Abstract

Charter school advocates see the infusion of market competition into the educational sector as a means to achieving greater efficiency, effectiveness, and equity. Within this framework, consumer demand is understood to regulate the charter sector. This article challenges the adequacy of this premise, arguing that the structure of the financing of charter schools plays a decisive, if not determining, role in directing growth. Drawing on an analysis of the financing that enabled the dramatic growth of the UNO Charter School Network (UCSN) in Chicago during the 2000s, the article explores the implications of speculative borrowing and spiraling debt burdens on charter schools and on the functioning of the charter sector more broadly. The analysis reveals that (1) new debt was increasingly used to retire existing debt, (2) the structure of new financing assumed continued growth, and (3) schools within the network were yoked together as revenue from existing—and anticipated—schools was pledged to repay new debt.

Introduction

Between 2000 and 2015, the charter school sector in the United States grew from approximately 400,000 to 2.9 million students, a sixfold increase in enrollment (“A Closer Look at the Charter School Movement” 2016). Proponents see within this growth evidence of strong demand for privately managed charter schools among parents and validation of the success of the charter model. The explosion of charter schools in many cities across the country—and the concomitant closure of traditional public schools—constitutes a fundamental restructuring of the governance, financing, and delivery of public education around logics of parent choice and market discipline. This transformation in education sits within broader urban political–economic shifts that are restructuring cities as markets for investment opportunity (Akers 2015).

From the perspective of market analysis, the lengthy waiting lists for charter schools can be interpreted as evidence of unmet demand, a position taken by the authors of a 2014 report published by the Local Initiatives Support Corporation (LISC):

[T]here are over 6,000 public schools operating under charters, educating . . . 5% of all public school students. However, as reflected in the one million students on charter school waiting lists nationally, this dramatic expansion of the sector has not kept pace with demand . . . (Abraham et al. 2014, p. 1)

In this framing, national charter school growth is understood to reflect the aggregated choice of many individual families who have opted to enroll their children in charter schools. Alongside this reframing of educational need as unmet demand, the withdrawal of the state from direct provision of public education has facilitated an expanded role for private capital in shaping the growth of the charter sector, reconstituting public schools as sites of capital investment and profit extraction. As one investor was quoted in a 2012 article in The Washington Post:

[Charter schools are] a very high-demand product. There’s 400,000 kids on waiting lists for charter schools . . . [and] the industry’s growing about 12-14% a year. So it’s a high-growth, very stable, recession-resistant business. It’s a public payer, the state is the payer on this . . . It’s a very solid business. (Strauss 2012)

It is a gross oversimplification to understand the growth of the charter sector in terms of market demand alone. The need to secure capital financing to grow shapes the behavior of charter schools and charter management organizations (CMOs) in ways that are obscured by simple stories of parent demand. This article argues that—alongside parent choice and administrative processes of charter school review—a better understanding of the role of financing in enabling and constraining the growth of charter schools is necessary for a fuller evaluation of the impact of charter expansion on cities and communities—and the redistribution of risk that expansion entails.

This article describes the expansion of a charter school network in Chicago, as it grew from one school in 1998 with fewer than 500 students to 15 schools with more than 4,000 students by 2013. The United Neighborhood Organization Charter School Network (UCSN) leveraged significant public and private financial resources to expand in an increasingly speculative fashion, as the financing assumed continued enrollment growth within the network. The article analyzes the financing of UCSN as a formative dimension in the geographic, political, and organizational expansion of the network. Our examination of the financing reveals three important dynamics, from which we draw implications. First, as UCSN’s outstanding debt burden grew, an increasing share of new debt went to retire existing debt obligations as opposed to directly funding educational expenses. Second, the financing assumed continued expansion of the charter network through opening new schools that, at the time of financing, the Chicago Board of Education had not authorized. Third, UCSN pledged revenue from multiple schools—both schools already operating and those yet to be opened—to repay the debt. Based on these financial obligations and assumptions, the article argues, first, that the on-the-ground reality of UNO’s charter school expansion directly challenges the motivating theory behind charter schools that growth is driven by parents and communities exercising choice, and, second, that the assumptions of the financing tie the widening network of schools together in ways that reorient success and failure around the financial viability of the entire network, potentially increasing the risk for students and communities of school closure and the reproduction of educational inequality. Finally, we suggest that continued expansion of privatized school “markets” nominally based on choice ultimately reduces inequality in education to matters of individual choice and responsibility, eliminating public responsibility for education.

Charter Schools in Theory and Practice

In 1991, Minnesota passed the first charter school legislation in the United States. The intent in laying the groundwork for publicly funded but privately run schools was to create space for educational innovation by allowing charter schools greater autonomy from school district bureaucracy. In addition, by exposing these schools to the market pressure of parental choice, charter schools were understood to face more direct accountability for their performance (Bulkley and Fisler 2003). The charter school sector has expanded dramatically over the ensuing quarter century, fundamentally changing the landscape of public education in many U.S. cities. Today there are more than 6,800 charter schools across the country, enrolling an estimated 2.9 million students (“A Closer Look at the Charter School Movement” 2016).

The charter school model has become inseparable from logics of choice and the marketization of public education. In principle, families choose to enroll in a specific charter school based on the quality of the education it provides or the school’s ability to meet their specific sets of needs. Proponents of charter schools argue that this exercise of choice by individual families exerts a fiscal pressure on schools that demands accountability in a way that traditional school district bureaucracies cannot.

The Forces Shaping Charter School Expansion: Parent Choice Is Only Part of the Picture

Proponents push charter schools as a strategy for granting access to better schools to all students and creating market incentives for all schools to improve (e.g., Kingsland 2015). That is, faced with the threat of enrollment loss (and subsequent closure through either direct fiscal pressure or administrative review), schools will develop and institute more effective teaching strategies, enabling them to educate students that the traditional public system has been unable to educate and thus providing quality public education to students who have been otherwise unable to access it. From this perspective, a functioning educational market will weed out underperforming schools. And, accordingly, charter advocates often frame the closure of charter schools as confirmation that the charter model is working and that market discipline is shuttering schools that do not perform.

Evidence suggests, however, that market competition is neither driving improved teaching and learning nor achieving greater educational equity (Lubienski 2013). Studies that have moved past the basic assumption that competition among schools for students improves learning have found that school administrators’ responses to competition are more complex and varied—and often emphasize marketing strategies rather than pedagogical innovation (Jabbar 2015; Kasman and Loeb 2013; Lubienski 2005). For example, in his study of Michigan schools, Lubienski (2005) revealed the tendency of schools in marketized systems of public education to divert resources toward marketing, speculating that promotional and branding efforts represent lower risk to the institution than would classroom innovation. He showed, also, how marketing could result in improved school performance by shaping a more selective student body. That is, by targeting their marketing efforts at the types of students and parents they would like to recruit, schools can achieve performance improvements without substantively changing classroom practices (see also Jabbar 2015; Lubienski 2007).

Further complicating the simple narrative of market accountability through parent choice, the growth of the charter sector is, in practice, also shaped and constrained by two additional processes: (1) bureaucratic oversight on the part of charter authorizers, who periodically review and either renew or revoke a school’s charter, and (2) the ability of schools to access the capital necessary to expand. Neither of these factors is exclusively driven by the enrollment choices of parents. Regarding the former, schools may lose their charter through bureaucratic channels for a variety of reasons beyond the market discipline of enrollment competition, including poor academic performance, regulatory violations, or financial mismanagement (Paino et al. 2014). Furthermore, charter closure through administrative review is more complicated—and politically fraught—than charter proponents generally acknowledge, meaning that failures across any of these dimensions might not necessarily result in a school’s closure (Hess 2001; Karanxha 2013). Regarding the latter—which constitutes the focus of this article—schools are limited in their ability to grow by their success in securing the capital required to finance new buildings and programmatic expansion. While per-pupil public funding is generally provided by states to charter schools for operating expenses, accessing capital for facilities development or acquisition is more difficult and can represent a limiting factor on growth. The availability and structuring of capital financing for charter school facilities plays a role in shaping the growth of the charter sector—a role often unacknowledged in popular debates over the merits of charterized school systems.

CMOs

During the early years of the charter school movement, most charter schools were started and run as independent organizations. However, the 2000s saw dramatic growth of networks of schools managed by central, nonprofit organizations, sometimes called charter management organizations (R. Lake et al. 2010). Farrell, Wohlstetter, and Smith (2012) described the emergence of CMOs as a response to (1) a smaller-than-expected impact of charter schools on broader educational systems, (2) mixed results on student achievement and pedagogical innovation, (3) an infusion of philanthropic funding, and (4) federal support for replicating successful charter models.

Furgeson et al. (2012) found that approximately 16% of charter schools nationally were run by CMOs in 2009 (including as CMOs all nonprofit organizations operating two or more schools). They also reported that CMOs are concentrated in urban areas and especially in cities with the largest charter sectors. In Chicago, for example, CMOs accounted for 40% of the charter schools in the city, a rate significantly higher than a national average under 20%. The authors found that 87% of CMOs operated 10 or fewer schools, with 41% operating only two or three schools.

Charter school proponents see possibilities in CMOs for scaling up successful charter school models and strategies. CMOs are able to achieve economies of scale that advantage them over stand-alone charter schools, particularly in their capacity to centralize in a home office the governance functions of the network—including the development expertise needed to secure financing for expansion (Wohlstetter et al. 2011). Wohlstetter et al. (2011) concluded that this gives CMOs the ability to expand much more rapidly than individual charter schools (see also R. Lake et al. 2010).

Financing Charters

By design, charter schools operate with some independence from public school bureaucracies. The institutional flexibility granted to charters to operate outside of traditional public systems structures how charter schools fund their operations and the cost of maintaining and/or building facilities. Charters lack the taxing powers of public school authorities to pay capital costs such as renting space or constructing new school buildings. Most charter schools receive public funds for instruction on a per-pupil basis, often through funding formulas that take into account charter enrollment, but typically receive little, if any, direct allocations to pay for facilities. In early phases of charter school growth in the 1990s, the funding gap for facilities presented impediments to parents, teachers, and other community members opening single, stand-alone schools (Wohlstetter et al. 2011). These financial limits to operating charter schools fostered the growth of CMOs, centralized and professionalized networks of schools that advocates believed could achieve economies of scale and broaden impact across multiple schools (R. Lake and Demeritt 2011).

Charter schools then have needed to act entrepreneurially to find resources. A variety of funding sources have developed to fund charter schools in addition to philanthropy, which has been a major supporter of charter schools. Funds for charter facilities include state and federal loans, tax credits, and tax-exempt bond financing. At the state level, support for charter facilities varies, with a few states providing limited per-pupil allocations for facilities and others opening public facilities to charters. In New York, for example, school districts are required to make available public school facilities for charter schools. Community Development Loan Funds (CDLFs) initially provided a source of funding to charter schools when traditional lenders were unwilling to finance an untested sector.

Given variation of state-level policy in charter school finance, the financial landscape differs widely across charter school networks and individual schools. Little research has analyzed in-depth how charter school finance impacts school operating budgets and charter school growth trajectories, although aggregate data paint a picture of an active and expanding marketplace in debt for charter schools. Through 2013, private nonprofit organizations have provided US$2.1 billion in facilities financing to charter schools, with about half of this amount funded through the federal New Markets Tax Credit (NMTC) program (Abraham et al. 2014). The tax-exempt bond market also provides a pool of capital for charter schools, with nearly US$10 billion in bonds issued by 2014 (Abraham et al. 2014). A 2012 LISC report found that nationally, among 309 outstanding charter school bond issuances that contained pro forma projections, the median share of operating revenue that schools were devoting to servicing the bonds was 13.4%, with a third of the bonds projecting debt burdens over 15% (Balboni and Berry 2012).

Charter school advocates and organizations that support charter growth through technical assistance, such as LISC, understand the charter school funding landscape as a limiting factor to school expansion. LISC’s 2014 report on the state of charter facilities financing noted,

[F]unding inequities persist at every level and securing adequate and affordable facilities remains a daunting obstacle, hindering the growth of some of the country’s highest performing schools. Unlike traditional school districts, charter schools do not have taxing authority and primarily rely on limited public capital funds and operating revenues to pay for their facilities . . . (Abraham et al. 2014, p. 1)

Presenting the differential financing for charter school facilities as an obstacle to growth assumes that, first, financing is fundamentally a constraining factor for all charter schools everywhere, and second, that the underlying relationships embedded in all financing play no active role in directing charter growth. We engage with and challenge both assumptions through studying a specific case of charter school expansion: UCSN in Chicago.

One of the main objectives of this article is to show how financing plays a decisive, but not determining, role in directing growth. Other accounts of charter school development provide evidence that financing environments are not merely passive “obstacles” to otherwise unrestrained charter success. In the provocatively titled article, “How Funding Shapes the Growth of Charter Management Organizations: Is the Tail Wagging the Dog?” the authors suggested that the financing sources that charter schools and organizations rely on fundamentally shape school and organization goals and strategies (Wohlstetter et al. 2011). They wrote,

CMO growth strategies were both funded by and in many ways shaped by the funders. Some CMOs did indeed grow more or less in accord with their own timetable and on their own terms—what we would call “premeditated” strategies. The growth strategies of the plurality of CMOs were somewhat more sensitive to the conditions of the funding environment, though, with CMO leaders adjusting their plans in a more “organic” fashion. To a far lesser extent, a few of the sample CMOs grew in a more “opportunistic” manner, largely in response to the financial environment that they encountered, not planning for growth so much as jumping at opportunities that presented themselves. In general, then, the rate and nature of CMO growth was heavily influenced by the overall financial environment in which they operated. (p. 170)

This introduces the idea that charter school operations and expansion operate in a complex environment where the institutional flexibility afforded to broadly innovate extends to financing and may push charters in different directions. In other words, we cannot assume that the financial relationships in which charters are enmeshed have no bearing on how charters develop, aside from whether they have the resources to do so.

Charter School Expansion Within Broader Processes of Privatization

Marketized school reforms, including charter school expansion, traditional public school closure, and testing regimes, are a part of broader patterns of urban restructuring and uneven development (Lipman 2008; Lipman and Haines 2007; Lipman and Hursh 2007; Means 2008; Smith and Stovall 2008). This article situates the following narrative of charter school expansion in Chicago as part of urban transformations characterized by processes of privatization, corporatization, and financialization that reorganize the city according to logics of development and investment opportunity (Brenner and Theodore 2002; Weber 2002). Studies of urban political–economic restructuring and education emphasize how urban underinvestment and the withdrawal of resources necessarily precede the reframing of urban space as new markets with investment potential.

Local state fiscal retrenchment is a recurring feature of U.S. federalism since the 1970s, only intensifying under post–2008 financial crisis urban austerity regimes (Peck 2012). In this context, the emergence of the “shadow state” in the form of the nonprofit sector creates differential access to citizenship for the most vulnerable individuals in society (R. W. Lake and Newman 2002). In the same way, the growth of the charter school sector and increased reliance on private operators to provide public education over the past two decades create the potential for greater inequality (Akers 2012). That is, variation in community capacity across social, political, and economic dimensions means that in practice the decentralization of education creates a more—not less—uneven geography of educational opportunity (Hankins 2005). Critics of the marketization of public schools have tied this transformation to a larger neoliberalization of urban space that reframes communities and schools as sites for profit extraction, exacerbating existing inequality (e.g., Buras 2013; Lipman 2011b).

In addition to the spatialized inequalities produced through the transformation of public education, the devolution of costs pushes state and local governments into rounds of fiscal restraint alongside the development of new policies and state powers that support and manage the expansion of market logic and activity (Akers 2015; Peck, Theodore, and Brenner 2009). Austerity and the shrinking role of public funding provide the space for expanding financial markets and actors into the void that retrenchment creates. Privatization of public services and infrastructure ostensibly reduces state involvement and costs, devolving the expense to the ultimate level of the household.

Yet, research on privatization and financialization provides a picture of continued and evolving state relationships to markets rather than a simple exit of the state (Ashton, Doussard, and Weber 2016; Starr 1988; Warner and Hefetz 2012). Within the context of devolution and austerity, privatization and financialization (1) reorganize the functions of the state and the management of the targeted infrastructure, service, policy, or project; (2) produce risks into the future that states must manage; and (3) often evolve recursively to require further fiscal restraint and additional rounds of new debt. The increasing influence of financial institutions and logic in urban governance and development requires continued state support and management. In Chicago, for example, Ashton, Doussard, and Weber (2012, 2016) described the reorientation of the local state from manager of infrastructure for public use to insurer of continued profitability and stability of the income derived from infrastructure as assets. The privatization contract and the inherent future orientation of finance, as based on the continued income-producing capability of an asset, mean that states are faced with unknown risks that they must manage going forward. In the process of reorganizing state functions and the purpose of urban space, privatization and financialization introduce new risks while reproducing inequality.

School Reform and Charter Schools in Chicago

Chicago’s current efforts to decentralize school governance date to the late 1980s, although the tenor of reform has shifted from local control and democratic accountability to school choice and market discipline. In 1988, the Chicago School Reform Act curtailed the authority of the central offices of the school district and established local school councils (LSCs) composed of parents and teachers that had the ability to make decisions on personnel, budgeting, curriculum, school monies, and school improvement plans. This dramatic reform came in response to the mobilization of a broad coalition of education stakeholders in the city, including the active leadership of community organizations (Gittell 1994).

Seven years later, the state legislature gave Mayor Richard Daley control of Chicago Public Schools (CPS), including not only the ability to appoint school board members but also the power to overturn school board decisions (Stovall 2013). Daley created a new Chief Executive Officer position to head the school district and appointed his former budget director, Paul Vallas. Under Vallas’s leadership, CPS pursued greater student and school accountability through standardized testing. In 2001, Vallas was succeeded as Chief Executive Officer (CEO) of CPS by Arne Duncan, a position Duncan held until becoming President Obama’s secretary of education in 2009. As CEO, Duncan continued the use of standardized testing to hold schools accountable and pushed for the diversification of schooling options, including a significant expansion of the charter sector.

In 2004, Chicago rolled out the Renaissance 2010 (Ren2010) plan, which called for the closure of more than 60 underperforming schools and the opening of 100 new schools by 2010, with goals that the new schools be one-third charter schools, one-third contract schools (privately operated schools that are similar to charter schools), and one-third CPS performance schools—all models that incorporate greater school autonomy and flexibility while dismantling or marginalizing the influence of labor unions and the democratically elected LSCs (Lipman 2011a; Lipman and Haines 2007). By spring 2010, the school district had closed, consolidated, or phased out 59 schools through Ren2010 and opened 92 (including 46 charter schools) (Lipman 2011a). The Ren2010 plan drew significantly on a report released the year before by the Commercial Club of Chicago, an independent organization of civic and business elites, that called for the infusion of principles of innovation and competition into the education sector as a strategy for increasing the performance of American students in reading, math, and science (Stovall 2013). The Commercial Club of Chicago committed to significant fund-raising in support of the Ren2010 plan, funds that would be directed to support new schools on a competitive basis (Lipman and Haines 2007).

Illinois passed a law allowing for the creation of charter schools in 1996 and the first Chicago charter schools opened their doors the following year. In Illinois, boards of education are authorized to grant, review, and renew/revoke charters, and thus the Chicago Board of Education is the authorizer for charter schools in the city and conducts an annual audit of active charter schools. Growth in the Chicago charter sector was initially slow, in part the result of a 15-school cap in the original charter legislation (Booker et al. 2009). However, the cap has since been expanded and charter enrollment in Chicago grew from approximately 5,400 to 48,700 students between 2000 and 2013 (“Charter Schools in Chicago” 2014).

The Geographical, Financial, Political, and Organizational Expansion of UCSN

Method

The story of the emergence and growth of UCSN is set within this national context of charter school growth and the institutional transformation of public education in Chicago. We follow UCSN not because it stands as a representative case of charter school management and network expansion but because the exceptional dynamics of UCSN, explored below, provide more information than a typical case (Flyvbjerg 2006). Therefore, the purpose of the selection of the UCSN case is to “clarify the deeper causes behind a given problem and its consequences,” as opposed to describing “the symptoms of the problem and how frequently they occur” through typical cases (Flyvbjerg 2006, p. 229). Specifically, in this article, we use the UCSN expansion to understand the role that financing can play in the growth of charter networks, the underlying assumptions of that growth, and the implications of those assumptions on the network, communities, and families.

The following analysis and discussion of the growth and financing of UCSN draws from three bond offering documents, three in-depth interviews with veteran experts in the field of municipal bond finance, and news and other technical reports. The bond offering documents are public records that provide potential bond investors information about UCSN business plans, local student enrollment contexts and market studies, and detailed information about UCSN’s debt structure, operating budget, and cash flow situations. The expert interviews provided background information that helped us analyze the technical aspects of the bond documents and understand broader market dynamics in public finance. We analyzed the bond documents for (1) the financial relationships established between UCSN and its creditors, (2) the expectations about charter school operations, and (3) the justifications for those expectations. To fill in the picture about the assumptions of school growth within UCSN and the sources and uses of the bonds and other financing, we analyzed the bond documents by constructing a timeline of funding that connected different funding sources to each other and to specific school facilities. This analytical tool shows how financing accumulated over time and how the assumptions about repaying the debt changed over time. Finally, we strategically reviewed news articles and practitioner reports to build the narrative of UCSN history and expansion and to situate the case within the broader landscape of charter school expansion and finance.

UCSN expanded with significant public and private financial support, as the organization acted entrepreneurially within the community development system in Chicago and Illinois. The financial arrangements and their assumptions about growth enabled UCSN’s expansion, which we describe along three dimensions. Geographically, UCSN opened charter schools across several Chicago neighborhoods while also expanding the network’s organizational apparatus; financially, the network’s total outstanding debt increased as well as the complexity and interconnectedness of its financial arrangements; and politically, UCSN used a growing charter network footprint—and extensive political connections—to leverage public resources. Each of these dimensions of growth built upon each other as the network expanded.

“Meeting Demand”: The Organizational and Geographical Expansion of UCSN

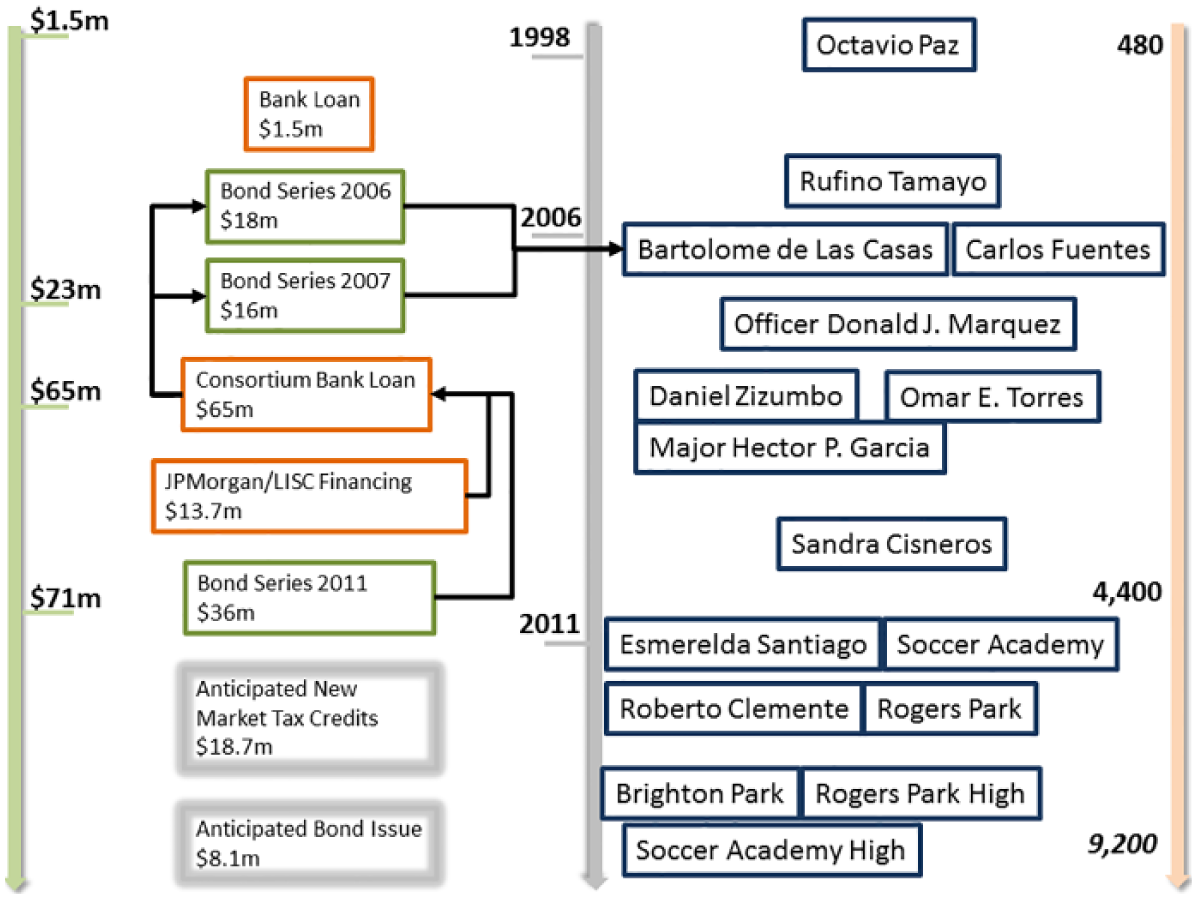

The United Neighborhood Organization (UNO) is a nonprofit organization that emerged in the 1980s to focus on community organizing efforts around issues facing the city’s Hispanic and Latino immigrant populations. In 1998, UNO founded its charter school organization, UCSN, and opened its first school, Octavio Paz, serving students in kindergarten through eighth grade in Little Village, a predominantly Hispanic and Latino neighborhood on the city’s west side. From 2005 through 2013, UCSN expanded the school network from one school with fewer than 500 students to 15 schools with more than 4,000 students (see Figure 1). Before plans for further expansion derailed in 2013, UCSN anticipated enlarging its network to more than 9,000 students by the 2015–2016 school year.

UNO charter schools opened from 1998 to 2013.

The story of this explosive expansion is, on one level, a story of machine politics and political influence. UNO’s well-connected CEO, Juan Rangel, built and drew on political connections with powerful Chicago politicians to finance and grow what became one of the largest charter networks in the city, including Mayor Richard M. Daley, Mayor Rahm Emanuel, Illinois House Speaker Michael Madigan, and Alderman Edward M. Burke (Byrne and Dardick 2013; Mihalopoulos 2012, 2016). The cards came tumbling down for Rangel in 2013 after a Chicago Sun-Times investigation exposed conflicts of interest in the awarding of millions of dollars in contracts paid out of a state grant to family members of UNO executives and UNO’s political allies (see Novak and Mihalopoulos 2013). As a result of this scandal—which led, also, to Securities and Exchange Commission (SEC) charges against UNO for securities fraud—Rangel stepped down as UNO’s CEO in December 2013. On one hand, UCSN’s expansion cannot be fully explained outside of the politics of funding and political favors. On the other hand, however, the use of debt financing through municipal bonds to support charter school expansion is not unique to Chicago (Abraham et al. 2014), and UCSN’s aggressive debt-financed expansion is an important—if extreme—case to understand the implications of capital finance in the growth of the charter sector more broadly. Between 2000 and 2011, UCSN’s debt ballooned from US$1.5 million to more than US$71 million, and it is the implications of this dimension of the Network’s growth that we probe here.

The charter organization originally opened Octavio Paz with the for-profit charter operator Advantage managing the school’s operations. During the 2000s, UCSN began to expand the network, managing its own operations and creating other entities affiliated with the expanding network such as UNO Janitorial and Maintenance Service (JAMS). Rufino Tamayo opened its doors in 2005 in the Gage Park neighborhood, with nearly 90% of its residents Hispanic and/or Latino, located to the south of the Octavio Paz school. During 2006 to 2008, UCSN added six additional campuses, most in neighborhoods near Gage Park, including Archer Heights to the west and Brighton Park to the north. Two other schools opened in Pilsen and in Chicago’s northwest in Avondale. A second period of expansion from 2010 to 2013 pushed the UCSN network facility footprint into the far west side in Galewood and to Rogers Park, the northernmost section of the city that borders Evanston.

The rationale underlying expansion is that there is a need for new schools, and that need is geographically uneven. Casting educational need within a “growth strategy” orients investment opportunity toward charter school expansion (“Illinois Finance Authority Charter School Refunding and Improvement Revenue Bonds (UNO Charter School Network, Inc. Project) Series 2011A” 2011; hereafter “Bond Series 2011”). Within the documents that provide investors with information about the risks and opportunity in school bonds, UCSN describes the lack of both educational quality and quantity, measured in number of seats available in schools, specifically for Hispanic students. The documents present a map indicating the proximity of UCSN schools to areas of the city experiencing a shortage of seats and state: “UNO and UCSN have undertaken to improve education for their constituent communities by addressing the challenge of overcrowded schools . . . UNO and UCSN identify communities in need of the alleviation of overcrowding and additional quality schools” (Bond Series 2011, p. B-5). In this way, a lack of capacity to educate students becomes more than just a community need but unmet demand that can be discursively and materially recast as an investment opportunity.

Financing UNO Charter Schools

Following UCSN’s growth shows how UNO relied on different financing sources to fund its expansion throughout Chicago and what assumptions about future growth that financing entailed. In what follows, we draw on an analysis of the investor prospectuses for Bond Series 2006, 2007, and 2011 issued by the Illinois Finance Authority as education revenue bonds. Our analysis reveals a deepening of the role of debt finance in the growth of UCSN, as it increased its total debt from US$1.5 million in 2000 to more than US$71 million in 2011, tripling its per-pupil annual debt payments during this period (see Figure 2).

UNO Charter School Network financing relationships and facilities.

The bonds are tax exempt and publicly traded, and the interest is paid by specific revenue sources, in this case the allocations from the CPS to UCSN. The bonds issued in 2006 and 2007 carried an “A” rating from Standard & Poor’s, the highest category of investment-grade debt. The 2011 issue was rated “BBB−,” the lowest possible rating that is still considered “investment grade.” According to Standard & Poor’s, this rating signifies that “adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitment” (“S&P Global Ratings Definitions” 2016). In the context of the public debt markets and from the perspective of investors, the UNO bonds are comparatively riskier investments because the underlying revenue sources are, all things being the same, considered less stable and assured than, for example, the City of Chicago’s general obligation bonds which are backed by the “full faith and credit” of the city or bonds issued by the Chicago Board of Education. Both entities have the authority to raise ad valorem taxes to satisfy debt obligations. In contrast, the Illinois Finance Authority has no taxing power and the bond documents cite the lease agreements and a guarantee by the UNO organization as collateral. Thus, the direct risk to taxpayers from the UNO bonds is minimal. However, in the final section of the article, we turn to consider two wider, more indirect, potential risks—first, that in the case that a financial collapse of the charter network imperils multiple schools and thousands of students, the state may find itself compelled to financially support the network, and second, this potential instability could increase educational inequality.

In this article, our analysis and claims about speculation in the financing of UCSN are based on the internal dynamics of its financing. We analyze the bond documents for evidence that we use to make claims about the speculative nature of UCSN’s expansion as an inherent feature of the financial arrangements themselves. The bond documents detail plans for financing and repayment that depend on expansion of the charter network, which is fundamentally uncertain, an expectation about events in the future. Of course, all debt financing is inherently speculative because the extension of credit is based on the anticipation that certain future events will occur and that the debt will be repaid. The important question is not whether the financing is speculative (it is, by definition), but rather what are the underlying assumptions and expectations, and what are the implications if they are met or not.

UCSN used funds from two tax-exempt bonds issued in 2006 and 2007 to acquire, renovate, and expand campuses for three schools: Bartolome de Las Casas, Carlos Fuentes Charter School, and Donald J. Marquez Charter School. In addition, UCSN used the funds to refinance an outstanding loan that had financed renovations to Octavio Paz.

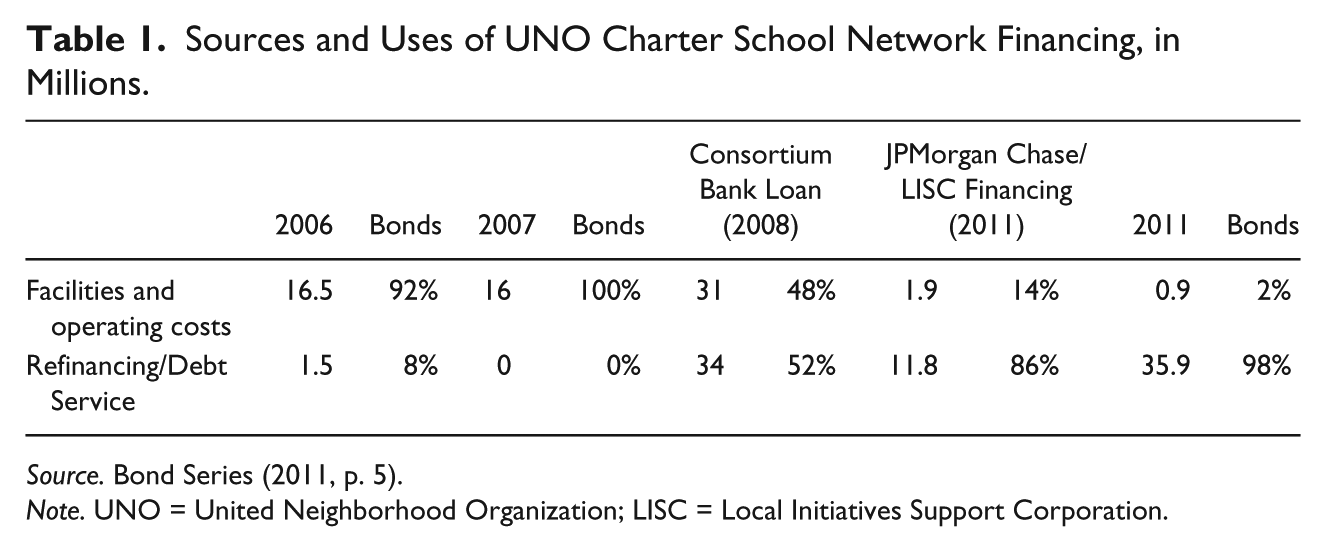

Tight credit markets after the 2008 financial crisis made it difficult to refinance UCSN’s existing debt. In a deal facilitated by Alderman Edward M. Burke, a consortium of banks extended a US$65 million loan to UCSN that was used to pay off the outstanding principal amounts of the 2006 and 2007 bonds and to acquire, construct, and equip the Veteran’s Memorial campus, which included two K-8 schools and a high school (Harris 2012). The proceeds from a US$36 million 2011 bond issue were designated for repaying a portion of the bank consortium loan as well as an Illinois Facilities loan and costs associated with renovations and equipment for the Humboldt Park campus.

The analysis of the bond issues shows a growing debt burden on UCSN characterized by increasing financial complexity and more speculative school growth. The growth in debt parallels the growth in the school network, with nine campuses and more than 3,000 students in 2011 from two schools and about 1,000 students in 2006. This growth strategy is similar to a private firm operating in a competitive market environment.

Starting from a small bank loan in 2000, UCSN used more complex financing arrangements as it expanded. The Bond Series 2006 and 2007 were retired through another bank loan in 2008, part of which was refinanced with the Bond Series 2011 and another loan from JPMorgan Chase and LISC in 2011. This JPMorgan/LISC financing was leveraged through an equity contribution from the sale of NMTC. This debt was expected to be refinanced eventually through a new bond issue. As the school network expanded, UCSN used new debt to refinance existing debt, rather than exclusively for new campus construction. Nearly all of the proceeds from the US$36.8 million 2011 bond issue went to pay off previous debt; about US$850,000 of the 2011 bond was used directly for facility construction and improvements (Bond Series 2011). The consortium bank loan in 2008 was used to purchase the land for the Veteran’s Memorial campus and is collateralized with this property. The basis for new debt increasingly relied on pledged revenues not only from the schools but also from new land acquisitions, deepening the financial leverage of the network and its affiliate UNO, who guarantees all obligations of UCSN. The school network increased its per-pupil leverage from about US$1,500 in 2006 before the bond issues to about US$16,000 in 2011 after that bond sale.

Assumptions About Growth

From a close reading and comparison of the budgets provided in the bond documents, assumptions about student enrollment within UCSN overestimate the actual growth. The bond documents state that when a new school opens, the maximum enrollment is assumed in the first year based on previous experience (e.g., see “Illinois Finance Authority Education Revenue Bonds (Illinois Charter Schools Project) Series 2006” 2006). While this assumption was justified by surrounding school overcrowding and other analyses of school demand, the enrollment was consistently overestimated for de Las Casas, Fuentes, Tamayo, and Paz schools. The overestimates are not large, however. For the 2007–2008 school year, the projected total network enrollment was 2,376, while the actual enrollment was 2,294—a difference of about 82 students or 4%. What is potentially more significant than the size of the discrepancy is the potential for financial distress if actual revenues do not meet expectation. All three bond issues specify that UCSN constructed enrollment projections—four years into the future in the case of the 2011 bond issue—based on the organization’s “experience”; however, more detailed methodology is not included. The 2011 bond issue additionally notes, “The projections of revenues and expenses . . . were prepared by the Borrower with assistance from its financial advisor and have not been independently verified by any party other than the Borrower” (Bond Series 2011, p. B-5). Of course, it is on these assumptions that the bonds are underwritten, marketed, and sold.

Importantly, a potential operating deficit of one school places additional pressure on the other schools to maintain their income to satisfy the debt payments. Each school must perform well financially otherwise the borrower will have to rely more heavily on the well-performing schools’ revenue. In this way, the underperformance of one school that, for example, did not meet enrollment expectations, could affect the whole network by placing additional demands on their revenue.

Furthermore, UCSN anticipated opening six future schools, which were without sites as of the 2011 bond issue, with enrollment projected to increase by 3,600 students by the 2014–2015 school year, doubling the total 2011 enrollment by 2014 (Bond Series 2011). The projected growth in revenue, however, is higher than the growth in enrollment. This anticipated growth is important because the revenues from every new school that is opened would be used to repay the bonds. Also, “revenues” mean the public funding provided based on enrollment in charter schools. Investment decisions in the bonds would be based on the assumption that future schools would be opened. And yet, three of those schools had not yet been approved by the Chicago Board of Education:

The Chicago Board of Education has approved the opening of three additional UNO/UCSN schools for the 2012-2013 school year and applications have been filed with the Chicago Board of Education for approval of three additional schools for the 2013-2014 school year . . . No physical facilities have been identified or secured for any of these six schools . . . The Borrower has covenanted . . . to pledge the Gross Revenues received from any new charter school built. (Bond Series 2011, p. B-5)

The bond agreement here details two significant elements of the financing that have material effects on the operation of the charter network: the assumptions of continued network expansion and the incorporation of any future schools as collateral for debt repayment. In the context of the broader charter bond finance market, projections about enrollment and refinancing are not unusual. LISC reports that in recent years more stringent underwriting standards have required charters to demonstrate historical stabilized enrollment patterns. In addition, about 25% of charter school bonds are used to refinance previous bond issues (Berry 2015). Nevertheless, we highlight how the expectations on which the UCSN financing is based could affect the stability and sustainability of the network.

An unprecedented US$98 million grant to UNO from the Illinois legislature in 2009 supported new UCSN facilities. Importantly, the 2011 bond issue required that any facilities constructed with the public funds, as well as any other schools opened, would fall under the bond agreement and revenues from these schools be used to repay the bonds. The underwriting assumptions of the bonds suggest that the orientation of UCSN is toward expansion of its system, which by 2011 had become an increasingly speculative endeavor with the new schools planned not yet having sites selected (Bond Series 2011; see also Table 1). Furthermore, most of the 2011 bond proceeds were used to refinance an existing loan and not for new campus construction. This demonstrates that UCSN not only anticipated growth but that the financial survival of the network depended on continued growth in enrollment to service the debt already incurred from expansion.

Sources and Uses of UNO Charter School Network Financing, in Millions.

Source. Bond Series (2011, p. 5).

Note. UNO = United Neighborhood Organization; LISC = Local Initiatives Support Corporation.

Conclusion: Market Expansion, Leverage, and Community Control

During the 2000s, as we have reviewed here, UCSN pursued a dramatic expansion of its facilities footprint, enrollment, and programmatic capacity. While charter schools often struggle to assemble the capital necessary for such development, UCSN was able to accomplish this startling growth, in part, by aggressively leveraging its current and anticipated assets to capitalize its projects through debt financing. On one hand, this behavior is unremarkable. Businesses expand in competitive environments by borrowing against their anticipated growth. On the other hand, UCSN was not just any business. It was an organization through which taxpayer dollars were being used to fund public education, which means (1) that it should be accountable to the public for performing that responsibility, and (2) that the risks of speculative growth are shared by the public that it serves.

The late-twentieth-century withdrawal of the state from the direct provision of social services in the United States and the increasing reliance within the public sector on private capital and market competition led the way for the marketization of public education witnessed over the past 25 years through the expanding charter sector. Proponents of charter schools extol the benefits of a system of schools regulated through the market pressure of parent choice.

In this framing, UCSN’s expansion can be understood as a reflection of the demand for charter schools among its Hispanic constituency in Chicago. However, UCSN’s skyrocketing debt burden and the risks that burden entailed for the entire network speak to a different logic at play. The increasingly speculative nature of the organization’s borrowing reveals an approach to growth shaped not by demand but by the aspiration of continued growth. This pattern suggests that the organization had begun valuing growth for its own sake over the potential social costs of missed growth targets. Advocates of an expanding charter sector point to charter school waiting lists as evidence of unmet demand in the market, arguing that charter schools require further access to capital to meet demand (Abraham et al. 2014; Rebarbar and Zgainer 2014). It is not at all clear, however, that UCSN’s expansion should be interpreted as having been driven by unmet demand. To the contrary, the spiraling debt burden that characterized the Network’s growth betrays a different process: one fueled by the pursuit of continued expansion.

Furthermore, the UNO case points to a set of dynamics associated with charter networks that are frequently not acknowledged by their proponents in the popular—and highly politicized—debates over the appropriate role for charter schools within public education. Charter advocates point to charter school failures as evidence that the system is working and that bad schools are being weeded out. However, when a network of schools is yoked together through the structuring of its financing, struggles at an individual school can threaten the whole network. This has the potential for making the already difficult task of closing charter schools even more difficult, if closure of a school imperils a larger network. Conversely, UCSN’s growth highlights the ability of a charter network to leverage expanding political influence and real estate assets into growth in a way that individual charter schools are not able to do. This has implications for how we conceptualize the charter sector: Is it a “market of choice” if some schools are able to grow by virtue of their asset base and are difficult to close by virtue of their financing structure?

Last, higher levels of debt place greater strain on charter schools and mean that the consequences of missing growth targets become more serious. This dynamic becomes more acute as an increasing share of debt is dedicated toward paying off or refinancing previous debt, as was the case with UCSN. As past obligations consume the proceeds of current debt, this necessitates some combination of continued revenue growth and future borrowing, and likely signals a reliance on debt as a condition of the network’s solvency. This financial arrangement places even more pressure on continued revenue growth, most obviously met through opening new schools and increasing network enrollment. In a debt-fueled cycle of expansion, missing growth expectations imperils not only future expansion but also the continued financial viability of the whole network.

The principles of a competitive market environment suggest that this risk enables growth and drives increased performance. We suggest that the assessments of risk in the bonds’ underwriting do not take into account the consequences for children and their families when a charter school they attend is forced to close—effectively transferring some of the burden of this risk onto their shoulders and raising questions about what is actually being leveraged in debt-financed growth within the charter sector. The marketization of public education and the withdrawal of the state from the direct provision of education have created a role for private capital in assessing the viability of educational institutions, strategies, and practices. In theory, the assessment of risk and performance incorporated into bond documents should be robust and objective. In practice, an underregulated market creates the opportunity for growth potential to dominate decisions about investment in charter schools and charter school networks. This is perhaps especially—and problematically—so in the educational sector, where the state’s obligation to educate children requires it to be a backstop in the event of a charter network’s collapse. In this way, in effect, the increased involvement of private operators and private capital in the public educational sector amounts to an off-loading of financial risk onto local communities and the state.

Finally, we consider how policy might deal with these risks at two levels, one situated within the existing charter school paradigm and one that challenges it. Our findings suggest a focus on accountability mechanisms and regulation of charter schools and their management organizations. The institutions tasked with oversight of the charter sector should be strengthened and funded at levels adequate for thorough review of charter schools as they come up for review. Charter school proponents argue that decentralized systems of school governance are more efficient, trimming bloated school district bureaucracies. However, if charter sector growth is not accompanied by the bolstering of administrative capacity to hold schools accountable, then local communities and families are put at greater risk of the consequences of underperforming or mismanaged charter schools. A robust institutional framework for charter school accountability should specifically include financial oversight. Policy makers should consider ways to limit the ability of charter operators to finance new schools by leveraging other schools—existing or planned—for capital borrowing. In addition, communities and families should be protected from overleveraged schools, perhaps by caps on the per-pupil debt burden that charter schools can carry. Future research is needed to explore the scales of the debt burdens that charter schools carry in different places and the implications of that debt on school governance, performance, and administrative review by the charter authorizer. Research should also draw out the various ways that schools are linked together through debt financing in other charter networks and in other cities.

Stepping beyond the case presented here and drawing out its implications as we have outlined them—the potential risks that are repositioned onto vulnerable communities—we suggest reconsidering school closure as an accountability mechanism. The simultaneous and often recursive strategies of public school closure, charter expansion, and charter closure fold into broader patterns of urban restructuring that increase inequality. A radical reform would treat the model of accountability via closure or threat of closure as a fundamentally problematic practice. A system of competitive school expansion that relies on and produces school closure and an educational landscape of instability and inequality should be seen as incompatible with any interpretation of the underlying charter school premise of democratic experimentation and innovation.

Finally, competitive market school reform ramifies the material, social, and political risks. That individuals and local communities would bear the consequences of the instability and risk inherent in the functioning of a marketplace of schools compounds the broader devolution of responsibility for educating children that has accompanied marketized educational reforms. An inadequately acknowledged consequence of using school choice as a motivating logic to shape the restructuring of public education is that, within an educational marketplace, if an individual fails to secure a good education, then the responsibility lies with that individual for not having made good choices. When the broader public is relieved of the responsibility of educating vulnerable children, it becomes much easier to frame schools as sites for capital investment. The logic and materialization of charter expansion may work recursively to undermine public education, increasing educational inequality and therefore new demands for choice, while erasing any legitimate claim that the production of this uneven landscape is anything more than a reflection of deficits within particular communities, households, and children.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge that some of the original research in the paper was funded with a grant from the American Federation of Teachers (AFT).