Abstract

We examine how regulatory intensity and increases in regulation affect the nonmarket activities of firms. Using a signaling theory perspective, we seek to better understand how firms respond to regulation in terms of corporate social responsibility (CSR) and corporate political activity (CPA), the two main pillars of nonmarket activity. Examination of both CSR and CPA in concert rather than in isolation provides insights into whether they are complements or substitutes. We use textual analysis of the US Code of Federal Regulations to measure regulatory intensity and increases in regulation. Based on a sample of 331 S&P 500 firms for the period 1998–2014, our findings suggest that regulatory intensity leads to more nonmarket responses from firms. We also find support for nonlinear relationships between CSR and CPA.

Keywords

Firms have long understood the importance of crafting an effective nonmarket strategy (Den Hond, Rehbein, Bakker, & Lankveld, 2014). Corporate political activity (CPA) and corporate social responsibility (CSR) initiatives are common nonmarket activities in which firms engage. Mellahi, Frynas, Sun, and Siegel (2016, p.144) define CSR as “corporate actions that appear to advance some social good that allows a firm to enhance organizational performance, regardless of motive” and CPA as “corporate attempts to manage political institutions and/or influence political actors in ways favorable to the firm.” CSR refers to voluntary practices beyond that which is required by law (Brammer, He, & Mellahi, 2015; Griffin, Bryant, & Koerber, 2014). Prior research shows that firms in more regulated industries are likely to expend more resources on and are likely to be more active in the nonmarket arena (Hadani & Schuler, 2013; Hillman, Keim, & Schuler, 2004). While this has received theoretical and empirical support, the general understanding of the influence of regulation has made only limited progress in recent years. Studies of regulation have generally been limited to case studies focusing on a particular firm or empirical examinations of a specific industry (Brown et al., 2019, Gil & Ruzzier, 2017; King & Lenox, 2000). If multiple industries are studied, a very coarse-grained approach is taken (Brown, Yaşar, & Rasheed, 2018). Often industries are categorized into two broad groups of “highly regulated” and “not highly regulated” industries, although it is more appropriate to understand regulatory intensity as a continuum with wide variation across industries. Also, such simple categorizations do not account for the fact that regulatory intensity tends to vary considerably over time for a given industry. Therefore, understanding how firms respond to changing regulation is of paramount importance in nonmarket strategy research on CPA and CSR.

In this article, we examine firm nonmarket responses to regulation and regulatory change. Using a signaling theory approach, we suggest that firms will use the nonmarket activities of CPA and CSR as responses to industry regulation. In addition, we examine the interplay between the two primary pillars of firm nonmarket activity, namely, CPA and CSR and we suggest that firms use these nonmarket activities in concert to a point, at which point resource constraints force firms to firms to make trade-offs between these two primary nonmarket activities.

The nonmarket theory has been developed and explained in the literature mostly by isolating each activity and examining it separately. Through this research, we have learned much about how firms use both CSR and CPA through a variety of theoretical approaches. For CPA, researchers often use the institutional theory (Dorobantu, Kaul, & Zelner, 2017; Mellahi et al., 2016) and resource dependency theory (Schuler, Rehbein, & Cramer, 2002), while CSR researchers often rely on the stakeholder theory (Ghobadian, Money, & Hillenbrand, 2015; Jones, 1995). Rayton, Brammer, and Millington (2015), for example, found that CSR promotes better firm–stakeholder relations. These theoretical insights have helped to guide our improved understanding of nonmarket strategy over the last few decades. Recently, researchers have begun to move away from compartmentalization of distinct nonmarket activities and toward consideration of the entire range of nonmarket activities more holistically. Generally, this has led to examining both CPA and CSR together to better understand how these two approaches can be complements, substitutes, or incompatible actions (Frynas, Child, & Tarba, 2017). But even when both CSR and CPA are examined together, researchers have tended to retain the multiple theoretical perspectives from the previously siloed literature studies (Mellahi et al., 2016). This has hindered the progress of nonmarket research from achieving a degree of theoretical coherence and integration necessary to become a more unified body of research. In this article, we suggest that the signaling theory may offer a promising theoretical approach to integrate nonmarket strategies when we consider firms using both CSR and CPA in concert.

This study makes several contributions to the literature. First, we examine the effect of regulatory intensity on the two major nonmarket activities that firms engage in, namely, CPA and CSR at the same time. The simultaneous examination of CSR and CPA as responses to regulation is a first step toward a more unified theory of nonmarket strategies. Second, we make a theoretical contribution by examining nonmarket activities using a signaling theory lens. We believe such an approach can provide not only novel insights into the actions of both firms and government actors but also provide better theoretical integration. We also contribute by suggesting a resolution to the current debate in the literature about whether CPA and CSR are complements or substitutes by suggesting a nonlinear relationship. We hypothesize an inverted U-shaped relationship between CSR and CPA and introduce the notion that they can be complements at their lower levels and substitutes at higher levels. Yet another contribution we make is the use of a novel approach to measure the regulatory intensity of a given industry. We use data obtained by a textual analysis of the US Code of Federal Regulations. This provides us with a much more fine-grained understanding of the regulatory burden on firms by industry. While this is helpful in our understanding of regulations’ impact on industry competition generally, this is especially relevant for nonmarket research due to the outsized importance of regulation on a firm’s nonmarket activity.

Research on Nonmarket Strategies

The effects of a firm’s CSR activities and its organizational outcomes have been the subject of considerable debate and controversy, both theoretically and empirically. At one extreme, CSR is seen as a case of market failure or an instance of moral hazard where in managers pursue social welfare at the expense of the shareholders. Friedman (1970) went as far as to call it “hypocritical window-dressing” and “fraud.” Institutional theorists explain CSR as efforts by managers to meet institutionalized norms and expectations about appropriate firm behavior (Campbell, 2007). Such behavior may confer legitimacy but may or may not lead to profitability. Stakeholder theorists (Freeman, 1984), on the other hand, argue that by managing the relationships with all stakeholder groups, a firm can gain competitive success over time. The instrumental stakeholder theory (Jones, 1995), a variant of the stakeholder theory, argues that firms prioritize the concerns of stakeholders whose cooperation ensures the highest benefits to the firm. According to this view, contracting costs are reduced when relationships are based on trust, and CSR activities by a firm lead to greater trust. Barnett (2007) and Barnett and Salomon (2012) recently proposed the concept of stakeholder influence capacity (SIC) which they define as the ability to identify, act on, and profit from opportunities to improve a stakeholder relationship through CSR. A firm gains SIC by engaging in CSR, and SIC is accumulated over time by persistent investments in CSR.

Research has focused on identifying the determinants of CSR (eg. Brower & Mahajan, 2013; Ioannou & Serafeim, 2012). Orlitzky, Louche, Gond, and Chapple (2017) suggest that firm, industry, country, and national business systems influence corporate social performance (CSP). Their multilevel study of 2060 large public companies over 5 years found that firm-level factors had accounted for the greatest variability in CSP. These findings support the view of McWilliams and Siegel (2000) who suggested that firm-level factors affect firm spending on CSR. Orlitzky et al. (2017) also argued that industry factors such as an economic downturn influence CSP. They found support for the influence of industry and national business systems on CSP. Petrenko, Aime, Ridge, and Hill (2016) examined the motivations for CSR and identified external and internal drivers. The external factors include, for example, the salience of external stakeholders, the activism of stakeholders, and institutional forces. Internal factors, for example, include executive incentives and the level of commitment to ethics on the part management. Their study focused on the internal factors that reflect executive psychology as they influence CSR. Petrenko et al. (2016) reported that executive narcissism influence CSR. Hambrick and Mason (1984) upper echelon perspective suggests that top management characteristics influence organizational decisions.

In addition to CSR, researchers have also examined CPA as a nonmarket activity of firms. The environment that a firm competes in has been shown to influence the type of CPA a firm chooses, and environment, including regulatory environment, has been found to also be influential beyond CPA mode choice (Hillman et al., 2004). Regulation is one of the most influential variables in determining the likelihood of a firm engaging in CPA (Mitchell, Hansen, & Jepsen, 1997), and regulation has a long history in nonmarket research (Stigler, 1971). Firms have been found to choose to lobby in order to encourage or discourage regulation within an industry. Firms respond to high levels of regulation in their industry with political involvement. One of the reasons for this is that political market attractiveness can influence a firm’s decision of whether or not they should become politically active (Bonardi, Hillman, & Keim, 2005), and in highly regulated industries, the political attractiveness increases because government has an increased role in the industry. This makes business government relationships more important than in a less highly regulated industry. Firms also engage in CPA during decreases in regulation such as when industries become completely deregulated. The pace and scope of deregulation has a great deal of influence on how firms will respond (Kim & Prescott, 2005; Vietor, 1994).

The above review of prior research on CSR and CPA suggests several conclusions. First, the CSR and CPA research streams have progressed mostly independent of each other. Given that these nonmarket activities may not be independent of each other from the perspective of the firm, it is imperative that we examine them jointly. Second, such a joint examination may require some degree of theoretical integration between the two. Therefore, in the next section, we suggest that the signaling theory may provide us with the tools to undertake such an integration. Toward this, we suggest possible nonlinear conceptualizations of the relationship in our hypotheses section.

Signaling Theory and Nonmarket Activity

“Signaling theory is useful for describing behavior when two parties have access to different information” (Connelly, Certo, Ireland, & Reutzel, 2011, p. 39). Actors of interest in the signaling theory are the Signaler and the Receiver. These actors engage in two main actions. The signaler will send Signals to the receiver to help decrease the information asymmetry between both parties. The receiver will then provide feedback to the signaler. As explained below, we find that each of these actors and actions are present in nonmarket strategy. The firm engaged in nonmarket activity is the signaler. The receiver is the politician of interest. The nonmarket action, whether CPA or CSR or both, is the signal that firms send to the receiver or politicians. Politicians provide feedback in a variety of ways, but the most important is passing favorable legislation for the firm or blocking unfavorable legislation from being passed. In one of the few examinations of nonmarket activity using the signaling theory, Ridge, Hill, and Ingram (2018) examined the politician as the signaler and the firm as the receiver. In some cases, such as the example they studied of politicians holding firm stock, this is the phenomenon of interest, but in general, firms are the ones sending signals to politicians as a part of an integrated nonmarket strategy consistent with previous nonmarket research (Hillman et al., 2004). The politicians, rather, are sending feedback to the firms through changing regulations.

In the nonmarket arena, politically and socially active firms are acting as signalers to government officials. Firms can use a variety of nonmarket actions to send signals to government officials about issues that are key to them. Two of the most important issues that government actors are concerned with are (1) funding future campaigns and (2) obtaining enough future votes to attain reelection. Next, we will discuss how firms can, by using a combination of nonmarket activities, provide positive signals to politicians in both of these areas. We then discuss political feedback through legislation.

CSR and CPA are two key nonmarket activities that firms use to signal to government actors that the firm will be a helpful asset for both future political funding and future votes. Naturally, contributions to political action committees (PACs) and lobbying through CPA will help candidates to fund their campaign. This direct or indirect transfer of money from the firm to the political system is highly sought after by political actors because it is necessary to succeed in the current political environment (Gilens & Page, 2014). In addition, CPA is very rarely a one-time event. It is often seen as relationship building that takes place over time (Brown, Drake, & Wellman, 2014). For this reason, firms engaging in CPA are not only contributing to a politician’s ability to fund his or her current campaign but they are also signaling future funding, often referred to as signal Reliability in signaling theory research. In addition, previous research has found that Frequency of signaling over time can help to increase the effectiveness of the signaler (Brown et al., 2014). Since one key resource that politicians must acquire is capital to fund future campaigns, CPA signals to political actors that access to capital in the future will be possible with continued relationships with this firm. But CPA is not sufficient in and of itself to politicians due to the varied nature of their needs.

Money alone will not obtain politicians their desired goal of reelection. It is a necessary but not sufficient tool. To succeed, politicians need to convert those dollars into future votes. In addition to funding, politicians need support from the general public. This is where CSR can come into play. CSR signals two things to politicians. First, CSR signals to the political actor that he or she will not have to worry about losing votes by working with a particular firm. A long line of research has shown that firms engage in CSR to gain a favorable reputation for the firm (Lii & Lee, 2012). This favorable reputation can increase the politician’s confidence that partnering with the firm could help him or her acquire more votes, or at the very least, partnering with firms that hold favorable public reputations should not hurt the politician going forward.

CSR is thus helping to indicate Fit between the firm and the politician. The signaling theory highlights the need for signal Fit for the signal to be appropriate and achieve the desired result. Busenitz, Fiet, and Moesel (2005) found that context matters in signaling; in their case, signal timing was important for signaling to be effective in long-term success for new ventures sending signals to venture capitalists. In nonmarket strategies, temporal fit is less important than ideological fit. Ideological fit has become increasingly important for politicians due to increasing political polarization which is currently at the highest point in two decades (Pew, 2014). Increased Chief Executive Officer political activism (Brown, Manegold, & Marquardt, 2020; Chatterji & Toffel, 2016a, 2016b) and a growing distaste by consumers for heavy political activity from individual leaders (McGregor, 2016), especially if that activity is counter to the consumers’ own political bents, must also be considered by politicians accepting funds from firms. Recently, politicians have attempted to distance themselves from political donations from organizations or individuals that they do not agree with or with whose association might be harmful by refunding or donating contributions given by individuals or groups that they do not want to be associated with (Martin, 2017; Willis, 2015). By providing a reputational benefit, CSR can mitigate the risk of firm CPA becoming ineffective through a lack of fit.

CSR, in addition to providing positive reputational signaling to the political actor, it can provide financial signaling as well. CSR is expensive. Cash donations to worthy causes have been found to act as a signal of financial strength (Shapira, 2012). This is more indirect than lobbying, but a strong CSR presence from a firm, combined with CPA, can provide positive signals of future financial support to government actors.

In the signaling theory, another important variable influencing the effectiveness of the signal is signal cost. Spence (1974) seminal work examined job applicants’ signaling behaviors in labor markets. Spence specifically illustrated that high quality candidates would engage in either costly or rigorous higher education. This decreased information asymmetry between the applicant and the firm regarding applicant quality. For nonmarket strategy, signal cost is easily measured by the amount of money spent on CPA and the intensity of CSR that the firm engages in. Signaling cost is one of the most important variables in effective nonmarket strategy. For CPA, large firms that can engage in the most political activity dominate the political landscape (Hillman et al., 2004) because they are able to provide the loudest signals of future funding to politicians.

Another important aspect of effective signaling for a firm is signal observability or the extent to which outsiders are able to notice the signal. While CPA is easily observable due to the mandated reporting requirements thus increasing large firms’ dominance in CPA, these large firms are also better able to maximize their CSR spending by publicizing their actions and increasing their reach and effectiveness (Servaes & Tamayo, 2013). The ability to publicize CSR activities increases the extent to which outsiders can notice the signal sent by the firm.

Finally, for firms and politicians to effectively use a signaling approach to solve the information asymmetry problem inherent in the nonmarket, politicians must have a feedback mechanism by which they communicate to firms. For politicians, this involves regulation. Previous nonmarket research has highlighted the effect that regulation has on firm nonmarket activities. Firms in highly regulated industries are more likely to engage in CPA (Hillman et al., 2004). We expect this because firms which compete in industries heavily influenced by government regulation would like to have a voice in the policy conversation regarding the large concentration of regulation they face in their industry. Regulation can have different impacts on different industries, but in heavily regulated industries, regulation has the effect of raising the heights of entry barriers, thus reducing competition within the industry.

In addition to CPA, prior research suggests that firms in highly regulated industries are more likely to engage in CSR (Campbell, 2007). Barnett (2007) suggests that firms can begin to engage in a nonmarket arms race with their competitors by increasing both indirect nonmarket activities such as CSR and direct nonmarket influence tactics such as CPA in concert and in response to their competitors. We expect that these two pillars of nonmarket strategy are satisfying different demands of the political actors they are intended to influence. The quid pro quo relationship between firms and politicians in the nonmarket will break down over time if firms begin to not reliably or frequently signal to the politician that the engagement in nonmarket activities will continue or if the politician consistently fails to provide the firm proper feedback in the case of favorable regulation.

The necessity to engage in nonmarket strategies increases as increase in regulation occurs or is anticipated to occur. Due to difficulties in measuring increase in regulation, we know little about how firms respond to regulatory increase outside of studies of individual firms and industries (Gruca & Nath, 1994; Hillman, Cannella, & Paetzold, 2000). A highly regulated industry might not necessarily experience regulatory uncertainty if the regulation is high but constant. In this article, in addition to examining regulatory intensity, we also shed light on the effects of regulatory increase on a firm’s nonmarket strategy. Politicians can use current legislation as a feedback mechanism to communicate to firms their approval of the firm’s current nonmarket approach. Politicians have direct control over the intensity of regulation for an industry. They can use increase in regulation as a feedback loop to encourage continued CPA and CSR from firms in the marketplace.

Hypotheses

The signaling theory is particularly useful in understanding situations characterized by asymmetric information (Akerlof, 1970; Spence, 1974). Firms engage in nonmarket activity in order to send nonmarket signals to politicians. This activity includes CSR and CPA. When there is government involvement or the potential for government involvement in an industry, firms in that industry experience information asymmetry. In industries with low regulation and low government intervention, companies are not incentivized to engage in nonmarket activity because of the absence of information asymmetry. They know what to expect from politicians in regard to government intervention and they are not incentivized to engage in nonmarket activity. In addition to the base level of regulation being important, regulation increase is also of interest to firms. For companies engaged in industries with small regulatory increases, there is minimal incentive to engage in political activity. They are unlikely to receive positive benefits from their nonmarket activity.

CSR constitutes a powerful signal to the general public that the firm is a good citizen and an important stakeholder in the community. For legislators, support from the public is a necessary requirement for reelection. CSR can help to ingratiate firms with the public. The rise in social media has led to a subsequent rise in individual activism. This activism can influence who firms hire or retain as leaders (McBride, 2014), perceptions of inclusivity (Wheeler & Sillanpa, 1998), and willingness to buy from the firm (Chatterji & Toffel, 2016a, 2016b). Firm’s CSR can mitigate the risks of negative public activism in the current environment. This is helpful for remaining competitive in the market, but it also can be helpful with the firm’s nonmarket activity. Politicians want to avoid being associated with negative public reactions and for that reason, they will avoid ties with firms likely to receive political backlash. Recently, politicians have returned or donated campaign contributions to charity after receiving backlash for accepting funds from individuals who have come under public scrutiny. Firms’ CSR aimed at the general public can mitigate these backlashes and help make nonmarket strategy less risky and more robust. Regulatory constraints are enacted and firm activities constrained when society in general perceives that firms in an industry are causing more social harm than good in their pursuit of profits. Good citizenship behavior can increase the social legitimacy of the firm and can lead to less negative attention by regulators. This is most important in regulatory environments which are high in both the level of regulation and in regulatory increase. High levels of government involvement in an industry and changing government involvement are expected to increase a firm’s participation in nonmarket strategies to manage this government involvement in the industry. Given that CSR is an important pillar of nonmarket strategy, we hypothesize that

In addition to firms using CSR as a nonmarket signal in response to the overall amount of regulation the firm faces in its industry, firms also respond to changing regulation with CPA. Firms engage in high levels of political activity in response to new and changing regulatory environments from a variety of industries including technology, banking and finance, and insurance, amongst others (Center for Responsive Politics, 2016). From a signaling theory perspective, this has the potential to create a self-perpetuating feedback loop (Ehrhart & Ziegert, 2005). As firms engage in CPA, they send a signal that they will be involved in supporting a particular platform over the long term. Politicians respond with favorable legislation as a feedback loop which is met with ever more consistent CPA from the firm. We see this in practice as firms very rarely engage in CPA as a short-term strategy but rather as a long-term investment in the political process (Brown et al., 2014). Policy demands of the constituents and public opinion have a far greater weight on large scale policy initiatives, but politically active firms are able to help craft the legislation in a way favorable to the firm or to obtain political concessions in tertiary related bills that politically inactive firms cannot obtain. For these reasons, we expect that in cases of both high regulation and high regulatory increases, we will see firms increase their political activity.

CSR and CPA have generally been studied in two separate streams of research (Ahammad, Tarba, Frynas, & Scola, 2017; Mellahi et al., 2016). While there is some recognition in the literature of the need to study their interrelationship, to date, we have only very limited research on the precise nature of the relationship between the two (Boddewyn & Buckley, 2017; Mellahi et al., 2016). Prior literature suggests three possible relationships between CSR and CPA. Arguments have been presented that they are complements, substitutes, or are mutually exclusive (Ahammad et al., 2017; Frynas et al., 2017; Mellahi et al., 2016). While there is growing interest in nonmarket activities, there is also little research on their combined effects (Liedong, Rajwani, & Mellahi, 2017). Some scholars argue that integrating CPA and CSR has implications for firm performance (Den Hond et al., 2014; Liedong, Ghobadian, Rajwani, & O’Regan, 2015; Rehbein & Schuler, 2015).

A recurring argument in the nonmarket literature has been that CSR and CPA complement each other (Den Hond et al., 2014; Liedong et al., 2015; Marquis & Qian, 2014; Rehbein & Schuler, 2015). CSR may contribute to CPA by “facilitating access to the political system and its efficacy” (Frynas et al., 2017, p. 561). However, Liedong et al. (2017) found no empirical support for complementarity in a study of political ties and CSR in 179 firms in Ghana. A competing theoretical perspective has been that CSR and CPA are substitutes as they involve the expenditures of limited and valuable firm resources (Mellahi et al., 2016). Support for this perspective comes from a study by David, Bloom, and Hillman (2007) who examined shareholder activism, managerial response, and CSP in a sample of 218 firms. A third perspective is that CSR and CPA are “distinct arenas” (Ahammad et al., 2017) or are mutually exclusive. Research by Jamali and Mirshak (2010) suggests that in conflict-prone regions, firms face incompatibility between social and political activities.

Prior research on the signaling theory has found that in some contexts, multiple signals work better than single signals because in combination, they tend to be more effective. For example, recent research on crowdfunding suggests that both start-up actions and founder characteristics serve as signals and together they reduce information asymmetry between founders and potential backers, increasing the likelihood of crowdsourcing success (Courtney, Dutta, & Li, 2017). Plummer, Allison, and Connelly (2016) suggest that new ventures will seek out investment to act as a signal of their potential to third parties. They also use this investment as additional signaling, such as a signaling of the entrepreneur’s characteristics and actions. The nonmarket is a noisy market and a combination of the two pillars of nonmarket activity can also combine to magnify the signaling in the nonmarket. That is why we see firms that begin to engage in nonmarket activity in one domain also begin to engage in the other. However, the ability to engage in multiple signaling is constrained by the availability of resources. While firms engaged in the nonmarket will often want to send multiple signals by engaging in both CSR and CPA, at some point, there is an inevitable trade-off between the two. When firms are engaging in extremely high levels of one nonmarket activity, they no longer have the resources or attention to effectively participate in both.

We propose a resolution of competing arguments from prior research by suggesting that the CSR–CPA relationship may be curvilinear. More specifically, we propose an inverted U-shaped relationship between CSR and CPA. Testing for curvilinear relationships allows us to examine more complex relationships between variables, further theoretical development, and highlight implications for the management of companies (Meyer, 2009). When a firm begins to engage in the nonmarket, it may engage in both CSR and CPA to a limited extent. Thus, initially, CSR and CPA have a positive relationship supporting a complementary relationship. At some point, this relationship becomes negative as firms must consider their costs and decide on where to expend their valuable resources. This suggests that beyond a certain level, CSR and CPA become substitutes. Therefore,

Methods

Sample

This is a longitudinal study that includes all firms identified in the S & P 500 on January 1, 2014. Data were collected from publicly available sources for each firm from 1998 to 2014. Regulation measures were collected from RegData. The source for the CSR data was the KLD (https://en.wikipedia.org/wiki/MSCI_KLD_400_Social_Index) database. The source for the CPA data was the Center for Responsive Politics. Compustat was used for the control variables. Full data across all variables were available for 331 firms.

Variables

Regulation

This study includes two variables of a firm’s regulatory environment: increase in regulation and level of regulation. We used the RegData database and collected measures of regulatory restrictions for each industry and year. “RegData annually quantifies federal regulations by industry and regulatory agency for all federal regulations” (Al-Ubaydli & McLaughlin, 2017, p. 109). RegData uses text analyses “to count binding constraints in the wording of regulations” by industry using the NAICS (https://www.naics.com/search/) System. The RegData database is an attempt to quantify the regulatory burden by examining the content of the regulatory text. Regulatory restrictions are measured by examining the text of the US codebook of regulation. The words shall, must, may not, required, and prohibited are used as proxies for regulation because these are words used in legal documents to create binding obligations or prohibitions. Using machine learning, probability of relevance was calculated for each regulation at the industry level by NAICS code. Using tens of thousands of publications from the Federal Register that specifically mention NAICS codes affected by regulation as training documents, machine learning algorithms are able to “learn” which regulations are targeted at which industries. Each firm in our dataset was identified by its major 3-digit NAICS code using Compustat. We collected data for the number of regulatory restrictions at the 3-digit NAICS level for each firm and year from RegData. We then operationalized the increase in regulation by calculating the increase in restrictions from one year to the next. We also operationalized level of regulation as the number of restrictions at the 3-digit NAICS level. The log of the level of restrictions was computed to normalize its distribution. For the analyses, the log of restrictions was lagged by one year. In sum, this study has two measures of regulatory environment: level of regulatory restrictions and the increase in regulatory restrictions.

CSR

This study measures CSR using the KLD database which is widely cited in previous empirical studies (e.g., David et al., 2007; Mattingly, 2017; Mattingly & Berman, 2006). Scholars suggest that the KLD measures have the advantage of construct validity and reliability and of being based in theory (Strike, Gao, & Bansal, 2006). KLD uses a range of sources such as data that are publicly available, surveys, and expert opinions (Jayachandran, Kalaignanam, & Eilert, 2013). It rates the CSR of firms in terms of strengths and concerns in key areas. We computed a measure of KLD strengths by summing up the scores for all KLD dimensions.

CPA

In this study, we measured CPA by summing the total lobbying expenditures and PAC contributions following Hadani, Dahan, and Doh (2015). We collected the CPA data from Open Secrets.org (Center for Responsive Politics, 2016). Lobbying expenditures and campaign contributions are the most commonly used measure of a firm’s CPA in the literature (e.g., Hillman et al., 2004; Lux, Crook, & Woehr, 2011; Mitchell, 1995). The Lobbying and Disclosure Act, 1995 requires the disclosure of lobbying expenditures and political contributions by companies.

Control Variables

We included two firm-level controls: size and slack. Firm Slack was measured as the debt to equity ratio, and it is commonly found to be highly influential in nonmarket research (Hillman et al., 2004). Firm Size was measured as the number of employees. In nonmarket studies, employee count has been used to control for firm size (Hadani, Doh, & Schneider, 2018; Hillman, 2003; Meznar & Nigh, 1995; Sambharya & Goll, Forthcoming; Su & Tsang, 2015). To normalize the distribution of firm size, we computed a log transformation. To control for industry-level influences, we included two controls. Industry Concentration was computed as the sum of squares of the market shares of firms in each industry. According to Boyd (1995), the H-Index can range from near zero to 1. Industries with many small firms of similar size fall on the lower end of the scale and a score of 1 indicates a monopoly. The second industry-level control measure is Industry Profit Margin. The industry-level variables were calculated at the 4-digit SIC level and taken from Compustat.

Results

The data were analyzed using linear regression with panel-corrected standard errors in STATA version 15 and the xtpcse command which produces the Prais–Winsten estimates when autocorrelation is specified. We calculated variance inflation factors (VIFs) for all of the regression equations. The VIFs for the variables as well as for the overall equations were below 10 suggesting multicollinearity was not a problem. We also computed Condition Indices for the predictors in each model. No Condition Index exceeds 30, the commonly recommended cutoff (Belsley, Kuh, & Welsch, 1980; Hallen & Pahnke, 2016). Our highest Condition Index out of all our models is 6.3209 and the mean VIF is 1.51, both of which are well below the thresholds for multicollinearity (Belsley, 1991).

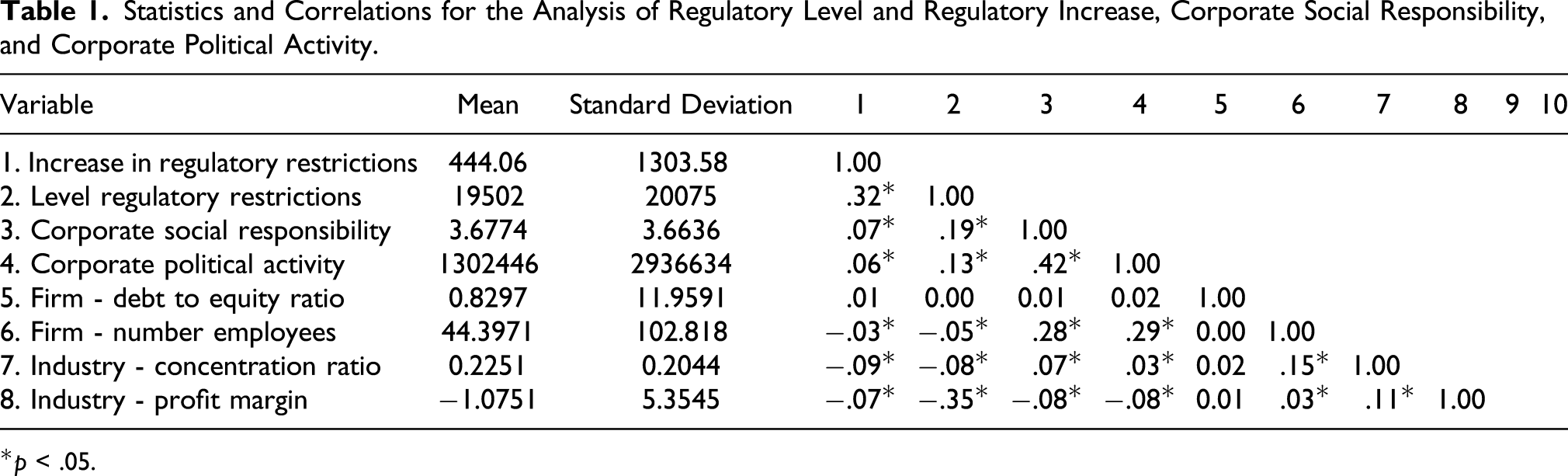

Statistics and Correlations for the Analysis of Regulatory Level and Regulatory Increase, Corporate Social Responsibility, and Corporate Political Activity.

*p < .05.

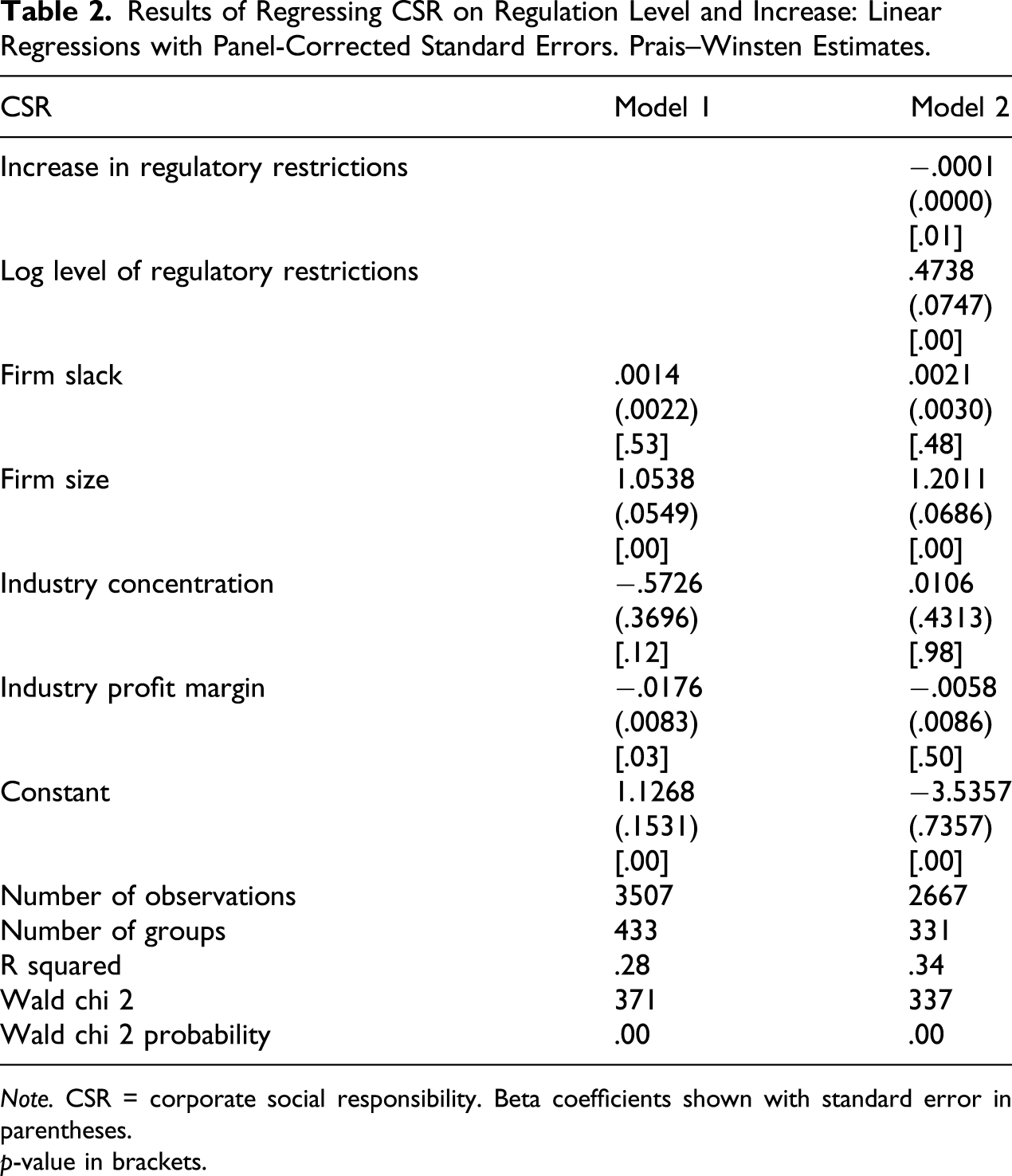

Results of Regressing CSR on Regulation Level and Increase: Linear Regressions with Panel-Corrected Standard Errors. Prais–Winsten Estimates.

Note. CSR = corporate social responsibility. Beta coefficients shown with standard error in parentheses.

p-value in brackets.

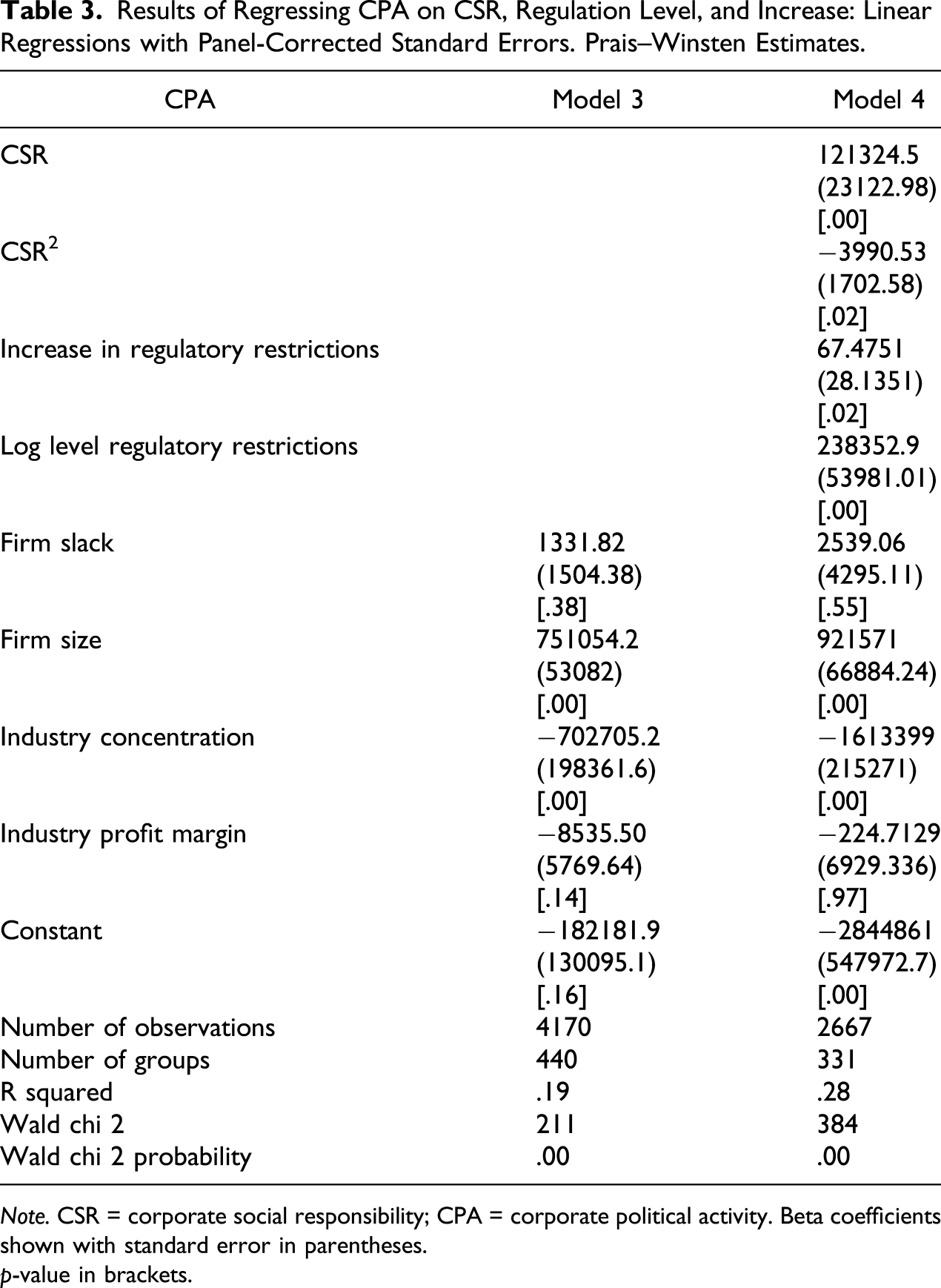

Results of Regressing CPA on CSR, Regulation Level, and Increase: Linear Regressions with Panel-Corrected Standard Errors. Prais–Winsten Estimates.

Note. CSR = corporate social responsibility; CPA = corporate political activity. Beta coefficients shown with standard error in parentheses.

p-value in brackets.

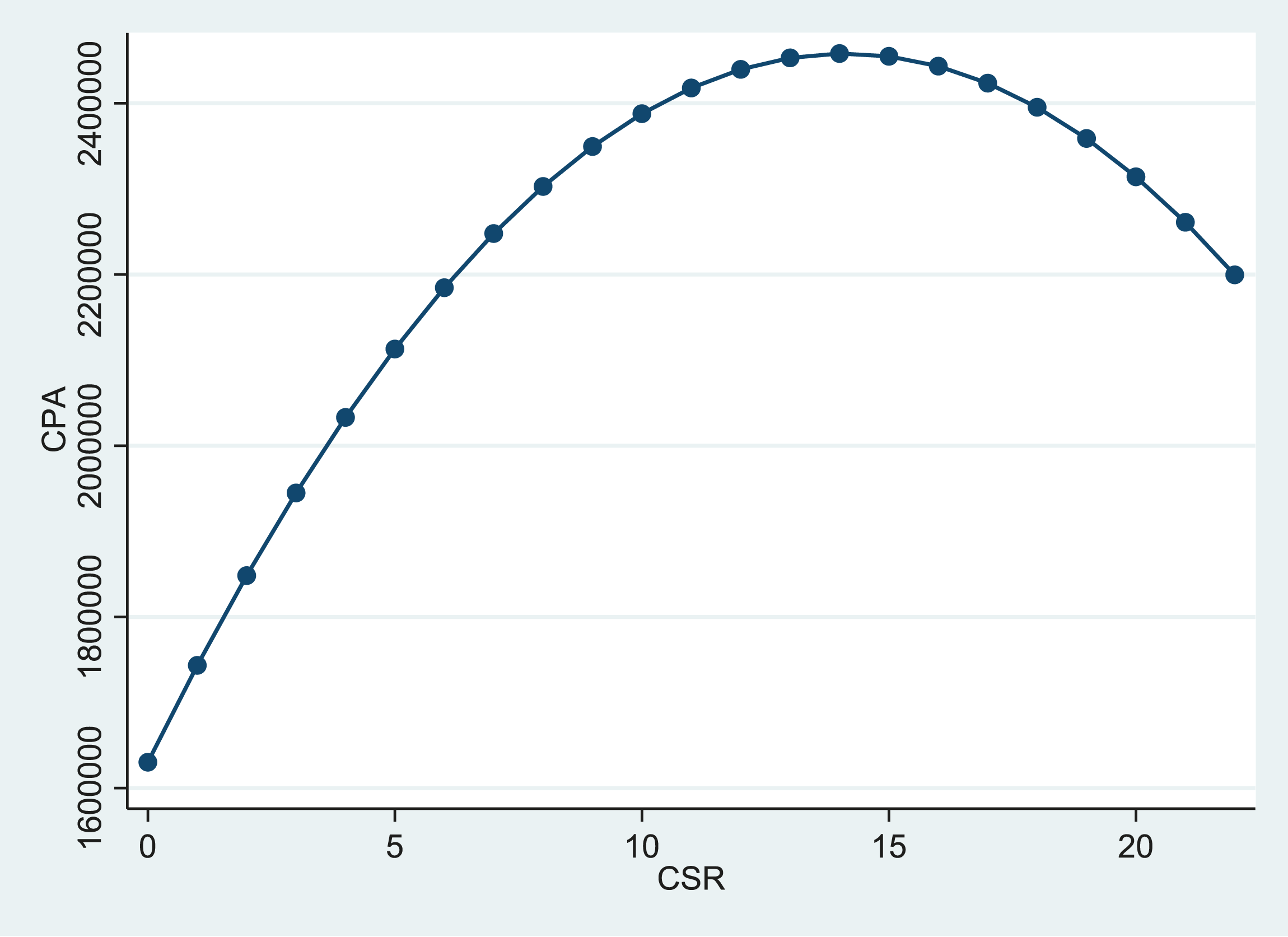

Results of regressing corporate political activity on corporate social responsibility.

Discussion

The results of our study provide interesting insights about how the regulatory environment of an industry affects the responses of firms in terms of their nonmarket strategies. We found a significant relationship between regulatory level and CSR. These results suggest that one way in which firms respond to regulation is by increasing their CSR. This serves as a signal to their stakeholders that the firm is committed to society at large. Even more importantly, it signals to the politicians and government officials that interactions with them will not become a political liability. In addition, CSR spending signals to government officials that the firm is well financed enough to be a potential political backer that can fund future campaigns. Thus the results of our study demonstrate that signaling theory can be a valuable theoretical tool to analyze and understand nonmarket strategies of firms that complements prior work on nonmarket activity in the literature.

This study suggests that firms also increase their political activities in response to both the level of regulation and additional increases in regulation. We reason that another way in which firms respond to the regulatory environment is by increasing their political activities such as lobbying and PAC expenditures. These findings support the literature on CPA which argues that firms engage in this nonmarket strategy by trying to influence the environment so that it is more favorable for conducting business. They also contribute to the literature by providing insight into how the variance in regulation across industries can influence the nonmarket strategies firms engage in.

The curvilinear relationship between CSR and CPA reported in this study makes a significant contribution to the nonmarket literature. As noted earlier, there is a debate in the management literature as to whether CSR and CPA are complements or substitutes (see Mellahi et al., 2016). While some researchers argue they are complements and others argue they are substitutes, our study suggests they are both, depending on their levels. This finding contributes to the theoretical literature that links CSR and CPA. At lower levels of CSR, CSR and CPA have a positive relationship. At higher levels, their relationship becomes negative as firms decide whether to pursue one nonmarket strategy or the other.

The joint examination of CPA and CSR in concert represents a more holistic approach to the study of nonmarket strategies than the prevalent approach of examining them separately. Further, the use of a fine-grained measure of regulation based on text analysis adds greater richness to the operationalization of regulation. Our findings suggest that firms in industries with high levels of regulation are highly likely to engage in both pillars of nonmarket activity. In highly regulated industries, satisfying a wide variety of stakeholders is paramount, and firms in these industries use both pillars of nonmarket activity to improve relations with government actors and the general public. Interestingly, we find that during times of regulatory increase, firms rely more on CPA than on CSR. We attribute it to the fact that the positive benefits of CSR are more long term whereas CPA tends to be more targeted and potentially capable of producing results in the near term. CPA can help firms to directly influence the legislators or administrative agencies responsible for the increasing regulation. CPA can influence not only the content of regulation but also its subsequent implementation. Therefore, it is understandable that firms respond to increases in regulation by committing greater resources to CPA.

Limitations and Future Research

This study has several limitations. The sample includes the largest firms in the United States identified in the S & P 500. As such, the results are generalizable to larger firms. Subsequent research can examine these relationships in smaller firms which may not have the same resources for their nonmarket strategies. Although the data are longitudinal, we cannot definitively determine cause and effect. Another limitation is the use of KLD strengths to measure a firm’s social responsibility. Future studies could extend this to include other measures.

The signaling theory would suggest that politicians provide firms feedback in the form of regulation that benefits the firm. This creates an ongoing nonmarket loop of Signal and Feedback as firms engage in lobbying and politicians pass new legislation over time. In this article, we do not test the full model feedback loop over time and instead we examine only one segment of this circular relationship. Future research should empirically examine the full theoretical model to better understand the firm—government interaction found in nonmarket behavior.

Future research should also investigate firm-level payoff from nonmarket activities. In some industries, nonmarket activities will pay off in the form of subsidies, while in others, it will pay off in the form of mitigated regulatory restrictions. In addition, some firms may be more likely to receive government contracts if they are successful in managing their nonmarket activities. While all of these activities will influence the business bottom line, future research should examine the heterogeneity in nonmarket benefits and the firm performance implications of these differences which we do not do in our work. In addition to firm-level payoff which is common in the literature, future research should further examine firm’s nonmarket response to industry-level regulation. While our dataset uses fine grained data to examine the industry response to firm regulation, the nature of the data may not perfectly measure regulatory impact as some regulation may be easier or more difficult to comply with which is not picked up by the magnitude of restrictions written into the law.

While outcomes of nonmarket activity might vary due to the unique industry dynamics that a firm faces, the dynamics of political polarization (Pew, 2014) might begin to change the way in which firms engage in the nonmarket altogether. Investigating the target of political spending might provide insight into nonmarket activity as political polarization increases.

Conclusion

In this article, we attempt to further our understanding of firm nonmarket activities in response to regulation. We found that firms engage in both main nonmarket activities (CPA and CSR) together and they do so in response to regulation. Both regulation levels and the increase in regulation led to increased nonmarket activity. The results suggest that firms are making complex nonmarket strategy decisions in response to the regulatory burden of their industries. There is clearly a greater need to develop a more refined understanding of the interplay between governments and firms. Governments may want to set the rules of the game, but firms also want a voice in setting these rules because they have an impact on both the strategic discretion available to firms and their performance. This article makes a modest beginning in that direction.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Note

Author Biographies

![]() is an assistant professor at University of Texas at Arlington. He received his Ph.D. from the University of Alabama. His research focuses on employees’ work and life domains, identity, and supervisor-subordinate dynamics in the workplace, including leadership and abusive supervision.

is an assistant professor at University of Texas at Arlington. He received his Ph.D. from the University of Alabama. His research focuses on employees’ work and life domains, identity, and supervisor-subordinate dynamics in the workplace, including leadership and abusive supervision.