Abstract

As organizations compete in an increasingly global and challenging environment, “working” often requires working harder for fewer rewards. In this article, we introduce the concept of “organization-wide hardship,” which refers to workforce-shared hardship that results from an organization’s pursuit of a strategy associated with its industry-positioning goals. We propose a model for predicting and explaining employees’ reactions to organization-wide hardship. Our analysis and model make several contributions to the justice literature. First, we highlight the importance of organization-wide hardship (associated with pay freezes or pay cuts, increased working hours, or reduced work–family balance) as a potential contributor to the experience of low fairness for all employees in the organization. Second, we argue that research on the effects of management accounts (explanations) for their decisions should be extended by considering the effects of accounts from nonmanagement sources. Third, we highlight the potentially paradoxical effects of providing external (rather than internal) accounts to employees as these likely heighten the hardship’s perceived fairness yet also heighten employees’ concern for their organization’s future and hence their intended or actual turnover. Fourth, our article’s theorizing adds a temporal (future-oriented) perspective to the largely past-oriented perspective of organizational justice–related theorizing and research. We discuss the implications of our model for organizations and leaders and scholars who aim to study employees’ reactions to organization-wide hardship.

Numerous studies have found that employees who perceive more (rather than less) fairness in their workplace generally express attitudes and behaviors that are “more favorable to their employer” (cf. Diehl, Richter, & Sarnecki, 2018, p. 2376). Among these more favorable work attitudes is employees’ commitment to their organization, or “affective commitment” (Brockner & Higgins, 2001), which is associated with low employee turnover (Chen, Choi, & Chi, 2002; Dittrich & Carrell, 1979; Van Yperen, Hagedoorn, & Geurts, 1996). This is why organizational justice scholars have long noted that understanding antecedents to employees’ perception of workplace fairness has practical and theoretical importance.

To date, theorizing and research regarding organizational justice has focused on various facets of justice. These facets refer to the extent to which fairness perceptions regard distributive qualities such as the allocation of valued resources (cf. Adams, 1965; Walster, Walster, & Berscheid, 1978; cf. Chen et al., 2002; Janssen, Lam, & Huang, 2010); procedural qualities such as the criteria used to determine reward allocations (cf. Leventhal, 1980; cf. Folger & Greenberg, 1985); informational qualities such as the type of explanations, or accounts, accompanying allocation decisions (cf. Bies & Moag, 1986; Greenberg, 1993); and interpersonal or interactional qualities such as the extent of interpersonal dignity shown in interactions with outcome-allocators or decision-makers, typically organizational authorities (cf. Bies & Shapiro, 1987, 1988; Greenberg, 1990a).

Although each facet of justice has been shown to be independently important for predicting and explaining individuals’ responses, more recent theorizing has proposed a more holistic approach to perceptions of justice. In particular, Ambrose and Schminke (2009) and Colquitt and Rodell (2015) have suggested the value of a general construct, overall fairness, that is theoretically “downstream” from particular facets of justice. Overall fairness is a holistic perception by individuals that their organization is treating them appropriately and fairly. Similarly, Ambrose, Wo, and Griffith (2015) proposed the construct of overall justice, suggesting that it encompasses the distinct facets of justice but is also influenced by other variables such as trust and positive affect. Ambrose et al. (2015) suggested that the construct of overall justice (or overall fairness) has the potential for providing a mechanism for integrating justice into the broader organizational literature, and especially for examining when justice is influential versus when it is not.

In this article, we focus on cases in which organizations impose sacrifices on all their employees. Such cases typically elicit strong reactions from those affected and make the issue of overall organizational fairness especially salient. Our major purpose here is to examine the effects of such imposed sacrifice on turnover intention and voluntary turnover, through the mechanism of perceived overall fairness. Our second purpose is to examine important boundary conditions for the effects of perceived overall fairness. These boundary conditions pertain to the perceived necessity of the imposed hardship, the informational sources of hardship-necessity perceptions (that include, but are not limited to, management), and the organization-wide hardship’s expected duration. In sum, we propose that perceived overall fairness will lead to adverse reactions under some but not all conditions, which we will explain on the basis of our model of employee reactions to organization-imposed hardship.

Organization-Wide Hardship: Its Contribution to the Literature on Organizational Fairness

We use the term “organization-wide hardship” to refer to a state of resource scarcity that results when organizations impose sacrifices on all their employees, creating the experience of loss for all employees of the organization. Resource scarcity–related losses that typically occur during times of organization-wide hardship can include pay freezes (Schaubroeck, May, & Brown, 1994), pay cuts (Greenberg, 1990a), mandatory furloughs (Halbesleben, Wheeler, & Paustian-Underdahl, 2013), or increases in required job output or performance that can impede work–family balance (Schawbel, 2016). In these situations, a reduction in resources occurs for all employees. Because no employees are exempted, the issue of overall organizational fairness is likely to become central (Fugate, Prussia, & Kinicki, 2012). In particular, it becomes likely that employees will perceive the organization’s overall fairness as lower after it has imposed sacrifices on them.

Our current analysis of reactions to organization-wide hardship in terms of overall fairness makes several contributions to the justice literature. First, we highlight the importance of organization-wide hardship (associated with pay freezes or pay cuts, increased working hours, or reduced work–family balance) as a potential contributor to the experience of low fairness for all employees in the organization. Such cases differ from those addressed by most organizational justice research that has examined how unfavorable decisions within an organization, such as rejections of resource requests (Bies & Shapiro, 1988), harsh performance appraisals (Folger & Greenberg, 1985), layoffs (Brockner, DeWitt, Grover, & Read, 1990), and a smoking ban (Greenberg, 1994), affect only a subset of organizational employees. We suggest that reactions to organization-wide unfairness may differ in important ways from reactions to intraorganizational unfairness.

Second, we add to the sparse yet growing literature suggesting the need for organizational justice scholars to consider variables outside, rather than just inside, the organization that influence employees’ perceptions of fairness in their organization (cf. Diehl et al., 2018). This includes the need to consider nonmanagement sources of information that employees use to assess their organization’s fairness. We propose that the effects of key variables investigated in prior organizational justice research are likely to be moderated by information that is now widely available (e.g., 24/7 news and Internet sources). In particular, we argue that research on informational justice, especially studies of the effects of management accounts (explanations) for their decisions, should be extended by considering the effects of accounts that come from nonmanagement sources.

Third, we emphasize the tradeoffs that managers face when they implement the widely accepted recommendations for enhancing informational justice. Such recommendations entail “transparency,” the need for managers to explain their decisions honestly and openly. This recommendation is especially important in cases where decisions result in negative outcomes for the recipients (e.g., Brockner et al., 1990; Brockner & Wiesenfeld, 1996). In such cases, recipients are more likely to accept management’s decisions if they view them as a response to external demands (hence unavoidable) rather than to management’s proactive, voluntary choice. Thus, when managers explain an unfavorable decision with an “external account” (i.e., an explanation invoking situational necessity) rather than an “internal account” (i.e., an explanation referring to proactive choice-based reasons), employees are likely to view the decision as more fair (Bies & Shapiro, 1987, 1988; Bies, Shapiro, & Cummings, 1988).

However, external accounts may have consequences that amount to, metaphorically speaking, a double-edged sword. Although external accounts typically enhance employees’ perceptions of the “evil’s” necessity, and hence its fairness, they may simultaneously signal the organization’s weakness or fragility, which in turn may increase employees’ intended or actual turnover. This is because an organization that needs to impose organization-wide hardship (as explained by an external account) will likely be seen as having a weaker industry-standing than does an organization that imposes this hardship without needing to do so (as explained by an internal account). By examining the industry-standing implications of managers’ external (vs. internal) accounts for imposing hardship, we provide a bridge between micro and macro variables that has been largely missing in theorizing and research on organizational justice dynamics (cf. Diehl et al., 2018). In highlighting this micro–macro bridge, we suggest that the long-presumed positive relationship between employees’ perception of fairness and their commitment to the organization may depend on their organization’s position in the market. As we will discuss, this has implications for the link between overall perceived fairness and turnover.

Fourth, our article’s theorizing adds a temporal (future-oriented) perspective to the largely past-oriented perspective of organizational justice–related theorizing and research (cf. Cosier & Dalton, 1983; Shapiro & Kirkman, 1999). Specifically, we posit that the effect of perceived overall fairness on turnover intentions and turnover will be affected by the expected duration of the organization-wide hardship. Although such temporal considerations have been relatively neglected until recently, it is clear that in dynamic organizational settings they can affect employees’ responses (e.g., Eldor et al., 2017; Fried, Grant, Levi, & Hadani Slowik, 2007; Fried & Slowik, 2004).

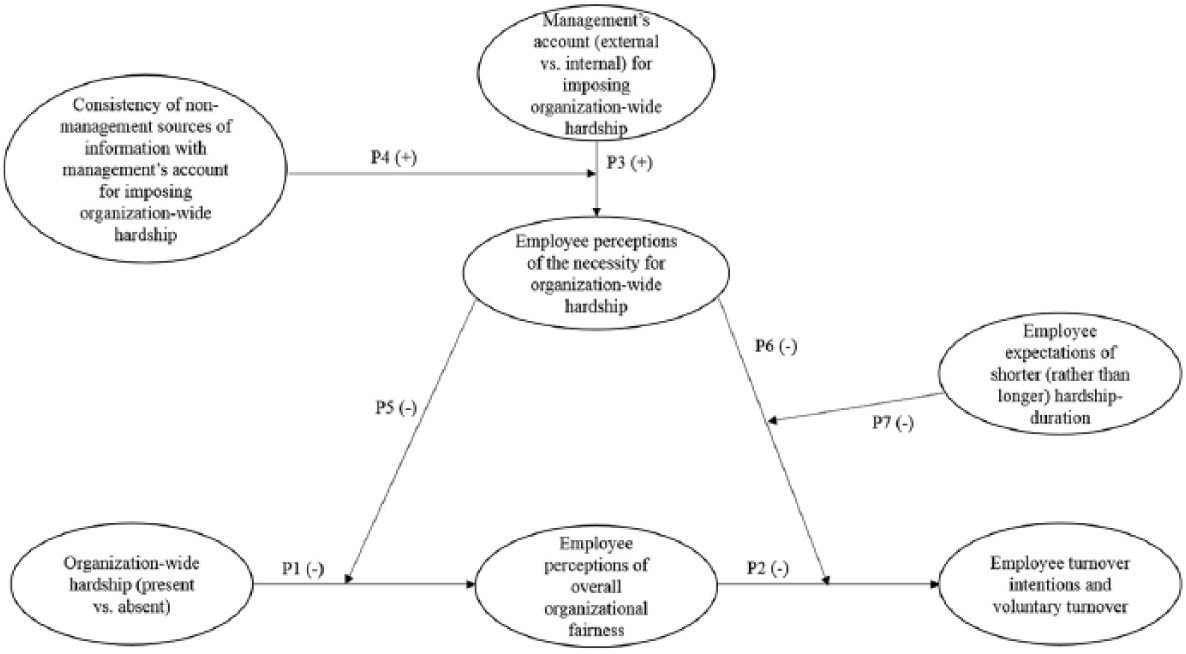

In the following sections, we develop several propositions for the linkages among organization-wide hardship, perceived overall fairness, and turnover intentions and turnover. Our rationale for these links draws on both prior research in the justice literature and our theorizing on boundary conditions for their direction and strength. Following this, we discuss the theoretical and practical implications of our propositions that we hope will inspire additional investigation of the links between the micro and macro levels of justice research. Our model is shown in Figure 1.

Model of organization-wide hardship.

Organization-Wide Hardship, Overall Fairness, and Turnover

When organization-wide hardship is imposed, employees are likely to experience feelings of loss and inequity as they experience a decrease in the outcomes they had been receiving relative to their inputs up to that point. Although the standard version of equity theory (Adams, 1965; Walster et al., 1978) focused on individuals’ comparisons between their own and others’ outcome/input ratios, it also accepted that individuals could compare their own ratios over time (Cosier & Dalton, 1983). Organization-wide hardship produces a situation in which all employees will perceive an unfavorable comparison between their earlier versus current ratios. This will lead to a widespread perception of inequity within the organization and, consequently, a general reduction in the perceived overall fairness of the organization.

A substantial literature indicates that employee perceptions of unfairness contribute to adverse psychological reactions (e.g., emotional exhaustion, threat appraisal) and are negatively related to positive psychological experiences (e.g., attachment, commitment, and organizational trust). And conversely, employee perceptions of organizational fairness are associated with positive psychological experiences, resulting in decreased withdrawal reactions (see, for example, Aryee, Budhawar, & Chen, 2002; Cole, Bernerth, Walter, & Holt, 2010; Fugate et al., 2012; Howard & Cordes, 2010; Olkkonen & Lipponen, 2006; Spreitzer & Mishra, 2002) that, in turn, tend to be associated with weaker turnover intentions (Chen et al., 2002; Hausknecht, Sturman, & Roberson, 2011; Iverson & Roy, 1994; Kim & Leung, 2007; Li & Cropanzano, 2009; Ronen, 1986; Schaubroeck et al., 1994; Shapiro & Kirkman, 1999) and turnover (Dittrich & Carrell, 1979; Telly, French, & Scott, 1971; Van Yperen et al., 1996; Wang, Zhao, & Thornhill, 2015), as well as other actions that can harm organizational functioning (see Rupp, Shapiro, Skarlicki, Folger, & Shao, 2017, for a review). Therefore, other things being equal, our first two propositions on which we subsequently build are the following:

Management Accounts for Organization-Wide Hardship

When implementing a policy that entails organization-wide hardship, management typically provides an “account,” or explanation, for doing so. Indeed, given the increasingly widespread understanding of the need for “fair process” (e.g., Brockner et al., 1990; Brockner & Wiesenfeld, 1996), executives typically take great pains to explain the necessity of the organization’s strategy and why employees need to accept some of the burden required to make the strategy succeed. Drawing on attribution theory (Harvey, Madison, Martinko, Crook, & Crook, 2014; Kelley, 1967; Kelley & Michela, 1980), these accounts can be characterized along an internal–external dimension. An internal account explains the policy as being adopted voluntarily by the actor (i.e., the organization) on the basis of its own goals and preferences. For example, an internal account for a policy that imposes high demands on all employees might revolve around the organization’s attempt to become the leader in its industry. In contrast, an external account explains the policy as being necessitated by the actions of external conditions such as competitors or governmental agencies. For example, an external account for an across-the-board pay cut might be that the organization is under threat of bankruptcy and thus cannot survive unless all employees make financial sacrifices.

In general, internal accounts are used when the organization’s standing in its industry or market is good, and external accounts are used when the organization’s standing in its industry or market is poor. In the latter case, the account will typically justify organization-wide hardship as necessitated by a desire to make the organization competitive again in its market or, in severe cases, to ensure the organization’s survival. For these reasons, internal versus external accounts for organization-wide hardship decisions are likely to be provided by leaders in organizations that are market leaders versus market laggards, respectively. These two account-giving strategies by management dominate the organizational justice literature, which assumes that the attributions employees make for strategic actions are strongly influenced by the account-givers (for an elaboration of this point, see Rupp et al., 2017). Thus, other things being equal,

Our theorizing to this point, and the empirical findings supportive of it, suggests that managers can influence employees’ perception of the necessity of the organization-wide hardship (and consequently also its fairness, as we will subsequently propose) by providing external rather than internal accounts for the policy. External accounts state or strongly imply that the hardship is a “necessary evil” to address adverse external conditions—and, thus, a defensive reaction rather than a proactive choice. The tendency for people to perceive “evils” (e.g., unfavorable management decisions) as fairer when they are attributed to external rather than internal factors (Bies et al., 1988) raises the possibility that managers may give external rather than internal accounts to appear more fair (e.g., Greenberg, 1990b) or, more broadly, to generate more positive impressions by their employees (Bies, 1987). Such an instrumental use of accounts is likely to succeed to the extent that managers control the information employees have about their organization.

However, although the accounts provided by management are important influences on employees’ attributions and their perceived necessity for the organization-wide hardship, they are not the only ones. Organizational justice scholars have recently noted the influence of the Internet and the numerous communication channels it has opened. Such channels provide independent (nonmanagement-provided) information and perspectives about organizations, their standing in their market, and their financial prospects and explanations for the policies they have adopted. Social media sites, including Facebook, LinkedIn, and Glassdoor, provide readily available information and opinions that can influence employees’ perceptions of their own organization, its leadership, and its decisions (cf. Conlon & Ross, 2012; Kulik, Pepper, Shapiro, & Cregan, 2012). In addition, technological advances have led to dramatic increases in people’s use of their mobile phones as cameras, as recording devices, and for distributing email, tweets, and videos. Thus, people’s access to news is exponentially greater than it was in the decades when the earliest theorizing and studies of organizations took place. Consequently, leaders have far less control over the “narrative” they want people to believe than they did in the past (cf. Rupp et al., 2017).

Alternative nonmanagement-provided challenges to organizational leaders’ or managers’ preferred accounts, justifications, or images have become widespread and often occur in cases involving potential threats to the organization’s reputation. One example of this is the attempt by Elon Musk, CEO of Tesla, to portray himself as an authentic and compassionate leader who was concerned with employees who had suffered injuries due to unsafe working conditions in the firm’s manufacturing plants. In May 2017, in response to news reports of these injuries, Musk emailed his entire staff that “No words can express how much I care about your safety and wellbeing” and that he would “meet with the safety team every week and with every injured person as soon as they are well” to improve conditions and prevent further injuries. However, shortly thereafter, several injured employees told reporters and stated on social media sites that Musk never did meet with them and that they did not believe he intended to do so (Wong, 2018). Musk’s attempts to restrict employees from disclosing information about the company to those outside the company did not prevent employees from doing so in social media and in reports to external news outlets. As a result, many have come to view Musk as a leader whose concern for his company’s image and reputation leads him to overpromise and make exaggerated claims about his business (Hansen, 2017).

Another example of the influence of nonmanagement-provided sources of information pertains to Amazon, Inc.’s CEO Jeff Bezos’s attempt to portray Amazon as having a culture that supports creative, driven, and achievement-oriented employees. Bezos’s narrative has been contradicted by news reports and employees’ social media complaints of the company’s harsh working conditions. These now widely known complaints revolve around both the higher-level knowledge-based and the operative-level warehouse jobs (Kantor & Streitfeld, 2015; Picchi, 2018).

One final example of the power of media generally, and social media in particular, is the inability of U.S. government leaders, such as Department of Homeland Security Secretary Kirstjen Nielsen, to maintain a preferred narrative about governmental actions occurring at the U.S.–Mexico border. Nielsen’s narrative is discrepant with the narrative provided by audio and video recordings taken by people outside of the U.S. government. A CNN (2018) report described the narrative challenge as follows: [U.S. President] Trump was supportive of having Nielsen appear at the White House podium, people familiar with the matter said, believing she could offer a consistent message on the administration’s practice. He has grown frustrated in recent days at the images of separated children playing out on television and the subsequent blame he’s received . . .

In sum, our key point here is that organizational accounts of events or decisions, even if provided by top management, are increasingly coming under challenge from nonmanagement-provided media sources. If information from such sources is inconsistent with management’s account, employees may doubt this account and in turn become cynical about the trustworthiness of top management. Such cynicism can have severe legal, financial, and reputational consequences, as has occurred in cases of police departments’ explanations for traffic stops resulting in injury or death of suspects (e.g., Drash, 2015; “Guelph Policy,” 2015; Stern, 2010), a university’s public relations efforts in addressing sexual abuse on campus (Kirby, 2018; Levenson, 2018), and a case involving an employee’s criticism of a high-tech organization’s policies and philosophy on diversity (e.g., Damore, 2017). Thus, the wide availability of alternative nonmanagement-provided sources of information and perspectives on organizational decisions and policies decreases the likelihood that employees will accept management accounts unquestioningly.

With respect to organization-wide hardship, the accounts provided by nonmanagement sources may be either consistent or inconsistent with managers’ accounts for the policy. Consistency refers to whether the nonmanagement explanations for why the policy was adopted agree with those offered by management, especially with respect to whether the policy was internally driven (i.e., was adopted proactively to improve the organization’s competitiveness) or externally driven (i.e., was adopted out of necessity to help the organization survive). We propose that employee acceptance of management accounts for organization-wide hardship is likely to be strengthened or weakened depending on the consistency of nonmanagement-provided sources of information with these accounts. Thus, we propose the following:

Why would management want employees to perceive that organization-wide hardship is necessary? The answer returns us to the two foundational relationships with which we began: employees tend to perceive more unfairness when their organization is experiencing organization-wide hardship (Proposition 1), and more perceived unfairness tends, in turn, to be associated with higher levels of turnover intention or actual turnover (Proposition 2). Therefore, the latter chain of events can be destructive to organizations. For reasons we explain next, we posit that the tendency for less fairness to be perceived by employees undergoing organization-wide hardship can be weakened when employees perceive the organization-wide hardship to be a “necessary evil” rather than a free choice; yet, on the contrary, we also posit that when organization-wide hardship is perceived as necessary, this may also weaken the tendency for employees who perceive more fairness during times of organization-wide hardship to be less likely to quit or to think about quitting. Next, we turn to both of these possibilities, thereby exposing the potential for organization-wide hardship’s perceived necessity to be a double-edged sword.

Organization-Wide Hardship’s Perceived Necessity as a Double-Edged Sword and the Mitigating Effect of Expected Duration of Hardship

Our theorizing to this point suggests that when management provides an external rather than internal account for organization-wide hardship, employees are more likely to perceive this hardship as necessary and unavoidable, and this tendency is stronger when management’s external account is consistent (rather than inconsistent) with news seen and heard by employees from nonmanagement sources outside their organization. Next, we consider how employees’ perceptions of organization-wide hardship as necessary rather than avoidable may weaken the two foundational premises with which we began.

Why the Perceived Necessity of Organization-Wide Hardship Likely Weakens the Tendency for Hard Times to be Associated With Greater Perceived Unfairness

Employees’ perception of their organization-wide hardship as necessary (rather than freely chosen) ought to weaken the tendency for employees who are experiencing this hardship to perceive unfairness. This is because employees who attribute unfavorable organizational events, such as management’s imposition of harsh policies, to external pressures are less likely to perceive the organization as deserving of blame, and thus also less unfair (Bies et al., 1988). This blame-mitigating effect of external accounts is consistent with Referent Cognitions Theory (Folger, 1986) and Fairness Theory (Folger & Cropanzano, 2001) and has been supported in numerous studies of individuals’ reactions to policies or decisions that resulted in unfavorable outcomes. For example, external accounts have reduced perceived unfairness among rejected job applicants (e.g., Gilliland, 1993; Truxillo, Steiner, & Gilliland, 2004), employees whose requests for resources were rejected (Bies & Shapiro, 1988), employees facing layoffs (e.g., Brockner & Wiesenfeld, 1996), and employees whose pay was cut (Greenberg, 1990a; Schaubroeck et al., 1994). In short, to the extent that a decision or policy is seen as a “necessary evil,” it will be seen as more fair. Logically, it follows from this that the tendency for organization-wide hardship to lower employees’ perceptions of overall fairness in the organization (proposed by Proposition 1) ought to weaken when the hardship is perceived to be necessary rather than unnecessary.

Southwest Airlines provides an example of employees responding more positively to organization-wide hardship when this is perceived as necessary rather than unnecessary—that is, when employees perceive organization-wide hardship to be imposed when an organization is under duress rather than in an already strong competitive position (O’Reilly & Pfeffer, 2000; Trottman, 2003). In its earlier years, when Southwest was considered an underdog in the industry in terms of size and number of routes (i.e., in an unfavorable competitive position), employees agreed to work for lower compensation relative to employees in similar positions in competitor airlines to help Southwest compete and grow. For example, in 1994, pilots agreed to a 5-year wage freeze that helped the company save on costs in exchange for a stock-option award in their contract. Given that airline stocks during that period had not been performing well, this meant that the pilots were willing to sacrifice their pay without knowing how soon, or whether, the sacrifice would pay off (O’Reilly & Pfeffer, 2000).

Later on, however, when Southwest had grown to become the fourth largest airline in the U.S. domestic arena, employees were less willing to sacrifice for the company. The company continued to ask employees to sacrifice despite its rapid growth and high profits: Southwest specifically challenged employees to work harder to save an additional 5% a day (Trottman, 2003) so that the company could maintain its competitiveness and continue its growth. However, this led employees to complain that Southwest was profitable, while their income had not increased to be comparable to that of employees at other airlines (Trottman, 2003). In 2002, for example, Southwest’s unit labor costs were 22% less than Continental’s, while the average salaries in the two companies were about the same (around US$60,000). Moreover, Southwest’s costs were significantly below those of American Airlines (41% lower), while American’s average salary was nearly $80,000 (Trottman, 2003). In the summer of 2001, Southwest’s ramp workers demonstrated their sense of grievance by picketing near company headquarters, carrying signs that read, “Record profits empty pockets” (Trottman, 2003). Thus, employees at Southwest clearly perceived the pay reductions (organization-wide hardship) as more justified and fair when the company had a lower standing and was under competitive threat in its industry than when it had a strong standing in its industry. This is why we propose that the perceived necessity of organization-wide hardship moderates the tendency for this hardship to lower employees’ perceived fairness. Thus,

Why the Perceived Necessity of Organization-Wide Hardship Likely Weakens the Tendency for Employees’ Perceived Fairness to be Associated With Less Turnover

Employees’ perception of their organization-wide hardship as necessary (rather than freely chosen) ought to weaken the tendency for employees who perceive overall organizational fairness to be less likely to consider leaving the organization or actually doing so. Thus, the perceived necessity of hardship will moderate the link between perceived overall fairness and turnover intentions and turnover. This is because employees who perceive organization-wide hardship to be necessitated by the organization’s status as a market laggard will likely infer that their organization is financially vulnerable, has a poor reputation, and will be unlikely to attain financial stability and success in the future. In contrast, when employees perceive the organization-wide hardship to be adopted for proactive and internally driven reasons (e.g., by the goal of improving the organization’s competitive position from an already favorable market position), they will likely infer that the organization is likely to attain its strategic goals. Under these more optimistic circumstances, employees are more likely to perceive that leaving their organization will require them to forgo valuable benefits that they would obtain by staying—a calculation that typically enhances the extent to which employees are “job-embedded” (Mitchell, Holtom, Lee, Sablynski, & Erez, 2001)—that is, likely to stay.

Given that turnover intentions and voluntary turnover are strongly driven by instrumental or utilitarian considerations (e.g., Holtom, Mitchell, Lee, & Eberly, 2008; Schoenfelder & Hantula, 2003; Shapiro, Hom, Shen, & Agarwal, 2016), employees who hold the pessimistic inferences about their organization that are associated with organization-wide hardship being necessary ought to be more likely to consider “jumping ship” or leaving their organization. Such pessimism may, therefore, also weaken the tendency for employees who perceive fairness to remain in the organization. For this reason, employees’ perception of organization-wide hardship as necessary is likely to be a double-edged sword: While it may help to ameliorate the tendency for employees to perceive unfairness during organization-wide hardship, it may weaken the tendency for employees who perceive fairness during hard times to stay committed to their organization. Stated conversely, employees who are optimistic about their organization’s future (which is more likely when employees perceive their organization as having a strong position in its market) are more likely to remain with their organization despite the hardship (cf. Cosier & Dalton, 1983).

Organizational examples that support our theorizing include employees’ commitment to relatively new market entrant Uber, despite their expressed dissatisfaction with demanding working conditions (Fairchild, 2017). Similarly, the willingness of employees to endure the harsh working conditions of Amazon illustrates how competitive success can mitigate the negative reactions that would typically occur in less successful organizations (Kantor & Streitfeld, 2015). Thus, we propose the following:

In summary, we have just proposed that employees’ perception of the necessity of hardship has dual moderating effects that work in opposition to each other. On one hand, we expect that when organization-wide hardship is perceived as necessary, this will weaken the tendency for organization-imposed hardship to decrease employees’ perception of overall fairness of the organization; yet, on the other hand, we expect that this hardship’s perceived necessity will probably increase employees’ pessimism in their organization’s future and thereby weaken the tendency for employees who perceive organizational justice to remain committed to their organization.

Is there a way to mitigate the double-edged sword quality of employees’ perceptions of organization-wide hardship as a necessity? For reasons we explain next, we posit that it is safer (more turnover-mitigating) to frame organization-wide hardship as necessary when this framing is accompanied by information regarding its expected (short rather than long) duration.

How the Expected Duration of Organization-Wide Hardship Likely Mitigates the Double-Edged Sword Quality of This Hardship’s Perceived Necessity

When organizations impose hardship, employees become motivated to estimate the expected duration of the hardship (Fried & Slowik, 2004; cf. Schaubroeck et al., 1994). This is because when a hardship’s duration is expected to be temporary, it is easier to tolerate and support. Anecdotally, this is why signs stating “Please pardon the temporary inconvenience for a permanent improvement” are often placed in organizations where construction activity is occurring. Extrapolating from this, we propose that the tendency for the negative association between employees’ perception of organizational fairness and employee turnover to be weakened by their perception of necessary (rather than a voluntarily chosen) organization-wide hardship (predicted by Proposition 6) is more likely to be observed when employees expect this hardship to last long and is less likely to be observed when employees expect this hardship to last only briefly. Expected duration of hardship, thus, may mitigate the potential for organization-wide hardship’s stated necessity to backfire—that is, to weaken the generally negative association between employees’ perception of organizational fairness and their intended or actual turnover. Our central idea here, consistent with the theorizing of Eldor et al. (2017), is that employees are likely to respond more positively to adverse circumstances when they expect that these circumstances will be temporary and will end positively. We thus expand on prior theorizing (e.g., Referent Cognitions Theory and Fairness Theory; Folger & Cropanzano, 2001) which has been past-oriented and, as such, has assumed that people think retrospectively about whether events should have happened, could have been avoided, or would have been different if other individuals had made the decision. In summary, we propose the following:

Implications of Model of Organization-Wide Hardship

We suggest five implications of our model of organization-wide hardship. The first implication is that organization-wide hardship is relatively unstudied due to researchers’ primary emphasis on injustice events that affect a subset of organizations’ employees. Our aim in this article has been to sensitize organizational justice scholars to the need to examine situations involving organization-wide hardship, that is, decisions or policies that affect all employees of an organization and that are likely to be seen as unfair.

A second and related implication of our model is that, unless managed effectively, organization-wide hardship likely reduces employees’ perceived overall fairness and increases their turnover intentions and voluntary turnover. Anecdotal evidence in support of this are the thousands of teachers across the United States who have protested for being underpaid and overworked, some of whom expressed the desire to leave their jobs (Pearce, 2018). Prior research has also supported the link between employees’ perceptions of organizational justice and turnover intentions and turnover (e.g., Cohen-Charash & Spector, 2001; Loi, Hang-yue, & Foley, 2006; cf. Ambrose & Schminke, 2009). However, research has also shown that this link is moderated by variables such as socioeconomic conditions and perceived social support. Our model incorporates additional moderators that act as boundary conditions for the link.

This raises the important issue of what it means to manage organization-wide hardship “effectively.” Our model is consistent with prior justice literature that emphasizes the importance for management to provide plausible causal accounts to enhance the perceived fairness of organization-wide hardship. However, our model further suggests that this is only half the battle: Managers will also need to pay attention to nonmanagement sources of accounts for organization-wide hardship that may compete with management’s narrative and pay attention to employees’ expectations regarding the likely duration of the hardship and the positivity of their organization’s future. Moreover, even when management has painted the organization as vulnerable and potentially subject to further difficulties (as is likely when they provide external accounts indicating the hardship is necessary), management needs to encourage employees to stay. Cumulatively, this suggests that there is a need to supplement organizational justice scholars’ typology of accounts (e.g., Bies, 1987; Folger & Cropanzano, 2001; Greenberg, 1993), all of which are past-oriented, with future-oriented vision-inspiring communications.

Our highlighting the fact that, in the Internet age, managers are not the sole source of accounts obtained by employees for their organization’s actions suggests the need to supplement fairness-enhancing communication strategies, all of which tend to be organizational authority–centric (cf. Conlon & Ross, 2012; Rupp et al., 2017), with communication strategies that involve others outside as well as inside the organization. Precisely who these other communicators may ideally be to ensure factual accuracy in employees’ understanding of their organization’s industry-standing and related challenges is another question in need of research—especially given the abundance of informational sources in today’s Internet-facilitated world and the abundance, too, of potentially “fake news” on social media sites and elsewhere (Lee, 2016).

A third implication concerns the issue of how organizations can encourage employees to openly share whatever information they may be obtaining from sources outside of management’s control so that factual inaccuracies can be identified and corrected. Furthermore, how can management enhance the credibility of “factual corrections” it may report back to employees regarding the information they have obtained externally? Might procedural criteria be needed to decide on which facts should be considered “accurate” in organizations today, and if so, how? These are among the questions that our theoretical model raises.

A fourth implication of our model is that while organizations should be concerned with employees’ perception of their overall fairness, this perception alone will not necessarily ensure employees’ loyalty to the organization. This loyalty will be strongly affected by the employees’ perception of their organization’s success or failure based on its position in the market as a laggard or leader. Therefore, organizations can improve their prospects for keeping employees if they are able to persuade employees—with supporting information from nonmanagement as well as management sources—that the organization will be able to overcome its difficulties.

A fifth implication of our model, which extends the previous point, is that managers should recognize the importance that employees will attach to the expected duration of the hardship. This is because duration tends to intensify the moderating effect of perceived necessity on the link between overall perceived fairness and turnover. As a result, management should aim to reduce the duration of hardship to the extent possible so that employees will be more likely to accept it.

Directions for Future Research

Guided by the implications of our theoretical model (stated above), we identify several questions in need of future research in addition to those posed above: (a) Are there differences in how employees react to individual-based injustice versus organization-wide hardship and its perceived injustice, and if so, what are those differences? (b) Which types of causal account-giving strategies are more effective in enhancing employees’ perceptions of overall organizational fairness during times of organization-wide hardship versus individual-based injustice, and are these fairness perceptions influenced by the consistency of management accounts with nonmanagement accounts, especially from media and other external sources? (c) To what extent are employees concerned with the accuracy of the accounts for organization-wide hardship communicated by management and obtained from nonmanagement sources? To the extent that employees are concerned with accuracy, how do they assess it? (d) During times of organization-wide hardship, to what extent are employees’ decisions regarding whether to stay or leave their organization influenced by their perception of overall organizational fairness versus their optimism about their organization’s ability to overcome its difficulties through shared sacrifice? (e) During times of organization-wide hardship, is the positive association that typically occurs between employees’ perceptions of organizational fairness and organizational commitment weaker for employees who perceive their organization to be a market laggard versus market leader and/or who expect the hardship to be long- rather than short-lasting? and (f) During times of organization-wide hardship, what communications by managers are more rather than less effective in getting employees to expect the hardship to be short- rather than long-lasting or, more broadly, to strengthen their organization’s competitive viability?

Investigating these questions will enable future researchers to empirically test all or parts of our theoretical model. If shown to be valid, our model can help guide managers to effectively influence employees’ perceptions of organizational fairness during times of organization-wide hardship. In today’s environment, when managers themselves have limited control over the narratives that come from nonmanagerial sources, this guidance will likely be especially valuable. Indeed, the shutdown of the U.S. government that stopped paychecks for all federal employees for 35 days from December 21, 2018, to January 24, 2019, might be an illustrative context for examining some, if not all, of the questions posed above.

Investigating our set of questions will require operationalizing the variables comprising our model. Such operationalizing, in the form of reliable and valid scales, already exists for overall organizational justice (Ambrose & Schminke, 2009; Masterson, 2001), organizational commitment (Allen & Meyer, 1990; Mowday, Steers, & Porter, 1979), and causal accounts for negative events communicated by management (e.g., Bies & Shapiro, 1987; Harvey et al., 2014; Staw, McKechnie, & Puffer, 1983). Assessing employees’ expectations for the duration of organization-wide hardship is likely to be straightforward (e.g., Schaubroeck et al., 1994).

Measuring the consistency of managerial and nonmanagerial accounts is likely to be somewhat more challenging. However, it should be possible to apply content analysis methods to identify the extent to which management and nonmanagement accounts are consistent, similar to how researchers in strategic management have evaluated the agreement between management perceptions of strategies and market conditions with more objective indicators (e.g., Baum & Wally, 2003; Morgan, Vorhies, & Mason, 2009). Of most relevance for our model, prior researchers have used content analysis methods to assess management explanations and justifications on the attributional dimension of external versus internal (e.g., Mitchell & Kalb, 1982; Staw et al., 1983). Coding schemes for this purpose have been developed and have been shown to produce reliable and valid measures (e.g., Staw et al., 1983; cf. Harvey et al., 2014). With regard to the consistency of management and nonmanagement communications, our model suggests that two categories or dimensions need to be measured: the causal attribution (external vs. internal) for implementing organization-wide hardship and the organization’s industry-standing (e.g., market laggard vs. market leader). Once both management and nonmanagement accounts or communications have been coded along these dimensions, the consistency of these communications can be assessed by using standard measures of reliability commonly used to assess other outcomes or measures (e.g., individual and group performance, leadership style). Thus, consistency of management and nonmanagement explanations will be a matter of degree, similar to measures of agreement or interrater reliability (cf. Dunlap, Burke, & Smith-Crowe, 2003).

With respect to which sources of nonmanagement explanations should be examined, this will likely depend on the particulars of the event in question. Typically, organization-wide hardship events will receive wide media coverage; if so, then news reports and news articles would be suitable sources. In addition, such events will also be the focus of numerous comments and responses on social media, from those both inside and outside the organization. These could also be coded for content (Kulik et al., 2012), although caution in interpreting these messages is warranted because they are likely to constitute an unrepresentative and possibly biased sample from the wider population of interest.

An example of how management and nonmanagement explanations of the same organization-wide hardship event can be compared comes from General Motors’s implementation of large-scale reductions in both its manufacturing labor force and its managerial ranks, due to major plant closings (Telford, 2018). Here we briefly sketch out how a content analysis can be applied to this case. First, we examine the account offered by GM CEO Mary Barra. In announcing GM’s plant closings and layoffs of up to 18,000, Barra stated, The actions we are taking today continue our transformation to be highly agile, resilient and profitable, while giving us the flexibility to invest in the future. We recognize the need to stay in front of changing market conditions and customer preferences to position our company for long-term success (Telford, 2018)

Barra’s announcement and subsequent communications from GM all emphasized that the company had a good industry-standing and that the plans were adopted primarily for strategic, future-oriented reasons. This would be coded as an internal account for the sacrifice.

With respect to nonmanagement accounts, coverage of GM’s plans was extensive. Some of this coverage simply reported on GM’s plans. However, there were also many writers, reporters, and politicians who offered their analysis and opinions of the plans. For example, in her analysis of GM’s plans, Denning (2018) stated that the layoffs were strategically necessary, not because GM was in a weak financial position but because the company’s good performance over the past several years enabled it to undertake a costly strategic repositioning. The layoffs were a “reinvestment opportunity” that would fund new products that would yield a higher return. Another business journalist wrote about GM’s plans: General Motors Co. is acting like a company in trouble . . .But it isn’t—and that’s what makes the automaker’s pessimism so optimistic . . .GM is getting ahead of the curve and angling to be a winner . . . pushing to optimize today’s car and truck business to fund next-generation technology and evolution. (Howes, 2018)

Both Denning (2018) and Howes (2018) agreed that GM had a currently favorable industry-standing but had imposed the layoffs voluntarily for proactive strategic reasons. Both these accounts would be coded as internal accounts for GM’s imposing the hardship. Thus, both the management account and the nonmanagement accounts would show high consistency, with respect to the internal versus external attribution dimension and the industry-standing dimension.

With regard to the research questions listed above, we focus briefly on those that are likely to yield novel and interesting findings on reactions to organization-wide hardship. First, how do employees’ reactions to reduced organizational fairness arising from organization-wide hardship differ from reactions to individual-based injustices? If the overall organization rather than an individual (e.g., supervisor) or a specific situation is seen as unfair, we might expect more consistent and perhaps unified reactions among employees rather than the more idiosyncratic reactions to individual-based unfairness posited by equity theory. Dynamic effects, in which aggregate employee reactions strengthen and become more unified over time, may also occur. This could be investigated by tracking employee turnover and turnover intentions over time subsequent to the imposition of hardship.

Substantial research supports the positive effects of external accounts on employees’ perceived fairness of organizational hardship. Our Proposition 3 reflects this finding. However, our model proposes an important moderator of this effect: the consistency between management and nonmanagement accounts (explanations) for the hardship (Proposition 4). This question has been largely neglected in the justice literature, and we suggest that it has become and will remain increasingly important as media sources proliferate. The challenge for the researcher here, as illustrated by the GM case, is in selecting the appropriate set of nonmanagement sources of accounts, and reliably and validly coding their level of consistency with management accounts. If management and nonmanagement accounts are consistent with respect to the internal–external dimension of causality, we expect that management accounts will be strengthened and that employees will view the organization as more fair. In contrast, inconsistency will weaken the effects of management accounts on overall organizational fairness. A subsidiary research issue concerns employees’ choice of which nonmanagement sources and accounts to attend to. For example, some employees may pay attention to traditional media outlets such as newspaper or television reports, whereas others may attend to social media such as Facebook or Twitter. The determinants of such choices, and their effects on consistency with management accounts and subsequently on perceptions of overall organizational fairness, would be worthwhile pursuing in future studies.

Another issue of likely concern to both scholars and practitioners is our notion that the perceived necessity of the hardship operates as a double-edged sword. If hardship is seen as a “necessary evil,” the organization will probably be seen as more fair, yet also as more likely to fail due to its weak standing in its industry and its vulnerability to external threats. By measuring the key variables in our model (perceived necessity of the hardship, perceived overall organizational fairness, turnover intentions and turnover), along with employees’ estimates of the likelihood of organizational success, it should be possible to investigate the processes by which individuals decide whether to trade the present exposure to organization-wide hardship in return for the expectation of positive work conditions in the foreseeable future. Relatedly, it will be interesting to study, with longitudinal study designs, how hardship survival affects employees’ motivation and behavior, contingent on whether their expectations for a better future have been met or not.

Finally, our model emphasizes the importance of employees’ expectations of the duration of the hardship. In essence, our model suggests that when employees expect the duration of the hardship to be short, they will be more likely to remain in the organization, regardless if they see the hardship as a “necessary” or “unnecessary” evil. Investigating the role of hardship duration adequately will likely require a longitudinal approach and a large sample of organizations that have implemented hardship policies.

Overall, future studies that provide answers to the above questions promise to advance our understanding of how employees respond to organization-wide hardship. In addition, such studies’ results should help managers effectively influence employees’ perceptions of organizational fairness during times of organization-wide hardship and, potentially also, during times when management explanations compete with explanations obtained from nonmanagement sources (e.g., 24/7/365 news sources on the Internet)—circumstances that are absent or nearly absent in the organizational justice literature to date.

Conclusion

In summary, our propositions and their visual summary in our theoretical model highlight the need for managers, during organization-wide hardship, to manage employees’ expectations about their organization’s future as well as employees’ current fairness perceptions. In addition, our propositions and theoretical model suggest that managers should strive, to the extent possible, to ensure consistency between their account for the hardship and the accounts likely to be available through both traditional media sources and the increasing number of Internet-based nonmanagement sources. Finally, our model highlights the need for managers to simultaneously manage employee fairness perceptions and turnover during organization-wide hardship. Empirically testing the relationships proposed by our model will require future studies of organizational justice to broaden the temporal perspective and the information sources typically used in justice measures. In sum, our model is intended to predict and explain responses to organizational policies that impose sacrifice on all employees. Employees’ reactions to such policies are influenced by their expectations of the hardship’s duration, its perceived likelihood of improving their organization’s market position, their perceived overall fairness of the organization, and the communications they receive about the hardship from sources that are not solely controlled by managers.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Associate Editor: Lucy Gilson