Abstract

This paper investigates the domestic political factors that shape the participation of autocratic regimes in bilateral investment treaties (BITs). We argue that autocratic time horizon positively affects governments’ motive to sign BITs by influencing the costs of complying with investor protection standards included in the treaties. These treaty provisions severely constrain discretionary policy maneuvers that are critical to autocratic survival. Autocratic regimes expecting to rule for a considerable time period are willing to relinquish some discretionary policy space in the interest of enhancing the credibility of their investor protection commitment—and hence promoting investment inflows. However, autocratic governments with short time horizons rely heavily on discretionary policy maneuvers to stabilize their grip on power and are likely to infringe on investors’ interests to extract resources to ensure their political survival, making the costs of compliance with BITs too high to bear. Using a country-dyad data set of BIT signatures from 1971 to 2009, we find strong support for our argument.

Introduction

Bilateral investment treaties (BITs) are generally considered useful tools for promoting foreign direct investment (FDI) to developing countries. A conventional view on the origins of these investment treaties posits that developing countries with weak institutions sign BITs to strengthen commitments on property rights and investor protection (Ginsburg 2005; Kerner 2009). Previous studies have maintained that BITs, which feature a legalistic process for dispute settlement that increases the cost of infringing on investors’ rights, could prevent governments with weak domestic legal and political constraints from extorting from foreign investors (Arias, Hollyer, and Rosendorff 2018; Guzman 1997; Rosendorff and Shin 2015; Salacuse and Sullivan 2005). If this is the case, then BITs should be regarded as particularly valuable for investment promotion by autocratic regimes that find it hard to make credible commitments to investors (Busse and Hefeker 2007; Jensen 2008; Li 2009). As Rosendorff and Shin (2015, 113) noted, “Autocratic states have much to gain from FDI, but their promises . . . are not credible. A BIT offers more credibility to the promise, and hence it is the more autocratic states that sign more BITs.”

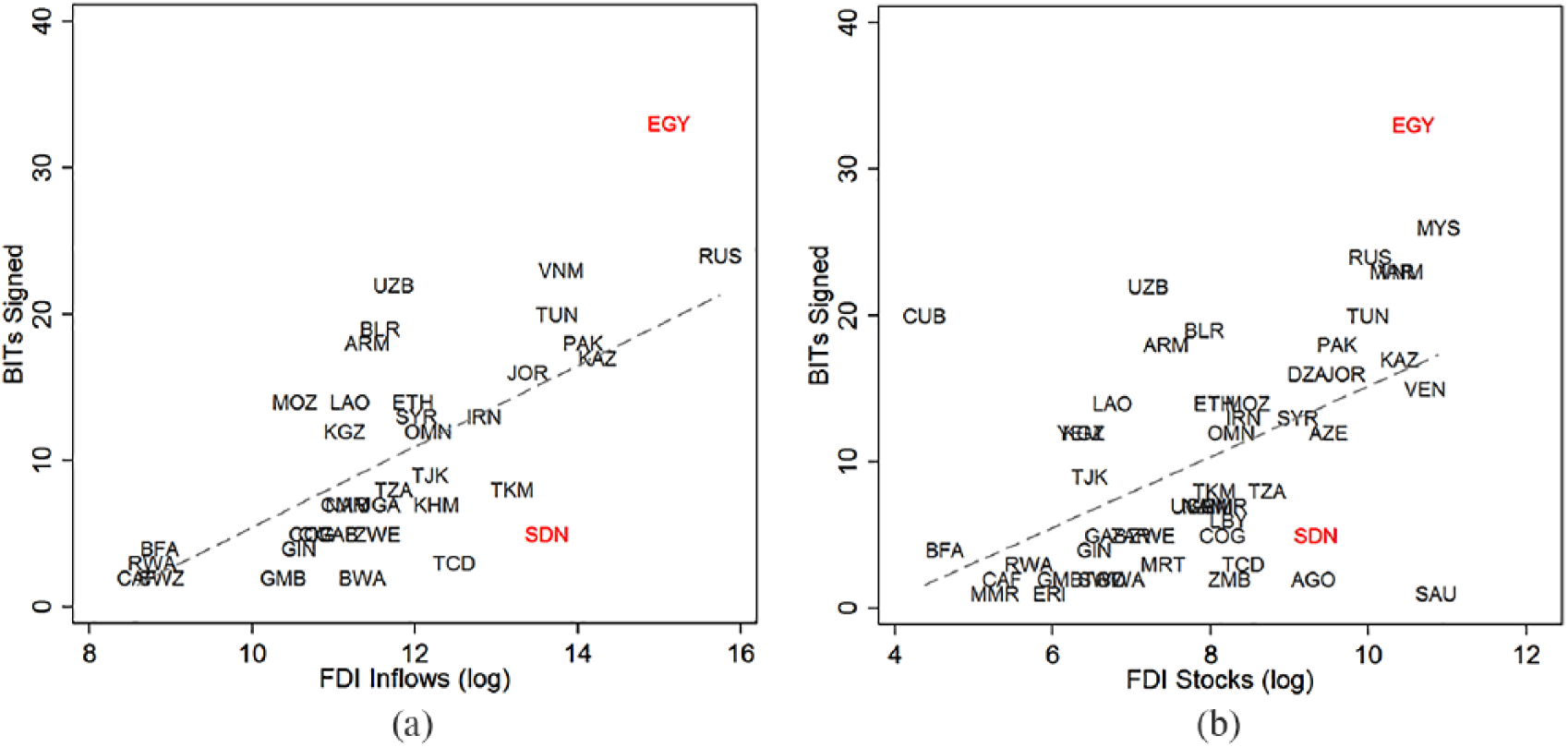

The pattern of BIT signing among autocratic regimes, however, is more divergent than expected. Even after accounting for their different investment positions, some autocratic governments are more enthusiastic about BITs than their peers. Using data from 2008, Figure 1 plots the number of signed BITs against the levels of (1) FDI inflows and (2) FDI stocks among 93 autocratic regimes as defined in Geddes, Wright, and Frantz (2014). Although signing BITs is positively associated with FDI inflows and stocks overall, much of its variation among autocratic regimes remains insufficiently understood. Contrasting Egypt and Sudan highlighted in Figure 1, the two neighboring African autocracies are in similar investment positions in terms of inflows and stocks, while the former signed many more BITs with capital exporters in the Global North (33) than the latter (5). Also, raw statistics do not seem to show that autocratic regimes favor BITs more. On average, countries that are ruled by autocratic regimes had signed slightly fewer BITs (9.8 per country) than their non-Organisation for Economic Co-operation and Development (OECD) democratic counterparts (10 per country) as of 2010, despite a handful of hyperactive autocratic BITs participants such as China and Egypt.

Investment positions and BITs among autocracies in 2008.

In this paper, we seek to provide a political account of the divergent BIT signing behavior of autocratic regimes, which has been overlooked in the literature. Consistent with previous studies such as Ginsburg (2005) and Cho, Kim, and Lee (2015), we believe the commitment benefit is the key motivation for autocratic regimes to sign BITs: they supply external hand-tying devices to remedy the time-inconsistency problem in the autocratic political context. But we argue that not all autocratic regimes are equally capable of harvesting such a commitment benefit from signing BITs. For BITs to be beneficial to sign, they need to impose incentive-compatible constraints on autocratic signatories. Given that the legalistic design of the dispute settlement process under the BIT regime makes noncompliance costly, signing new BITs is rational for a government only if it expects to gain from willingly complying with the treaty obligations ex ante.

The key determinant of the incentive compatibility of BITs resides in the signatory’s opportunity cost of compliance, which is determined by the political value of the alternative policies that must be forgone to comply with the BIT provisions. These policies consist of discretionary and redistributive moves in industrial regulation, taxation, and social welfare. The political value of the forgone policies is an increasing function of the autocratic ruling group’s current perception of the intensity of threats to the regime’s rule. This perception inversely corresponds to the regime’s time horizon (Wright 2008a, 2008b). When its time horizon is relatively long, indicating the regime foresees no imminent threats to its rule, the government is well positioned to gain from signing and complying with BITs. Shortening the time horizon increases the political value of the forgone policies, because the regime would now expect more frequent threats that could be addressed by these policies. BITs signed under a short autocratic time horizon are hence likely to see low levels of compliance which would both nullify their commitment function and idly increase the cost of stabilizing policy maneuvers.

We therefore contend that autocratic time horizon should be expected to be positively associated with the probability that a regime will sign new BITs. We empirically test our claim in an event history analysis of a dyad-year level data set on BITs formation from 1971 to 2009 that models variables contributing to the “demise” of BIT-free country-dyads. Following previous studies (Blake 2013; Moon 2015; Wright 2008a, 2008b), we use the estimated probability of autocratic regime failure to measure autocratic time horizon. We choose a dyadic over monadic design because it uniquely allows us to adopt a gravity-model type specification to control for a battery of confounding determinants of BITs at state, bilateral, and systemic levels. The empirical results consistently support our theoretical claim and pass a series of robustness check analyses with different proxies for regime time horizon, alternative model specifications, and additional controls.

Our paper contributes to the literature on investment treaties in a number of respects. First, studies that evaluate the commitment effect of BITs among states with weak accountability institutions (e.g., Arias, Hollyer, and Rosendorff 2018) have yet to systematically examine the factors shaping the decision to sign BITs. Meanwhile, research that has broadly examined incentives to sign BITs (e.g., Cho, Kim, and Lee 2015; Rosendorff and Shin 2015) have not sufficiently taken political variation among autocratic regimes into account. By focusing on regime time horizon, we complement previous studies that explicitly examine autocratic regimes’ decisions about whether to sign BITs. Our finding adds to this strand of research by suggesting that the commitment effect of BITs in autocratic regimes may be conditioned by their capability to manage and absorb the negative domestic impact of the treaties. Second, some studies have highlighted the conditional nature of the effect of investment treaties on domestic governance by emphasizing the importance of legal institutions and government capabilities (Rose-Ackerman and Tobin 2005; Tobin and Rose-Ackerman 2011). Our paper adds to this line of inquiry by introducing regime time horizon as another domestic political factor that shapes the selection process underlying the formation and effect of BITs.

Finally, our paper offers a different perspective to help understand the significance of time horizon on economic policy making in autocratic regimes. Existing theories on time horizon in autocratic regimes tend to conceptualize it as an indication of the ruler’s patience or the discount factor (Blake 2013; Kono and Montinola 2015; Moon 2015; Wright 2008a, 2008b). For example, Blake (2013) suggested there is a negative relationship between time horizon and the scope of provisions in BITs. Blake considers time horizon mainly as the discount factor in the government’s calculation, which is assumed to be exogenous to its compliance incentive. We argue that time horizon affects a regime’s decision to sign BITs by shaping not only the way the expected payoff is discounted but also its structure. After all, the payoff from BITs varies greatly depending on the ensuing compliance behavior. We characterize time horizon as one factor shaping the endogenous compliance incentive and hence government decisions about whether to sign BITs.

Although we argue that autocrats consider the cost of compliance when deciding whether to sign BITs, other scholars may disagree. For example, Poulsen and Aisbett (2013) and Poulsen (2014) suggested that capital-hosting signatories of BITs are boundedly rational and tend to underestimate the legal risk associated with BITs. We argue that autocrats factor in the cost of compliance for three reasons. First, we do not necessarily argue against the potential “bounded rationality” of BIT signatories. Instead, our argument connects an autocratic regime’s evaluation of political risk with the level of prudence exercised before the decision to sign new BITs. On one hand, shortening the time horizon of an autocratic regime increases the opportunity costs of compliance. On the other hand, it also makes an autocratic regime more risk averse in signing new BITs, given the regimes’ compromised capacity for treaty compliance. Although autocrats may not always consider all possible consequences when signing BITs, they are more likely to do so when they expect compliance to be difficult. Second, evidence from recent studies (Arias, Hollyer, and Rosendorff 2018; Mazumder 2016; Rosendorff and Shin 2015) suggests that BITs have a significant political impact on autocratic signatories. These studies posit that autocratic governments internalize, at least partially, the negative consequence of violating provisions in BITs. Our argument and analysis are in line with this conventional premise underlying the existing literature. Finally, our empirical analysis accounts for the signatory’s cognitive lag in assessing the risk associated with BITs by controlling for the “learning” effect induced by investment dispute cases (Manger and Peinhardt 2017; Poulsen and Aisbett 2013). Our main finding remains highly robust after controlling for such an effect. 1

The rest of the paper is organized as follows. The second section explains the sources of the domestic political significance of BITs in the political economic context of autocracies. The third section elaborates our theoretical argument, which is centered on the relationship between the opportunity costs of compliance and the benefits of signing BITs, from which the key hypothesis is derived. We then discuss the design of the empirical analysis and present the empirical findings and discussion. The final section concludes by discussing the broader implications of our research.

Investment Treaties and Autocratic Political Economy

The provisions formalized in BITs codify the guidelines of investor protection and empower investors to file litigation against capital-hosting states. Recent developments in investor–state relationships highlight four provisions in investment treaties that serve as key sources of the constraining power of BITs: protection against (direct and indirect) expropriation, fair and equitable treatment (FET), national treatment, and most importantly, investor–state dispute settlement (ISDS). Protection against expropriation is a cornerstone provision that prohibits the taking of investors’ property, directly or indirectly, without due process and compensation. The FET and national treatment standard are designed to protect investors more broadly against “serious instances of arbitrary, discriminatory or abusive conduct by host states” (United Nations Conference on Trade and Development [UNCTAD] 2012). In case of disputes, the ISDS provision in BITs allows investors to bring disputed cases to international tribunals for arbitration.

These provisions impose constraints on both expropriation behavior and discretionary policies and regulatory initiatives. BIT clauses such as the FET and national treatment standard widen the scope of investor protection beyond illegal takings of properties. For example, investors have routinely utilized the FET standard to challenge many regulatory policies of host states based on bold and expansive readings of “fairness” and “equity” (Vandevelde 2010). Similarly, many discretionary policies and regulatory moves of the host that indirectly affect particular investors have triggered claims alleging “indirect takings” by the government (Pelc 2017). Although the national treatment standard seeks to foster a level playing field for domestic and foreign investors, it also curtails a government’s ability to protect politically significant domestic sectors (Blake 2013).

The ISDS clause represents the key protective provision in BITs. A remarkable feature of the dispute settlement design in investment treaties is the private standing of investors vis-à-vis sovereign governments in international tribunals. The enforceability of rulings issued by investment tribunals stems from both the Convention on the Recognition and Enforcement of Foreign Arbitral Awards and the sovereign state’s voluntary adoption of the UNCITRAL (United Nations Commission on International Trade Law) Model Law on International Commercial Arbitration in domestic legislation. The legalistic nature of ISDS draws a striking distinction between investment disputes arbitration and dispute settlement rules in other areas of global governance (Choi 2007). As the legality of arbitration is firmly grounded in the ISDS provision in BITs, host signatories face significant legal risks: investors are capable of filing claims against them whenever harms caused by the government are perceived. In this sense, BITs incur significant sovereignty costs on the host by increasing the international legal risk of domestic regulatory policy maneuvers (Pelc 2017).

The Effect of BITs on Discretionary Policy Space in Autocracies

The sovereignty costs associated with BITs are politically significant in autocratic regimes. Along with the dispute settlement regime, constraints arising from BITs make policy and regulatory moves by the host government costly. Autocratic governments frequently wield their unconstrained discretionary executive power to maneuver policies to cope with challenges to their political rule. The highly discretionary use of executive power is at the heart of autocratic politics: the stability of the winning coalition hinges on the incumbent’s ability to strategize the distribution of economic resources and rents among the selectorates and make timely adjustments when challenges emerge (Bueno de Mesquita et al. 2005). Discretionary policy maneuvers are crucial to autocratic political rule because they allow regime leaders to selectively punish or reward groups or individuals (Acemoglu, Robinson, and Verdier 2004). These discretionary policy maneuvers can be conducted in agricultural and industrial policies (Bates 1986), taxation and social welfare (Acemoglu, Robinson, and Verdier 2004; Robinson, Torvik, and Verdier 2006), trade and exchange rate measures (Hankla and Kuthy 2013; Steinberg and Malhotra 2014), and macroeconomic policy (Pepinsky 2009). Due to the weak institutionalized constraints in autocratic polities, policy moves that are distributive or redistributive in nature are less likely to be challenged domestically (Busse and Hefeker 2007; Jensen 2003; Li 2009).

Discretionary policy maneuvers, however, jeopardize the policy consistency and regulatory stability valued by investors (Henisz 2004): BIT provisions counter such risks by asserting the lawful rights of foreign investors in volatile political environments. As FDI grows in importance, autocrats’ policy choices become more consequential for investors. BIT-protected investors harmed by discretionary moves most frequently allege breaches of the indirect expropriation clause and FET standard. BITs greatly constrain autocratic policy choices: they force autocrats to pay additional costs for discretionary policies that adversely impact investors. Policies intended to consolidate political control will risk litigation that inflicts various types of losses on the regime.

The consequence of ISDS procedures heightens the significance of BITs’ influence on discretionary policy maneuvers in autocracies. Once they are brought before international arbitration bodies, the operational and legal costs incurred by the respondents can be substantial. If a ruling is issued in favor of the investor, the award to be paid by the defendant can also be sizable. But, more importantly, being brought to arbitration institutions as the respondent in ISDS cases incurs considerable reputational costs on capital-hosting signatories. The incidence of both registered and lost ISDS cases at the International Center for the Settlement of Investment Disputes has led to sizable declines in future FDI flows into the respondent country (Allee and Peinhardt 2011). We expect the reputational significance of the ISDS mechanism to increase in autocratic signatories associated with low levels of transparency (Broz 2002; Hollyer, Rosendorff, and Vreeland 2011; Stasavage 2003; Svolik 2006). Due to the lack of transparency in institutions and policy processes, autocratic governments potentially suffer more reputational damage when ISDS disputes deliver negative information to prospective and existing investors.

In summary, the scope and mechanism of the protections that BITs afford to investors can significantly interfere with the autocratic advantage of politically motivated discretionary policy maneuvers. For autocratic signatories, complying with the provisions in BITs would inflict a political cost. The next section explicates how the political costs of compliance can vary across autocratic regimes according to their time horizon and shape the decision calculus regarding whether to sign BITs.

Opportunity Costs of Compliance, Regime Time Horizon, and BIT Signing

Although BITs constrain an autocrat’s policy choices, they could still be deemed favorable as they may promote investment inflows by strengthening property rights commitments. Scholars have argued that BITs serve as hand-tying devices and render the host’s commitment more credible (Allee and Peinhardt 2011; Haftel 2010; Kerner and Lawrence 2014). An autocratic regime could benefit from the greater credibility induced by BITs and thus acquire a strong incentive to sign them.

It is important, however, to recognize that several recent studies suggest that the commitment effect of BITs is conditional: they can only be effective hand-tying devices when the host countries have good domestic institutions and the signatories are shown to have complied with their provisions (Aisbett, Busse, and Nunnenkamp 2018; Allee and Peinhardt 2011; Tobin and Rose-Ackerman 2011). Signing but failing to comply with BITs will cancel out their commitment feature and backfire on the host signatories. In the meantime, complying with BITs can be politically costly for autocratic regimes because doing so greatly constrains the policy options available to governments. We therefore contend that the commitment effect of BITs is conditional on the autocratic signatories’ cost of complying with them. An autocratic regime will be prone to sign BITs and willingly comply with them only when the compliance costs are politically acceptable to the regime.

We conceive the compliance costs of BITs as the opportunity cost of bringing a signatory’s policy conduct into conformity with the treaty’s investor protection standards. These opportunity costs reflect the political value of the alternative policies that must be forgone to comply with BIT provisions. Although BITs typically have similar standards of investor protection, the political value of the forgone policies in compliance with BITs varies across regimes. When the political value of the alternative policies is low, the autocrat suffers limited political losses at home from compliance. Accepting the constraints imposed by BITs and complying with them could be rational for the regime if the costs of compliance are lower than the commitment benefits. However, when the political value of the forgone policies is high, compliance is no longer rational as it incurs an unacceptable political cost to the regime. As a result, the commitment benefits of BITs will dissipate as the signatory loses the incentive to comply. The presence of BITs, particularly the ISDS mechanism, would increase the cost of discretionary policies on the government. Autocratic regimes that expect high political values in the forgone policies would thus be hesitant to sign BITs.

Based on this line of reasoning, our key contention is that the opportunity costs of compliance with BITs are shaped by an autocratic regime’s time horizon, which reflects the ruling coalition’s expectation of remaining in power into the future (Moon 2015; Wright 2008a, 2008b). Associating regime time horizon with the compliance cost of BITs distinguishes our argument from those found in existing studies such as Blake (2013), who considers treaty compliance to be exogenous to time horizon. The autocratic regime time horizon is inversely associated with the autocrat’s assessment of the risk of domestic political challenges. The political value of the forgone discretionary policies necessary for compliance with BITs rises with the regime’s assessment of the intensity of threats to its rule. In countries with a stable autocratic rule and no imminent political challenge in sight, the regime should be willing to give up some discretionary space in exchange for the benefits of investment promotion. The commitment benefit of BITs will take time to materialize following consistent records of compliance, resulting in increased investment inflows over the long term (Aisbett, Busse, and Nunnenkamp 2018; Hallward-Driemeier 2009). Signing BITs is thus more likely for regimes with a long time horizon, which is conducive to compliance and reaping the commitment benefits in the long run.

But as the threat to the regime’s rule intensifies, the political value of the discretionary policies grows. In such a case, an autocratic regime will find BIT provisions that curtail its ability to stabilize its rule too costly to comply with. Shortened autocratic time horizons often follow the deterioration of a regime’s economic situation, which weakens its ability to collect resources and rents to cope with domestic political challenges. Responding to this situation, the regime will more aggressively enact discretionary and extractive policies to extort rents (Li 2009; Moon 2015). Complying with investor protection, provisions in BITs become politically impracticable in such a scenario. As a result, compliance with signed BITs is expected to drop as the regime time horizon shortens. Given the low levels of compliance and great risks of ISDS litigation, signing BITs that empower investors to file claims against the regime will make discretionary maneuvers more costly for autocratic regimes. The incentive to sign BITs thus wanes as a result of a decreasing autocratic time horizon.

Notably, alternative reasoning may exist where autocratic regimes with shorter time horizons may be more tempted to sign BITs. Three lines of logic could underlie such a conjecture. First, regimes featuring short time horizons and political instability often have compromised institutions and lower commitment credibility. The greater need for credible commitment devices could prompt them to sign more international agreements as a way to boost government credibility (Chow and Kono 2017). Second, governments with shorter time horizons are likely to be more short-sighted given the limited expected time to govern. If the commitment benefit of BITs is concentrated in the short term while the costs loom larger in the long term, BITs would be considered more favorable for regimes with short time horizons. Finally, similar to a lock-in rationale in the issue area of human rights documented in the literature (Moravcsik 2000; Simmons and Danner 2010), a “liberalizing” autocrat with a short time horizon may have a strong incentive to sign BITs to prevent future rollbacks in liberalization undertaken by his or her successors.

Combining our argument with the existing evidence, we believe support for these three possibilities is limited. First, previous studies have documented that the commitment effect of BITs is contingent on domestic institutions and compliance (Aisbett, Busse, and Nunnenkamp 2018; Allee and Peinhardt 2011; Tobin and Rose-Ackerman 2011). At the same time, existing research has found regimes with short time horizons are associated with weak institutions for property rights protection (Moon 2015; Wright 2008a). Indeed, poor domestic institutions and noncompliance were shown to have canceled out much of the commitment benefit of BITs (Allee and Peinhardt 2011; Tobin and Rose-Ackerman 2011). Thus, regimes with short time horizons that signed BITs without the capability to comply with them may not expect to gain meaningfully from signing them in the first place. Second, the effect of BITs in promoting FDI inflows has been shown to take years to materialize (Hallward-Driemeier 2009), reducing the appeal of investment treaties to regimes with a short expected time to remain in power. Third, a liberalizing leader foreseeing a regime failure may be less concerned about backsliding in investment liberalization than in the area of human rights. If a democracy emerges following a regime failure (which ensued with 56% of failures in our sample), the literature suggests the new regime is likely to push through further liberalization in trade and investment policies (Milner and Kubota 2004; Pandya 2014). If another autocratic regime rises following regime failure, existing studies remain agnostic as to whether the new regime will necessarily be prone to roll back investment liberalization measures. Although there may exist individual cases where such a “lock-in” incentive was at work in the signing of BITs, preventing future rollbacks of investment liberalization may not be a prevailing motivation among autocrats with short time horizons contemplating signing new BITs.

In summary, authoritarian governments would avoid signing new BITs under short time horizons because they expect themselves to be incapable of complying with the provisions. The additional legal burden of these treaties, and the risks and reputation costs of investor litigation, represent deadweight losses for autocratic governments. However, autocratic governments with longer time horizons and greater confidence in their rule would find BITs more incentive compatible. We now propose the following main hypothesis for our empirical test.

Autocratic Time Horizon and BIT Signing: A Survival Analysis

Our sample consists of 1,806 yearly country-dyads between developed countries (the home country of FDI) and autocratic countries (the host country of FDI) defined by Geddes, Wright, and Frantz (2014) from 1971 to 2009. Following existing empirical works on BIT formation (Cho, Kim, and Lee 2015; Elkins, Guzman, and Simmons 2006; Jandhyala, Henisz, and Mansfield 2011; Neumayer and Plümper 2010), we choose a dyadic level rather than a monadic-level research design. Since BITs are essentially institutional arrangements in pairs of countries, their occurrence is the outcome of joint decisions that are best captured by event history data at the country-dyad level. Setting the unit of analysis at this level also allows us to model for a wide range of determinants of bilateral treaty signing that could exist at multiple levels while accounting for the gravitational forces in the dyads. Membership in the OECD is used as a proxy for identifying the home country in the dyads. 2 We also exclude from our sample all country-dyads between authoritarian countries and other capital-hosting countries in the Global South. Although BITs between capital-hosting countries in the Global South (so-called South-South BITs) increased rapidly during the 1990s, they are considered less relevant to the current analysis (Elkins, Guzman, and Simmons 2006; Jandhyala, Henisz, and Mansfield 2011) as there is little potential for cross-border capital flows in the dyads. As our theory hinges on the assumption that the perception of increasing FDI inflows (after signing BITs) enters into the cost–benefit calculation of autocratic regimes’ decisions about whether to sign BITs, we drop those South-South dyads from our sample.

Dependent Variable, Independent Variable, and Controls

The dependent variable counts the consecutive years in which a BIT in the dyad was not signed since the dyad came into being post-1958. This formulation marks the start of the “risk” of signing a BIT in the dyad either in 1958 or in the year the dyad formed if one or both of the countries gained independence and joined the world system after 1959. The BIT signing data comes from the International Investment Agreement Database (UNCTAD 2014). We focus on the signature rather than the ratification of BITs because ratification is the outcome of distinctive domestic processes (Haftel and Thompson 2013) that are beyond the scope of this paper. The cross-country variation in the idiosyncratic procedures for treaty ratification is likely to lead to larger measurement errors if the ratification of BITs is taken as the dependent variable. In addition, 88 percent of BITs in our sample were ratified by both parties by 2009, suggesting that signing BITs without the intention to ratify is rare. Our use of BIT signature rather than ratification is also in line with the empirical strategy used in mainstream studies exploring the political mechanism underlying the proliferation of BITs (Cho, Kim, and Lee 2015; Elkins, Guzman, and Simmons 2006; Jandhyala, Henisz, and Mansfield 2011; Neumayer and Plümper 2010).

Following previous studies (Dionne 2011; Kendall-Taylor 2011; Kono and Montinola 2015; Moon 2015; Wright 2008a, 2008b), we use the “yearly predicted probability of regime failure” to capture the time horizons of autocratic regimes. The risk index, or predicted probability of regime failure, is based on a panel logistic model that takes into account “observable causes” that lead to the failure of authoritarian rule (Wright 2008a, 2008b). This measure is exclusively tailored to autocracies and does not apply to democratic regimes. A low (high) predicted value reflects a low (high) risk of regime failure, and hence a long (short) time horizon. This risk evaluation of regime failure, as assumed in the conceptualization of Wright (2008a, 2008b), reflects the same calculus to which autocratic rulers are attuned as external observers. Wright’s risk index of regime failure is the most suitable dynamic measurement of autocratic regime time horizons. It not only accounts for the effect of different leaderships within an authoritarian regime but also captures the dynamic impact of economic and social factors on regime time horizon. The original index from Wright’s model covers the years 1971 to 2003. We use the same procedure of generating predicted probability of regime failure to extend the index to 2008. 3

We also include four types of control variables: political, economic, global or systemic, and cultural and geographical controls. The political control variables capture dissimilarities between the two countries in the dyad in terms of their domestic political systems and the quality of their domestic legal infrastructures. As a number of existing studies have pointed out, BITs play an important role in bridging the differences in political and legal practices between home and host countries (Bubb and Rose-Ackerman 2007; Neumayer and Spess 2005). The expected utility of an investment treaty increases if investors face a significantly different political and institutional environment abroad that requires an interstate arrangement to manage the costs of accommodating investment risks in host states (Allee and Peinhardt 2010). The “dissimilarity” is measured by the absolute value of the difference between two countries in each of the three variables, namely, democracy (Polity2 index from Polity IV data set), political constraint on the executive (Henisz 2000), and latent judicial independence index (Linzer and Staton 2015).

The economic control variables cover factors that account for economic gravity dynamics underlying the need for a BIT in the dyad. The sum of gross domestic product (GDP) in the dyad and the squared difference in GDP between the home and host states capture the potential for horizontal FDI flows between two countries. Difference in per capita GDP between the home and host countries in the dyad captures the potential for vertical FDI flows in the dyad. GDP growth rate in the host country indicates the investment opportunities and potential for FDI. Trade openness is measured as the sum of exports and imports as a percentage of GDP. Countries with deeper integration in global trade networks may see greater drives for FDI and hence a stronger push for the harmonization of investment policies. We control for trade openness in the host and home countries. The Preferential Trade Agreement (PTA) dyad variable indicates whether both countries are parties to any such common agreement. This is an important control variable, as recent scholarship has found linkages between the dynamics of cross-national investment and international trade institutions (Büthe and Milner 2008). Finally, the net outflows of FDI as a percentage of GDP in the home country indicates the importance of ensuring the security of its overseas investments for the economy of the home country and the strength of the push from the home country government to conclude BITs.

Global or systemic control variables account for the impact of global politics and institutions on bilateral FDI flows and investment arrangements at the dyadic level. The global BITs variable controls for the global trend of BIT formation. We also control for the cumulative number of BITs signed by capital-importing countries in the same region to capture the competition logic of BIT signing as elaborated in Elkins, Guzman, and Simmons (2006). We consider regional peers to be economic competitors, because states in the same region may have comparable economic structures, infrastructures, and factor endowments that are attractive to similar types of foreign investors. Hence, foreign investors could well consider neighboring states as substitutes when deciding where to invest. A Cold War dummy variable is added to account for possible effects of the change in great power dynamics during or after the Cold War on foreign investments and global investment institutions. Finally, cultural and geographic controls account for geographical distance, common language, and colonial linkages between two countries in a dyad. These control variables are intended to capture features that are fixed to each dyad and potentially affect the formation of BITs. Descriptive statistics and data sources for all variables can be found in Table A1 of Online Appendix A.

Results

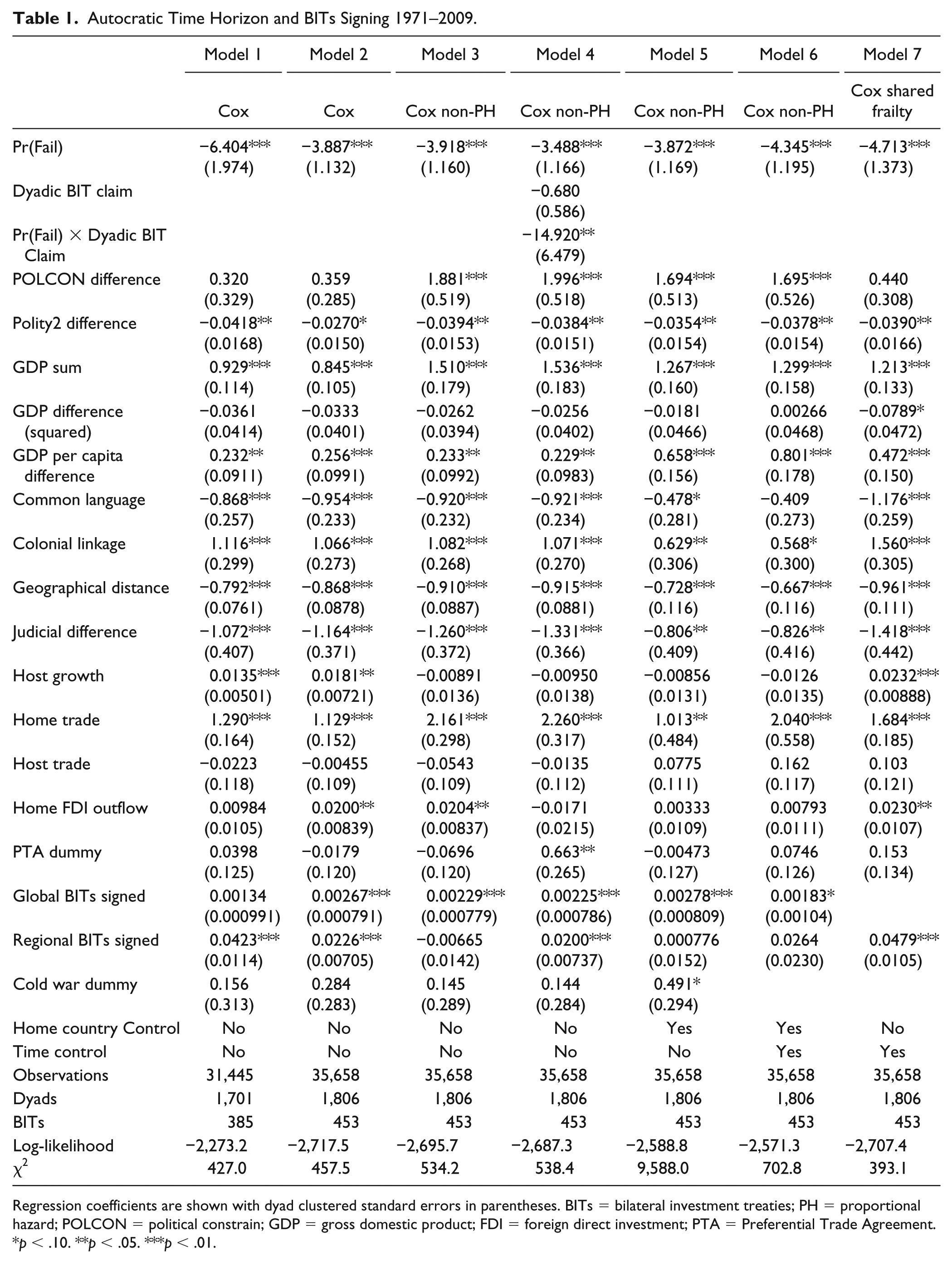

To test our hypothesis, we employ a Cox model to analyze the duration of time before a BIT is signed (Cho, Kim, and Lee 2015; Elkins, Guzman, and Simmons 2006). All independent variables are lagged by one year to alleviate simultaneity. Our main results are shown in Table 1. In all models, a positive coefficient indicates a higher probability of signing a BIT as the value of the independent variable increases. Model 1 uses Wright’s (2008a) original index of predicted probability of regime failure, while model 2 employs our updated index. We find strong evidence that autocratic regimes with long time horizons (i.e., a low risk of regime failure) are more likely to sign BITs with OECD countries in models 1 and 2. The advantage of using the basic Cox model is that it makes no assumptions about the baseline hazard function. However, it does assume that hazard rates are proportional across units. We therefore test this proportional hazard assumption with Schoenfeld residuals (Haftel and Thompson 2013). Although our regime failure variable Pr(Fail) passes the test, the assumption is violated by some of our control variables, which suggests that the effect of those variables is likely to vary depending on the time duration. We correct the nonproportionality by interacting those “offending variables” with time duration (Box-Steffensmeier, Reiter, and Zorn 2003). As shown in model 3, the key result remains the same when a nonproportional hazard Cox model is employed.

Autocratic Time Horizon and BITs Signing 1971–2009.

Regression coefficients are shown with dyad clustered standard errors in parentheses. BITs = bilateral investment treaties; PH = proportional hazard; POLCON = political constrain; GDP = gross domestic product; FDI = foreign direct investment; PTA = Preferential Trade Agreement.

p < .10. **p < .05. ***p < .01.

We further explore whether the effect of regime time horizon varies according to the availability of information on the costs of BITs. When these costs become more observable, autocracies with shorter time horizons are much less likely to sign investment treaties. States have been found to learn the sovereignty cost of BITs when they are directly involved in investor–state dispute arbitrations (Haftel and Thompson 2018; Manger and Peinhardt 2017; Poulsen and Aisbett 2013). Poulsen and Aisbett (2013) emphasize the importance of the first BIT-related claims in updating states’ assessments of the costs of signing BITs. We use their data to construct a binary variable that captures whether host or home countries have been hit by their first BIT claim in a given year, and interact this variable with the regime failure index in model 4. The interaction term gains statistical significance at the 95 percent confidence level, indicating that the negative impact of the regime failure index on the probability of signing BITs is stronger after states experience their first BIT-related claim. This result lends support to both the “learning” mechanism and the conjecture that autocratic regimes with short time horizons are much less likely to sign BITs when the updated information regarding the costs of BITs becomes more accessible.

Model 5 controls for home countries’ idiosyncratic “taste” for BITs (partly reflected in the BIT “programs” of major capital-exporting countries) by including home country dummies. We also account for time trend or time-specific shocks by using half-decade dummies in model 6. The signing of BITs may cluster in time dimensions and occur in waves (Jandhyala, Henisz, and Mansfield 2011). As shown in models 5 and 6 of Table 1, our main results are robust to the inclusion of home country and time controls. It is possible that some dyads are inherently more likely to sign BITs than others due to unobserved dyad-specific heterogeneity. To alleviate this concern, we employ frailty models in the duration analysis. Observations within the same dyad have a “shared” frailty that prompt them to sign BITs earlier than other dyads (Box-Steffensmeier and Jones 2004). Meanwhile, we also more finely account for time-specific factors by including year dummies. As shown in model 7, our main result continues to hold.

Figure 2 illustrates the substantive effect of regime time horizon on BIT signing based on model 2. We plot the estimated survival rate of country-dyads without BITs when our key independent variable of Pr(Fail) is one standard deviation below and above the mean. We find that autocratic time horizon, Pr(Fail), has a meaningful substantive effect on BIT formation. In the late 2000s, fifty years after the inception of BITs, the signing rate of autocracies with Pr(Fail) that is one standard deviation above the mean is about 10 percent less than those with a Pr(Fail) one standard deviation below the mean. We also estimate the substantive effect of our key independent variable by calculating the percent change in the hazard rate associated with a change in the regime failure index using the following formula:

where x1 and x2 are the values of regime failure variable at one standard deviation below and above the mean, respectively. According to the result in model 2, the percent change in the hazard rate is about −34.15 percent with a 95 percent confidence interval of [−48.52, −16.59]. This change is statistically significant, indicating that the hazard rate of signing a BIT decreases by about 34 percent when the regime failure index changes from one standard deviation below the mean to one standard deviation above the mean.

Survival estimates at high (M + SD) and low (M – SD) level of autocratic regime risks.

Finally, regarding our control variables, we find that dyadic differences in judicial independence and Polity2 scores between the home and host countries tend to reduce the likelihood of signing a BIT, while the result for the differences in the political constraint variable is mixed depending on the model specifications. Consistent with the finding in Allee and Peinhardt (2014), this result implies that countries with very different domestic legal and political institutions are not more likely to sign a BIT than otherwise. In addition, the potential for horizontal and vertical FDI flows within dyads significantly increases the likelihood of signing a BIT. We also find that common language and dyadic distance decrease the likelihood of signing a treaty, while colonial linkage, trade openness in the home country, and the global number of BITs increase the probability of signing a BIT.

Robustness Check: Alternative Proxies for Autocratic Time Horizon and Additional Controls

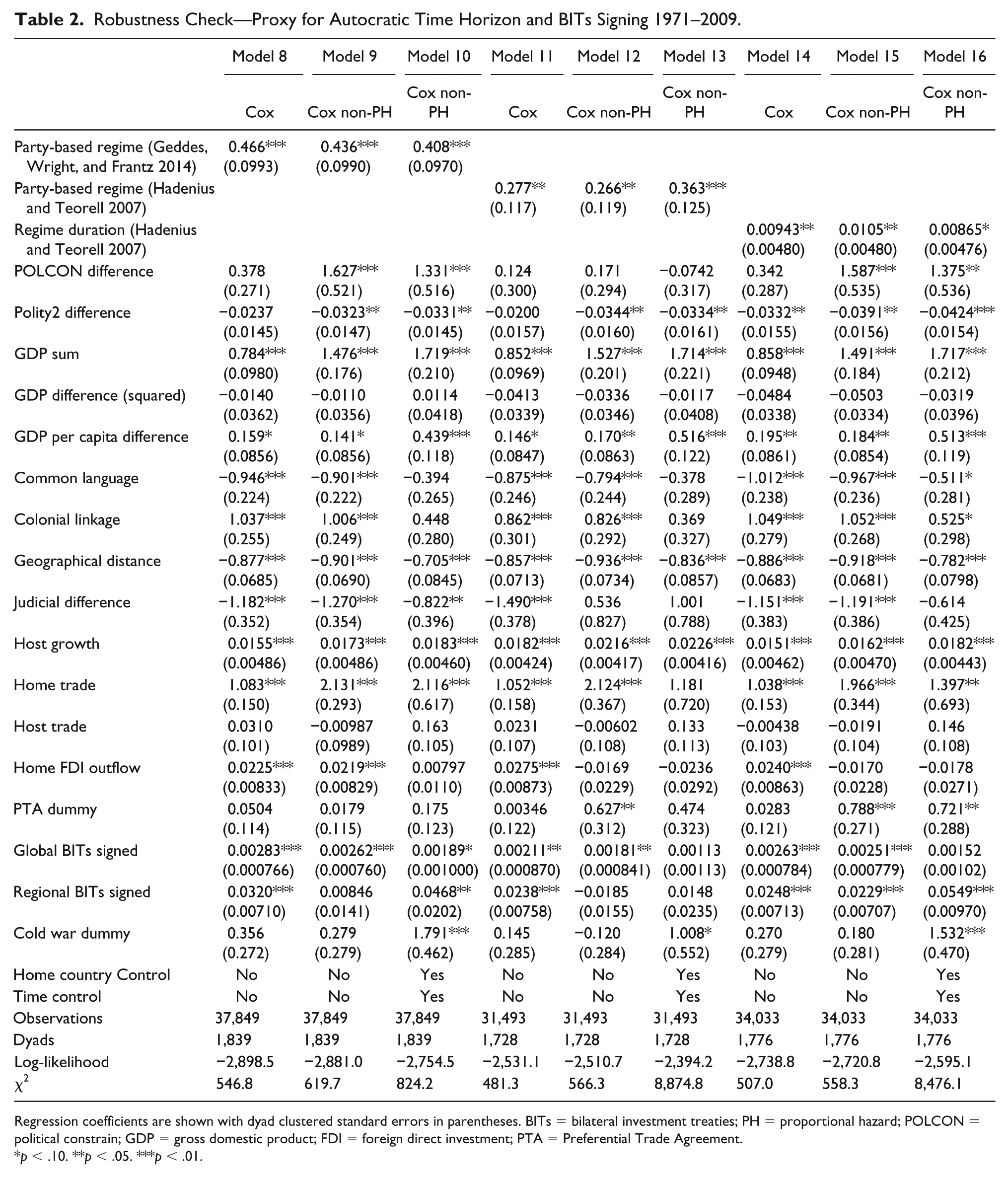

We use three alternative observed proxies for regime time horizon to check the robustness of our results. Scholars have explored the survival rate of autocratic regime by subtype and found that party-based autocracies tend to be more durable and stable than their nonparty-based counterparts (Geddes 2003; Magaloni 2008). We thus construct a binary variable of party-based regime using two different data sets—Geddes, Wright, and Frantz (2014) and Hadenius and Teorell (2007). A party-based regime is coded as 1, and 0 otherwise. Following Hankla and Kuthy (2013), we also use a regime duration indicator, totdur1ny, from Hadenius and Teorell’s (2007) database to capture regime stability. This variable measures the number of years the current regime type has been in place, backdated to 1960. Table 2 shows the results for these three proxies of autocratic time horizon. We find strong support for our argument that autocratic time horizon has a positive impact on the likelihood of signing BITs with developed countries.

Robustness Check—Proxy for Autocratic Time Horizon and BITs Signing 1971–2009.

Regression coefficients are shown with dyad clustered standard errors in parentheses. BITs = bilateral investment treaties; PH = proportional hazard; POLCON = political constrain; GDP = gross domestic product; FDI = foreign direct investment; PTA = Preferential Trade Agreement.

p < .10. **p < .05. ***p < .01.

Similar to the way we assess the substantive effect of the regime failure index, we also calculate the percentage change in the hazard rate associated with a change in our three alternative proxies for autocratic time horizon. Moving from a nonparty-based to a party-based regime, the percentage change in the hazard rate is about +60.18 percent with a 95 percent confidence interval of [31.65, 93.80] for Geddes, Wright, and Frantz’s (2014) regime classification (model 8) and about +32.81 percent with a 95 percent confidence interval of [5.20, 66.21] for Hadenius and Teorell’s (2007) database (model 11). According to the result in model 14, as the values for the regime duration variable move from one standard deviation below the mean to one standard deviation above the mean, the percentage change in the hazard rate is about +29.70 percent with a 95 percent confidence interval of [0.51, 65.56]. All these changes are statistically significant at the 95 percent level, suggesting that autocratic time horizon substantively increases the probability of signing BITs. The robust results using autocratic regime types as proxies for regime time horizon also alleviate concerns of causal simultaneity. After all, a reverse-causal linkage between the type of autocratic regime and the formation of BITs is unclear, given the lack of evidence documenting any causal effect of BITs on autocratic regime type.

We also test the robustness of our hypothesis by including additional control variables. It is likely that left-leaning autocracies representing workers’ interests may be more skeptical of BITs and capital in general. We therefore control for autocrats’ ideology using data from the Database of Political Institutions (Beck et al. 2001). Following Gehlbach and Keefer (2012), we construct two binary variables for capital-hosting authoritarian countries: rightist (rightist regimes coded as 1, otherwise 0) and leftist (leftist regimes coded as 1, otherwise 0). In addition, scholars have found that states are able to learn the costs of BITs from investor–state dispute arbitrations (Haftel and Thompson 2018; Manger and Peinhardt 2017; Poulsen and Aisbett 2013), which are likely to affect their willingness to sign new BITs. To account for this “learning” mechanism, we include two additional variables: (1) total number of publicly known investor–state dispute arbitrations at international adjudication institutions around the world and (2) a binary variable that captures whether either the host or home country has been hit by its first BIT claim in a given year. The data source is Poulsen and Aisbett (2013). Table A3 of Online Appendix A shows that our results are largely robust to these additional controls.

Conclusion

This paper joins scholars who emphasized the importance of the distinct political context of authoritarian rule in understanding the dynamics of economic policy making in autocratic governments (Hankla and Kuthy 2013; Steinberg and Shih 2012). We argue that BITs are not cost-free instruments for investment promotion; their costs must be analyzed and understood in the political context of the signatories. Our study highlights the impact of domestic political parameters on autocratic regimes’ decisions about whether to sign BITs. We examine how variation in regime time horizon explains the differential participation of autocratic countries in BITs.

We argue that the compliance costs of BITs are likely to be lower in autocracies with longer time horizons, which increases their likelihood of signing BITs. As BITs require autocratic countries’ policy conduct to conform with stringent investor protection standards, they constrain discretionary and redistributive policy maneuvers that are critical to autocratic survival. The opportunity costs of complying with BIT provisions, and the political value of forgoing discretionary policies, however, vary by autocratic time horizon. Autocratic governments with long time horizons are able to give up some discretionary space in exchange for the commitment benefit of signing BITs. Yet for governments with short time horizons, the political value of the forgone discretionary policies is much higher—thus lowering their probability of signing BITs. We tested our claim using dyads between all autocratic countries and capital-exporting OECD countries from 1971 to 2009. The empirical results strongly support our argument that autocratic regimes with long time horizons are more likely to sign BITs with capital-exporting countries. The results are robust to the inclusion of additional control variables, alternative measures of autocratic time horizon, and different model specifications.

Our study has implications for understanding the causal effect of BITs on investment promotion amid concerns of selection bias. The main finding of this paper suggests that there is indeed a specific self-selection mechanism underlying the formation of the investment treaty regime: autocratic regimes with long time horizons are more capable of managing the costs of treaty compliance than their peers and are hence more likely to sign BITs. This selection mechanism, however, is unlikely to completely offset the effect of BITs as our argument unfolds. After all, low costs of compliance may be insufficient to precipitate compliance in the absence of institutions with monitoring and enforcement apparatus. The constraints imposed by BITs still makes a difference because they transform the state’s capability to comply into a willingness to comply. Although researchers evaluating the effect of BITs on investor protection and investment promotion have been well aware of the self-selection mechanism, our argument and findings imply that such a selection effect and the “treatment” effect of BITs can coexist in a logically consistent conceptual framework. Such a perspective may provide a novel analytical angle that could integrate the dynamics of BIT formation into the examination of their impact in future research.

Supplemental Material

Online_Appendix – Supplemental material for Cost of Compliance, Autocratic Time Horizon, and Investment Treaty Formation

Supplemental material, Online_Appendix for Cost of Compliance, Autocratic Time Horizon, and Investment Treaty Formation by Jia Chen and Fangjin Ye in Political Research Quarterly

Footnotes

Acknowledgements

We thank Tim Betz, Cristina Bodea, Tim Büthe, Michael Colaresi, Erica Frantz, Andreas Fuchs, Soo Yeon Kim, Sung Min Han, James Hollyer, Sung Eun Kim, Bumba Mukherjee, Damian Raess, Mi Jeong Shin, Min Tang, Yu Zheng, and Thomas Zylkin for helpful comments (authors are listed alphabetically). Three anonymous reviewers and the Political Research Quarterly (PRQ) editor also provided excellent suggestions.

Authors’ Note

Earlier versions of this article were presented at the annual meetings of the Midwest Political Science Association 2016, American Political Science Association 2016, and Political Economy of International Organization 2017, Workshop on Conflicts at Michigan State University Political Science Department, Fudan University and Shanghai University of Finance and Economics.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Jia Chen received support from the National Social Science Fund of China (No. 17CGJ032: The Evolution of the Dispute Settlement Mechanism in the Investment Treaty Regime).

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.