Abstract

A growing literature demonstrates that “unearned income”—such as that which stems from natural resources—stabilizes authoritarian regimes. In this paper, we refine this argument to emphasize not just the volume of these rents but also their diversity and the extent to which they can act as substitutes for one another. Specifically, a greater number of distinct sources of rents, and a more equitable distribution among them, provide an important hedge against any sudden change in the ability of autocracies to capture these rents and should lead to more stable regimes. We use a procedure from the literature on market concentration to develop a single measure, termed rent diversification, which captures these characteristics. We then use this new measure in a quantitative analysis examining the likelihood of regime failure. Our findings provide strong evidence that autocracies with more diversified rent portfolios are much less likely to collapse.

Will the recent decline in global oil prices lead to regime collapse in oil-dependent autocracies such as Venezuela, Angola, or Saudi Arabia? Would aid-dependent autocrats like those in Rwanda and Uganda survive a sudden decline in foreign aid receipts? Answering these questions seems straightforward if one considers the large body of existing research on the so-called resource curse. Although the precise causal mechanisms vary, most prior research argues that oil, aid, and other non-tax revenues stabilize autocracies by generating rents that fund elaborate patronage systems and repressive capacities that co-opt citizens and regime insiders alike (e.g., Morrison 2009; Ross 2012; Smith 2004; Wright, Frantz, and Geddes 2015). From this vantage point, unanticipated declines in the volume of rents—whether from volatility in global commodity markets or changes in aid allocations—undermine a crucial tool of autocratic power consolidation and may hasten regime collapse.

This paper offers an alternative answer to such pressing policy questions by advancing a new theory on the political effects of rents. Specifically, we argue that it is not just the total volume of such rents that matters for regime stabilization but also their diversity. In our argument, a greater number of distinct sources of rents, and a more equitable distribution among them, provides autocracies with an important hedge against any sudden change in their ability to capture these rents and should therefore reduce the likelihood of autocratic regime collapse.

Collectively, we refer to these aspects—diversity of sources and the income smoothing made possible by substituting between them—as rent diversification. When autocracies have diversified rent portfolios, unanticipated declines in individual rent sectors need not threaten the regime’s existence, as alternative sources are more readily available. By contrast, regimes whose rent portfolios are concentrated in a single source face increased risk of collapse. We use a technique from the literature on market concentration to develop a new measure that accounts for these characteristics. Results from a quantitative global analysis of authoritarian regimes demonstrate that rent diversification shapes the likelihood of regime collapse as expected, and that the magnitude of this effect vastly exceeds the impact of a regimes’ total rent volume.

Natural Resources, Rents, and Political Regimes

Over the last fifteen years, political scientists have converged on an important set of findings regarding the political effects of natural resource wealth. Although Ross’s (2001) classic “oil impedes democratization” thesis has been questioned (Haber and Menaldo 2011; Liou and Musgrave 2014) and described in more conditional versions (Dunning 2008), there is a relatively high degree of consensus in the literature that oil significantly reduces the likelihood of democratic transition (Andersen and Ross 2014; Ramsay 2011; Ross 2012; Wiens, Poast, and Clark 2014) and stabilizes autocracies (Andersen and Aslaksen 2013; Cuaresma, Oberhofer, and Raschky 2011; Omgba 2009; Smith 2004; Wright, Frantz, and Geddes 2015).

Such pernicious effects are not limited to oil. Ulfelder (2007), for instance, finds that a broad set of natural resources impede democratization. Morrison (2009) demonstrates that an increase in any sort of non-tax revenue stabilizes autocracies by providing additional resources for social spending and patronage projects. Foreign aid has also been shown to impede democracy (Djankov, Montalvo, and Reynal-Querol 2008) and stabilize autocracies (Licht 2010). 1

Despite the varying nature of these studies, most share a common theoretical premise, namely, that what underpins these regime effects is the extent to which these income sources provide rents—that is, “profits above and beyond production costs, where the costs include a normal rate of return on the capital invested” (Ross 2012, 35)—to the state. When these rents accrue to the government, they provide the means by which autocrats’ tighten their grip on power and stabilize their rule. 2 This “rentier” logic is common in the existing literature. Jensen and Wantchekon (2004) argue that, in the context of weak institutions, executive discretion over the distribution of rents facilitates large increases in public spending across African regimes and has aided in autocrats’ consolidation of political power. Alternatively, Bueno de Mesquita and Smith (2010) apply their selectorate model and argue that autocratic regimes that acquire large volumes of aid and natural resource revenues can provide more public goods to citizens, which helps dissipate revolutionary threats from the masses. Ross (2012, 69) also argues that oil wealth allows regimes to provide more benefits than citizens expect given their tax burden, thus placating citizens and avoiding “democratizing rebellions.”

A similar logic suggests that rents also protect rulers from challenges by regime insiders. For instance, Omgba (2009) argues that oil wealth accruing to the state fuels the pervasive clientelism critical to leaders’ tenure. Thies (2010) demonstrates that natural resource wealth also tends to enhance state capacity, and thus reduces the risk of civil war. Most recently, Wright, Frantz, and Geddes (2015) argue that oil wealth deters coups by providing the means for increased military spending.

We argue that, when it comes to autocratic stability, this emphasis on the volume of rents is incomplete. Autocracies can also be stabilized by the presence of distinct sources of rents, and a more equitable distribution among these sources, as this diversification provides an important hedge against un-predictable fluctuations in global commodity markets or aid allocations. We refer to these joint characteristics—that is, diversity of sources and the extent to which multiple sources provide opportunities for regimes to substitute between them as a form of income smoothing—as “rent diversification.” In our theoretical argument, rent diversification stabilizes autocracies, though this effect is subject to diminishing returns. We explore each component in turn. 3

First, a greater number of rent sources helps solve one of the fundamental problems of rentier states, namely, that dependence on revenues subject to global economic forces can lead to economic policy blunders, such as overspending during commodity price booms (Karl 1997; Ross 2012, 6). Although this pattern is perhaps most obvious in the global oil market, similar dynamics underpin almost every commodity market (Deaton 1999). Regimes with multiple sources of rents are thus uniquely positioned to survive any sudden decline in their ability to capture rents from a particular source. If oil prices fall, regimes with diversified rent portfolios can turn to other revenue sectors to help sustain the spending policies that have kept them in power. Put in terms of the arguments that underpin much of the existing literature, multiple sources of rents raise the probability that a regime will still have some source of revenue sufficient to maintain the redistributive and spending policies that co-opt regime insiders and mass citizenries.

A more equitable distribution of these sources further enhances regime stability. When a regime’s rents come from multiple sources that contribute roughly equally in terms of total revenues, regimes are better able to substitute between the various sources. The net result of this process is a form of income smoothing that helps mitigate the potential political consequences of inherently volatile commodity markets or shifting foreign aid allocations. Collectively, the greater the number of sources of rents, and the closer to substitutes these sources are in terms of their relative size, the more likely it is that authoritarian regimes will be able to capture some source of regime-stabilizing revenue.

Our emphasis on regimes’ ability to smooth their income by substituting one rent source for another is rooted in important theoretical models of political economy. For instance, Bueno de Mesquita et al.’s (2003) selectorate model suggests that leaders of small coalition regimes maintain their power through the distribution of private goods to coalition members. In their model, leaders are only replaced when some current member of the incumbent’s winning coalition defects to support a challenger. Defection, however, is unlikely to occur as any defector would lose the private goods he or she is currently consuming. More central to our argument, defection is also risky because challengers cannot credibly commit to maintaining these defectors in their winning coalition should they succeed in replacing the incumbent. As incumbents are better able to credibly commit to the level of private good provisions that keep coalition members satisfied, such regimes tend to have strong “loyalty norms.”

We extend this model to suggest that the promises made by incumbents with access to multiple sources of rents are afforded more credibility. For instance, if coalition members know that leaders are dependent on a single source of rents, incumbents’ future promises regarding the distribution of private goods is wholly dependent on the continued performance of this sole source. Given the inherent volatility in many commodity markets, future revenues of consistent magnitudes are far from certain. By contrast, coalition members are likely to view the commitments of incumbents with access to multiple and equitable sources of rents as more credible, as they estimate a greater probability that the leader will retain enough revenue to provide the private goods necessary for their loyalty, so regimes should be more stable.

To the best of our knowledge, our emphasis on income smoothing via substitution between rent sources is a novel contribution to the growing literature on authoritarian regimes and the resource curse. However, there is at least one prior study that suggests this process is plausible, even though the theoretical argument differs from ours in some critical ways. Specifically, Kono and Montinola (2009) developed a model where autocratic leaders, because of their dependence on smaller winning coalitions, are able to stockpile foreign aid revenues to a greater extent than their democratic counterparts. In the event that negative economic shocks limit the ability of autocrats to distribute private goods to their supporters, they are able to draw on these stockpiled reserves to maintain the level of spending necessary to keep them in power. The net result of this is that aid tends to promote authoritarian survival over the long run. Though Kono and Montinolo emphasize stockpiling, as opposed to substitution, we find their general argument that unearned income is an effective strategy of smoothing income (i.e., the rents they are able to acquire) and smoothing consumption (their spending to maintain loyalty) consistent with our underlying argument.

The final component of our argument is that rent diversification has a non-linear effect on regime collapse. To illustrate this idea theoretically, consider a regime where all unearned revenues originate in a single source, for instance, foreign aid. If this regime suddenly discovered oil, and even if the increase in oil rents was offset by a commensurate reduction in aid allocations such that the total volume of rents in the regime remained constant, our argument suggests that the likelihood of regime collapse would diminish. This hypothetical regime now has an alternative—and in this example perfectly equitable—source of rents. Gaining some ability to substitute when such an option was previously impossible ought to reduce the likelihood of collapse.

By contrast, if a regime that currently relies on a number of distinct and relatively equitable sources of rents gains one more source, the impact on regime collapse should be smaller. The baseline level of diversification in such regimes has already provided an important layer of protection from collapse, and the addition of one more source is unlikely to matter to the same extent. Moreover, excessive diversification entails greater coordination efforts on the part of the regime to extract and capture these revenues. This too suggests that the overall impact of rent diversification will attenuate at higher levels.

In summary, our argument suggests that it is not just the volume of rents that exerts strong regime effects but rather the extent to which leaders can draw from diverse and relatively substitutable source of rents to consolidate their power. Moreover, the predicted impact on autocratic regime stability should be concentrated at the low end of the scale, where regimes gain some ability to substitute between these sources. Few scholars have articulated this specific view on the role of rent diversification. The closest we have found is Smart (2009), who shows that a measure based on the diversification of natural resource exports is associated with higher levels of democracy. However, he is principally interested in the effects of institutions on economic development and thus does not anchor the study in the same theoretical perspectives. We test our specific argument below.

Measuring Rent Diversification

Prior studies tend to measure the rents that accrue from natural resources, and oil specifically, as the total value of these rents either as a share of gross domestic product (GDP) or in per-capita terms. Such measurement approaches are ill suited to capture the multi-dimensional nature of our theoretical argument. In general terms, our argument suggests that gaining some ability to substitute between distinct sources of rents should help prevent the collapse of an autocratic regime. This effect should be independent of a regimes’ total dependence on rents. We therefore create a new variable, which we term rent diversification, which captures the number of distinct sources of rents and the potential substitutability between them in a single measure.

The construction of this variable draws on a frequently used index of market share, the Herfindahl–Hirschman Index (HHI) of concentration. In the traditional application, an HHI measures the market share of firms in a particular industry, often in support of anti-trust claims. By considering the share of a total market that an individual firm controls—General Motors’ share of all cars sold in the United States, for instance—and then summing across all firms in the market, these indices provide a summary statistic that measures the extent of market concentration. Calculated HHI values range from 0 to 1, with higher values indicating greater concentration in a particular market. The standard formula for calculating such an index appears below, where si is the share of firm i in the market, and N is the number of firms. The index is thus the summation of the squared values of market share for all firms in the designated market:

This procedure underlies several common variables in existing political science research. For instance, measures of ethnic or religious fractionalization, including those described by Easterly and Levine (1997) and Alesina et al. (2003), use the HHI procedure. Higher values of these measures imply that a single ethnic or religious group has greater “market share,” or more generally, accounts for a larger proportion of the total population. This calculation has also been used in measures of multipartism used in the study of electoral systems. For instance, Rae (1968) describes a measure of seat share fractionalization, constructed as 1 minus an HHI of the proportion of seats in a legislature occupied by members of the same party (i.e., summing the squared values of each party’s proportion of seats). 4 Across both applications, HHI-based measures provide an intuitive sense of the degree of concentration in a particular market.

We adopt this procedure for our purposes by asking how concentrated is the market of rents in a dictatorship. At an abstract level, we conceptualize dictators as presiding over economies consisting of two elements. First, there is the share of total economic output that is attributed to the kinds of rent-generating sectors highlighted in the existing literature. Second, there is the share of total economic output that comes from non-rent sectors. Given the nature of our argument, we focus on the degree of concentration in the former. When the market of rents is more concentrated, regimes will be less able to substitute one source for another and should therefore be more prone to collapse. Conversely, when the market of rents is more diversified, regimes should be less likely to collapse.

We calculate our specific measure as follows. First, we use World Bank data to measure the rents generated from the following five natural resource: coal, forest, mineral, natural gas, and oil. This collection of natural resource sectors is consistent with the existing literature’s identification of sectors that can generate rents. 5 For each sector, we measure total rents generated (i.e., the total value of production at world prices minus the costs of production) as a share of a country’s total GDP. We add to these a sixth measure, namely, recorded disbursements of official development assistance (ODA), also measured as a percentage of GDP. Specifically, we use data described by Tierney et al. (2011), from a database known as AidData, to capture a broad set of bilateral and multilateral aid disbursements. We calculate the total yearly value of aid disbursements in constant U.S. dollars, and then adjust these values to represent a share of GDP, which standardizes this measure to the World Bank’s reporting of rents from natural resources. 6

Next, we sum these six components to provide a measure of a regimes’ total rent dependence, a variable we label total rents (% GDP). Then we divide each rent sector variable by this measure of total rent dependence, so that the variables become measures of individual rent-generating sectors as a share of total rent dependence, instead of shares of total GDP. This step is necessary from a theoretical perspective. For instance, suppose a country relied on oil rents for 10 percent of their GDP. What is important for our argument is the extent to which this individual component—oil—accounts for the share of total rent dependence. Dividing 10 percent by the measure of total rent dependence transforms the variable into a measure of the importance of the oil sector relative to other rent-generating sectors. If a country has a total rent dependence of 15 percent of GDP, the relative importance of oil will be higher than if a country has a total rent-dependence level of 30 percent of GDP; in the former hypothetical instance, oil accounts for two-thirds of the total “market” of rents, while in the latter, it only accounts for one-third. We repeat this process for each of the six components. 7

Once we have re-scaled the individual components in this way, we follow the convention in constructing such indices and sum the squared values of these six components. This process generates a measure that can range from 0 to 1 and captures the extent to which regimes can draw on diversified sources of rents to consolidate their power. 8 To be consistent with the directional nature of our theoretical argument, we subtract this HHI from 1 so that rather than measure concentration, the variable becomes an index of diversification. Higher values of rent diversification indicate that the market for rents is more diversified and, according to our argument, that regimes are better able to substitute between multiple sources and thus should be less prone to collapse.

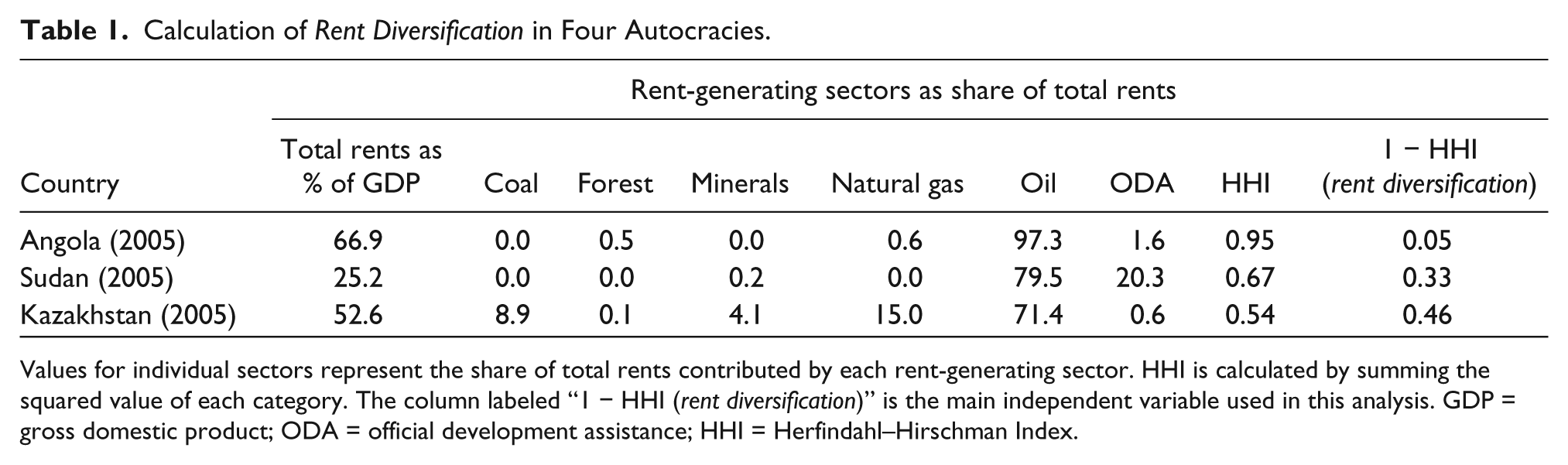

Some examples of this process are instructive. Table 1 reports information for three autocracies drawn from our sample: Kazakhstan, Sudan, and Angola. The first column reports each regime’s total dependence on rents, as a percentage of GDP, for the year 2005. Each country is relatively dependent on rents; even Sudan’s value of over 25 percent of GDP, the lowest of the three example regimes, is well above the mean value for all countries we include in our sample. Our argument, however, suggests that the degree to which this rent dependence is diversified into multiple and substitutable sectors should also affect regime stability. When considered from this angle, these three highly rent-dependent regimes display considerable heterogeneity. In Angola, oil rents alone account for over 97 percent of all rent sources. Other components make minimal contributions to the total rent volume, such that our calculated HHI is quite high at 0.95, and our preferred variable of 1 minus this index (i.e., rent diversification) is very low at 0.05.

Calculation of Rent Diversification in Four Autocracies.

Values for individual sectors represent the share of total rents contributed by each rent-generating sector. HHI is calculated by summing the squared value of each category. The column labeled “1 − HHI (rent diversification)” is the main independent variable used in this analysis. GDP = gross domestic product; ODA = official development assistance; HHI = Herfindahl–Hirschman Index.

By contrast, Kazakhstan, which has a similarly high overall level of rent dependence, has a far greater amount of diversification. Oil rents account for over 71 percent of total rents, yet the regime has other sectors that contribute to the total volume. When we calculate our specific variable of interest, Kazakhstan displays a much higher level of rent diversification than does Angola, with Sudan falling in the midpoint. In Figure 1, we report simple pie charts that visualize the extent of concentration or diversification in these regimes’ market of rents.

Concentration in the market of rents.

These simple examples also illustrate an important point for assessing our argument, namely, that our measure of rent diversification is distinct from a regimes’ total rent dependence. Countries with high overall levels of rent dependence can have either high or low levels of rent diversification, as the Angola and Kazakhstan examples illustrate. Similarly, countries with low levels of total rent dependence also vary in terms of how diversified this portion of the economy appears. Separating out the effects of total rent dependence from our emphasis on diversification is essential to testing our argument.

Before moving on, we address two potential criticisms of this measure in terms of whether or not it captures the underlying theoretical argument we have posited. 9 First, we have followed the convention in the existing literature and based our variable on data that measure potential government rents, despite the fact that a number of factors may preclude governments from directly capturing any (or all) of these rents. Although it is unlikely that private entities capture ODA disbursements, there is nothing inherent in the reporting of the value of natural resource rents, for instance, that implies that governments are the main beneficiaries. In terms of oil, Jones Luong and Weinthal (2006) have argued that private ownership not only prevents governments from capturing these lucrative rents directly but may even prevent the realization of the “curse” of oil abundance generally.

We have adopted this measurement approach quite simply because the kinds of systematic data that would distinguish all potential rents from those rents directly captured by governments do not exist. More generally, we lack reliable data on government revenue, much less fine-grained data that would allow researchers to measure the extent to which revenue derives from specific rent sectors. Both types of data collection efforts might allow us to construct measures more directly tied to our argument, yet we are forced to leave this important issue for future research. How consequential is this decision?

Theoretically, we believe this decision has little influence on the conclusions we draw. Certainly the vast majority of prior research in this area has argued that governments are uniquely able to capture the rents that accrue from natural resources. Moreover, it would be difficult to make sense of the oft-observed tendency for resource-abundant regimes to be more stable (e.g., Smith 2004; Wright, Frantz, and Geddes 2015) if government capture of potential rents was the exception rather than the rule. The evidence from empirical tests of this tendency also supports our measurement strategy. Thies (2010), for instance, uses a simultaneous equations approach to model the relationship between primary commodities, state capacity, and civil wars. His results suggest that primary commodities tend to enhance state capacity, as opposed to undermining state strength. Although his ultimate focus is on how these factors shape civil war, the results are consistent with our assumption that governments tend to appropriate the resource rents available in their economies.

In Section 3 of our online appendix (see http://prq.sagepub.com/supplemental/), we provide our own empirical evidence consistent with this assumption, including demonstrating that greater levels of total rents in an economy are associated with greater reliance on both non-tax revenue and state-owned enterprise revenue, and are associated with a greater likelihood of creating a national oil company (NOC), which we take as a proxy for the kinds of institutions regimes create to capture potential rents.10 Although future research should prioritize more fine-grained measures of government reliance on rents, we believe our current approach is acceptable and does not bias in favor of our argument.

Second, our measure is premised on the assumption that the various rent-generating sectors respond to different stimuli, or at the very least, the prices of these sectors do not move together. If, for instance, all natural resource sectors responded similarly to external price shocks, then the existence of multiple sources of rents would be ineffective in facilitating the kind of substitution our theory emphasizes.

Although plenty of post-war development theory emphasized the potential for widespread commodity price shocks to destabilize export earnings, whether this renders our measure ineffective is ultimately an empirical question. A close look at the data underlying our measure of rent diversification suggests that this is not the case. Across our estimation sample of authoritarian regimes (described below), the average within-regime correlation between the various rent-generating sources is relatively low. For instance, the average correlation between oil rents and natural gas rents is −0.21, quite low considering that both represent important fuel sources that, at least from a theoretical perspective, respond to similar market conditions. The average correlation between oil rents and foreign aid is also negative and relatively small, at −0.25. If one calculates the average within-country correlation between the sum of all natural resource rents and rents from foreign aid, the correlation is −0.68, a higher correlation in absolute terms, but a negative one, suggesting that aid rents increase as natural resource rents decline, and vice versa. Although these exercises are not definitive proof of regimes’ substitution between rent sources, we believe they suggest that one potential objection to the variable has little empirical support.

The best evidence of our causal mechanism at work would come in the form of detailed data on the origins of government spending over time, which might enable us to observe how governments make up any revenue shortfalls resulting from a decline in one rent sector by substituting the revenues from another sector. Such detailed data are, unfortunately, not available. However, as a second-best approach, we can examine the overall level of government spending. If our argument is correct, regimes with greater levels of rent diversification ought to display less variability in government spending; the greater number of sources of rents and the more equitable distribution among them should minimize the year on year fluctuations in spending.

To test this argument, we collect World Bank data on general government spending as a percentage of GDP, and calculated the standard deviation of this measure across each regime included in our estimation sample. Regimes that have greater fluctuations in annual government spending will, predictably, have higher standard deviations. If our argument is correct, we would expect regimes with higher levels of rent diversification to be associated with smaller standard deviations of government spending (i.e., smaller fluctuations in government spending). Simple empirical analyses support this argument. For instance, regimes with low levels of rent diversification (defined here as below the mean for this variable) have an average standard deviation of government spending of 3.6. By contrast, regimes with greater levels of rent diversification (above the sample mean) have an average standard deviation of government spending of 2.7. These findings are consistent with our argument that diversification provides regimes with a way to smooth their income by substituting between distinct sources of rents.

Space constraints prohibit further modeling of regimes’ substitution between different commodities, while issues of data availability render it difficult to provide empirical evidence of the actual substitution process in government spending. Nevertheless, these exercises demonstrate that our measure is immune from several plausible theoretical objections.

Empirical Analysis

We test our argument that rent diversification reduces the likelihood of autocratic collapse with a statistical model using a global sample. We use Geddes, Wright, and Frantz’s (GWF; 2014) newly collected data to define the sample of autocracies as all country-years in which executives achieved or maintained power through means other than “direct, reasonably fair, competitive elections” (Geddes, Wright, and Frantz 2014, 317). We include all sub-types of autocratic systems in our sample. Importantly, the GWF data enable us to separate out distinct authoritarian regimes that govern a country, even if there were no democratic interludes during the observed time span. Our dependent variable autocratic regime failure is created using these authors’ binary variable, which denotes any year in which an autocratic regime fails as a “1,” while all other years are coded a “0.”

In terms of the theoretical discussion above, we expect that greater rent diversification should reduce the likelihood that autocratic regimes fail, but that the effect will become smaller as the level of rent diversification increases. To capture this non-linear effect, we include both rent diversification and the squared term, rent diversification 2 . We also include the measure of total rents (% GDP) to capture the general impact of rents on autocratic stability. As noted above, including this variable is necessary so that we can be confident any effect of rent diversification on regime collapse is not simply reflecting the well-known effect of total rent levels.

Empirical analyses based on observational data like these face a number of challenges to causal inference, with endogeneity often at the top of the list. In this instance, we find it unlikely that autocratic regimes facing imminent threats to their survival can easily adjust the size and diversity of their rent sectors—especially as the extraction of some of these rents requires time-intensive procedures and investments, or in the case of ODA, is appropriated annually through bureaucratic processes. More generally, our statistical models include a number of control variables corresponding to factors that render regimes more unstable and might plausibly affect the extent to which regimes rely on diverse sets of resource revenues.

Our model includes two measures of economic performance, log GDP per capita and economic growth (lagged one year), from the Penn World Tables and World Development Indicators, respectively. The overall level of development, measured by log GDP per capita, should have an impact on the extent to which a country relies on natural resource revenues, while higher levels of economic growth should reduce the likelihood of regime failure generally. We control for the extent to which the autocratic regime faces domestic threats by including a dummy variable measuring whether there was a coup attempt in the prior year, using data from Powell and Thyne (2011). We also include a dummy variable for autocratic regimes that are party based, drawing on a growing literature that shows how the institutionalization of authoritarian politics through party systems stabilizes regimes (Boix and Svolik 2013; Magaloni 2008). We use the Geddes, Wright, and Frantz (2014) data to create this variable.

We evaluate the robustness of our main results by including three additional control variables. First, we include a measure of repression, as regimes willing to use repression may be better able to avoid domestic threats to their power. Moreover, scholars have long postulated that resource wealth may facilitate the development of greater and more effective tools of repression (e.g., Ross 2001). We measure a state’s use of repression with the composite variable physical integrity, which is drawn from Cingranelli, Richards, and Clay (2013). We also include a measure of population size and religious fractionalization, using data from Alesina et al. (2003).

Given the nature of our dependent variable, we estimate probit regressions. We deal with the temporal dependence in these data by including polynomial transformations of the duration in years of individual authoritarian regimes (labeled time), up to the year of failure. Specifically, our models include the variables time, time 2 , and time 3 . Carter and Signorino (2010) show that such an approach is a simpler and more interpretable approach than prior methods of modeling time dependence, and the inclusion of time polynomials has become a standard method of analysis in studies of autocratic regime duration (e.g., Wright and Escribà-Folch 2012). Given the nature of our dependent variable and the structure of our analysis, we report standard errors clustered on individual autocratic regimes.

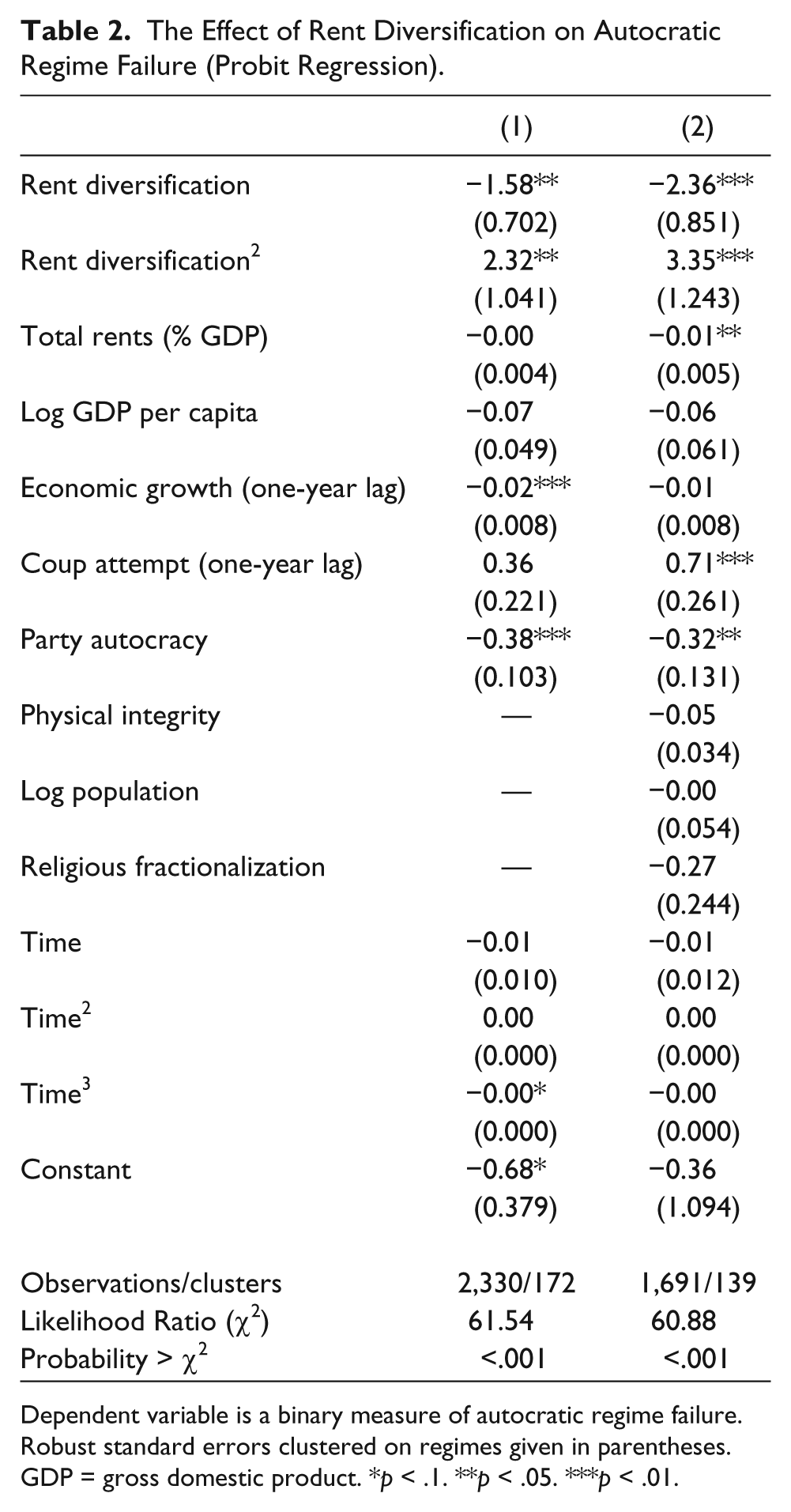

Table 2 presents our main results. In Model 1, the coefficients for rent diversification and the squared term are both in the expected direction and statistically significant. Increases in rent diversification are associated with a reduction in the likelihood of autocratic collapse, though the magnitude and importance of the effect changes as the overall level of rent diversification increases. Growing economies also reduce the risk of failure, while those regimes that are institutionalized through party structures are also significantly less likely to fail, a finding consistent with the growing literature on authoritarian politics.

The Effect of Rent Diversification on Autocratic Regime Failure (Probit Regression).

Dependent variable is a binary measure of autocratic regime failure. Robust standard errors clustered on regimes given in parentheses. GDP = gross domestic product. *p < .1. **p < .05. ***p < .01.

These same patterns of statistical significance remain in Model 2, which includes the three additional variables physical integrity, population, and religious fractionalization. This model suggests that past political instability, as measured by prior coup attempts, also hastens the collapse of autocratic regimes. Most importantly, however, the core results on the non-linear impact of rent diversification remain consistent. It is important to note that this effect exists even when controlling for the overall impact of total rents, which also has a negative and statistically significant coefficient in the model.

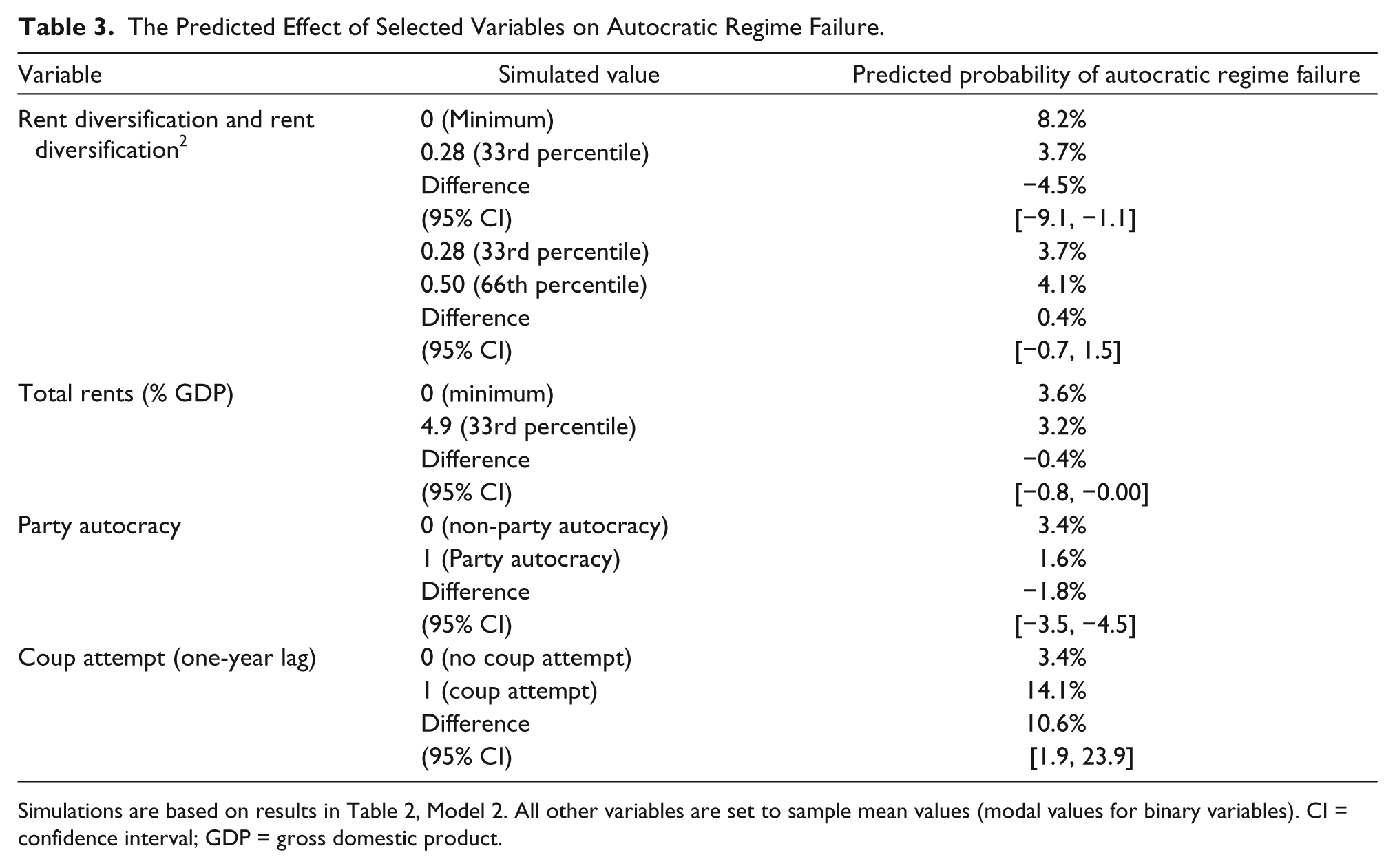

To better understand the substantive impact of these findings, we use the regression results in Model 2 to perform a series of simulations (King, Tomz, and Wittenberg 2000). Specifically, we estimate predicted probabilities of autocratic regime failure at varying levels of our key independent variables rent diversification and the squared term, while holding all other variables in the model at their sample mean or, for binary variables, their modal values. The results of these simulations are presented in Table 3.

The Predicted Effect of Selected Variables on Autocratic Regime Failure.

Simulations are based on results in Table 2, Model 2. All other variables are set to sample mean values (modal values for binary variables). CI = confidence interval; GDP = gross domestic product.

The top panel of Table 3 presents these simulation results for our key independent variable. When we set the value of rent diversification and the squared term equal to the minimum value of 0 (meaning that a country has no rents), the predicted probability of autocratic regime failure is 8.2 percent. If the values of rent diversification increases to a level equal to the thirty-third percentile, however, the predicted probability of autocratic regime failure is only 3.7 percent or a difference of −4.5 percent and a reduction in the relative risk level of almost 55 percent. As these simulation results are averages, this change in predicted probability has a confidence interval, which we report in the table. Note that for these simulated levels of rent diversification, this change is statistically significant with a confidence interval that does not include zero.

Consistent with the non-linear effect we described above, however, the effect of rent diversification changes as the overall levels of this variable increase. For instance, Table 3 also reports the results of analogous simulations, only this time increasing the value of rent diversification and the squared term from levels equal to the thirty-third percentile to the sixty-sixth percentile. The estimated change in the predicted probability of regime collapse from this scenario is not statistically significant. In other words, the protective influence of rent diversification is concentrated at lower levels of the measure, when regimes gain some ability to engage in the substitution process we have described in our theory.

Autocratic regime failures are relatively rare events, so the baseline probability of regime failure will almost always be relatively low. Nevertheless, it is instructive to compare the substantive impact of rent diversification with other variables included in the model. To do this, we perform analogous simulations with three other theoretically and empirically relevant variables, total rents (% of GDP), party autocracy, and the one-year lag measure of coup attempt. The results of these simulations are reported in the remaining panels of Table 3. Regimes with greater total volume of rents are less likely to collapse, and though the effect is statistically significant, the overall impact is relatively small in magnitude; an increase from the minimum to a value approximating the thirty-third percentile of the distribution reduces the probability of collapse by less than half a percent.

All else equal, the predicted probability of regime failure in party autocracies is roughly half the risk in these other less institutionalized categories (1.6% vs. roughly 3.4%). The substantive impact of prior coup attempts is also large; regimes with a past coup attempt have a predicted probability of collapse of 14.1 percent, versus 3.4 percent for those without such past instability. These simulations aid in interpreting key variables in the model, but for our purposes, the comparisons to the predicted probabilities reported in the top panel are most important. Taken collectively, these results suggest that difference in the level of rent diversification are more consequential to the stability of autocratic regimes than is the creation of institutionalized party systems, and about half as large as the impact of a coup attempt in the prior year.

Table 4 reports the results of several additional analyses that provide important evidence of the robustness of our central findings. Using Model 2 from Table 2 as the baseline, each of the six regressions estimated in Table 4 rely on alternative specifications or measurement strategies. Column 1 excludes all observations in which autocracies are completely devoid of rents, and therefore rent diversification is 0. If such autocracies have different surival rates than those with some rent sources, our findings above may simply reflect this underlying difference. Excluding such observations controls for this potential impact. Column 2 reports the results from re-estimating the main model while altering our calculation of rent diversification. Specifically, Column 2 reports the results from combining oil and natural gas into one category of “fuel” rents before creating the index of concentration. If prices of both sources of fuels move in tandem, autocracies will be unable to smooth their incomes by substituting between these two sources. The results, however, are substantively the same across these alternative measurement strategies. Column 3 includes a dummy variable for oil states, using Ross’s (2012) criteria as those whose per-capita oil income exceeds $100. Column 4 also includes this dummy variable for oil states, though this time excludes the more general measure of total rents. Together these models provide some confidence that our results are not simply a reflection of the well-known impact of oil on autocratic stability.

Robustness Analyses (Probit Regression).

Dependent variable is binary measure of autocratic regime failure. Probit regression with standard errors clustered on regimes in parentheses. See text for full variable description. Model descriptions are as follows: Model 1 excludes observations where rent diversification = 0. Model 2 calculates rent diversification with oil and natural gas values combined as a single “fuel” rent category. Model 3 includes a dummy variable for oil states using the Ross (2012) measure. Model 4 is same as Model 3 but excludes the measure of total rents (% GDP). Models 5 and 6 exclude ODA from the calculation of rent diversification and total rents (% GDP). GDP = gross domestic product; ODA = official development assistance.

p < .1. **p < .05. ***p < .01.

We also examine whether our results are robust to excluding ODA from our index of rent diversification and measure of total rents (% GDP). As noted previously, Bermeo (forthcoming) has demonstrated that foreign aid is not always as fungible as other rents and may therefore have different effects on democratic transitions depending on the strategic logic of donors. Bermeo is particularly interested in the effect of aid on democratic transitions, a different dependent variable than we are investigating. Nevertheless, we re-estimate our regression models while excluding ODA from the calculation of both of these variables and report these results in Columns 5 and 6. Our key findings remain significant, suggesting that our results are not dependent on the unique properties of foreign aid.

Finally, Section 2 of our online appendix replicates the main analyses while using an alternative approach to missing data in the calculation of rent diversification. As described therein, this process results in a much smaller sample, yet our main results are still validated.

Conclusion

The resource curse literature has been greatly enhanced by the growing recognition that it is not oil per se, but rather the underlying rentier nature of oil revenues, that shapes regime dynamics. This change has led to a growing number of studies that demonstrate how other sources of rents provide important tools for regimes’ consolidation. Nevertheless, existing studies tend to look at these sources in isolation from one another. A logical extension of these arguments suggests that a greater variety of sources of rents should also facilitate the stabilization of autocracies. Given the potential to substitute between these rents, those autocracies best able to diversify their rent portfolios have a hedge against the fluctuations inherent in volatile commodity markets. We have tested this argument by creating a novel measure of rent diversification, based on a technique to measure market concentration, and assessing the measures’ impact on the likelihood of autocratic regime collapse. The evidence is consistent with our argument; diverse sources ensure these autocracies possess some source of rents necessary to maintain the policies and behaviors that help cement their hold on political power.

These findings also have sobering policy implications. While a simple reading of the prior resource curse literature might view the recent decline in the global oil prices as precipitating a collapse of oil-dependent autocracies, our findings suggest that such optimism should be tempered considerably. Even among rent-dependent autocracies, there is considerable variation in the degree to which this dependence is diversified, and our results have shown that this diversification leads to stabilizing factors that are sufficient to counterbalance any revenue losses from a particular sector. More generally, new technologies continue to aid in the discovery, exploitation, and production of oil and natural gas, particularly in the developing nations of sub-Saharan Africa (Mann 2013; Ross 2012), which suggests that autocracies will find themselves increasingly able to diversify their sources of rents and, as a result, strengthen their hold on political power.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.