Abstract

We have little empirical evidence about the environmentally friendly, intention of owner-managers of small- and medium-sized enterprises (SMEs) in emerging country context despite recent developments of proenvironmental, practices. The main objective of our study is to address this gap by exploring the antecedents of environmentally friendly intentions among SME owner managers in, emerging market context. To achieve this objective, we test our, hypotheses in the textile–clothing industry in Tunisia. The textile–clothing industry represents high ecological risk due to the waste discharged into the environment. Our empirical observations confirm that the reasoned action approach is particularly robust to predict environmentally friendly intentions of SME owner-managers in an emerging market context.

Keywords

Introduction

In this study, we aim to draw attention to the environmental friendly intentions of the owner-managers of small and medium-sized enterprises (SMEs). Our study is motivated by the fact that the environmental effects of SMEs are more damaging to the natural environment than those of large companies. SMEs have significant environmental impacts. They represent an important part of the whole firms in Europe and in developing countries with negative cumulative environmental consequences (Gadenne, Kennedy, & McKeiver, 2009; Williamson, Lynch-Wood, & Ramsay, 2006). 1 Given their number dominance, their collective ecological footprint is highly significant particularly in industries such as leather tanning and textiles production. In addition, SMEs often do not have the necessary financial resources and organizational expertise to reduce the impacts of their activities on the environment (Jamali, Lund-Thomsen, & Jeppesen, 2017). Nonetheless, little research has focused on SME owner-managers and their environmental practices (Fitzgerald, Haynes, Schrank, & Danes, 2010; Longenecker, Moore, Petty, Palich, & McKinney, 2006; Roxas & Coetzer, 2012; Spence, Ben Boubaker Gherib, & Ondou Biwolé, 2007) or on the impacts of SMEs on the natural environment and strategies owner-managers adopt to reduce these effects (Aragón-Correa, Hurtado-Torres, Sharma, & Garcıa-Morales, 2008). This is a significant gap in the empirical research, as we know that SME owner-managers face different challenges from those of large enterprises (Lepoutre & Heene, 2006).

Moreover, the research on environmentally friendly intentions of firms during the past 20 years (Bamberg & Möser, 2007; Papagiannakis & Lioukas, 2012; Rodríguez-Barreiro et al., 2013) has significantly advanced our knowledge about the antecedents of environmentally friendly intentions of firms, especially in manufacturing industries (Álvarez Gil, Burgos Jiménez, & Céspedes Lorente, 2001). The researches, however, have been conducted mainly in developed countries, such as Europe and the United States (Ben Boubaker Gherib, Spence, & Ondoua Biwolé, 2009; Rice, 2006; Roxas & Coetzer, 2012; Starik & Marcus, 2000). Because the theoretical principles of the environment in developed countries are not necessarily valid in emerging countries (Nawrotzki, 2012; Rice, 2006; Roxas & Coetzer, 2012; Spence, Ben Boubaker Gherib, & Ondou Biwolé, 2011), the resulting bias toward firms in developed countries clouds our understanding of how the environmentally friendly intentions of SMEs are affected in an emerging country context (Oreg & Katz-Gerro, 2006).

Because emerging countries remain poorly studied in the field of the environment, our understanding remains vague about the factors that are related to the development of environmentally friendly intentions of owner-managers. To obtain insights into this issue, this study’s main objective is to explore the antecedents of environmentally friendly intentions among SME owner-managers in an emerging market context. As Hines, Hungerford, and Tomera (1987) indicate, environmentally friendly behavior seems to be positively correlated with environmental intention. In this well-established line of research, the notion of intention is often used by scholars (Lo, Peters, & Kok, 2012; Lülfs & Hahn, 2014) to investigate human conduct, because intention is the best predictor of actual behavior (Ajzen, 1991).

The rest of this article is structured as follows. In the next section, we present the theoretical framework and hypotheses. In the subsequent section, we describe the methodological design, sampling strategy, and statistical methods. In the penultimate section, we present the empirical results. Finally, we discuss the results in light of existing knowledge, as well as the limitations and perspectives for future research.

Theoretical Development

Intention refers to the will to act or behave in a certain way (Hines et al., 1987), and thus, environmental intention determines the way in which managers respond to environmental issues (Martin-Pena, Diaz-Garrido, & Sanchez-Lopez, 2010; Vazquez Brust & Liston-Heyes, 2010). Indeed, when investigating environmentally friendly intentions in SMEs, we generally focus on the managers and owner-managers of those SMEs. This focus on SME owner-managers is justified because they are key decision makers and define the strategic direction of their companies (Kreiser, Marino, & Weaver, 2002; Lumpkin & Dess, 2001) and generally play a crucial role in developing environmental strategies (Alt, Díez-de-Castro, & Lloréns-Montes, 2015; Aragón-Correa et al., 2008; Banerjee, Iyer, & Kashyap, 2003; Cordano & Frieze, 2000; Flannery & May, 2000; Schaltegger & Wagner, 2011; Sharma, 2000).

To understand how intentions are formed in the first place, we adopted the reasoned action approach (RAA) of Fishbein and Ajzen (2010), because of its detailed and consistent theoretical specification and the great amount of cross-disciplinary research devoted to testing, advancing, and criticizing the intention model (Armitage & Conner, 2001; Sheeran, 2002). In addition, the intention formation model of the RAA, earlier known as theory of planned behavior, has been widely used to study the environmental intentions of individuals (Cordano & Frieze, 2000; Flannery & May, 2000; Kaiser & Scheuthle, 2003; Oreg & Katz-Gerro, 2006; Steg & Vlek, 2009; Wall, Devine-Wright, & Mill, 2007). As a result, RAA has good predictive validity to explain various types of environmentally friendly behavior (Bamberg & Möser, 2007; Fielding, McDonald, & Louis, 2008; Lülfs & Hahn, 2014; Steg & Vlek, 2009), such as the choice displacement mode (Kaiser & Scheuthle, 2003; Oreg & Katz-Gerro, 2006; Wall et al., 2007), engagement in environmental activism (Fielding et al, 2008; Kaiser & Scheuthle, 2003), water conservation (Harland, Staats, & Wilke, 1999), treatment of wastewater (Flannery & May, 2000), prevention of pollution (Cordano & Frieze, 2000), recycling and environmental citizenship (Oreg & Katz-Gerro, 2006), and environmentally responsible purchase behavior (Follows & Jobber, 2000).

The core of the RAA is the notion that intentions have three conceptually independent determinants, namely, attitude toward the behavior, perceived norm, and perceived behavioral control (PBC; Fishbein & Ajzen, 2010). Attitude toward the behavior refers to the tendency to respond with some degree of favorableness (or unfavorableness) to the behavior in question. Perceived norm refers to the perceived social pressure to perform a specific behavior or not. PBC refers to the perceived ability to carry out a certain course of action. According to Fishbein and Ajzen (2010), these three theoretical antecedents should be sufficient to predict the formation of intentions. We next propose a conceptual model to explain how environmentally friendly intentions are formed using the RAA before testing it empirically in an emerging market context.

Attitudes and Environmental Intentions

Our interest in attitudes is based on the premise that environmental attitudes are one of the determinants of the environmentally friendly intentions of SME owner-managers (Lülfs & Hahn, 2014). Individuals with environmentally friendly attitudes are probably more committed to reduce the harmful effects of humans on the environment (Papagiannakis & Lioukas, 2012). As a support, earlier studies demonstrate that environmental attitudes are highly correlated with environmental intention (Cordano, Frieze, & Ellis, 2004; Papagiannakis & Lioukas, 2012) and significantly influence environmental behavior (Roxas & Coetzer, 2012).

To understand better the mechanism between attitudes and intention formation, it is important to understand how attitudes are formed in the first place. Attitudes are based on values that are more stable over time (Best & Mayerl, 2013; Follows & Jobber, 2000). According to the value theory of Schwartz (1992), values can influence individuals to develop environmental intention and evaluate environmentally responsible behavior through attitudes. Attitudes refer to values that indicate the degree to which individuals are motivated to promote the welfare of people and nature. In the framework of the RAA, attitudes are examined through their evaluative component. As pointed out earlier, Fishbein and Ajzen (2010) define attitudes as the degree of favorableness or unfavorableness of a person’s reaction to a behavior. Thus, scholars in environmental field are interested in the evaluative component of environmental attitude (Kaiser & Scheuthle, 2003; Lülfs & Hahn, 2014; Rodríguez-Barreiro et al., 2013). If we perceive that environmentally friendly behavior has positive consequences, our attitudes toward environmentally friendly behavior are automatically positive and influence our intention. For SME owner-managers, the positive consequences of the adoption of environmentally friendly practices can be related to increased performance and financial benefit (Aragón-Correa & Sharma, 2003; European Commission, 2011; Papagiannakis & Lioukas, 2012), new market development (European Commission, 2011), improved relations with social partners, customers and suppliers, adoption of a differentiation strategy, competitive advantage (Banerjee et al., 2003; Chan, 2005; European Commission, 2011), enhanced brand image and corporate reputation (Aragón-Correa & Sharma, 2003; Buysse & Verbeke, 2003; Papagiannakis & Lioukas, 2012), and increased involvement and motivation of employees (European Commission, 2011).

According to Cummings (2008), there should be no significant difference between environmental attitudes in developed and developing countries. As such, we could expect that SME owner-managers in emerging markets would also perceive environmentally friendly behavior, leading to potential benefits for their business, such as increased market share abroad (Labaronne & Gana-Oueslati, 2011) and financial performance (Dögl & Behnam, 2015). Based on the above discussion about attitudes and positive behavioral outcomes, we hypothesize the following about SME owner-managers in emerging markets.

Perceived Norm and Environmental Intentions

Social norms are said to help us understand voluntary participation in environmental organizations, because they positively influence environmental commitment (Garcia-Valiñas, Macintyre, & Torgler, 2012; Lokhorst, Werner, Staats, Van Dijk, & Gale, 2013; Osbaldiston & Schott, 2012), and contribute directly to the explanation of environmental behavior (Bamberg & Möser, 2007; Osbaldiston & Schott, 2012). Nevertheless, despite the theoretical relevance of social norms, their role in environmental intention remains insufficiently studied (Kaiser & Scheuthle, 2003; Lo et al., 2012; Lülfs & Hahn, 2014).

The RAA considers social norms by highlighting the role of perceived norms in explaining the formation of intentions toward particular behavior. Fishbein and Ajzen (2010) define perceived norm as perceived social pressure to perform (or not) a given behavior. These social pressures stem from beliefs that stakeholders do or do not want one to perform a given behavior (i.e., injunctive norm) and beliefs that important others are themselves performing (or not) a given behavior (i.e., descriptive norm).

The effects of perceived norms, and especially the influence of different stakeholders, on the behavior of firms have been well documented (Álvarez Gil et al., 2001; Aragón-Correa & Sharma, 2003; Banerjee et al., 2003; Buysse & Verbeke, 2003; Gadenne et al., 2009; Murrillo-Luna, Garcés-Ayerbe, & Rivera-Torres, 2008; Papagiannakis & Lioukas, 2012). According to this tradition, managers are conditioned by stakeholders to adopt environmentally friendly behavior (Aragón-Correa & Sharma, 2003; Cordano & Frieze, 2000). The pressure exercised by stakeholders can be very constraining, especially for firms that carry out polluting activities (Del Brio & Junquera, 2003b).

In contrast to injunctive pressures, the influence of stakeholders can be perceived as an opportunity. For example, intentions to obtain ISO 14001 certification (Del Brio & Junquera, 2003b) or improve legitimacy and market reputation (Papagiannakis & Lioukas, 2012) can be regarded as opportunities rather than normative obligations. Indeed, managers in the chemical industry (Fineman & Clarke, 1996) and oil and gas industry (Sharma, 2000) consider regulation to perform environmental practices as a competitive advantage, because they have the means to comply with regulation and internalize the costs involved (Fineman & Clarke, 1996).

Regardless whether the pressures of stakeholders are perceived as a constraining threat or as an environmental opportunity (Aragón-Correa & Sharma, 2003; Papagiannakis & Lioukas, 2012; Roxas & Coetzer, 2012; Sharma, 2000), these injunctive norms (Fishbein & Ajzen, 2010) could play an important role in the development of environmental activities in emerging markets. According to Dögl and Behnam (2015), regulatory, market, and social stakeholders influence managers’ implementation of environmental practices. In this way, we are interested in the impacts of social pressures coming from stakeholders on the environmental intentions of owner-managers. Based on the above discussion about perceived norms, we hypothesize the following about SME owner-managers in emerging markets.

The second determinant of perceived norms predicting environmental intention concern the effect of role models on implementing environmental practices, that is, descriptive norms (Fishbein & Ajzen, 2010). Role models are a key determinant in an entrepreneur’s decision making, because they create awareness and motivate people (Bosma, Hessels, Schutjens, Van Praag, & Verheul, 2012; Meek, Pacheco, & York, 2010). Based on the theories of role identification and social learning, Bosma et al. (2012) define role models as a common reference, which might stimulate or inspire other individuals to achieve certain goals. Thus, role models provide legitimization and encouragement to turn entrepreneurial ambitions into reality.

In an environmental context, several studies indicate the relevance of role models on motivating sustainability-related behavioral intentions. When observing others with whom they identify engaging in sustainable practices, individuals are more likely to follow suit (Lülfs & Hahn, 2014). Environmentally friendly business practices result from the observation of benefits achieved by role models’ environmental programs. Environmentally successful behavior supports the pro-environmental intentions of others (Steg & Vlek, 2009). Based on the above discussion about the influence of descriptive norms (i.e., role models), we hypothesize the following about SME owner-managers in emerging markets.

Perceived Behavioral Control and Environmental Intentions

Scholars in the environmental field have acknowledged the role of personal control as an important predictor of environmentally friendly intention (e.g., Lülfs & Hahn, 2014). Personal control is related to individuals’ knowledge and abilities, which affect environmental intention (Hines et al., 1987; Lo et al., 2012; Papagiannakis & Lioukas, 2012; Rodríguez-Barreiro et al., 2013; Steg & Vlek, 2009). For example, knowledge, skills, and abilities of managers have been found essential for the implementation of wastewater treatment practices (Flannery & May, 2000).

The RAA considers personal control through the concept of PBC, which refers to the “perceived ability to carry out a certain course of action” (Fishbein & Ajzen, 2010, p. 160). In essence, PBC is related to the presence or absence of perceived resources and opportunities. The presence of required resources and opportunities increases our perceived control about the behavior: “The more resources and opportunities individuals believe they possess, the greater should be their perceived behavioral control over the behavior” (Ajzen, 1991, p. 196). As such, PBC involves the degree of knowledge and mastery that an individual has of his or her ability, as well as the resources needed to achieve the desired behavior. As a move in the direction of understanding the role of PBC in explaining the formation of environmentally friendly intentions, we examine the role of (a) training, (b) past experience, and (c) perceptions of resource availability.

First, educational programs contribute to enhance environmental intention (Lülfs & Hahn, 2014). In support of this notion, in the past scholarly work, a significant relationship has been observed between environmental training and environmental commitment (Gadenne et al., 2009; Garcia-Valiñas et al., 2012; Rodríguez-Barreiro et al., 2013; Torgler & Garcia-Valiñas, 2007). For example, Duerden and Witt (2010) note that an international education program on the environment influences the environmental intention of American students.

In emerging countries, researchers suggest that more highly educated individuals possess higher levels of environmental knowledge, which translates into proenvironmental behavior (Vicente-Molina, Fernández-Sáinz, & Izagirre-Olaizola, 2013). Cummings (2008) supports the notion that environmental education favors environmental management. Vazquez Brust and Liston-Heyes (2010) contend that lack of specialized training of managers is an obstacle to achieve environmental intention in emerging markets. As such, we propose that training in environmental issues would help SME owner-managers to improve their perceived control, which in turn would contribute positively to the formation of environmentally friendly intentions. Hence, we hypothesize that:

Second, past behavior is decisive in explaining environmental behavior (Lo et al., 2012), because past behavior seems to increase a manager’s self-confidence and level of intentions toward environmentally friendly behavior (Flannery & May, 2000). Even though past experience might not directly explain future behavior, the absence of similar past behavior can strengthen resistance to new behavior (Ajzen, 1991). In support of this notion, Martin-Pena et al. (2010) confirm that managers’ similar past experience in the environmental field can be a determining factor in organizational strategies. As such, we propose that past environmental experience of owner-managers improves their PBC, which in turn contributes positively to the formation of environmentally friendly intentions. Hence, we hypothesize the following.

Third, perceptions about the availability of resources and conditions that are necessary for the expected behavior drive the formation of intentions (Ajzen, 1991). Managers actively participate in building their future through wise and appropriate control of the environment (Aragón-Correa & Sharma, 2003; Sharma, 2000). In addition, the role of a firm’s resources in the implementation of environmental strategy is well acknowledged in the environmental literature (Álvarez Gil et al., 2001; Aragón-Correa et al., 2008; Aragón-Correa & Sharma, 2003). For example, the lack of human resources is an insurmountable obstacle to environmental business development (Del Brio, Fernandez, & Junquera, 2007). Indeed, employees can play an important role in promoting ecoinitiatives and achieving competitive advantage based on environmental action in their firm (Del Brio et al., 2007; Ramus & Steger, 2000; Sharma, 2000).

Furthermore, the availability of adequate financial resources and incentives can affect owner-managers’ intentions to address environmental issues (e.g., Lokhorst et al., 2013; Osbaldiston & Schott, 2012). At least, the lack of adequate financial resources can be a major obstacle to becoming aware of environmentally sustainable practices (Gadenne et al., 2009). In the solar energy industry, state-sponsored incentives have been observed to be related directly to new firm entries (Meek et al., 2010). In addition, informational strategies (Steg & Vlek, 2009) and physical environmental conditions (Nawrotzki, 2012) seem to be related to environmental concerns.

Vazquez Brust and Liston-Heyes (2010) claim that a lack of different resources in an emerging country represents an obstacle to achieve its environmental intentions. On the contrary, employees trained in sustainable development contribute to the commitment of SME managers in this area (Spence et al., 2007), and the availability of financial resources and incentives influence managers’ environmental intentions (Lülfs & Hahn, 2014). As such, we propose that perceptions of the availability of resources improve the PBC of owner-managers vis-à-vis environmental issues, which in turn contribute positively to the formation of environmentally friendly intentions. Hence, we hypothesize the following.

A summary of the hypothesized model is presented in Appendix A.

Research Design

Sampling Procedure

Emerging countries face massive environmental challenges, such as polluted cities, contaminated water, and eroded soil (Dögl & Behnam, 2015). Our study explores the antecedents of environmentally friendly intentions among SME owner-managers in an emerging market context. To achieve this objective, we tested our hypotheses empirically in Tunisia. This country is among the emerging countries that have made the most significant progress in recent decades, measured by the Human Development Index (0.721; United Nations Development Programme, 2015). In addition, Tunisia is an emerging country (Ben Boubaker Gherib et al., 2009; Labaronne & Gana-Oueslati, 2011; Spence et al., 2011) where environmental policies have only begun to be implemented in the past 15 years (Ben Boubaker Gherib et al., 2009; Labaronne & Gana-Oueslati, 2011).

Indeed, in Tunisian’s framework for a recent program of environmental upgrading, priority has been given to the textile–clothing industry. To achieve the target of this program for this industry, it was important to identify the owner-managers that intend to implement environmental practices, because we know little about the process of environmental intention and environmental commitment in Tunisia (Labaronne & Gana-Oueslati, 2011; Spence et al., 2011; Tounés, Gribbaa, & Messeghem, 2014). Because of financial incentives and environmental support for the program of environmental upgrading, there is pressure on public authorities to recommend the program, and the rewards for undertaking environmental practices might influence environmental intentions and consequently might influence the environmental behavior of owner-managers. Thus, RAA seems particularly relevant. Its detailed and theoretical components can examine and measure consistently the effect of the factors listed above on environmental intention in the dynamic context of upgrading Tunisian’s environmental program.

The textile–clothing industry is promising for our study in general because the production processes in this industry pose high ecological risk and damage to the environment (Chan, 2005; Cohen & Winn, 2007; Williamson et al., 2006). According to Williamson et al. (2006), firms in this industry potentially contaminate water and air (waste and greenhouse gas emissions) and use large quantities of energy and raw materials in their production processes. In Tunisia, the textile–clothing industry represents 20% of the country’s GDP and employment. 2 In addition, the textile–clothing industry is an economic driver because of its foreign exchange earnings and the jobs it creates. Furthermore, the industry attracts foreign direct investment. The industry in Tunisia comprises 1,852 firms, or 32% of the manufacturing firms in Tunisia. The textile–clothing industry employs 34% of the total workforce in the manufacturing industry (179,000 jobs). 3

This study focused on textile–clothing firms in the region of the Sahel in eastern Tunisia, which contains about half the firms (889) in the country’s textile–clothing industry. 4 To obtain access to these firms, we used the database of the National Agency for Environmental Protection. Of all the potential 889 firms in the Sahel region, we removed 277 firms with foreign owners, because the parent company might have been the instigators of environmental strategies. In addition, we filtered firms according to the Organization for Economic Co-operation and Development definition of SMEs (i.e., 10-249 employees). As a result, 111 companies with 250 employees or more (30 from Sousse, 68 from Monastir, and 13 from Mahdia) were removed from the database. The total potential sample size was 501 SMEs.

Development of the Survey Instrument

The lack of research on environmental intention led us to conduct an exploratory study carried out among SME owner-managers. We interviewed 20 SME owner-managers in the textile–clothing industry in the region of the Sahel. We conducted semistructured interviews (Gavard-Perret, Gotteland, Haon, & Jolibert, 2008) to understand better the current situation of SME owner-managers vis-à-vis environmental issues. This step contributed to the operationalization of different measurement scales. In the second stage of the methodological protocol, we submitted the questionnaire to an expert panel formed by 11 people in the domains of corporate social responsibility and environment (Murrillo-Luna et al., 2008). In addition, we consulted seven researchers and four executives in the Tunisian Ministry of Environment and Sustainable Development. In the third phase, we tested the questionnaire with nine SME owner-managers. These actions helped strengthen the validity of items in the questionnaire by omitting and developing items for the measurement scales.

In the fourth and final stage, we finalized the questionnaire written in French. In Tunisia, French forms part of compulsory education at school. This language is very well mastered, in particular by those in their 50s. During the third quarter of 2012, we sent out the questionnaire to all (492) owner-managers of our sample, excluding 9 who participated in the testing of the questionnaire. Of these, 233 owner-managers responded to our survey. 5 After excluding seven erroneous and incomplete questionnaires, our final sample comprised 226 responses.

Measures

Dependent Variable

To measure the environmental intentions, we adapted the scale of Ajzen and Fishbein (1980), which is widely used to measure entrepreneurial intention in the field of entrepreneurship (see Appendix B). Principal component analysis indicates that environmental intention (EI) is a unidimensional variable; the three items relate significantly to the same component. They each have a factorial contribution coefficient greater than 0.90. In addition, the items give back 88.27% of the variance. The reliability of this variable is very good (Cronbach’s α = .93).

Attitudes

To develop a scale for environmental attitudes, we followed previous studies in the environmental field (Czap & Czap, 2010; Gadenne et al., 2009; Milfont & Duckitt, 2010; Rodríguez-Barreiro et al., 2013) and the results of the semistructured interviews of this study. We included 18 items (see Appendix B) to capture the positive outcomes of the expected environmental behavior. Each item was evaluated by the respondents on a scale from 1 (strongly disagree) to 6 (strongly agree). A factor analysis (oblim rotation) produced four distinct factors in the following manner.

The first attitude factor (ATT-DOMESTIC), composed of four items, reflects that environmental actions increase the legitimacy and improve the brand among domestic markets. The reliability of ATT-DOMESTIC is very good (Cronbach’s α = .90). The second attitude factor (ATT-INSTITUTIONS), composed of six items, reflects that environmental actions increase the legitimacy and improve the brand among governing institutions. The reliability of ATT-INSTITUTIONS is good (Cronbach’s α = .85). The third attitude factor (ATT-EFFICIENCY), composed of four items, seems to reflect that environmental actions improve the internal operations of the firm. The reliability of ATT-EFFICIENCY is acceptable (Cronbach’s α = .79). Finally, the fourth attitude factor (ATT-FOREIGN), composed of four items, seems to reflect that environmental actions increase the legitimacy and improve the brand among foreign partners. The reliability of ATT-FOREIGN is good (Cronbach’s α = .87).

Perceived Norm

We first set out to identify important referent individuals or groups whose approval or disapproval of performing environmental behavior (i.e., injunctive norm) is of concern for SME owner-managers in the Tunisian textile–clothing industry. Drawing on the literature on stakeholders and previous environmental research (Aragón-Correa et al., 2008; Banerjee et al., 2003; Buysse & Verbeke, 2003; Cordano & Frieze, 2000; Flannery & May, 2000; Henriques & Sadorsky, 1999; Murrillo-Luna et al., 2008; Sharma, 2000), we listed 11 categories of stakeholders: public authorities, public environmental organizations, competitors, foreign outsourcers, customers, subcontractors, environmental associations, media, employees, shareholders, and labor unions. However, the identification of the salient stakeholders of any firm is in large part an empirical question (Buysse & Verbeke, 2003). Our consultations with 11 experts and qualitative survey with 20 owner-managers showed that four types of stakeholders appeared to be irrelevant in the Tunisian textile–clothing industry: employees, shareholders, labor unions, and media.

In the survey, the respondents were asked to indicate the degree of importance they attach to the opinions of these stakeholders to undertake environmental measures or policy, with possible answers ranging from 1 (very low) to 6 (very high). Principal component factor analysis with oblimin rotation produced two components (see Appendix B). The first component (SN-INSTITUTIONS), composed of two items, expresses the importance the owner-managers attach to the opinions of public authorities (government and local authorities) and environmental associations. The reliability of this variable is very good (Cronbach’s α = .93). The second component (SN-COMPETITORS), composed of one item, emphasizes the importance the owner-managers grant to the opinions of competitors to implement environmental measures or policy.

Furthermore, the second potential source of perceived norms among owner-managers is the role models who have already implemented environmental practices (i.e., descriptive norm). Because the literature on environmental strategy and environmental psychology rarely addresses the impact of role models on environmental intention, commitment, or strategy, we were unable to identify a dedicated scale. Therefore, we developed our own scale to measure role models based on the qualitative survey with 20 owner-managers and consultations with 11 experts. We decided to use four different items to capture the extent to which respondents would consider other owner-managers in their industry as role models (see Appendix B). Factor analysis revealed a unidimensional variable (SN-ROLEMODELS). The reliability of this variable is very good (Cronbach’s α = .92).

Perceived Behavioral Control

We investigated the role of three different sources of such control: environmental training programs, past environmental experiences, and resources availability.

First, to investigate the role of environmental training (PBC-TRAINING), we adapted the scales of Tkachev and Kolvereid (1999) and Tounés et al. (2014) used in an entrepreneurship education context, and measured it using eight items on a 6-point Likert-type response scale (see Appendix B). The principal component analysis shows that PBC developed through environmental education is unidimensional. The reliability of this variable is very good (Cronbach’s α = .93).

Second, past environmental experience might be related to previous firms at which the respondent worked. We failed to identify any existing scales to measure past environmental experience. As a result, we created a two-item scale that measures potential prior experience of owner-managers in implementing environmental measures or policies (see Appendix B). The principle component analyses related to PBC gained through managing or participating in the implementation of environmental actions or policy produce unidimensional factor (PBC-EXEPRIENCE-OLD). The reliability of this factor is at the limit of acceptable (Cronbach’s α = .69).

Third, based on the existing literature (e.g., Álvarez Gil et al., 2001; Aragón-Correa et al., 2008; Aragón-Correa & Sharma, 2003; Buysse & Verbeke, 2003; Del Brio & Junquera, 2003a, 2003b; Lokhorst et al., 2013, Meek et al., 2010; Nawrotzki, 2012; Osbaldiston & Schott, 2012; Rodríguez-Barreiro et al., 2013; Steg & Vlek, 2009), resource availability was measured using eight items by distinguishing three types of resources: financial, advice and support, and human resources (see Appendix B for details). Principal component analysis with oblimin rotation indicated three principal components. The first component (PBC-RES-FIN), consisting of four items, reflects access to financing and specialized information. The reliability of this variable is at the limit of acceptable (Cronbach’s α = .70). The second component (PBC-PUBLIC), composed of two items, reflects access to public subsidies and benefits. The reliability of this variable is good (Cronbach’s α = .86). The third component (PBC-HR), composed of two items, reflects access to qualified workforce. The reliability of this variable is acceptable (Cronbach’s α = .78).

Control Variables

To control for effects that might otherwise explain intentions for environmental actions, we controlled for factors at the levels of owner-manager, firm, and industry. In terms of owner-managers, we controlled for gender and age; concerning firms, we controlled for size; and concerning industry, we controlled for domain of activities.

Gender (male = 1)

Gender environmental research claims that women are more likely to commit to environmental issues than men are (Hechavarría, 2016). According to Zelezny, Chua, and Aldrich (2000), women report stronger environmental attitudes and behavior than men do.

Age

The mainstream concept is that age is negatively associated with intention and behavior (Garcia-Valiñas et al., 2012; Nawrotzki, 2012; Oreg & Katz-Gerro, 2006; Rice, 2006; Torgler & Garcia-Valiñas, 2007). Following the example of Gadenne et al. (2009), we operationalized age into five age ranges. We created four dummy variables: (a) 31-40 years (AGE1), (b) 41-50 years (AGE2); (c) 51-60 years (AGE3), (d) 61 years and older (AGE4). The modality “younger than 30 years” is the reference category for the variable “age.”

Size

In keeping with previous research on environmental strategy (Aragón-Correa et al., 2008; Martin-Pena et al., 2010; Papagiannakis & Lioukas, 2012; Roxas & Coetzer, 2012), firm size (measured by number of employees) can have a significant influence on the level of undertaking proactive environmental practices, such that large organizations are more likely to be environmentally proactive than SMEs are. In addition, firm size might strengthen access to resources and ease stakeholders’ pressures. Large firms deploy more advanced environmental management, because they have flexible resources to invest in environmental practices, enjoy economies of scale for the valuation of waste, and are subject to higher levels of public audit (Álvarez Gil et al., 2001; Aragón-Correa et al., 2008).

Industry

We considered industry-specific variability by including the type of activity in which firms operate in the textile–clothing industry as a control variable. According to Banerjee et al. (2003), there is empirical evidence that the level of pollution and its toxicity vary from one industry to another. Five subsector dummy variables were included: (a) fading, coloring, and printing (FCP); (b) clothing manufacturing (CLOTH); (c) weaving (WEAV); (d) embroidery (EMBR); (e) and spinning and finishing (SPFINISH). We considered modality “finishing” as the reference category for this variable.

Statistical Analysis

In our statistical analysis, we adopt a stepwise multiple regression. This regression is recommended as the most appropriate and is particularly sensitive to multicollinearity. The interpretation of the regression results is performed at two levels. First, the model fit is estimated with the coefficients of linear determination R2 and the Fisher–Snedecor test. Second, we analyze the contribution of every independent variable to the explained variance of the model. This is assessed using beta regression coefficients and their associated student’s t (Gavard-Perret et al., 2008).

Descriptive Statistics

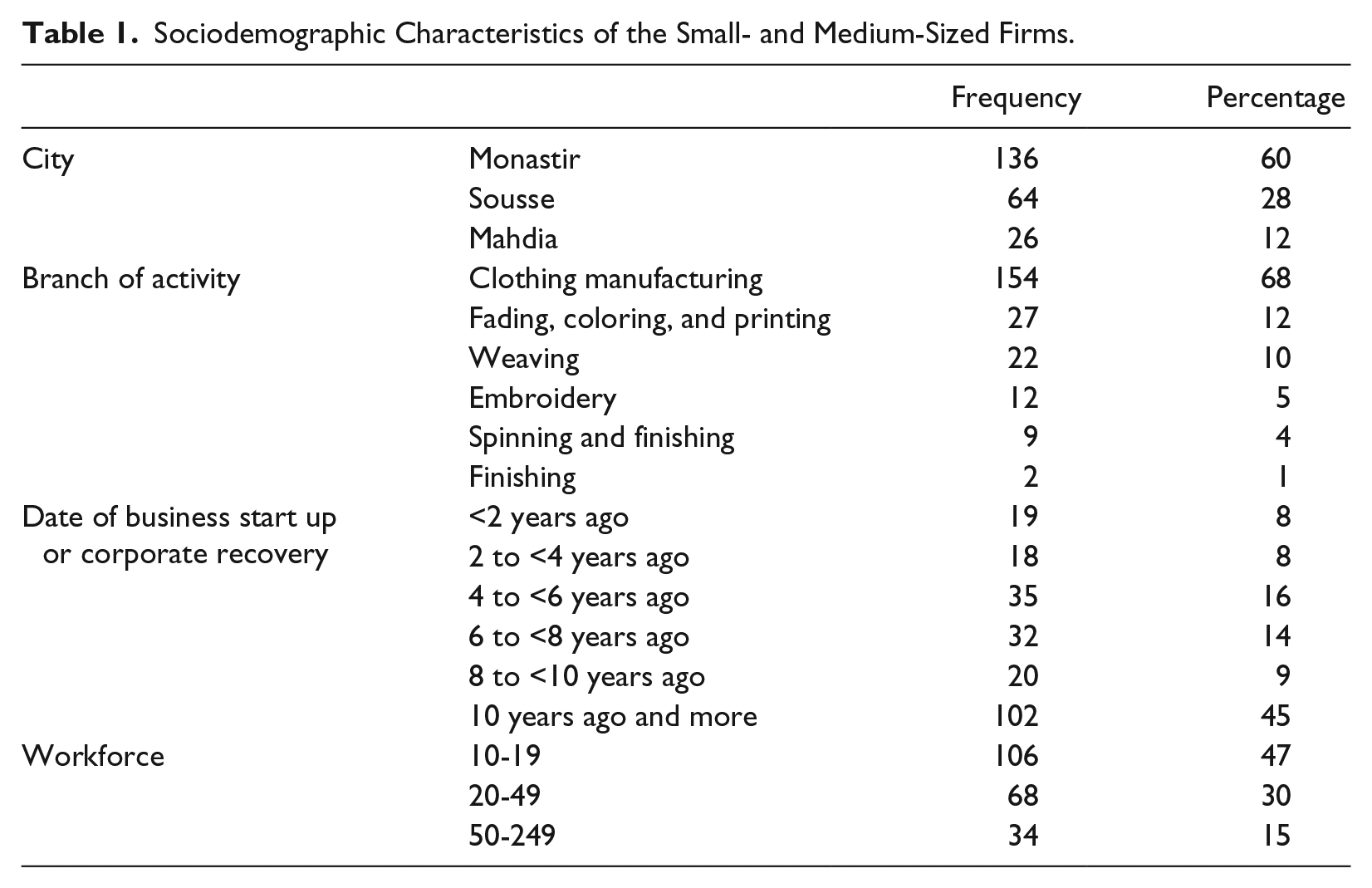

Table 1 presents some descriptive statistics on the surveyed SMEs. Around 60% of the firms are located in the city of Monastir. More than two thirds of the companies are in the industry of clothing manufacturing. More than half of the companies were created within the past 10 years. Almost 80% of the SMEs had workforces of 10 to 49 employees.

Sociodemographic Characteristics of the Small- and Medium-Sized Firms.

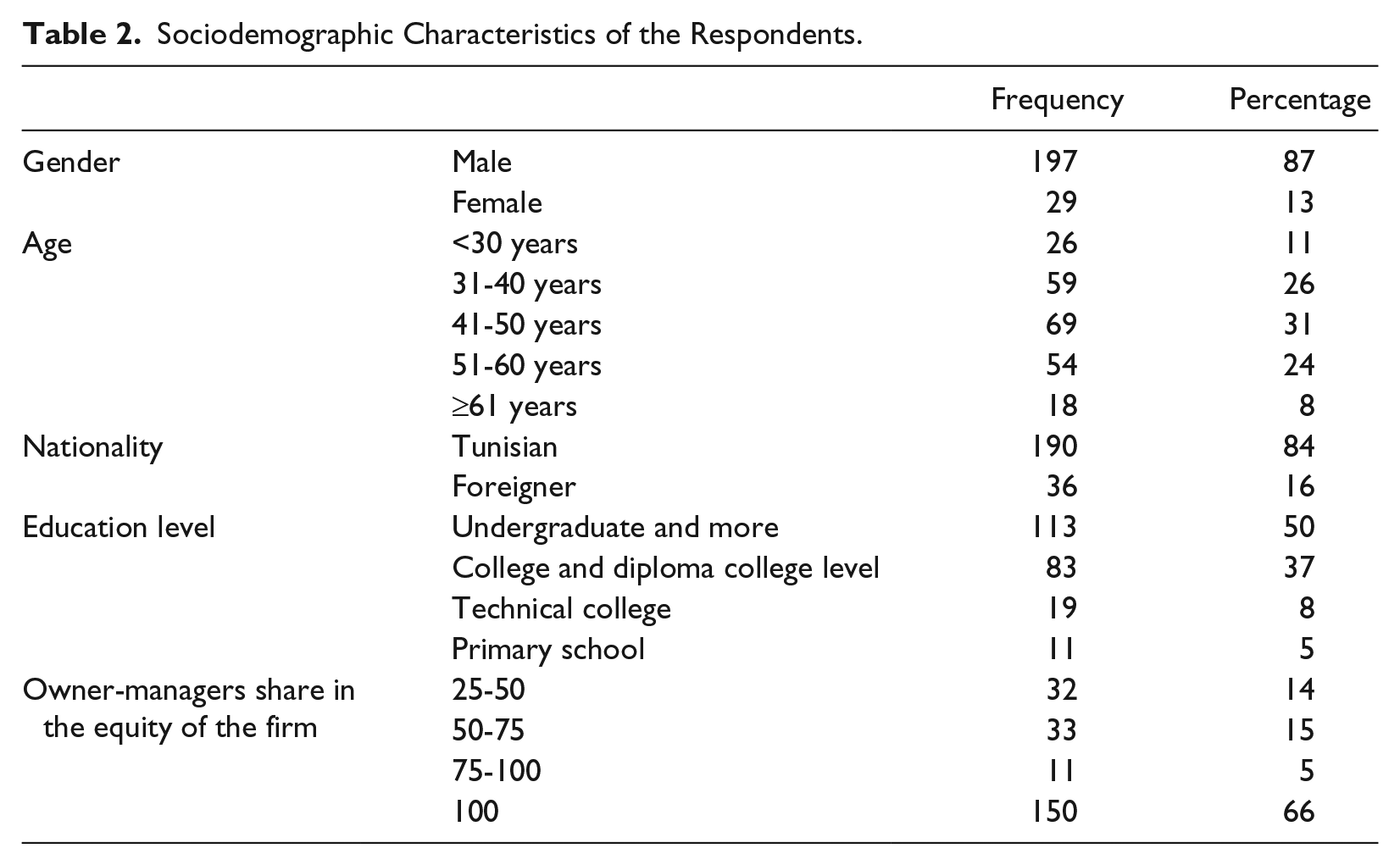

Table 2 describes the respondents and shows that the respondents are predominantly male (87%). The nonnegligible share of women (13%) is concentrated in a traditionally women-dominated branch of the industry, namely clothing manufacturing. The age profile of the owner-managers shows that the 41- to 50-year-old group has the highest number of respondents (31%). The respondents are mostly Tunisian (84%). The foreign respondents are French, Italian, Spanish, and Belgian. Half of the respondents have an undergraduate degree or higher level of education. Around 85% of the respondents hold the majority of the equity of their firms.

Sociodemographic Characteristics of the Respondents.

Empirical Results

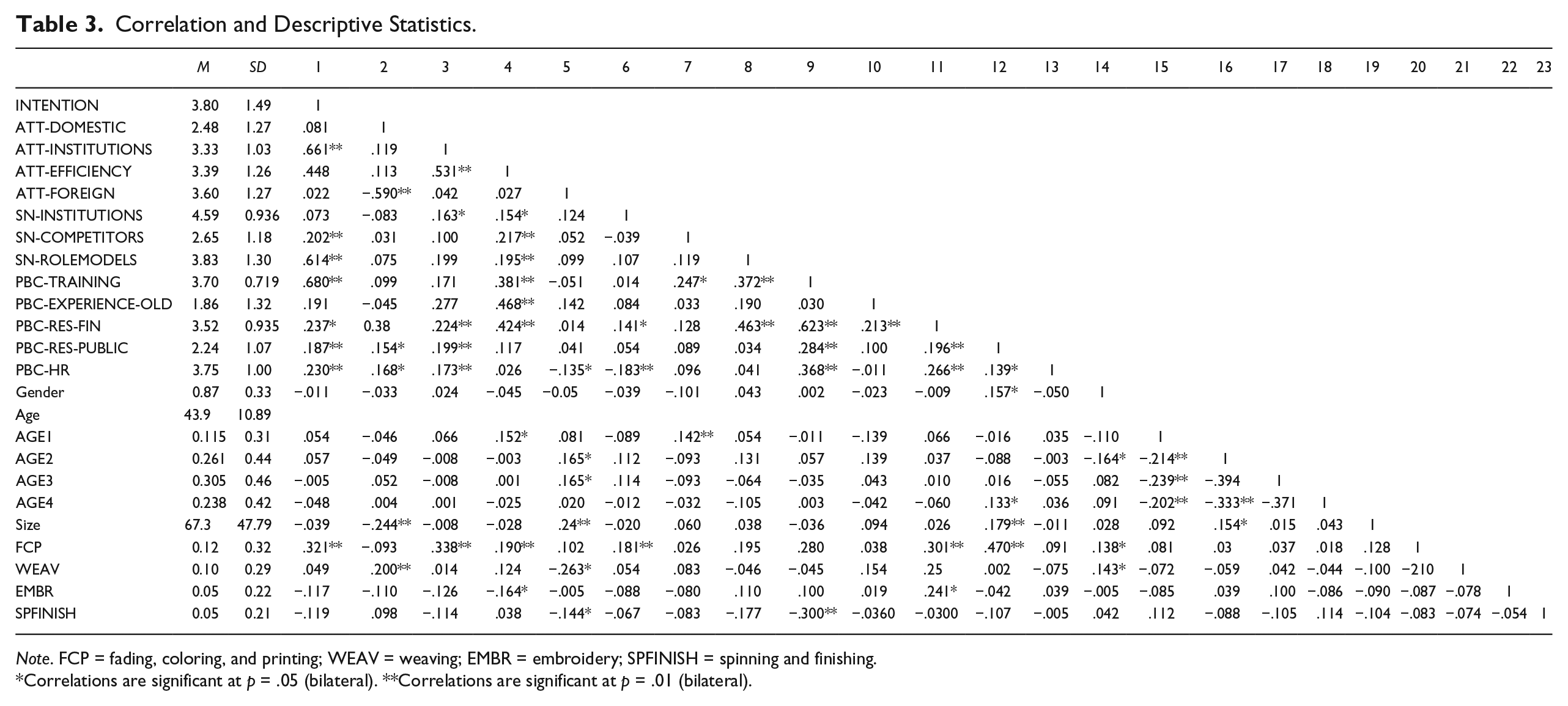

To investigate the potential risk of multicollinearity between variables, we run Pearson’s correlation test (Table 3). The highest correlation between the variables is 0.68, which is below the threshold of 0.70 (Gavard-Perret et al., 2008). Furthermore, we proceeded to two complementary statistical tests to eliminate risk of multicolinearity and common variance between variables. The first test concerns the variance inflation factors (VIFs). The VIF thresholds (maximum = 1.9) fall below 10, the recommended threshold of Lomax (1992), except for the variable clothing manufacturing (VIF = 18,004). We decided to omit this variable to avoid the effects of multicollinearity in the analysis.

Correlation and Descriptive Statistics.

Note. FCP = fading, coloring, and printing; WEAV = weaving; EMBR = embroidery; SPFINISH = spinning and finishing.

Correlations are significant at p = .05 (bilateral). **Correlations are significant at p = .01 (bilateral).

The second test is the common method variance, which calculates the possible effects of variance for the variables collected using Harman’s (1976) one-factor test. If common method variance were a serious problem in the study, we would expect a single factor to emerge from a factor analysis or one general factor to account for most of the covariances in the independent and dependent variables (Podsakoff & Organ, 1986). All the items used to create the main variables, a total of 54 items, were factor analyzed using principal axis factoring where the unrotated factor solution was examined, as recommended by Podsakoff, MacKenzie, Lee, and Podsakoff (2003). Kaiser’s criterion for retention of factors was followed. The sample size seemed to be large enough for the factor analysis, at least based on the Kaiser–Meyer–Olkin measure of sampling adequacy (KMO = 0.75).

Factor analysis indicates the existence of 16 factors with eigenvalues greater than 1.0. The 16 factors explained 74% of the variance among the 54 items, and the first factor accounted for 17% of the variance. Since several factors, as opposed to one single factor, were identified and since the first factor did not account for the majority of the variance, a substantial amount of common method variance does not appear to be present. Thus, we conclude that common method variance bias is not a threat to the validity of the results. One should bear in mind though that this procedure does nothing to statistically control for the common method effect: It is just a diagnostic technique (Podsakoff et al., 2003). Hence, the possibility of common method issues cannot be fully discarded.

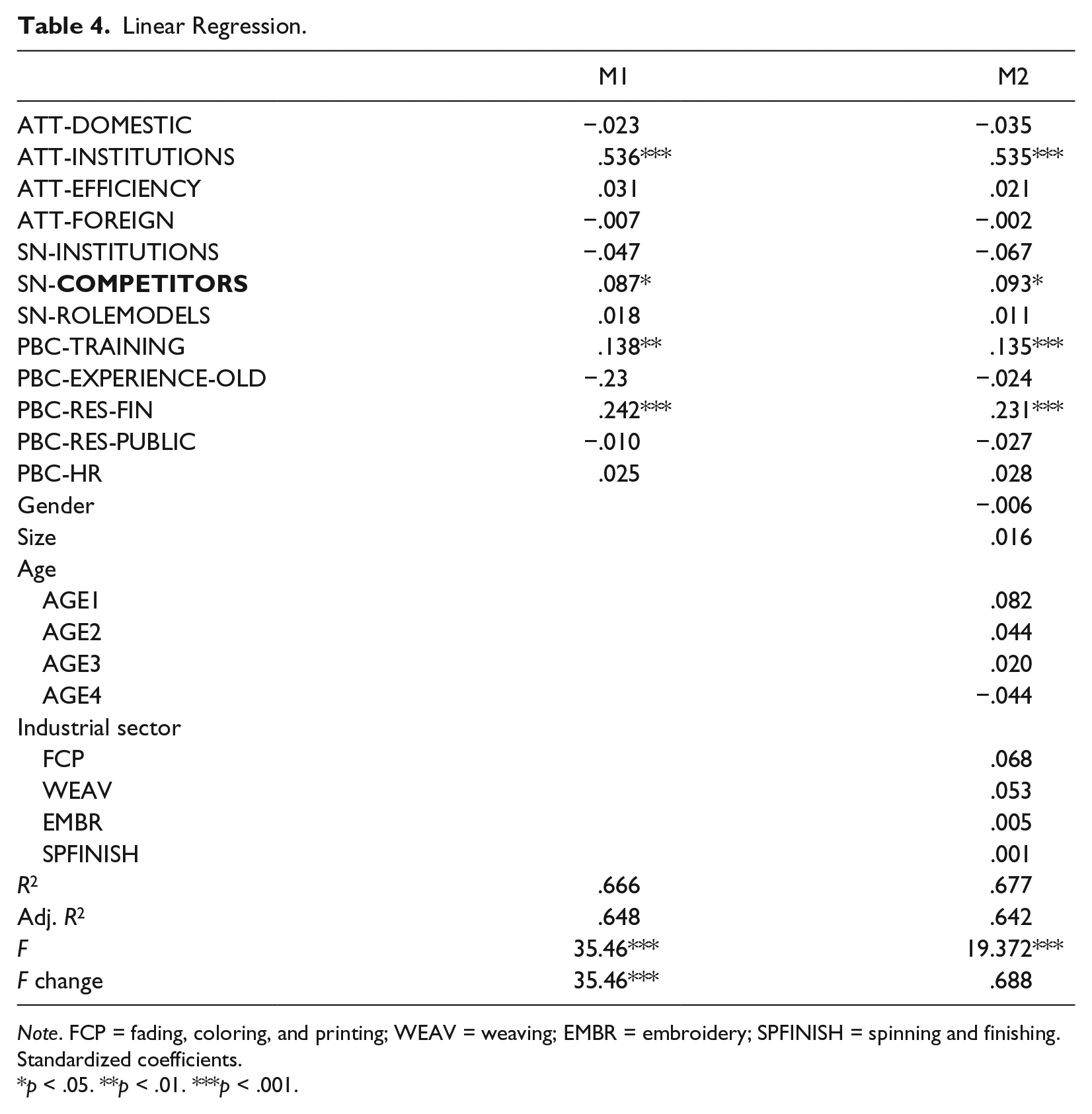

Table 4 presents the results of the regression analysis. The first model (M1) includes the main variables referring to attitudes, perceived norms and PBC. The second model (M2) reports the results when the control variables are added. The change in the F statistics from the first model (M1) to the second model (M2) is not significant, indicating that the control variables do not contribute significantly to the explained variance in the dependent variable. Indeed, the explained variance (adjusted R2) does not vary significantly (from .648 to .642) when all the control variables are included in the model. The coefficient of Fisher–Snedecor shows that the determination coefficient is statistically significant (Model 2: F = 19.372; significance <.000; for 28 and 197 degrees of freedom). Therefore, we conclude that the model fit obtained by the multiple stepwise regression is satisfactory.

Linear Regression.

Note. FCP = fading, coloring, and printing; WEAV = weaving; EMBR = embroidery; SPFINISH = spinning and finishing. Standardized coefficients.

p < .05. **p < .01. ***p < .001.

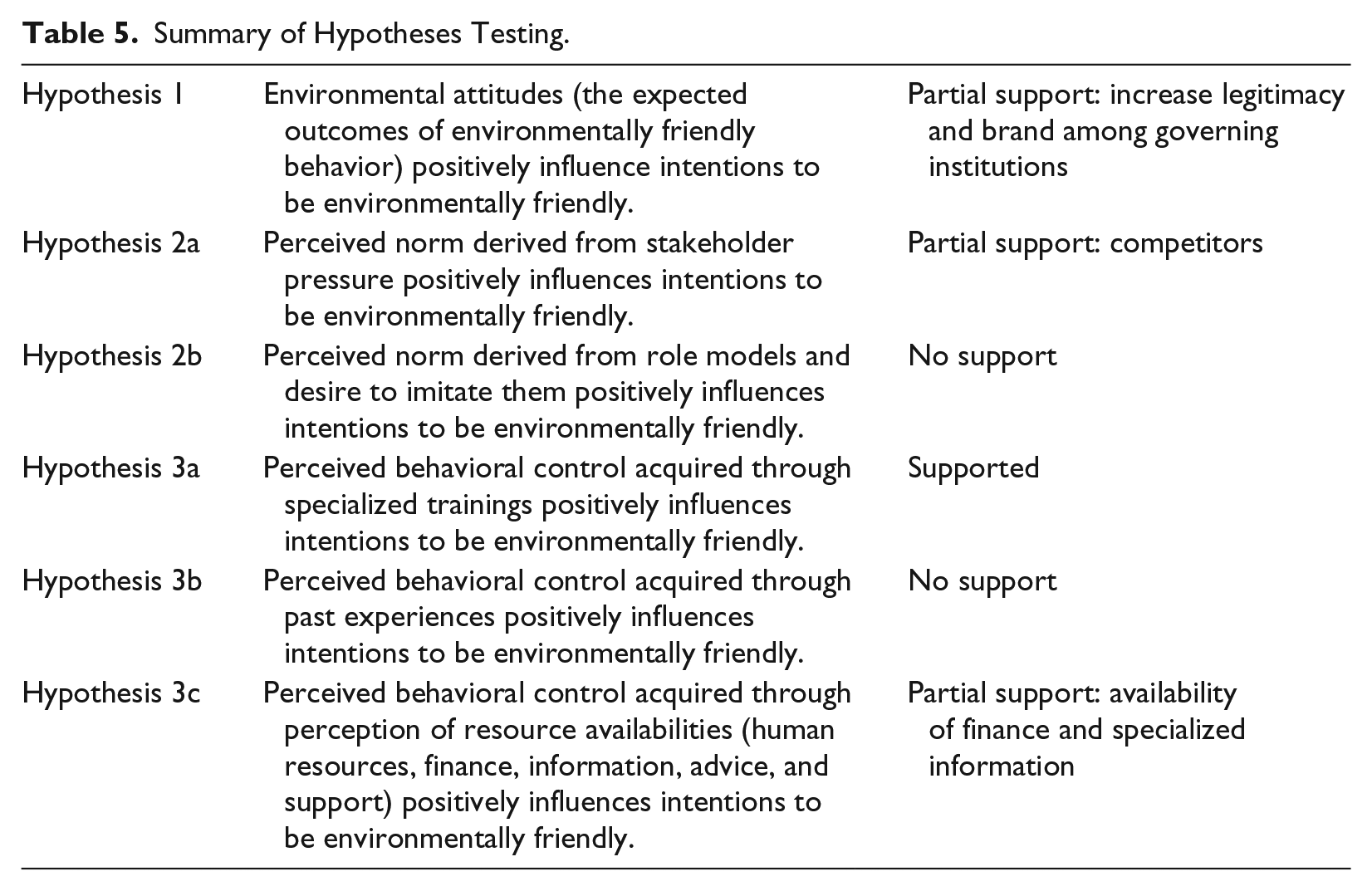

Hypothesis 1 predicts that environmental attitudes positively influence environmentally friendly intentions. As Table 4 shows, of the four different environmental attitudes, only one has a significant positive relationship with intentions. Indeed, it seems that environmental actions bring benefits in terms of increasing legitimacy and improving the brand among governing institutions. As such, Hypothesis 1 is only partially supported.

Our second set of hypotheses investigated the role of perceived norms in explaining the formation of environmentally friendly intentions. Hypothesis 2a considered the role of stakeholders (injunctive norm). As Table 4 shows, of the three stakeholder variables, only the one related to competitors has a statistically significant and positive relationship with the formation of environmentally friendly intentions. Indeed, it seems that perceived norms are related especially to social pressure coming from competitors, rather than from public authorities and environmental associations. This partially supports Hypothesis 2a. Moreover, Hypothesis 2b considered the effects of role models (descriptive norm). Our results failed to identify statistically significant support for this hypothesis. Indeed, we found no evidence that environmentally friendly intentions would be affected by role models and what they are doing.

Our third set of hypotheses investigated the role of different types of PBC in explaining the formation of environmentally friendly intentions. Hypothesis 3a considered the role of environmental training. As Table 4 shows, environmental training has a significant and positive relationship with the formation of environmentally friendly intentions. This supports Hypothesis 3a. Furthermore, Hypothesis 3b considered the role of past experience. As Table 4 shows, this variable turned out not to be statistically significant. As such, we found no support for Hypothesis 3b. Indeed, earlier environmental experience did not seem to be linked to the formation of environmentally friendly intentions. Finally, Hypothesis 3c considered the role of resource availability. Only the availability of finance and specialized information seemed to have a relationship with the formation of environmentally friendly intentions. We found no support for the two other resource availability variables. As such, Hypothesis 3c received only partial support. Table 5 summarizes the main results.

Summary of Hypotheses Testing.

As Fishbein and Ajzen (2010) have pointed out, even though a regression coefficient might be nonsignificant—an indication that the variable is not an important predictor of intentions—it is interesting to also check the zero-order correlations between the hypothesized predictor variables and intentions. As can be seen from Table 3, and contrary to the results related to regression analysis, the predictor variables of role models (perceived norm), access to public subsidies and benefits (PBC), and access to qualified workforce (PBC) all have statistically significant zero-order correlations with intentions. According to Fishbein and Ajzen (2010, p. 186) “If the predictor has a high zero-order correlation with intention, it is likely to have at least some influence on that intention.” As a consequence, we cannot rule out the possibility that some of the nonsignificant predictor variables in the regression analysis might have an influence on intentions in the absence of other factors.

Considering the control variables in the multiple regression, all the Beta regression coefficients indicate that control variables do not influence significantly the formation of environmental intention. In addition, the Table 3 shows that fading, coloring, and printing industrial activity has significant zero-order correlation with environmental intention. We take into consideration the possibility that this industrial sector can have a significant impact in the absence of others control variables.

Discussion

Our main objective in this study was to explore the antecedents of environmentally friendly intentions among SME owner-managers in an emerging market context, and therefore, this research contributes to clarify the intentional process leading to environmental behavior (Flannery & May, 2000; Martin-Pena et al., 2010). As such, environmentally friendly behavior can be understood through the formation of environmental intention (Lülfs & Hahn, 2014; Rodríguez-Barreiro et al., 2013). From a theoretical viewpoint, explaining the determinants of environmental intention is particularly interesting in the underresearched contexts of SME owner-managers and developing countries (Aragón-Correa et al., 2008; Jamali et al., 2017).

While few empirical studies have tested complete RAA models (Lülfs & Hahn, 2014)—earlier known as theory of planned behavior—we found such a model to be particularly robust in predicting environmentally friendly intentions in the Tunisian textile–clothing industry. A broader approach to environmental intention formation is likely to yield better forecasts for emerging countries (Vazquez Brust & Liston-Heyes, 2010). As such, our results support the applicability of the complete RAA model in explaining the formation of environmentally friendly intentions of SME owner-managers in an emerging market context.

The dynamics instilled by the evolution of institutional and regulatory frameworks (Labaronne & Gana-Oueslati, 2011; Spence et al, 2011) and the context of uncertainty in the Tunisian emerging market (Turki, 2014) do not seem to weaken owner-managers’ intention in the environmental field. Indeed, the RAA model explained around 65% of the environmental intentions of owner-managers in the Tunisian textile industry. The level of explained variance in our study is higher than that observed in earlier studies focusing on firms in polluting industries not only in developing countries (49% in Vazquez Brust & Liston-Heyes, 2010) but also in developed countries (19% in Cordano & Frieze, 2000; 42% in Martin-Pena et al., 2010). We take this as an indication that the complete RAA model seems to explain the determinants of pro-environmental intentions well in developing countries.

In addition, our study brings new insights regarding the specificities of owner-managers’ environmentally friendly intentions in the context of developing country comparing to developed countries. If environmental intention seems to be strongly influenced by attitudes, the nonsignificance effect of attitudes related to domestic markets and efficiency improvements characterizes owner-managers’ environmentally friendly intentions in Tunisian context. Owner-managers do not seem to care about customers’ environmental expectations, as it is the case in different countries in Europe (European Commission, 2011). Also, the productivity efficiency that can be gained through the environmental behavior is not perceived as positive consequence of environmental behavior comparing with Spain (Aragón-Correa et al., 2008), the United Kingdom (Williamson et al., 2006), and several countries in Europe (Garcia-Valiñas et al., 2012). In addition, perceived norms in the field of the environment seem to singularize the environmental intention of the Tunisian owner-managers compared with those of managers in developed countries. Indeed, contrary to developed countries such as Australia (Gadenne et al., 2009) and Greece (Papagiannakis & Lioukas, 2012), perceived norms related to government regulatory frameworks do not drive environmental intentions of Tunisian owner-managers. The importance of each antecedent of intention in the context of the Tunisian country is discussed in detail in the next subsections.

Behavioral Attitudes and Environmental Intentions

Although empirical evidence suggests that attitude alone is a poor predictor of environmental intention in developed countries (Vicente-Molina et al., 2013), attitude plays an important role among the different antecedents of environmental intentions in an emerging market context (Roxas & Coetzer, 2012; Vazquez Brust & Liston-Heyes, 2010). Indeed, our empirical observations in Tunisia suggest a strong positive linkage between environmental attitudes and the formation of environmental intention. Environmental attitudes represent the variable that has the strongest incidence of explanation of environmental intention. Specifically, attitudes related to legitimacy increase vis-à-vis public authorities and financial institutions (ATT-INSTITUTIONS) seem to be a significant factor in explaining the formation of environmentally friendly intentions among SME owner-managers. It seems that owner-managers who look for institutional legitimacy as expected outcome are more likely to adopt environmentally friendly practices in the future. The institutional void left by the Tunisian state does not seem to discourage the environmental attitudes of owner-managers to conquer public legitimacy through environmentally friendly intention. In addition, improving a firm’s image is widely cited as important by Tunisian managers in the industry ISO 14001 certification process (Gherib & Ghozzi-Nékhili, 2012). Financial institutions often have important direct effects on the decision making of top management. A climate of economic crisis in Tunisia seems to reinforce the relationship between the quest for legitimacy vis-à-vis the financial authorities and environmentally friendly intentions. This can be explained by the threat that the removal of financial resources could have on the firm and its negative signaling effect on other stakeholders (Buysse & Verbeke, 2003; Murrillo-Luna et al., 2008).

It was somewhat surprising to find that attitudes related to domestic markets (e.g., domestic legitimacy and domestic brand), efficiency improvements, and international markets (e.g., international legitimacy and international brand) had no significant effect on the formation of environmentally friendly intentions. Consequently, SME owner-managers seem to perceive that the desired environmental behavior would have effects neither on their firms’ domestic or international legitimacy nor on the efficiency of their internal operations. Because these observations directly contradict earlier studies on the positive impacts on environmental behavior of domestic (Roxas & Coetzer, 2012) and international legitimacy (Aguilera-Caracuel, Aragón-Correa, Hurtado-Torres, & De La Torre-Ruiz, 2010) and efficiency (Álvarez Gil et al., 2001; Banerjee et al., 2003; Bansal & Roth, 2000), we conducted interviews with a dozen owner-managers in our sample to learn more about these surprising observations. In essence, according to the owner-managers, Tunisian customers give no importance to the environmental quality of the local products they consume, which might explain why gaining domestic legitimacy is not a driver of environmental intentions in developing countries. Furthermore, the owner-managers pointed out that they often work with small European firms whose brands are not known and do not require environmental production conditions. The business-to-business market (vs. the business-to-consumer market) could explain why SME owner-managers’ attitudes do not affect their environmental intentions.

Perceived Norms and Environmental Intentions

Perceived norms, and especially injunctive norms, express the importance given to stakeholders’ expectations. According to our empirical observations, injunctive norms seem to play a weak role in explaining the formation of environmentally friendly intentions. In the Tunisian context, the multiplication of stakeholders (trade unions and consumer associations) and the evolution of their expectations over the past decade seem to have acted weakly on the environmentally friendly intentions of owner-managers. Indeed, competitors (SN-COMPETITORS) are the single stakeholder group that influences the formation of environmentally friendly intentions among owner-managers in a developing country context. This observation supports the stakeholder literature (Freeman, 1984), according to which competitive forces drive the adoption of environmental strategies (Álvarez Gil et al., 2001; Banerjee et al., 2003; Delmas & Toffel, 2004; Fineman & Clarke, 1996).

Within the context of our empirical observations, our results contradict the findings of previous research in developed countries, which suggests that the environmentally friendly intentions of owner-managers are driven by government regulatory frameworks (e.g., Aragón-Correa et al., 2008; Buysse & Verbeke, 2003). Indeed, in developing countries, such as India and China, regulatory pressure exerted by public authorities has a low impact on environmental commitment up to now (Spence et al., 2011) and on the implementation of environmental practices of owner-managers (Lülfs & Hahn, 2014). This finding can be explained by the low level of control and deterministic constraints of national and local government agencies in developing countries (Jamali et al., 2017; Rice, 2006; Roxas & Coetzer, 2012) concerning the environmental impact of activities of industrial firms. In Tunisia in particular, public authorities do not exercise the necessary controls when granting technical assistance, support, and grants (Gherib & Ghozzi-Nékhili, 2012).

Furthermore, it was somewhat surprising to find that perceived norms related to institutions (i.e., public authorities and environmental associations) were a nonsignificant factor in explaining the formation of environmental intentions. This finding contradicts earlier studies, which have concluded that environmental organizations and associations influence owner-managers to undertake environmental initiatives in the textile–clothing industry (Flannery & May, 2000; Papagiannakis & Lioukas, 2012). Our finding could suggest that environmental intentions have little to do with managing stakeholders in the regulatory sphere in the emerging market context. In other words, the weight of institutional pressures does not represent significant coercive constraints in emerging markets. This is especially true when regulatory devices are limited in number and not sufficiently known, as in Tunisia.

In addition, our empirical observations showed that role models do not influence environmentally friendly intention, which is contrary to earlier studies in developed countries (e.g., Steg & Vlek, 2009). In other words, descriptive norms (e.g., role models) do not seem to strengthen the perceived norms of owner-managers in an emerging market context. Furthermore, and contrary to earlier studies in Tunisia (e.g., Ben Boubaker Gherib et al., 2009), it was surprising to learn that the foreign outsourcers for whom the majority of our surveyed companies work do not seem to influence owner-managers’ intentions to implement practices that respect the environment. This lack of a relationship between descriptive norms and intention might be due to weakness of internal and external control systems by Tunisian managers. External pressure to engage in environmental practices has low impact in Tunisia, like in Egypt (Rice, 2006), where governance systems are largely based on interpersonal and informal relationships.

Perceived Behavioral Control and Environmental Intentions

According to our empirical observations, PBC plays an interesting role in explaining the formation of environmentally friendly intentions. Specifically, we found empirical support for the view that PBC influences the formation of environmentally friendly intentions through specialized training in the environment and sustainable development (PBC-TRAINING). As such, it seems that behavioral control in an emerging market context is built in particular through specialized environmental training, as in Argentina (Vazquez Brust & Liston-Heyes, 2010), Brazil, and Mexico (Vicente-Molina et al., 2013). The evolution of technology and the modernization of the textile–clothing industry in recent years in Tunisia reinforce perceptions about the importance of environmental training.

In addition, our findings demonstrate that access to resources and especially to banking finance, information and advice, and support from specialist organizations for a sufficient period (PBC-RES-FIN) contribute to explaining the environmentally friendly intentions of SME owner-managers in Tunisia. In emerging countries, the implementation of sustainable development is particularly influenced by the resource conditions and economic uncertainty that firms face (Vazquez Brust & Liston-Heyes, 2010). In periods of economic turmoil, such as that persisting in Tunisia since 2010, companies have fewer financial resources to change their environmental behavior. Thus, owner-managers perceive external financing (bank financing) and support from specialist organizations as important drivers for environmentally friendly intentions. This observation is in accordance with earlier literature. In an emerging market context, the absence of financial resources has been observed to be an obstacle to the commitment of owner-managers to social corporate responsibility (Gadenne et al., 2009; Labaronne & Gana-Oueslati, 2011).

However, while existing scholarly work seems to point out that we should take into account prior experience to understand environmental decisions (e.g., Papagiannakis & Lioukas, 2012), our empirical evidence points in the direction that perceived environmental abilities acquired through past experience (PBC-EXPERIENCE-OLD) do not influence the environmentally friendly intentions of SME owner-managers. While several empirical studies have reinforced the fact that past behavior directly causes subsequent behavior when attempting to initiate environmental practices (Cordano & Frieze, 2000; Garcia-Valiñas et al., 2012), past behavior seems to make a significant contribution to the prediction of the future environmental behavior only when circumstances remain relatively stable and past behavior resembles future behavior (Harland et al., 1999). In support of this notion, Lo et al. (2012) point out that experience in recycling a certain material does not automatically lead to recycling and waste management behavior for other materials. Given our failure to link past behavior to environmental decisions, it might be the case that the past environmental experience of the sampled SME owner-managers is different from what they intend to implement in the future.

Practical Implications

While owner-managers are concerned about the impact of their firms on the environment, they are not necessarily fully and reliably informed about environmental challenges and their consequences for nature and humans. From a managerial viewpoint, we propose actions for SME owner-managers in emerging markets to overcome this lack of information and communication. To provide adapted support for production processes in industries with high ecological risks (e.g., the textile industry in our study), it is necessary to intervene upstream by sensitizing these owner-managers about the environmental issues of their industries. Because environmental awareness is a factor that strongly influences environmentally friendly intentions, we recommend that initiatives aiming to increase awareness through seminars and connected events are given a high level of support. However, the implementation of environmental awareness and accessible information about environmental practices remain modest in many emerging markets. For effective sensitization, the point is not only to inform managers about how to comply with legislation but also to give them information on the benefits of environmental measures for firm competitiveness. The challenge is to provide a framework for developing environmental integrative strategies exceeding the legal conformism and the coercive pressures of government.

In addition, our study reveals that public authorities should promote access to financial resources in emerging markets to foster the development of environmentally friendly intentions among SMEs. If policy makers provide financial incentives for innovative pollution prevention for environmental approaches, a company would be more likely to invest in a proactive environmental strategy. Moreover, authorities in charge of the environment should pay particular attention to specialized training in the environmental field. Environmental training programs aim to change environmental intentions by increasing environmental knowledge.

Finally, because SME owner-managers seem to be conditioned by what their competitors do, it would be important to consider this social pressure when designing interventions for encouraging environmentally friendly behavior. For example, in addition to implementing large-scale public campaigns to encourage as many SME owner-managers as possible to adopt environmentally friendly practices, it would be effective to convince selected SMEs to adopt such practices. A few industry examples could press other competing SMEs to follow the same direction in adopting environmentally friendly practices, especially if those few examples are made publicly known.

Limitations and Directions for Future Studies

Generalization and interpretation of our results are subject to certain limitations. For the obvious reason of the homogeneity of the sample surveyed, the determinants of environmentally friendly intentions revealed in this study were appropriate only for the industries studied. Beyond the limitations of the temporal stability of environmental intention (Lokhorst et al., 2013), the variety of the types of environmental behaviors and efforts required to perform them (Osbaldiston & Schott, 2012) limit the representativeness of our results to the environmental issues studied in the research. Furthermore, another limitation of the research is related to the nature of the country for which the data were collected (Buysse & Verbeke, 2003). The findings express the perceptions of polluting firms operating in Tunisia and might not be generalizable to other developing economies, where cultures are different and industries might face different challenges and environmental concerns (Vicente-Molina et al., 2013).

Furthermore, with regard to our methodological design, even though we carried out an exploratory study with interviews for the development of the principal data collection instrument, the data used in the statistical analysis were collected from single respondents and were cross-sectional in nature. We did our best to estimate common method bias to overcome the dependence on single respondents but could not improve the cross-sectional nature of our data. We hope that future studies could explore our findings using more longitudinal research designs whereby the measurement of the independent variables and the dependent variable could be separated in time. With longitudinal designs, future scholarly works could integrate realized behavior into their theoretical models (i.e., intention–behavior linkage). To delineate clearly between environmentally responsible intention and behavior (Follows & Jobber, 2000), future research should explore the conditions under which pro-environmental intentions among SME owner-managers transform into actual behavior in their SMEs; we could not include this objective in our study owing to the cross-sectional design of our empirical work.

Last, some of our measurement scales are not validated by previous research. For example, to evaluate resource availability and the effect of previous experience on environmentally desired behavior, we relied only on expert consultations and qualitative study of owner-managers in our empirical context. We encourage future researchers to improve on our approach by verifying whether the measures identified through a qualitative approach are context sensitive.

Footnotes

Appendix A

Appendix B

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.