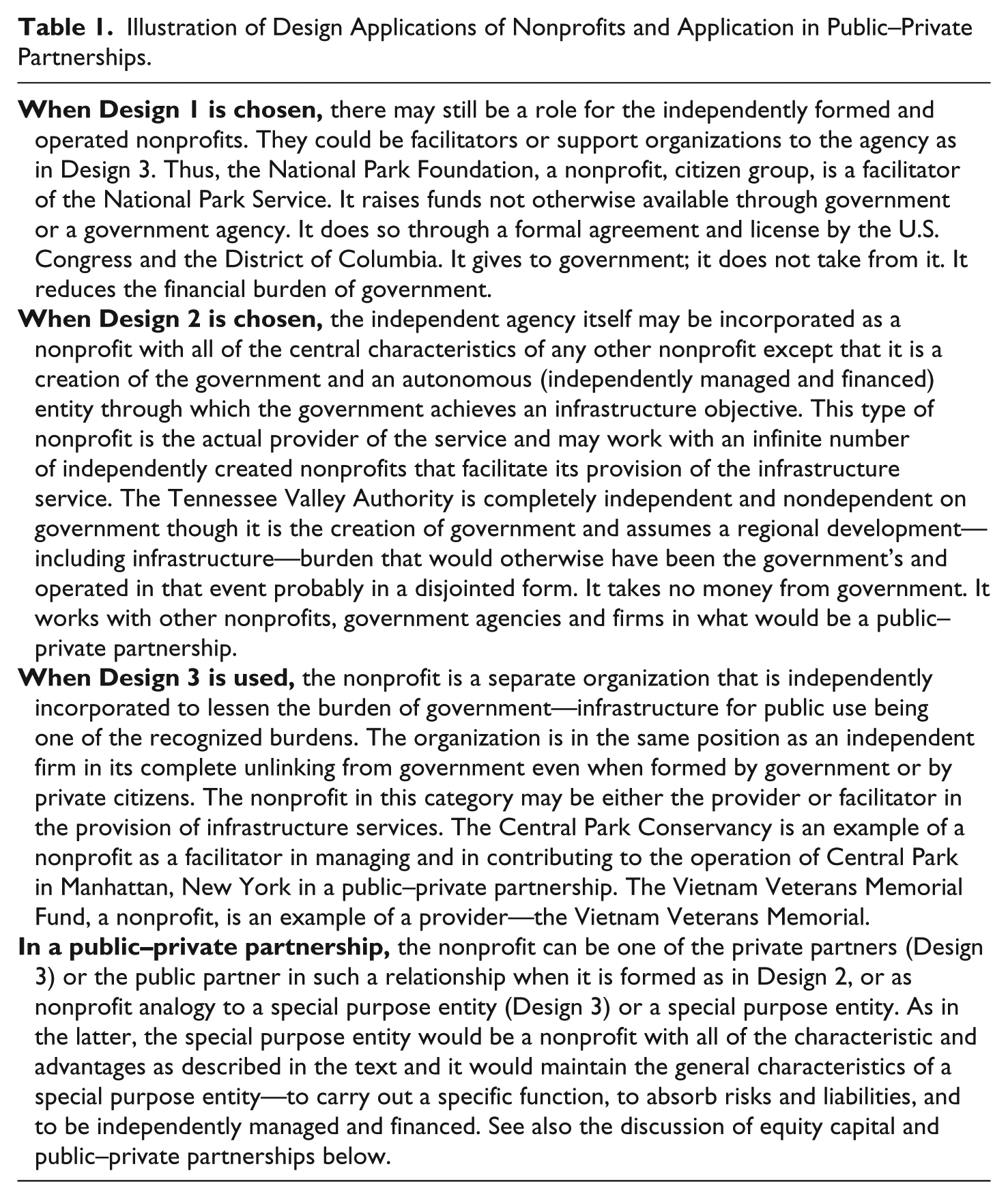

Abstract

From a policy, practice, and theoretical perspective, this article promotes the use of the nonprofit to lessen the financial burden on government in advancing the wellbeing of the general public. The burden in this article is the cost of providing critical physical infrastructure for the benefit of an entire population or jurisdiction. How can the nonprofit materially lessen this financial burden? How may the trade-off between government agency appropriations and tax expenditures to nonprofits favor the use of a nonprofit? What about accountability to citizens and to government-why is this not an obstacle? Why is the nonprofit a versatile design for the provision of infrastructure either singularly or in any combination of public- private partnership? Why should this strategy be embraced if infrastructure requires a large upfront and continuous flow of cash and debt? Could this strategy bring infrastructure online quicker and at a lower government cost?

Keywords

The advancement of the general welfare of the population is one of five purposes of government stated in the Preamble of the Constitution of the United States. Therefore, if and how governments discharge this duty is more than a party, political, or academic issue and is a duty of the federal government, and by extension through their adoption of a similar Preamble and their allegiance to the Constitution, of each state and of each municipal government.

The concept of general welfare in the Preamble includes advancing the economic, social, political, and general happiness of the population—one way being through the provision of infrastructure. In

In addition, the Constitution empowers the U.S. Congress (and by extension state and local legislatures) to pass legislation in regard to the provision of infrastructure (the 10th Amendment). Furthermore, in Article 1, Section 8 (the welfare or the general spending clause) it empowers the Congress to raise funds through taxes, debt, and various fees to finance the attainment of the general public welfare. The government’s duty to provide, to pass legislation to provide, and to raise the funds to provide infrastructure is therefore grounded in the Constitution as a nondelegable duty—one from which the government cannot free itself.

Alternative Organizational Designs for Carrying Out the Infrastructure Duty

To proceed to provide for the general welfare of the population through infrastructure, the government may choose at least from three discreet, noncommercial organizational designs. Organizational designs are the attributes of the institutions created to solve public problems as in Ostrom (2005, 2012). The organizations are the units that may form networks, collaborations, or partnerships such as the public–private partnerships. Three noncommercial organizational options from which the government may elect are discussed here:

Design 1: The Government Can Do It Itself

The government may organize for this activity by carving out a specific segment of its organizational body and by calling it a ministry, a department, or agency to which it assigns a class of infrastructure and its services; for example, the transportation department. These agencies are part of the whole government and rely on the central government for appropriations and may also rely on it for contract negotiation and resolution, the defense or launching of suits, for policies they will enforce, rules and codes of employment, and any contract dealing with the infrastructure. These agencies are in a ministerial or a servant–master relationship to the government of which they are a part. Therefore, they are subordinate parts and not treated by law or accounting as separate and independent but as extensions of the government itself and therefore the latter is liable for the former and the former is controlled by the latter.

Special purpose districts are a variation of government doing it. In this case, the government creates a subdivision within its jurisdiction to do it. These subdivisions are classified as special purpose governments 41 CFR 105-50.001-4 at https://www.law.cornell.edu/cfr/text/41/105-50.001-4 or units. The U.S. Census Bureau defines a special district: All organized local entities (other than counties, municipalities, townships, or school districts) authorized by state law to provide only one or a limited number of designated functions, and with sufficient administrative and fiscal autonomy to qualify as separate governments; known by a variety of titles, including districts, authorities, boards, and commissions—according to the assumed benefits to the property affected by the improvement. (https://www.census.gov/govs/definition/index.htm/#s)

Hence, a special district may be organized around an infrastructure as its core mission; for example, a transportation authority. The special district’s power to tax which is usually based on the property tax, to set infrastructure prices, to exercise policing powers, and eminent domain are granted when needed to carry out the requirements of that infrastructure in the public interest within that jurisdictional geographic space that constitutes or surrounds that special district. The geographic space does not have to be contingent or even isolated to one jurisdiction. Nevertheless, the power is limited and restricted and does not supplant the powers of the general government of which the special district is a part. Thus, all special districts do not have the same powers including taxing powers and powers of eminent domain even in the same state or need them (the Mosquito district in Minnesota). See New York State, https://www.assembly.state.ny.us/comm/StateLocal/20,070,823/specialdist.pdf and see Washington State, http://mrsc.org/Home/Explore-Topics/Governance/Forms-of-Government-and-Organization/Special-Purpose-Districts-in-Washington/What-is-a-Special-District.aspx. These are determined by the local and state legislatures without whose assignment of authority the powers cannot be exercised by the special district or any other entity.

This Design 1, the carving out of the bureaucracy or of jurisdictional space, is a choice that is indicated in these distinct circumstances: when the project cannot finance itself, when prices cannot be charged, and when exclusion of nonpayers is not possible or where the externalities are so extensive that most taxpayers will receive some benefit at times arguably larger than their marginal tax cost to support the infrastructure—commonly, where the market would fail to provide or sufficiently approximate an optimal solution. A main road is an example. But, in the case of special districts, it is indicated when the property tax assessment is sensitive to infrastructure addition or improvements in a specifically designed geographic area. Therefore, unlike general taxes, special districts can mesh benefits presumed to be received equally by all beneficiaries located in a geographical space with a specific tax to cover costs. Location and not the specific amount of use is what matters.

The organizational management of the district, however, can be an association of the residents and businesses within the geographic space—a nonprofit organization specifically created for that purpose and through which the residents express their preferences first by choosing to be there and second by choosing among options once there. Downtown commercial districts are often created this way for infrastructure improvements and financed by a tax increment strategy which assesses the increase in value associated with the improvement.

Design 2: The Government Can Create an Independent Agency or Authority to Do It

In Design 2, the agencies or authorities are independently incorporated organizational entities functioning as instrumentalities of the government that created them to carry out a specific mission or class of mission such as a bridge or bridges, a highway or highways. In their design, they may vary in how independent they are from the government that created them so as to isolate and to organize in one unit the burdens of risks, liabilities, and management. These too are nonprofits that may or may not be technically (legally and accounting-wise) be categorized as government depending upon the degree of independence they have from the government(s) that created them. The greater the dependency even as a guarantor of their debt—the less the burden they remove. Hence, Design 2 allows for variations in independence or dependence and, as a consequence, variations in the amount of burden that can be lessened.

These organizational units may depend upon the government for a budget, financing, contracting, hiring, or to support or to issue or guarantee debt, for hiring and contracting, for operating decisions, and for their liabilities or pensions and medical benefits. The more dependent they are on the government that created them, the more they are deemed under accounting and legal convention to be controlled by that government and the less the burden they remove. In short, the less applicable is off-balance sheet financing of the burden—because the government retains them, just in a different unit of its corpus as in Design 1.

Accordingly, to be deemed as independent, a reasonable person must be able to conclude that the agency is not under the control of the government by having a board of its own and a vast reach of discretion over operating policies, budgeting, earned revenues, debt, expenses, investments, contracts, terms of employment, its ability to sue and be used, and its ability to acquire property consistent with its mission. I have cataloged these according to U.S. and international conventions in Bryce (2017b, Chapter 5). The agency must at the same time be denied powers restricted to a government or allowed to exercise them in a very constrained way. They cannot be a vehicle through which the government transfers its powers but one to which the government transfers a burden and only those powers in limited form that are necessary for operating success. They cannot, for example, tax, exercise unrestricted policing powers or powers of eminent domain—all decidedly nondelegable powers assigned to a government. If they should, they may be classified as government as special districts are in Design 1.

Independence is necessary when operating culture and conditions are different from that of government even when the objective is the same—to serve a public good. The maximum of independence (and therefore burden relief) occurs when the infrastructure assigned to the independent agency can fully finance itself through debt and user prices that can cover all costs including the carrying cost of the debt plus a reserve for repairs and contingencies; the activities are highly specialized and would be a strain on the capacity of the government or its ability to attract qualified staff; creditors are willing to assess the project and organization positively; there is a need to minimize the uncertainties due to political decisions (called policy risks) or appropriations; users are sufficiently dependent that they will be heard; and when users have a vested interest in how well the project works—so that they would require meaningful accountability individually or often through the formation of a nonprofit that does.

When these elements of independence come together in an organization formed by government they may carry the labels: autonomous, independent, authority as an initial clue that they are nonprofits outside of the corpus and management sphere of government. Then, the question is which of these essential powers—particularly to self-finance through earnings or debt or contributions—does it have and what decision-powers does it have. The greater of these, the greater the “facts and circumstances” indicate autonomy or independence as an institution—and not the government doing itself and this becomes Design 2.

Design 2 is indicated where the infrastructure is large, critical, and complex to manage and operate and where the control by government may create serious inefficiencies, uncertainties, and failure—where the operating rules of government (as opposed to government oversight) is not efficiently applicable. The Tennessee Valley Authority and the Panama Canal Authority are a domestic and foreign example but so too are many transportation, water and sewer systems, and ports. These too are special purpose entities, but they are nonprofits outside the government corpus unlike Design 1. They are independent and make independent decisions about management, contracting, employment, pricing, financing, debt specifically—all specifically related to the infrastructure rather the government’s general funds, budgets, or processes while operating within the laws. Hence, this independence protects the government and the people and removes uncertainty that would affect users and lessens the burden of government. The government sets the rules and performs oversight just as if the entity had been a privately operated power plant. In general, when self-sufficiency is possible, the more independent the unit in Design 2 may be and the lower the burden left on the government. But the more important do the mechanisms of accountability and responsibility become.

Design 3: The Government Can Create a Nonprofit or Encourage the Creation of One by Citizens to Do It

These nonprofit entities in Design 3 are not extensions of government or dependent upon government in the strong form as in Design 1 or the very weak- to nonexistent form as in Design 2 even though they too may be formed by governments and also by citizens. They are not subdivisions of governments or special purpose entities as in Design 1. Rather, they are totally independent of government as free standing corporations created in accordance with nonprofit corporate law and given tax exemption under the Internal Revenue Code 501 (c) and not because of a relationship or control by government.

The government may sanction, cooperate, or regulate these nonprofits for purposes of the infrastructure. It sanctions it by acknowledging that the burden is a real burden of government and by entering into an agreement (not necessarily a contract) as to how and what specific infrastructure burden the nonprofit will lessen for the general public. It also gives it license to perform that function and reviews and approves planned programs or activities to be sure that they are consistent with the overall intent. It cooperates with the nonprofit by scheduling and by offering facilities if available, approving specific infrastructure related tasks that the nonprofit elected to do for and with the infrastructure and often by providing in-kind services.

The government does not have to commit any funds or financing and often is the recipient of it from these organizations—especially as they may serve as special fund-raising vehicles or ones generating excess profits from their activities. Under these agreements, the government is not signing a quid pro quo contract unless it wants to do so. It is signing a permission and an agreement as to what this permission requires. Finally, it regulates the organization, it does not control as in Design 1 or those dependent organizations in Design 2, but it does so as it regulates but does not control the power plant owned by a private corporation. It regulates for public safety and adequacy of performance.

Their commonality with the usual special purpose entity or vehicle formed by firms or formed in combinations of government and firms in the usual public–private partnerships is that they too are formed with a singular mission and enter into the partnership because the latter helps in the performance and success of the infrastructure which is their singular mission in achieving success with the infrastructure. Like every other partner they contribute the uniqueness of their corporate being—what special they have to offer.

Their special offer or contribution derives from the special attributes of their organization. The nonprofit in Design 3 is formed as an independent nonprofit or nonstock corporation as any other nonprofit. This means that it cannot use stock as a form of raising capital, but it can use debt and any form of business or investment income—a contract or the charging of fees being forms of the latter. It also means that maximizing returns to shareholders is not a motive for how they perform or their existence. They have to earn their revenues rather than to collect on the sale of capital shares. While fees for membership or client status may be charged, these are basically user fees that are market sensitive even in a monopolistic market; that is, they may be the only provider of a good or service but users can modify their use. The pressures are not distant shareholder pressures, but those from whom they serve. This fact contributes to their efficiency and optimality of size and offering.

The nonprofit in Design 3 must also be certified as tax exempt by the Internal Revenue Service and specifically to lessen the burden of government including those relating to infrastructure for the benefit of the public and evidence that they are capable of doing so. The burden must be recognized and acknowledged by government to be its if not for the existence and operation of the nonprofit. This harmonizes the nonprofit’s goal and purpose with the government and its constitutional responsibility (https://www.irs.gov/pub/irs-tege/eotopic184.pdf). In essence, the government’s constitutional duty is consistent with the nonprofit’s purpose for existing as required for it to obtain an exemption.

In addition, the nonprofit must also conform to other stipulations consistent with tax exemption as an independent organization. This means that all of its assets must be used in connection with its singular mission—lessening the specific burden of government and not paid in private benefits (excess compensation) or as dividends. Recall they have no capital stockholders. Moreover, there is no diversion of energy or assets as the nonprofit is assigned and approved for one mission (or class of mission). Assuming that the nonprofit is profitable, the excess beyond its needs can be transferred to the government and used at its discretion for the public’s benefits. In Designs 1 and 2 this is required. In Design 3, this is negotiated and may come in the form increased services. But in Design 3, the government nevertheless is paid any interest, rent, licensing, or other fees. This means that not only does the nonprofit reduce the burden, but it can become an effective cash cow for the government.

Furthermore, the tax-exempt nonprofit can, if it is properly designed, receive donations that are deductible to the donor and received by the nonprofit without income taxes on itself. It does this by showing that 10 to 30 percent of its revenues are from the public at large, corporations, or foundations and also by showing that their boards have elected or appointed officials representing the people’s and the government’s interest. The incentive to be responsive to the public as well as the government is obvious and so too is a source of income to support the work of the nonprofit in lessening the burden of government and to support those who cannot pay full price for the infrastructure services.

The nonprofit design provides for the most complete independence of government that is possible. This is so because structurally and operational it is distinctly incorporated as standalone and separate from government—raising the issues of accountability and the role of the elected or appointed government official addressed later in this article. Distinctly separate and independent also means that its risks and liabilities are not the government’s unless it (the government) chooses to make them so. In addition, separate and independent also means that it has its own board, raises its own funds through charging fees and prices, is capable of raising its own debt on the capital market and be solely responsible for it, has its own administrative and management capability, and requires an agreement or understanding as to its accountability and responsiveness to the government through its agencies or elected officials.

An example of the above is the National Park Foundation. It is a nonprofit chartered by the U.S. Congress with its own board and direction which gets no funds from the government but which has the mission of raising huge private (tax) deductible funds for the operation of the parks. It uses its status to reach capital sources the government could not, raises funds otherwise, and uses them all to help finance the parks and their programs. Its board is private except it contains high-ranking public officials as well.

The nonprofit therefore is conceptually capable of being fully independent and most capable of lessening the government’s burden (financial and nonfinancial) even to zero providing that it has certain operating powers. This would include the power to negotiate and to enter into contracts, to control its employment, to sue and be sued, to enter into long- and short-term debt on its own and without recourse or commitment of the government to back such or any organizational debt, to acquire and to dispose of property, to exercise policing powers that are limited to its boundaries the limits of which are specifically designed to fit the project under its responsibility, and to write and execute a budget and to maintain its own financial accounts and investment plan as discussed in Bryce (2017b). Furthermore, the nonprofit, because of its independence and separation and the requirements that its funds be spent on its mission, best protects the infrastructure reserves from government invasion “called borrowing” as occurs with other trust funds.

The nonprofit organizational Design 3 is indicated when “government fails” either in the public choice use of that term—meaning that the representative system does not lead to the most economical or efficient outcome or in the sense of Salamon (1995, 1987) and Salomon and Anheier (1998), that the organization may be a compliment or substitute for government as in Young (1998); or because contracts fail as in (Hansmann, 1980) or because the nonprofit is a social capital asset of the community formed to perform in a principal-agent context competitively or cooperatively with a high benefit to costs ratio (Bryce, 2005/2012) which would include infrastructure (Bryce, 2017b). Neither the government nor firms could do what the National Park Foundation does for the National Park Service. But government failure is not necessary since these organizations may be formed based on the motivations of government or citizens to help or to find a more efficient and satisfactory way.

In Table 1, we summarize the options described above and also show their relationship to public–private partnerships.

Illustration of Design Applications of Nonprofits and Application in Public–Private Partnerships.

The Financial Cost Burdens Relieved

Infrastructure affects the size and flexibility in both capital and operating budget considerations of government. It is both a long- and short-term recurring costs well into the future—representing a burden on the government and taxpayer when not lessened by the nonprofit. How does the nonprofit tackle these costs compared with government? How is the burden lifted by the nonprofit?

Capital Funding (Debt)

Both the nonprofit and the government can finance the capital cost of the project (construction, major replacement and repairs) through debt that is tax exempt. Specifically, both can issue revenue bonds—that is bonds that are not guaranteed by the state or by any other source other than the earnings from the project or by insurance. But only the government can finance a project with tax money or use its taxing powers to back a debt as in Design 1. It may do so through a general obligation bond—one that is backed with the full taxing powers of the jurisdiction—or by guaranteeing a revenue bond with the government’s taxing power as a recourse if the project’s earnings are insufficient to cover the debt service. Only the jurisdiction can support an infrastructure either directly or indirectly by imposing taxes or promising to do so.

But using this course is not always wise—especially when the underlying infrastructure is capable of self-liquidating that debt (toll roads) or where the risk is substantial and therefore exposes the entire community or simply unsound such as the recent case of the Harrisburg incinerator. Harrisburg, the surrounding counties, and the State had to come up with the money to pay creditors when the project failed because they had guaranteed payment for a project that could not satisfy creditors or basic market revenue criteria of size and sustainability to cover debt service. A lesson: a guarantee may occur not only in the specific debt agreement, but may be stated or deduced from existing state or local laws.

Thus, when the nonprofit issues debt, Design 3, it alone is responsible for paying it from the earnings of the project. It cannot use the government or taxpayer as a guarantor without the affirmative written permission by the legislature and executive of the government. Therefore, the taxpayers are not placed at risk unless their elected and appointed officials choose.

When the nonprofit is the issuer and there is no government guarantor of payments of debt service, the debt is not counted against the government’s debt limit and the taxpayer cannot be committed to a liability without the expressed written affirmation of their elected and appointed officials and sometimes by a referendum vote by the taxpayers themselves. But the nonprofit, being independent, must also pass credit tests and being self-managed is able to adjust to cash flow needs—even to the extent of seeking a nonrecurring and nonobligatory transfer assistance from a government—state, local, regional, or federal.

As a result of the debt being the nonprofit’s, the government’s debt capacity, measured in terms of its statutory debt limit, is not at risk and therefore not reduced. It can then be used to finance other projects which the jurisdiction might need and at a lower interest cost than if the capacity had been used absent the nonprofit. Therefore, the burden that the nonprofit lessens is not only the cost of that particular infrastructure but the opportunity cost of those that would not otherwise have been funded but for the nonprofit.

It is more than hiding debt. The debt limit of a local or state government is determined differently to the debt limit of a firm or the federal government. The debt limit of the latter is determined by Congress every year. The debt limit of a firm is determined by its financial ratios, covenants, and earnings performance as projected. The debt limit of a state and local government, however, is often constitutionally determined (often as a fixed percentage of a past revenue stream) and may require a popular as well as a legislative vote as if it were an amendment to the constitution or charter. Removing this debt burden therefore is a significant hurdle that usually cannot be done without the passage of time or for a single project. Fortunately, federal programs (e.g., housing, transportation, environmental, development) have facilitated nonprofits entering into debt for infrastructure projects intended to relieve a burden of government. So, in addition to saving the debt capacity, reducing the burden, the nonprofit has access to capital (government and private) the governments may not.

In sum, the nonprofit option is most indicated when the nonprofit is capable of independent management and financing: It is credit worthy and when it can raise funds either through the capital market or otherwise including donations from corporations, foundations, and persons with interest aligned with the project (a capital campaign that nonprofits run all the time). In general, the smaller the reliance on the government (either because of the size of the debt, the credit worthiness of the organization, or the ability of the infrastructure project to generate income to cover the debt), the better. If a government guarantee is needed, it is the responsibility of the political leadership and the taxpayers to give it or not. It cannot be assumed or preempted by the nonprofit or its creditors. There is full transparency because at the time of borrowing, the nonprofit has to reveal if there is a government guarantor in its documentation for the debt.

Capital Funding (Private Equity)

Private equity financing is available to both the nonprofit and to the government and is commonly in the form of a public–private partnership. When the nonprofit lessens the burden of government in this form, it may attract private investors or private providers including construction companies. When it does so, the basic rule is that it, the private investor, is investing in the project with expectations of a profit; e.g., it is recorded as an investment and not as a charitable gift. Furthermore, the investment is not in the nonprofit but in the project which is expected to have a cash flow that justifies the investment. And, at bottom, the project is of public benefit and is the mission of the nonprofit as a form of lessening the burden of government to provide for the public welfare.

Take a 1960s example that became national models. Bedford Stuyvesant in Brooklyn, New York, and Woodlawn in Chicago, with the underlying support of the Ford Foundation, developed lower income housing and the supporting community infrastructure using private construction firms, nonprofit management at the center of the public–private partnership, and government tax credits to attract private investors mostly large profitable firms that could use a tax credit for their investments and a tax deduction for the depreciation of the housing and other infrastructure, and the nonprofit used subsidized rents to meet operating expenses including the servicing of debt. In lieu of a government guarantor, the government offered forgiveness if necessary for any debt owed it by the nonprofit or taxable income and it transferred assets (mostly abandoned homes) to the nonprofit for development in this program. In the public–private partnership the arrangement was tripartite, in which each partner needed the other. The nonprofit could not do it itself, the firm investors could find better investment within its or related industry, the developers could gentrify and do better, and the government while holding the responsibility for the general welfare could probably do none of this (see Bryce, 2017a). Today, there are several variations of private equity coming through partnership—some less complex including sales-lease back arrangements variously structured (Bryce, 2017a and 2017b).

Capital Funding (Gifts, Reserves, and Transfers)

Capital grants are available from government (intergovernmental transfers) to the nonprofit or from state or federal governments to a local government. For the nonprofit, the reserve can also be acquired through a grant, a loan, or through restrictions placed on earnings to create a reserve or through a capital campaign or a board decision as a percentage of depreciation or of net revenues (earnings). When the reserve is created by a loan to a nonprofit, it can often be done cheaper than for some governments. This is so because some governments are up to their limits, have limited tax base, and poor credit ratings.

One of the ways this reserve can be created by government is through the creation of a nonprofit (either by government or private citizens) through which this reserve is channeled. This method was used, for example, to repair the Statue of Liberty. The government has an additional method (other than a percentage of fees) that is not available to the nonprofit and that is to create a reserve from a set-aside of a percentage of taxes. The nonprofit cannot tax. In short funding capital expenses is a burden the nonprofit can relieve the government and the taxpayer to the extent that it does not require transfers from the government in question and can extract from its own reserves or from grants and donations or specific capital campaigns.

Capital Funding (Lease Arrangements)

Some infrastructure assets already exist. Some were paid for by government, others are simply the result of the national patrimony—such as the waterfronts, springs, hills and mountains, and caves. In such cases, the property can be leased to the nonprofit providing a flow of income to the government depending upon the terms of the lease. Subsidized leases are not necessarily one-sided. The government benefits by shifting all other operating costs to the nonprofit and by putting an unused resource (e.g., abandoned property as in Bedford Stuyvesant) into play and under supervision by the public through a public organization, the nonprofit, and for the benefits the public (Bryce, 2009).

Financing (Operating Costs)

When the government runs the infrastructure, operating expenses can be covered principally through short-term operating debt (such as tax anticipation notes), prices (user fees), taxes, and appropriated transfers from its general or earmarked funds. It could also cover part of operating expenses through the use of volunteers and donations by creating a nonprofit attached to or affiliated with the government agency with the sole mission of facilitating the agency’s operations through various approved fundraising and programming activities for the benefit of the agency and its mission.

When the nonprofit is the operating entity carrying the full load of the operating burden, it does so principally through short-term borrowing, through user fees (prices), the use of any reserves it set up for that purpose, its fundraising activities, volunteers, donations, or contributions. The amount of burden the nonprofit lessens is reduced by any government transfers (contractual or otherwise) to it. The government contribution is not always a transfer of funds. It may be an in-kind service (such as police) that it renders the nonprofit or unused property. When the government transfers money, its purpose often is to subsidize infrastructure use by the general population. A good part of it, therefore, is a subsidized user fee.

Appropriations and Tax Expenditures as Sources of Funding and Financing

In the previous section, we identify the financial cost burdens that the nonprofit lessens and how it may do so compared with the government. In this and the following sections, we extend the argument to show that the distinguishing methods of financing the infrastructure effort also offer opportunities to lower the underlying burden and to make the process more efficient—leading to a more optimal result at a lower overhaul cost.

When the government covers those costs, it raises some or all of the funds through taxation and then makes appropriations of a fraction of these revenues to the infrastructure project. Yes, the government may also raise revenues by charging a price. The amount that is appropriated should be correlated with needs or returns from the project itself—and there is no evidence that it normally is. Rather, appropriations are typically political decisions to which public choice theory and the discussion that follow speak.

Appropriations have the following characteristics and consequences: (a) they breed uncertainty into the project because appropriations are discretionary political decisions; (b) appropriations can be withdrawn or withheld at the sole discretion of the political decision of the legislature and often for reasons unrelated to the infrastructure itself or not spent by the executive; (c) appropriations can cause delays followed by increases in cost if only due to inflation; (d) to the extent that there are appropriations, they are opportunity costs as other projects are foregone—but also there are costs associated with the need to lobby, logrolling, rent-seeking, government interference, and whatever crowding out effect that may exist on other sources of revenues including the willingness of users to pay a market rate; (e) in many cases, appropriations would be a waste of public resources as the nonprofit is quite capable of self-financing and should; (f) the appropriation process is also biased for most who will cast a vote may have no attachment or use of the infrastructure and they may tend to undervalue it; on the other hand, if they pay for it the users in effect transfer the cost of their utility to others—a problem of both equity and efficiency; (g) appropriations are a poor measure of preferences—see, for example, the impossibility theorem or the median voter theory—or the revelation of preferences or of true value; (h) the legislature or other government official may be motivated by selfish interests and so too the bureaucracy; (i) vigilance may give to the “illusion” recognized by Buchanan and Tullock (1962) on what representative democracy produces; (j) the entrepreneurial spirit, both on the revenue and expenditure sides, is dampened by the “certainty” of an appropriation; (k) appropriations and government performance of the infrastructure create its own abundant opportunities for corruption. Infrastructure are frequently the targets of corruption by officials as in the Harrisburg case cited above.

The Preference for Tax Expenditures

When a nonprofit operates an infrastructure, its revenues are primarily from the fees it charges users that often completely replace the need for appropriations by the government. There are no contract fees, capital costs, or expenses. Lessening the burden of government is not synonymous with a contract and a quid pro quo or compensation. The underlying document is an agreement and the operating reality is that they may or may not receive some aide from the government (Bryce, 2017b).

Put another way, when the government or one of its dependent agencies carries out the burden, the government is committed to annual appropriations. It is also so committed if it enters into a contract with a firm or a nonprofit. When the nonprofit is chartered to lessen the burden of government, it does so through an agreement and is not, unless the agreement specifies, committed to making any payments or contributions. It may elect to do so and it may also elect to contribute in-kind which does not require an appropriation. See Bryce (2017b) for an example of the agreement and examples of actual ones.

But because the government foregoes an appropriation by using a tax-exempt nonprofit, it does not mean that there is no tax expenditure—the revenues foregone if the nonprofit were taxed. The remainder of this section discusses this trade-off and why a tax expenditure (due to the existence of exemption for the nonprofit) is a bargain for the government.

To explain, if the government taxed the nonprofit’s revenues from these operations, it would tax the gross revenue received, minus the expenses, other deductions, and any applicable tax credit. This means that the entire cost of operating the facility plus current interest would be deducted, making the nonprofit’s tax base significantly lower. It would become smaller yet because the tax exempt revenue bonds upon which these nonprofits may depend would now become taxable and have a higher interest cost which would also be deduced as an expense. Among the deductible expenses would also be the cost of preparing and filing the taxes and the depreciation of the infrastructure itself or a leasing fee, if applicable.

Moreover, in those states and municipalities without an income tax, the income tax expenditure would be zero and the issue would be moot. In addition, a tax would reduce the available reserve for future needs (repairs, expansion, replacement) which the government may find itself having to make up to keep the infrastructure a going concern that is not badly impaired.

In calculating the true net loss (if any) from the tax expenditure, the government would also have to include the taxes it would be imposing on its own agencies operating a similar infrastructure anywhere in its jurisdiction. This is so because government agencies are tax exempt under a basic theory as the nonprofit—income derived from performing its mission to advance general welfare is exempt (Robert Routhan and Amy Henchey; https://w.w.w.irs.gov/pub/irs-tege/eotopicb93.pdf). In these cases, the mission of the nonprofit is the same as the agency—to advance general welfare through providing the infrastructure for public welfare (rather than private profits such as a firm). If the mission is taxable for one, pari passu, it is arguably taxable for the other. As a matter of practice, net earnings of a nonprofit or government that are unrelated to their mission are already taxed and at corporate rates.

Another source of revenues for the nonprofit lessening a burden of government is donations. Calculating the tax expenditure of a donation would require the government to decide whether the tax expenditure is to be attributed to the donor (because the donor received the tax deduction), the nonprofit which received a “revenue” tax free or whether it should apply to both with a credit given to one. This avoids double taxation or counting, and these alternatives would give different answers because the tax base and impact would be different.

More fundamentally, a problem with donations is that they often account for a small percentage of the revenues of many of these nonprofits lessening the burden of government and a substantial part of their contributions is in the form of volunteer work and space for which the donor gets no deduction but the organization has to assign a value in its accounting. In addition, for a corporation faced with such a tax, it could be easier for it to record the transaction as a marketing expense (one intended not for social purposes but to improve public perception of the firm). In that case, it would deduct the amount anyway.

Another problem with deductions is that many of the organizations that reduce the burden of government may receive in-kind contributions from the government itself. This comes in various forms including dedicated police services, collection of assessments, grounds and equipment services, and space. The government would not be taxed because it is tax exempt. If the nonprofit is taxed, the government would actually be paying itself for a lease. In some instances, this may work as in the discussion of leases above, and in others it may discourage the nonprofit from using certain related services from the government. Neither per se may be necessarily bad but point to charging a lease as a straight forward transaction rather than a tax and its consequences.

Finally, the government would have to consider whether taxing to remove the tax expenditures would not reduce the organization’s ability to lessen the burden and subsequently require the government to make greater assessments to the nonprofit to keep it operating at the same level or raise prices which would reduce use especially by those least able to pay. Such a consequence would be contrary to the concept of general welfare.

Sales taxes are not generally imposed by the federal government but by states and local governments—making the sales tax expenditure issue moot at the federal level. At the other levels, the nonprofit does under current law collect a sales tax on its sales and passes it on to the appropriate government. But only on its mission-related purchases, it is generally exempt so that the sales tax expenditure would apply only to this kind of transaction. The yield of this would depend upon the revenue productivity of the infrastructure. But it will almost certainly be passed on to the user because the demand for many infrastructure is, presumably, fairly inelastic—meaning that in addition to raising money it could become very regressive.

On the local level, it is not the income tax that creates the tax expenditure problem, but it is the property tax. Here the government’s arguments are that the nonprofit imposes an actual cost on local government (policing, fire, roads, etc.) for which it should pay as well as an opportunity cost because the property could otherwise have been used in a manner that generates property tax revenues. In the case (http://www.minnesotanonprofits.org/mcn-at-the-capitol/Property-Tax-Final-Revenue-Bulletin.pdf) Minnesota gives specific conditions that must be met; in particular that while the public at large must be served a substantial number of those who receive service must be disadvantaged for the nonprofit to receive property tax exemption for lessening the burden of government. Some counties in Pennsylvania have used another compromise that allows the nonprofit to pay a fee (which they calculate) in lieu of taxes. In either event, there is an acknowledgment that tax expenditure may be a bargain.

The Economic Efficiency of the Nonprofit Organizational Design

When the government provides an infrastructure, it usually pays for it through the imposition of a compulsory tax over the general population or a specific population, but with few exceptions, these taxes usually have limited if any connection to the use of the infrastructure.

The Scope of Efficiency

The nonprofit may offer a more efficient solution because it cannot impose a tax or impose a commitment on the government to impose a tax or assessment, and therefore relies on prices or fees imposed upon users and sometimes these fees are collected as an earmarked tax by the jurisdiction and passed on to the nonprofit. To accommodate those who are less able, the nonprofit may price discriminate and charge a lower amount for some select population. Accordingly, the connection between use and amount paid is better established. Because a user can use the facility to the extent that his or her marginal use at that price equals the marginal benefit to him or her, this in effect is maximizing the individual benefits from the infrastructure and reaching a level of equilibrium with the user. A summation of all users leads not only to a maximization of their benefits but to an optimal size and use of the infrastructure and a more efficient outcome.

When price discrimination is not possible or desirable, a lower than market price could be charged to all with the difference being made up either by special jurisdictional assessments which would still lower the amount of burden relieved or through gifts and donations including in-kind gifts from the jurisdictions. To the extent that these come from a nongovernment source, it lowers the burden. It also lowers the burden of a local government if the transfer comes from the federal or state governments and would not otherwise have been available through a channel other than the nonprofit.

Furthermore, those who receive external benefits without actual use do not necessarily escape to the extent (e.g., with commercial use) that the price they pay reflect the price to the commercial user; for example, the taxi driver and the truck driver incorporate the user fee in the price charged. They pass it on. Furthermore, a considerable amount of external value is or otherwise captured in other forms of taxes. For example, to the extent that the infrastructure causes property values or desirability or livability to rise, that is captured in property and real estate sales taxes.

The nonprofit also advances the causes of efficiency and the maximization of public welfare when it acts as a facilitator rather than as a doer or provider as in the previous paragraphs. It may be a facilitator to the government in one or more phases of the project—in planning, in the acquisition, financing, or operation of the infrastructure. In any of these, it reduces the burden of government. Thus, the National Park Service Foundation a 501 (c)(3) has as its exclusive mission the raising of funds from corporations and elsewhere for the National Park Service and to conduct programs with the public utilizing the infrastructure of the national parks. It finances itself.

Indeed, when an infrastructure crosses jurisdictions, some form of a nonprofit whether as an authority or one under 501 (c) may be indicated as a doer, facilitator, and coordinator. Jurisdictions vary in their rules, their constraints, their use, and depth of interest even though they may all be heavily invested in the project the sum of which will well exceed their individual budgetary possibilities. Some form of independently incorporated joint venture in the form of a nonprofit is usually indicated so that the project may proceed with a commonly shared interest and total cost allocation.

For this to happen, the joint venture has to be incorporated to have its own identity and power (given by the group of participating governments) to negotiate contracts, to sue and be sued, to acquire and dispose of property, and to develop rules that are peculiar to the joint venture but not necessarily any of its partners. All partners in the venture will agree to the terms of the joint venture and if they will give recourse to any debt burden. That joint venture may be a nonprofit under 501 (c)—including an association, or it may be an independent authority—a nonprofit formed by the governments on which their elected or appointed officials and residents may serve—that is— Designs 2 or 3. The Chesapeake Bay Foundation is an example of Design 3. The Metro Authority in D.C. is an example of Design 2. These designs are preferable because the government cannot be on the board of a firm. Therefore, it would have no inside influence on what the firm does as it would with the typical nonprofit created by the government or citizens for infrastructure purposes. Among other things, they keep the organization committed to its infrastructure mission to serve the public and protect the assets from being diverted to any other use—private benefits such as dividends and mission creep.

Benefit–Cost Calculation of Nonprofit Lessening the Infrastructure Burden of Government

Using a nonprofit (Design 3) rather than doing it (Design 1) is an investment choice for the government. A basis of such a choice should be the estimated benefits/cost ratios as discounted for time and risks. In most infrastructure cases, it is possible to calculate this rate within a margin of error. Table 2 shows how each component of this ratio would work—assuming that the useful life of the project is implicit in the project itself and, therefore, not whether it is done by the nonprofit or the government. The discount rate could vary but not necessarily always in favor of the government. Nonprofits also issue tax exempt bonds, and some may also have a better credit rating than the government because their ratings are determined largely by the project and not by “all other debt” unrelated to the project many of which have no or negative cash flows. The project expected earnings from which debt service is to be taken is also calculable and made protected only for project purposes. But the risk and political uncertainty of government and the direct input of users in the reliability and management of the infrastructure again due to the political process (not necessarily the technical skill) causes higher discount rates in Design 1 than in Design 3. Obviously, these could vary by situation and by project.

Calculating the Benefit/Cost Ratio of Nonprofits Lessening the Infrastructure Burden of Government.

Agency, Accountability, and Role of Government

When a nonprofit is created to lessen the burden in part or in whole of government for the provision of any part or aspect of an infrastructure, it does not release the government from its Constitutional duty to provide for the general welfare of the population nor does it release elected and appointed officials from their responsibilities to make policy and to insure their compliance. The government prevails as policy maker and regulator. The nonprofit simply assists in fulfilling these responsibilities by either doing the work of providing the infrastructure and related services or by facilitating the government in getting it done. In agreeing to the arrangement for the assumption of the burden, the government cannot quit its obligations to the public of which it is an agent. Thus, Fyall (2012) correctly concludes, “Regardless of who ultimately provides a public service, those in government are responsible for ensuring the match between citizen preferences and public outcomes. Accountability remains with the government.”

In fulfilling its Constitutional responsibility, the government may enter into various collaborative structural designs as in (Bryce 2017b), contracts, or agreements and in so doing set the terms of performance and accountability. So, the failure to have adequate accountability terms is ultimately the failure of the people’s representative (elected legislatures and administrators) to stipulate and to enforce them. The nonprofit cannot unilaterally set these terms. Governments can (Thynne & Wettenhall, 2004).

In addition to this accountability to the government, the nonprofit has accountability directly to the people. Its accountability to the government comes not simply because of the argument above, but because it is the government that agrees and licenses the nonprofit to perform. Infrastructure requires not only an organizational charter, but a number of construction, finance, and operating licenses given only by government. Without them the nonprofit cannot legally exist, initiate, or fulfill any part of an infrastructure project.

The nonprofit also has a duty of accountability directly to the people because it is an organizational creation of citizens or government to perform a specific infrastructure function therefore it is their agent. Furthermore, the nonprofit is supported by the citizens and government through a variety of means including paying for their services and through tax deductible contributions from citizens and others and a resulting tax expenditure by government. Therefore, the nonprofit is in a contractual and structural principal–agent relationship directly with the residents and is also their agent—in this instance, the organizational vehicle through which they accomplish and carryout the infrastructure mission. As such, it is accountable to the principal (the people) and to the government acting on behalf of the people through the principal–agent relationship and through the Preamble of the Constitution. Accountability of the nonprofit is at least doubly binding—to the people directly and to the government as a representative of the people (Bryce, 2005/2012).

The character or type of infrastructure project merely defines how that accountability for that project may best occur—the mechanism, content, frequency, and timeliness. The two principal targets of accountability are set by the description above. To the extent that there are creditors, users, and others, the accountability to them is subordinate as investors, risk takers, and users, and in many respects, they are negotiated separately with each of these parties and within the parameters allowed by the primary principals—the people directly, and the people through the government.

Government’s Responsibility for Accountability: Managing the Exercise of Control and Costs

The challenge for the policy maker and administrator is to specify the terms of accountability and performance and to negotiate these terms in the approval or agreement the nonprofit needs to sign to qualify as lessening the specific burden of government. Within these terms, the nonprofit negotiates and works with all others with whom it may engage including creditors who normally have a demanding protocol of accountability even if it is self-serving. The overall motives of accountability by the government is to insure that its agent (the nonprofit) is meeting the government’s obligation to the people (its principal) under the Constitution including general welfare and public safety and to insure that the actions of the nonprofit do not impair its own ability to fulfill this obligation as needed in the future.

The motive is not to control the nonprofit. For the government to control the organization is to render the concept of an independent agent null and the government would be liable for the obligations of the nonprofit and the burden would not be lessened but at best made contingent—waiting to happen upon the occurrence of some negative event. To regulate the nonprofit means it can monitor, seek amendments, require approval, require it to make and honor even discretionary decisions or promises to the public, and the power to penalize or discontinue the relationship. Through all this the government maintains its power to investigate, adjudicate and to penalize the organization and its management as it does any private entity within its boundaries that it does not control. The government remains powerful even as it transfers the burden of performance to the nonprofit and so fulfills its Constitutional responsibilities discussed at the outset of this article. This power resides at all levels of government.

Setting the terms of accountability can be affected by weak governments, inadequately informed governments, the self-interest of government bureaucracies and leadership as described in public choice theory, the persuasive strength of the public at large or of a strong self-interest group, the “selling out” of some elected and appointed officials, and consciousness of the cost of compliance. As a practical matter, Bovens and Schillemans (2014) argue that accountability comes with collateral costs—increased project cost, red tape, and negative effects of important public values, trust, and learning. These costs are often real, but we need note, they are often the excuse by which accountability is defeated by the self-interested with those in power.

Core Attributes of Infrastructure and Accountability: Metrics and Standards

The terms of accountability within these constraints can be strengthened due to certain core attributes of infrastructure. Therefore, the nonprofit can be held to certain objective standards. In general, infrastructure projects are associated with commonly accepted metrics and standards of performance (inputs and outputs) and expectations in the industry in which the infrastructure falls without reference to the organization being private, public, or nonprofit.

Infrastructures are largely tangible and observable, are located and anchored in a known geographic location so that one can map their sphere of primary influence (or geography of a market even when the service may be intangible) and the jurisdictional rules that apply as well as the predictability and other constraints in a market space. Geographic accountability is important not only because of client needs but also because of externalities both negative (the environment) and positive (value added) radiate regionally.

Infrastructure, depending upon type, is subject to a standard method of accounting from which a nonprofit provider is not exempt. Books as well as operations must be recorded in a transparent manner set by accounting and industry standards as well as that which is required by the various levels of government by industry and by the nonprofit organization as an entity. These data (barring some exceptions) must be available to the public.

For a nonprofit operating or contributing to an infrastructure, its FORM 990 is not enough as it may be with other nonprofits. Accountability to the agency that they are formed to assist or whose burden they are proposing to lessen may include submission of annual budgets, detailed financial statements, program and activity plans, as well as organization bona fides and approval for each program activity. Additional approvals may include proposals for price increases, proposals for disposition or acquisition of assets, approval of debt, and requirement of filing debt-related documentations. A principal purpose of these types of accountability is to insure the ability of the organization to perform that which is agreed upon and that which is conducive to the burden reduction.

Depending upon the jurisdiction, infrastructures are subject to inspection, while this may be motivated by safety, it is also a window for the determination of the care and durability of a public asset. Some of this inspection, a form of accountability, may occur at all three levels of government as well as professional organizations.

The Mechanisms of Accountability in General

Accountability may be expressed in a variety of forms including government inspections, surveys, and public hearings as they are requested by government agencies and citizen groups, in press releases, and other publications and in required government filings at all levels. Accountability should also have to do with the acquisition, disposition, diversion, or deterioration of any public asset or any other that may impair the ability of the nonprofit to perform.

As an independent organization, the nonprofit is not controlled by government and the mechanism of accountability is not hierarchical. It is horizontal and one-way. The government is not necessarily accountable to the nonprofit, although it is expected in a collaborative arrangement to do as it promised or as accountability is necessary to meet the criteria of a third party such as a creditor or the citizens who may need transparency about what their government is contributing or requiring.

As an independent agent, the nonprofit has its own board of directors and management that provides an internal mechanism of accountability and expert knowledge. Their duties are the same as any other nonprofit board—including to make sure that the nonprofit sticks to its mission and promise. In this case, it is the furtherance of the general public welfare of the population through lessening the specific burden of government. But unlike most other nonprofits, these boards are heavily technical and at the same time overly exposed to the risk of self-dealing because they are often purposefully drawn from people with a local or commercial interest in the project or representatives of the government agency that is having its burden lessened. This is done with the hope that they will best represent those at risk because they themselves are.

Choosing the Right Nonprofit: Relevance of Details

When a nonprofit is formed to lessen the infrastructure burden of government, a secondary but important question is, “What type of nonprofit?” The Internal Revenue Code allows the use of (c)(3)s, (c)(4)s and (c)(6)s. Which? It depends. Table 3, also prepared by this author, shows what the jurisdiction(s) should consider given extant law, this article which represents mostly 501 (c)), and what may be the objective.

Tax-Exempt Categories and Probable Best Fit.

Summary

The main conclusion of this article is that the government’s capacity, cost, and budgetary burdens for the provision of infrastructure grounded in the Constitution can be efficiently lessened by nonprofits specifically designed and created for that special and singular purpose. The nonprofit can operate self-sufficiently, singularly, as a facilitator or as a part of a public–private partnership. Furthermore, it can operate efficiently and the tax expenditure that it may cause is a likely bargain compared with the cost of government appropriations and management. Thus, the nonprofit (as in Design 3) may offer a partial yet efficient solution to the dilemma: Annual recognition of need for expenditures on infrastructure for the public’s safety and general welfare and the failure of government to appropriate an adequate level of funding to fix the problem despite its Constitutional purpose and promises.

But because the government must regulate rather than control these nonprofit entities because they are not part of government as in Design 1, the article shows how the nonprofit may reduce the burden with no meaningful loss of the influence of citizens or government through accountability and everyday regulation already in practice. Indeed, the nonprofits could contribute to increased citizen satisfaction and involvement at the same time that they reduce specific actual and opportunity costs that are identified in this article as burdensome. The ultimate test of these assertions and in Bryce 2017b is in the ability or imagination of the public policy maker and administrator to find and make good the principles that are outlined when the situation fits them and the nonprofit is competitive. It often is (Bryce, 2005/2012) and available for engagement when designed and empowered as described in (Bryce, 2017b).

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.