspective on the positive and significant influence of sponsor-directors’ ownership on climate change information disclosure, which adds to the existing body of knowledge.

However, there are a few limitations to the study that might lead to further research in the future. First, we collected data from the published annual reports of listed banks. We did not consider other media of communication channels such as websites, newspapers and so on. Second, we focused only on the banking sector. Therefore, it creates a new avenue for other researchers to conduct similar research in different industries in the country.

Footnotes

Declaration of Conflict of Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.