Abstract

This article shows how accounting and rugby have been used as tools of control. It compares the role of accounting in amateur and professional sport, initially analysing the Fiji Rugby Union’s (FRU) internal documents from the period when Fiji was a British colony and rugby was an amateur sport. During this period, the FRU practised rudimentary accounting since it relied primarily on internally-generated funds and therefore had virtually no public accountability. The FRU board emphasized rugby’s core values and downplayed the importance of money. However, in the professional period, donors require more sophisticated financial reporting and auditing to monitor usage of their grants and evaluate the impact of their investments. The FRU has encountered conflict with its donors due to repeated financial losses and alleged mismanagement. This article reveals that those losses originated in the amateur period through diseconomies of scale, inequitable arrangements for international matches and unsustainable funding models. Rather than helping the FRU to address these underlying problems, powerful stakeholders continue using financial resources and governance structures to control and exploit Fiji rugby.

Keywords

Introduction

This article examines the changing role of accounting (Burchell et al., 1980) in the transition from amateur to professional sport, revealing how accounting enables powerful interests to exert control over sporting bodies. Adopting a historical perspective, the article examines the transition to professionalism in the context of the Fiji Rugby Union (FRU), which manages rugby union in Fiji. Rugby union distinguished itself from other football codes like soccer, rugby league, Australian Rules Football (Aussie Rules) and American Football by holding steadfastly to its amateur values for over a century before turning professional in 1995 (Dewey, 2008). Rugby union has recently enjoyed significant global growth (Chadwick et al., 2011) 1 and is now played by over five million people in 117 countries. This growth has contributed to the re-inclusion of Rugby Sevens 2 as an Olympic sport from 2016.

In former British colonies like Fiji, rugby union has economic and socio-cultural significance which extends well beyond the sporting arena. Rugby, like Christianity, is part of Fiji’s colonial heritage and was used by British colonialists to legitimize their hegemony over the Fijian people (Dewey, 2008; Kanemasu and Molnar, 2012, 2013; Schieder, 2012). Since it was introduced in Fiji, rugby has become one of the most central institutions in the life of indigenous Fijians (Durutalo, 1986) and an integral part of contemporary Fijian culture (Kanemasu and Molnar, 2012). In addition, Fiji has enjoyed considerable on-field success in Rugby Sevens at an international level (Dewey, 2008). However, off the field, Fiji rugby has been plagued by conflict between the FRU and its major stakeholders. This conflict has been fuelled by the FRU’s financial losses and aggravated by allegations of financial mismanagement which have raised significant questions about accounting and governance in the FRU (Tora, 2011).

The historical analysis in this article commences with the introduction of rugby union by British colonialists in 1884 and continues to later eras, including amateur rugby, with national-level rugby administration by the Fiji Rugby Union (FRU) in the 1960s and 1970s; and finally a post-professional era, with international-level management by the International Rugby Board (IRB) since 2001. The time periods examined in this article contrast the amateur and professional periods of rugby union. These periods also involve profound institutional and political change within Fiji, which affected rugby both directly and indirectly. The first period (subsequently referred to as the amateur period), from 1960 to 1974, was a significant period in Fiji’s political history because it traversed the transition from colonial rule to early independence. Fiji became a British crown colony in 1874 and gained independence in 1970. The second period (subsequently referred to as the professional period), from 2001 to 2014, was also significant because the FRU turned professional in 2001. In addition, Fiji had a military government from December 2006 to September 2014; the military government emphasized an anti-corruption platform and established the Fiji Independent Commission Against Corruption (FICAC) to investigate allegations of corruption by those in public office.

Consistent with Miller, Hooper and Laughlin’s (1991) approach to “new accounting history”, this paper adopts an interpretive and critical attitude in examining the past (see also Carnegie and Napier, 1996). Such an approach generates valuable insights into recent and common accounting phenomena (Carnegie and Napier, 1996). Focusing on broad accounting phenomena enhances the generalizability of research findings based on case studies (Napier, 2009). This article is also consistent with “social-historical accounting research” (Napier, 2009), which emphasizes the importance of contextualizing accounting issues in order to understand how accounting impacts individuals, organizations and societies (Carnegie, 2014). In line with Napier’s (1989: 241) argument that a good history paper “tells a good story”, the analysis includes several narratives to communicate the story effectively (Napier, 2009; Carnegie, 2014).

In relation to research methods, this article is based on detailed analysis of the FRU’s private and public documents. These include minutes of the FRU Board Meetings from 1960 to 1974, which are held in the Fiji National Archives, as well as annual reports for selected years, which were obtained from the Fiji National Archives and the FRU. 3 The minutes and annual reports were analysed to identify relevant material for the study, through a three-stage thematic analysis. First, the authors examined the contents and identified three broad themes: financial resources, governance structures and social responsibility. Second, a research assistant classified the contents using themes identified in the first phase. The “classified” content was reviewed by one of the authors and further refined to identify issues related to accounting. Three broad themes emerged from this process, namely: financial performance and loss making; fundraising and sponsorship; and governance structures and accountability. Finally, the authors collectively used the output from the second phase to derive the four themes used in the analysis section of the article.

The remainder of this article is organized as follows. The next section reviews the literature on accounting and sport, while subsequent sections: provide a background to rugby union, both globally and within Fiji; analyse the research findings; discuss significant issues; and present the conclusions.

Literature on accounting and sport

This section draws from the emerging literature on accounting and sport as well as the sociological literature which has examined sport in the context of colonization, professionalization and player migration (see for example Kanemasu and Molnar, 2013). Previous studies in accounting and sport have examined three major themes: how clubs account for players in their financial statements (Trussell, 1977); how teams’ performance on the field impacts their clubs’ financial performance (Pinnuck and Potter, 2006); and the interaction between accountability and power in professional sport (Cooper and Johnston, 2012).

The first major theme in accounting and sport has focused on accounting for individual players in their clubs’ financial statements. Studies within this theme examined how to account for players and human resources in general (Trussell, 1977) and how to classify and measure football players in financial statements (Trussell, 1977; Morrow, 1996; Shareef and Davey, 2005; Bullen and Eyler, 2010). They challenged the traditional accounting practice of expensing player costs, and advocated that capitalizing these costs would provide a better reflection of the clubs’ true value. Capitalization of contracts is more common in the professional sporting era, given the growing number of contracted players. IAS 38 permits sporting clubs to recognize player contracts as intangible assets, amortized over the contract period. However, the conventional approach of expensing player costs has persisted due to practical difficulties with controlling and reliably measuring the future economic benefits, if any, embodied in players and human beings in general. For instance, Amir and Livne (2005) emphasized the high degree of uncertainty associated with player contracts, even in relatively sophisticated set-ups like the English Premier League. 4 Other studies showed that clubs which chose to capitalize player contracts could window-dress their financial position by deliberately over-estimating players’ registration rights (Risaliti and Verona 2012). 5 Capitalization also creates a tension between the value of individual players and the value of the team (as opposed to the club, which is the reporting entity), since the value of the team is not necessarily equal to the aggregate value of individual player contracts.

Capitalization presents another conceptual challenge in relation to control since a player could simultaneously be an asset for a club side and a national team. This is particularly relevant for Pacific Island rugby nations, which are renowned for producing some of rugby’s greatest talents. Professionalism provides greater incentives, funding and opportunities for Pacific rugby players, who are increasingly sought after around the world and readily lured abroad by lucrative contracts (Dewey, 2008). Therefore, these players are likely to appear on the balance sheet of their respective overseas clubs. However, before leaving their country of birth, they would not have appeared on the balance sheet of their local club or national rugby union if neither could afford to offer them professional contracts. This illustrates the detrimental impact of global sports migration on local clubs and national teams, which cannot match overseas offers. In particular, Pacific Islanders who choose to play international rugby for their adopted country become ineligible to subsequently represent their country of birth. Therefore, Pacific nations are unable to field their best team at Rugby World Cups, further widening the gap between the Pacific and Tier 1 nations (Dewey, 2008). 6

The second major theme in accounting and sport has focused on the financial and non-financial performance of sporting teams, particularly how teams’ on-field performance have impacted their clubs’ financial performance. Pinnuck and Potter (2006) found a positive association between these two facets of performance among clubs in the Australian Football League (AFL), with on-field performance quantified in terms of wins in the three most recent games and current position on the league ladder, while off-field performance was measured through revenue streams from match attendance, gate-takings and sponsorship revenue. Similarly, Panagoitis (2009) found the profitability of Greek football clubs was positively associated with their short-run success on the field, but not their long-run success. The lack of association in the long-run can be explained by fan loyalty, which may remain stable over several seasons since staunch fans are unlikely to switch allegiance to another club. However, match attendance within a season may gain or lose momentum in accordance with a team’s on-field performance, which may in turn impact related revenue streams.

Accounting studies on team performance illustrate how professionalism has transformed value systems in sport by replacing core sporting values and non-financial accountability with the business principles of financial performance and accountability. In the amateur period of sport, players were intrinsically bound to particular clubs by a shared identity such as provincialism, ethnicity or citizenship. Therefore, they were more likely to focus on altruistic motives such as pride and glory. In contrast, many professional rugby unions have now adopted revenue models involving multi-million dollar sponsorship deals, brand endorsements, and the sale of broadcasting rights for local and international competitions. These models were originally designed for business corporations with profit motives, and rugby unions have adopted them to ensure their own financial survival. However, the transition to professionalism has encountered resistance from those who cherish rugby union’s amateur values (O’Brien and Slack, 1999) such as players’ pride in their respective jerseys. For instance, in the Queensland Rugby Union (QRU), those involved with developing the sport in schools regarded rugby as a hobby and source of enjoyment. Consequently they were less receptive to the additional rules and regulations required in the professional period. Unsurprisingly, full-time rugby players welcomed professionalism because it directly and positively affected their personal income (Skinner et al., 1999).

The third major theme in accounting and sport has focused on power and legitimization in the context of the interaction among club owners, management and other stakeholders. The increased importance of funding in sport has allowed powerful professional groups to influence the rules of the field and marginalize less powerful stakeholders. For instance, Cooper and Joyce (2013) showed how the Scottish Premier League (SPL) was able to marginalize other stakeholders because its lawyers had an intricate knowledge of the law, particularly the 1986 UK Insolvency Act. The Scottish football club Gretna had played in the Scottish Third Division, but following considerable cash injections by its owner it achieved three consecutive promotions and eventually qualified for the SPL. The owner’s death resulted in loss of funding and Gretna’s performance declined to such an extent that it was relegated back to the Third Division. Based on the Insolvency Act, Gretna should have been liquidated soon after its relegation. However, the SPL urged Gretna’s administrators to continue operating until the end of the season, and even paid the administration fees to facilitate their acquiescence. Gretna subsequently incurred further losses before the end of the season and was unable to pay its creditors, when it was eventually dissolved.

Other studies on power and sport emphasize how powerful interests managed crises by using financial disclosures and audits to legitimize their own actions and marginalize the interests of fans. In this context, some business interests have provided a meaningless and vulgate form of accountability based on financial disclosures to obfuscate their “real” nature and immunize themselves from criticism (Cooper and Johnston, 2012). For instance, Manchester United Football Club provided relevant financial disclosures after it was taken over by an American billionaire. However, its fans were more concerned with issues of identity and on-field performance. Therefore, they reacted unfavourably to the hostile takeover because they felt threatened by the loss of control to foreign interests (Cooper and Johnston, 2012). These findings suggest that sporting fans may be primarily concerned with non-financial aspects of their team’s performance. They also show that sport can arouse strong emotions and reactions based on regional and national identities.

In summary, player contracts and club profits were less relevant during the amateur period of major sports and remain so in amateur sports that are funded through donations and membership fees. However, they have become increasingly pertinent in the professional period of sport, given the stronger emphasis on financial performance. This article complements and extends the literature on accounting and sport by examining how the focus on financial performance in the professional period presents different roles for accounting compared to those employed in the amateur period. It also examines how powerful stakeholders can use accounting to exert control and assign blame. In practice, accounting performs various roles which may differ from its officially stated functions like decision making and stewardship. For instance, accounting can also be used to negotiate interests, support counter claims and explicate political processes (Burchell et al., 1980). More generally, the role of accounting is impacted by social dynamics and power structures so that accounting systems become a reflection of the societies and organizations in which they operate. In other words, what is (or is not) accounted for can shape organizational participants’ views of what is (or is not) important. Irrespective of specific power structures, accounting will always have a purpose, which is essentially to account for what is perceived as important in a given context (Hopwood, 1983).

Background and context to rugby and Fiji

According to rugby union mythology, the sport originated in 1823 at Rugby School in Warwickshire, England. 7 The sport was referred to as rugby football from 1871 when it was codified with its first set of established rules (Baker, 1981). In 1895, a schism over player payments resulted in the formation of two separate codes; rugby union and rugby league (Dunning and Sheard, 1976). Class distinctions were a fundamental factor in the bifurcation between amateur and professional rugby (Collins, 2006). The union code clung to its amateur status and prohibited players from receiving any financial rewards (Malcolm et al., 2000), which is not surprising since it was played by the British elite who had secure incomes and only played sport for enjoyment. In contrast, the league code chose to become professional. It paid working-class players who would have been unable to play during working hours unless they were compensated for loss of income from their regular employment.

Rugby union was the last football code to embrace professionalism. In maintaining its amateur status, rugby union emphasized the importance of protecting “core rugby values” from being corrupted by money flowing into the sport (O’Brien and Slack, 1999). The opponents of professionalization regarded rugby as more than just a game; they argued that rugby was about forming character, including qualities such as courage, friendship, leadership, respect, sportsmanship and team spirit. They also emphasized the unselfish nature of rugby whereby team achievement was regarded as more important than personal achievement (Rugby Football Union, 2007). In summary, supporters of amateur rugby believed it should be played out of love for the game and the values it represented rather than for remuneration (O’Brien and Slack, 1999).

Organizational change often results from a “jolt” (or perhaps more aptly in the case of rugby, a kick) from external environmental forces (Laughlin, 1991). In 1995, rugby’s governing body then known as the International Rugby Football Board (IRFB), 8 was coerced into repealing the sport’s amateur status after many decades of enforcing the principles of amateurism. The IRFB faced intense pressure from two sources. First, professional rugby league clubs were offering players lucrative contracts to switch codes. Second, a rival body named the World Rugby Corporation (WRC) was recruiting players to participate in a professional international competition for rugby union. Given this sustained pressure, the IRFB declared the sport “open” through the Paris Declaration of August 1995. Henceforth, rugby union players could openly receive financial compensation for their playing services. However, the degree of professionalism varies significantly from one country to another. The countries that have successfully attained full professional status are relatively large and resource-rich nations like Australia, France, Japan, New Zealand, South Africa and the United Kingdom. Members of the IRB also enjoy varying degrees of representation and influence. The eight founding members (Australia, England, France, Ireland, New Zealand, Scotland, South Africa and Wales) have the most power on the IRB Council, with two votes each, while Argentina, Canada, Italy and Japan each have one vote. In contrast, Pacific nations like Fiji, Samoa and Tonga have no direct voting rights on the Council (Dewey, 2008), where they are collectively represented through the Federation of Oceania Rugby Unions (FORU), which has one vote.

Relatively few studies have examined accounting and sport in small developing countries whose limited resources present specific challenges in the transition to professionalism. This transition is predicated on a certain level of economic resources. It also assumes funding for player contracts is available and sporting infrastructure, which may be problematic in many developing countries. The FRU became a member of the IRB in 1987 and is responsible for developing and promoting rugby through 36 unions and 500 local clubs across Fiji. In 2001, the FRU was forced to turn professional due to pressure from the IRB coupled with its own poor financial performance. Despite sweeping changes to its constitution and management, 9 the FRU has continued to experience financial losses and stakeholder conflict, both of which have been reported and debated publicly.

Accounting, rugby and control

Fiji provides a suitable setting to study both accounting and rugby as tools for control. Rugby union was first introduced into Fiji by foreign soldiers and policemen in 1884, during British colonial rule. Britain used rugby as a civilizing force in some of its colonies (Kanemasu and Molnar, 2013). Although this may not have been the intent of introducing rugby in Fiji, the church encouraged the sport as a replacement for traditional warfare, which involved violent inter-tribal conflict. In fact, Fiji’s strong martial history has manifested in rugby through the “cibi”, a war dance performed by the Fiji national team before an international rugby match. In 1904, New Zealand expatriates established the Fiji Rugby Football Union for white colonists and a year later, a separate “Native Union” was established. In 1945, the two unions merged and in 1963 the organization was renamed the FRU, the governing body for rugby (Robinson, 1973). By that time, rugby was considered an indigenous Fijian sport, yet most coaches and board members of the FRU were Europeans 11 (Kanemasu and Molnar, 2012). Rugby has played a significant role in shaping Fiji’s culture and history. Durutalo (1986) argued that indigenous Fijian culture can be summarized by four important institutions: ratuism, 10 royalism (this is related to the Royal Family of Britain, Fiji’s colonial rulers), religion (predominantly Christianity) and rugby. He referred to these institutions as the “four R’s”. Rugby became an essential part of the “vaka-i-taukei” (indigenous Fijian way of life) as it represented characteristics such as courage and strength, which indigenous Fijians regarded as desirable physical attributes of Fijian males (Robinson, 1973).

In the context of colonialism, accounting was used to exploit and legitimize power structures (Davie, 2005a). According to Padmore (1936: 61), colonized people were governed through indirect rule, “with their own chiefs and political institutions under the control of European officials … the whites however hold the real political, financial and military powers in their hands while the chiefs serve as their own marionettes”. The British colonists gave some indigenous Fijian chiefs positions within the colonial administration. These chiefs were paid for their services, albeit much less than white officials. Accounting was implicit in indirect rule because the form of charging and accounting for tax forced colonized people to remain in their villages, work on the land and produce agricultural crops. In this context, Davie (2005a) criticized the British administration for denying Fijians many citizenship rights, such as individual land ownership and the right to choose their leaders. However, the British colonists simply exploited the existing social structures and power dynamics. Therefore the more implicit criticism may be that the British did not use their power to reform what could be regarded as an inherently unjust society. This perceived injustice included a focus on upward accountability, with less emphasis on downward accountability (Davie, 2005b; Rika et al., 2008).

Analysis of accounting during colonialism, independence and professionalism

This section analyses accounting and power in the FRU under four themes derived from the thematic analysis outlined in the introduction. First, it analyses the FRU’s governance structures to determine how they have changed over time. These changes are important because they are linked to the type of accounting practised within the FRU. Second, it compares the Fiji team’s performance on and off the field, showing how professional sport emphasizes accounting for financial performance. Third, it reviews a public lottery which the FRU organized to fund its 2011 World Cup campaign. The lottery resulted in a financial loss and led to conflict with the Fiji government over allegations of financial mismanagement. Finally, it examines issues of power in the FRU’s relationships with its major donors: the IRB and the Fiji government.

The FRU’s governance structure

During the colonial era, the board and management of the FRU encapsulated Durutalo’s four R’s of royalism, ratuism, religion and rugby. Rugby was linked to the institution of royalism through the patron of the FRU. This position was held by the Governor who was the resident representative of the British monarch and head of the colonial government. As patron, the Governor sat at the very apex of Fiji rugby in much the same way as he headed the Great Council of Chiefs (GCC),

12

indicating his supremacy over all indigenous chiefs. However, the patron’s role was symbolic and motivational rather than administrative, since he was not expected to attend board meetings. The following excerpt indicates that the Governor’s association with the FRU reinforced the national significance of rugby: We wish to thank His Excellency the Governor for the intense interest he has shown and the support which he has given the Union in this, his first year as Patron. His influence on the morale of both the team and the Executive has been considerable. (FRU Annual Report, 1964)

Rugby was linked to the institution of ratuism through the practice of an indigenous Fijian chief accompanying each overseas tour, either based on an appointment by the FRU or at the invitation of the host country. For example, Ratu Edward Cakobau (later Fiji’s first Deputy Prime Minister) accompanied the 1964 tour to Wales as a “Fijian chief … on invitation of the Welsh Rugby Union” (FRU Annual Report, 1964). From the FRU’s perspective, an indigenous chief was better able to control players because they inherently respected his status (FRU Annual Report, 1964). A chief can be a source of inspiration who is able to appeal to the ‘yalo’ (emotions) of players, particularly their sense of national pride. Indigenous Fijian players would also have been inspired to perform their best on the field in order to uphold the chief’s honour. Such a motivation was illustrated by Major General Sitiveni Rabuka who played representative rugby for Fiji in the late 1960s and went on to became a senior military officer, coup leader and elected Prime Minister. Reflecting on his playing days, he said “during my time, we played for God and Country despite being paid only 10 shillings as pocket money during the England tour in 1970” (Nasokia, 2014). Rabuka may have spoken for many other players of his time, whose on-field performance was motivated by their inherent sense of commitment to God and country rather than monetary rewards.

Between 1962 and 1974, the FRU board was dominated by men, who were either white, part-European or indigenous Fijians (see Appendix 1 for a listing of office bearers in 1974). Many of the white men held positions in government (including the colonial administration) or religious institutions, while the indigenous Fijians and part-Europeans were often coaches and in many cases former players. One of the most significant changes in the FRU’s leadership occurred in 1970, when Sir Maurice Scott was succeeded as president by Ratu Sir Penaia Ganilau, an indigenous Fijian chief. Scott was a third-generation European who served as the FRU president from 1948 to 1970, while Ratu Penaia was a government official who later became Fiji’s Deputy Prime Minister, final Governor-General and first President. Ratu Penaia had previously managed numerous international tours by the FRU. 13 Since Fiji gained independence in 1970, the FRU’s patron and president have generally been indigenous chiefs. To this day, the patron’s role remains symbolic and he often speaks to players who are departing on an international tour, motivating them through wise words and appeals to their sense of national identity. In this sense, the patron is valuable as a respected chief, who continues to connect the institution of rugby with Durutalo’s concept of ratuism.

In the professional period, the FRU board has included people from diverse backgrounds, including some with little or no previous involvement in rugby. The military government has been represented on the board, particularly since the military coups of 1987, 2000 and 2006, which were accompanied by the militarization of cabinet, public service management, and boards of state-owned enterprises. Recent Commanders of the Fiji Military Forces, including Mosese Tikoitoga and Frank Bainimarama, have served as president of the FRU. This represents a break from the tradition of appointing a chief as president. These leadership positions have also enabled the military government to influence the composition of the FRU’s board and management. In 2009, the military government insisted that the FRU’s chairman and chief executive officer both resign as a condition for continued government funding of the 2011 World Cup Campaign. The government also influenced board appointments, since the Prime Minister was directly involved in nominating the FRU’s chairman (Mr Filimoni Waqabaca), who was also the Permanent Secretary for Finance. Waqabaca publicly acknowledged that Prime Minister Bainimarama had approached him on more than one occasion to take on the position. It is difficult to say conclusively which role Bainimarama was playing when he approached Waqabaca. On the one hand, his action could be interpreted as the Prime Minister approaching a senior bureaucrat. On the other hand, it could also be interpreted as a senior rugby official reaching out to a fellow rugby enthusiast. Two women

14

have served on the FRU board, although they are both qualified professionals who appear to have been appointed on merit rather than as “token” women. The board has also incorporated business people such as Baljeet Singh, who is the Chief Executive Officer of a supermarket chain. In welcoming such appointments, the FRU president said: We need brains and commercial thinkers in [the] FRU … [Tikoitoga] said it was a timely start to get prominent men and women to join the board, including business people. (Bola-Bari, 2013b)

These appointments may have filled a skill gap on the FRU board, which was previously dominated by people who had extensive knowledge about the on-field aspects of rugby but did not necessarily possess the skills needed to monitor and control off-field performance in the professional era.

Tension between performance on and off the field

As discussed in the literature review, professional sport emphasizes financial performance which is measured through accounting profit. However, in the late colonial era of the amateur period, public discourse concerning rugby union prioritized on-field performance rather than off-field performance. Although the sport already enjoyed a wide public following amongst indigenous Fijians at the time, the FRU’s financial performance received minimal disclosure in the news media. For example, in 1970 the FRU reported a loss of $4,635 15 which was attributed to financial losses on overseas tours (see Appendix 2). A review of articles in the daily newspaper (The Fiji Times) up to two months after the FRU’s 1970 Annual General Meeting revealed no discussion of the losses. Over the same period, the newspaper emphasized on-field performance by reporting on international tours and domestic tours by international teams. The lack of media emphasis on the FRU’s financial performance could reflect a lack of disclosure by the FRU since its financial statements were only available to its members and not to the general public. The FRU was not publicly accountable because it did not receive any financial assistance from the government, despite the national popularity of rugby. Neither did the board request any such assistance. The lack of media coverage could also reflect limited public interest in the losses, which were relatively small. Fans may well have been more interested in their team’s on-field performance than its financial status (see Cooper and Johnston, 2012). Given the absence of public discourse regarding the FRU’s financial performance, it is useful to examine discourse within the FRU, as summarized in Narrative 1.

Narrative 1: Money and losses

The amateur status of rugby featured prominently in an FRU board meeting in June 1961 at which board members expressed their concern that there was “too much money creeping into our rugby” and money was “always coming into the picture”. The board emphasized that the FRU should “try to keep the idea of amateur status in our rugby”. Mr Peterson (a Lomaiviti Provincial Union delegate) emphasized that players selected to represent Fiji against touring teams should not expect to be paid. He stressed that when inviting players to join the national team, the FRU should “make it quite clear that only travelling expenses will be paid” (FRU Minutes Book, 1961).

In 1962, the FRU’s chairman acknowledged that its losses were unhealthy and emphasized that although “the money we have is not to be sneezed at … we can’t go on making losses” (FRU Minutes Book, 1962). He made these comments after the FRU incurred a total loss of £1,064 following a visit by Tonga in 1959 and a tour to Australia in 1961. In relation to the 1964 tour of Wales, the FRU clarified that it was “not concerned about the results, but … [acknowledged] it was important that the team leave a good impression behind them – in their play and in their behaviours off the field” (FRU Annual Report, 1964).

In 1972, the board said, “Success on the field maybe considered by some to be a fitting reward for the efforts involved but unless tours of this nature can be operated profitably future tours could be placed in serious jeopardy” (FRU Annual Report, 1972).

Narrative 1 indicates that the FRU was making financial losses as early as 1962. The FRU board approached the losses pragmatically, recognizing that the situation could not continue in the long term because losses would deplete its cash reserves and negatively impact future cohorts of rugby players. However, there is no evidence that the board sought to develop appropriate policies and strategies which could prevent such losses from recurring. Nor is there evidence that the board accepted personal ownership and responsibility for the losses. This underscores the absence of effective mechanisms for financial accountability, since the FRU had no full-time management staff and the voluntary treasurer was also a member of the board. Therefore, in discussing the financial losses, the FRU board was essentially engaged in a conversation with itself, rather than with an agent or an independent third party who could hold it accountable.

In relation to the 1964 tour of Wales, the FRU prioritized non-financial performance, arguing that short-term financial losses were justified in exchange for a long-term presence in international rugby and a good name for Fiji. The FRU emphasized the need to develop a favourable image, supported by positive relationships which would establish the FRU in good standing amongst the international rugby community and secure Fiji’s continued participation at international level. However, there is no evidence that the board explicitly developed policies and strategies to fund future participation, or assigned responsibility for raising the required funds.

In general, the board’s position in Narrative 1 emphasized the amateur values of rugby union, including the display of good sportsmanship and the development of good friendships, rather than scoring points or winning matches. Mr Peterson’s comment upheld the ideals of amateur rugby, where on-field performance was not motivated or ‘corrupted’ by monetary rewards. Indeed, the board was distressed that money was becoming too significant within the FRU. Mr Peterson’s comment also echoed the original schism between rugby union and rugby league concerning payments to players. The FRU’s minutes provide the context of these comments by revealing that English Rugby League scouts were active in Fiji in 1962 and the board was worried that some of its top players might join the rival code. It actively sought to discourage players from defecting and dissuaded local agents from assisting the scouts. In addition, Mr Peterson’s comment was consistent with the values of indigenous Fijians such as Sitiveni Rabuka, who regarded rugby as a medium to demonstrate pride in “vanua” (i.e. land and people) and to assert their strong Christian beliefs and values (Schieder, 2012; Kanemasu and Molnar, 2013). Donning the national jersey epitomized players’ commitment and honour in relation to their country. Consequently they accepted and expected little more than a nominal allowance on overseas tours. This was just as well considering the FRU’s financial losses and its inability to afford anything more than basic allowances. In summary, Mr Peterson’s comment incorporated commitment to the amateur values of rugby, together with a contextual understanding of the indigenous Fijian psyche and the vulnerability of the FRU’s financial position at the time.

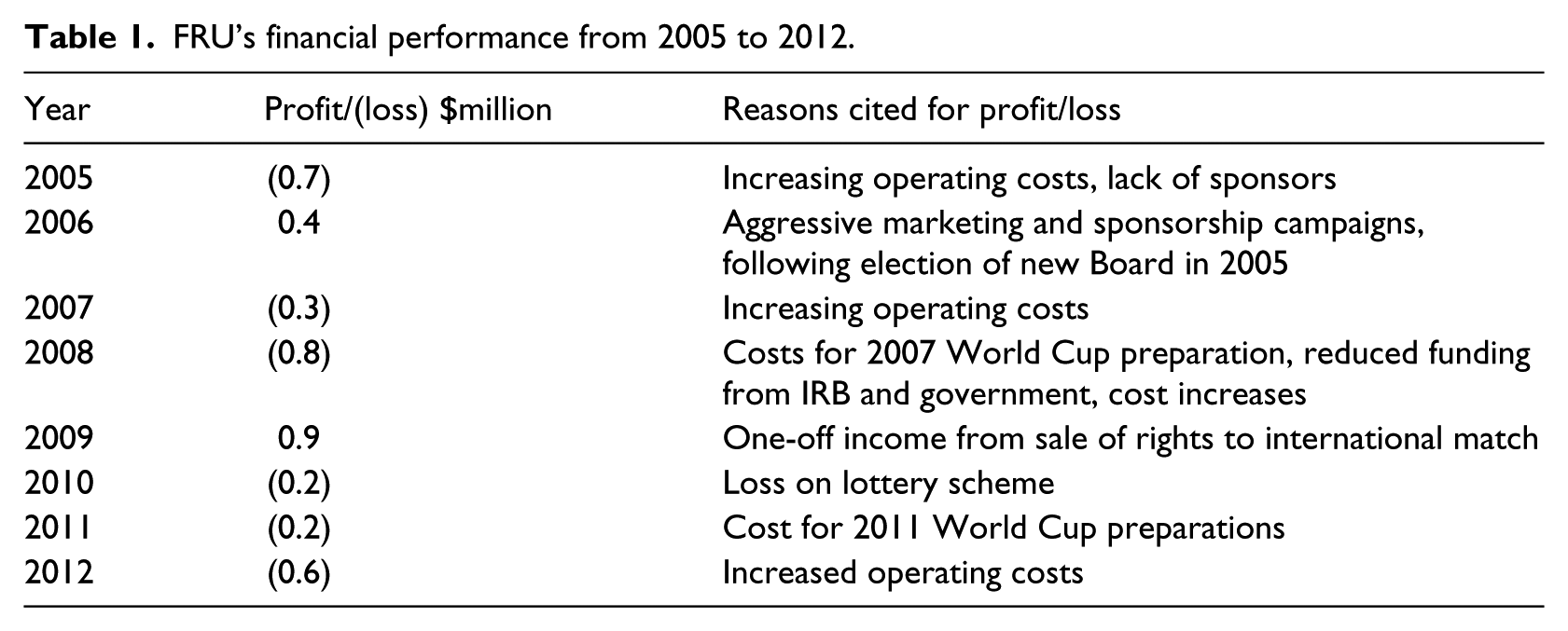

In the professional era, the FRU has experienced tension between different approaches to measuring performance, namely on-field success versus financial profitability. Seven years after the FRU officially turned professional, some members of the FRU’s management team continued to stress that rugby was not all about making money. They included Ratu Timoci Tavanavanua, who was the FRU’s CEO at the time of the 2007 World Cup. Tavanavanua downplayed the significance of the FRU’s financial losses in 2007 and 2008 (see Table 1), arguing that Fiji’s on-field performance at the World Cup outweighed the losses. Tavanavanua believed that expenditure on the World Cup was “money well invested because we’ve been able to show the world what we are capable of on the rugby field. If you put a value on the performance of the team, it far outweighs the shortfall” (Planetrugby, 2008). His view can be contrasted with that of the FRU’s Finance Director at the time (Mr Iowane Naiveli), who described 2008 as one of the worst in his 20 years of involvement with the FRU (Chand, 2009). In Tavanavanua’s view, the national team’s on-field performance was equally important to (or possibly more important than) the FRU’s financial performance. Tavanavanua felt the Fijian team had produced a good return on the funds spent to prepare for the World Cup and participate in it. In that sense he felt the FRU had been accountable for the funds and thus regarded the financial losses as relatively unproblematic. However, in the professional era, funders impose stringent requirements for financial performance which they expect organizations to meet. In the lead up to the 2011 World Cup, Fiji’s national (Fifteens) team struggled to secure a sponsor because of its comparatively poor on-field performance. In contrast, the Fiji Sevens team has successfully obtained financial sponsorship due to its consistent on-field performance in the World Sevens Series. In this context, the national team’s performance at the 2007 World Cup was valuable in terms of facilitating future matches against other national teams and securing corporate sponsorship that could be regarded as off-setting some of the FRU’s financial losses. The team’s performance was also important as a means of solidifying rugby’s public image and maintaining national pride.

FRU’s financial performance from 2005 to 2012.

Sporting lotteries, accountability and conflict

During the amateur period, the FRU generated funds predominantly through gate-takings and affiliation fees from sub-unions (Robinson, 1973) (also see Appendix 2). The FRU minutes indicate considerable difficulty in collecting annual affiliation fees, even though they were quite nominal at three guineas (FRU Annual Report, 1963), which is roughly equivalent to one British pound. Income from affiliation fees and gate-takings was unable to keep track with the rising costs of administration, facilities and coaching (FRU Annual Report, 1972). The board was particularly concerned that insufficient funding would cause Fiji to fall behind other rugby playing nations which were reducing their reliance on natural talent and making concerted efforts to improve their playing efficiency (FRU Annual Report, 1970). However, the FRU had few realistic options for enforcing the collection of affiliation fees, since suspending a member union would be detrimental to the sport.

In the 1960s, the FRU solicited and received donations from corporate sponsors such as the Fiji Tobacco Company which donated trophies and funded tournaments (FRU Minutes Book, 1970). Similarly, Qantas and Fiji Airways facilitated donations of tackling machines, while ad-hoc donations were occasionally received from individuals and overseas rugby unions, including Australia, Wales and Singapore. The FRU also organized ad-hoc fundraising activities to address its immediate financial requirements, as opposed to its future aspirations. These activities included lotteries (raffles in contemporary terms) and “taralala” (dances) to supplement the financing of overseas tours. For instance, the Bulumakau Lottery 16 in 1963 produced a modest gain of £100 while another lottery in 1965 raised £490. However, some board members felt these fundraising activities were not worthwhile because the profits they generated were too small (FRU Minutes Book, 1963). When the FRU’s bank balance declined to $800 in 1970, the FRU board acknowledged the need to strengthen its finances by developing additional income streams. However, there is no evidence that this consideration was ever implemented.

Narrative 2: Lotteries

The FRU organized a large-scale public lottery to fund participation in the 2011 Rugby World Cup. The lottery was necessary because the FRU had been unable to secure sufficient sponsorship for the team. However, the lottery was unsuccessful and contributed to the FRU’s loss of $0.2 million in 2010 (Fijilive, 2011). As the drawing date drew near and many tickets remained unsold, the lottery organizers authorized a reduction in the ticket price from $20 to $10. Following complaints from members of the public who had purchased tickets for $20, the Fiji Commerce Commission 17 investigated the FRU for contravening five statutory provisions of the Commerce Commission Decree 2010 (NZ Herald, 2011), including failure to provide a special audited financial report to the Office of the Solicitor General. As a result, the FRU was fined $125,000, although no public disclosure has been made to verify whether the fine was actually paid.

In addition, the FRU was accused of misappropriating funds after failing to account for over $155,000 of the $350,000 raised from ticket sales (NZ Herald, 2011). The media reported allegations that some of the proceeds had been used to fund certain directors’ travel to Sevens tournaments in Hong Kong, Scotland and England. The Government cited these allegations when calling on the FRU chairman (Viliame Gavoka) to resign. Gavoka and the board subsequently resigned under protest.

The small raffles of the amateur period can be contrasted with the 2011 lottery documented in Narrative 2. First, the small raffles of the amateur period did not involve any direct costs to the FRU and were thus guaranteed to make a profit, albeit a small one. However, the 2011 lottery offered prizes which had to be funded from the proceeds in order to break-even. This required accurate budgeting and thorough accounting. Second, the small raffles involved a restricted group of people who were closely connected to the sport. However, the 2011 lottery involved accountability to the general public because the FRU was accepting funds from people right across Fiji and even abroad. These people had no direct access to financial information about the lottery and some of them may not even have been rugby fans. Third, the 2011 lottery was conducted in a highly litigious environment since the military government was enforcing its anti-corruption platform through FICAC, which investigated allegations of corruption by holders of public office.

The 2011 lottery led to several serious allegations against the FRU, including a lack of adequate accounting and accountability. From a probity perspective, the FRU was unable to account for a substantial portion of the lottery proceeds. This raised questions about the integrity of board members, who were alleged to have used lottery proceeds to fund their own travel to international Sevens tournaments. The FRU did not clarify whether the travel was a budgeted expense of the lottery. In addition, the FRU’s failure to explain the price reduction (from $20 to $10) negatively impacted public opinion, especially among those who had purchased tickets at the original price. In terms of performance or output, the lottery fell short of its target revenue and recorded a loss. The FRU could only disclose a rudimentary and descriptive account of the lottery in its financial statements, since the Commerce Commission had seized all relevant documents as part of its investigations. The FRU also limited its disclosures to avoid prejudicing the outcome of the investigations (FRU Annual Report 2011: 45).

The FRU’s relationship with its major donors

The lottery row detailed above brought the FRU’s financial losses to a head, first with the military government and later with the IRB. The FRU had accumulated losses of $0.9 million by the time it embraced professionalism in 2001 (Dewey, 2008), which indicates that it had made some losses during the independent era of the amateur period. From a historical perspective, the FRU’s 1970 annual report linked the disparity between expenses and income to inequity in the arrangements governing international tours, which required the home team to pay all tour expenses but also entitled it to take all profits. 18 This arrangement was based on the assumption that expenses and profits would even out in the long run through reciprocal tours. However, the FRU board pointed out that while Fiji had already played a total of 128 games overseas, it had only hosted two international matches (against New Zealand and Wales) and four tours by the New Zealand Maori. This created a permanent financial problem, since the FRU’s operating expenses were “no less than those of other Unions” (FRU Annual Report, 1970), but it hosted far fewer tours. When Fiji did host international teams, the income from gate-takings was often insufficient to cover the visitors’ travel and accommodation costs. Low gate-takings reflected the public’s inability to afford higher ticket prices, and, in some cases, the FRU’s inability to control (and therefore charge for) access to sporting venues. The board highlighted these issues following Tongan and English visits in the early 1970s which attracted smaller crowds than expected. The board attributed the low attendance to inflation, saying: “people are less willing to take a day off work and lose wages to see a match than they used to be” (FRU Annual Report, 1974). Given Fiji’s relatively small population size and low income levels, rugby matches may never attract the same number of spectators as larger countries or enjoy their economies of scale.

In spite of various reforms in the professional era, the FRU recorded further losses and became technically insolvent until 2005 when the elected Fiji government provided a $1.2 million grant to off-set its debt. 19 However, the FRU accumulated further losses following the 2007 World Cup. In 2011, the FRU reported a loss of $0.2 million which it attributed to the cost of preparing the national Fifteens team for the 2011 Rugby World Cup (Tora, 2011). In 2012, the FRU recorded yet another loss of $0.6 million, despite a further government grant of $2.3 million (Bola-Bari, 2013a). More signs of financial distress became evident in late 2013 when a lack of finances caused the FRU to drop its backline coach prior to the European tour. In a related move in early 2014, the FRU also terminated five of its employees, including the Fifteens’ head coach. At face value, the FRU’s continuing financial losses may seem to indicate financial mismanagement. However, according to the FRU chairman, it requires a $10 million budget to operate at a level that satisfies the current requirements of a professional rugby union (Kumar, 2013). By comparison, annual grants from the IRB and the Fiji government collectively totalled $6 million in 2011. Therefore, the total level of funding is still insufficient to cover the FRU’s core requirements. The FRU’s financial performance can also be attributed to increased operational costs and low gate-takings from matches (see Table 1).

The FRU has received regular funding from the IRB, which is now the FRU’s main donor. Narrative 3 examines these funding arrangements, which keep countries like Fiji permanently dependent on the IRB. The narrative indicates volatility in the FRU’s relationship with the IRB, which has been aggravated by the Fiji government’s active involvement in the FRU’s administration. In particular, the IRB threatened to expel Fiji in 2011 after the Fiji government demanded the resignation of the entire FRU board (Rugbynews, 2011) during the lottery row. However, the IRB later clarified that it did not want to interfere in the row between the FRU and the Fiji government, re-affirming its commitment to support the FRU in developing rugby. In addition, the IRB was satisfied that its “investment in the union was adequately managed and met thorough reporting and auditing standards, and was managed in accordance with the FRU constitution” (Narayan, 2013).

Narrative 3: Grants from the IRB

The IRB grants are determined through detailed reviews and recommendations of member unions, which are conducted by the IRB management, development managers in the respective regions and the relevant regional associations (International Rugby Board, 2007). In 2008, the IRB committed £18.6 million to Fiji and other Tier 2 countries including Canada, Japan, Romania, Samoa, Tonga and the United States. This followed an IRB-commissioned report highlighting the growing disparity between Tier 1 and Tier 2 countries (Singh, 2008).

In 2010, the IRB’s contribution to Fiji tripled to over $3 million, reflecting funding for the FRU’s preparations towards the 2011 World Cup. The IRB pledged its commitment and on-going support to the FRU, praising the union for its “impressive and inspirational achievements” (International Rugby Board, 2013) which included winning the Rugby Sevens World Cup twice in 1997 and 2005 and being the only Pacific nation to reach the quarter-finals of the 2007 Rugby World Cup.

However, the FRU twice declined the IRB requests to conduct its own audit, following the FRU’s request for emergency funding in 2011. The FRU’s new board finally agreed to the audit in October 2013. The IRB audit letter was received in December 2013, and, according to the FRU’s acting chief executive, it “highlighted financial, administration and governance issues that … [the] current board is working hard to complete before reengaging with IRB” (Fijilive, 2014). Following the audit, the IRB suspended all direct funding to the FRU until the FRU adopted key reforms in the three areas identified in the letter.

The IRB also emphasized the FRU’s precarious financial position, stating that it (together with the Federation of Oceania Rugby Unions Regional Association) had “formally expressed concerns that the financial position of the union is unsustainable and could create instability and impact on the management of the union and key IRB-funded development and high performance programs” (Kumar, 2014).

The IRB uses its financial power as a major donor to hold the FRU accountable; in the short-term, the IRB enforces probity and process accountability while in the long-term it holds the FRU accountable for on-field performance. The IRB assesses accountability through the accounting and auditing standards adopted by the FRU. It also relies on external audits to monitor the use of grant funds. In addition, the IRB requires the FRU to uphold governance principles documented in its own constitution. However, the IRB describes its funding as an “investment” which indicates that it also expects long-term outcomes in terms of improved performance and narrowing the gap between countries in Tiers 1 and 2. This is consistent with the IRB’s positive comments about Fiji’s successful on-field performance at major sporting events.

Discussion

Based on the preceding analysis, this section summarizes how the role of accounting has changed in the course of rugby’s transition from amateurism to professionalism. It also reveals how domestic and global interests have exerted power over Fiji rugby and how accounting reports have been used for this purpose.

During the amateur period, accounting seems to have played a rather insignificant role within the FRU, which employed very rudimentary accounting systems and produced basic accounting reports (see Appendix 2). In addition, the FRU lacked short-term financial planning in terms of budgets and long-term planning in terms of strategic financial goals. Rugby was an amateur sport throughout the colonial period, and neither players nor management were very concerned about money. If anything, players were content to play for “God and country” and the board was anxious to prevent money from becoming too important in the sport. This context is useful in explaining the rudimentary accounting practised. During this period, the FRU was not required to discharge public accountability because it received no financial contributions from the government. Although the FRU received some donations, they were often received in kind and the cash donations were generally philanthropic in nature. 20 Therefore, the donors may have been satisfied with a receipt and probably did not require any further financial accountability. In essence, the FRU produced accounting reports only for its internal stakeholders (i.e. member unions and sub-unions) and was not held to account by any external body or group.

When Fiji was a British colony, the colonial administration did not invest significantly in rugby union since it was an amateur sport, which was supposed to be played for the love of the game. Rugby provided colonialists with a tool to control indigenous Fijians, who had a natural flair for the game and needed no coercion to participate. Rugby allowed indigenous Fijians to channel their energy and disposition for battle into sport rather than warfare (Kanemasu and Molnar, 2013). Therefore, organizing rugby matches would have been a relatively inexpensive way for the small population of British colonialists to control the local population, given the limited size of the local police constabulary and the lack of any British military presence. In this way, rugby may have actually helped the British colonial administration to reduce expenditure in the colony. Allowing rugby to operate on a shoestring budget was a less overt strategy than the taxation system analysed by Davie (2005a), but contributed to the same overall objective. The FRU only had sufficient funds to operate at a basic level. Therefore it could be argued that by not providing any financial assistance for rugby, the colonial administration prevented it from becoming too powerful or autonomous and posing a threat to the British colonialists. The authority of indigenous chiefs was also used to control rugby players, in a similar manner to the taxation system discussed by Davie (2005a). In addition, the FRU upheld the rugby union code which prevented Fijians from receiving financial benefit from sport and thereby attaining a higher degree of financial independence. This was particularly relevant in the 1960s when rugby league scouts started recruiting Fijian players.

In the professional era, the IRB has used accounting to monitor its investment in the FRU and thereby control Fijian rugby from a distance. The IRB even threatened to withhold further funding pending receipt of satisfactory accounting reports from the FRU, which has only survived through significant financial investment from the IRB. The FRU is required to account for the IRB’s operating grants by providing audited financial statements which comply with IFRS. However, these grants keep FRU in a perpetual state of dependence. The relationship is beneficial for the IRB, which benefits from its own investment in Fiji rugby, particularly as it strives to develop the sport among Tier 2 nations. In addition, the Fiji Sevens team is a major draw-card at all IRB tournaments.

As the FRU’s second largest donor, the Fiji government has also used accounting to exert control over the FRU. In the light of sustained losses, the FRU has relied on the Fiji government to bail it out through operating grants. However, the form of accountability emphasized by the Fiji government has aggravated the FRU’s poor financial performance by withholding funds when they were most needed. In particular, the government withdrew funding from the FRU between 2008 and 2010, and also demanded the resignation of the FRU board. The government took this action on the basis of inadequate accounting and alleged misuse of funds in relation to the 2011 lottery (Field, 2011) . The government based its intervention on notions of accountability, financial prudence and transparency, and justified its concerns by the need to safeguard taxpayers’ money. However, rugby fans may be more interested in the on-field performance (Cooper and Johnston, 2012) of the national team. The FRU’s records analysed in this article suggest that neither players nor fans have historically demonstrated much interest in the FRU’s financial performance.

The governance structures within an organization play an important role in shaping and upholding accounting and accountability. In the sporting context, the British colonial administration appropriated indigenous power structures by installing the Governor in the benevolent position of patron of the FRU. In this way, the indigenous people’s allegiance and devotion to their own chiefs was seamlessly transferred to the British crown by placing the Governor at the apex of the existing indigenous leadership structures for government and sport. The British colonialists also utilized indigenous Fijians’ respect for their own chiefs in order to maintain control over Fijian players during overseas tours. This reinforced the idea of playing for God and country. The colonial administration was able to further influence the FRU because many board members were civil servants or had other close links to the administration. In summary, the institutions of royalty, ratuism and religion were very influential, while commercial thinking was less relevant.

The composition of the FRU board reflects changes in Fiji’s society which have affected the power of particular institutions. However, changing the FRU board will be futile unless all stakeholders confront economic reality. First, without a sustainable funding model, the FRU will continue recording losses, and successive boards may continue to be blamed for problems which are not entirely of their making. As early as the 1960s, the FRU board had identified that it would continue making losses because of inequitable funding arrangements governing international tours. These arrangements place small, isolated, developing countries at a permanent disadvantage because they lack the financial resources to host visiting teams. Small population size and lower income levels mean that sporting bodies are unlikely to generate the same level of income as their counterparts in more affluent nations. Second, at the player level, socio-cultural changes are likely to contribute to a shift in accountability, which is now less linked to religious values or national pride and more closely linked to financial incentives. However, the FRU’s financial constraints prevent it from contracting players, and therefore Fiji continues to lose many of its best players to overseas clubs. If this trend persists, Fijian rugby is likely to face continued challenges in terms of on-field performance.

Conclusion

This article re-affirms the need to interpret accounting reports and results in their own operating context (Burchell et al., 1980; Carnegie 2014). Revisiting and understanding its own history may help the FRU and its stakeholders to tackle underlying issues and problems. For instance, some stakeholders have highlighted financial losses in the FRU, without acknowledging the practical difficulties associated with diseconomies of scale and comparatively low income levels. By reviewing the FRU’s history, this article highlights that such underlying problems had been identified as early as the 1960s but remain unaddressed in the professional period. While the IRB and Fiji government provide the FRU with substantial funding, the FRU chairman has publicly stated that this is insufficient to meet the requirements of the professional era. Although the IRB provides some financial assistance to cover the cost of international tours, the host team still retains all match profits.

This article complements the literature on accounting and sport by showing how the form of accounting changes in the transition from amateur to professional sport. In the amateur period, rugby union was regarded as a hobby, so both players and management were more focused on amateur values, as documented in the sociological literature (O’Brien and Slack, 1999). The sport was not about making money and the FRU was self-funded, so it only practised basic accounting with an internal focus. However, in the professional period, sporting bodies have increasingly focused on reporting to a broad range of external stakeholders; powerful stakeholders may enforce accountability for financial performance by demanding that sporting bodies produce audited financial statements. As shown in this article, the FRU is increasingly dependent on external funding and cannot escape such demands from its major donors. The FRU must comply with reporting procedures in order to maintain legitimacy with the IRB and the Fiji government, thereby securing continued funding for its operations. Although the IRB supports rugby in Fiji and other Pacific countries through financial grants, this is problematic for several reasons. Grants keep Pacific countries in a continuous state of dependency where they survive through hand-outs from the IRB. The grants also make Pacific countries accountable to the IRB, which constrains their options by controlling the timing of disbursements and dictating how the funds should be used. Furthermore, these small countries cannot change the way the IRB operates because they are denied meaningful representation on the IRB Council.

This article also extends the literature on financial and non-financial performance in sport, which has previously been focused at club level (Pinnuck and Potter, 2006; Panagoitis, 2009). In the context of national sporting bodies, sponsorship is more forthcoming when a team performs well on the field. This may explain why the FRU has emphasized the on-field success of its teams at World Cups. Some of the FRU’s senior managers have even cited on-field performance as justifying financial losses and demonstrating accountability for expenditure. However, the emphasis on financial performance in the professional era has drawn rugby away from its original amateur values, where rugby was played for “God and country”. In this context, board members who never played rugby are essentially a metaphor for those who are not bound to the amateur values of rugby union and therefore will have no personal conflict in emphasizing the need for strong off-field performance. These board members and other “commercial thinkers” may encounter resistance from those who still cherish rugby’s amateur values.

Finally, this article extends the literature on accounting and sport by showing that sport and accounting have been used independently and jointly as tools of control. Powerful stakeholders exert hegemony through their control of financial resources and governance structures. Although international and domestic donors have used the FRU’s accounting reports and their own financial power to hold management responsible for financial losses and mismanagement, these same stakeholders may have an interest in keeping sporting bodies afloat, even when they are technically insolvent. Cooper and Joyce (2013) demonstrated a similar phenomenon in the context of the Scottish Premier League. In relation to rugby union, the IRB benefits from Fiji’s continued participation, particularly on the international Sevens circuit, where it is among the top-ranked teams and able to draw significant crowds. This contributes to the IRB’s revenue streams from gate-takings and broadcasting rights. Fiji’s participation also serves the IRB agenda in terms of developing Tier 2 nations. Domestically, rugby has continued to receive government grants and bail-outs because of its national importance and public interest in the sport.

During the amateur period, the British colonial administration used rugby to exert its control over indigenous Fijians by subtly diverting their physical energy and inclination for warfare into sport. This provided the British colonial administration with a cost-effective way to control the indigenous population. Therefore, rugby fulfilled a similar role to the taxation systems based on agricultural produce which have previously been documented by Davie (2005a). British hegemony extended as far as advocating the rugby union code and discouraging Fijians from signing with rugby league scouts, despite the opportunities that league offered in terms of migration and improved income. Hegemony continues in the neo-professional period where the IRB’s decision to embrace professionalism has allowed more affluent nations to exploit the natural talent of rugby union players from less developed Pacific nations which cannot afford professional rugby contracts. This is cost effective for countries like Australia, New Zealand, France and Japan, since Pacific nations provide source markets which yield an abundant supply of rugby talent. Player mobility has increased significantly in the professional period, since overseas clubs pay lucrative salaries to recruit the best international talent. Player migration may benefit Pacific Island players through better incomes and greater financial security. Migration may also benefit Pacific economies through remittances from players, although these funds are unlikely to be channelled into developing rugby union. However, player migration ultimately allows more affluent nations, including the Tier 1 countries, to exert hegemony by extracting the best rugby talent from Pacific nations and weakening the standard of domestic competition.

Footnotes

Appendix

Acknowledgements

The authors acknowledge valuable comments and suggestions on an initial version of this article by participants at the Accounting History Special Interest Group at the Accounting and Finance Association of Australia and New Zealand (AFAANZ) Conference held in Perth, Australia in June 2013. The authors also acknowledge the valuable suggestions of the anonymous reviewers.

Funding

This work was supported by a research grant from the Faculty of Business and Economics at the University of the South Pacific.