Abstract

One of the principal aspects of environmental ergonomics in open-plan offices is the acoustic comfort. Human factors/ergonomics experts should be able to evaluate these spaces in terms of their acoustic condition and propose optimal interventions. We examined the acoustic conditions of a typical open-plan bank office. The acoustic condition of the bank was not desirable, and the inappropriate design of the workstation partitions was one of the major acoustic problems in the bank. We proposed a practical approach for designing an optimal acoustic plan for the workstations and prioritized functional schemes to improve the acoustic conditions of the bank.

Keywords

Human factors/ergonomics experts should evaluate open-plan offices in terms of acoustic comfort.

Open-plan office refers to offices and similar workspaces designed for more than one person where people interact and talk with each other. In open-plan offices, there is no private space or a wall between people, and the workstations are only separated by partitions. Nowadays, to meet the economic concerns and optimally use available spaces, the use of open-plan offices is becoming more popular. About 60% of French companies use open-plan offices (Pierrette, Parizet, Chevret, & Chatillon, 2015). Although communication and interaction between staff are facilitated in open-plan offices, the acoustic comfort has decreased in such spaces (Brookes & Kaplan, 1972; Golmohammadi, Aliabadi, & Nezami, 2017; Sundstrom, Burt, & Kamp, 1980).

Acoustic comfort is one of the important aspects of environmental ergonomics in office spaces. According to a report by the World Health Organization (WHO), noise has direct and indirect effects on the mental and physiological health of individuals. Noise in open-plan offices reduces mental function, decreases productivity, weakens the ability to understand coworkers’ speech, increases human errors, causes stress, and particularly increases the stress and fatigue in staff (Basner et al., 2014; Golmohammadi et al., 2017; Haapakangas, Hongisto, Hyönä, Kokko, & Keränen, 2014; Lee, Lee, Jeon, Zhang, & Kang, 2016).

Human factors/ergonomics (HF/E) experts should be able to evaluate and comment on the acoustic conditions in open-plan offices. Additionally, the ability to find the main causes of acoustic discomfort in staff and provide ways to improve their acoustic comfort are the factors that enhance the competence of the HF/E experts. In this study, we aimed to evaluate the acoustic conditions of a typical open-plan bank office. Accordingly, we used a structured design to find out the main causes of disturbance in the acoustic comfort of staff. Finally, we proposed plans to improve the acoustic conditions of such open-plan offices.

Open-Plan Bank Office

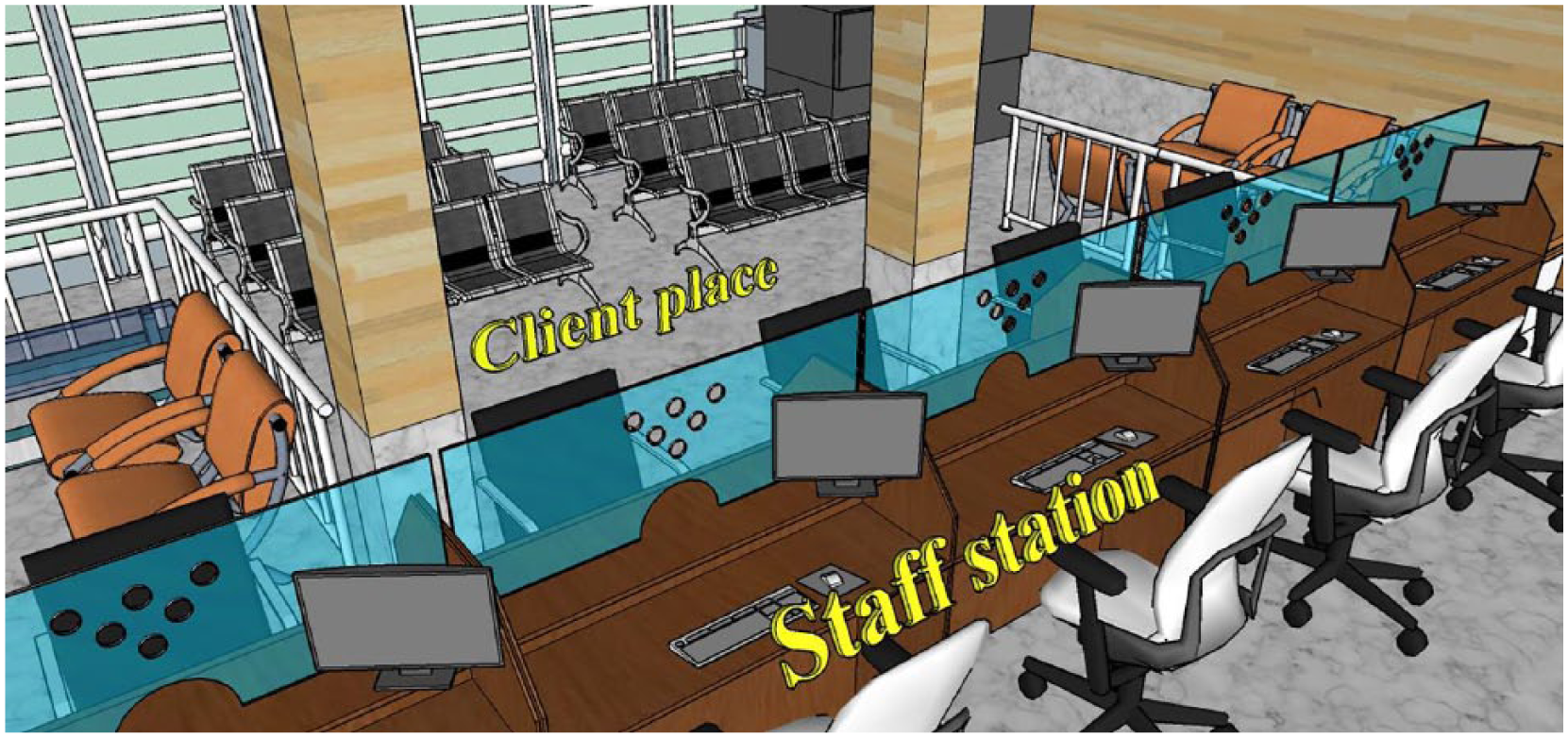

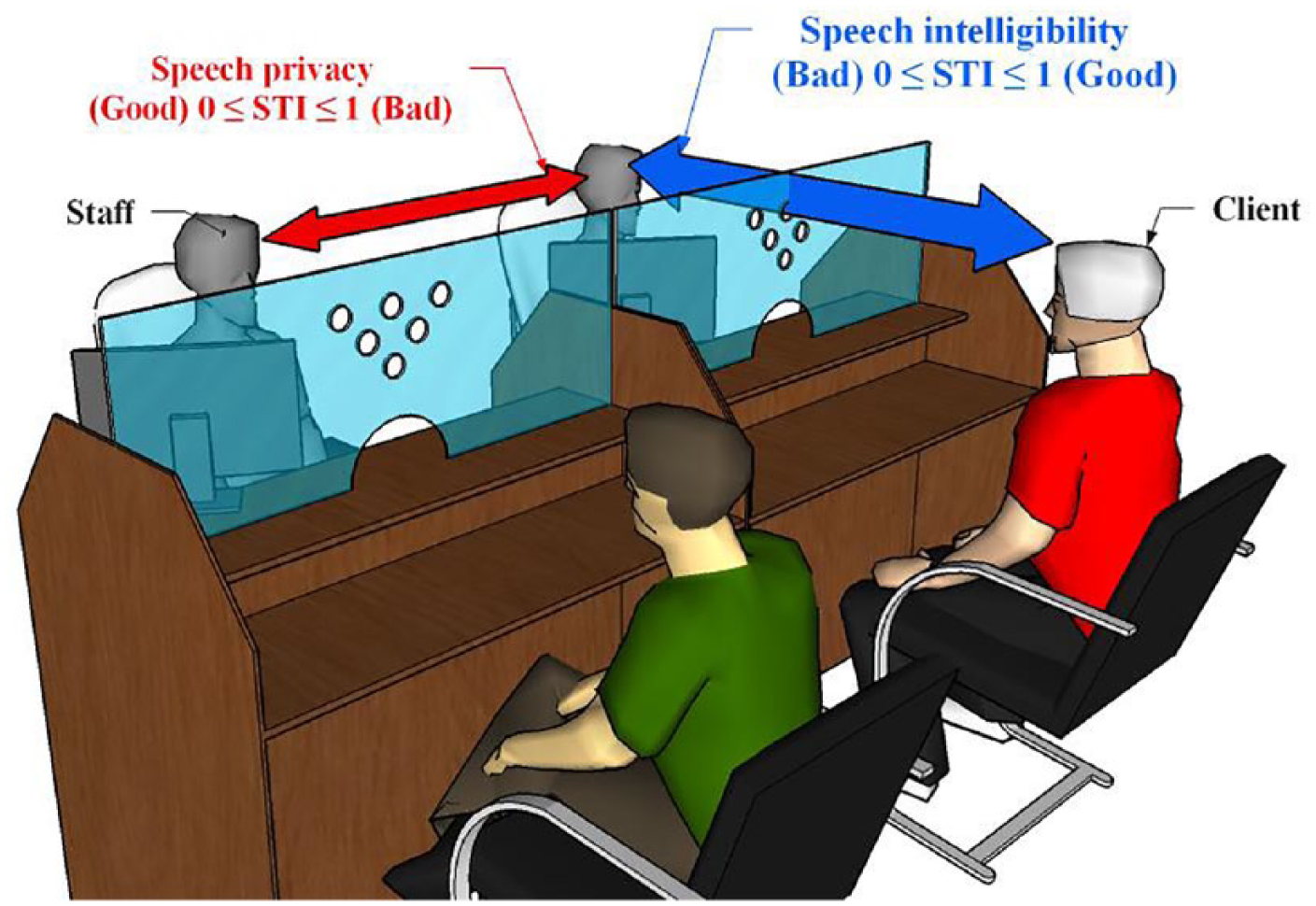

This study was conducted in a typical bank with a typical shape that used a special type of the partitions between staff and clients (S&C) and between the workstations of staff as well. As shown in Figure 1, the staff were on one side and clients were on the other side of the partitions; on the top of the partitions, between S&C, there was a thick layer of glass. To allow face-to-face communication, the glass had a number of circle holes for verbal communication. The semicircular holes in the bottom of the glass were usually used to exchange documents.

Shape of the partitions installed between the workstations of staff and between staff and clients (S&C) of the bank.

To carry out their tasks effectively, staff must be able to communicate verbally with clients. Staff must perform many computational, financial, and administrative activities, and these types of activities impose a heavy workload that requires focus, precision, and attention. Noise is one of the most important factors involved in disrupting the concentration and comfort of the staff in these work environments. We prepared a structured design to assess the acoustic conditions of the bank as well as the acoustic comfort of the staff at their workstations in three steps.

Step 1: Determining the Noise Source in the Bank

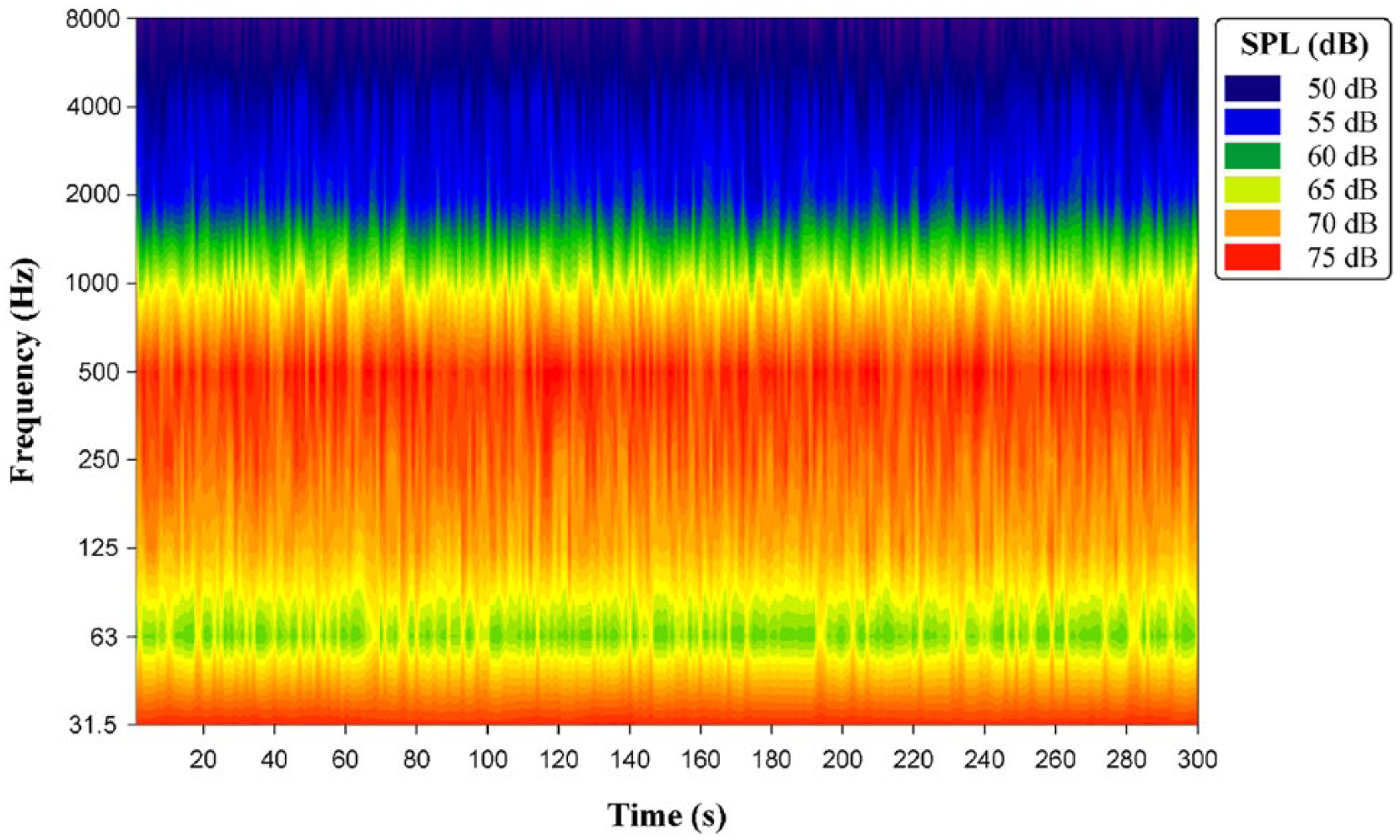

During the working hours (the busiest hours of activity in the bank), we measured the background noise by a calibrated sound level meter (Svantek model 971) for 30 min (Goelzer, Hansen, & Sehrndt, 2010; International Organization for Standardization, 2012, 2017). To increase the accuracy of measurement, we measured the background noise according to the aforementioned method in three different working days and calculated the average values of measured parameters. Furthermore, following the ISO 3747 standard, we measured the noise of every device in the bank during the hours of bank inactivity (in the absence of S&C). It is important to note that all devices in the bank were installed on rubber rings and were very heavy. Therefore, the transmission of sound via structure vibrations was unlikely. A spectrogram of the background noise in the bank is shown in Figure 2, indicating that the sound had a continuous steady state based on ISO 12001 standard (the changes in sound pressure level were less than 5 dB).

A spectrogram of the background noise in the bank. The 31.5 and 500 Hz octave bands exhibit the highest sound pressure levels (SPL).

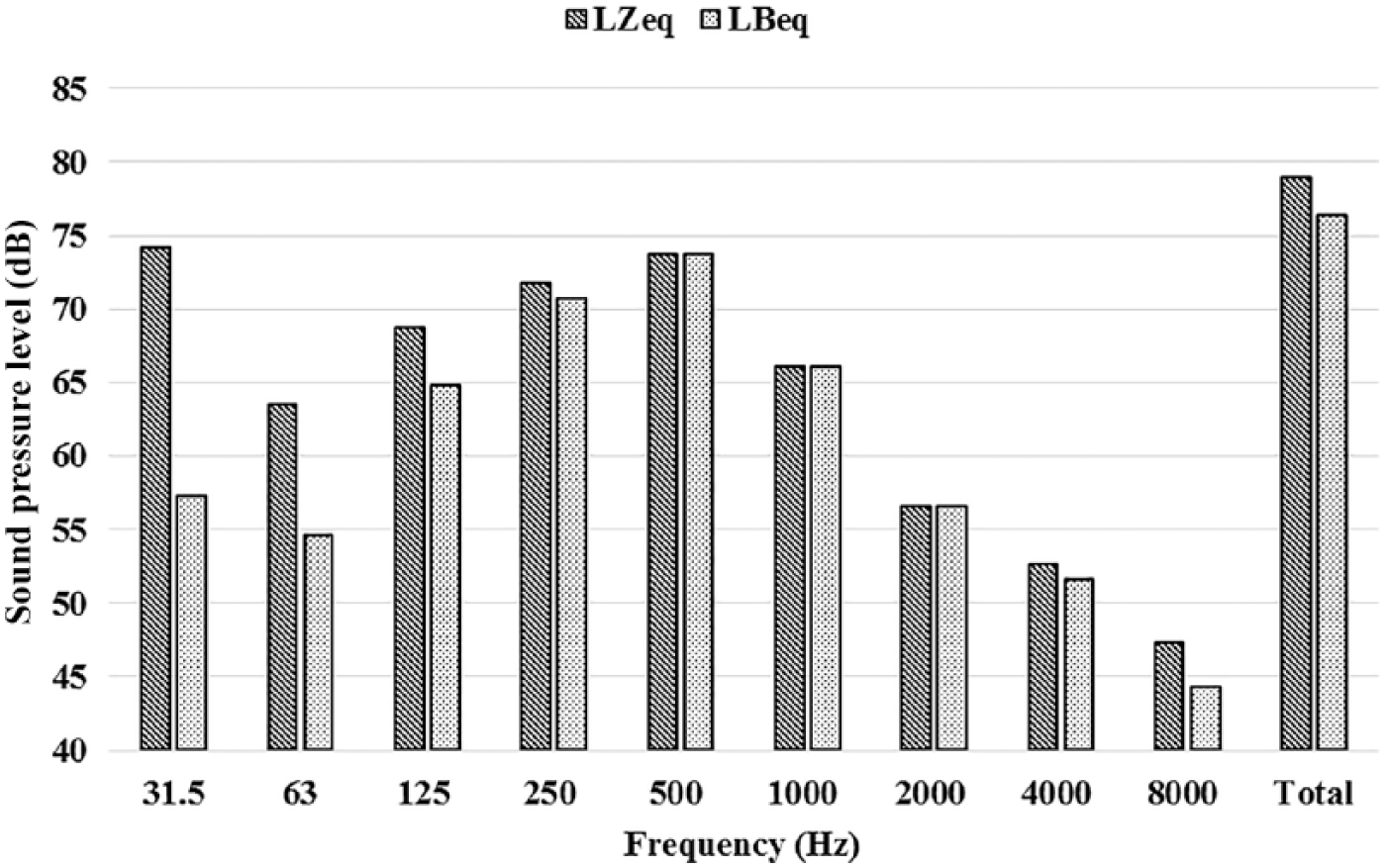

Using the frequency bands analysis, the measured sound pressure level (SPL) was evaluated. Hence, during the measurement of the SPL, we set the sound meter to one-octave band frequency analysis mode. In the one-octave band frequency analysis, the SPL was displayed separately at 31.5, 63, 125, 250, 500, 1,000, 2,000, 4,000, 8,000, and 16,000 Hz center frequencies. In this study, following the ISO3382 standard, we examined the frequency range between 31.5 and 8,000 Hz. Figure 3 presents the results of measuring the background noise in the bank in two states, unweighted equivalent continuous sound level (LZeq), and B-weighted (based on the sensitivity of the human ear to hear the SPL at different frequencies) equivalent continuous sound level (LBeq; International Electrotechnical Commission, 2013).

Frequency analysis of the background noise in the bank in two states. LZeq (unweighted equivalent continuous sound level) and LBeq (B-weighted equivalent continuous sound level).

The background noise in the bank was higher than the recommended value of 55 dB(A) for the office environment (French Standard, 2016). Some acousticians recommend an even lower background noise level of 45 dB(A) (Cowan, 2007). We observed the highest SPL at frequencies of 31.5 and 500 Hz. The high SPL at the frequency of 31.5 Hz was attributed to the noises of automatic teller machines (ATM) and currency-counting machines (CCM). The high SPL at the frequency of 500 Hz was caused by the voice of S&C (the irrelevant speech noise in the bank). The building of the studied bank was constructed on the ground floor, and there was no floor or underground. Therefore, there was no structure-borne sound (the noise of footsteps on a floor that can be heard in a room downstairs). The central layer of the structure of the walls was concrete, and windows were heavy double glass. The bank was located in a quiet area in a region with a mild climate. Thus, it was possible to exclude noises of traffic and air conditioning systems as potential sources of noise. As a result, ATMs, CCMs, and clients were the main sources of noise in the bank.

After identifying the main sources of noise in the bank, to reduce the SPL in the bank, we suggested transferring the ATMs into another room, separated from the main bank office. To minimize the noise produced by the CCMs, it was suggested to build a suitable chamber for CCMs. It was also recommended to implement a proper maintenance system for ATMs and CCMs. In addition, it was also possible to utilize more expensive engineering approaches such as active noise control and sound masking system (Kuo & Morgan, 2008; Torn, 1975). To control the noise produced by the clients in the bank, it was suggested to separate the waiting room for the clients from the main bank office (a completely separate room). Moreover, we suggested installing warning signs such as “Please Be Quiet” and “Mobile Phone Calls Are Forbidden.” In addition, we recommended implementing management measures such as redesign the work processes and minimize the time of the presence of the clients in the bank to prevent overcrowding by clients. Based on the results of Golmohammadi et al.’s (2017) research, 95% of the staff in the banks were suffering from noise, and the main cause of noise in banks was the irrelevant speech of clients.

Step 2: Assessment of Reverberation Time

The reflection of sound on the interior surfaces of the bank is one of the factors that can increase the SPL in the bank. The material used for building bank’s interior surfaces and equipment can have a significant effect on the reflection of noise inside the bank. The ceiling of the bank was covered by perforated plaster acoustic tiles, and the floor was fully covered with marble. The walls were covered with polished marble up to a height of 1 m and with polyvinyl chloride (PVC) panel from a height of 1 m to 3.5 m. The windows were made of glass, protected by steel fences. Closets, partitions, and other equipment were made of a combination of metal and medium-density fiberboard (MDF). The back and front sides of the chairs were made of cotton or woven fabric or artificial foam. The chairs used at the waiting area were made of fully colored metal. The length, width, and height of the studied bank were 13 m, 10 m, and 3.5 m, respectively.

To measure the reflection of noise inside the open-plan offices, an important and useful index called reverberation time (RT) is used. RT refers to the time it takes to reduce the mean energy density of the sound in the environment by 60 dB after the sound source is turned off (International Organization for Standardization, 2008). Following ISO3382-2 standard and using a device manufactured by the BSWA Company, we measured RT in the bank in an unoccupied room (Aliabadi et al., 2014; Golmohammadi et al., 2017; International Organization for Standardization, 2008). Figure 4 shows the results of RT measurement at various frequencies.

Reverberation time (RT) measured in the bank (recommended reference value: VDI 2569: 2016 standard).

As shown in Figure 4, RT at frequencies of 125, 2,000, and 4,000 Hz was higher than that at other frequencies. Considering the results of the previous step, ATMs and CCMs were one of the main sources of noise in the bank, with the high SPL in the low-frequency band. The high RT at a frequency of 125 Hz indicates that some internal surfaces in the bank reflect a higher SPL at a frequency of 125 Hz, which also increase the SPL generated by these devices in the bank environment.

The average noise reduction coefficient (NRC) of material surfaces that exerts a considerable effect on reflection of sound waves in the bank is calculated by measuring NRC of materials at frequencies of 31.5 Hz to 2,000 Hz (frequencies with the high SPL in the bank) (British Standards Institution, 2003). The average NRC of the bank was 0.15. Changing the materials used to make some of the bank’s internal surfaces can be effective in reducing the SPL in the bank. For example, we can replace the marble with PVC to cover the floor. In addition, PVC panels can be used instead of polished marbles (1 m in height) to cover walls, and acoustic panels can be used on the walls. In addition, we can reduce speech transmission from the clients to the staff by hanging an acoustic panel from the ceiling. Interestingly, this intervention will not only reduce RT but also reduce footstep noise (caused by walking clients and staff) and may slightly decrease sound insulation. Doing these changes in a bank’s internal surfaces, it is possible to increase NRC up to 0.37 and consequently decrease RT to less than the recommended value.

Step 3: Assessment of Workstation Partitions

Bank staff need to be focused and have a high level of concentration to perform their tasks effectively. As a result, to prevent distraction and disturbance, the partitions of the workstations should be designed in such a way that staff receive the lowest SPL from the adjacent workstations or at least do not clearly hear the voice of conversations between their colleagues and clients in the adjacent workstation. The partitions installed between S&C, as shown in Figure 5, are made of MDF up of a height of 120 cm to 150 cm and made of glass from a height of 120 cm to 175 cm.

Schematic image of the partition installed at the workstations.

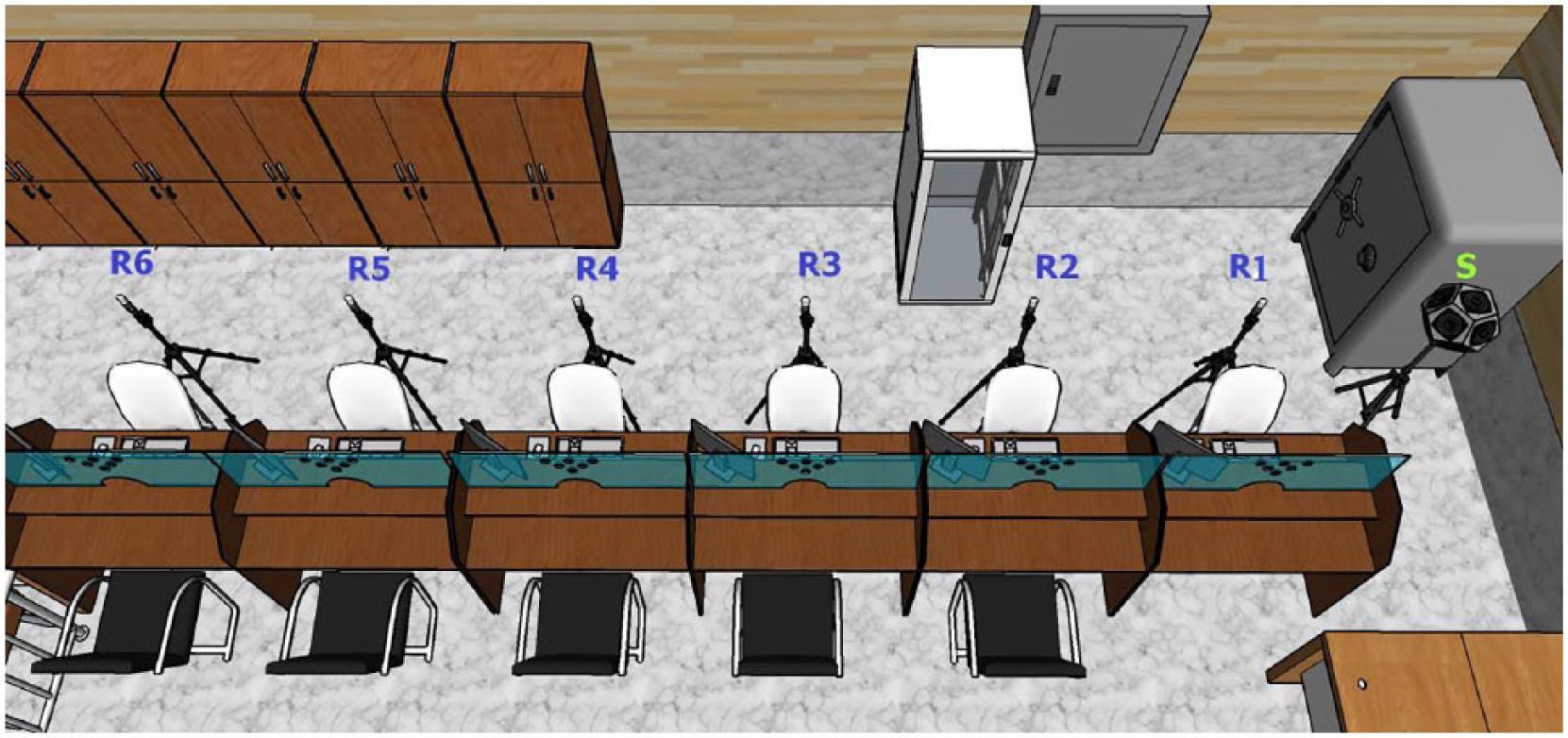

To assess the sound transmitted between the workstations, we used speech transmission index (STI). STI represents the quality of speech transmission between the speaker and listener. The value of this index is between 0 and 1, respectively, indicating the worst and best quality of speech transmission between the speaker and listener. Following ISO3382-3 standard and as shown in Figure 6, we used an omnidirectional source of sound (model QS002) and placed a microphone 1.2” (model MPA231) in each of the workstations.

Measurement points (S = source; R1–R6 = receivers) for acoustic parameters (STI = speech transmission index) on the basis of the ISO3382-3 criteria.

Finally, we calculated STI at each workstation using IEC 60268-16: 2011 standard. Taking into account the values of STI calculated at each workstation and the distance of microphones from the source of sound at each station, we plotted a diagram shown in Figure 7 and obtained the regression line. Following ISO3382-3 standard, to prevent distraction, the appropriate distance between workstations provides a STI less than 0.5. As shown in the regression line presented in Figure 7, the appropriate distance between workstations to prevent distractions (distractions distance: rD) in the bank must be at least 2.81 m. Unfortunately, the distance between the workstations was 1.30 m, and based on the items stated, staff were distracted by the noise of the adjacent workstations. Jahncke, Hongisto, and Virjonen (2013) conducted a study on cognitive performance during irrelevant speech conditions in open-plan offices and concluded that the cognitive performance of the studied staff was increased with reducing the level of clarity of the background speech in office environments.

Diagram for determining the appropriate distance between workstations to prevent distraction in the staff.

In addition, staff working in the bank must be able to verbally communicate with clients properly to fulfill their requests. To evaluate this, as shown in Figure 8, we placed an omnidirectional speaker and microphone in S&C sites.

Placement of the microphone and omnidirectional speaker to measure speech transmission index between staff and clients (S&C).

We measured all the distances between tables and chairs as well as the sound produced by the speaker using ISO3382-3 standard. Figure 9 presents the results of STI measurement in seven workstations.

Results of the speech transmission index measurement between staff and bank clients at each of the workstations.

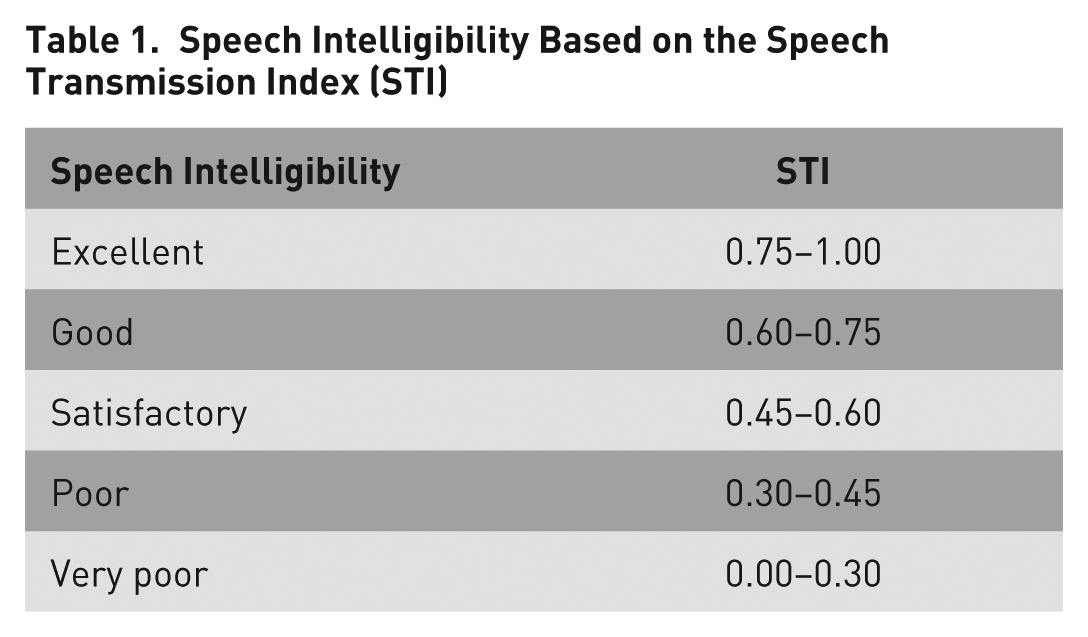

After determining the STI, we used Table 1 to evaluate the intelligibility of speech between S&C.

Speech Intelligibility Based on the Speech Transmission Index (STI)

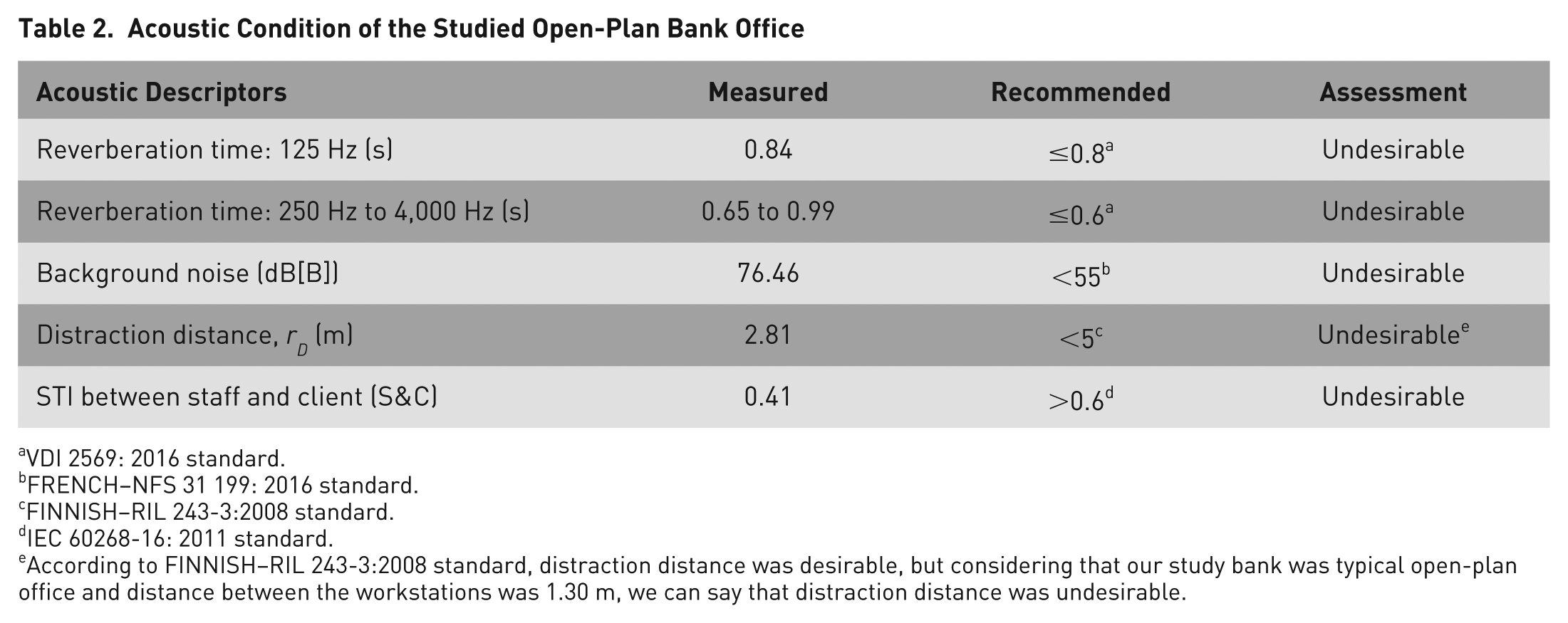

Based on the results presented in Figure 9 and Table 1, we found that the quality of speech transmission between S&C was poor. In such a condition, the staff cannot properly hear the voice of clients; this problem is largely due to the structure and type of partitions designed for the workstations. In addition, due to the inappropriate design of the partitions, the noise transmitted between the workstations was high and led to staff distraction. Passero and Zannin (2012) conducted a study and concluded that the high prevalence of distraction in open-plan offices indicated that the existing partitions were not efficient. In summary, Table 2 presents the acoustic condition of the bank.

Acoustic Condition of the Studied Open-Plan Bank Office

VDI 2569: 2016 standard.

FRENCH–NFS 31 199: 2016 standard.

FINNISH–RIL 243-3:2008 standard.

IEC 60268-16: 2011 standard.

According to FINNISH–RIL 243-3:2008 standard, distraction distance was desirable, but considering that our study bank was typical open-plan office and distance between the workstations was 1.30 m, we can say that distraction distance was undesirable.

Partition Design Approach

There are many banks with a condition similar to that observed in this study. As a result, a suitable design for partitioning workstations can be also used in similar environments to improve the acoustic condition for a large number of staff working in such work environments. Taking into account the results of our study and as shown in Figure 10, our proposed criteria and strategy for the optimal design of the workstations had the following features:

STI between workstations is decreased so that the noise of the adjacent workstations does not disturb staff concentration and focus.

STI between S&C is increased so that staff can have a good verbal communication with clients.

Proposed criteria and strategy for redesigning the workstations of the bank.

To implement an optimal design, we can prepare several designs such as the following: designing partitions for S&C from floor to ceiling through making a booth or cubicle (using absorbent materials), designing and using double-glass structures on partitions that reaches up to the ceiling (International Organization for Standardization, 2004), and designing a suitable hole in the double-glass structure (between S&C) as a path of communication between S&C.

Because of the high level of background noise in the bank, S&C tended to talk louder for communication (Lombard effect). The need to talk louder has a direct relationship with absorption/reflection on the partition surfaces (around the S&C; Nijs, Saher, & den Ouden, 2008). Hence, we can decrease the SPL needed by each person to talk through increasing the absorption of the partition surfaces. Moreover, it can help decrease the background noise of the bank.

Prior to making any change in the bank environment, acoustic simulator software such as ODEON, CATT, RayNoise, Ulysses, Ease, and so on can be used to evaluate new designs through utilizing the strategy shown in Figure 10; it can help to select the best design (Ahnert, 2000; Allen & Berkley, 1979; Atmoko, Tian, & Fazenda, 2007; Dalenbäck, 2011; Meng, De Borger, & Van Overmeire, 1995; Naylor & Rindel, 1992; Rindel, 2000). It is worth noting that most of the aforementioned room acoustic software uses the geometric acoustic simulation method introduced by Allen and Berkley (1979).

Conclusion

We studied the three aspects of the acoustic condition, including the sources of noise inside the bank, material of internal surfaces in the bank (effective in the reflection and intensification of noises), and acoustic condition of the workstations of the staff. This study was conducted to fill the gap observed in our previous study regarding acoustic problems in the bank (Golmohammadi et al., 2017). The results showed that the most important problems in the bank were the inappropriate design of partitions in the workstations, high level of background noise, and high RT. To improve the acoustic conditions of the bank, first, it is recommended to redesign the workstations through adopting a proper strategy and implementing an optimal design to solve the problems. In addition, the materials used for building the internal surfaces in the banks, such as polished stones used in the floor and some parts of the walls and ceilings, must be changed to increase the absorption coefficient of the surfaces and reduce the sound reflection from bank’s interior surfaces. Thereby, we tried to decrease the SPL inside the bank and improve speech conditions. Second, the ATMs must be placed in a separate room, and a suitable chamber must be built for CCMs to prevent the audibility of the noise produced by devices inside the bank. Third, an appropriate maintenance system must be devised to repair and maintain devices under a regular schedule to produce less noise. Fourth, the waiting room for clients must be separated from the main bank office (a completely separate room). In addition, management measures can be adopted to reduce the sound of clients (irrelevant speech noise) in the bank. Finally, considering the current results, it can be concluded that the acoustic conditions of the bank were not desirable, and consequently, the staff did not enjoy a favorable level of acoustic comfort. Acoustic treatment can improve acoustical conditions a lot and improve the working conditions.