Abstract

Central Asia is becoming an increasingly attractive destination for foreign direct investment (FDI). Although a first wave of foreign investments targeted Central and Eastern Europe in the early 1990s, followed by a second one to South-east Europe in the early 2000s, FDI is now moving even further eastward towards Central Asia. The Central Asian countries are all relatively small landlocked economies and need to promote trade and investment which enable them to closely integrate into the international economic order to achieve sustainable economic development. The level of intra-regional trade in Central Asia is low and their trade is concentrated in few commodities and hence the possibilities of setting up joint ventures emerges so that instead of exporting and importing the same product, one country may decide to set up a joint venture in the partner country (with a more favourable investment climate and cost advantage) to buy back the same in the home country. The track record of FDI in Central Asia demonstrates the urgent need to strengthen good governance, transparency, stability and the fair application of the rule of law in the region. Therefore, this article seeks to examine the prospects and challenges of regional investment cooperation and provide some of the measures to enhance the effectiveness of bilateral investment treaties and double tax avoidance treaties among the Central Asian countries.

Keywords

Introduction

Almost two decades after the break-up of the former Soviet Union (FSU), Central Asian Republics (CARs), namely, Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan and Turkmenistan are still struggling to find suitable arrangements for regional cooperation mechanisms among themselves. CARs were the poorest part of the FSU and poverty has increased sharply during the transition period as a result of the output contraction and increased inequality in the distribution of income. Rural populations, especially in the more remote parts of the region, have traditionally been the poorest. Poverty, together with artificially drawn borders, which cut across traditional transport routes and created a number of enclaves, 1 has led to social and economic tensions among the countries and peoples. The situation is particularly difficult in the densely populated Ferghana valley, shared by Uzbekistan, Tajikistan and the Kyrgyz Republic. If poverty and trade barriers are not addressed, the area may well become a breeding ground for future civil and social unrest, despite the fact that the CARs have emerged as one of the world’s fastest-growing regions since the late 1990s and have shown immense development potential.

There are a number of reasons, which seem to serve as the basis for investment cooperation in Central Asia. These include shared historical, cultural and religious and institutional factors. All the states had economies specialised to the production of primary commodities, before their withdrawal from the Soviet system of trade and commerce. It is also important to note that these countries have had important similarities as well as differences among themselves. The states were quite different in terms of their national resource endowments, connections to the foreign markets and government strategies.

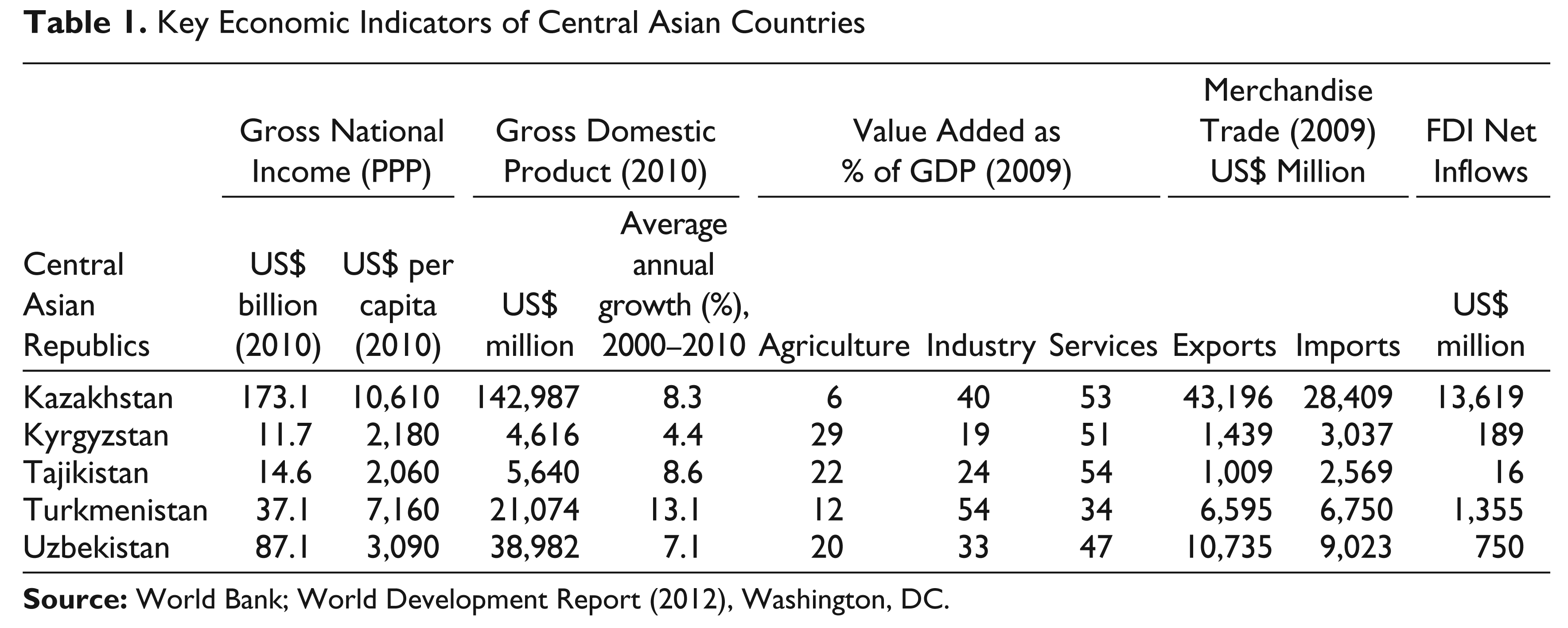

For instance, agriculture contributes a large proportion of employment in all the CARs but makes a strikingly different contribution to the overall gross domestic product (GDP). In the case of Kyrgyzstan, the contribution of agriculture in the country’s GDP was higher (29.50 per cent) followed by Tajikistan with 22 per cent, Uzbekistan (20 per cent), Turkmenistan (12 per cent) and Kazakhstan (6 per cent) in 2009. The contribution of the services sector is dominating with more than 50 per cent of GDP in Kazakhstan, Kyrgyzstan and Tajikistan, while the industry sector is dominating in Turkmenistan (54 per cent) and Kazakhstan (40 per cent) in their GDP. Among the five CARs, Kazakhstan is dominating in all the economic indicators, that is, gross national income at PPP, GDP, merchandise trade and FDI net inflows in 2009–2010 (see Table 1).

Key Economic Indicators of Central Asian Countries

Central Asian countries are all relatively small economies and land-locked (or even double land-locked) and therefore, they need to promote and facilitate investment and closely integrate into the international economic system to achieve sustainable economic development. Most prominent advantage of the region lies in their high-priced commodities (such as oil, gas, uranium, gold and cotton), infrastructure, abundance of skilled human capital and the legacies of Soviet rule. A location between Asia and Europe is an added geostrategic advantage. An important step towards the development of global markets is closer regional cooperation, especially with regard to the enhancement of regional and bilateral trade and investment flows.

With this background, this article seeks to examine prospects and challenges of regional investment cooperation in the five CARs to assess the reasons why their regional cooperation would be desirable in the future. This article is organised under the following six major sections besides introduction. The first section outlines new waves of FDI in Central Asia. The second section examines the recent pattern of FDI inflows and outflows in the Central Asian region. The third section examines the regional and bilateral FDI in Central Asia. The fourth section identifies the barriers in attracting FDI from the world and within the region. The fifth section examines the measures to enhance the effectiveness of Bilateral Investment Treaties (BITs) and Double Tax Avoidance Treaties (DTTs) among the CARs. Finally, the last section provides a few concluding remarks aimed at taking regional investment cooperation process forward in a faster manner to maximise the mutual benefits to the CARs in coming future.

New Wave of FDI in Central Asia

In terms of area, Kazakhstan ranks first, dominating with huge area of 2.71 million sq. km, while in terms of population, Uzbekistan ranks at the top (27.8 million) followed by Kazakhstan (15.9 million); the lowest in the region is the Kyrgyz Republic with 5.2 million. All Central Asian countries are landlocked while Uzbekistan is double landlocked. 2

These countries are inter-linked with land borders and are also connected with China, Iran, Afghanistan and Russia. Kazakhstan has land borders with three Central Asian Republics, namely, Kyrgyzstan, Turkmenistan and Uzbekistan; Kyrgyzstan has borders with Kazakhstan, Tajikistan and Uzbekistan; Tajikistan has borders with Kyrgyzstan, Uzbekistan and Afghanistan; Turkmenistan has borders with Kazakhstan and Uzbekistan. Uzbekistan has borders with all the other four countries of the region, namely, Kazakhstan, Kyrgyzstan, Tajikistan and Turkmenistan. Remoteness and isolation from major markets is the major bottleneck for trade integration with the world. In many cases, the merchandise trade of landlocked countries must travel great physical distances before it can reach international trade routes and markets. This challenge is especially acute for the transitional Central Asian economies. The capital cities of Kazakhstan, Kyrgyzstan, Tajikistan and Uzbekistan are all more than 4,000 km from the nearest port. 3

The road toward economic development and integration has been a long one for the five Central Asian economies. The prospects of investment cooperation among the Central Asian countries are currently very limited; though more than a dozen multilateral agreements, organisations, communities, programmes and forums have been initiated, actual cooperation has been limited, and many signed documents are either not enforced or are contradicted by national legislation. Three of the CARs, namely, Uzbekistan, the Kyrgyz Republic and Tajikistan are low-income, while Kazakhstan and Turkmenistan are oil rich middle-income countries.

The landlocked geographic location of Central Asian countries requires greater regional cooperation to improve trade, investment and economic development. Central Asian economies have taken steps individually to liberalise their investment regimes to attract FDI. The liberalisation of FDI policy regimes in combination with macroeconomic stabilisation has led to an increase in FDI inflows in the Central Asian economies. The CARs had very similar trade policy regimes at the time of their independence, but these have diverged significantly since then. Today, trade policy regimes in the CARs vary widely from the very liberal in the Kyrgyz Republic, to fairly liberal in Kazakhstan and Tajikistan, to quite restrictive in Uzbekistan.

During the period between 1992 and 2010, three major features emerged in terms of direction and patterns of trade in Central Asia: (a) low level of intra-regional trade; (b) share of intra-regional trade in exports and imports are quite different; and (c) intra-regional imports and exports vary significantly across different countries. In the Central Asia region, low levels of trade flows are directly or indirectly associated with high trading transaction costs as the cost burden is largely caused by the landlocked geographical position and high administrational barriers.

The ability of a country to attract FDIs and invest outside its borders, that is, outward foreign direct investments (OFDI) have far-reaching implications for economic development (Kornecki and Rhoades 2007). The collapse of communism reshaped the global economic and political development in the twenty-first century (Kaynak, Yalcin and Tatoglu 2006). Following the fall of the Soviet Union, countries of the Central Asian region began the transformation towards a market economy. These countries have seen their economies stabilising and some have even seen considerable growth in their economies. They have privatised many state-owned enterprises, signed foreign trade agreements with other countries, and have generally achieved a significant level of macroeconomic stability with improved growth rates (Kutan and Vuksic 2007). These countries have attributed these positive trends to a significant increase in FDI.

Among the Central Asian region, this is quite true particularly in the case for the economy of Kazakhstan, which gained independence from the Soviet Union in 1991. In the case of Kazakhstan, one of the most striking new trends is that the country has been engaging in OFDI by actively investing outside its borders. According to the United Nation’s Conference on Trade and Development (UNCTAD 2008), Kazakhstan has emerged as the second-largest recipient of FDI in South-east Europe and Commonwealth of Independent States (CIS), after the Russian Federation. Similarly, Kazakhstan now ranks as one of the largest outward investors in the CIS in general and Central Asian region in particular. It is interesting to note here that the standards of policy reforms in terms of FDI policy are high, while the implementation of investment promotion activities and the facilitation services being provided to investors is less advanced. A coherent review process of the systems restricting FDI from foreigners would also help to further eliminate discriminative practices against foreign investors.

Improving investment policy frameworks and developing more targeted investment promotion capabilities is imperative to further attract FDI as these countries are over-dependent on natural resources. Although FDI inflows in the Central Asian region grew at 19 percentage points above the world average (CAGR) in the period 1998–2008 (UNCTADstat database), the region has attracted less per capita investments than neighbouring regions such as Eastern Europe and the South Caucasus, and investments are mainly concentrated in energy and energy-related sectors.

Most Central Asian economies are over-dependent on natural resources, and the region’s exports are heavily concentrated in a few primary products whose prices are determined in world markets. This commodity concentration makes the economies vulnerable to the volatility of oil prices and overly exposed to global commodity market developments in general. 4 Turkmenistan, Uzbekistan and Kazakhstan have adopted significant legislative changes since the fall of the former Soviet Union in an effort to attract foreign direct investment into their energy sectors. Of the three republics, Kazakhstan has been the most successful in attracting foreign interest, but all three republics face significant challenges in further development of oil and gas infrastructure.

The issue of diversifying sources of FDI remains a priority for many of the economies of the region. In Kazakhstan, for example, 70 per cent of all FDI inflows to the country in 2009 went to the energy extraction sectors and related geological services—approximately twice the ratio level of the mid-1990s (Republic of Kazakhstan 2010). Yet, the country has other high-potential sectors that could be developed to increase its wider competitiveness. In order to sustain competitiveness reforms and make progress, three mutually reinforcing pillars should be addressed: (a) sector-specific policy barriers; (b) developing human capital; and (c) supporting investment policy, promotion and innovation. The sector-specific approach could be of benefit to all the economies of Central Asia in increasing their competitiveness and laying the groundwork for sustainable growth. Now, the Central Asian countries must correct domestic distortions and continue institution-building in order to increase and diversify trade and investment in the region. A favourable domestic economic environment is crucial for stimulating investment (and attracting foreign investors) and for an effective economic response to good trade policies.

Foreign investors have an interest in improved regional integration, since this promotes more efficient production and offers greater opportunities for sales. Countries that do not receive large amounts of foreign investment because their markets are small or because they lack such natural resources as petroleum and natural gas which are attractive to investors, or because foreign investors have little confidence in their investment opportunities, have much to gain by becoming parts of regional markets. For this reason, transition economies, and above all the countries of Central Asia and the CIS, can attract more direct foreign investment on the basis of regional integration. Regional integration in Central Asia could enhance production efficiency on the basis of functional specialisation and economies of scale.

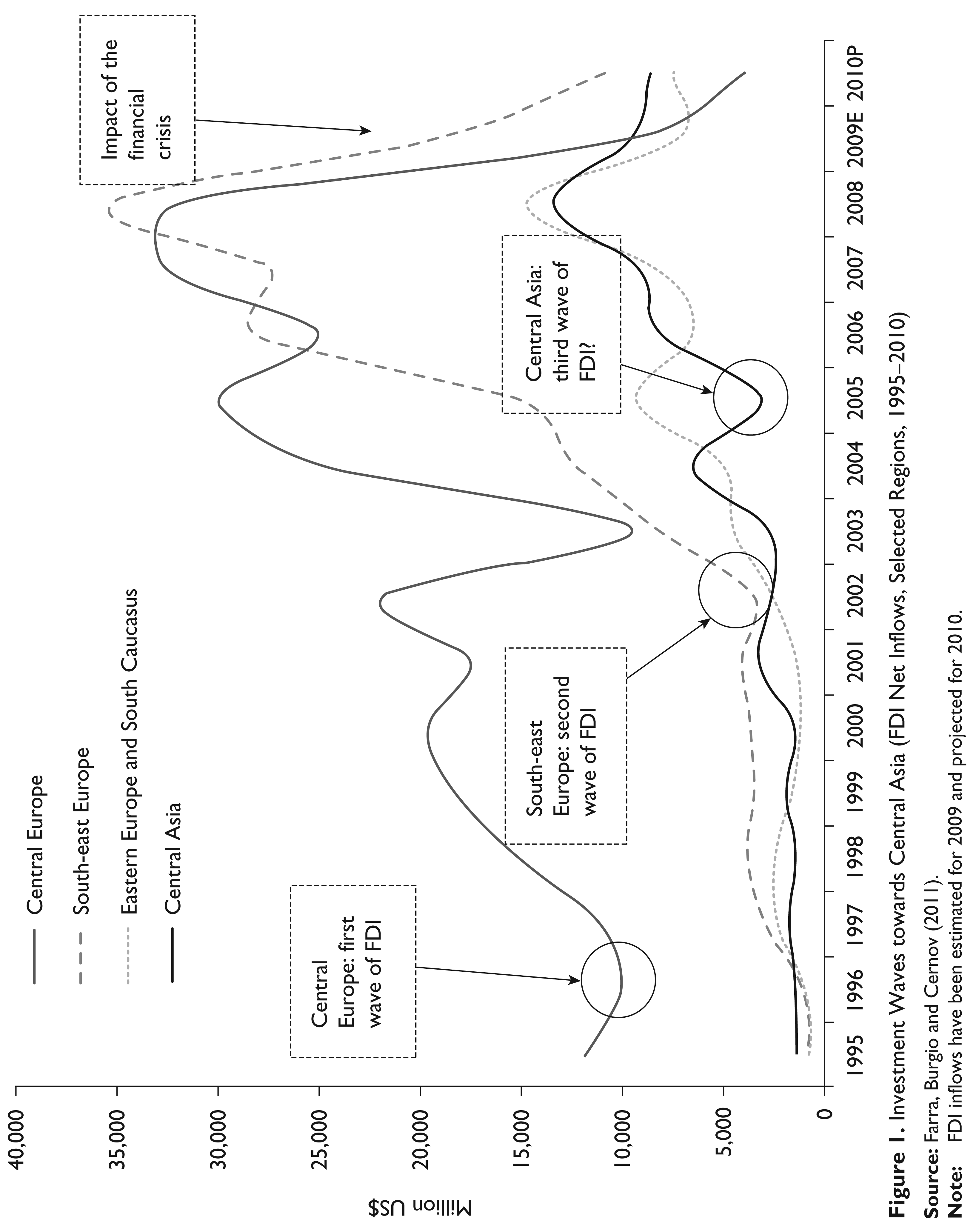

Central Asia is becoming an increasingly attractive destination for FDI. Although a first wave of foreign investments targeted Central and Eastern Europe in the early 1990s, followed by a second one to South East Europe in the early 2000s, FDI is now moving even further eastward towards Central Asia. From 2005 to 2009, FDI to the region increased from US$3 billion to around 19 billion. Despite the negative effects of the financial crisis, this upward trend is expected to continue (Farra, Burgio and Cernov 2011) and is presented in Figure 1.

According to the World Investment Report, 2011, Kazakhstan ranked 25th in inward FDI performance index, while Kyrgyzstan ranked 36th, Uzbekistan (74) and Tajikistan (117) in 2010. Central Asian countries have followed almost same trends in the ranking for inward FDI potential index. Kazakhstan ranked 54th in inward FDI potential index in 2010 followed by Kyrgyzstan (90), Uzbekistan (106) and Tajikistan (109), while ranking data for Turkmenistan is not available in this report. The ranking in terms of inward FDI potential index has declined significantly for Kazakhstan, Kyrgyzstan and Tajikistan in 2010 as compared to 1995 which indicates that these three countries are gradually becoming favourable destinations for foreign investors while reverse for Uzbekistan as their ranking increased marginally during the same period (see Table 2).

Inward FDI Performance and Potential Index Rankings of Central Asia, 1995–2010

FDIs are one of the driving forces of the process of globalisation and are a defining element of the modern-day world economy. FDIs promote the restructuring of industry at the regional and global levels and thus, ensure the integration of a national economy into the world economy more effectively than trade. FDIs stimulate economic growth and development, providing economies in transition with not only financing for development but also new technologies, better management techniques and access to international markets. In addition, FDIs integrate production systems with one another. In this way, FDIs can play a key role in the development of transition economies and in their rapid integration into the world community.

Pattern of FDI Inflows and Outflows

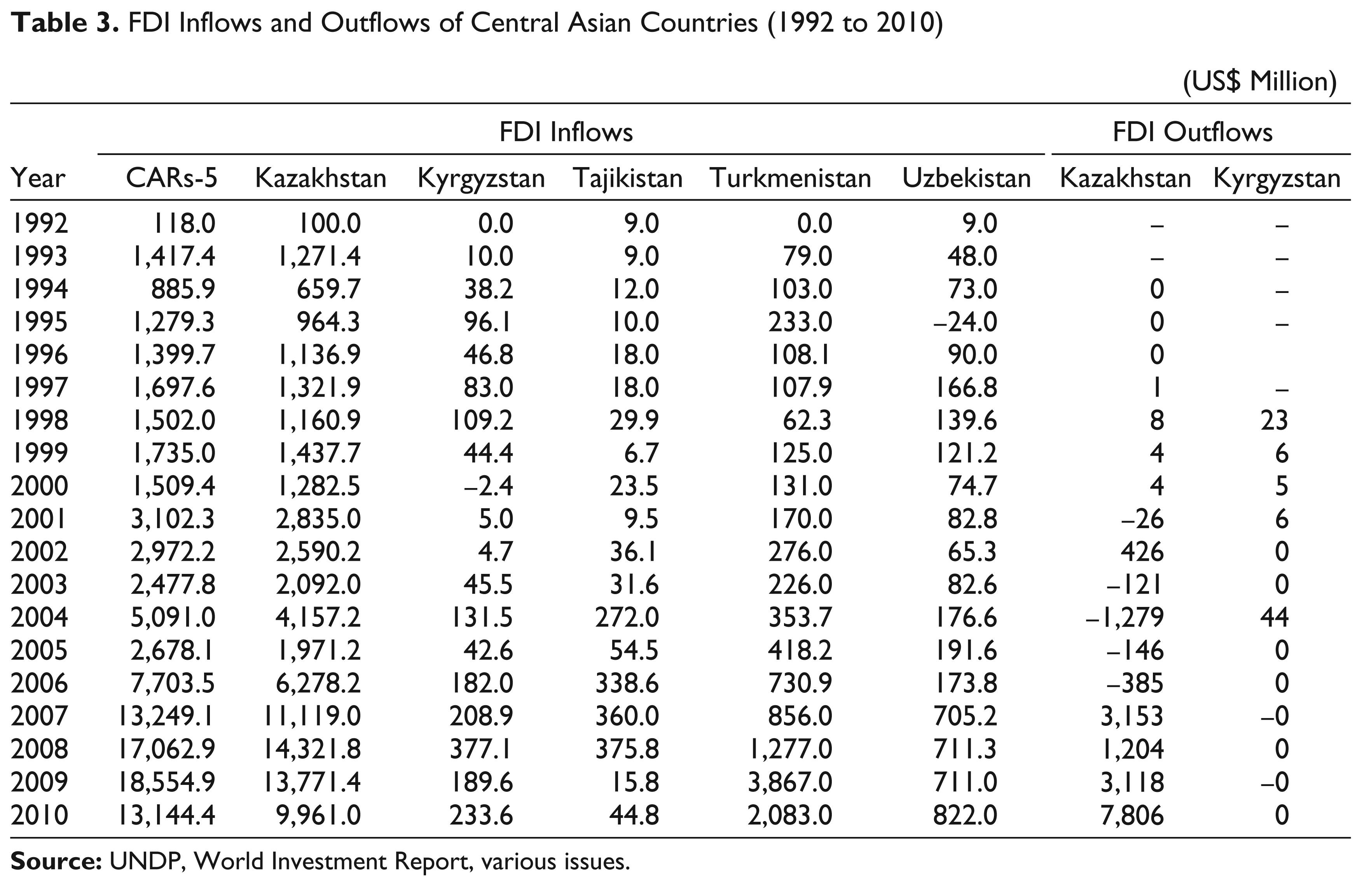

As can be seen from Table 3, the total FDI inflows in Central Asia region as a whole attracted US$118 million in 1992, but it increased significantly in the next year 1993 and reached US$1,417.4 million. Since then, the FDI flows in the region recorded fluctuating trends and increased significantly with highest ever US$18,555 million and provisional figure of 2010 recorded US$13,144.4 million. The inconsistency or fluctuations of the quantity of FDI flows reflect international investors’ lack of confidence in the Central Asian region’s market to ensure the rule of law, enforce contracts and maintain an economic system conducive to the transparent and fair conduct of free market commercial transactions. Among the Central Asian countries, Turkmenistan ranks top in the inward FDI stock with US$8,186 million followed by Kazakhstan (US$81,352 million), Uzbekistan (US$4,460 million), Kyrgyzstan (US$974 million) and lowest in Tajikistan with US$915 million in 2010. While in terms of outward FDI stock, Kazakhstan is the only one country in Central Asia which is dominated with US$16,176 million in 2010.

FDI Inflows and Outflows of Central Asian Countries (1992 to 2010)

It is quite clear from Table 3 that Kazakhstan is dominating in the FDI inflows among the Central Asian countries throughout the period between 1992 and 2010. FDI in Kazakhstan increased every year since 1994, with the exception of 1998, 2000, 2002 and 2005. FDI inflows in Kazakhstan was merely US$100 million in 1992 which increased significantly to the highest ever point at US$13,771 million in 2009 and in 2010 it recorded US$9,951 million as a provisional figure. Turkmenistan is the second in FDI inflows ranking in the region with US$2,083 million, followed by Uzbekistan (US$822 million), Kyrgyzstan (US$233.6 million) and Tajikistan (US$44.8 million) in 2010. Among the Central Asian economies, only Kazakhstan has FDI outflow figure which is around US$7,806 million, remaining other four countries are insignificant in FDI outflows.

The share of Kazakhstan’s FDI inflows in the region ranges between 74 and 92 per cent during the period between 1992 and 2010. Even in 1993, Kazakhstan’s FDI inflows constituted around 90 per cent followed by Turkmenistan (5.6 per cent), Uzbekistan (3.4 per cent), Kyrgyzstan (0.7 per cent) and Tajikistan (0.6 per cent), but after 18 years, Turkmenistan is emerging as the second-largest country with 15.8 per cent of total regional FDI inflows, while Kazakhstan’s share declined but still dominated with 76 per cent of the regional FDI inflows in 2010. Uzbekistan constituted little over 6 per cent of regional FDI inflows, while Kyrgyzstan constituted merely around 2 per cent and Tajikistan around 0.3 per cent in the regional FDI inflows in 2010.

FDIs in Kazakhstan, in terms of flows and stock, were dominated by investors from developed countries, primarily from the United States, the United Kingdom, the Netherlands and Italy. Among the developing economies, the Russian Federation and China dominated the FDI situation in Kazakhstan. In Kazakhstan, real estate and mining dominated in FDI during the period 2003 to 2009. The biggest share of investment went to the following sectors of Kazakhstan’s economy: real estate (53 per cent), mining (26 per cent), trade (5 per cent), electricity, gas and water (5 per cent), construction (3 per cent), manufacturing (3 per cent), financial activities (2 per cent) and transport and communication (1 per cent). The biggest investors in Tajikistan’s economy are companies from Netherlands (28 per cent), USA (16 per cent), China (6 per cent), United Kingdom (6 per cent), Virgin Islands (4 per cent), Italy (4 per cent), Russia (4 per cent) and Japan (3 per cent) up to 2009.

Kyrgyzstan was very quick in implementing its liberal and democratic transition policies to reach macroeconomic stabilisation and restructuring (UN 2003). Kyrgyzstan has no foreign exchange controls and acceded to the World Trade Organization (WTO) in 1998. In Kyrgyzstan, foreign investment is governed by law No. 66 on investments, of 27 March 2003. The law provides foreign investors and domestic investors with equal rights and opportunities to perform economic activities in Kyrgyzstan. According to the law, there are no restrictions on foreign investments; all economic sectors are open to foreign investment projects. Foreign investors have the right to own 100 per cent of the property in all sectors, which means that no industries and sectors are restricted with regard to the performance of business activities. Investors are also given the right to freely repatriate capital, dividends and other forms of revenue. Despite these policies, FDI in Kyrgyzstan is still low and half of the foreign investment goes to a single project, Kumtor gold mining, which is a joint venture set up by the Kyrgyz government and Cameco Gold Co. of Canada.

Kyrgyzstan’s foreign investment projects were concentrated mainly in manufacturing industries, and mining and financial activities. The main foreign investors were Kazakhstan, accounting for about 19.2 per cent of total investment, followed by Germany (17.3 per cent), the United Kingdom of Great Britain and Northern Ireland (14.0 per cent), Canada (12.4 per cent), Turkey (7.7 per cent), United States (5.6 per cent) and Cyprus (5.0 per cent). Other countries account for the remaining 18.8 per cent. The largest industrial investors in Kyrgyzstan were Kumtor Operating Company (Canada), Reemstsma Kyrgyzstan (Germany) and Kyrgyzpetroleum Company (Canada). The largest investors in finance activity were the Demir Kyrgyz International Bank from Turkey, Amanbank from the Russian Federation and the Kyrgyz Investment and Credit Bank from the European Union.

There are many impediments blocking FDI flows. Among these are excessive red tape, corruption, large-scale smuggling, lack of legal stability, lack of regional cooperation and security concerns. The existence of these impediments is accepted by many observers including A. Akaev, the current president of Kyrgyzstan. It is promising that the problems are identified in a clear and precise way, although the solutions to these problems are not easily realised because of a lack of appropriate institutions and the political resistance to change (IID 2002). The majority of FDI (in gold mining) in Kyrgyzstan unfortunately does not contribute heavily to the economic development, because it does not offer much opportunity for local companies to learn from foreign firms’ experience, and second, does not provide much employment opportunity either. It would have been so if FDI had concentrated more on manufacturing industries. 5

In Tajikistan, favourable conditions are being consistently created to attract foreign investments, support market structures and develop commercial banking and finance system. The process of registration of joint ventures and enterprises with other forms of property has been simplified. Tajik government’s policy measures create favourable conditions for foreign direct investments’ flow into the country’s economy. Tajikistan has adopted the National Development Strategy until 2015. The article defines the following priority sectors for investment: energy, mining industry, chemical industry, civil construction and manufacturing of construction materials, light industry and food industry, agriculture and processing of agricultural products, transport and communication and tourism.

The biggest volumes of investment in the period from 2007 to 2009 went to the following sectors of Tajikistan’s economy: energy (US$419 million), civil construction (US$201.4 million), banking services (US$194.4 million) and communication (US$188.9 million). According to the CIS Interstate Statistical Committee, in the years preceding the crisis, Tajikistan remained the leader among the other CIS countries in terms of investment growth in fixed capital. In 2008 investments in Tajikistan’s fixed capital increased by 60 percent compared to 2007. The volume of foreign direct investments reached US$760 million and amounted to 14.6 percent to GDP (UNDP, 2010). At present, the biggest investors in Tajikistan’s economy are companies from Russia, Kazakhstan, Cyprus, China, Canada, USA and the United Kingdom. Among them are Gazprom, Tethys Petroleum (exploration and extraction of oil and natural gas), United Energy Systems of Russia (power generation), Zijin Mining (exploration of gold and silver deposits), Adjind International (textile industry), Hyatt (hotel chain) and other companies. The most successful major enterprises with joint capital are as follows: Sangtuda-1 hydropower plant, Sangtuda-2 hydropower plant, ‘Penjikent–Zeravshan’, ‘Darvaz’, ‘Aprelevka’, ‘Javoni’, ‘Marmar’, ‘Obi Zulol’ (Government of Tajikistan 2010).

Since independence, the Turkmenistan government has sought to build a business environment that would attract foreign investment as well as facilitate the growth and privatisation of its own businesses. Turkmenistan’s ‘open door’ policy has created a favourable environment for the active influx of foreign investments and developed several joint-ventures with international companies involved in the oil and gas industry, transportation and agriculture. The government continues to look for interested parties who could build business relations with Turkmenistan in other industries such as agriculture, infrastructure, communication, food processing and packaging and many others.

Most of the foreign investment in Turkmenistan 6 is directed toward the oil and gas sector. Such investments include three onshore Production Sharing Agreements (PSAs): the Nebitdag Contractual Territory operated by Burren Energy UK/ENI, the Khazar project operated jointly by the Turkmennebit state oil concern and Mitro International of Austria, and the Bagtyarlyk Contractual Territory operated by the Chinese National Petroleum Corporation (CNPC). In addition, there are five PSAs for offshore operations: the Cheleken Contractual Territory operated by Dragon Oil (UAE), Block 1 operated by Petronas of Malaysia, Blocks 11 and 12 operated jointly by Maersk Oil of Denmark and Wintershall of Germany, Block 23 operated by RWE of Germany, and Block 21 operated by Itera of Russia.

In Turkmenistan, large-scale investment projects continued to be carried out in 2007, including in the oil and gas sector (construction of new and reconstruction of existing [inter-State] gas pipelines, allowing for the export of more hydrocarbons), and in the transport sector (construction of railways and motorways), and the development of the Avaza national tourist area and other manufacturing and non-manufacturing facilities. To promote its investment policy, the government has begun to monitor current laws and regulations and draft new ones to establish an investment environment favourable to increasing foreign investment flows into the economy.

In Uzbekistan, the most attractive sectors for investment are banking and finance, textile, natural resources, chemicals, energy, electro-technical, tourism, automobile production, telecommunications, media, transport, construction materials, real estate, retail, food processing and agriculture. The most successful investment acquisitions and investments in Uzbekistan were (a) Telecom: (i) MTS (Russia)—74 per cent share in Uzdunrobita; and (ii) VimpleCom (Russia)—100 per cent of Buzteland Unitel; (b) Oil and Gas: (i) Gazprom (Russia)—deals worth more than US$1.5 billion; and (ii) Lukoil (Russia)—deals worth more than US$1 billion; and (c) Food Processing: Nestle SA (Switzerland)—dairy and mineral water products production.

Uzbekistan has a lot of oil and natural gas and has so far identified 187 hydrocarbon fields, including 91 gas and gas condensate fields and 96 oil and gas, oil condensate and oil fields. The country is developing 88 of these fields; 58 fields are ready for development; nine are ‘held in reserve’, and 17 are in ‘geological exploration’ (>Interfax 2004).

Uzbekistan has two older refineries at Fergana and Alty-Arik, and a newer one at Bukhara—all with a total refining capacity of 11.1 million tonnes per year (World Bank 2003). Uzbekistan’s natural gas has a high sulphur content which requires significant processing. The majority of Uzbekistan’s gas is produced at the Mubarek processing plant, which has a capacity of approximately 28.3 million BCM per year (US Department of Energy 2008). A relatively new Shurtan Gas–Chemical Complex was completed at the cost of about $1 billion, and the Kodzhaabad underground gas storage facility was completed in 1999 at the cost of $72 million (World Bank 2003).

Uzbekneftegaz is the state-owned company that may sign oil and gas exploration and production contracts, independently perform petroleum operations in certain areas, act as a participant in joint ventures, and supervise petroleum operations (US Department of Energy 2008). Uzbekneftegaz is a holding company which is regulated under Presidential Decree No. UP-2154 (Republic of Uzbekistan 1998a) and COM Resolution No. 523 (Republic of Uzbekistan 1998c). Uzbekneftegaz controls downstream and related activities in the energy sector, including (a) Uzneftedobycha (oil extraction); (b) Uzneftegaz Pererabotka (oil and gas processing); (c) Uztransgaz (gas and oil transportation and pipelines); and (d) Uzvneshneftegaz (foreign economic relations) (Uzbekneftegaz National Holding 2009,

In addition to its role as the nominated state co-venturer in exploration and production ventures with foreign investors, Uzbekneftegaz has also now been designated as the ‘Competent Body’ to regulate the oil and gas industry (Republic of Uzbekistan 1994). Such a dual role as both a producer and regulator might be considered by foreign investors as a conflict of interest. Uzbekneftegaz was founded by the decree of the President of Uzbekistan on 11 December 1998 (Republic of Uzbekistan 1998a, 1998b). The holding company was created out of nine companies in 1998 to unite the country’s entire petroleum sector, and is now a mammoth state-run concern (Michael 2009).

Regional FDI in Central Asia

Major investment projects of Kazakhstan in the Central Asian region are implemented in Kyrgyzstan, particularly in the banking sector. Successful economic reforms fostering market discipline and high standards allowed Kazakhstan to establish a well-functioning banking sector outperforming that of most other CIS countries, allowing the banking sector to pursue an active expansion strategy abroad (Libman 2008). Currently, the main holdings of the banks of Kazakhstan in Central Asia include Nacional’nyi Eksportno-Importnyi Bank (Kyrgyzstan) owned by TuranAlem (originally purchased by Temirbank), Kazkommerzbank Kyrgyzstan (Kyrgyzstan) and Kazkommerzbank Tajikistan (Tajikistan) owned by Kazkommerz, ATF Bank Kyrgyzstan (Kyrgyzstan) owned by ATF Bank, Finance Credit Bank (Kyrgyzstan) owned by the Seimar Alliance Financial Corporation and Halyk Bank Kyrgyzstan (Kyrgyzstan) owned by Kazakhstan People’s Bank. The state-owned Development Bank of Kazakhstan has a representative office in Uzbekistan. Investments from Kazakhstan account for about 30 per cent of the capital of the banking system of Kyrgyzstan being the sole major foreign investor (Abalkina 2007), and the share of the banks controlled by Kazakh banks may reach 50 per cent of the market for banking services (Kuz’min 2007).

There are several other sectors where investors from Kazakhstan achieved relative success. In Kyrgyzstan, one may mention the tourist industry—in particular the recreation facilities in the Issyk-Kul region (UNDP 2006). The most well-known deal is the agreement to hand over four facilities to Kazakhstan signed in 2001 and ratified in 2008. It probably only covers the tip of the iceberg. In March 2008, Kazakhstan and Kyrgyzstan announced their plan to construct a new road connecting Almaty and Cholpon-Ata at Issyk-Kul, which, however, is still very far from implementation. It is certain that a clear advantage is the geographic proximity of the region to Almaty, increasing the potential market for the tourist services for customers from Kazakhstan.

Further sectors of the investments from Kazakhstan include mining, construction and media industries, as well as real estate. In Kyrgyzstan, Kazakh companies control the Kant Cement and Slate Plant, maize syrup plant, two concrete plants, Tokmak Brick Plant, Kadamjai Stibium Plant, Tokmak Wool Processing Plant, Kyrgyzenergoremont in Bishkek; and participate in the development of gold deposits at Jeruy (Visor Holding) and Taldy Bulak (Sammergold). In Tajikistan, KazInvestMineral acquired the Adrasman mining complex in 2006 for $3.2 million. In the field of gas supply, Kazakhstan’s state-owned KazTransGaz and Kyrgyz Kyrgyzgaz established a joint stock company, KyrKazGaz, in 2004 to operate the gas pipelines to the North of Kyrgyzstan and the South of Kazakhstan. As in the CIS in general, the dominant instrument is still the acquisition of existing assets, though there is an increasing presence of greenfield investments (like the recently initiated project of a ferrosilicoaluminium plant in Tash-Kumar [Kyrgyzstan] for $100 million). BRK-Leasing, a subsidiary of the Development Bank of Kazakhstan, provided €7 million for financing the development of textile production in Bishkek. In December 2008, the ambassador of Kazakhstan in Uzbekistan Zautbek Turisbekov proposed to provide finance to farmers from the banks of Kazakhstan, as well as to establish joint food-processing plants in the border zone (Libman 2009).

Finally, Kazakhstan seems to be extremely interested in power utilities in Kyrgyzstan and Tajikistan (in January 2008, Kazakhstan declared its plans to participate in the reconstruction of the Kambarada Power Plant in Kyrgyzstan, and in February—in the reconstruction of the Rogun Power Plant in Tajikistan); however, any perspectives in this field are still vague, especially given the active position of Russian business in the area. The investment activity seems to be driven by both relatively cheap labour (compared to Kazakhstan) and access to natural resources. Access to markets seems to be less important in this sector (unlike banking services).

The opposite direction of investments from Uzbekistan, Tajikistan and Kyrgyzstan to Kazakhstan seems to be insignificant. In the first nine months of 2007, Uzbekistan accounted for about 0.004 per cent of total FDI inflow to Kazakhstan (or 11 per cent from the CIS), 7 and Kyrgyzstan for 0.008 per cent (or about 22 per cent from the CIS). There is no data on the investment activity of Tajikistan, as well as cross-border investments in Central Asia beyond Kazakhstan. Now, it is quite clear and looks like the Central Asian regionalisation is as asymmetric as the regionalisation process in the CIS in general, with Kazakhstan as the main source of outward investments and Kyrgyzstan as the main recipient of FDI. In Tajikistan, investments from Kazakhstan are important, but less active, than those of Russia (in Kyrgyzstan the situation is exactly the opposite). Uzbekistan and (especially) Turkmenistan are much less active in the development of intra-regional investment ties (Libman 2008).

It is quite clear now that the Central Asian regionalisation is as asymmetric as the regionalisation process in the CIS in general, with Kazakhstan as the main source of outward investments and Kyrgyz Republic as the main recipient of FDI. In Tajikistan investments from Kazakhstan are important but less active, than those of Russia (in the Kyrgyz Republic the situation is exactly the opposite). Uzbekistan and (especially) Turkmenistan are much less active in the development of intra-regional investment ties. The role of Turkmenistan in the regionalisation processes is negligibly small. FDI expansion from Kazakhstan in the CARs and increasing labour migration to this country crucially depends on the sustainable economic performance of Kazakhstan. Recent turbulences related to the global financial crisis, which seem to have a significant impact on the banking system of Kazakhstan (the driving force of FDI integration), raise some questions regarding the viability of the model. Therefore, the coming few years could be quite interesting from the point of view of informal regional integration in Central Asia.

Barriers to FDI Inflows in the Central Asia

The most important advantages for attracting FDI into Central Asia are as follows: (a) endowment in natural resources as a potential for further resource-related FDI; (b) high growth rates; (c) huge FDI in the energy sector as a catalyst for other related FDI; and (d) cheap and productive labour. Central Asia is endowed with abundant natural resources, including oil, natural gas, coal and metal ores. These resources are unequally distributed across the countries of this region. Kazakhstan is an energy-rich country with huge reserves of oil and natural gas, but is also rich in coal, iron, chrome, gold and other metal ores. Uzbekistan and Turkmenistan are rich in natural gas and coal and have some reserves of oil. The Kyrgyz Republic is rich in gold and hydropower, while Tajikistan, in addition to hydropower, has some reserves of uranium, petroleum, coal, gold and silver.

Huge FDI in the energy sector and other extraction industries can be a catalyst for other related FDI, with important multiple effects for economic development in the region. Cheap and productive labour, high growth rates and some progress in transition can be considered a good precondition for attracting more diversified, labour-intensive FDI. Nevertheless, this can only be considered a potential advantage, due to a number of barriers for the realisation of these advantages, including poor physical infrastructure and lack of regional cooperation.

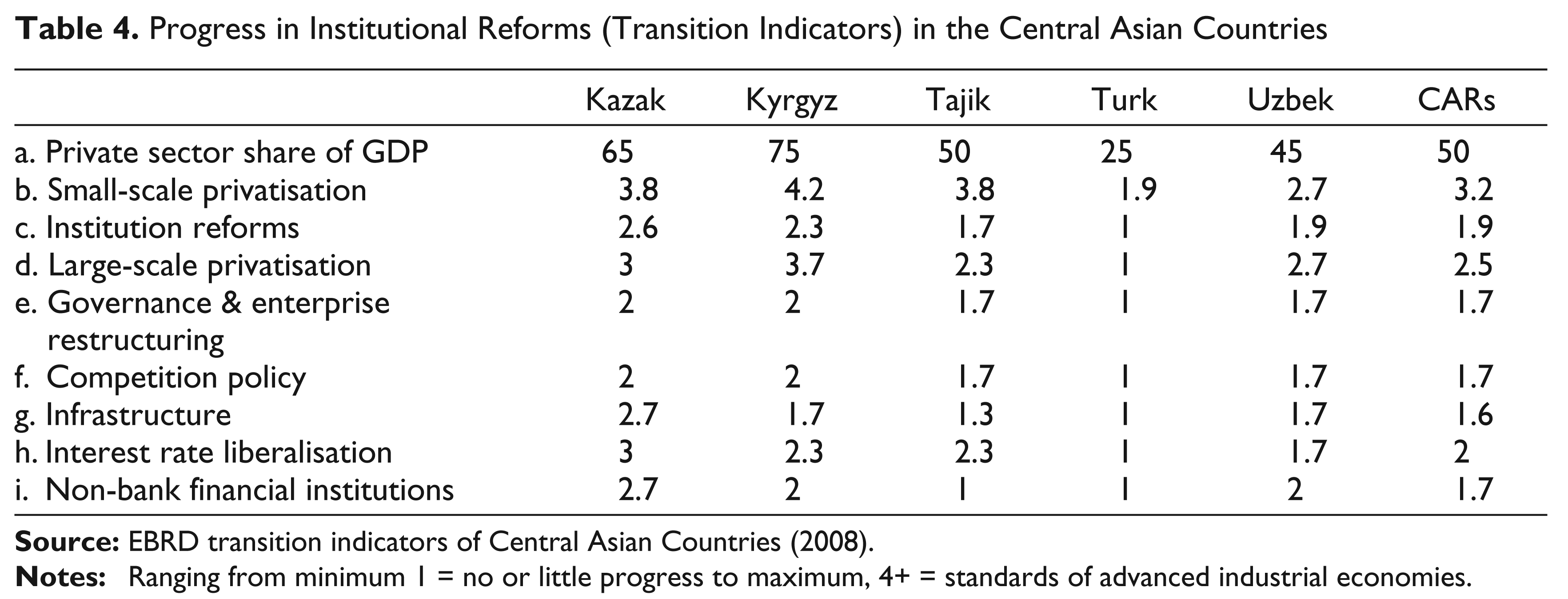

In the World Bank’s 2011 ‘Ease of Doing Business’ list of 183 countries, Kyrgyzstan performed the best of the CARs, ranking at number 44. Kazakhstan followed closely at number 59; Tajikistan and Uzbekistan lagged behind at numbers 139 and 150, respectively, while Turkmenistan was not included in the World Bank list. Weak institutional infrastructure, lack of entrepreneurial capacity and lack of competition policy in the CARs are generating a number of obstacles for the improvement of the business and investment environment, and are crucial impediments to private sector development and long-term prosperity. Physical infrastructure is underdeveloped in the Central Asian region, and all Central Asian countries, with the exception of Kazakhstan, are lagging far behind other countries in transition in almost all utilities sectors (see Table 4).

Progress in Institutional Reforms (Transition Indicators) in the Central Asian Countries

A lack of adequate roads, export energy infrastructure and railways, and the poor quality of existing ones, together with inadequate water supply, are important obstacles to FDI in Central Asia. Inadequate export energy infrastructure is a serious impediment to increased gas production and exports not only in Uzbekistan but also from other Central Asian countries rich in natural gas, such as Kazakhstan and Turkmenistan. Among the CARs, weak institutions present an obstacle to good governance, resulting in poor implementation of laws, development of informal processes and widespread corruption in the region. Transparency International’s Corruption Perception Index identifies high levels of corruption throughout the Central Asia region.

Since 2000, the CARs have taken serious measures to attract FDI. According to the Organization for Security and Cooperation in Europe (OSCE), FDI into Central Asia increased from $3 billion to $19 billion between 2005 and 2009. Despite the high figures, Central Asia’s experience with FDI since 1991 illustrates the need for increased governing capacity.

The participation of business intermediaries, employers, civil society and other stakeholders in the consultation process with the policy-makers is crucial for improving the transparency and effectiveness of policies (OECD 2007). Figure 2, based on the PfC26 survey, highlights areas where the public and private sectors are aligned on the need for policy reforms—like access to finance—but also areas of misalignment like human capital development and investment policy and promotion. For instance, there is a need to strengthen public–private dialogue between government officials and foreign investors through regular consultations to assess and improve the host country’s regulatory environment concerning foreign investment or in the area of human capital development.

The misalignment on the perceived level of reform between private and public sector representatives may be the result of a lack of communication between the regulators and the business representatives, and their different perception about the success of reform in the country. It may also reflect difficulties in implementing reforms throughout the country and bottlenecks related to enforcement. The public sector is encouraged to engage in a more regular dialogue with representatives of business, civil society and other stakeholders in order to learn about their real needs and constraints and adjust their policies according to these needs in order to ensure private sector development (Farra et al. 2011).

Experience shows that similar barriers to FDI inflows are more or less present in both regions: (a) high investment risks; (b) underdeveloped institutional infrastructure due to slow progress in institutional reforms; (c) underdeveloped physical infrastructure; (d) unfavourable legal environment—governance and corruption problems; (e) weak regional cooperation; and (f) relatively small size of domestic markets and low purchasing power. Even though relatively high investment risks characterise the countries of both regions, they are more severe in South Caucasian countries due to unsolved political and territorial disputes still present in the region. Since private foreign capital is very sensitive to security and the general political environment, it is crucial for these countries to find peaceful solutions to existing political tensions. This is an important precondition for regional cooperation.

It is also important to note that despite continuing trade policy reforms and FDI liberalisation policy initiated in the CARs, the FDI inflows cannot be fully realised without entering in concluding bilateral investment treaties (BITs) and double taxation treaties (DTTs) to assure investors that investments will be legally protected under international laws favouring all investment or through a business environment. Hence, an attempt has been made here to examine the measurement to enhance the effectiveness of BITs and DTTs in the Central Asian countries.

Measurement to Enhance Effectiveness of BITs and DTTs

In the past two decades, FDI has been spurred by the widespread liberalisation of the FDI regulatory framework, combined with advances in information and communication technologies and competition among firms. Most countries have opened themselves to foreign investment, improved the operational conditions for foreign affiliates and strengthened standards of treatment and protection. In fact, virtually all countries now actively encourage FDI, as it can bring capital, technology, skills, employment and market access. Investment promotion strategies include the establishment of Investment Promotion Agencies (IPAs), the offering of incentives, the preparation and dissemination of investment guides, and, notably, the conclusion of international investment agreements, especially bilateral investment treaties (BITs) and double taxation treaties (DTTs). For countries, the basic purposes of concluding BITs and DTTs are, respectively, to assure investors that investments will be legally protected under international law and to mitigate the possibility of double taxation of foreign entities and in this manner, to help increase FDI inflows.

Generally, developing countries sign BITs with the aim of attracting inward investment to promote economic development. There are two competing hypotheses about the relationship between a country’s BITs and FDI. First, a BIT signed with a particular home country sends a signal to investors in ‘that’ country that prospective investments in the host country will be well protected. Second, BITs send a signal to ‘all’ investors, whether or not their own home country has signed a BIT with a particular host country. Investors consider the BITs regime in a developing country as an overall indication of its willingness to protect the interests of foreign investors. The number of BITs with investor countries could then indicate that the country is protecting investors either through the enactment of general laws favouring all investment or through a business environment that is particularly favourable to external investors. Firms see a willingness to sign BITs with investor countries as a credible signal from the host country to investors throughout the world. 8 However, not all BITs are equal. Some BITs are signed with countries that are likely to be sources of FDI; others are signed between developing countries, neither of which is likely to invest much in the other.

The participation of Central Asian countries in other forms of FDI undertakings such as BITs and DTTs is negligible. Although Central Asian countries are involved in total 177 BITs and 125 DTTs with the world but there are only 10 BITs in the region. Similarly, DTTs are in force primarily among Kazakhstan, Kyrgyzstan and Turkmenistan. Tajikistan and Uzbekistan are not members of any such treaties. Among the CARs, Kazakhstan has signed and entered into DTTs with 41 countries (including Kyrgyzstan and Turkmenistan), Kyrgyzstan with 17 countries (including Kazakhstan), Tajikistan with 18 countries, Turkmenistan with 25 countries (including Kazakhstan) and Uzbekistan with 50 countries as of June 2011 (see Table 5).

Total Number of Bilateral Investment Treaties (BITs) and Double Taxation Agreements (DTTs) Concluded from Central Asian Republics (as of 1 June 2011)

As of now, BITs in the Central Asian region are underutilised and investor protection mechanism needs to be strengthened. Participation of Central Asian countries in forms of FDI undertakings such as BITs and DTTs at the regional level is small. These agreements provide relief from double taxation in respect of incomes by providing exemption and also by providing credits for taxes paid in one of the countries.

In a bid to promote and protect investments in the region, Kazakhstan has entered into BITs with 43 countries (including Kyrgyzstan and Uzbekistan), Kyrgyzstan with 27 countries (including Kazakhstan, Tajikistan and Uzbekistan), Tajikistan with 32 countries (including Kyrgyzstan), Turkmenistan with 25 countries (including Uzbekistan) and Uzbekistan with 50 countries (Kazakhstan, Kyrgyzstan and Turkmenistan) as of June 2011 (see Table 5). 9 These agreements provide for relief from double taxation in respect of incomes by providing exemption and also by providing credits for taxes paid in one of the countries. Some double taxation avoidance agreements provide that income by way of interest, royalty or fee for technical services is charged to tax on net basis. This may result in tax deducted at source from sums paid to non-residents which may be more than the final tax liability.

Deepening regional cooperation on investment among the CARs economies, as well as addressing issues, that is, visa scheme for business travellers, motor vehicular agreement, Non-tariff Barriers (NTBs), and LCSs would be substantial catalysts for improving the business environment and making Central Asia a more attractive destination for investment. While Central Asia has progressively started to liberalise FDI policies in the last decade, divergent policies among individual countries remain stumbling blocks. The investment regime in the CARs is not only restrictive but also lacks policy harmonisation. Supporting mechanisms are needed to support the flow of capital and to help attract more FDI from members. While a coordinated programme of regulatory reform and investment climate harmonisation will take time, efforts at the national level through individual country reforms are a significant first step.

Over the past 20 years, FDI’s track record in Central Asia illustrates the need to strengthen good governance, transparency, stability and the fair application of the rule of law. Only with these political-structural components satisfied will the long-term benefits of FDI be realised and the peoples of Central Asia will reap the benefits of a free and open market (Sholk 2011). The trends of FDI among the Central Asian countries revealed that Kazakhstan is the most attractive country, followed by Uzbekistan, Turkmenistan, Kyrgyzstan and Tajikistan. Turkmenistan is presently implementing a policy of openness to the world as well as vigorous policies to attract investment, which has had an important effect in increasing the country’s investment attractiveness. Completion of a gas pipeline to China also positively influenced its investment attractiveness. On the other hand, there is severe political confusion in Kyrgyzstan, which decreases its FDI attractiveness.

Conclusion

The overall assessment that emerges from this article is that Central Asian countries have created a conducive business environment to enhance regional and bilateral investment flows through the liberalisation of the FDI regulatory framework. The progressive liberalisation investment regime has already transformed the nature of economic links among these Central Asian countries and this process looks set to continue even further.

Central Asian economies would benefit from taking a sector-specific approach to investment promotion, which helps focus scarce resources on positioning a country strategically among its global competitors. In this context, agribusiness and information technology sectors are the best examples to initiate sector-specific approach to investment promotion in the region. There is an urgent need for the Central Asian countries to build competitive economies which will help them to unlock the full potential of investment opportunities across their economic sectors. They must further improve their investment policy frameworks by reducing state control over foreign capital flows and by removing slow and burdensome regulatory procedures. Policy reform should be accompanied by targeted investment promotion activities aimed at attracting high-quality investments that support job creation, income growth, technological diffusion, innovation and enterprise development.

Among the Central Asian countries, Kazakhstan is dominating in the FDI inflows and outflows, while remaining other four countries of the region are insignificant in FDI outflows. The issue of diversifying sources of FDI remains a priority for many of the economies of the region. In Kazakhstan, for example, 70 per cent of all FDI inflows to the country in 2009 went to the energy extraction sectors and related geological services—approximately twice the ratio level of the mid-1990s. Yet, the country has other high-potential sectors that could be developed to increase its wider competitiveness. In order to sustain competitiveness reforms and make progress, three mutually reinforcing pillars should be addressed: (a) sector-specific policy barriers; (b) developing human capital; and (c) supporting investment policy, promotion and innovation. The sector-specific approach could be of benefit to all the economies of Central Asia in increasing their competitiveness and laying the groundwork for sustainable growth. Now, the Central Asian countries must correct domestic distortions and continue institution-building in order to increase and diversify trade and investment in the region. A favourable domestic economic environment is crucial for stimulating investment (and attracting foreign investors) and for an effective economic response to good trade policies.

In a bid to promote and protect investments in the Central Asian region, Kazakhstan has entered into BITs with 43 countries (including Kyrgyzstan and Uzbekistan), Kyrgyzstan with 27 countries (including Kazakhstan, Tajikistan and Uzbekistan), Tajikistan with 32 countries (including Kyrgyzstan), Turkmenistan with 25 countries (including Uzbekistan) and Uzbekistan with 50 countries (Kazakhstan, Kyrgyzstan and Turkmenistan) as of June 2011. Over the past twenty years, FDI’s track record in Central Asia illustrates the need to strengthen good governance, transparency, stability and the fair application of the rule of law. Only with these political–structural components satisfied will the long-term benefits of FDI be realised and the peoples of Central Asia will reap the benefits of a free and open market.

To attract FDI inflows and promote vertical integration of industries in Central Asian region, Kazakhstan can be promoted and developed as a business hub for the region. Because of its location, stability and relatively better logistical systems, Kazakhstan has clear potential as a regional hub, serving neighbouring countries and bordering regions of these countries as well as becoming an important bridge between Asia and Europe. Kazakhstan can also significantly leverage its competitiveness effort by extending the level of regional economic cooperation. Kazakhstan has already attracted significant resource investment but needs to aggressively target companies serving the domestic as well as regional market, that is, consumer goods, transportation and logistics, financial services and retailing.