Abstract

The article aims to examine the history of Vietnam’s accounting practices and standard setting in the context of its transition towards a market-based economy. Vietnam is chosen as a case study because of its unique combination of factors and the accelerated changes occurring in recent years. More specifically, the article has three research objectives: (1) to explore the distinctive stages in the evolution of accounting practices in Vietnam, (2) to explain the institutional pressures that have shaped the evolution of accounting standards in Vietnam and (3) to understand the implications of these historical developments on the changes in Vietnam’s accounting standards. To achieve these research objectives, we employ a theoretical framework that incorporates elements of the institutional theory to the 7Ps model proposed by Carnegie and Napier. This framework analyses the issues under study in terms of the seven dimensions: periods, places, people, practices, propagation, products and profession.

Introduction

The principal aim of this article is to critically examine how accounting standards in Vietnam (Vietnamese Accounting Standards (VAS)) evolved over time, particularly in the last 160 years in the context of political change, economic reform and international integration. Vietnam was selected as a case study in view of its unique combination of factors and the accelerated changes that have taken place in recent years (Nguyen and Richard, 2011). First, it is a transition country. Its gradual transformation from an inward-looking, centrally planned economy to an outward-looking, market-based economy provides an interesting opportunity to study how accounting standards evolved in response to institutional changes. Second, due to its history over the past 160 years, accounting in Vietnam was influenced by accounting conventions in France, China, the former Soviet Union and the United States (Nguyen, 2016). Third, it is an important emerging country with a sizeable population, rapidly growing economy and expanding international and investment trade ties (United Nations, 2015). Its experiences in accounting standard setting may thus be of some assistance to other emerging countries. Fourth, from an academic perspective, the changes in accounting and auditing standards in Vietnam have been relatively under-researched (Nguyen and Kend, 2017). Furthermore, a systematic study of the evolution of VAS using an accepted historical framework for accounting research seems to be still missing.

To achieve the overall objective mentioned above, the following three related research questions can be identified:

What are the various stages in the evolution of accounting practices in Vietnam? What are the institutional pressures that shape the evolution of accounting standard setting in Vietnam? What are the implications of these historical developments on changes in Vietnam’s accounting standards?

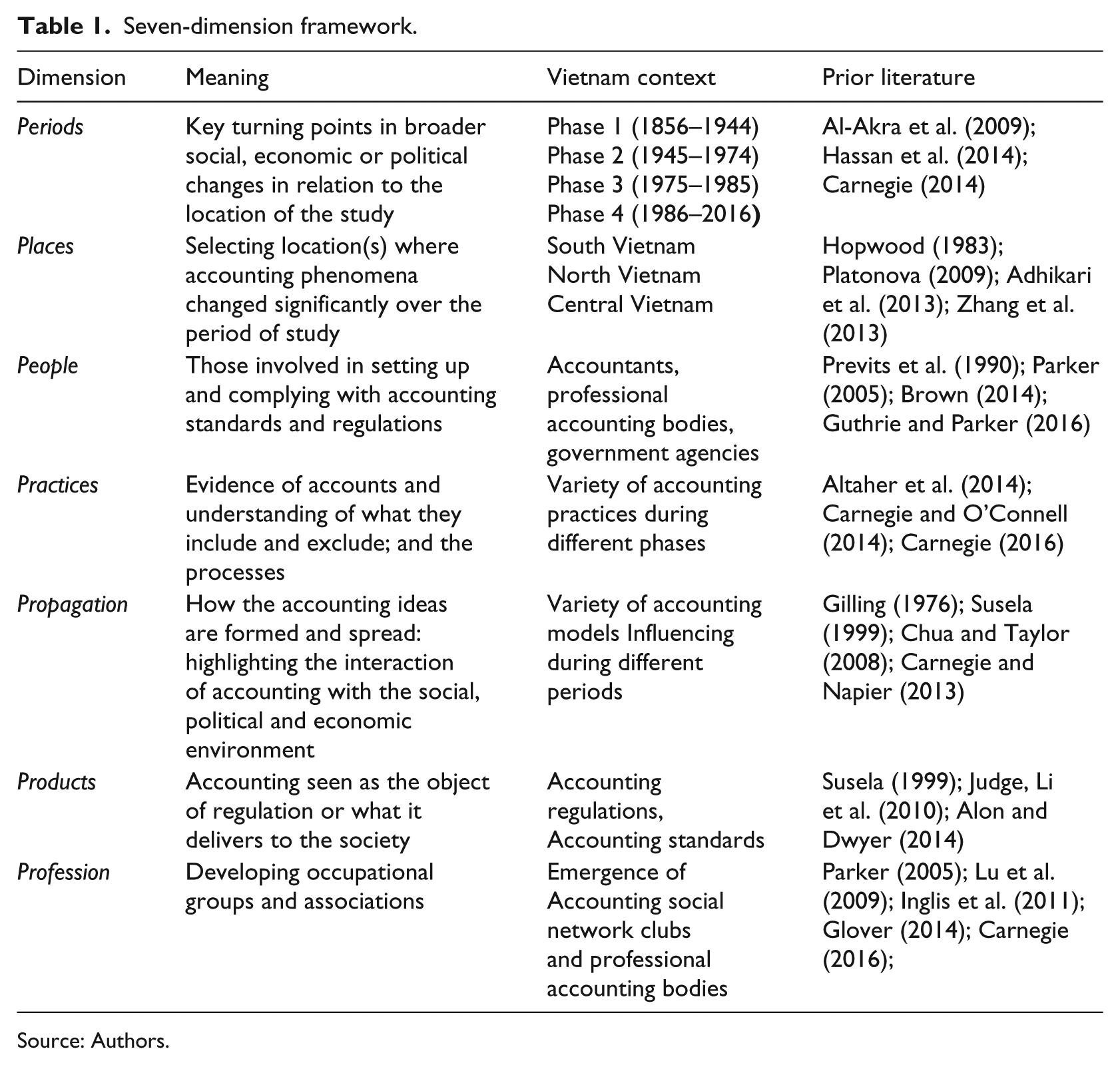

In answering the above questions, the article employs a theoretical framework that incorporates elements of the institutional theory into the 7Ps model proposed by Carnegie and Napier (2002). The 7Ps model is a widely accepted approach in accounting history research. It analyses the issues under study in terms of seven dimensions: periods, places, people, practices, propagation, products and profession. To the best of the authors’ knowledge, the present article is the only study that formally employs an explicit theoretical framework to assess the evolution of accounting standard setting in Vietnam.

By examining the process of development of accounting standards in Vietnam, the article makes three contributions to the International Financial Reporting Standards (IFRS) literature in general and accounting history literature in particular. First, it contributes theoretically to the accounting history literature by applying the 7Ps framework and interpreting the findings in terms of the neo-institutional theory by DiMaggio and Powell (1983). Second, the study of IFRS implementation in Vietnam from the institutional theory perspective not only adds to the IFRS literature but also guides others such as the Association of Southeast Asian Nations (ASEAN) and similar countries in the process of IFRS adoption. Third, the article provides a practical contribution by making some suggestions to the International Accounting Standards Board (IASB) on how to handle the global IFRS transition in emerging economies, which have agreed to participate in the movement to a single set of globally accepted accounting standards, in spite of the challenges imposed by their different histories, cultures and local institutional factors.

The remainder of the article is organised as follows. In section ‘Background and motivation for the study’, a historical overview of the accounting system in Vietnam and motivation for the study is provided. Section ‘Literature review’ presents a review of the relevant literature of English-language studies on accounting standards setting. It is shown that, in this respect, Vietnam can be regarded as one of the relatively under-researched countries. In section ‘Theoretical framework’, the theoretical framework for analysing the three research questions is discussed. Section ‘Findings and discussion: Historical review of the accounting system in Vietnam’ then applies this framework to examine the evolution of accounting practice and accounting standards in Vietnam. It is argued that a combination of international pressures and cooperation has driven changes in accounting practices and accounting standard setting in Vietnam. Section ‘Concluding remarks’ will conclude.

Background and motivation for the study

During its history, Vietnam has been controlled by other more powerful and dominating foreign countries, including China (about a thousand years), France (about 70 years) and Japan (about five years) (Doan and Nguyen, 2013). Under Chinese domination, Confucianism became the foundation of the social and education system in Vietnam. During this period, changes to the self-sufficient Vietnamese economic system could be characterised by the introduction of new economic sectors in addition to traditional agricultural and handicraft industries. Under the new colonial capitalist system, the introduction of light industry was one such example of French influences in Vietnam (Chu, 2004; Bui, 2011). According to Chu (2004) these economic changes were mainly due to France’s exploitation which turned Vietnam into a growing economy in mining, textiles, agriculture, construction and transportation and as a provider of natural resources.

After China, France colonised Vietnam from 1887. French colonialism (1887−1954) brought major changes into Vietnam, politically, socially, educationally and culturally. Vietnam moved from an essentially autarkic economic system towards a colonial capitalistic system with new economic sectors including light industry, trade and finance in addition to the traditional economic sectors of agriculture and handicraft. The previous Vietnamese writing system based on Chinese characters was replaced by a new Vietnamese script sourced from the Latin alphabet, created by French and Spanish clergy. The widespread acceptance of the modern, alphabet-based Vietnamese script over that of traditional Chinese is strong evidence for the open and flexible attitude of Vietnamese when exposed to interferences from other cultures (Duiker, 1983). In terms of economic policy, the French exploitation turned Vietnam into a provider of natural resources. Economic development during the French colonial period was primarily based on mining, agriculture, textiles, construction and transportation.

In the early 1920s, Vietnam opened its markets to the rest of the world, interacting with foreign cultures including the democratic cultures of Western countries. As a result, a number of Vietnamese revolutionary organisations evolved, emerging from a new worldwide trend in ideological thinking in Marxist−Leninist thought. Supported by the international communist movement, Ho Chi Minh led the Communist Party of Vietnam (CPV) to unite all the Vietnamese revolutionary parties between 1930 and 1944 (Corfield, 2008).

Vietnam suffered both French and Japanese colonial rule between 1941 and 1945 and the Japanese presence in Vietnam attracted the attention of the United States (Bradley, 2003). The United States wanted to protect its imports of raw rubber, half of which came from Vietnam. Soon after the withdrawal of the French army from Vietnam, the United States entered Vietnam, Laos and Cambodia under the pretext of preventing the spread of communism in Indochina (Tonnesson, 2010). An internal civil war between North Vietnam and South Vietnam ensued. The North Vietnamese government was supported by the Soviet Union, China and other communist countries, while the South Vietnamese government was supported by the United States, Australia, South Korea and other US allies.

Subsequent to French liberation in 1954, the Chinese accounting model was followed in North Vietnam during 1955 to 1960. After, 1960, North Vietnam followed the Soviet Union accounting model for 15 years until the withdrawal of the US from the South and the unification of the country in 1975 (Bui, 2011).

Vietnam was eventually reunited on 30 April 1975 with withdrawal of the United States from the South and the victory of the North Vietnamese communist government. The CPV formally renamed Vietnam ‘the Socialist Republic of Vietnam’ and led Vietnam towards socialism. The CPV extended the centrally planned economic model, which was based on a Soviet economic model and previously applied in the North, to all provinces in Vietnam between 1975 and 1980. Under this model, private ownership was replaced by state ownership. All key businesses were owned, controlled and managed by the State and, hence, are referred to as state-owned enterprises (SOEs). Private South Vietnamese businesses that had been operating under the pre-1975 capitalist models were obliged to transform themselves into SOEs (Vu, 2012).

Chinese influence in Vietnam increased considerably during 1949–1959 as the Chinese language was introduced in most schools in North Vietnam, and Chinese officials trained Vietnam accounting officials along with other officials in different departments. The impact of this influence was evident in the decision of North Vietnam government to introduce industry-based accounting, more specifically accounting for industrial and capital construction sectors (Sarikas et al., 2009). On the similar lines, Olsen (2006) and Bui (2011) also noticed the training and development activities organised by Chinese officials in North Vietnam.

After the period of Chinese influence (1960–1975), the Vietnam accounting system was influenced by the Soviet accounting philosophy in respect of accounting and record maintenance. Similar to the previous period of Chinese influence, the period between 1960 and 1975 experienced the training and development of Vietnamese accountants and other relevant personnel, and technical assistance support by the Soviet Union (Chu, 2004; Bui, 2011). During this period, the Soviet accounting model was modified to make it more suitable to the needs of Vietnamese industry. Nguyen et al. (2012) and Bui (2011) reported that Vietnamese accounting practices used 12 journal vouchers instead of 17 employed in the Soviet Union accounting system.

The history of early accounting developments in Vietnam suggests that there were no accounting or accounting standards in Vietnam and this may be due to non-existence of professional accounting bodies or less active groups of professional accountants. Accounting practice was primarily regulated by the Ministry of Finance (MoF) and the State played a dominating role in regulating and running the affairs of the accounting profession in addition to its primary function of ensuring the country’s economic development (Bui, 2011).”

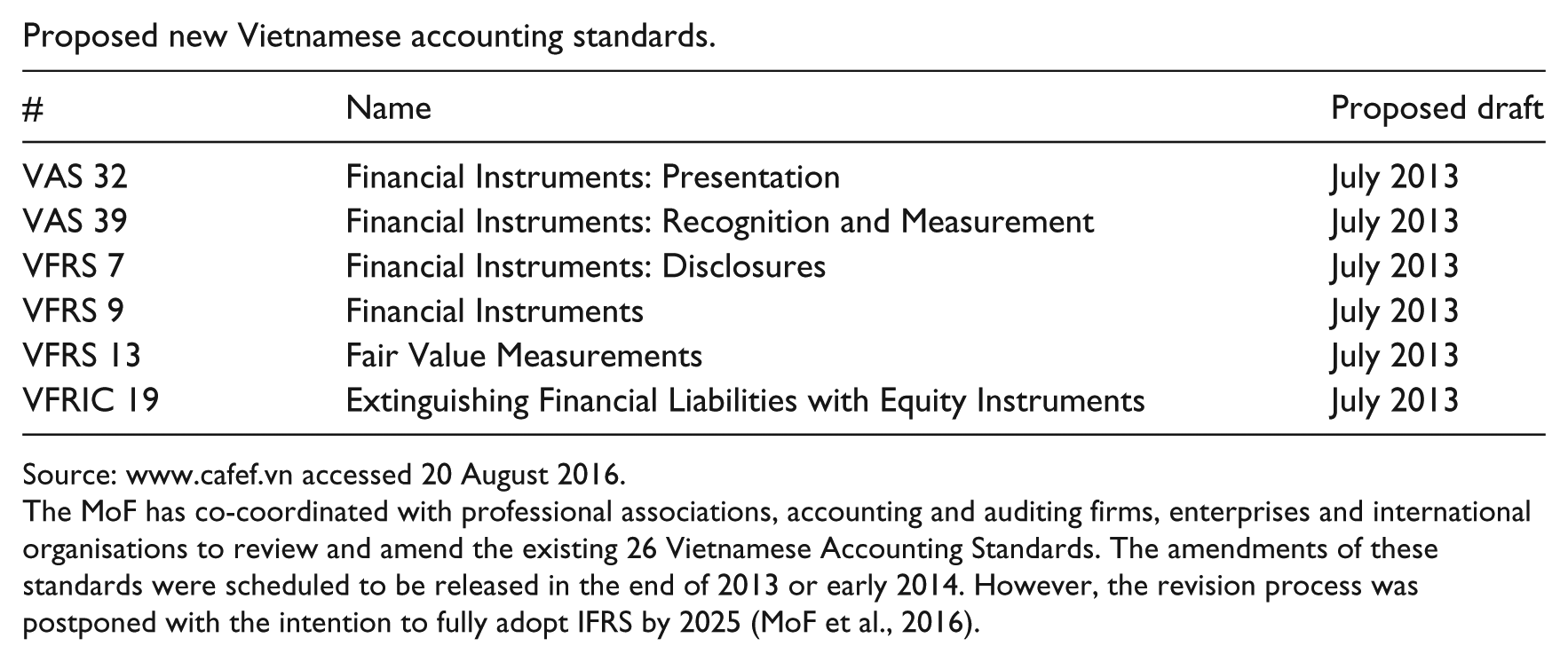

In the last three decades, Vietnam has been witnessing a rapid growth of the accounting profession, substantial changes in the accounting systems, connections with international professional accounting bodies and participation in the international harmonisation move initiated by the IASB through its acceptance of the IFRS. For example, in 2006, the MoF replaced the old 1988 accounting system with the new Enterprise Accounting System with the objective of aligning financial reporting requirements with accounting standards. All business organisations incorporated in Vietnam, despite ownership and listing status, are required to comply with this new enterprise accounting system. In the same spirit, in 2011, the MoF formed the Vietnamese Accounting Standards Board (VASB) to revise the existing VAS (Appendix 2) and published new standards to align with the current IFRS. Finally, in 2016, the MoF organised a series of IFRS workshops to obtain feedback from Vietnamese accounting academic and practitioners on IFRS adoption approach and its implementation roadmap for 2025 (MoF et al., 2016).

In summary, Vietnam is a growing economy located in the ASEAN region and has witnessed various streams of social, economic and financial models influenced by its historical and political developments in the past 160 years. These historical influences have significantly shaped the development of the accounting profession in Vietnam, including the development of accounting standards. Moreover, Vietnam’s willingness to participate in the move towards greater international globalisation and the VASB’s updating of the accounting standards in line with IFRS have resulted in fast changes in the accounting profession in this country. The abovementioned historical developments in Vietnam and current trends in Vietnam accounting practices are the primary motivation for this study as this study presents a unique location for understanding the evolution of accounting practices that have been influenced by multiple political and institutional factors. The article explains the history and process of accounting standard setting in Vietnam in the political and economic context of this transition.

Literature review

The conceptual nature of this article is set in transitional economies where Western models of accounting are implemented in countries with diverse histories, sociologies and economic systems. The process of this change is mediated by multiple factors that are beyond accounting as a procedural framework. It elevates the experience of an accounting researcher into an equivalent of a social science researcher. The nature of investigation extends into a multi-disciplinary framework. The difficulty of this task is multiplied because of the highly rigorous academic literature existing in this field. Many authors (e.g. Burchell et al. (1985); Cooper et al. (1998); Robson (1991); Miller and Napier (1993); Bailey (1995); Richard (1995); Mennicken (2008, 2010) have already established a very serious reputation in this domain. This kind of literature review makes the task of a researcher both difficult and easy. It is difficult because the conceptual scale of these works is highly comprehensive but it is also easier. As one comprehends the rigour of the exercise, it becomes a targeted exercise in terms of research goals.

Burchell et al. (1985) revealed in their value adding accounting approach in the United Kingdom its significant social importance. They highlight that an accounting event has specific social reasoning behind its origin. There are issues, institutions and processes involved in this. Robson (1991) extended the specificity of social content into a generalised social environment and located the entire question within the accounting and social changes through a metaphor of translation. Of course, translation here does not only mean linguistic translation but also includes cultural, social and practice-oriented interpretation. It underlines one important fact that audit universalisation may not be seen as delicate an exercise as it seems to be. It may carry with it many invisible forces. Miller and Napier (1993) added a further layer by postulating accounting history within a larger set of genealogy of calculations as if it operates within a larger universe of social anthropology. They posited that accounting as a discipline is an offshoot of a larger need of calculation which is a historical contingent matter and not just a disciplinary one. Bailey (1995) elaborated it with a study of central and east European states in the post-Soviet era when market economies started emerging amidst a complete lack of independent audit firms or an accounting community. From a state-centric accounting system where no autonomous price mechanism exists, the system shifts to a market-based model where prices carry serious economic information. Therefore, the system of accounting is a derivation from the historical change of regime and not vice-versa. Despite being from a common communist system, the post-communist accounting order took two different trajectories (Richard, 1995). Romania copied the French model because of political and cultural reasons, whereas Russia embraced the traditional model derived from Schmalenbach’s chart of accounts steering towards the American systems.

Cooper et al. (1998) took it further into the operational experience of a big accounting firm when it entered Russia. Although the obvious goal was to extend the predominance of the Western accounting systems, the on-the-ground experience of working was unchanged. The actual practice of these goals is mediated through managerial identities, nationalistic feelings and even political values too. Such a case study method illustrated by authors delves deep into the field of globalisation/uniformisation of accounting systems. Mennicken (2008, 2010) highlighted further that such an audit universalisation and global comparability of financial reports is just not an outcome of simple division of labour; rather, this process encounters deeper problems embedded in power distribution and exclusion as well as intra-professional struggles. The critical element is linked ecologies of audit and market where the authors detail the rise of Russia audit firms to portray the fact that market demand for audit firms defined the evolution of a profession and not the other way round. Therefore, in post-Soviet Russia, audit firms are more of a market- and power-related phenomenon and less of a technically skilled set of globally distributed professionals.

To put it in perspective, accounting standards may seem as global and universal at the outset but in reality, the implementation challenge is mediated by multiple factors. In no way can the ecologies of accounting practice be ignored. Their range is huge though in most studies, the predominant factor has been nation, national identity or national history. This is not to deny the variety of the forces at play; rather, this is to highlight that a national zone becomes the largest carrier of multiple narratives within which accounting operates. Ideas may come from outside but accounting as a policy choice (Stadler and Nobes, 2014) is predominantly mediated by factors like country, industry and sectoral topics in order of importance.

Seven-dimension framework.

Source: Authors.

A decision to adopt IFRS is a radical departure from multiple perspectives and it would be an influenced as well as influential decision. McEnroe and Sullivan (2013) investigated the perceptions of auditors and chief financial officers for choosing between rules-based and principles-based accounting standards in the context of US Generally Accepted Accounting Principles (GAAP) versus IFRS. Interestingly, eight out of 10 professionals supported the use of rules-based standards as it was already embedded in the practice domain. This bias is confirmed again in another study by Braun et al. (2015) where auditors’ choice for rules-based standards is preferred despite auditor’s reservations. These studies hint at the fact that accounting standards cannot function in a top-down manner; rather, their effectiveness is achieved by a complex set of factors that are locally prevalent and are practice-oriented. That is why without changing the institutional framework, no serious choices of practice or attitudes can be made. These choices can be critical as well as implementable too as Joshi and Ramadhan (2002) paint an encouraging picture of adoption of International Accounting Standards (IAS) by Bahrain.

Larson and Street (2004), while studying the history of IFRS adoption in the European Union (EU), examined the progress of the system into ‘two standards’ where listed firms adopted the new standards and non-listed firms could continue with existing practices. This anomaly may be because of numerous factors related with nature of convergence, health of capital markets, training infrastructure of accounting professionals or lack of fully viable IFRS-compliant transactions in areas like pensions. Jermakowicz (2004) pointed out the impact of IFRS-like accounting systems on matters of finance and strategy. Nurunnabi (2015) examined the cultural factors behind the adoption and implementation of new accounting standards. Poudel et al. (2014), through case analysis in Nepal, highlighted that IFRS adoption was not supported by local accounting ecologies; rather, it was necessitated by their need for external funding from global bodies. Hassan et al. (2014), while studying IFRS adoption in Iraq from the perspective of institutional isomorphism, realised that coercive isomorphism was critical. Since the end of the Baathist regime, the most pressing need for Iraq was aid from foreign bodies. International military relations in Iraq were also a subtext not out of bounds when new accounting standards were adopted. There is much more to this as standards setting has to meander through many more treacherous paths.

Xu et al. (2013) explored the institutional settings through a unique perspective of ‘cultural hegemony’ as proposed by Gramsci. It is a study of four periods of Chinese history: Confucian period, Maoist period along with that under the Cultural Revolution and Deng period from late 1970s. In these periods, the authors highlight the deep impact of political leadership and ideology on the systems of accounting. The accounting institutional framework was a subset of hegemonic structure imposed by a prevailing political regime. Lu et al. (2009) confirmed the predominance of government’s role in accounting standards’ setting too. This is unlike many nations where the accounting profession leads the development of accounting not the State. Assenso-Okofo et al. (2011) also emphasised the role of institutional factors along with legal, political and economic factors in the evolution of accounting standards in Ghana that has fully adopted IFRS recently. Irvine (2008), while investigating the case of the United Arab Emirates’ (UAE) adoption of IFRS, observed serious isomorphic pressures that belong to all three categories of coercive, normative and mimetic. Within this context, it is reiterated that accounting standards setting is a function of a comprehensive set of factors and they need to be considered in any conceptual framework of accounting standards.

The broader framework of this article is focussed upon exploring past Vietnamese accounting institutions and practices from the nineteenth century till the present so as to develop a chronological sequential effect on the future of the same systems. Such a comprehensive task requires elaboration as well as authentication from various cross-border and inter-disciplinary studies. Some authors (e.g. Albu et al., 2014; Stadler and Nobes, 2014) confirmed the deep inter-linkages of such studies. Albu et al. (2014), while exploring the case of IFRS adoption in Romania, highlighted the importance of local factors as well as their depth and diversity. Rodrigues et al. (2012) explored the history of twentieth-century Brazil through a series of significant events that had serious influence upon the development of financial reporting culture. These are very diverse beginnings from the birth of Brazilian accounting profession in 1931; the impact of American trade as well as their accounting system; the 1960s period of high inflation, development of stock market, financial market reforms and finally the emergence of IFRS adoption in 2007. Furthermore, Muniandy and Ali (2012) found that the colonial past of Malaysia has significantly impacted the financial reporting environment of the country. This encompasses multiple factors like those of social, economic, political and regulatory culture too. For standards setting, serious inputs on such issues are very critical in terms of charting out an adoption trajectory of new accounting standards.

Narayan et al. (2000) observed the correlation between the histories of development of accounting in Vietnam and admission that Vietnamese accounting practices have created a strong connection between military, social and trade practices in Vietnam over recent decades. With similar observations, Adams and Do (2003) concluded that the history of accounting development in Vietnam has paralleled the political history and economic conditions of the country. Doan and Nguyen (2013), while investigating the period from mid-1980s to the present era of VAS, identified their hybrid nature as being a mix of Western style of accounting and Soviet- and French-style systems of financial reporting. This elaboration is narrow and further historical research as well as a conceptualisation framework too. Nguyen and Richard (2011) investigated and challenged the history of Vietnamese accounting system as to why there were two different accounting systems, that is, Uniform Accounting System (UAS) borrowed from the old system of the planned economy and VAS modified from the IAS. This article focusses upon the Vietnamese trajectory of IFRS adoption and the hidden challenges facing it. Vietnam does not have a singular national history: it was a colony for many years; even after its independence, it was impacted by multiple sets of foreign political and military influences, and then, it made a significant shift from a centrally planned economy to a market-based economy. This all has happened in a span of just over 100 years. Accounting systems cannot remain unaffected in these distinct historical shifts. Institutional responses, legal and corporate frameworks and executive decisions are all embedded in this journey. Therefore, this is a continuous process of mutual reactions and adaptations.

Theoretical framework

Accounting history dimensions

The article conducts a study of accounting development in Vietnam using the accounting history framework proposed by Carnegie and Napier (2002). This approach presents a chronological record of development of accounting practices in Vietnam along with the factors influencing the changes in accounting in the Vietnamese context such as colonial, cultural and political influences. Carnegie and Napier (2002) argued that contemporary accounting practice/regulation in any country is an outcome of innovations across the globe rather than regulatory evolution and influencing factors within that specific country. These dimensions include periods, places, people, practices, propagation, products and profession. Table 1 explains how we have used these dimensions to explore the history of development of accounting standards in Vietnam.

The abovementioned dimensions in the Vietnam context will be used to explain the development of the accounting profession and practice in Vietnam. The scope of this article covers periodical developments of accounting regulation and the emergence of professional bodies in Vietnam; therefore, we focus on periods, places, propagation and profession as explanatory dimensions. However, the remaining three dimensions are briefly discussed in the Vietnamese context. It is believed that these three dimensions will be further explored by researchers who are primarily interested in studying the emergence of the accounting profession in Vietnam.

Institutional theory

Institutional theory provides valuable insights into understanding the behaviour and actions of regulators in the face of ever-increasing adoption of IFRS globally. Institutional theory presumes that organisations respond to pressures from their environment by adopting best management practices and structures (Meyer and Rowan, 1977). New institutional sociology posits that various components of formal organisational structure, policies and procedures develop from established societal attitudes of what constitutes conventional practice and the views of significant constituents (Scott, 2008). Campbell (2007: 946) contended that “the relationship between basic economic conditions and corporate behaviour is mediated by several institutional conditions including: public and private regulation” and the presence of nongovernmental and other independent organisations that monitor corporate behaviour.

Organisations and, in this case, countries adopt these rules and structures to maintain and enhance their legitimacy and resources (Kondra and Hinings, 1998). Rules, accreditation processes and public opinion together make it critical or, at least, advantageous for organisations or countries to embrace the new structures. Furthermore, influential organisations or stakeholders seek to impose their aspirations directly on the social order. These pressures to achieve legitimisation help initiate isomorphism. This is a process that forces one unit in a population to resemble other units that face the same set of environmental conditions (DiMaggio and Powell, 1983). Institutional isomorphism promotes the success and survival of organisations (Meyer and Rowan, 1977). Hence, enterprises vie not merely for funds and clients but also for political influence and institutional legitimacy, for social as well as economic correctness (DiMaggio and Powell, 1983). An important concept in institutional theory is isomorphism. Three mechanisms of isomorphism were proposed by DiMaggio and Powell (1983), which include coercive, mimetic and normative isomorphism.

Coercive isomorphism is represented by ‘rules preserved in regulatory systems’, and can take in ‘pressures from the global networks of multinational corporations’ (Guler et al., 2002: 212−213). In the context of developing countries, the two primary organisations that represent a major global institutional force are the World Bank (WB) and the International Monetary Fund (IMF). Some researchers argue that these international lending agencies push developing countries to adopt IFRS or develop national standards based on IFRS as a mandatory requirement of their loans (Irvine, 2008; Phan et al., 2016b).

Mimetic isomorphism can be defined as achieving conformity through imitation and is regarded as ‘a simple and efficient reaction to uncertainty’ (DiMaggio and Powell, 1983: 151). It reflects a desire to mirror others’ practices that are recognised as superior or more successful (Scott, 2008) and in situations where there are uncertainties about the proper approach to proceed, mimicking the actions of a successful reference group is recommended. Mimetic pressures come from trade partners and multinational corporations. Globally, multinational corporations have contributed to the increasing desirability of expanding and accepting the harmonisation of financial reporting.

Normative isomorphism refers to legitimation by aligning to professional values ‘stemming from a code of conduct exerted by professional bodies and further reinforced by university education and professional training programs’ (DiMaggio and Powell, 1983: 152). In other words, normative isomorphism refers to pressures, which are brought about by professions. In this regard, the accounting profession may carry out various activities to promote better accounting practices while aiming to enforce the adoption of the perceived high-quality accounting legislations (Phan et al., 2016a). Similarly, global accounting firms (such as the Big Four) can also generate normative pressures in accounting legislation (Phan, 2014; Rodrigues and Craig, 2007).

Overall, research reveals that IFRS adoption in developing countries is subject to coercive, normative and mimetic institutional pressures from multinational lending agencies, capital markets, the Big Four accounting firms and the IASB (Judge et al., 2010). These factors have influenced the consideration of the standard setters of developing countries to adopt or permit reporting under IFRS (Phan and Mascitelli, 2014).

Findings and discussion: historical review of the accounting system in Vietnam

This section presents the history of accounting standard setting in Vietnam as an emerging transition economy and the social political economic factors that have influenced it. We rely on the 7Ps framework introduced by Carnegie and Napier (2002) as discussed above.

Periods

The first ‘P’ – periods – represents the period between 1856 and 2016. We propose to breakdown this period into four phases, corresponding to four distinctive political and economic stages of Vietnam. The first phase is characterised as the French and colonialist economy (1887−1954). The second phase includes the internal war period between North and South Vietnam from 1954 to 1975, with both regions building war economies. The third phase is the first decade of reunification and socialism building under a centrally planned economy (1975−1985). The last phase between 1986 and 2016 is characterised by the well-known ‘Doi Moi’ (renovation) transition towards globalisation and a market-oriented economy. The choice of Vietnamese accounting model is strongly correlated with the political and social economy of Vietnam in each historical phase. Overall, the development of accounting in Vietnam can be divided into four phases:

Phase 1 (1856−1944): French influence due to French colonialism. Phase 2 (1945−1974): Chinese and Soviet influences in North Vietnam and American influence in South Vietnam. Phase 3 (1975−1985): Soviet influence continues after the independence and reunification of Vietnam. Phase 4 (1986−2016): the evolution of VAS, the convergence progress towards international accounting best practices (IFRS convergence).

Changes in accounting during these phases will be explained by institutional theory. This theory highlights that organisational changes are influenced by socio-political changes over time. For example, French rule influenced Vietnamese businesses and accounting practices to meet the requirements of French colonial administration, whereas accounting practices in the second and third phases were influenced by China and Soviet Union accounting models. These examples explain the presence of coercive isomorphism in the first three phases of Vietnam accounting developments. Mimetic isomorphism and normative isomorphism are present only in the last phase, and these shall be discussed in more detail in the propagation section.

Places

The second ‘P’ – places – is Vietnam, described as an emerging economy, geographically located in South East Asia among Asian-oriented cultures, and having been economically and politically influenced by socialism. The unique character of Vietnam with its political and military upheaval means that for the purpose of analysis, the country is divided into different regions: North, South and Central Vietnam. For example, during the French colonial period, Vietnam was divided by France into three parts with different and autonomous political systems. North Vietnam was known as ‘Tonkin’ in French or ‘Bac Ky’ in Vietnamese, under French semi-protectorate. Central Vietnam was known as ‘Annam’ in French or ‘Trung Ky’ in Vietnamese, under a French protectorate. South Vietnam was known as ‘Cochinchina’ in French or ‘Nam Ky’ in Vietnamese, under French colonial control (Corfield, 2008).

People

The third ‘P’ – people – represents different stakeholders involved in accounting regulatory processes which mainly includes the government, accountants and accounting professional bodies. There have been different stakeholders and accounting functionaries during different phases of accounting developments in Vietnam. For example, during Phase 1, accounting work was undertaken by French accountants rather than the locals and they reported back to their home country. Vietnamese workers simply played a bookkeeping role under instruction of French accountants. Similarly, in Phase 2, these groups of stakeholders revolved around two setups, that is, the socialists in the North Vietnam and the capitalists in the South Vietnam. From Phase 3, the Vietnamese accounting community is unified as a socialist group (Puxty et al., 1987).

Driven by French, Soviet and American influences, the Vietnamese government used a selective accounting system between 1986 and 1997 to determine its accounting practice for the transition of its economy to a market-oriented economic system from an unsuccessful centrally planned economy. The case of accounting developments in Vietnam differed from other South East Asian nations in spite of Vietnam’s colonial heritage. From Phase 3, the State played a key role in developing the accounting profession and regulating the accounting practice. The State directly influenced the development of the accounting profession through their direct involvement in the accounting practice and the training of the accountants with a view to ensure the success of the state’s economic and political agenda. The agreement between the MoF and the Association of Chartered Certified Accountants (ACCA) to operate a joint examination scheme to provide internationally recognised qualifications to Vietnamese participants though a Memorandum of Cooperation signed by both bodies in December 2003 can be seen as a clear indication of government’s intensions to control and regulate the accounting profession and the supply of future accountants.

The Vietnamese government, motivated by its socialist agenda, has worked for the upliftment of the various sectors in the society including regulating and promoting the accounting profession in Vietnam. With this socialist objective in its operating philosophy, the Vietnamese government (the state) has had to influence the development of the accounting profession and accounting practice in Vietnam. To achieve this objective of developing and promoting the accounting profession, the Vietnamese Government established the Vietnam Association of Accountants and Auditors (VAA) and Vietnam Association of Certified Public Accountants (VACPA). Both the professional bodies were regulated by the state and thus provide evidence of direct control of the state over the accounting profession and the practice. Similar to the case of the Chinese accounting profession, the Vietnam government maintains its control in the accounting and auditing certification and accounting practice through the MoF.

The accounting profession in Vietnam is a state-controlled profession and is subject to state regulations. Only MoF has the authority to issue Vietnamese CPA certificates. Being foreign professional bodies, the ACCA and CPA Australia are not able to compete with the VAA and VACPA, due to the fact that these professional bodies are set up by the MoF. However, the ACCA and CPA Australia have signed cooperative agreements with the MoF to provide more opportunities for accessing internationally recognised qualifications to Vietnamese accountants and auditors. This agreement also enables the VAA and the VACPA to gain international knowledge and experience in managing their operations in Vietnam.

Practices

The fourth ‘P’ – practices – examines evidence of accounting and understanding of what they include and exclude, and the processes:

Phase 1: Accounting work and practice in this phase was regulated and controlled by the needs of French authorities to exercise control over revenues including export earnings, tax collections and expenditures (Chu, 2004).

Phase 2: Vietnamese accounting procedures in Phase 2 primarily included maintaining asset registers and inventory management procedures following the Chinese accounting model at the beginning and Soviet accounting model near the end of Phase 2 (Sarikas, Vu and Djatej, 2004). Similar accounting procedures have been highlighted by Bui (2011) arguing that accounting in this period was mainly used for recording double entry records for budget receipts and spending, including accounting for heavy industry, transportation, and recording of materials.

Phase 3: Accounting policies and procedures were used to record specific activities of individual industries (Yang and Nguyen, 2003). They further advise that MoF prescribed how the chart of accounts were prepared including financial reports, initial records, budgeting and accounting books.

Phase 4: This phase shows significant developments of accounting practice in Vietnam as the MoF introduced series of VAS between 2001 and 2005. The objective of this phase was to harmonise the Vietnamese GAAP with the best international accounting practices that are available, including the convergence of VAS to IFRS by 2025 (Phan et al., 2016a).

As discussed above, the accounting practices in the first three phases were influenced by the rules and regulations from the ruling nations. These findings can be explained by the elements of coercive isomorphism as coercion can be exercised directly and also indirectly influenced by the administrative agencies from the ruling countries (Hassan et al., 2014) by ensuring compliance by the similar bodies in the country being ruled. For instance, Vietnam being a colony was not only under direct political influence but also its accounting community was under the indirect influence of the corporate, tax and other regulatory bodies from the ruling countries. However, in the last phase, developments were influenced by indirect coercive isomorphism from multinational funding agencies such as the WB, IMF, Asian Development Bank (ADB) and the World Trade Organization (WTO). There is also an evidence of mimetic isomorphism that comes from the multinational corporations and global trade partners as Vietnam has witnessed a high growth in these business arrangements (Phan, 2014). The Vietnam government has promoted trade and investment relations with other countries in order to develop efficient capital markets in the country.

Propagation

The fifth factor – propagation – highlights the interaction of accounting with social, political and economic environment. Accounting was used mainly as a tool for planning and budgeting in the first three phases (1856–1985) and more as a reporting means only in the last phase (1986−2016).

Phase 1 (1856−1944)

In 1856, France controlled Vietnam, Laos and Cambodia; and these three countries were referred to as Indochine Francais (French Indochina). French colonialism in Vietnam lasted more than six decades, and during this period, France propagated Vietnam businesses to use French finance and administration schemas. For these reasons, it would be reasonable to expect that the French would have contributed to initiating the establishment and development of an accounting profession in Vietnam (Cumings, 2004). The French did not set up and develop accounting in Vietnam but they set up budgets which enabled them to control tax collection and earnings for the colony’s operation. It can be argued that the development of accounting in Vietnam was not established by the French during their domination but rather by the independent Vietnamese Government in the post-colonial period.

Vietnam businesses used French accounting systems during this phase to support the French administration. Adams and Do (2003) highlighted that through the Commercial Code in 1807, based on the Savary Code, issued in 1673, the government made it mandatory for businesses in Vietnam to maintain accounting books for accounts and a central ledger. This implies coercive isomorphism as explained by DiMaggio and Powell (1983). However, the Commercial Code did not prescribe how to prepare books of account (Wittsiepe, 2008). The purpose of propagation of French accounting work in Vietnam was to control revenues and expenditures through the exercise of centralised power and authority (Nguyen and Richard, 2011). Al-Akra et al. (2009) described colonisation as a strong force that facilitates a shift in a country’s accounting system, and we argue that Vietnamese accounting systems and practice in this phase were strongly influenced by the French. The French government also initiated the move of preparing budgets for each of Tonkin (North Vietnam), Annam (Central Vietnam) and Cochinchina (South Vietnam) to allow them to exercise central control of revenues, tax collection and export earnings and expenditures (Bui, 2011).

Phase 2 (1945−1974)

During Phase 2 (1945−1975), the Vietnamese accounting system was at a very early stage of development as it was mainly designed to serve the purpose of recording revenues and expenses of the government budget aligned with the Chinese accounting model. This highlights that Chinese socialism was a source of coercive isomorphism in influencing the design of the accounting model and practices in Vietnam.

Accounting regulation in Vietnam began with Decree 1535/VP/TQD dated 25 September 1948 titled ‘Regulation on Revenues and Expenditures and the General Accounting of the Democratic Republic of Vietnam’. After 1954, the Democratic Republic of Vietnam began the process of building socialism in the North; however, the economic system was not well developed as the country was at war. Consequently, the Department of Accounting Policy (DAP) was established in 1956 according to Decree No. 1076-TTG dated 11 October 1956. In 1957, the DAP issued the first two accounting regulations: the Accounting Policy for Industrial Enterprises and the Accounting Policy for Construction. Based on these two accounting regulations, the DAP issued industry-specific accounting policies such as accounting policies for commerce, transportation and agriculture (Chu, 2004).

The decade between 1961 and 1970 was the period of foundation setting of Vietnamese accounting. In the North, Vietnam’s socialist government issued the first 5-year plan with the intention to build the foundation of accounting system in Vietnam. Decree number 175/CP dated 28 October 1961 was the first high-level legal document to serve as a foundation for setting up the accounting system for the Vietnamese centrally planned economic system (Chu, 2004). The Vietnamese accounting system during this period was perceived as aligned with Soviet accounting practice. However, the Department of Accounting claimed that the socialist accounting practice in Vietnam was derived from that of China (Sarikas et al., 2009).

During the 1960s, the DAP issued a series of subsequent accounting policies to improve and strengthen the Vietnamese accounting system (see Appendix 1). In addition, the DAP issued different accounting policies which were industry-specific. However, until the end of 1960s, the Vietnamese accounting system was not considered to be a complete accounting system. The Vietnamese accounting system during 1961–1970 was mainly designed to serve the war economy in the North (Chu, 2004).

In 1970, the DAP decided to follow the Soviet accounting system. With the technical assistance from the Soviet accounting experts, the Vietnamese accounting systems started introducing voucher-journal bookkeeping system. This indicates the presence of coercive isomorphism from Soviet socialism in Vietnam, as explained in Phase 1. In Phase 2, the most important accounting regulation was Decree 176/CP dated 10 September 1970 titled ‘New Regulation for the Chief Accountant’. This decree expanded the role of the chief accountant as the State financial controller with the intention to reorganise and strengthen the accounting requirements at the level of state enterprises and organisations. Other noteworthy accounting policies during 1970s are listed in the Appendix 1.

Phase 3 (1975−1985)

The Vietnam War ended on 30 April 1975. North and South Vietnam were reunified to form the Socialist Republic of Vietnam. With the commitment to pursue socialism, the DAP brought the unified accounting system used in North Vietnam to South Vietnam. During this phase, the Soviet Union provided technical support for the DAP. Many Vietnamese accountants were trained overseas and in Vietnam to contribute their knowledge to continue building and improving the Vietnamese accounting system following the Soviet Union accounting model. Similar to Phase 2, it can be concluded that the Vietnamese accounting practices during this phase resulted from the Soviet coercive isomorphism. Accounting was used as a tool to manage capital and assets for the benefit of the State, one-sector only economy. However, the failed implementation of the second Five Year Plan (1975−1980) as a central planned economy led the country into crisis in the late 1970s. As a result, the government moved forward to the third Five Year Plan (1981−1985).

Under the third Five Year Plan (1981−1985), private enterprises were allowed more scope to operate independently from the State. The economy moved forward from the centrally planned model to a ‘three plan’ economic system (Plans A, B and C) in which the SOEs not only produce for the state using state-supplied inputs (Plan A) but also purchase inputs from outside, specialise their production (Plan B) and freely sell the surplus output to the market (Plan C). The ‘three-plan’ economy allowed enterprises to have more autonomy, and thus enhanced market-oriented behaviour within the SOEs (Riedel and Leung, 2001). However, there was no market for independent accounting/auditing services. Accounting services were mainly for taxation and statistical purposes of the government. There is also no evidence of the existence of an accounting profession in Vietnam prior to 1985. In summary, for a decade after reunification, the accounting regulations were solely to serve the economic and financial management demand of the State.

Phase 4 (1986−2016)

In 1986, the Sixth Congress of the CPV put forward a proposal to the National Assembly for the comprehensive renewal of the Socialist Republic of Vietnam. This reform process gave rise to the promulgation of the 1992 Constitution, which was based on a market-based economy, and the introduction of the Ordinance on Accounting and Statistics. This Ordinance was promulgated by order of the President of the State Council of the Socialist Republic of Vietnam, dated 20 August 1988.

The Ordinance provided regulations for the accounting and statistics standards to be applied to all Vietnamese enterprises in the national economy. The Ordinance required uniform implementation of all the accounting and statistics throughout the national economy. MoF and the General Department of Statistics have roles to play in completely regulating the system to standardise all the accounting and statistical forms.

The Law on Statistics of Vietnam, which replaced the Ordinance on Accounting and Statistics of 1988, was passed by the National Assembly on 17 June 2003, and came into effect on 1 January 2004. The 2003 law stipulated that the Prime Minister shall promulgate the National Statistical Indicators System (NSIS). To complete accounting policies for private sectors and non-SOEs, Decision No 229/QD/CDKT (December 1988) and Decision No 598/QD/CDKT (December 1990) were issued, respectively. The chart of accounts and accounting reports were amended through Decision 212/QD/CDKT (December 1989) and Decision 224/QD/CDKT (April 1990), respectively (Government Office of Statistics (GSO), 2016). From 1994 to 1995, the first two accounting and auditing companies were established, specifically, the Vietnam Auditing Company and the Accounting and Auditing Service Company; and in 1994, the State Audit of Vietnam was founded (Huynh et al., 2012).

The period from 1986 to 2016 showed significant developments of accounting in Vietnam. During this period, Vietnam became a member of ASEAN and WTO. To qualify for these membership requirements, the MoF introduced a series of VAS between 2001 and 2005. The development of the VAS results from the technical and financial assistance of the WB, the ADB and the Euro-Tap Viet project (Nguyen, 2016). The objective of this phase was to harmonise the Vietnamese GAAP with the best international accounting practices that are available (Narayan et al., 2000).

During Phase 4, the IFRS convergence in Vietnam has been strongly influenced by institutional isomorphism. We argue that the WB and the WTO serve as a coercive force behind IFRS convergence in Vietnam. Albu et al. (2014) presented a similar argument that the relationship between domestic agencies (e.g. the accounting profession, the Ministry of Economic Affairs and the State) as well as international funding agencies (WB, IMF and ADB) produced institutional pressures to push the local accounting standard-setting body to develop financial regulations in accordance with IFRS. The Accounting Law 2003 establishes the legal framework for VAS for both public and private sectors. This body of law governs the principles of accounting, concepts and definitions of accounting, conduct and organisational structure of accounting practice, the Vietnamese accounting profession and the State control of accounting practice. In addition, this accounting law covers quality control benchmarks and professional ethics of the practicing accountants.

Key milestones during the period 2006−2016 include the following:

In 2006, the MoF replaced the old accounting system (1988) with the new accounting system (2006). The main objective of the accounting system (2006) was to align financial reporting requirements with IAS. All business organisations incorporated in Vietnam, despite ownership and listing status, are required to comply with this new accounting system. In 2011, the MoF formed the VASB and a project team of 44 members was organised to assist the VASB to revise the existing VAS and publish new standards to align with IFRS. In 2013, the VASB proposed six new accounting standards for capital markets and amendments for eight existing accounting standards. In 2014, the MoF replaced the accounting system (2006) with the new accounting system (2014) that brings Vietnamese GAAP closer to IFRS. In 2016, the MoF organised a series of IFRS workshops to obtain feedbacks from Vietnamese accounting academics and practitioners on the IFRS adoption approach and roadmap by 2025.

After almost three decades of economic reforms since the launch of Doi Moi in 1986, Vietnam has recorded significant economic achievements. From a poor, war-ravaged, centrally planned economy closed off from much of the outside world, Vietnam became a middle-income country with a dynamic, market-based economy extensively integrated into the global economy (WB, 2008). During this period, there has been much activity in Vietnamese accounting legislative systems with efforts from the Vietnamese government to reform the national accounting jurisdiction and thus boost the nation’s economic development to attract foreign investment. Most importantly, on 20 November 2015, the MoF issued Accounting Law No. 88/2015/QH13 (‘Accounting Law 2015’), which superseded the Accounting Law 2003. The Accounting Law 2015 will be effective from 1 January 2017, including 6 Chapters and 74 Articles, regulating the contents of accounting work, the organisation of accounting system, accountants, accounting services, State management of accounting and accounting professional organisations.

The key change of Accounting Law 2015 is the introduction of a fair value definition which abolished the key gaps between VAS and IFRS. Article 28 of Accounting Law 2015 regulates that assets and liabilities must be re-evaluated and recognised at fair value at the financial reporting date, including (1) financial instruments as required by accounting standards to be recognised and measured at fair value, (2) monetary items denominated in foreign currencies to be measured at actual exchange rates and (3) assets or liabilities which have frequent volatility in value as required by accounting standards to be re-evaluated at fair value. The fair value revaluation of assets and liabilities must be established reliably. Where there is no basis to determine a fair value reliably, the assets and liabilities are recognised at historical cost.

In the context of international accounting convergence towards IFRS, Vietnamese accounting reform progressed to a new stage. In 2014, to provide guidance for local and foreign enterprises, the MoF issued Circular No. 200/2014/TT-BTC (Circular 200) and Circular No. 202/2014/TT-BTC (Circular 2002), which enhance the comparability and transparency of corporate financial statements and bring the two systems closer. In particular, Circular 200 provided guidelines on accounting policies for both local and foreign enterprises in Vietnam for the financial year beginning 1 January 2015. It applies to the selection of a foreign currency for accounting purposes, accounting principles for turnover from sale of goods and services, and other areas. It replaces the current Vietnam accounting system regulated by Circular No. 244/2009/TT-BTC dated 31 December 2009 and Decision No. 15/2006/QD-BTC dated 20 March 2006.

Products

The sixth ‘P’ – product – may be seen as the object of regulation or an outcome that it delivers to its stakeholders including the financial statements. However, in this article, we consider accounting standards, accounting systems and other corporate regulations as products. Circulars and notifications issued by the government may also be described as a communication product that delivers compliance requirements to the companies and other reporting entities. The hierarchy of Vietnamese accounting regulation is described in Figure 1 and it highlights how Accounting Regulators and Corporation Law in Vietnam regulate the process of accounting regulation in Vietnam. Once a regulatory decision is made, it is communicated to various interested parties through circulars and reporting entities are expected to comply with such notified accounting regulation. Accounting standards need to be incorporated into the accounting systems as having the force of company law for entities preparing financial reports. This process of developing and communicating the accounting regulatory framework may be described as a final product of the chronological occurrence of various influences, national and international, as discussed by Carnegie and Napier (2002).

Vietnamese accounting regulatory framework.

A key product in the Vietnamese economy during the last phase (1986−2016) was the accelerated privatisation progress which transformed the ownership of key businesses from 100 per cent SOEs to privatised enterprises with more limited government ownership. For example, in 2015, Vietnam offered a 3.47 per cent stake of Airports Corporation of Vietnam to the public, of which 80 per cent was purchased by foreign investors (Petty and Nguyen, 2015). A shift from state to private ownership consistently leads to a more efficient use of capital and labour, and enhances the performance of the reformed SOEs in terms of profitability (Tran et al., 2015). As the SOEs are privatised, their financial and management practices are placed under increasingly greater scrutiny, which raises a demand for improved corporate governance and enhanced disclosures and reporting practices. The efforts made by the Vietnam government to attract foreign investors to invest in their country show little success as the average foreign ownerships of Vietnamese publicly listed firms are still comparatively low with an average of 14.36 per cent (Vu et al., 2011).

Profession

Despite French rule over a half century (1887−1954), the accounting profession in Vietnam was not originated by the French. The French accountancy profession did not have a tradition of becoming involved in developing the accounting profession in colonial countries, in contrast to the British accountancy bodies (Yapa, 2006). During the war time (1955−1975) and the early independence period (1975−1985), foreign and private sectors’ involvement was limited in comparison to the dominance of SOEs; thus, there was no incentive to establish accounting profession during this time. The seventh P, profession, occurred in the last phase (1986−2016). The beginning of accounting profession in Vietnam started with the forming of the SOE Chief Accountant Club. Although this club is a form of social networking club with no influence at all on the accounting regulatory progress, the establishment of this club signalled the demand of forming ‘proper’ occupational group or groups for Vietnamese accountants.

Two national professional bodies specialised in accounting and auditing were founded in late 1990s and early 2000s. In particular, the VAA and VACPA were founded in 1994 and 2005, respectively. Besides these national professional bodies, there are also international professional bodies, in particular the ACCA from 1996, the CPA Australia from 2006 and other (less active) organisations such as the Institute of Chartered Accountants in England and Wales, and the Institute of Chartered Accountants in Australia. The international professional organisations have contributed in providing high-quality training for technical personnel of accounting firms, foreign investment enterprises, financial institutions, banks, universities and government authorities in finance and accounting fields. In 2016, there were over 10,000 members of national accountancy professional bodies and over 2,000 members of international accountancy professional bodies in Vietnam, working in 108 registered accounting firms across Vietnam. This is evident of the existence of normative isomorphism resulting from both national and international accounting professional bodies in Vietnam.

The results indicate that the Vietnam Government adopted IFRS due to mimetic isomorphism as they are willing to participate in the global harmonisation project to achieve legitimacy. Mimetic isomorphism is evident when developing counties participate in internationalisation projects to align their rules and regulations with developed countries and the Vietnamese government’s decision to adopt IFRS is seen to be such a move. Nguyen and Tran (2012) also supported a case of mimetic isomorphism in Vietnam by citing the increasing number of investors and other similar reasons that prompted the government of Vietnam to endorse IFRS.

Concluding remarks

The article examined the historical development of Vietnam’s accounting practices and accounting standards in its transition towards a market-based economy. Vietnam was chosen as a case study not only because it is an emerging and transitional nature but also because of its lack of systematic inquiry into the historical development of accounting. To contribute to this literature, we employed a theoretical framework that combines the 7Ps (periods, places, people, practices, propagation, products and profession) model proposed by Carnegie and Napier (2002), and institutional theory developed by DiMaggio and Powell (1983). This framework was utilised to address three related research objectives: (1) the various distinctive stages in the evolution of accounting practices in Vietnam, (2) the institutional pressures that have shaped the evolution of accounting standards in Vietnam and (3) the implications of these historical developments on changes in Vietnam’s accounting standards.

The period under study is from 1856 to 2016, and was divided into four phases: 1856−1944 (colonialist economy), 1945−1974 (war economy), 1975−1985 (socialist economy) and 1986−2016 (transition economy). Within Vietnam, the locational factor identified North, Central and South Vietnam for the colonialist phase; North and South Vietnam for the war phase; and Vietnam for the last two phases. Similarly, the stakeholder factor recognises the French accountants and their Vietnamese assistants during the colonialist phase, the socialist and capitalists during the war phase, domestic agencies in the socialist phase, and the accountants, domestic agencies, and international businesses and institutions in the transition phase.

The accounting practices in the first three phases were influenced by the rules and regulations of the ruling countries (France in Phase 1; China, the United States and, to a lesser extent, the Soviet Union in Phase 2; and the Soviet Union in Phase 3), whereas the practices in Phase 4 have been influenced by international funding institutions (WB, IMF and ADB) and, to a lesser extent, foreign investors. In terms of propagation, accounting was mainly utilised as a tool for central planning and budgeting in the first three phases, and only properly used as a reporting means in the transition phase. In terms of key products, it is conceivable to mention accounting standards such as VAS and VASB, and accounting regulation such as the Vietnamese Accounting Regulatory Framework. Finally, the accounting profession in Vietnam can be said to emerge in the last phase with the establishment of the domestic professional organisations (Chief Accountant Club, VAA and VACPA) together with the presence of international professional bodies (ACCA and CPA Australia). We argue that development of the accounting profession during the last phase has been a driving factor for the development of accounting standards in Vietnam. This may be due to change in the Vietnamese economy from a centrally planned economy to a market-oriented economy leading to the emergence of international trade, and thus participation of the Vietnamese accounting bodies in the IFRS convergence move.

Our analysis has confirmed the relevance of the institutional approach in interpreting the history of accounting practices and standards in Vietnam. More specifically, the evolution of accounting in Vietnam was powerfully influenced by external political forces. The first three phases of Vietnam’s accounting history illustrated coercive isomorphism from France, China and the Soviet Union, respectively, whereas mimetic and normative isomorphism only become visible in the fourth phase. As an emerging economy, it is helpful to note that while accounting standards and regulations were tightly controlled by the Vietnamese government, particularly the MoF, there was also increasing demand, especially by the foreign invested sector, for using the best international accounting practices available. Thus, not surprisingly, the current accounting development in Vietnam is strongly influenced by the global move towards a single set of accounting standards.

In recent years, Vietnam has made efforts to strengthen capital market supervision and enforcement of accounting standards. During the time of the preparation of this article, the Vietnamese standards setters considered adopting IFRS (at least for public interest business entities) by 2025; however, the official roadmap is not yet announced. A worthwhile area of research would be to consider the implications of IFRS adoption upon the different stakeholders in a transition economy where the governance structures and source of finance is different to market-oriented countries. For example, disclosure under IFRS in annual reports and financial statements of companies in a transition economy may not be perceived in the same way as in the market of well-developed countries. Finally, the usefulness of IFRS in the context of transition economy could be investigated by regressing market data against financial ratios. In addition, comparative studies of firms in different countries or regions would provide a useful insight into the different institutional arrangements of each country and could be used to explain the differences in accounting practices between different countries.

Footnotes

Appendices

List of key accounting regulations in Vietnam.

| Accounting regulations during 1945–1961 | ||

| 29/05/1946 | Law No.75 | The organisation of Ministry of Finance by the President of Democratic Republic of Vietnam |

| 25/09/1948 | Decree 1535 VP/TDQ | First accounting regulation (budget accounting) |

| Accounting regulations during 1961–1965 | ||

| 28/10/1961 | Decree 175/CP | Promulgating the Charter for Organisation of State Accounting |

| 29/11/1961 | Decision 776 TC/CDKT | Promulgating accounting regulation for industrial sector |

| 6/12/1961 | Decision 273 TC/CDKT | Promulgating accounting regulation for capital construction |

| 23/08/1962 | Decision 259 TC/CDKT | Promulgating accounting regulation for goods warehouse |

| 22/11/1962 | Decision 714 TC/CDKT | Promulgating temporary regulations on accounting inspection |

| 29/11/1962 | Decision 730 TC/CDKT | Promulgating accounting regulation on fixed assets |

| 1/12/1962 | Decision 732 TC/CDKT | Promulgating regulations on physical assets inventory |

| 21/02/1964 | Decision 07 TC/CDKT | Promulgating regulations on accounting vouchers and books |

| Accounting regulations during 1966–1970 | ||

| 10/09/1970 | Decree 176/CP | Promulgating the new Regulations for Chief Accountants (replaced Chapter II of Decree 175/CP regarding the Charter for Organisation of State Accounting) |

| 14/12/1970 | Decision 425 TC/CDKT | Promulgating the unified chart of accounts applicable to all sectors including industry of the economy |

| 14/12/1970 | Decision 426 TC/CDKT | Promulgating the accounting books followed the journal voucher system applicable to all state-owned industrial enterprises |

| 1/12/1970 | Decision 233/CP | Promulgating the regulation on accounting and statistical reports of industrial enterprises |

| 1/12/1970 | Decision 583/LB/TC-TK | Promulgating the initial recording system |

| Accounting regulations during 1971–1975 | ||

| 10/09/1970 | Decree 176/CP | Promulgating the new Regulations for Chief Accountants (replaced Chapter II of Decree 175/CP regarding the Charter for Organisation of State Accounting) |

| 14/12/1970 | Decision 425 TC/CDKT | Promulgating the unified chart of accounts applicable to all sectors including industry of the national economy |

| 17/07/1971 | Circular 231 TC/CDKT | Providing guidelines on the implementation of the Decision 425 |

| 28/07/1972 | Circular 11 TC/CDKT | Providing the regulations on the application of journal voucher accounting system in the national economic sectors |

| 28/10/1975 | Circular 34 TC/CDKT | Providing amendments to the unified chart of accounts issued in the Decision 425 |

| Accounting regulations during 1975–1985 | ||

| 28/10/1975 | Circular 34 TC/CDKT | Providing amendments to the unified chart of accounts and detailed regulations on the contents and application of the unified chart of accounts in the national economic sectors |

| 18/01/1980 | Circular 03-TC/CDKT | Promulgating accounting regulations for enterprises alliances |

| 11/10/1980 | Decision 222 QD/CDKT | Promulgating accounting policies for fixed assets of SOEs |

| 23/10/1980 | Circular 11-TC/CDKT | Promulgating accounting for tools and equipment |

| 21/01/1981 | Decision 25-CP | Regarding policies and measures to promote the autonomy in production and financial activities of SOEs |

| 10/03/1981 | Decision 278 TC/CDKT | Promulgating accounting for private industrial and trading businesses |

| 10/03/1982 | Circular 06-TC/CDKT | Promulgating accounting for borrowings, cash deposit at bank in foreign currency |

| 18/05/1982 | Decision 217 TC/CDKT | Promulgating accounting for labour and salaries |

| 14/01/1984 | Decision 33 TC/CDKT | Promulgating policy on accounting inspection |

| 16/05/1985 | Circular 24-TC/CDKT | Providing amendment to accounting work |

| 1/07/1986 | Decision 189 TC/CDKT | Providing guidelines on accounting for agricultural cooperatives |

| Accounting regulations during 1986–2013 | ||

| 7/02/1987 | Circular 10 TC/CDKT | Promulgating amendments to accounting regulations for economic units |

| 1/04/1987 | Circular 26 TC/CDKT | Providing amendments on certain matters of the unified chart of accounts |

| 10/05/1988 | Ordinance 1988 | Ordinance on Accounting and Statistics |

| 18/03/1989 | Decree 25-HDBT | Promulgating the Charter on Organisation of State Accounting (replaced Decrees 175-CP and 176-CP in 1961 and 1970 respectively) |

| 18/03/1989 | Decree 26/HDBT | Promulgating the Charter on Chief Accountant of state-owned enterprises (SOEs) (replaced Decrees 175-CP and 176-CP in 1961 and 1970 respectively) |

| 15/02/1989 | Decision 212 TC/CDKT | Promulgating unified chart of accounts applicable to every sector and industry |

| 24/04/1989 | Circular 475 TC/CDKT | Detailed guidelines on implementation of the Ordinance on Accounting and Statistics, the Charter on Organisation of State Accounting, and the Charter on Chief Accountant of SOEs |

| 15/12/1989 | Decision 212-TC/CDKT | Unified Chart of Accounting applicable to every sector and industry in Vietnam |

| 18/04/1990 | Decision 224 QD/CDKT | Periodical accounting reports applicable to SOEs |

| 19/05/1990 | Decision 90 QD/CDKT | The initial record system |

| 1/06/1990 | Decision 257 QD/CDKT | Accounting regulation for administrative and non-productive units |

| 20/11/1990 | Directive 408-CT | Continued reorganising of finance and accounting and economic accounting in SOEs |

| 8/12/1990 | Decision 598 QD/CDKT | Accounting regulation on business activities of non-state sector |

| 20/11/1991 | Decree 388-HDBT | Establishment and closing down of SOEs |

| 14/12/1994 | Circular 113-TC/CDKT | Guidance on application of new chart of accounts for business enterprises |

| 14/12/1994 | Decision 1205-TC/CDKT | Promulgating a new Chart of Account for Enterprises |

| 20/06/1995 | Decision 361-TTG | Establishing of the Committee for the preparation of establishing a securities market in Vietnam |

| 1/11/1995 | Decision 1141-TC/QD/CDKT | Accounting regulation for business enterprises |

| 28/11/1996 | Decree 75/CP | Establishment of the State Securities Committee |

| 20/03/1997 | Circular 10-TC/CDKT | Amendment to accounting regulation for business enterprises issued in Decision 1141 |

| 28/01/1997 | Decision 832 TC/QD/CDKT | Issuing the Statute on Internal Auditing |

| 1/09/1997 | Circular 60 TC/CDKT | Providing guidelines for implementation of accounting and auditing in FIEs and foreign organisations in Vietnam |

| 23/10/1997 | Decision 769/TC/QD/TCCB | Providing the Regulations on training of chief accountants of SOEs |

| 16/08/1999 | Decision 92/1999/QD-BTC | Regarding the establishment of the National Council for Accountancy |

| 27/09/1999 | Decision 120/1999/QD-BTC | Regarding the issuance and announcement of four Vietnamese Standards of Auditing (1st batch) |

| 7/10/1999 | Circular 120/1999/TTBTC | Amendment to accounting regulation for business enterprises issued in Decision 1141 |

| 14/03/2000 | Decision 38/2000/QD-BTC | Issuance and announcement the application of Vietnamese Accounting Standards and Vietnamese Standards of Auditing |

| 28/03/2000 | Decision 276/QD-BTC | Regulations on organising and working of the National Council for Accountancy |

| 29/12/2000 | Decision 219/2000/QD-BTC | Issuance and announcement of six Vietnamese Standards of Auditing (2nd batch) |

| 21/12/2001 | Decision 143/2001/QD-BTC | Issuance and announcement of six Vietnamese Standards of Auditing (3rd batch) |

| 31/12/2001 | Decision 149/2001/QD-BTC | Issuance and announcement of four Vietnamese Accounting Standards (1st batch) |

| 31/12/2002 | Decision 165/2002/QD-BTC | Issuance and announcement of six Vietnamese Accounting Standards (2nd batch) |

| 17/06/2003 | Law 03/2003/QH11 | Accounting Law |

| 14/03/2003 | Decision 28/2003/QD-BTC | Issuance and announcement of five Vietnamese Standards of Auditing (4th batch) |

| 28/11/2003 | Decision 195/2003/QD-BTC | Issuance and announcement of six Vietnamese Standards of Auditing (5th batch) |

| 30/12/2003 | Decision 234/2003/QD-BTC | Issuance and announcement of six Vietnamese Accounting Standards (3rd batch) |

| 9/07/2004 | Decision 59/2004/QD-BTC | Regulations on examinations and issuance of the independent auditor certificate and the accounting practitioner certificate |

| 26/04/2004 | Decision 43/2004/QD-BTC | Regulations on training and issuance of chief accountant certificate |

| 18/01/2005 | Decision 03/2005/QD-BTC | Issuance and announcement of six Vietnamese Standards of Auditing (6th batch) |

| 15/02/2005 | Decision 12/2005/QD-BTC | Issuance and announcement of six Vietnamese Accounting Standards (4th batch) |

| 14/07/2005 | Decision 47/2005/QD-BTC | Transfer of some of state management duties on managing the practicing activities to accounting associations |

| 1/12/2005 | Decision 87/2005/QD-BTC | Announcement and issuance of professional code of ethics of the accounting and auditing profession in Vietnam |

| 28/12/2005 | Decision 100/2005/QD-BTC | Issuance and announcement of four Vietnamese Accounting Standards (5th batch) |

| 29/12/2005 | Decision 101/2005/QD-BTC | Issuance and announcement of four Vietnamese Standards of Auditing (7th batch) |

| 20/03/2006 | Decision 15/2006/QD-BTC | Issuing the Corporate Accounting Regulations |

| Decision 48/2006/QD-BTC | Vietnamese Accounting System for Small and Medium Enterprises (SMEs) | |

| 15/05/2007 | Decision 32/2007/QD-BTC | Regulations on quality control of accounting and auditing services |

| 16/11/2007 | Decision 94/2007/QD-BTC | Regulations on examinations and issuance of the independent auditor certificate and the accounting practitioner certificate |

| 24/08/2009 | Circular 171/2009/TT-BTC | Amendments and supplements of certain Articles in the Regulations on examinations and issuance of the independent auditor certificate and the accounting practitioner certificate issued in the Decision No. 94/2007/QD-BTC dated 16 November 2007 by Minister of Finance |

| Accounting regulations from 2014 to date | ||

| 22/12/2014 | Circular 200/2014/TT-BTC | Vietnamese Accounting System for Enterprises |

| 20/11/2015 | Law 88/2015/QH13 | Accounting Law |

| 21/03/2016 | Circular 53/2016/TT-BTC | Providing Amendments and supplements to certain articles in Circular No. 200/2014/TT-BTC (‘Circular 200’) on the Vietnamese Accounting System for Enterprises. |