Abstract

Globally, governments at all levels—national to local—are fiscally constrained, especially in the developing countries of the Global South (Africa, Latin and Central America, and the developing countries of Asia). One such country is India, which is also experiencing rapid growth in urban populations and is seeking additional revenues from public finance sources, such as development charges. In India, these charges need to meet the rational nexus principle to be legally robust. Through a review of India’s state-level enabling legislation, this article seeks to identify ways in which the enabling legal framework for development charges can promote or hamper the rational nexus principle. Finally, this article provides insights that can help jurisdictions in India, and potentially in other Global South countries, craft or amend enabling legislation so that such legislation can withstand rational nexus principle–related legal challenges.

Keywords

Introduction

Globally, governments at all levels—national to local—are fiscally constrained, especially in the developing countries of the Global South (Africa, Latin and Central America, and the developing countries of Asia). In this region, local and state governments in particular are in a fiscal bind because a large proportion of tax and fee revenue typically accrues to national governments. Moreover, local and state governments have very little authority to levy new taxes. Furthermore, national governments have very high external and internal debt, limiting their ability to grant urban development funds to state and local governments. In addition, municipal bond markets are either underdeveloped or nonexistent, which limits these countries’ ability to access private capital markets for funding urban development. Finally, residents resist traditional revenue sources such as property and income taxes. In such a scenario, these countries urgently need additional revenue sources to fund urban development projects, especially due to their rapid rate of urbanization. For example, between 2014 and 2050, three Global South countries—India, China, and Nigeria—will account for 37% of the projected increase in the world’s urban population, amounting to increases of 404 million, 292 million, and 212 million, respectively (United Nations, 2014). Here, development charges are a potential revenue source.

Globally, these charges go by various names. For example, they are called impact fees or system development charges in the United States and infrastructure charges in Australia. Therefore, in the rest of this article, we use the phrase development charges for all these types of fees. In India, these charges are often very low, and typically, they are not tied to the cost of mitigating the impacts of the charge-paying development, including the cost of providing external infrastructure/services such as roads, parks, and schools that serve the development (see Mathur’s (2016) review of development charges in Tiruchirappalli, Tamil Nadu, India). Furthermore, in many cases, they have not been updated for decades. Therefore, they have not kept pace with the increasing cost of developing urban infrastructure and services.

In India, property developers often pay development charges at the time of seeking government approval to change/institute the use of their land parcels and/or to improve them. The property developers pay these charges to public agencies, which, in turn, use the revenues from these charges to mitigate the impacts of the charge-paying development, for example, by developing the infrastructure/services needed to service the proposed development. From a legal standpoint, these charges are considered a fee, not a tax, in India. Accordingly, the courts in India, like those in the United States, require these charges to meet the “nexus” and “rough proportionality” principles (Phatak, 2013).

The nexus principle stipulates that there should be a connection/link between the charges and the impacts caused by the charge-paying development (Altshuler & Gómez-Ibáñez, 2000). For example, the charges might be needed to (a) augment existing infrastructure such as sewer lines, wastewater treatment plants, and roads if the capacity of these infrastructure needs to be expanded to serve the charge-paying development; (b) provide new infrastructure needed to serve the charge-paying development; or (c) mitigate the environmental or social impacts caused by the charge-paying development. Such impacts could include vehicular pollution and noise.

The rough proportionality principle calls for the charges to be in proportion to the cost of mitigating the impacts of the charge-paying development. For example, if a proposed development pays US$100,000 in charges, then that amount should be roughly equal to the amount needed to mitigate the impacts of the development. Combined, these two principles constitute the “rational nexus” principle.

As India seeks to increase development charges or to levy them, there is an urgent need to investigate how these charges can meet the rational nexus principle; otherwise, these charges can be successfully challenged in court. Indeed, the rational nexus principle was cited to legally challenge the state of Tamil Nadu’s Infrastructure and Amenity Fee (Indian Kanoon, 2015). This article seeks to begin to fill this research gap by reviewing several pieces of state-level enabling legislation to (a) show how the legislation hinders or promotes the rational nexus principle and (b) identify major insights that can help India and potentially other developing countries craft or amend legislation that can withstand legal challenges.

India is a suitable study area for the following reasons:

It is a large and diverse country with approximately 18% of the world’s population (United Nations, 2017).

It is a democratic country with a local, state, and national government structure that is similar to the governance structure of other developing countries, a large majority of which are also democratic countries.

Like other countries of the Global South, India’s population, including the urban population, is increasing rapidly.

Over the last three decades, as the country has started to open its hitherto socialist economy, it has welcomed more neoliberal market-based solutions and public financing tools, such as development charges. Such solutions are also finding acceptance in other Global South countries. In fact, the United Nations Human Settlements Program (UN-HABITAT) published a reader for developing countries that provides an overview of such financing tools (UN-HABITAT, 2016). This publication also calls for developing a region-wide legal framework to ensure uniform application of such tools.

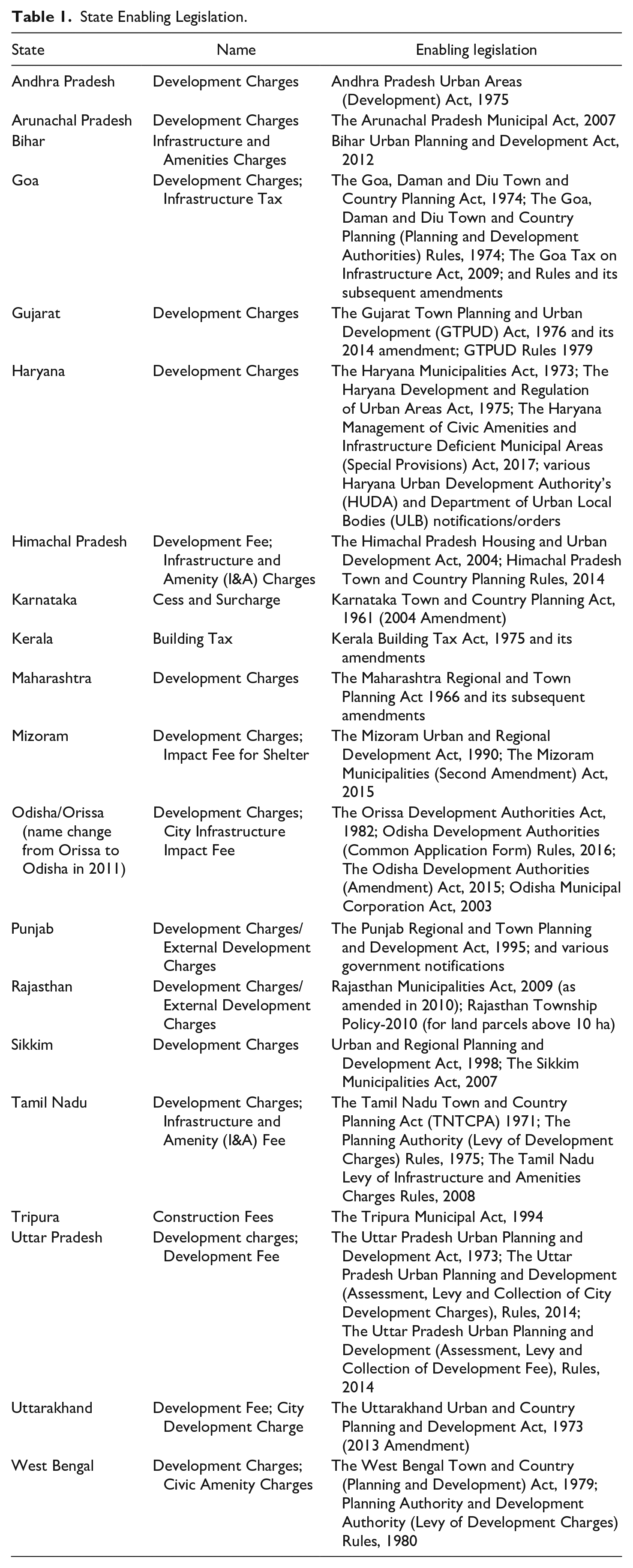

A large number of states in India (20 out of the 24 states reviewed in Government of India [GoI], 2017) have enacted legislation to employ development charges, providing a large number of legislation to review.

Similar to many Global South countries, India is experiencing significant infrastructure finance gap that is not being met with traditional revenue sources such as property tax (GoI, 2017).

Literature Review

There are three major strands of development charge–related literature. The first and perhaps the most developed strand seeks to theoretically and, more recently, empirically ascertain who bears the burden of development charges. Motivated by equity concerns, this literature examines the impact of the charges on property prices, especially house prices (e.g., see Altshuler & Gómez-Ibáñez, 2000; Been, 2005; Bryant, 2017; Evans-Cowley et al., 2009; Ihlanfeldt & Shaughnessy, 2004; Mathur, 2007, 2013; Yinger, 1998), generally finding that development charges increase house prices. For example, Evans-Cowley et al. (2009) and Bryant (2017) find a 537% and 400% price increase, respectively. A couple of studies that examine the price impact at a more disaggregate level find that it varies by the type of infrastructure funded by the developer charge. For example, Burge and Ihlanfeldt (2006) find that although development charges for water/sewer do not affect house prices, nonwater/sewer charges increase the prices of small, medium, and large houses by 39%, 82%, and 127% of the amount of the charge, respectively. Mathur (2013) finds that although development charges for parks increase prices of new houses, charges for fire protection reduce them.

Examining the effect of development charges on commercial properties, Burge (2009) argue that the charges are likely to have two countervailing impacts. While, on the one hand, they are likely to dampen investment in and supply of commercial properties, on the other hand the limited supply is likely to increase value of commercial properties.

The second strand of literature examines the efficiency and impacts of the charges in regard to various other dimensions of urban development. For example, Burge and Ihlanfeldt (2006) find that development charges increase the rate of residential development, Nelson and Moody (2003) find a similar positive effect on job growth, and Burge et al. (2013) find that zone-based development charges could reduce sprawl by shifting development from urban fringe areas toward the inner-city areas.

The third, more applied, strand of literature seeks to identify and demonstrate ways to make development charges legally defensible. The development charge–levying government must have the legal authority to levy development charges and must follow the procedures and standards stipulated in the enabling legislation, where applicable (Evans-Cowley, 2006). Furthermore, the charges must meet the rational nexus principle (see Evans-Cowley, 2006; Nelson, 1995; Nicholas, 1988). Primarily U.S. based, this literature calls for data-intensive studies as inputs for designing the charges, for example, inventorying existing infrastructure systems and their planned expansions, conducting detailed infrastructure demand studies, and identifying level of service (LOS), the kind of detailed studies that are often not feasible to conduct for public agencies in many developing countries. Therefore, there is a need to examine (a) whether context-sensitive exemplars of how enabling legislation is promoting or could promote rational nexus principle in developing countries already exists and (b) some of the ways these pieces of legislation hinder the rational nexus principle and how such hindrances can be removed.

One such recent study, Mathur (2016), begins to fill this research gap through a comparative examination of three development charge programs—one from a developing country (Tamil Nadu, India’s Infrastructure and Amenity Fee) and two from developed countries (Fremont, California, USA’s impact fee, and Brisbane, Queensland, Australia’s infrastructure charges). The study identifies the features of a development charge program that promote the rational nexus principle and applies the findings from the developed country case studies (the U.S. and Australian cases) to the Indian case. Although Mathur (2016) synthesizes strategies that promote the rational nexus principle, due to a different focus, it does not examine how the enabling legislation promotes or hinders the rational nexus principle. Furthermore, it would be useful for this strand of literature to examine whether/which developing country-sensitive strategies could enhance the rational nexus principle. Furthermore, although I believe that studying individual development charge programs provides useful insights, I argue for a higher level—enabling legislation level—examination due to the ability of such legislation to have a broader policy impact by influencing a large number of development charge programs. This article begins to fill this research gap.

Method

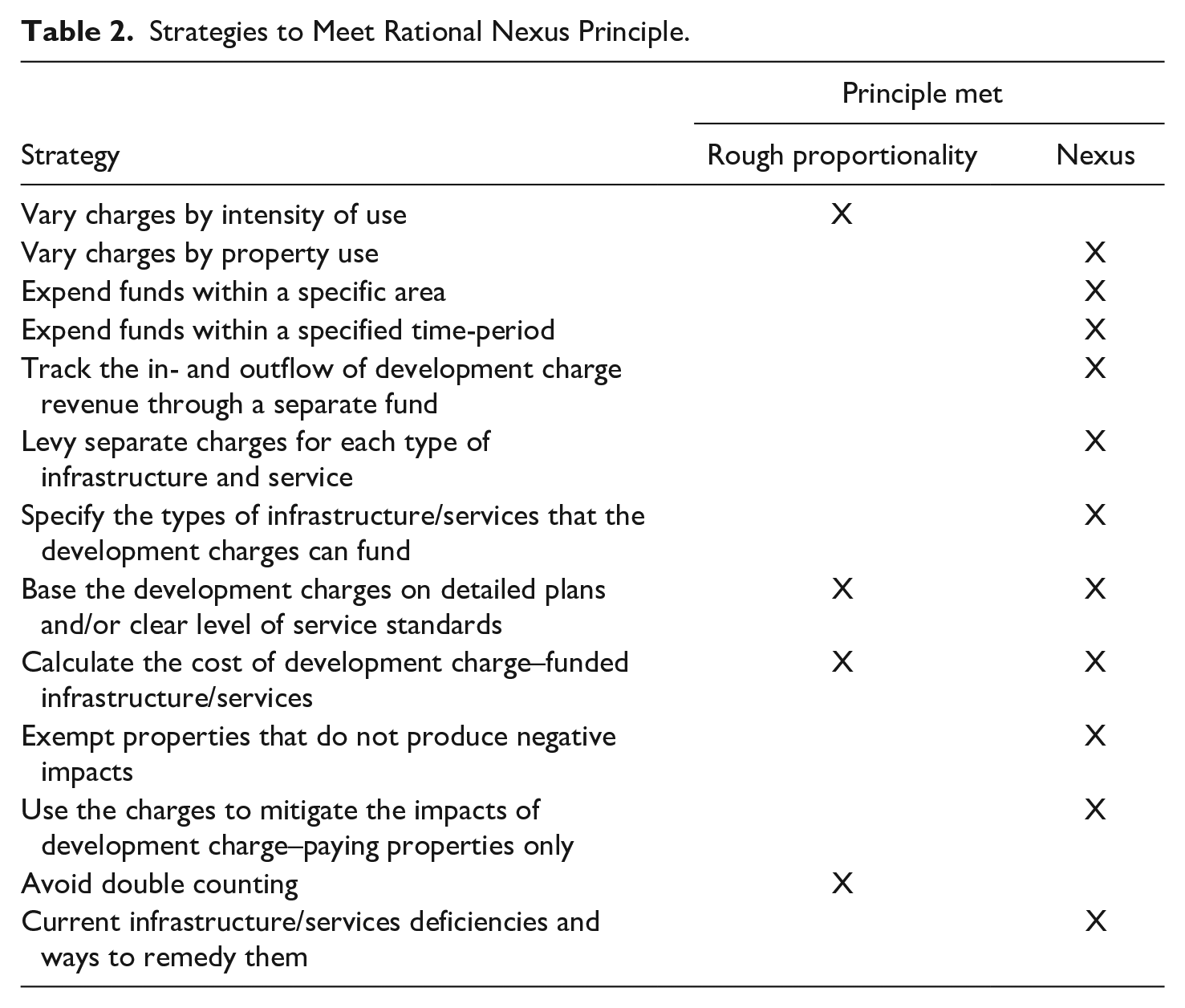

Using a recently published report by the Government of India (GoI, 2017) that identifies development charge–related state-level legislation for 22 states, I conducted an online search to collect the state-level acts and rules identified in this report. These acts and rules provide the enabling legal framework for levying development charges. At this data collection stage, I also found a few errors in the report, which I corrected. For example, for the states of Nagaland and Madhya Pradesh, the report erroneously notes enabling legislation for betterment levies (such levies are based on the value of land rather than on the cost of providing infrastructure/services or the cost to mitigate the negative impacts of a proposed development) instead of legislation for development charges. In such cases, I conducted an extensive internet search for development charge–related state-level legislation. Similarly, in a few cases, such as for the state of Goa, I found and reviewed additional enabling legislation. After excluding Nagaland and Madhya Pradesh from the 22 states identified by GoI (2017), I ended up with enabling legislation for 20 states (see Table 1). Next, using the strategies to promote the rational nexus principle identified in Mathur (2016), I examined whether/how these pieces of legislation hinder or support the rational nexus principle. Mathur (2016) provides a series of questions to assess whether a development charge program employs strategies to meet the rational nexus principle. These question include (a) whether development charges vary by intensity of use, (b) is the revenue from the charges expended within a specified area, and (c) what steps are taken to avoid double counting. Table 2 lists these strategies and notes whether they help fulfill the rough proportionality principle or the nexus principle, or both. Finally, I synthesized the findings to highlight how legislation can support or hinder the rational nexus principle.

State Enabling Legislation.

Strategies to Meet Rational Nexus Principle.

Overview of Development Charges in India

What Are They Called?

Of the 20 state-level pieces of legislation studied for this project, a large majority (16 states) levy at least one fee called a development charge/fee (see Table 1). The names used by the remaining four states—Bihar, Karnataka, Kerala, and Tripura—are Infrastructure and Amenities Charges, Cess and Surcharge, Building Tax, and Construction Fees, respectively. Eight states impose a fee in addition to a development charge, such as the civic amenity charge, the city infrastructure impact fee, and the infrastructure and amenity charge (see Table 1). The need to levy another fee primarily arises because the revenues from the original development charges are often inadequate to fund urban development. This is so because the charges have not increased for various reasons, often because their maximum rates (e.g., rate per square meter of floor space) were fixed by state legislation several decades ago and have not been periodically revised.

For example, the state of Tamil Nadu last revised its development charges in 1996. As a result, revenues are inadequate to meet the rising cost of providing infrastructure and services. Therefore, many states decided to introduce a new revenue source. For example, the Tamil Nadu Town and Country Planning Act (TNTCPA) 1971 and the Planning Authority (Levy of Development Charges) Rules, 1975, allow the use of development charges, whereas the TNTCPA, 1971, and the Tamil Nadu Levy of Infrastructure and Amenities Charges Rules, 2008, allow the use of Infrastructure and Amenity (I&A) Fee. The I&A fee is much higher than developer charges. For example, in the city of Tiruchirappalli in Tamil Nadu, the development charges vary between US$0.05 and US$0.15 per square meter of floor area, whereas the I&A fee is more than 20 times higher, ranging between US$1.07 and US$5.07 per square meter of floor area (Mathur, 2016; US$1 = approximately 70 Indian Rupees).

Similarly, the Orissa Development Authorities Act, 1982, allows the use of development charges, whereas the Odisha Development Authorities (Amendment) Act, 2015, allows the use of City Infrastructure Impact Fee. Please note that the name of Orissa changed to Odisha in 2011.

Furthermore, often times, the new charges apply only to a subset of property types that pay development charges. For example, only apartments and commercial and office buildings pay the Tamil Nadu’s Infrastructure and Amenity Fee, not single-family residences (Tamil Nadu Government Gazette, 2008).

The Enabling Legal Environment

A state-level legal document—usually a piece of legislation—provides the framework for the use of development charges. The legislation is typically of the following two types:

Town and country planning acts that provide the legal framework for all planning activities statewide, including for the use of development charges.

Municipal corporation and development authorities acts: These acts provide the legal framework for all the activities undertaken by a local government such as a municipality or a development authority.

In one case—Rajasthan Township Policy, 2010—planning policies provide the state-level enabling legal framework, and in another—Kerala Building Tax Act, 1975—an act is promulgated specifically to levy development charges. Table 1 lists the enabling legislation for each state.

In some states, the state-level act provides the only legal framework (such as the Bihar Urban Planning and Development Act, 2012). In other states, however, the powers authorized in the acts are exercised as per state-level rules—for example, The Gujarat Town Planning and Urban Development (GTPUD) Act, 1976, is implemented through the GTPUD Rules, 1979—or as per state government notifications, for example, the Punjab Regional and Town Planning and Development Act, 1995, is implemented through various state government notifications.

In a few cases, separate rules are framed to levy development charges. For example, the West Bengal Town and Country (Planning and Development) Act, 1979, authorizes the use of development charges, whereas the Planning Authority (Levy of Development Charges) Rules, 1980, provide implementation details. In a few cases, the act and the rules are in the same document, for example, the Goa Tax on Infrastructure Act, 2009, and Rules.

Findings: Strategies to Promote the Nexus and Rough Proportionality Principles

Below, I summarize whether, how, and how well the various state-level legislation employ strategies identified in Mathur (2016) to promote the nexus and rough proportionality principles.

Vary Charges by Intensity of Use

Usually, the intensity of use of a building/space is directly proportional to the need for infrastructure/services. For example, the larger the retail space is, the greater the number of customers that it is likely to attract. Therefore, development charges are often levied on a per-unit of floor area or land parcel.

In a large majority of the case study states, the charges vary per unit area of land and building. However, in a couple cases, the charges do not vary by building area—in Punjab, they vary only by land area (Government of Punjab, 2005), and in Maharashtra they vary by land value (Government of Maharashtra, 2015). To the extent that the intensity of use is reflected in land values (land parcels in areas with strong real estate demand are utilized more intensely and are also valued more compared with parcels in areas with weak real estate markets), land value is a reasonable proxy for intensity of use. However, this is not always the case. For example, land values might be high due to supply restrictions, such as restrictive building regulations (limitations on height and the floor area ratio [FAR]) and zoning.

To vary the charges, a couple states use additional factors that impact intensity of use. For example, Goa varies the charges in proportion to the maximum allowed FAR (see Table 3), assuming that developers will construct the floor space to the highest FAR allowed (Government of Goa, Daman and Diu, 1977). Haryana provides another variant by classifying cities into three categories based on their potential to attract real estate development—high/hyper, medium, and low potential. The charges increase in proportion to the development potential (Government of Haryana, 1996).

Development Charges Vary by Land Use and Intensity of Use in State of Goa.

Note. US$1 = approximately 70 Indian Rupees as of December 2019. FAR = floor area ratio.

Vary Charges by Property Use

Often, the use of a building/space affects the type and amount of infrastructure/services needed to serve that development. For example, compared with commercial spaces, residences might generate a greater need for libraries, parks, and schools.

In a large majority of states, legislation requires the charges to vary by residential, commercial, and industrial use. One state, Punjab, classifies uses in greater detail, namely, residential plotted (usually single-family houses), residential group housing (usually multistory apartments), commercial buildings, marriage places (buildings rented out for marriage ceremonies), petrol pumps, hospitals/multimedia centers/hotels, institutions, recreational uses, and industrial/warehouses/cold storage. The fee is highest for group housing followed by commercial uses (Government of Punjab, 2016).

In a couple states—Bihar and Mizoram—the enabling legislation does not provide any guidance on whether the charges vary by use. In one state—Uttar Pradesh—the charges do not vary by use.

Expend Funds Within a Specific Area

As development charges are used to fund the infrastructure/services needed by a new development and/or to mitigate negative impacts of a new development, the nexus principle calls for spending the revenues from such charges within a reasonable geographic area around the new development. A new development might require an expansion of a water treatment plant located several kilometers away or might need new sidewalks adjacent to the development. Therefore, the geographic area is likely to vary by infrastructure/service and by locality.

In almost all states, the charges need to be expended within a specified area, usually the area under the jurisdiction of the charge-levying entity (typically a municipal corporation). The state of Punjab uses a zone-based approach. For example, a zone could include an area under a municipal boundary and a 3-km band around it, or a 1-km-wide band around a state highway (Government of Punjab, 2016). However, in a couple cases—Haryana and Tamil Nadu—the charges can be expended statewide, undermining the nexus principle because even though the geographic area impacted by a new development might be large, for example, city- or region-wide, it is very unlikely to be statewide.

Expend Funds Within a Specified Time-Period

In none of the states does the legislation specify the number of years within which the revenues from the development charges need to be expended. Notably, a majority of the state-level pieces of impact fee legislation in the United States stipulate a time requirement, which usually ranges from 5 to 15 years (Mullen, 2015)

Track the Inflow and Outflow of Development Charge Revenue Through a Separate Fund

Tracking the inflow and outflow of revenue, ideally by creating a separate fund, helps strengthen the nexus principle. The states in India show a wide variety of practices, ranging from strong to weak tracking. For example, several pieces of enabling legislation specifically require the fee revenue to flow into a local government fund. For example, the Rajasthan Municipality Act notes that “the municipality shall keep a separate account of such development charge and shall not divert it for any other use” (Government of Rajasthan, 2012).

Uttar Pradesh goes one step further by establishing additional requirements, such as requiring the vice-chairman of the development authority to provide a detailed account of fee revenues and expenditures annually at the first meeting of the fiscal year of the board of the development authority. Uttar Pradesh also requires a development authority to submit this statement to the state government (Government of Uttar Pradesh, 2014a).

Several states employ weaker practices of at least three types. First, in a couple states—Haryana and Tamil Nadu—the revenues go into a statewide fund, making it almost impossible to link expenditures with the development charge–paying properties. Second, in the state of Gujarat, although a separate local-level fund exists, revenues from development charges and several other types of fees flow in and out of it, making tracking the inflow and outflow of development charges difficult. Finally, Odisha’s enabling legislation requires separate fund for one type of fee (infrastructure impact fee) but not for another (development charge), making it possible to track inflow and outflow of revenue for infrastructure impact fee but not for development charge.

At the other extreme, in several states there are no separate funds. Indeed, the enabling legislation in the state of Goa requires that the revenues go into the state’s treasury (equivalent to the general fund of a state in the United States).

Levy Separate Charges for Each Type of Infrastructure and Service

Among the case study states, the charges do not vary by the type of infrastructure and service. In fact, they are used to fund a variety of infrastructure and services, thus weakening the rational nexus principle. For example, charges collected from offices might fund infrastructure/services such as libraries, even though the offices might not have generated the need for libraries.

On a positive note, revenues from development charges can often be used to purchase land and to operate and maintain (O&M) infrastructure/services. This type of usage is a welcome practice because in the absence of adequate funds for purchasing land and for O&M, government agencies might not be able to spend development charge funds, for example, if the funds can be used only to construct a library building but not to operate it or to purchase the land for the library.

Specify the Types of Infrastructure/Services That the Development Charges Can Fund

The enabling legislation in several states—such as Andhra Pradesh’s Urban Areas (Development) Act, 1975—allows the charges to fund any kind of development activity within a specified area, including both capital and operating expenses and the purchase of land. Such a blanket authorization weakens the nexus principle. On a positive note, some states list the kinds of infrastructure/services eligible for funding, though they do so broadly. For example, the Goa Infrastructure Tax 2009 defines infrastructure as “potable water, electricity and other amenities like roads, drains, foot paths, sewerage systems, etc.” (Government of Goa, 2009).

The state of Maharashtra provides limited linkage of charges with infrastructure. The enabling legislation allows development charges to be increased 100% for vital urban transport projects such as metro rail (Government of Maharashtra, 2015).

Base the Development Charges on Detailed Plans and/or Clear LOS Standards

Surveying the state-level impact fee–enabling acts in the United States, Mullen (2015) notes that impact fee calculations are either plan based and/or based on an LOS ratio (e.g., 1.2 ha [3 acres] of parks per 1,000 people). Under the plan-based calculations, first, the cost of infrastructure/services needed to serve the projected growth over the plan period is ascertained. Next, the cost of providing the infrastructure/services is divided by the projected growth in service units (e.g., one firefighter per 1,000 new residents) to calculate the impact fee for each infrastructure/service. Mullen (2015) further argues that since the service unit calculation implicitly assumes a certain LOS, impact fee calculations cannot be made without some implicit LOS standards. However, only half of the impact fee–enabling acts in the United States explicitly require the adoption of LOS standards.

My review of India’s state-level enabling legislation also finds no requirement for adopting LOS standards. Similar to the U.S. examples, I hypothesize that the local/state governments in India use implicit LOS standards when determining the rates for development charges. The case of Haryana, where higher development charges are allowed for areas identified as deficient in infrastructure and services, provide a hint of such implicit standards. However, the threshold/standard for determining deficiency is not specified.

Furthermore, a large majority of states do not require development charges to be based on detailed plans. However, a few pieces of state enabling legislation note the need for a plan, although they do not provide guidance about how detailed the plans need to be. For example, the Rajasthan Municipalities Act, 2009, notes that development charges may be used “in accordance with any development plan or while approving any sub-division plan” (Government of Rajasthan, 2012). Odisha’s enabling legislation is even more ambiguous, calling for the charges to be spent for “city level infrastructure as specified in the development plan in operation and such other purposes” (Government of Odisha, 2015; emphasis by author).

Gujarat’s enabling legislation provides the clearest language. The GTPUD Rules note that when a local authority submits application to the state government for approval of development charges, it needs to provide “statements, plans estimates, development works likely to be undertaken in the area, etc.” (Government of Gujarat, 1979, p. 24). However, the Rules somewhat dilute this requirement by prescribing maximum fee rates. These rates were increased in 2014 for the first and only time, 38 years after they were instituted in 1976. Moreover, the rates are not indexed to any cost of development metrics such as a wholesale price index or construction cost indices.

Calculate the Cost of Development Charge–Funded Infrastructure/Services

No state—except Gujarat and, to a small extent, Punjab—requires a calculation of the cost of development charge–funded infrastructure/services. Coupled with no/little requirement of preparing detailed plans, it weakens the rational nexus principle.

Gujarat’s enabling legislation (GTPUD Rules, 1979) requires that when a local authority submits application to the state government for approval of development charges, it needs to provide “statements, plans estimates, development works likely to be undertaken in the area, etc.” (Government of Gujarat, 1979, p. 24), thereby linking the cost of infrastructure/services to the development charge. Finally, to a lesser extent, Punjab’s state legislation seeks to secure this link by requiring that the charges cannot exceed the total cost of providing the infrastructure (Government of Punjab, 1995). The legislation implicitly assuming that such cost calculations will be made and that revenue from the charges will be compared against such costs.

Exempt Properties That Do Not Produce Negative Impacts; Use the Charges to Mitigate the Impacts of Development Charge–Paying Properties Only

The nexus principle calls for development charges to mitigate the impacts of the development charge–paying properties only. Therefore, properties that do not cause such impacts should be exempt from paying charges.

Almost none of the state-level legislation provides such an exemption although almost all allow the owners of development charge–paying properties to appeal the charge. In a few cases, single-family houses are exempt from paying the charge, perhaps due to the weak assumption that such houses generate no/little need for infrastructure/services. Often, such exemptions are based on the ability-to-pay (ATP) principle. In the field of public finance, the ATP principle calls for the rich to bear a larger share of the cost of government-provided goods and services than the poor. For example, in Goa, single-family houses built on land parcels smaller than 100 m2 are exempt from paying infrastructure tax, whereas houses on larger parcels pay the tax. Goa also exempts building that serve the larger public interest, such as orphanages and old age homes. The legislation notes, “. . . but does not include building constructed for educational institution, orphanage, old age home, home for spastic/retarded children or by any other non-profitable organization and such other organizations as may be notified by the Government in public interest” (Government of Goa, 2009, p. 646). Finally, all pieces of enabling legislation exempt government properties from paying development charges. Notably, even in the United States, where impact fees have traditionally received close legal scrutiny, almost half the state enabling acts do not require waivers and exemptions (Mullen, 2015).

Except for Bihar, no other state enabling legislation provides guidance on whether the fee should mitigate the impacts of the development charge–paying properties only. Bihar’s enabling legislation, the BUPDA Act, 2012, notes, “levy charges so as to meet the impact of development and for providing adequate infrastructure and basic amenities . . .” (Government of Bihar, 2012, p. 64).

Avoid Double Counting

Except for one state, Uttar Pradesh, the enabling legislation of other states does not require steps to avoid double counting, weakening the rough proportionality principle. Uttar Pradesh charges two somewhat overlapping fees—the development charge and the development fee. The development fee is not levied if (a) development charges are payable or if development charges are already paid and (b) the cost of infrastructure has already been covered by other sources (Government of Uttar Pradesh, 2014b).

Current Infrastructure/Services Deficiencies and Ways to Remedy Them

No state enabling legislation requires identifying current infrastructure/services deficiencies and ways to remedy them, weakening the nexus principle because the absence of such identification could lead to the use of development charges to fill existing deficiencies.

Policy Recommendations

The review of the state enabling legislation provides several insights/exemplars to promote rational nexus. At the same time, through examples of how legislation impedes rational nexus, the review highlights pitfalls to avoid. Below, I synthesize the “Findings: Strategies to Promote the Nexus and Rough Proportionality Principles” section and provide key insights for jurisdictions/states in India, and potentially in other Global South countries, that seek to adopt/amend development charge–enabling legislation.

Do Not Stipulate Maximum Allowable Development Charges; Otherwise, Require Periodic Updates

Several states (e.g., Rajasthan and Tamil Nadu) prescribe a maximum rate for development charges without allowing periodic updates except through legislative amendments. Such amendments are susceptible to lobbying and other political vagaries. As a result, over time, especially in countries such as India with historically high inflation rates, development charges cannot keep pace with the rising cost of providing infrastructure and services. Some states have adopted simple solutions—either not prescribing maximum rates or linking such rates to escalation factors. For example, Uttar Pradesh’s legislation requires annual revisions based on a statewide construction cost index or an equivalent index stipulated by the state government (Government of Uttar Pradesh, 2014a).

Use a Direct Measure That Is Proportional to the Intensity of Use

Many pieces of state legislation require jurisdictions to use a direct measure of development intensity to calculate development charges—charges per unit of floor area. However, the review also shows that a few states vary development charges by other, indirect measures, such as land value and land area, which is problematic. However, varying the charges per unit of land area might be suitable in a few cases, for example, when the intensity of use is proportional to the land parcel size—for example, a commercial vehicle yard.

Furthermore, once the charges vary by floor area, overlaying a second parameter—the maximum allowable FAR—as required in the state of Goa, is also problematic because it assumes that the costs of providing infrastructure and services are higher for compact development (a higher FAR leads to more compact development). Such a requirement could incentivize sprawl and contradicts the literature, which suggests that compact development leads to cost savings.

Vary Fees by Property Use Through a Classification System That Is Consistent With Related Planning/Permitting Processes

Several pieces of state legislation require the charges to vary by property use, with a large majority of states using a simple classification typology where the charges vary only by three uses—residential, commercial, and industrial. On the other hand, Punjab provides an example of a more detailed property-use classification. However, jurisdictions should not use a property-use classification system that is more detailed than the classification used for the related planning/permitting processes. For example, from an implementation perspective, it makes little sense to vary the charges by various types of commercial uses (retail, wholesale, petrol pumps, hotels, etc.) if a jurisdiction’s land use plan, zoning, or building bylaws do not differentiate between such commercial uses, or adopt a simpler typology (e.g., only two types of commercial—retail and wholesale). Finally, the legislation in three states (Bihar, Mizoram, and Uttar Pradesh)—which either do not provide any guidance or do not require the charges to vary by use—shows how legislation can impede meeting the rational nexus principle by not requiring charges to vary by property use.

Ideally, Link Planning With Infrastructure/Service Provision; However, Less Optimum Strategies Could Be Employed

Linking planning with infrastructure/services provision is a comprehensive way of ensuring close adherence to the rational nexus principle. Gujarat’s enabling legislation shows how, in very simple language, legislation can require linking development charges with the urban and infrastructure planning processes. As noted earlier, Gujarat’s legislation states that when a local government or its agency (e.g., a development authority or a municipal corporation) submits application to the state government for approval of development charges it needs to “provide statements, plans estimates, development works likely to be undertaken in the area, etc.” (Government of Gujarat, 1979, p. 24). This requirement would compel jurisdictions to calculate the cost of development charge–funded infrastructure/services, keep development charges proportional to the cost of development, and, through the accompanying city/neighborhood planning documents, justify why the infrastructure/services need to be provided. The area under the city/neighborhood plans could constitute the area within which the funds from the development charges would be expended and the timeline for executing the development works would provide the time-period within which the funds would be expended.

However, many local jurisdictions in India as well as in other Global South countries may not have the institutional or technical expertise to develop detailed plans. In fact, as noted earlier, half the states in the United States and most of the states in India do not require detailed plans. In such a scenario, specific requirements can be written into the legislation, such as a clear identification of the geographic area and the time-period within which the funds must be expended.

Simple, Yet Effective Ways Exist to Track Inflow and Outflow of Funds

Although most of the pieces of legislation reviewed for this research hamper the nexus principle by not requiring revenues from development charges to flow in and out of a separate fund, a couple exemplars exist. Rajasthan requires local jurisdictions to create a separate account for each development charge. In addition, Uttar Pradesh requires the agency-in-charge to provide a detailed annual report of development charge revenues and expenditures. These two examples, especially that of Uttar Pradesh, highlight a simple yet effective way of tracking development charge funds.

Exempt Properties That Do Not Produce Negative Impacts and/or Require a Robust Appeal Process

Almost no state in India exempts properties that do not produce negative impacts from paying the charges. Moreover, such exemptions are difficult to provide in the absence of detailed studies. Therefore, it is essential for legislation to provide a robust appeal process to dispute development charges. Almost all the pieces state legislation reviewed for this research either prescribe or allow an appeal process.

Simple Language Can Help Prevent Double Counting

No state legislation in India, except that of Uttar Pradesh, helps prevent double counting. Happily, the simple language of Uttar Pradesh’s legislation (it notes that a development fee cannot be levied if the cost of infrastructure has already been covered by other sources) highlights that state legislation can include text that can help prevent double counting without being particularly prescriptive.

Conclusion

Through a summary and synthesis of India’s development charge–enabling state legislation, this research advances the strand of applied research that seeks to examine ways to make development charges legally defensible by showing how these charges can be designed to meet the rational nexus principle. The extant research in this line of inquiry has been largely U.S.-based and calls for data-intensive studies as inputs for designing the charges. However, conducting such studies is often not feasible in many developing countries. Therefore, I used India as an example to examine whether (a) context-sensitive exemplars of how enabling legislation is promoting or could promote the rational nexus principle in a developing country already exist and (b) what are some of the ways these pieces of legislation hinder the rational nexus principle and how the hindrances can be removed. Finally, I provided several key insights that jurisdictions in India and potentially in other Global South countries can use as they adopt/amend development charge–enabling legislation.

Although this research focused on the rational nexus principle, there are other aspects of development charges used by developing countries that present future research opportunities. For example, it is useful to know what strategies and legislative actions are being taken to mitigate impacts of developer charges on lower income households and small businesses. Furthermore, future research can (a) examine how much of the new infrastructure/services is being currently funded by development charges; (b) examine how the governments uses the funds generated by development charges; (c) conduct financial sensitivity analysis to estimate how much these charges need to increase to significantly fund the infrastructure and services needed; and (d) examine how these charges fit into the larger public finance landscape of developing countries.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received financial support for the research, authorship, and/or publication of this article: The research for this paper was partially funded by the San Jose State University, College of Social Sciences, 2019 Research Grant.