Abstract

In Europe, banks have been slow to increase green lending while they continue to finance high-GHG-emitting activities, leading to a ‘green banking gap’. Based on 88 interviews, we argue that explanations for the green banking gap can be grouped into three broad categories: bankability, business model, and regulation. First, there are not many green firms and projects that meet banks’ desired risk/return profile, while high-GHG-emitting activities remain bankable. Second, there are constraints to decarbonise banks’ portfolios arising from the change in banks’ business model in recent decades, making (green) corporate and project lending less important. Even when they lend, the characteristics of the lending process imply a bias towards high-GHG-emitting firms, as balance sheets are locked in old loans and banks prioritise long-term relationships with their clients. Finally, there are constraints on green lending and a lack of disincentives to high-GHG-emitting lending arising from financial and sustainability regulations and overall policy uncertainty.

Keywords

Introduction

Despite the severity of the environmental crisis, the financing for investments needed for the green transition remains too low, while the funding for fossil fuels and other high-greenhouse gas (GHG)-emitting activities continues at high levels. In Europe, the behaviour of commercial banks is an important part of the explanation of these trends. Indeed, there is evidence of what we term a ‘green banking gap’: banks have been slow to increase green lending (Altavilla et al., 2024; EBA, 2025; ECB, 2024; World Bank, 2024) and continue to finance high-GHG-emitting activities (Mack, 2023; Rainforest Action Network et al., 2025; Urban and Wójcik, 2019). Moreover, many banks have recently begun to backtrack on their previous climate commitments, including abandoning the Net-Zero Banking Alliance, which was dissolved in late 2025.

Against this background, this article asks: What are the reasons behind the green banking gap? Despite its many important contributions, the literature in the field of International Political Economy (IPE) and cognate disciplines studying the challenges of financing the green transition has so far paid little attention to private banks, focussing instead on non-bank financial institutions (NBFIs) (Ameli et al., 2020; Babic and Sharma, 2023; Baines and Hager, 2023; Buller, 2022; Christophers, 2019; Cooiman, 2023; Golka, 2024; Guter-Sandu et al., 2024; Murau et al., 2023; Sharma and Babic, 2025) or public and development banks (Dörry and Schulz, 2024; Marois, 2021; Mertens and Thiemann, 2023). The relative neglect of banks is surprising, as they remain the largest financial institutions in Europe: euro area banking assets represent 290% of GDP (Buch, 2024). Moreover, bank loans account for 75% of European corporate borrowing and 30% of their total funding (Buch, 2024; Mack, 2023). Importantly, banks could play a crucial role in financing key areas for the transition, including the greening efforts of small and medium-sized enterprises, and the building of housing retrofits, among others (Flögel et al., 2024; Mack, 2023). Banks’ relevance to the European financial system is clearly explained in the scholarship discussing the change in the behaviour of commercial banks in the past decades (Beck, 2022a, 2022b; Braun and Deeg, 2020; Hardie et al., 2013; Howarth and James, 2022). However, this literature does not elaborate on the consequences of their findings for the problems of green financing. Thus, an analysis of the role of banks in the green transition remains largely missing. This article aims to fill this gap, contributing simultaneously to the literature on the financing of the green transition as well as that on the characteristics of private banks.

To find an answer to our question, we interviewed 21 bank employees and 67 practitioners working in areas related to sustainable finance in NBFIs, the public sector, academia, and civil society organisations (CSOs). As our interviewees work for entities based in or active in Europe, and we draw mostly on academic literature focused on that region, the geographical scope of our paper is Europe. However, our interviewees and academic sources point to similar issues in other jurisdictions. Moreover, Europe is leading in sustainable finance regulation, so our results apply to non-European banks operating in Europe as well (Interview 27; 47; 68; 70; 81). Finally, our empirical focus is on large universal (i.e., those that combine traditional and market-based activities) global banks. Thus, some of the challenges that they report are also found in their operations outside of Europe. In this way, our findings are likely to apply to other places and could fruitfully inform future research with a different geographical scope.

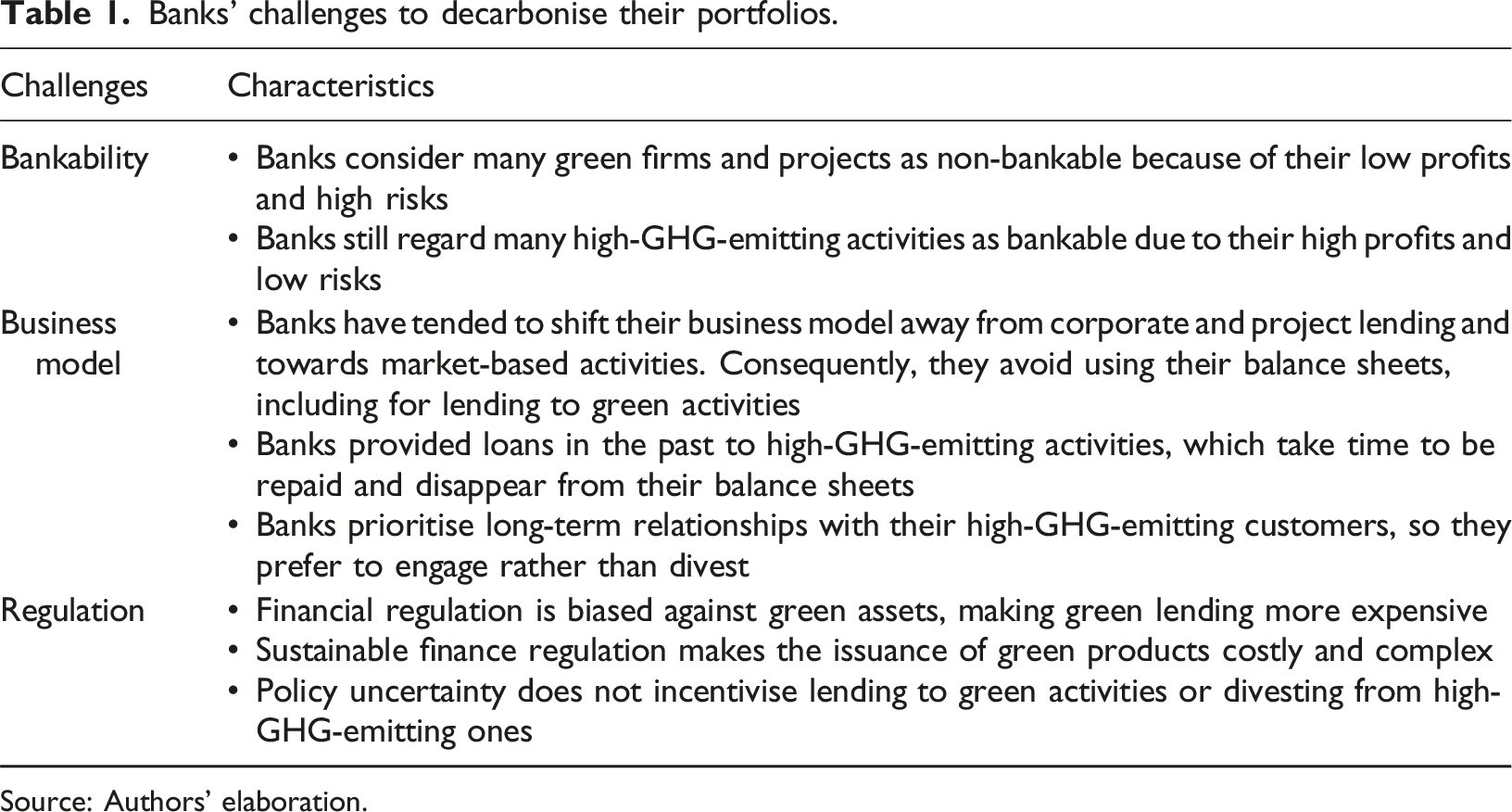

Based on a critical analysis of our empirical findings, we argue that the challenges that large universal global banks active in Europe face in decarbonising can be grouped into three broad categories: bankability, business model, and regulation. First, the category of bankability refers to banks’ structural pressures to maximise profits and minimise risks (Christophers, 2024). In this regard, interviewees argue that green firms and projects are generally not bankable because banks consider many green investments to be either not sufficiently profitable or too risky. In contrast, banks continue to regard high-GHG-emitting firms and projects as highly profitable and low risk, so they keep investing in them.

The second category, business model, encompasses two distinct elements: the transformation in banks’ business models and the nature of the lending process. Regarding the former, in the past decades, large universal global banks moved away from their traditional activities and diversified their business, focusing increasingly on market-based activities and the provision of financial services (Beck, 2022a, 2022b; Braun and Deeg, 2020; Hardie et al., 2013; Knafo, 2022; Sgambati, 2019). Consequently, interviewees argue that banks avoid using their balance sheets, including for lending to green activities. When it comes to the latter, interviewees argue that the character of the lending process does not allow for fast decarbonisation of banks’ portfolios because their balance sheets are locked in old loans that take time to be repaid. Moreover, banks prioritise long-term relationships with their existing (including high-GHG-emitting) clients, so they prefer to engage rather than divest from them.

Third, the category of regulation describes challenges to the decarbonisation of bank portfolios arising from the current policy framework, including financial regulation, sustainable finance regulation, and general policy uncertainty. Interviewees claim that capital and liquidity requirements are biased against green assets, constraining and making green lending more expensive. Moreover, they emphasise that sustainability regulation in Europe makes the issuance of green products costly and unnecessarily complex. Finally, interviewees argue that policy uncertainty about the future path of decarbonisation of the economy does not incentivise investment in green activities nor divestment from high-GHG-emitting ones.

Banks’ challenges to decarbonise their portfolios.

Source: Authors’ elaboration.

The remainder of the paper is organised as follows. In the second section, we provide a theoretical discussion on the characteristics of banks in the era of market-based finance. The third section reviews the literature on the current role of banks in the green transition, focusing on Europe. The fourth section explains the article’s methodology and shows our findings on the challenges that banks face in increasing green lending and decreasing lending to high-GHG-emitting activities, organised in three subsections reflecting the three categories of explanations: bankability, business model, and regulation. The conclusion summarises the main arguments and elaborates on the consequences of our findings for discussions on the financing of the green transition.

Banks in the era of market-based finance

Banks are driven by the imperative to maximise profits and minimise risks in their competition with other financial institutions. The means through which they do so have evolved based on their characteristics and changing strategies leading and responding to innovations, regulations, and macroeconomic factors (Cerpa Vielma et al., 2019; Knafo, 2022). Traditionally, banks were the central institution of the financial system, having the legal privilege to grant credit by issuing liabilities that are accepted as means of payment (Cerpa Vielma et al., 2019). Their business model was characterised by the provision of long-term loans to corporate clients and the taking of stable deposits from loyal customers under a regulatory environment that shielded them from competition with NBFIs (Beck, 2022a; Braun and Deeg, 2020; Hardie et al., 2013).

Hardie et al. (2013) introduce the concept of market-based banking to describe the transformations that have taken place in the last few decades. According to them, banks have changed their funding sources, becoming less reliant on deposits and more dependent on short-term wholesale funding. They have also shifted the management of their assets towards securitisation and the selling of loans (the so-called originate to distribute model), as well as hedging and marking-to-market the assets that they keep in their books. As a result, the share of banks’ income derived from interest tended to decrease whereas that derived from other sources tended to increase.

While recognising several important insights from this approach, recent scholarship criticises the market-based banking concept. Beck (2022a) and Knafo (2022) argue that this concept leads to the paradoxical image of banks that became central but weak, as they are subject to the pressure of external market forces, and cannot explain why, while some banks are indeed weak, others are quite profitable and powerful. Similarly, Sgambati (2019) contends that, although banks face external pressures from financial markets, one should not lose sight of their agency and power.

To account for banks’ agency in this process, these scholars emphasise that the transformation of the banking sector was underpinned by large US banks’ strategies to maximise profits, starting from a shift towards liability management since the 1960s (Cerpa Vielma et al., 2019; Knafo, 2022). Knafo (2022) argues that rather than relying on deposits, banks turned to short-term borrowing in money markets through instruments such as certificates of deposit and repos. The shift to liability management subsequently changed the way they managed their assets: their capacity to borrow capital cheaply with few restrictions underpinned their move to proprietary trading. Moreover, the rise of new management techniques employing a mark-to-market approach, combined with the volatility of funding through liability management, rendered it costly and risky for banks to hold loans on their balance sheets, so they began to develop ‘originate to distribute’ practices.

Beck (2022a, 2022b) adds that the rise of liability management enabled US banks to outperform their European counterparts, including within Europe. The financialisation of US banks exerted thus pressure on European banks to catch up, forcing them to find dollars in foreign markets: the Eurodollar market in the 1970s and, later, the US money market directly. To operate in the US market, European banks had to change their business models towards liability management, overcome certain regulatory restrictions, buy institutions, and hire personnel. One consequence of this process was that European banks reduced their corporate loans, as they no longer yielded sufficient profits, and turned towards originating and trading securities from the 1990s.

The change in large banks’ strategies took place against the background of a global wave of banking and financial account deregulation from the 1980s until the great financial crisis of 2007-9, which eliminated barriers between commercial and investment banking, and for mergers and acquisitions (Alessandrini et al., 2016). The result of these processes is that banks have been growing and diversifying their activities, relying on increasingly internationalised and market-based structures (Braun and Deeg, 2020; Cerpa Vielma et al., 2019; Hardie et al., 2013; Howarth and James, 2022; Ioannou et al., 2019; Sgambati, 2019). The emerging archetypal institution has been the large, interconnected, complex, international bank, the so-called too big to fail banks or global systemically important banks (G-SIBs).

The financial stability risks associated with banking systems dominated by G-SIBs became abundantly clear during the 2007-9 crisis and the subsequent enormous bailouts. As a consequence, several countries adopted banking regulations of varying stringency, and new international Basel III rules were developed (comprising, among others, new capital, leverage, and liquidity requirements, macroprudential regulations, and a different treatment for G-SIBs) (Howarth and James, 2022). Despite post-crisis banking regulation, the size of G-SIBs has not significantly diminished, and their importance continues to grow (Ioannou et al., 2019).

Still, considerable variation in banks’ business models remains. Differences in business models can be attributed to several reasons (Ayadi et al., 2025). These include external factors such as those of a macroeconomic, regulatory, or historical nature, and those derived from the characteristics of their customers. However, there are also important internal factors, which give banks’ managers significant agency pertaining to the best way to maximise profits and minimise risks.

In this way, banks’ business models present important differences between and within jurisdictions. Despite the previously identified global trend towards market-based banking, it should be noted that the extent to which banks have departed from their traditional activities varies between countries, for instance, between continental Europe and the US and UK (Howarth and James, 2022). Furthermore, even within Europe, there is heterogeneity between banks’ business models. Existing classifications yield different categories, ranging from traditional retail-focused banks to investment banks, and several combinations in between, finding that the largest banks are increasingly universal while the smallest tend to remain retail-focused (Ayadi et al., 2025; Hryckiewicz and Kozłowski, 2017; Roengpitya et al., 2017).

In summary, there has been a trend towards convergence in the activities of large global banks as US banks penetrated the European market and European banks adopted a US-style of banking (Beck, 2022a; 2022b). Thus, in this article, we focus on large, globally active, universal banks operating in Europe. However, it should be noted that smaller regional banks remain important in many European countries (Alessandrini et al., 2016) and could also play an important role in the green transition (Flögel et al., 2024).

The recent transformation of banking practices provides the context in which the greening efforts of banks should be discussed. Despite its important contributions, the literature reviewed in this section, which studies the change in the behaviour of banks in the past decades, does not elaborate on the consequences of its analysis for the problems of green financing. We address this issue in the next section.

Banks and the green transition: The current state of affairs

Excellent and comprehensive recent literature reviews on the engagement of IPE and adjacent disciplines with the role of finance in climate change governance (Babic and Sharma, 2023) and green finance (Sharma and Babic, 2025) almost do not mention commercial banks. This reflects a focus on the contribution (or lack thereof) to the financing of the green transition of several NBFIs (Buller, 2022), including institutional investors (Ameli et al., 2020; Christophers, 2019), index providers (Fichtner et al., 2024), impact funds (Golka, 2024), venture capital funds (Cooiman, 2023), and asset managers, including their ESG funds (Baines and Hager, 2023; Golka, 2024). Scholars have also been scrutinising the greening efforts of public and development banks (Dörry and Schulz, 2024; Marois, 2021; Mertens and Thiemann, 2023) as well as those of regional banks (Flögel et al., 2024), although recognising that these institutions have different characteristics from their private counterparts. Thinking ahead, scholars see a secondary role for commercial banks in financing the green transition, arguing that the shadow banking system has more elasticity in the US (Murau et al., 2023) while a combination of off-balance-sheet fiscal agencies and shadow banks could best support green financing efforts in Europe (Guter-Sandu et al., 2024).

Without denying the importance of the role that NBFIs have been playing and will continue to play in financing the green transition, we argue that commercial banks are also key actors in that process: they remain the largest institutions in Europe, bank loans continue to be the largest source of corporate funding, and they could play a crucial role in financing important green activities (Buch, 2024; Flögel et al., 2024; Mack, 2023). Despite this, few contributions in IPE and adjacent fields pay sufficient attention to their role and challenges, and the topic is only emerging in other disciplines (see Akomea-Frimpong et al., 2022).

In the past decade, several public and private actors have built a consensus stating that banks should concern themselves with the environmental crisis because of the so-called double materiality (Bolton et al., 2020; Chenet et al., 2021; Christophers, 2017; D’Orazio and Popoyan, 2019; Flögel et al., 2024; Kedward et al., 2023; Morris and Collins, 2023). On the one hand, the environmental crisis affects financial institutions by exposing them to climate-related and environmental (C&E) risks. These include physical (arising from material destruction), transition (derived from changes in policy, technology, or preferences), and liability risks, which expose banks to falls in asset prices and default of their customers. Hence, banks should alter their behaviour to shelter themselves from the materialisation of C&E risks. This ‘single materiality’ framework has been the dominant European approach to green banking regulation, based mostly on disclosures and incorporating C&E risks into banks’ decision-making processes (Baer et al., 2021; Smoleńska and van ’t Klooster, 2022), although it is also evolving (van ‘t Klooster and Prodani, 2025). On the other hand, double materiality also means acknowledging that banks’ activities have an impact on the environment, for example, by financing fossil fuel companies that drive carbon emissions.

In addition to the steps taken to comply with the emerging green financial supervision, some banks have taken voluntary measures in response to pressures from civil society and clients, reputational concerns, and internal demands raised by environmentally conscious employees and managers (Akomea-Frimpong et al., 2022). European banks are setting up sustainability divisions, disclosing C&E risks, creating new climate metrics, making decarbonisation commitments, and drafting transition plans, as well as requiring their customers to make them (ECB, 2022b, 2024). They are also adopting credit risk assessment models incorporating C&E risks, which could lower (increase) capital requirements for green (dirty) lending, exclusion criteria that have sometimes led to divestment, and engagement approaches to influence their clients’ decisions (Interviews 28/29, 39, 41, 44, 45, 46, 47, 59, 68, 80, 81).

However, these steps have been moderate so far. Indeed, a growing body of empirical Economics literature has been adding evidence of what we term the green banking gap, namely that banks have been slow to increase lending to green firms and projects, while they continue to finance high-GHG-emitting ones. A European Central Bank (ECB) analysis of 95 European banks covering 75% of euro area loans finds that about 90% face high transition risks due to the misalignment of their portfolios with the goals of the Paris Agreement, and some 70% are also subject to high reputational and litigation risks as they made public net-zero commitments that are not yet fulfilling (ECB, 2024).

Banks remain misaligned partly because they have not significantly increased their lending to green sectors. According to the World Bank (2024), green loans amounted to only 0.15% of GDP in advanced economies and a meagre 0.06% in emerging market and developing economies in 2023, while sustainability-linked loans did only marginally better, reaching 0.29% and 0.15% respectively. In Europe, the European Banking Authority estimates that the green asset ratio (GAR), that is, the share of a bank’s taxonomy-aligned assets over taxonomy-eligible ones, was only 2.76%, while the loan-GAR was slightly higher at 6% in mid-2024 (EBA, 2025).

At the same time, European banks continue to finance high-GHG-emitting firms and projects: they derive more than 60% of their total non-financial corporate interest income from the 22 most GHG-emitting industries (ECB, 2022a). According to the ECB (2024), over 50% of banks’ misalignment is due to the financing of clients that are too slow to phase out their high-carbon production capacities, and over 30% from insufficient financing of build-out efforts. More concretely, banks are still highly engaged in lending to fossil fuels (Mack, 2023). Estimates show that fossil fuel financing by the world’s largest 60 banks not only stood at an extremely high USD 869bn in 2024, but also increased compared to 2023 (Rainforest Action Network et al., 2025).

Furthermore, a decrease in bank-financed emissions in the euro area does not necessarily indicate a fall in banks’ overall financed emissions. First, banks could diminish lending to fossil fuels in Europe while continuing or even increasing fossil fuel financing in countries with less stringent climate policies (Altavilla et al., 2024; Benincasa et al., 2022; Laeven and Popov, 2023). Indeed, a significant part of the lending by European banks to emissions-intensive sectors happens outside of the euro area (Benincasa et al., 2022; ECB, 2024; Sastry et al., 2024). Second, a decrease in bank lending to fossil fuels may be (more than) compensated by an increase in other forms of fossil fuel financing in which banks play a role, including bond and equity underwriting, loan securitisation, lending to private equity, and other mechanisms (Kedward et al., 2024; Schairer et al., 2025; Urban and Wójcik, 2019).

In conclusion, there is still no clear evidence of a significant reduction of banks' lending to high-GHG-emitting firms and projects or an increase in their lending to green ones. Against this background, we ask: why is there a green banking gap?

Why is there a green banking gap?

To answer this question, we conducted semi-structured interviews with 88 partners, of which 21 work for banks, 19 for NBFIs in divisions related to sustainability, 21 work in the public sector in areas related to financial regulation (including central banks and the European Commission), one works in academia, and 26 work for CSOs with a focus on environmental and/or financial topics. An anonymised list of interviewees can be found in the online Appendix.

Due to the article’s focus, the interviews with bank employees are particularly relevant. Consequently, we use them to guide the analysis, while the other interviews help us cross-check the results. Interviews were, in some cases, translated into English by the authors and edited for clarity (removing filler words and correcting errors) while preserving the meaning and, as much as possible, the original formulation. Interviews were conducted between November 2022 and October 2024 in Belgium, France, Germany, Luxembourg, Switzerland, the Netherlands, the UK, the US, and online.

Our empirical focus is on large global universal banks active in Europe. The interviewees work for eleven different banks headquartered in France (2), Germany (5), the United Kingdom (4), and the United States (2). Of these, seven are considered G-SIB by the Financial Stability Board, two are within the 32 largest European financial institutions according to the EBA, one is one of the United Kingdom’s ‘Big Four’ clearing banks, and one is a smaller bank (assets exceeding EUR 10 billion) that offers financial services to corporate clients. Moreover, we conducted interviews with two large European development banks, which supported our findings.

In addition, we organised three Policy Innovation Lab (PIL) meetings in 2023, 2024, and 2025 with selected participants from different professional backgrounds and significant experience in their fields. PIL members were involved in the development of the research from its inception and provided critical advice throughout. They also contacted us with potential interviewees based on their personal connections. We also followed a purposive sampling approach and contacted potential interviewees without personal referrals. Subsequent interviews came from snowball sampling. While this strategy might entail some selection bias, our large and diverse sample size mitigates it.

Discussions at the first PILs allowed us to identify the key factors at stake, which we translated into multiple preliminary criteria to code the interviews. Interviews were transcribed using Amberscript and later manually edited and coded using MAXQDA. Three coauthors coded the interviews independently and later compared the results. Based on a critical analysis of the empirical findings guided by insights coming from the literature review, we came up with three broad analytical categories of challenges, which we subsequently validated at the last PIL: bankability, business model, and regulation. These are discussed in turn in the following subsections.

Bankability

The first category involves banks’ structural pressures to maximise returns and minimise risks, expressed in their assessment of whether an investment is bankable. A firm or project is bankable if the bank considers that the client will be able to repay in due time at the agreed interest rate. Bankers want to know as precisely as possible the cash inflows that prospective borrowers will generate, and on what schedule, to assess their debt-servicing capacity (Christophers, 2024). Moreover, they are interested in finding out if borrowers have sufficient equity or can post enough good-quality collateral to ensure repayment.

This logic is also applied by banks to assess whether to lend to green firms and projects. When financing green projects, banks can either grant green loans or underwrite green bonds (proceeds of which are tied to a specific use) or issue sustainability-linked loans or underwrite sustainability-linked bonds (that are not tied to a specific use but require the client to improve certain key performance indicators – KPIs). An interviewee from a British bank notes that investors ‘are going to look at the sustainable finance investment and think, okay, is this going to contribute to our firm’s sustainability targets and is it going to drive profit? Does it have the right level of risk?’ (Interview 45). So far, however, our interviewees report that green firms and projects often fail to meet bankers’ expected risk/return profiles while high-GHG-emitting activities do (Interviews 8, 10, 21, 26, 28/29, 31, 38, 39, 41, 42, 45, 46, 47, 49 54, 75, 79, 80, 81, 85, 87/88).

Unprofitable and risky: The lack of bankability of green activities

An interviewee from a German bank argues: ‘It is not realistic to do something for ideological reasons’. Hence, the interviewee argues that the sustainable finance division of the bank needs to ‘make sustainable finance as attractive as possible’ (Interview 31). Putting things bluntly, an interviewee from a British bank states: ‘To be honest, our investor group is not [composed of] activist investors. They’re interested, but they’re more interested from the perspective of how are you going to make sure that these commitments don’t interfere with your returns’ (Interview 41).

While managers have important levels of discretion, shareholders can exert pressure on management to slow down the pace of decarbonisation if they do not find it profitable enough. As an interviewee from a US bank put it: ‘Everybody is trying to balance on this tightrope between going too slowly and being left behind or going too quickly and losing shareholder support’ (Interview 80). Consequently, an interviewee from a German bank points to the need for banks to move together in coordination (Interview 32).

In this regard, the problem is that there are not enough green profitable activities. Discussing renewable energy, Christophers (2024: xxix) finds that ‘The developments that renewables project sponsors propose to capital-rich financial institutions all too frequently are not considered suitable, investible or – to use the word favoured by the finance sector – “bankable.” And, invariably, the primary reason is (…) “bankable” essentially means “expected to be profitable.”’ Indeed, estimates place the share of projects that meet expected risk/return profiles at 40% for climate mitigation and 20% for adaptation (Finance Watch, 2024).

There are several reasons for this. Kedward et al. (2020) argue that some green investments, such as natural protection and restoration projects, are often not profitable because they prevent economic activity from happening and thus cannot be monetised. 1 Moreover, green firms and projects that are small-scale or confined to a local area tend to lack the minimum investment values required to justify transaction costs (Ameli et al., 2020; Kedward et al., 2020).

When green investments are profitable, their returns get quickly squeezed due to increasing competition for their financing (Christophers, 2024). In an attempt to green their portfolios, many banks have been drawn to the sustainable finance market, thus reducing the pool of available profitable green projects (Interviews 28/29, 31, 37, 52). This lack of green projects, according to an interviewee from a French bank, also limits the issuance of green bonds: ‘Once you don’t have any green projects anymore, you cannot issue green bonds because you have nothing else to fund’ (Interview 38). Hence, from getting a green premium due to the higher risks of renewable projects, investors could now even pay a premium to gain exposure to them (Christophers, 2024).

Competition among lenders gives more bargaining power to borrowers, who could, paradoxically, force banks to lend to high-GHG-emitting projects in exchange for allowing them to fund their green ones. As stated by an interviewee from a French bank: ‘Green assets are more and more in demand and we see more and more clients coming to us and saying, “if you want my green project, then you will first finance my 10 other brown projects”’ (Interview 28/29).

However, even green firms and projects with profit potential are considered riskier than high-GHG-emitting ones (Interviews 10, 79, 81, 87/88). An interviewee from a German bank states: ‘Green loans do not mean risk-free loans. And the risk profile of renewable energies is increasing massively’ (Interviewee 37). Similarly, according to an interviewee from a US bank: ‘The problem at the moment is [that] there’s no connection between credit risk and green, or there’s not the right connection. […] Because in fact, green has [had] a worse credit risk over the last couple of years’ (Interview 80).

One reason why green activities are deemed riskier is that some of them entail the use of new technologies. Although some green technologies already have an extensive trajectory, an interviewee from a British bank considers that they ‘are often not well established or let’s say, younger, less mature, which means they are riskier’ (Interview 39). Similarly, an interviewee from a French bank argues: ‘You have some technologies that are not mature and green doesn’t mean less risk as such’ (Interview 28/29). Even if banks do not see a problem with the technology itself, they might find it with the firms using it, which are, in some cases, young start-ups (Interview 10, 87/88). For instance, an interviewee from a European supervisory authority states that, in the case of the solar industry in Europe, ‘the technology itself is a tool for sustainability, but the counterparty has very high default risk (Interview 85).

Moreover, green projects are said to involve risks derived from their investment horizons. They are generally long-term commitments that exceed the time frame in which most banks are willing to conduct business. The typical bank lending horizon, for example, is 5 to 7 years, whereas the time frame for some green investments can extend beyond 15 or 25 years (Interview 26, 39).

All things considered, the risk/return profiles of green activities make them generally unattractive to banks. An interviewee from a British bank summarises the issue as follows: ‘So you have something like quite low profitability, high risk, uncertainty […] it’s a lot of issues’ (Interview 39). As a result, another interviewee from the same British bank argues: ‘Most of the financial industry infrastructure is built around risk and return. And I think that there it’s really hard to insert net zero or climate impact into this bilateral framework’ (Interview 46). In a similar vein, an interviewee from a US bank states: So sometimes there's a misunderstanding, and I see this repeated at every level of the system. If only banks would do the right thing, all our problems would go away. If only they would stop lending to this and lend to that instead, problem solved. That's never going to happen. And people don't realise why. But for the most part, banks just can't […] take credit risk that is not justifiable. And they can't reduce returns in a way that upsets shareholders. (Interview 80).

The consequence of this view is that the challenge of financing the green transition does not lie in the lack of money, but rather in the lack of bankable activities. In the words of an interviewee from a public development bank: ‘I don’t actually think we have a lack of funding out there. I think we have a lack of bankable, robust projects out there’ (Interview 49). An interviewee from a German bank makes a similar observation: One issue I've never understood is, and I read this everywhere, that there's a lack of money for [the] transformation. [...] In developing countries, I can completely understand the argument. [...] But in Europe? There is so much ready-to-invest money that likes to go into these green applications; what is missing are viable business models. (Interview 37).

An interviewee from a US bank also expressed frustration with a narrative ‘catalysed around COP26’ according to which ‘you have a wall of green capital, investors who are willing to invest are going to invest in the real economy, and we’re going to see changes in public policy’. The interviewee argues that ‘the order should be completely reversed, because ultimately, when you think about what an investor does, if it’s not an impact investor and philanthropic investor, they will have to have the right risk/return profiles’. The interviewee concludes: ‘We facilitate the transition, but we are not in a position to drive it because that would mean that we would have to be denying the market conditions or the risk/return profiles or whatever is happening in the real economy’ (Interview 45).

In this regard, an interviewee from a German bank criticises the presumption that banks should lend at cheap rates to governments for green projects: ‘[For] public players, I have to be honest, we’re getting a bit desperate because local authorities, in particular, expect free loans, and we’ll never give them. The public sector would have to step up to the plate itself’ (Interview 31).

High profitability and low risks: The continued financing of high-GHG-emitting activities

Unlike green firms and projects, high-GHG-emitting ones continue to be deemed highly profitable and low risk (Interviews 21, 37, 39, 68, 75, 79, 80, 81, 82, 85, 87/88). Regarding the profitability of high-GHG-emitting activities, an interviewee from a public asset owner explains the challenges of getting banks to divest from them: Look, we've been engaging with banks for the last three years on fossil fuel finance. […] [First,] we supported proposals that said immediately cease new fossil fuel expansion financing. And they failed fairly miserably with the shareholders. The reality is that [for] the bank shareholders […] this is a profitable line of business. It's going to make you money. You should keep doing it. (Interview 68).

Similarly, an interviewee from a supervisory authority states: ‘Some of these carbon-intensive exposures are very profitable. So the banks are extremely reluctant to get rid of those’ (Interview 85). As a result, an interviewee from a British bank stresses that banks could face a competitive disadvantage if they do not finance high-GHG-emitting firms and projects, as ‘someone else will do it because it’s profitable’ (Interview 39). In other words, it continues to be rational for them to invest in dirty projects in the short term (Ameli et al., 2020; Christophers, 2019).

Moreover, C&E risks are not yet fully priced in. Interviewees argue that physical and transition risks associated with high-GHG-emitting lending are not yet well understood and thus also not thoroughly included in risk calculations (Interviews 23, 32, 35, 42). Thus, high-GHG-emitting firms and projects remain considered less risky (Interviews 79, 80, 81, 87/88). An interviewee from a US bank puts it plainly: ‘Right now, if you’re a bank that is lending money to gas and oil where those prices have been post Russia-Ukraine, your credit risk looks great’ (Interview 80). In a similar vein, an interviewee from a supervisory authority states that, more often than not, dirty companies ‘have much better financial standing than the green projects that are start-ups that have actually [a] much higher probability to fail within the near future’ (Interview 87/88).

To conclude, an interviewee from a US bank argues: ‘There are fundamental misunderstandings of the role of finance in all of this. […] Because people think [that the] private sector is going to magically solve it. And it's not. It's never going to happen. And so we need to move beyond that’ (Interview 80). This leads us to consider another source of misunderstanding regarding the role of finance in the green transition, namely the characteristics of banks’ business models.

Business model

The second category involves limits that banks face to increase green lending or decrease lending to high-GHG-emitting activities, which arise from the characteristics of their business model. This involves two interrelated dimensions. First, the change in banks’ business model during the past decades means that corporate, and particularly project lending, has tended to decrease in importance in their activities. Second, when banks lend, the character of the lending process prevents fast decarbonisation of their portfolios.

The change in banks’ business model

The previously discussed change in the business model of large universal global banks active in Europe has concrete consequences for the financing of the green transition, particularly when it comes to lending to green activities. As an interviewee from a US bank puts it: ‘There’s a perception that banks are sort of lending. And, lending is actually a tiny part, relatively speaking. It’s really capital markets that probably drive the most fuel. […] Bank lending is typically a tiny piece, and it’s mostly undrawn’ (Interview 80).

In principle, what the shift in banking practices indicates is that banks are increasingly avoiding using their balance sheets. According to an interviewee from a British bank: ‘[Our activity] it’s connecting, typically in the capital markets. We are not the lender, [it] is not our money. But we are in the middle of that flow’ (Interview 39). This limits their willingness to increase green lending. For instance, an interviewee from a French bank states that when a customer comes with a green investment, ‘we say yes, we can accompany you, but we can’t accompany you over the entire term […]. Because we can’t or don’t want to provide our own balance sheet’ (Interview 26).

The change in banks’ business model also allows them to support the financing of high-GHG-emitting activities without directly lending to them (Kedward et al., 2024; Schairer et al., 2025; Urban and Wójcik, 2019). For example, banks continue to underwrite the issuance of bonds from these firms and are starting to securitise their dirty loans to offload them from their balance sheet (Interviews 7, 70, 82, 83). In this way, looking at their loan portfolios might not give an accurate picture of banks’ actual involvement in the financing of high-GHG-emitting activities.

The character of the lending process

Still, lending continues to be an important part of banks’ business. The character of the lending process, however, prevents a fast decarbonisation of their portfolios. First, banks cannot quickly decrease financing to high-GHG-emitting firms because they have already provided loans that take time to be repaid. An interviewee from a French bank explains: ‘The balance sheet [has] some kind of inertia. […] It’s about 10 to 15% of the balance sheet that changes every year. […] So it takes time to change that’ (Interview 28/29). The subjective estimates of interviewees could be biased to overstate the risks involved. The average maturity of a European bank loan is 7 years (ECB, 2024). Moreover, 40% of banks’ loans mature in 1 year, and 80% within five. However, rollovers are common as relationships are long-lasting.

Second, the prioritisation of long-term relationships with customers limits banks’ decarbonisation efforts as they might be too lenient on their criteria and evaluation to avoid divesting from their current clients (Flögel et al., 2024). An interviewee from a British bank states: ‘These are relationships with big companies that existed [for] like 150 years. And maybe we’ve been banking them that long. It’s like a family or a friend or something. You don’t just want to walk away from that’ (Interview 46). Similarly, the bank for which an interviewee works decided to ban coal investments, but they had existing clients that still had open orders, so the bank decided to finance them until the end and then revise the exclusion criteria (Interview 21).

Indeed, banks try to work with their high-GHG-emitting clients towards a transition path to keep their business instead of divesting (Interviews 23, 32, 38, 40, 41, 45, 46, 72/73, 80). Interviewees point to these long-term relationships as a lever that banks could pull to influence their customers into shifting towards more sustainable activities. An interviewee from a British bank argues: ‘I have 2 years to get this client to start to report on their disclosures. So I’m going to engage them now and say, in 2 years, if you haven’t done this, then I can’t offer you a normal revolving credit facility for your everyday needs’ (Interview 41).

Another interviewee from a US bank explains that, because engagement policies have become generalised, they are starting to have an impact: I think carbon-intensive clients […] are starting to be a little bit anxious and listening to banks a bit more, so that's an incentive for them to do the right thing. […] Look, it's not just for us, it's other banks, it's investors that are demanding it. So you can't really ignore all this (Interview 80).

Moreover, interviewees suggest that engagement is more effective than divestment. An interviewee from a British bank reasons that it is better if international banks that can exert some influence on the behaviour of their clients keep financing high-carbon clients, rather than leaving and letting smaller regional banks ‘that are not going to have any qualms about it’ replace them (Interview 41). Furthermore, bank divestment could lead to shadow banks filling the gap, thus not reducing the overall funding for fossil fuels while potentially reducing scrutiny of these activities (Schairer et al., 2025).

While banks’ efforts towards engagement can be motivated by a genuine attempt to steer their clients’ activities, it is important to keep in mind that high-GHG-emitting lending continues to be a profitable business, and banks do not want to lose it. Hence, banks might refrain from adopting strict engagement policies to keep customers, even when they are not decarbonising fast enough (Flögel et al., 2024). An interviewee from a British bank makes this point clearly when arguing: ‘[We have] almost like a heat map of which clients are contributing most to those financed emissions. And we realise that in order to meet our targets, yes, we can just withdraw financing, but that’s also our revenue’ (Interview 46).

Moreover, in cases where high-GHG-emitting borrowers run into profitability issues, banks still want to get repaid, explaining banks’ reluctance to cut ties with ‘zombie’ dirty borrowers (Giannetti et al., 2023). Finally, sector-specific specialisation and existing knowledge of fossil fuel technology are additional factors making banks reluctant to divest (Beyene et al., 2021). In particular, banks with relatively high fossil exposure find it easier to continue lending to carbon-intensive sectors in other geographical jurisdictions instead of changing the sectoral composition of their portfolios (Laeven and Popov, 2023).

Regulation

The final category refers to constraints that regulation imposes on banks’ capacity to lend to green activities and a lack of incentives to divest from high-GHG-emitting ones. Interviewees voice their concerns regarding financial regulation, sustainable finance regulation, and the overall policy environment.

Financial regulation

Research shows that financial regulation limits green lending. For instance, liquidity requirements induce banks to hold more high-quality liquid assets and require them to match long-term assets with more expensive long-term liabilities. This biases banks against investment in green assets, which are typically long-term and less liquid (Campiglio, 2016; D’Orazio and Popoyan, 2019). Something similar could be said about capital requirements as they entail higher risk weights for green assets (Campiglio, 2016; Chenet et al., 2021; Dafermos and Nikolaidi, 2021; D’Orazio and Popoyan, 2019).

Our interviewees echo such concerns (Interviews 14, 40, 45, 46, 47). A member of the Net-Zero Banking Alliance states: ‘The Basel Capital rules make it very, very hard to hold long-term credit risk’ (Interview 40). Likewise, an interviewee from a US bank notes: ‘When it comes to Basel (…) it’s a real concern that this is going to limit investments, especially in green activities’ (Interview 45). An interviewee from a British bank points out that this is particularly problematic because banks might manage to find profitable green assets, but if they are too risky, they will not lend to them due to the capital requirements associated (Interview 47).

Sustainable finance regulation

The EU developed a sustainable finance regulatory framework based on a classification system of economic activities (the green taxonomy), a comprehensive disclosure regime (including the Corporate Sustainability Reporting Directive and the Sustainable Finance Disclosure Regulation), and the introduction of standards such as the European Green Bond Standard (Mertens and Van der Zwan, 2025).

In what pertains to banks, the CSRD should increase the information that they receive from their clients so that they can assess C&E risks and take them into account in their operations. Moreover, the SFDR prescribes that they disclose sustainability information. In this regard, interviewees point to the poor quality of reporting and auditing (Interviews 23, 32, 34, 37, 52, 56). Furthermore, they complain that disclosure regulations impose costly and strict requirements for something to be considered ‘green’ (Interviews 9, 21, 26, 41, 72/73, 80, 81).

Issuing green instruments entails a process of developing new technical capabilities and hiring auditors and verifiers, among others (Christophers et al., 2020). While the sale of sustainability-linked products could be a source of additional fees for banks and thus a business opportunity (Flögel et al., 2024), our interviewees state that the costs often outweigh the benefits. As an interviewee from a US bank states: ‘I think managers are like, you know what? It’s not worth my while trying to get a label’ (Interview 80). Even further, an interviewee from a British bank suggests that green products could lead to losses: From a bank's perspective, if it's like a sustainability-linked product, sometimes we're even losing money on it than if we just offered the normal product line because we're offering an incentive or a discount to get them to do sustainability. It requires significantly more governance internally and controls. So it costs us more to actually provide the products (Interview 41).

More concretely, interviewees argue that producing the metrics and KPIs to get green bonds certified is time-consuming and costly (Interview 70). In this regard, an interviewee from a French bank states: You do have some cost [for] issuing those kinds of bonds as well. You need to have your numbers audited. You need to have a framework that is made. You need to have a second-party opinion. [...] And you do have a lot of human resources as well that are required. (Interview 38).

The increased scrutiny implied in green lending practices and demanded by regulation also makes it less attractive to customers: ‘It costs our clients more to get the product if we’re going to label it because they have to disclose significantly more information’ (Interview 41). Clients often lack the knowledge on how to originate a green asset with the necessary requirements (Interviews 21, 41, 49). As it costs both the banks and their customers more, an interviewee from a British bank asks: ‘Why are we doing these products? […] We could offer the traditional for a green purpose and not call it green, and we make more money’ (Interview 41).

Finally, interviewees highlight the reputational risk of being accused of greenwashing as a barrier to increasing their green-labelled lending. While this shows that regulations have been to some extent successful at tackling the issue of greenwashing, interviewees claim that they often refrain from using green labels, choosing instead regular products (Interviews 9, 10, 21, 26, 42).

In summary, the risks and costs associated with issuing green instruments compliant with sustainable finance regulation act as a limiting factor for banks’ willingness to offer these instruments and so increase their green (at least so labelled) lending. An interviewee from a US bank concludes: For a lot of stakeholders, their starting position was ‘if only we could provide more green bonds or transition bonds or create this transition label, this magical transition label then finance would flow towards green hydrogen to decarbonise steel’. No, it's not like [that]. These products obviously are very helpful, but they're not substitutes for government policy (Interview 80).

This leads us then to consider government policy more broadly.

Policy uncertainty

Policy uncertainty is a key reason for the reluctance of investors to finance green assets (Ameli et al., 2020). According to interviewees, firms cannot plan appropriately if they do not know the pace of the transition (Interviews 26, 32, 37, 45, 47, 56, and 79). They will find alternative ways of producing only if they have certainty that, in 5 or 10 years, it will be significantly more costly to keep business as usual.

An interviewee from an index provider explains that policy uncertainty also affects banks’ capacity to support green activities, as they ‘need to know [at] what pace this is going to happen […] to make sure the companies repay them. Investors need to know that as well, to have the confidence that they will get a good return on their investments’ (Interview 79).

As a result, interviewees advocate for stronger financial policies and public commitments toward the future path of decarbonisation (Interviews 21, 27, 45, and 79). An interviewee from a US bank summarises the issue as follows: Don't let my colleagues [...] hear that I said we need more state intervention. We do need more state intervention. [...] And this is what we need to have because allowing the private sector, in the absence of any incentives, to sort it out between them because they want to do the right thing, it's just never going to happen (Interview 80).

Conclusion

There is growing evidence that banks have not increased funding for green firms and projects at the required pace and scale while continuing to provide significant financing for high-GHG-emitting activities, leading to a ‘green banking gap’. Motivated by an attempt to understand why this is the case, we conducted interviews with 21 bank employees, supported by interviews with 67 practitioners working for NBFIs, the public sector, and CSOs. We argue that there are three broad categories of challenges that banks face to decarbonise their portfolios: bankability, business model, and regulation. By doing so, we contribute to the literature on the financing of the green transition by showing the structural, institutional, and policy-related challenges to the decarbonisation of private banks, which have so far received relatively little attention from scholars in the fields of IPE and cognate disciplines.

At a structural level, the category of bankability refers to the fact that green activities do not meet the desired risk/return profiles of banks, while high-GHG-emitting ones continue to do so. A conclusion that many interviewees draw from this is that the problem of the green transition, at least in the Global North, is not a lack of finance, but of bankable projects. Consequently, they argue that policies have been misguided as they focus too much on finance as if that alone were enough to green the productive economy.

At the institutional level, the business model category comprises two dimensions. First, the business of large global universal banks has changed in the last few decades as they have tended to move away from corporate, and particularly project, lending. Thus, interviewees argue that expecting banks to significantly increase green lending is not realistic, given that they try to avoid using their balance sheets. Second, interviewees claim that, when banks lend, there are limits to the decarbonisation of their portfolios arising from the characteristics of the lending process, particularly the inertia of their balance sheets as they are locked in old loans, and the prioritisation of long-term relationships with their clients.

At the policy level, the regulation category refers to limits on green lending coming from financial and sustainability regulations, as well as the overall policy environment. Liquidity and capital requirements are currently biased against green assets, thus constraining green lending. Sustainable finance regulation is deemed too costly and burdensome, so banks avoid using green labels or issuing green instruments. Finally, the uncertainty resulting from weak political commitments to the future decarbonisation path limits banks’ willingness to invest in green activities or divest from high-GHG-emitting ones.

Still, it is important to bear in mind that bankers are likely to emphasise the external constraints preventing taking meaningful action while downplaying their responsibility. It is thus necessary to take their statements seriously but not to accept them at face value. Rather, we aim to provide a critical reading, especially considering that they come from large universal global banks with significant power and agency. Additionally, interviewees often present estimates of profitability and risk as objective, when they are largely influenced by banks’ assumptions and biases.

Our results are, however, only preliminary findings of what we hope will become a broader research agenda. Further research should continue to build an accurate depiction of the current workings of the financial system. In this regard, more qualitative work is needed to understand what banks and other financial institutions actually do, and how this may support or challenge the financing of the green transition.

To conclude, we hope that our research helps design policies that are effective in leading to the decarbonisation of the economy. Our findings suggest that existing regulations do not respond to the challenges at the necessary scale and depth and point to the need for public intervention, including through credit guidance policies, to steer capital towards green activities and away from high-GHG-emitting ones. Nevertheless, they also point to the limits of a one-sided financial approach. Credit policies should be complemented with fiscal and industrial policies for a green structural transformation. This includes larger public investments in crucial activities for the green transition that are, for different reasons, not bankable and thus not attractive for private capital.

Supplemental material

Supplemental Material - The green banking gap: How bankability, business models, and regulations challenge banks’ decarbonisation

Supplemental Material for The green banking gap: How bankability, business models, and regulations challenge banks’ decarbonisation by Nicolás Aguila, Paula Haufe, Riccardo Baioni, Jan Fichtner, Simon Schairer, Janina Urban, Joscha Wullweber in Competition & Change.

Footnotes

Acknowledgements

The authors would like to thank Mareike Beck, Christoph Scherrer, participants at the Finance and Society Conference 2024 at the University of Sheffield and the 28th FMM Conference in Berlin for valuable feedback and comments. We would also like to thank all our interviewees for the time and effort they have taken to talk to us and share their expertise.

ORCID iDs

Ethical considerations

In accordance with the University’s data protection officer, our project did not have to consider further ethical standards aside from the written and oral consent of interviewees and protecting their data following the stipulations of the declaration of consent regarding anonymity, use of data, etc.

Consent to participate

Prior to the interviews, interviewees received a written declaration of consent outlining the conditions for participation, including information on the collection, processing, and storage of personal interview data. Interviewees were asked to sign the declaration of consent or give oral consent. When interviewees stated that they did not want to be recorded, we followed their instructions.

Consent for publication

In the declaration of consent mentioned above, interviewees agreed to the use of their interviews, including the use of anonymous quotes, for the purposes of publishing in scientific journals. When interviewees stated that they did not want to be quoted, we followed their instructions.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: the research was funded by the German Research Foundation (DFG) under the Heisenberg Professorship Programme, reference WU 780/2-1, and the German Federal Ministry of Education and Research (BMBF) under the programme ‘Climate Protection & Finance (KlimFi)’, reference 01LA2207A.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.