Abstract

This article analyses the opportunities and incentives of 32 accountants, resident in four very different parts of the British Empire (Scotland, Ireland, India and Australia), to import an English accountancy qualification in the late 1870s and become in 1880 the first “English” chartered accountants outside England and Wales (EW). This “export” and “import” of qualifications is one way in which professional accountancy has spread around the world since the late nineteenth century. The opportunities arose as the Society of Accountants in England (SAIE), set up in London in 1872, challenged the prevailing localism and exclusivism, and as attitudes in EW towards the concept of “Englishness” within the UK and the Empire changed. From 1875 the SAIE opened its membership to accountants within the Empire outside EW. The incentives of these accountants to join the SAIE depended on whether or not a body already existed in their own locality, how exclusive the body was, and its status in comparison with an English qualification. The paper concludes with a study of the varied impact of the 32 on accountancy globally.

Keywords

Introduction

When the Institute of Chartered Accountants in England and Wales (ICAEW) was established on 11 May 1880, as the result of the amalgamation of five bodies set up in England in the 1870s, 32 of its 600 founding members were, despite the name of the new body, located outside England and Wales (EW), although within the bounds of the British Empire. This article tells the story of the 32, explaining where these persons were located, how they were able to become members, what incentives they had to apply for admission to a predecessor body of the ICAEW, what their impact was on the development of the accountancy profession in their own countries, and how they set a precedent for the import and export of accountancy qualifications.

Today, British-based bodies are by far the most active global exporters of accountancy qualifications. For example, in 2012 no less than 51.3 per cent of the 158,574 members of the Association of Chartered Certified Accountants (ACCA) worldwide were located outside the UK and Ireland (Financial Reporting Council, 2013). Most of these had qualified by taking their examinations overseas. The ACCA has built upon the recruitment policy of its predecessor body, the London Association of Accountants, founded in 1904. Outside Britain the only comparable exporter of accountancy qualifications is CPA Australia, which in its 2012 annual report claimed a membership of over 144,000, of whom 26 per cent were located outside Australia. The explosion in the number of qualifications exported by the ACCA and other British bodies since the 1970s was documented by Briston and Kedslie (1997), updating figures collected by Johnson and Caygill (1971). As the latter show, before its amalgamation in 1957 with the chartered accountancy bodies of England and Wales, Scotland, and Ireland, the Society of Accountants and Auditors (SAA), founded in 1885, also had a substantial number of members who had qualified overseas (see also Garrett, 1961). However, credit for pioneering the idea of the export of an accountancy qualification and admitting to membership the first 32 accountants within the British Empire to import qualifications from outside their own country, must go to the Society of Accountants in England (SAIE), a predecessor body of the ICAEW.

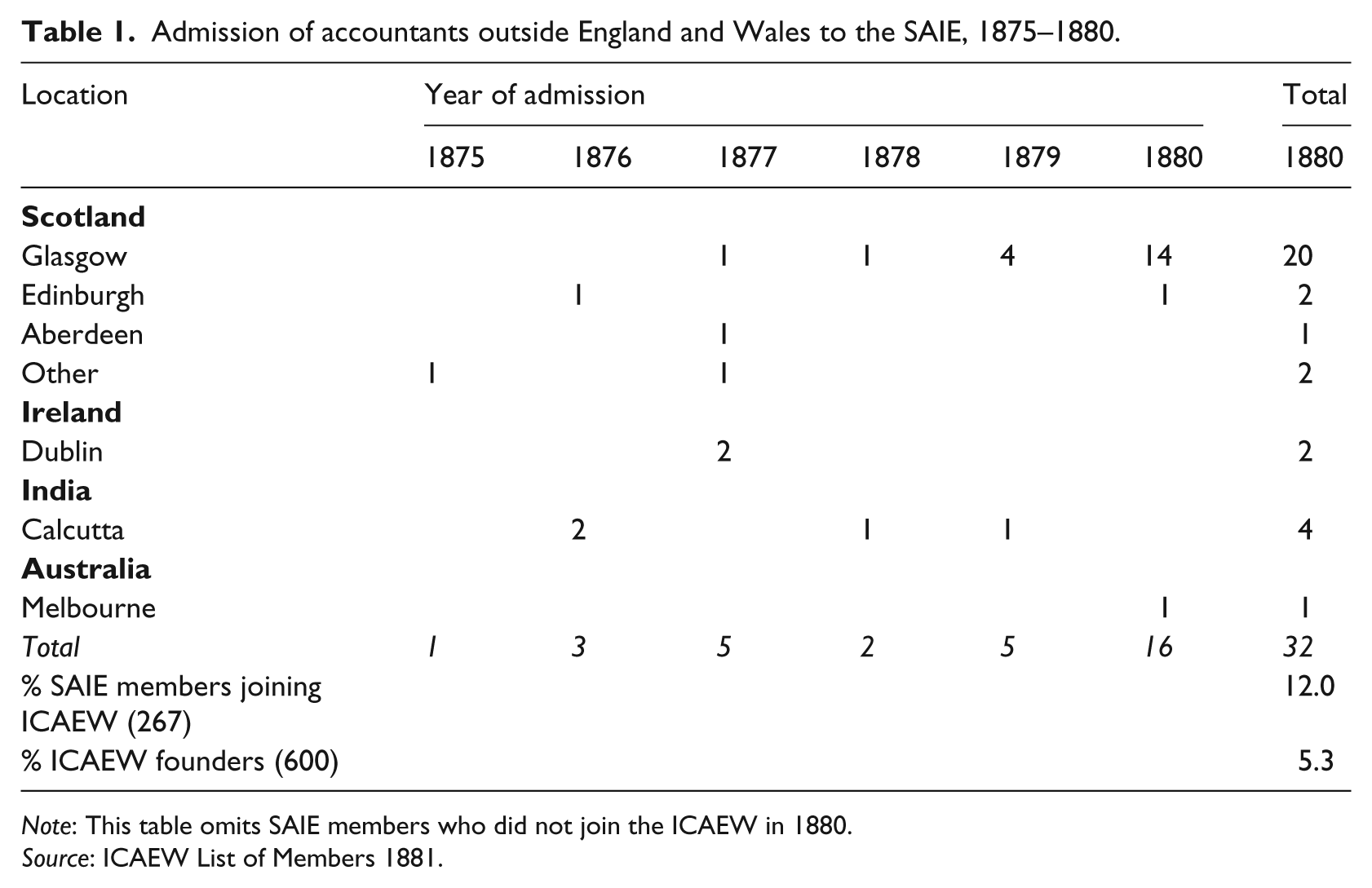

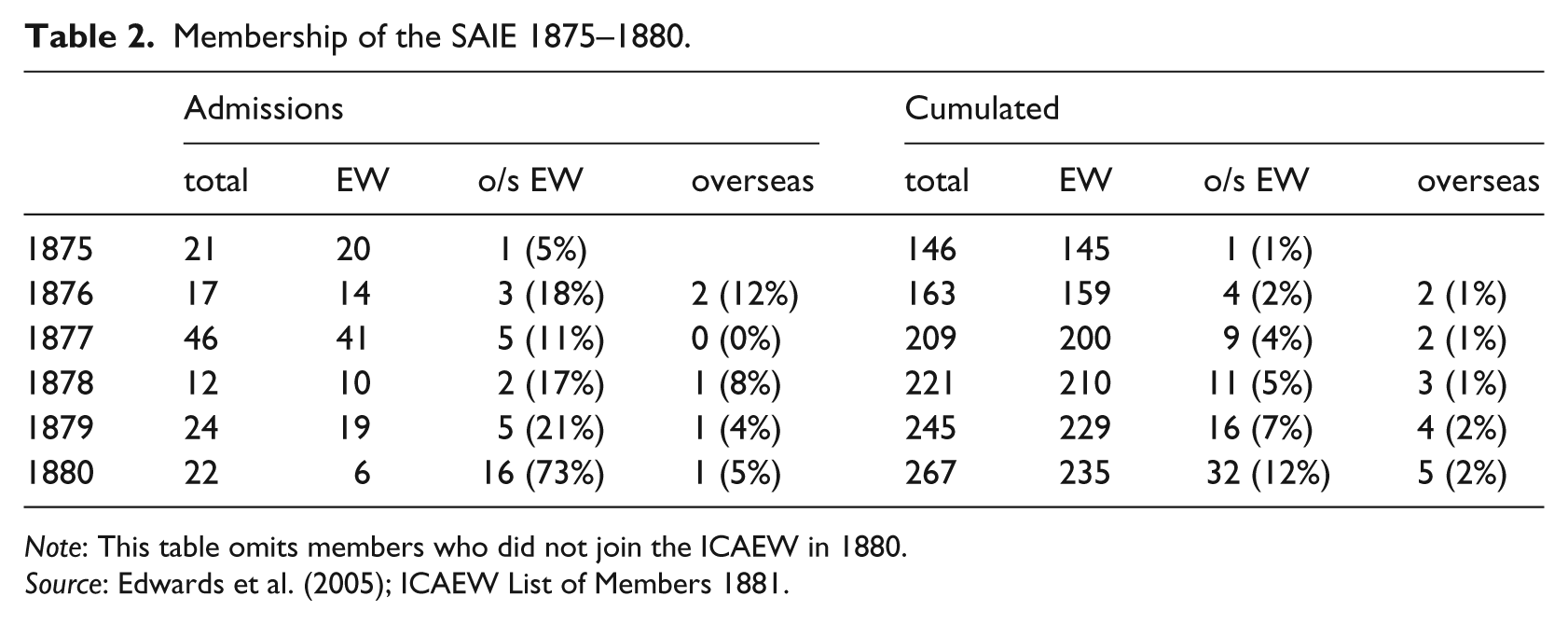

The ICAEW was established by the merger of five bodies based in EW: the (London) Institute of Accountants, the Incorporated Society of Liverpool Accountants, the Manchester Institute of Accountants, the Sheffield Institute of Accountants and the SAIE. According to Boys (2004), on its foundation date of 11 May 1880 the ICAEW had 600 members, 267 of whom were former members of the SAIE and 188 were former members of the (London) Institute. None was a member of both these bodies, but 23 of the members of the SAIE were also members of the other three bodies. The first List of Members (1881) shows that all 32 of the members outside EW had joined by virtue of membership of the SAIE. Details of the 32 are given in Appendix 1 and summarised in Table 1. The table shows that 66 per cent of them were admitted in 1879 or 1880. To put this in context, the percentage of members admitted in these years was high in all the predecessor bodies, ranging from 15 to 46 per cent (Edwards et al., 2005: Table 1). In 1880 the 32 were resident in four very different parts of the British Empire: 25 in Scotland, two in Ireland, four in India and one in Australia. Table 2 compares the total admissions to and membership of the SAIE with its membership outside EW and overseas. It shows a steady increase in both of the last two. At the date of the merger, 235 (88%) of the members of the SAIE were located in EW. Of the 32 outside EW, 27 (10%) were located within other parts of the UK, and five (2%) outside the UK. Thirty-two is a small number but as a comparison the Liverpool Society brought only 31 members into the new ICAEW and the Sheffield Institute only 33 (Boys, 2004: 39). Moreover, there were more members outside EW than there were in Wales.

Admission of accountants outside England and Wales to the SAIE, 1875–1880.

Note: This table omits SAIE members who did not join the ICAEW in 1880.

Source: ICAEW List of Members 1881.

Membership of the SAIE 1875–1880.

Note: This table omits members who did not join the ICAEW in 1880.

Source: Edwards et al. (2005); ICAEW List of Members 1881.

The import and export of qualifications is one way by which professional accountancy can spread globally. Johnson and Caygill (1971) were the first to highlight its importance, writing mainly from the point of view of the exporters (but ignoring the SAIE). Parker (1989), in a paper which extended the export/import terminology to accounting techniques (such as double entry bookkeeping) and accounting concepts (such as a true and fair view) as well as accounting institutions, distinguished the export of qualifications from the physical transfer of accountants from one country to another and from the import of professional accountancy as an idea implemented by local accountants. Later writers have concentrated on the impact on professional accountancy in countries within the Empire of importing by all three methods. Briston and Kedslie (1997) argued that the influence of the British accountancy profession overseas has been changed significantly by the export of qualifying examinations rather than accountants. Carnegie and Parker (1999a) found that in the settler colonies of Australia the formation of local bodies was more influenced by the import of the idea of professional accountancy than by accountants, immigrant or native-born, with British qualifications. They quoted approvingly the view of The Accountants’ Magazine (June, 1901: 285) that “colonial accountants should be encouraged, and if need be assisted to form their local associations. … But we rather suspect that [they] have shown themselves capable of organising without assistance”. By contrast, Annisette (1999) found that in the non-settler colony of Trinidad and Tobago, even after independence, British qualifications, whether held by expatriate Britons or imported by Trinidadians, retained an advantage over local qualifications. Both Carnegie and Parker (1999a) and Annisette (1999) discussed the actions and motivations of named individual accountants. The latter, following Briston and Kedslie (1997), has stressed in later papers (e.g. Annisette, 2010) that the availability of an “imperial” qualification, however distinguished, may discourage local bodies rather than encourage them.

This article is written from the perspective of the accountants resident outside EW rather than from that of the SAIE as exporter. The first part explains how these accountants were given the opportunity in the 1870s to import an English qualification and what incentives there were for them to take advantage of the opportunity. The second part of the article discusses the impact of the 32 in their countries of residence, and in particular their involvement with accountancy bodies other than the ICAEW. The sources for both parts of the article include lists of members and histories of accountancy bodies, histories of accountancy firms and obituaries.

Obituaries, as Fowler (2007) demonstrates, help to determine who is remembered and what is remembered, and provide a “selective ‘justification’ of certain individuals at death” (2007: 41). No less than 13 (41%) of the 32 were deemed sufficiently important to receive obituaries in one or more of the three leading professional journals of the period: The Accountant (first published 1874 and the unofficial journal of the ICAEW from 1880), The Incorporated Accountants’ Journal (IAJ) (the official journal of the SAA from 1889) and The Accountants’ Magazine (TAM) (the official journal from 1897 of the Scottish chartered bodies in Edinburgh, Glasgow and Aberdeen). These obituaries are listed in Appendix 2. Who was included in the obituary pages and who was excluded depended on the editorial policy of each journal, which was heavily biased towards members of the body that they represented. TAM, which published obituaries of three of the 13, covered two of three who became members of the Glasgow Institute, plus one who was a partner of an Institute member. The IAJ, which published obituaries of nine, covered all seven who eventually joined the SAA (see Table 4 below) plus two others who had declined an opportunity to join the SAA. The Accountant’s policy is harder to discern. It published obituaries of only five of the 32, but three of them (none members of the SAA or the Scottish chartered bodies) were not obituarised in the other journals. The contents of the obituaries are as interesting for what they exclude as for what they include. For example, none of the obituaries revealed that its subject was ever a member of a body called the Society of Accountants in England.

Opportunities to import

The initiative of the SAIE

In 1875 accountants outside EW, resident in Scotland, Ireland, India, Australia and elsewhere in the British Empire, were given the opportunity to apply for admission to the SAIE. At its third AGM in May of that year, the SAIE became the first body explicitly to decide to export its qualification. At the meeting, John Bath, the vice-president, proposed the resolution: “That the council of this Society be empowered to receive applications from, and admit as members of the Society, persons who may reside in Great Britain, or any of the dependencies of the British Crown”. The resolution was passed after a brief discussion in which Bath stated that the reason for it was that, because of the word England in the name, “an accountant in Scotland or Ireland might take it for granted that he was not eligible for election”, and it was revealed, amid laughter, that an application had been received from Hong Kong (The Accountant, 15 May 1875: 7).There is no surviving documentary evidence as to why the SAIE sought members outside EW. The council perhaps hoped to take advantage of a pent-up demand created by the exclusionary policies of the Scottish chartered bodies, thus achieving extra revenue or an enhanced status. It is noteworthy that the text of the resolution refers to Great Britain rather than the UK. It seems probable that Scotland was expected to be the source of most applications. Then, as now, an Englishman could more readily than a Scotsman envisage the term “England” as covering both countries. Ireland is treated as a dependency of the British Crown rather than as part of the UK. The rest of the British Empire was perhaps an afterthought. Nevertheless, the resolution has, in accordance with the spirit of the times, an unashamedly imperial ring and contains a recognition that many of the Empire’s inhabitants might be regarded as “English”.

Empire and diasporic identity

The British Empire was a complex polity and already the largest and most geographically widespread empire ever known. It was centred on the United Kingdom and the imperial capital, London. The UK of the 1870s and until after the First World War had three components (EW, Scotland and an unpartitioned Ireland) with very different characteristics. EW had much the largest population and economy: 26 million in 1881, for example, compared with 5 million for Ireland and 4 million for Scotland. The principality of Wales was subsumed within EW. Annexed to England in 1536, it had not retained its own legal system. In 1707 the Act of Union had abolished the Scottish parliament, and EW and Scotland were joined together as the United Kingdom of Great Britain. Scotland retained its own legal and educational systems but was increasingly integrated with the English (and Welsh) economy. Crucially for nineteenth-century accountants, the rules relating to bankruptcy and insolvency were not the same. The Irish relationship with England was very different from that of Scotland. Ireland was more of a dependency and not part of the Union until 1801. The Act of Union of 1800 abolished the Irish parliament and created a United Kingdom of Great Britain and Ireland. Ireland was not partitioned until 1922.

The late Victorian overseas empire, its components brought closer together by the steamship and the electric telegraph, was an empire of subject peoples, migrant settlers and expatriates (Richards, 2004; Bickers, 2010; Harper and Constantine, 2010). Peopled by migrants from the UK, the settler colonies (such as Victoria, of which Melbourne was the capital city) had the power to enact and enforce their own domestic legislation. Many in these colonies did not regard themselves as any less British or English because they were not living in the “mother country”. They saw themselves as part of the “imagined political community” of a “Greater Britain” (Bell, 2007: 171), an idea popularised by Sir Charles Dilke in his book of that title published in 1869. Being British outside the UK meant not just acceptance of the superiority of British-style institutions but also a claim to set up institutions such as accountancy bodies of similar standing and equal rights to those in Britain, and to support them by local legislation. By contrast, the non-settler colonies were ruled directly by British officials, backed up by force if necessary. India was by far the largest non-settler colony and large numbers of British civil servants, soldiers and merchants were employed there.

Who was considered to be “English” by the inhabitants of England changed during the nineteenth century. They began to regard “English” and “British” as synonymous terms and an expanded notion of English identity emerged. By the late nineteenth century “Englishness” had been “translated from the national identity of the English living in England into a diasporic identity beyond any geographical boundaries which included all the English who had now emigrated all over the globe” (Young, 2008: 231). “England” was extended (by most English people, but not by most Scots and Irish) to mean, loosely, Great Britain (EW and Scotland), the UK (Britain plus Ireland), or even the British Empire (especially the settler colonies). This enabled English accountancy bodies, beginning with the SAIE, to see themselves, if they so wished, as providing a qualification for all “English” people within the Empire. All of the 32 could, if they so wished, be regarded and treated as “English”. The SAA was using this definition of Englishness when in its Seventh Annual Report it applauded clause 40 of the 1890 Local Government Act of the Australian colony of Victoria as “the first statutory recognition of the Accountancy profession in England” (SAA,1891: 7, italics added; see also Carnegie and Parker, 1999a). It took longer for “Englishness” to be extended to “natives” in non-settler colonies. The first Indian (Kalyan Subramani Aiyar) was admitted to membership of the SAA in 1890 (Obituaries, 1940). The SAA was more interested in expansion in the settler colonies of South Africa and Australia.

Incentives to import

Inclusion and exclusion

This and the following sections of the article make use of the concepts of inclusion and exclusion as introduced by Weber (1968) and developed by later writers such as Parkin (1979), Murphy (1984, 1986, 1988), Witz (1992) and Macdonald (1995). These ideas have been explained and elaborated in an English professional accountancy context by Anderson et al. (2005). In the present article they are applied to individual accountants as well as accountancy bodies. In order for their qualifications to be worth acquiring, all would-be professional bodies have to pursue exclusionary recruitment strategies to a greater or lesser extent. Exclusion from membership of elite bodies can be achieved by restricting membership to those persons acceptable to existing members in that they are known to be reputable and to possess a minimum technical competence. This is more achievable if the body is local, so that aspiring members are easily observed; if aspiring members are apprenticed to existing members; and if they have parents who can afford to pay a substantial premium in advance and support their sons financially during the period of apprenticeship. Localism also makes it easier to set and administer examinations but none of the pre-1880 English bodies subjected applicants to them, being concerned more with recruiting established accountants (of varied merit) than establishing training criteria for newcomers. This meant that importers of the SAIE’s qualification, whatever their location, were able to seek and gain admission quite quickly, in spite of problems of distance.

If they become too exclusionary, elite bodies risk loss of control of the market for their professional services by failing to admit to membership a sufficient proportion of the total number of the suppliers of those services. On the other hand, a more inclusive strategy risks the admission of marginal practitioners (Macdonald and Ritzer, 1988: 257–258). Elite bodies are attractive to those individual accountants able to fulfil the admission requirements. Those not able to do so have incentives to set up or join competing bodies. The establishment of such bodies is possible within the British tradition of autonomous, self-regulating groups of professionals, largely independent of state control, and acting as qualifying associations (Millerson, 1964). They are likely to include a wider spectrum of members than elite bodies. Although they may fail to exclude some of the less reputable and the less competent, they may also include, and give an opportunity to, reputable and competent accountants unable to join the elite bodies for financial reasons or because they are practising in the wrong locality. The widening of a catchment area can signal not just the end of localism but also the establishment of a “pecking order” of professional qualifications, with the more exclusionary bodies at the top and the less exclusionary bodies below. The pecking order is not static. All bodies not at the top and their members, in order to maintain their place in the pecking order, have to follow a “dual exclusionary/ inclusionary” strategy, striving for inclusion upwards but also for exclusion downwards. Bodies at the top, especially those with relatively few members, may be challenged by, or in danger of being merged with, a body lower in the pecking order.

The names of the accountancy bodies in Edinburgh, Glasgow, Aberdeen, Liverpool, London and Manchester established by the early 1870s proclaimed their localism (Parker, 2005: 21). There was, it could be argued, room for competing bodies aiming at a wider geographical coverage, less exclusive admission policies and willing to take the risk of the admittance of marginal practitioners. The coverage could be restricted to either Scotland or EW or, more ambitiously, extended to all of Britain or the UK, or even to the whole British Empire. No competing bodies were formed in Scotland before 1880, even though, as Kedslie (1990: 185) points out, the “the new profession [in Scotland] was scarcely open to young men other than those from a professional or socially privileged background”. It was, of course, not open to any young women at all. In EW, the first three bodies founded in the early 1870s followed the same route (Anderson et al., 2005). The body that in 1872 deliberately broke with the traditions of localism and highly exclusionary admission policies was, as we have seen, the SAIE, which was to play an important if rather “underdog” role in the emergence of an organised accountancy profession covering the whole of England and Wales (Walker, 2004a, 2004b).

The admission requirements of the SAIE were much laxer than those of the Institute of Accountants in London and the other local bodies. The Institute required associates to have been in practice in London for five consecutive years as a public accountant or to have been clerk to a member for five years. Entry fees were high. In contrast, membership of the SAIE was open to accountants throughout EW, including those employed by a corporation or public body; only three years of experience were required; and the fees were only about a third of those demanded by the Institute (SAIE, 1879b). The admission requirements (but not the entry fees) of all five bodies are summarised by Anderson et al. (2007: 386–387). As Walker (2004b: 129) succinctly observes, the Institute’s rules “discouraged growth”. The London body responded to the SAIE in 1872 by changing its name from London Institute of Accountants to Institute of Accountants, but its maintenance of a highly exclusionary admissions policy meant that it grew slowly: from 134 in 1871 to 178 in 1879 (Walker, 2004b: 129). By contrast, its inclusionary membership policy enabled the SAIE to grow quickly, if unevenly, reaching 245 in 1879 (omitting members who did not join the ICAEW in 1880: see Table 2). By the end of the decade, both the Institute and the SAIE had more members than the Society of Accountants in Edinburgh, the largest of the Scottish bodies (ICAS, 1954: 173). When the localised elite EW bodies sought state recognition of a national body, the SAIE was large enough and covered sufficient of EW for its members not to be left out of the merger (Walker 2004a, 2004b; Edwards et al., 2005). However, one fifth of the former SAIE members were subsequently expelled from the ICAEW. These included John Bath, the proposer of the 1875 resolution, but only one member (William Nicholls in India) outside EW (Chandler et al., 2008).

An analysis of the 32 accountants who are the subjects of this article shows that the incentives to import the SAIE qualification varied from country to country. For the seven accountants in Ireland (Kevans and Kean), India (Browne, Nicholls, Ross and Young) and Australia (Flack), the incentives to join the SAIE were different from those of the Scots. Although the idea of professional accountancy and an awareness of the advantages of membership of a professional body and of a professional designation had already spread to these three countries, no local bodies had yet been established. If one were to be established in the future, it could be an advantage for intending applicants to hold a qualification imported from the imperial centre. This incentive was weaker for the 25 accountants based in Scotland, where the existing bodies were well entrenched and a qualification imported from England would be lower than theirs in the local pecking order. We now look at the accountants of each country in turn.

The Scots

None of the 25 Scottish accountants admitted to the SAIE was a member of one of the existing Scottish chartered bodies, although Hoey had been admitted to the Institute of Accountants and Actuaries in Glasgow (IAAG) in 1870, had resigned in 1873 and was refused reinstatement in 1879 (Stewart, 1977: 91; Kedslie, 1990: 227). It is likely that most of them were unable or unwilling to meet the stringent conditions for membership, especially unpaid apprenticeships and high indenture fees (premiums). Edwards and Walker (2007: 83), using 1881 census data, show that, as measured by the number of their “live-in” servants, they were lower in status, income and wealth than members of the chartered bodies. The 19 of them who were also members of the Scottish Institute of Accountants (SIA) (see below) in 1881 employed on average 1.5 domestic servants per household, whereas members of the IAAG employed 2.4 servants on average. The early joiners of the SAIE may have been attracted by that body’s appeal to accountants outside the big cities. They did not come predominantly from Glasgow or Edinburgh, but from the smaller towns of Aberdeen, Ayr and Fraserburgh. Of these, Alexander McConnachie of Aberdeen was refused admission to the Aberdeen Society of Accountants in December 1876 on the grounds that his experience of four years in an advocate’s office did not fulfil the admission requirements of the Society (Kedslie, 1990: 210). He was admitted to the SAIE on 28 November 1877. James Robertson Grant, who worked for the Bank of Scotland in Aberdeen and later in Fraserburgh, was probably the first Scottish member of the SAIE, being admitted on 28 July 1875.

Those admitted in 1879 and 1880, however, were mainly from Glasgow. Their later actions (see the Impact section below) suggest that, unable to join the existing Scottish bodies, they sought a “chartered” designation, preferably a Scottish chartered designation, and saw membership of the SAIE as a stepping stone thereto. The English accountancy bodies, including the SAIE, did not originally seek incorporation by royal charter but by July 1879 it was clear that this was the most likely route (Walker, 2004b: ch. 12). The dates on which the Scots were admitted to the SAIE and their geographical distribution are revealing. As Table 1 and Appendix 1 show, six were admitted before 1879, four in 1879 and 15 in 1880, six of them as late as 28 April of that year. There were 20 Scottish SAIE members based in Glasgow in 1880, compared with only three on 1 January 1879, one of whom, James Sdeuard (a variant spelling of Steuart), did not join the ICAEW. There were only two from Edinburgh, Scotland’s capital and second largest city: John Macfarlane Cook who joined the SAIE in 1876 and Robert Murdoch Rose who joined at the last moment on 28 April 1880. Both were in practice (Walker, 1988: 76), although Rose’s address in the ICAEW List of Members is always given as H.M. Register House. A partial explanation of the disparity between the Glasgow and Edinburgh SAIE membership numbers is that, whereas in 1880–81, according to the post office directories, there were 26 per cent more CAs than non-CA accountants in Edinburgh (117 as against 93), in Glasgow there were 164 per cent more non-CA accountants than CAs (282:107) (Kedslie, 1990: 183, 199).

The names of all the 22 Glasgow and Edinburgh members (but not those in other Scottish locations) can be found in The Edinburgh Gazette of the 1870s as trustees and commissioners of sequestrated estates. One (Davies) moved to London in 1897, one (Brown) emigrated to South Africa in 1884, but the others did not stray far from their office addresses in 1881.

The Irish

The accountancy landscape in Ireland in the mid-1870s was quite different from that in Scotland. Compared with Scotland, Ireland had a larger population but a much weaker and less industrialised economy. There were fewer accountants. Many had already imported the idea of professional accountancy but there was no professional body from which anyone could feel or be excluded from and as yet no move to establish one. Leading Irish accountants saw little need to join a body such as the SAIE. It attracted only two of them, John Morris Kean and Edward Kevans (1837–1920), who were in practice together in Dublin and were admitted to membership in 1877, Kean probably following the lead of his partner. Although the SAIE in London may have regarded Kevans as somehow “English”, he was, like most Dubliners, an Irish Catholic, but practising a profession which even in Dublin was dominated by Protestants (Annisette and O’Regan, 2007).

India and Australia

As at 1 January 1879, three members of the SAIE were working in the non-settler colony of India and none in the Australian settler colonies. These numbers had increased by May 1880 to four in India (all in Kolkata – then called Calcutta and the capital of British India) and one in Melbourne, Victoria. All were Englishmen who had gone out as expatriates or migrants. With numbers so small, SAIE membership overseas cannot be shown not to have been random, but India and Australia were, in the 1870s and until the end of the century, the top recipients of British investment in the Empire (Stone, 1999) and the membership lists show that they remained the main destinations of ICAEW members within the overseas Empire throughout the 1880s and 1890s.

Within that Empire, an English qualification had high status, but faced varying degrees of local competition. In the non-settler colonies the imperial power gave little support to local accountants (as distinct from expatriates) and an importer of an English qualification might be seen as an instrument of imperialism rather than as an importer of professionalism. In the increasingly self-governing settler colonies, however, the colonists regarded themselves as entitled to set up their own local versions of the bodies that had been set up in Britain and to receive the support of their colonial governments. In principle, they had no need to import a qualification. They could devise their own, modelling them on British precedents. There were thus more incentives to join an English body in India than in Australia. In India there was little competition from local accountants and English accountants were expatriates, who expected to return home. In Australia they faced local competition and were more likely to be migrants who intended to settle permanently, although possibly retaining professional contacts in England and wanting to keep open the option of returning there. Moreover, some Australian accountants might regard local qualifications as lower in the pecking order than an imported imperial qualification. Or they might see advantages in acquiring both a local and an imported qualification, in that the latter might appeal to overseas investors in Australia and be more widely accepted than an Australian qualification in other parts of the Empire.

The four SAIE members in India were William Nicholls (admitted in 1876), William Adolphus Browne (1876), Gilbert Grange Ross (1878) and Frederick Maxwell Young (1879). Ross worked for the Indian Government Dockyard, Young for the Bank of Bengal. The only Australian member of the SAIE, Joseph Henry Flack (c1849–1918), emigrated to Melbourne, Victoria, in 1874, as a young man of 25, having been on the staff of Price Waterhouse in London since 1870 (Carnegie and Edwards, 2001). He joined a firm that had been founded by Thomas J Davey in 1872, becoming a partner in 1879. He was admitted to the SAIE at the last possible moment, on 28 April 1880 (just 13 days before the grant of the royal charter to the ICAEW on 11 May), perhaps recommended to do so by his London contacts.

It is certain that Browne and Flack were already overseas when admitted to the SAIE. The lack of surviving membership records before 1879 means that one cannot be absolutely certain about Nicholls, Ross and Young. It is probable, however, that all five first exported themselves and then imported an English qualification. This “exotic flower of imperial accountancy” (to adopt the phrase of one of the referees of this article) did not become the norm. For example, the two accountants who succeeded Browne as resident partners in his firm in Calcutta were admitted to the ICAEW in London in June 1880 before going out to India in 1881 and 1883 respectively (see “Expatriates in India” in the Impact section below).

Impact of the 32 outside England and Wales after 1880

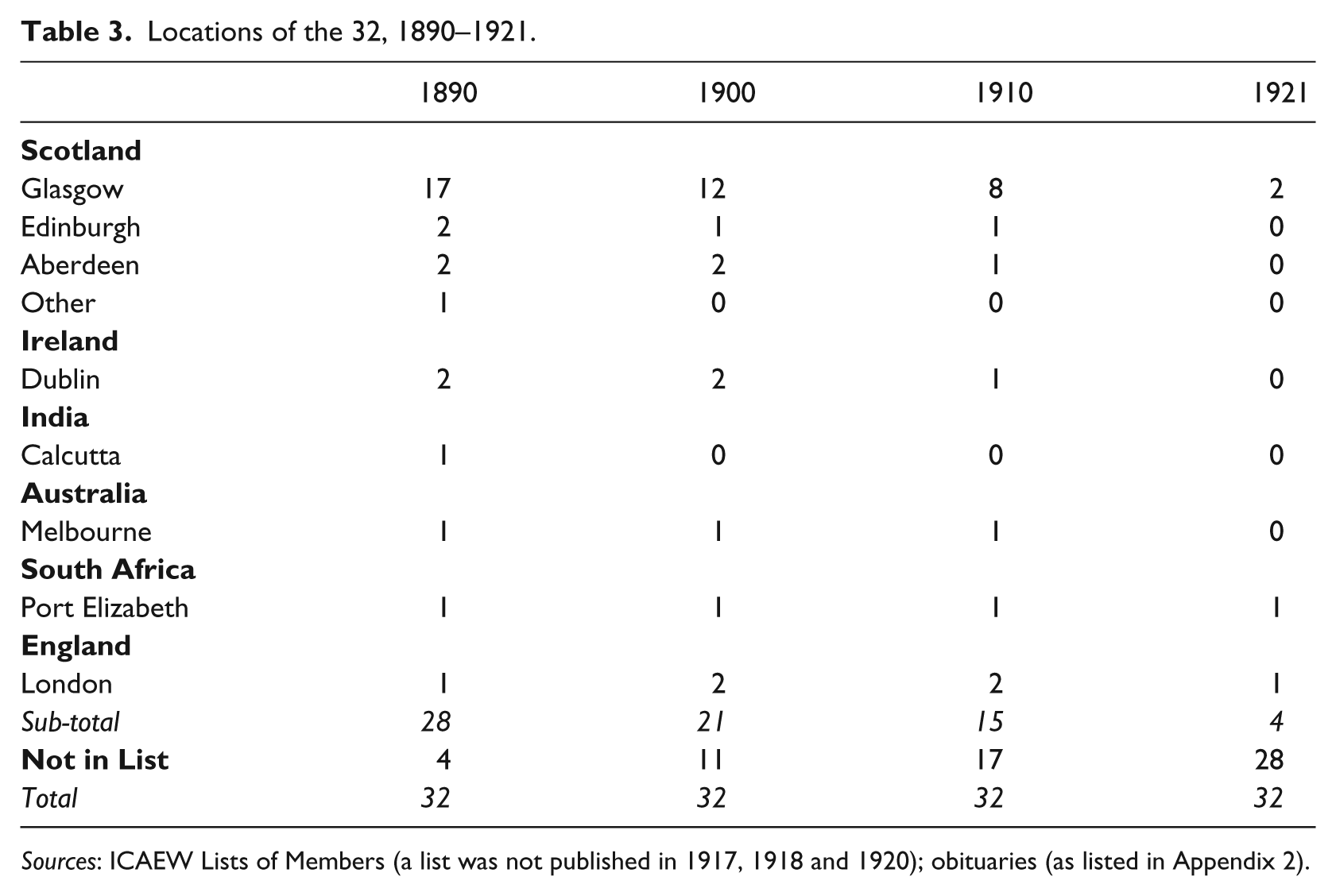

Table 3 shows that most of the 32 (with the exception of those in India) did not relocate but stayed where they were in 1880. The table, based upon a search of later volumes of the ICAEW Lists, summarises the locations of the survivors of the 32 over the next 40 years. It shows also the pattern of the inevitable decline in their numbers over time. Only two are recorded as ever resident in England after 1880 and only one moved between two countries outside EW (from Scotland to South Africa).

Locations of the 32, 1890–1921.

Sources: ICAEW Lists of Members (a list was not published in 1917, 1918 and 1920); obituaries (as listed in Appendix 2).

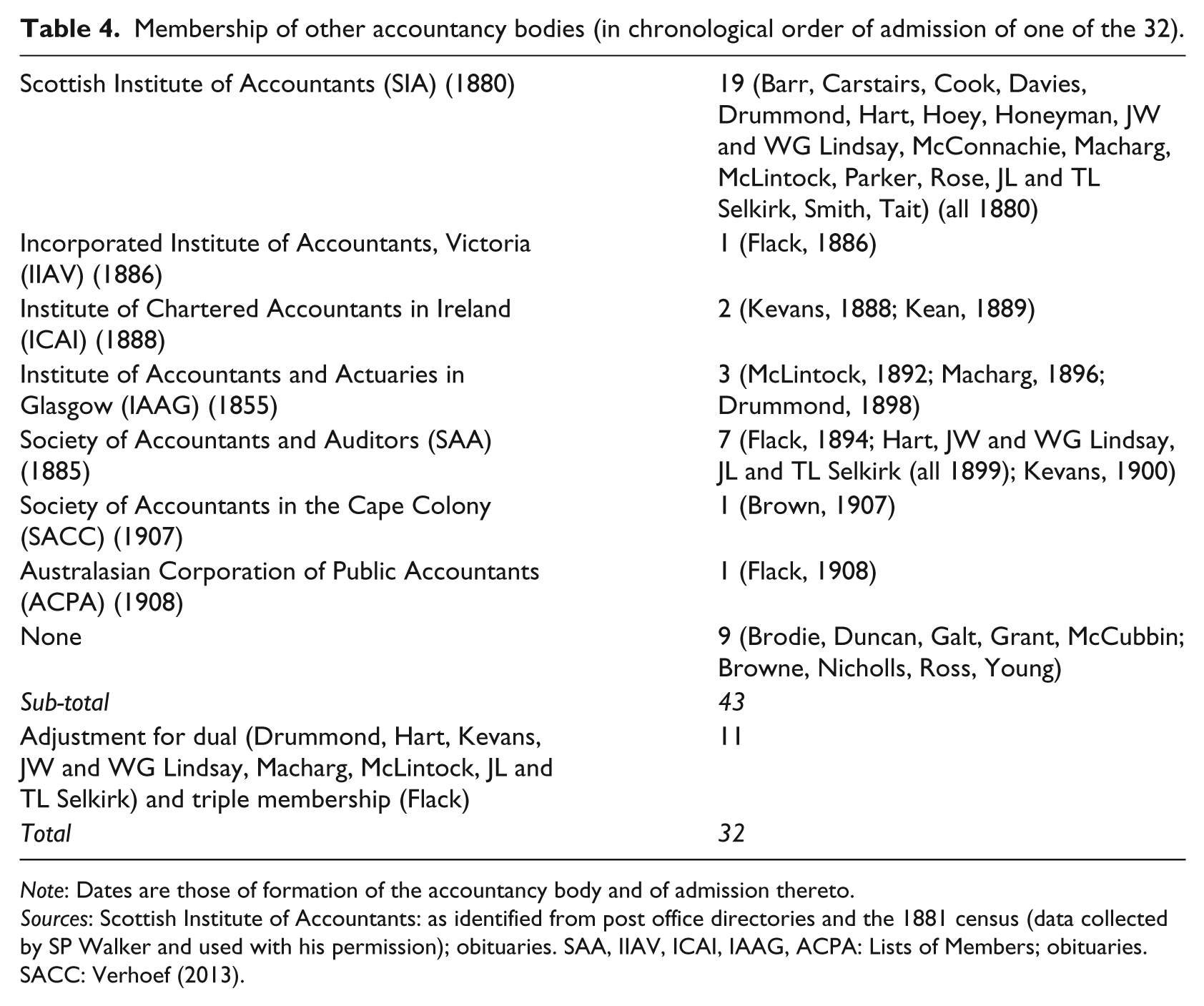

Staying in one place does not mean that the 32 were inactive or could sensibly remain so. After 1880, former members of the SAIE in EW were members of a body at the top of the pecking order and which was taking active steps to remain there (Anderson et al., 2005). Outside EW, however, ICAEW members were not necessarily at the top of the pecking order and this affected the decisions of the 32 to join other bodies or help to set them up. The story of the 32 after 1880 is one of both success and failure. The impact in Scotland is a good example of the struggle by individuals for upward inclusion and downward exclusion; in Ireland of the effect of one individual on a small stage; in Australia, South Africa and India of the differing trajectories of professionals in settler and non-settler colonies. As shown by Table 4, 23 of the 32 were involved in the foundation of (and in some cases were council members and office holders of) new accountancy bodies: in Scotland, Ireland, Australia and South Africa, but not, for reasons explained below, in India. Most accountants have little impact, positive or negative, on their profession. Those in at its beginnings have more chance to do so, not only by helping to found new bodies, but by striving, even with little success, to change the structure and composition of the profession (e.g. Selkirk in Scotland and Kevans in Ireland); founding or building up successful and long-lasting firms (especially McLintock in Scotland and Flack in Australia, with the help of their sons; and Browne in India); featuring in leading legal cases (Kevans); or contributing modestly to the literature (Kevans and Selkirk). A crude measure of impact is the publication of obituaries by the leading professional journals. As already mentioned, 13 of the 32 were considered worth an obituary; one, Thomson McLintock (Glasgow) received three; Edward Kevans (Dublin) and Michael Honeyman (Glasgow), two each; the other 10, one each.

Membership of other accountancy bodies (in chronological order of admission of one of the 32).

Note: Dates are those of formation of the accountancy body and of admission thereto.

Sources: Scottish Institute of Accountants: as identified from post office directories and the 1881 census (data collected by SP Walker and used with his permission); obituaries. SAA, IIAV, ICAI, IAAG, ACPA: Lists of Members; obituaries. SACC: Verhoef (2013).

Upward inclusion and downward exclusion in Scotland

As already noted, whereas in EW former members of the SAIE, as members of the ICAEW, became members (albeit rather lowly members) of a body at the top of the national pecking order, this was not the case in Scotland, where the chartered bodies in Edinburgh, Glasgow and Aberdeen were still in top place. For most of the 25 Scottish accountants who became entitled to call themselves (English) chartered accountants in 1880, membership of the ICAEW appears to have been regarded as a first step to becoming a Scottish chartered accountant. According to the obituarist of McLintock and Hart (Obituaries 1920): “On June 17th, 1880, about two dozen gentlemen, all Scottish, and mostly Glasgow, who had not long previously been admitted Associates of the Institute of Chartered Accountants of [sic] England and Wales, met in Glasgow and decided to form the Scottish Institute of Accountants”. Census records suggest that there were in fact 19 of them (listed in Table 4). The date of formation was five weeks after that of the ICAEW. All but three (Barr, Cook, and McConnachie) of the 19 had joined the SAIE in 1879 or 1880 and all but three (Cook, McConnachie and Rose) were located in Glasgow. To expand they had to recruit other Scottish accountants, both within and outside Glasgow. The census shows nine new members by 1881. Although the former SAIE members were entitled to the designation “ACA”, they could not become fellows (“FCAs”) unless they practised in EW. Their preferred designation was “CA”, of which the members of the Glasgow Institute and the Edinburgh and Aberdeen Societies claimed a monopoly. The obituary notices of Honeyman (1908), TL Selkirk (1909) and Hart (1920) in The Incorporated Accountants’ Journal even up to 40 years later use the CA designation for accountants who were not members of the Glasgow Institute (see also Walker, 1991: 262). The Accountants’ Magazine noted the death in 1908 of Honeyman (probably because he was a partner of Drummond who had been admitted to the IAAG in 1898), but called him simply an “accountant”, even though he was a member of the ICAEW. The minutes of SIA council meetings have not survived, but according to the obituarist writing in the IAJ in 1920, one of their first resolutions was that the use of initials to designate their membership of the ICAEW was “undesirable” (Obituaries, “Two Glasgow Accountants”, 1920). The long but unsuccessful fight of the SIA to obtain a charter has been chronicled and analysed at length by Walker (1991). Faced with strong opposition from the Edinburgh and Aberdeen Societies and the Glasgow Institute, the SIA failed three times in this attempt and became instead the Scottish branch of the SAA in 1899. Only five former SAIE members of the SIA (the two Lindsays, the two Selkirks and Hart) continued as members of the SAA.

To attract desirable members of the SIA, the chartered bodies relaxed their apprenticeship and examination rules in the 1890s. Sixteen of the Glasgow members of the SIA who had been in public practice for more than 10 years were admitted to the Glasgow Institute. Only three of them (Thomson McLintock, in 1892; Ebenezer Simpson Macharg, in 1896; and James Drummond, in 1898), were former members of the SAIE. One (not a former member of the SAIE) was admitted to the Aberdeen Society; none was admitted to the Edinburgh Society (Kedslie, 1990: 226–227).

The two of the 25 with the greatest influence (in different ways) on the profession in Scotland were James Landells Selkirk (1838–1904) (Obituaries, 1904) and Thomson McLintock (1851–1920) (Obituaries, 1920; Winsbury, 1977). Selkirk, never a member of the IAAG (his son was admitted in 1896), established himself, in partnership with his younger brother Thomas (1844–1909), as a successful practitioner in Glasgow and was a council member of the SIA from its formation. He became its Secretary after the failure of its first royal charter application in 1884 and was closely involved in the two later applications, which also failed. He continued as Secretary when the SIA became the Scottish branch of the SAA in 1899 and became one of the Scottish representatives on the council of the SAA in London. His laudatory obituary (1904) in The Incorporated Accountants’ Journal describes how “carefully … he husbanded the resources, moral and monetary, of the Scottish institute, and how bravely he bore the brunt of struggle”. It was, however, a struggle that failed, and served to confirm the dominance of the three chartered bodies. The SAA was to achieve greater success in South Africa and Australia than in Scotland. Not surprisingly, Selkirk received no obituary in The Accountants’ Magazine. His death also went unrecognised in The Accountant.

Selkirk’s contribution to the professional literature, “Some notes of the nature and scope of the work of a professional accountant” (The Accountant, 14 Sept. 1901), three years before his death, illustrates dual exclusion and inclusion, the simultaneous striving for inclusion upwards and exclusion downwards. The material in the paper on the work of a professional accountant could equally have been written by a Scottish chartered accountant. The paper concluded with the comment that “the various Institutes and Societies now embrace within their membership a large proportion of the entire practising members of the profession throughout the United Kingdom, besides many holding important official positions”. Ignoring (perhaps considering it no longer relevant) his own early career, he lamented that there was “nothing to hinder anyone, no matter what his antecedents may have been, to begin business as an accountant” and called for legislation barring such persons from practising. A few years later, the Finance Act 1903, by defining an accountant as “a person who has been admitted as a member of an incorporated society of accountants”, encouraged the establishment of new bodies, including the London Association of Accountants (LAA) in 1904 (Stacey, 1954: 70–71). When the LAA sought to use the designation “Incorporated Accountant, Lon. Asson”, the SAA went to law to prevent them and in 1908 changed its own name to Society of Incorporated Accountants and Auditors (Garrett, 1961: 51–61).

Selkirk’s career contrasts with that of Thomson McLintock (1851–1920), who was undoubtedly the most distinguished of the 32 accountants in this article. He is the only one included in Parker’s (1980) book of leading British accountants. Thirteen years younger than Selkirk, McLintock had worked in Selkirk’s office before setting up on his own at the age of 26 in 1877, in time to benefit from the work created by the collapse of the City of Glasgow Bank in 1878. He was a member, but not a prominent member, of the SIA. He built up his firm to a leading position in both liquidation and audit, and, as already noted, was admitted to the Glasgow Institute in 1892. He was the only one of the 32 to be given an obituary in all three journals. The three obituaries all agree on his high standing in the profession but, not surprisingly, focus on different aspects of his career. The obituary in The Accountants’ Magazine (the one chosen for reproduction by Parker) describes him as one of the most prominent and most respected members of the IAAG, but makes no mention of the SAIE and the SIA and does not explain how and why he became a member of the ICAEW 12 years before his admission to the IAAG. By contrast, the IAJ makes much of the SIA connection, even though McLintock did not join the SAA. The Accountant’s obituary was a slightly amended version of that in TAM.

In an age of family firms the best way for a firm to grow was for its principals to encourage talented children to enter the profession. Here McLintock was very fortunate. His son William (1873–1947, Sir William McLintock, Bt. from 1934), became a leader of the profession in EW as well as in Scotland. Like other sons of the 32, he did not attempt to qualify as an English chartered accountant. He was admitted to the IAAG in 1896. Unlike his father, he had no need to join the ICAEW, but, again unlike his father, he did need to spend much of his time in London, where a thriving office was established. According to his obituary, Sir William “throughout the [First World] war and for some time afterwards … usually worked in London for part of the week and in Glasgow for the remainder, with two nights in the train” (Obituaries, 1947). Thomson McLintock & Co’s strong presence in London (where Sir William moved permanently in 1921) was very much that of a firm of Scottish chartered accountants.

Other Glaswegians had less impact on the profession than McLintock and the Selkirk brothers. Two other brothers, William Giffen Lindsay (1832–1905) and James Walkinshaw Lindsay (Obituaries, 1905, 1914), the sons of a professor of exegetical theology and biblical criticism at the United Presbyterian College in Edinburgh, were in practice together in Glasgow. Both were founder members of the SIA who joined the SAA in 1899. John McQueen Barr (1843–1899) retired early and died early (Obituaries, 1899). James Drummond (1840–1916) and Michael Honeyman (1824–1908) were in partnership from about 1866. In 1898, Drummond (but not Honeyman, by then in his seventies) was admitted to the IAAG. Neither joined the SAA in 1899. David George Hoey, “a well-known citizen of Glasgow” according to The Accountant, died in Chicago in 1891 on a visit to the US to inspect the ventilation of the underground section of the Baltimore and Ohio Railway (Obituaries, 1892). Hart (1839–1920) died in the same year as McLintock and shared an obituary with him in the IAJ (Obituaries, 1920). Unlike McLintock, according to the obituary, he devoted himself to the demands of his large business and “played little or no part in professional movements” in Glasgow.

The story of the Scottish members of the SAIE who became English chartered accountants and who tried, but mainly failed, to become Scottish chartered accountants, is testimony to the strength of the exclusionary strategy of the well-established bodies in Scotland and their determination to hang on to their de facto monopolies. It also illustrates the complex nature of the pecking order in Scotland. To be a “chartered accountant” through membership of the ICAEW was not sufficient. Selkirk, McLintock and the others made use of the concept of English diasporic identity but their actions reveal only Scottishness. They personally made little contribution to the spread of the profession outside Scotland. The SIA’s rhetoric was about a national rather than a local profession but the nation was Scotland not the UK.

Brown and Davies were the only two to move away from Scotland. Davies set up a London office, and that is listed as his primary address from 1897, although he is still listed also under Glasgow. Brown (1853–1927) emigrated to South Africa and was one of the founder members of the Society of Accountants in the Cape Colony (SACC) in 1907 and a member of the Legislative Assembly (1908–1927). His son (1876–1932) of the same name was president of the SACC (1916–18) (Verhoef, 2013; see also Poullaos, 2010: 25). Brown senior did not join the SIA. Nor apparently did Brodie, Duncan, Galt, Grant and McCubbin. Few members of the ICAEW located themselves in Scotland by physical transfer from EW. There were only two of them in 1898, for example. By contrast, a sufficiently large number of Scots CAs went to work in EW to enable the formation in that year of an Association of Scottish Chartered Accountants in London (ICAS, 1954: 45). For four decades former members of the SAIE made up the bulk of ICAEW representation in Scotland, their numbers gradually dwindling. By 1914 only nine were left, equal in number to those who had transferred from EW. By 1921, after the deaths of McLintock and Hart in 1920, only two former SAIE members (McConnachie and Tait) were resident in Scotland.

A maverick in Ireland

Edward Kevans (1837–1920) was an almost exact contemporary of James Selkirk and died in the same year as Thomson McLintock. He joined every accountancy body for which he was eligible: the SAIE in 1877, the ICAEW in 1880, the Institute of Chartered Accountants in Ireland (ICAI) in 1888, the SAA in 1900. When an Irish branch of the latter was set up in 1901 he became its first president. According to his obituary (Obituaries, 1920: 116), however, he denied that he was simply a joiner. He claimed that he joined the SAA (the successor of the SAIE as an exporter of accountancy qualifications to Ireland, but which had only 19 members there in 1900, four of them members of the ICAI), because it favoured a more inclusive approach than that of the chartered bodies.

Kevans’s inclusionary preferences extended to the acceptance of women accountants. Never loath to upset the English and Irish establishments, in 1901 he requested exemption from the ICAI’s preliminary examination for his daughter Cecily, which would have made her potentially eligible for admission as a member of that Institute. Barker (1988), an Irish woman chartered accountant of a later generation, gives a lively account of what happened next:

The members of the Institute, in a bit of a tizz about this application, decided to consult the sister organisation in London [the ICAEW]. London fairly bristled! There was stiff opposition to the notion of allowing a woman into the profession. This probably confirmed London’s belief that the Irish were just a bunch of crackpots. Faced with this formidable opposition, Kevans agreed not to pursue the matter. (Barker 1988: 209; see also O’Regan, 2008: 56, n. 5)

Kevans combined an inclusionary approach with family ambition. He was less fortunate than McLintock in bringing his children into his firm, although he too did not attempt to make them members of the ICAEW. His son Patrick qualified as a member of the ICAI, the firm became Kevans & Son, but Patrick died at an early age. Kevans was later joined in partnership by his clerk T Condren Flinn, a member of the ICAEW (from 1906) and the SAA.

The turn of the century was a busy time for Kevans, then in his early sixties. In 1900 he was the unsuccessful appellant in a leading auditor liability case, The Irish Woollen Company, Lim. v. Tyson and Others (The Accountant Law Reports, 1900: 13). He contributed the section on Irish bankruptcy law to Lisle’s six volume Encyclopaedia of Accounting, published in Edinburgh in 1903.

Kevans died in 1920, having lived through the First World War and the Easter Rising in Dublin of 1916, and witnessed the approach of civil war in Ireland. More positively, he survived just long enough to see the ICAI open its membership to women on equal terms with men (Barker, 1988: 209–210). He was given a short factual obituary in The Accountant and a long one in the IAG, which noted that he resigned his seat on the council of the ICAI in order to sit on the SAA’s council in London. His long career was full of incident but not typical of his fellow founders of the ICAI, an elite group intent on appropriating to itself the economic and social benefits attached to professional status and obtaining a chartered designation for Irish accountants faced with competition from English-based chartered firms and the attempts of the SAA to establish an Irish branch (Hill Vellacott, 1988; O’Regan, 2008: 35, 39–40, 49). Ireland was more open than Scotland to English competition and far more English chartered accountants from EW transferred physically to Ireland than to Scotland. By 1914, for example, there were 17 of them compared to nine in Scotland.

Expatriates in India

None of the four ICAEW members in India (Nicholls, Browne, Ross and Young) joined any other accountancy bodies. As practitioners in a non-settler colony, they had little incentive to encourage the creation of local bodies. Young died in Calcutta on 22 March 1883 (Fibis database). Whether Nicholls and Ross also died in India or whether they returned to England is uncertain, but neither appear in the ICAEW Members Lists after their entries in Calcutta cease after 1881 and 1890 respectively. Nicholls was expelled from the ICAEW in January 1882 as a result of bankruptcy (Chandler et al., 2008: Table III).

William Adolphus Browne (c1846–1915) (Obituaries, 1915; Datta, n.d.) was the only one to leave a mark on the profession in India. He set out for India in 1872 when he was in his twenties, founding what was to become the leading firm of accountants in Calcutta, and hence in India. The firm, now known as Lovelock & Lewes, and part of the PricewaterhouseCoopers network, remains one of India’s largest. In 1881 Browne was joined in partnership by Arthur Samuel Lovelock and in 1883 by John Herbert Lewes (1859–1935), the latter becoming a partner in 1886 (Obituaries, 1935). Both had been admitted to the ICAEW in June 1880. The firm’s name became Lovelock & Lewes in 1889 when Browne, by then in his forties and in practice in London as W.A. Browne & Co, cut his links with the Indian firm. Like Lewes (Obituaries,1935), he was one of many Englishmen of his time who made money in Indian commerce in his youth and, who, if he survived the climate, returned to England in middle age to retire or semi-retire.

Unlike McLintock, Kevans and Flack (see below), Browne does not appear to have encouraged his son into the profession, relying on the recruitment of accountants outside the family. According to his obituary, Browne had been a keen member of, and a lieutenant-colonel in, the Calcutta Volunteer Rifles, an occupation of higher social status in British India than that of a “box-wallah” (Allen, 2008: 84–95). His son Edmond Waller Browne followed him into a military career rather than accountancy, also became a lieutenant-colonel, and married a granddaughter of the 23rd Lord de Clifford.

A migrant in Australia

From the mid-1880s, accountants in the Australian colonies began to set up their own bodies and were also being wooed by the London-based SAA. Migrant chartered accountants were arriving from EW and Scotland (Carnegie and Parker, 1999a). The first president of the Incorporated Institute of Accountants, Victoria (IIAV), established in 1886, successfully opposed the suggestion that that body should become a branch of the SAA and ridiculed the idea “that no good thing can be done here [in Melbourne] unless it bears the seal of a body of gentlemen sitting in London who are unknown to us and to whom we are mostly unknown” (Crellin, 1886). The SAA was more successful in establishing links with local bodies in South Africa (Garrett, 1961: 55–59).

Faced with a multitude of accountancy bodies, Joseph Henry Flack (1847–1918) became an even more prolific joiner than Kevans in Ireland. A member of the ICAEW since 1880, he helped to found the IIAV in 1886, joined the SAA in 1894 (perhaps because his son Edwin was training to become a member) and the Australasian Corporation of Public Accountants (ACPA) in 1908. He was also a corresponding member of the Glasgow Institute. Marshall (1982: 22), the historian of Touche Ross & Co in Australia, comments that few of his contemporaries could boast such impressive credentials. Carnegie and Parker (1999a: 93) suggest that, although he was a founder member of the IIAV in 1886, he probably did not play a primary role in its formation. He was not a member of the committee which considered a proposal to set it up and, although invited, did not attend its first annual general meeting. He did, however, serve from 1886 to 1893 as its first secretary (Macdonald, 1936: 10, 26–27). In his later years he appears to have been regarded as an influential accountant who should be asked to join new bodies but who was not himself active in their establishment. These included the ACPA, a body which had been founded deliberately to exclude accountants not in practice, and which in 1928, ten years after Flack’s death, metamorphosed into the Institute of Chartered Accountants in Australia (ICAA).

Flack lived through both the booming “Marvellous Melbourne” of the 1880s and the crash of the 1890s (which of course also brought work to accountants). He died a few months before the end of the First World War. According to his obituary in the IAJ (1918: 240), before the war he “was in the habit of visiting the Old Country about every two years … and did much to promote the splendid feeling between the Home Country and the Dominions”. This strongly suggests both that, as senior partner of one of Australia’s leading accountancy firms, he was a wealthy man, and that, like many Australians of his generation, he had retained his diasporic English identity. It was on one of these visits that he purchased the nucleus of the IIAV’s library (Macdonald, 1936: 13–14).

Like McLintock, Flack was fortunate in his son, Edwin Harold Flack (1873–1935) (Obituaries, 1935). Born in London just before his father emigrated, Edwin was sent to England to gain experience with Price Waterhouse but not to qualify as an English chartered accountant. Whilst there he not only became a member of the SAA (in 1897) but also, in 1896, the first Australian to win an Olympic gold medal (Jones, 1995: 98). Like William McLintock and Patrick Kevans, he became a partner in his father’s firm (in 1899, the firm’s name changing to Flack & Flack in 1904). Like his father, he became a member of the two local bodies, the IIAV and the ACPA, and thus, from 1928 (when the latter body was granted a royal charter), an Australian chartered accountant.

Concluding observations

From the 1870s and 1880s onwards, accountants throughout EW, the UK and the British Empire were faced with an increasingly wide choice of professional organisations. This article has been written from the perspective of these individual accountants rather than from that of the bodies to which they might seek admission. In particular, it has discussed the opportunities, incentives and impact of the 32 accountants who were the first to join a body outside their own country. They were the forerunners of the thousands of accountants throughout the former British Empire and Commonwealth who have imported and continue to import a qualification from bodies based in London. This is just one aspect, but an important one, of the globalisation of the profession. Importers need an exporter. The export was begun by the SAIE but abandoned by the ICAEW in 1880. Some ICAEW members overseas later lobbied for an export of its examinations, but the London leadership resisted this until the 1920s by which time it was too late, given the opposition, especially in South Africa and Canada, of the local bodies and state agencies. The export of qualifications was, however, successfully revived by the SAA, and embraced later by the LAA (now the ACCA) and other bodies (Johnson and Caygill, 1971; Chua and Poullaos, 2002; Poullaos, 2010). This article has not investigated why the SAIE chose to be an exporter but has focused on the opportunity that that body, with its liberal but increasingly popular interpretation of “Englishness”, gave to accountants within the Empire (including Scotland and Ireland) outside EW. The Scots among the 32, practising in a part of the UK where there were already well-established bodies, sought admission to the SAIE, it is argued, mainly in the expectation of being able to call themselves “chartered accountants” (but not “CAs”). Having achieved this, they were then emboldened to take the lead in forming the SIA, thus challenging the dominance of the existing Scottish chartered bodies. In this they were unsuccessful. Three of them, however, achieved “upward inclusion” into the ranks of the Glasgow Institute, one of whom (Thomson McLintock) is today remembered, paradoxically, as the founder of a leading firm of Scottish CAs with a strong practice in both Scotland and EW, and, eventually, as part of KPMG, throughout the world. Five others, including James Landells Selkirk, established themselves as leading members of the Scottish branch of the SAA. The Irish, with no local body until 1888, were less attracted to the SAIE (or perhaps less aware of the possibility of becoming a member of an English chartered body), with the notable exception of Edward Kevans, who went on to become the champion of the SAA in Ireland. Outside the UK, the expatriate William Adolphus Browne in India and the migrant Joseph Henry Flack in Australia, founded leading firms but operated in very different professional environments. Daniel Brown migrated from Scotland to South Africa to become a founder member of the Society of Accountants in the Cape Colony.

Footnotes

Appendix 1

Members of the SAIE outside England and Wales who were founder members of the ICAEW, classified by location in 1880 and by date of admission.

Appendix 2

Acknowledgements

I am much indebted to the comments of GD Carnegie, JR Edwards, CW Nobes, two anonymous referees, the Guest Editor, and to the unfailing helpfulness of the librarians of the Institute of Chartered Accountants in England and Wales and the information officers of the Institute of Chartered Accountants of Scotland. All in their different ways have helped to improve this article.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.