Abstract

Municipalities debating land value taxation or split-rate taxation need empirical evidence to understand how the transition of property tax regimes will affect their tax base. Using a valuable dataset on split-rate taxation from municipalities in Pennsylvania, this article empirically estimates the impacts of split-rate taxation on real estate market values and land values. The estimated impact of switching from conventional property taxation to split-rate taxation on aggregate market values is significantly positive, but the average impact from changing split-rate tax parameters during the sample period is smaller depending on the empirical specification and the sample used. In addition, the impacts vary across property types. Commercial properties appear to benefit more from split-rate taxation compared to residential and industrial uses. The Pennsylvania experience also suggests that split-rate taxes have a negative impact on land values during the sample period, but it does not appear that land values would drastically fall. The findings have important policy implications.

Introduction

Economists contend that a land value tax is more efficient (Mills 1998; Nechyba 1998) and more equitable (George 1879) than conventional property taxes which tax land and structures equally. Henry George's solution to an inequitable wealth distribution (particularly within cities) was a tax on the value of land alone; the proceeds of which would be redistributed to reduce poverty or improving infrastructure. Further, land value taxation is expected to improve economic efficiency since the land is not mobile and is (practically) fixed in supply; it does not distort economic decisions. However, the capital that constitutes the structure on the land is free to move to the best use location, and thus a tax on structures will create distortions in the after-tax return to that capital. Recent studies continue to show that land taxes reduce the distortions in economic behavior and encourage land development (Banzhaf and Lavery 2010; Brueckner 2001; Brueckner and Kim 2003; Capozza and Li 1994; Cohen and Coughlin 2005; Oates and Schwab 1997; Plassmann and Tideman 2000; Yang 2014).

In practice, a variant of land value taxation, a split-rate tax, is more frequently implemented. It taxes the value of land at a higher rate than structures built upon that land. In the United States, approximately twenty municipalities in Pennsylvania have implemented split-rate taxes, including the cities of Pittsburgh and Scranton which adopted a split-rate tax in 1913. In more recent years, a number of smaller PA cities implemented the tax as an effort to stimulate urban economic development and reverse economic decline by attracting new investment. Interestingly, seven municipalities switched back to conventional property taxes after 2000, including Pittsburgh. The underlying causes of these repeals are difficult to determine, but conducting a fair, accurate, and consistent land assessment is difficult; so, when reassessments are needed, they can be politically unfavorable. It appears that most of the municipalities that switched back to traditional property taxation did so around their reassessment years. That said, adoptions and rescindments of split-rate taxation in Pennsylvania provide researchers with an excellent opportunity to examine the impacts of split-rate taxation.

Existing empirical research primarily focuses on the impacts of split-rate taxation on land development. 1 There are a number of simulation studies that explore the distributive impacts of switching from conventional property taxation to split-rate taxation (Cohen and Fedele 2014, 2017; England 2003; England and Zhao 2005). These studies provide valuable insights into the effects of split-rate taxation. An important question for policy makers considering split-rate taxation is how this tax affects the property tax base.

Theoretical research has shown that switching from a uniform property tax to a split-rate tax affects both land and building values. Brueckner (1986) showed that the effect on structure values is expected to be positive due to reduced taxes on structures, but the impact on land values depends on whether the split-rate tax is imposed in only a small part of the housing market or the entire housing market. If it is imposed in only a small part of the housing market, such as one city in a large metropolitan area, the impact is also expected to be positive. Note that when switching to a split-rate tax, the tax rate on structures is normally reduced while the land tax rate is raised. As Brueckner (1986) argued, lowering the structure tax rate indirectly raises land value whereas the higher land tax rate depresses it, but the positive effect of the reduced structure tax dominates the negative impact of the higher land tax, resulting in an increase in land value. However, if the land value tax is imposed on the broader housing market, the impact on land values then depends on the elasticity of housing demand. It remains an empirical question whether switching to split-rate property taxation raises the real estate tax base overall. In addition, the theoretical analysis in that article also suggests that responses vary by types of land with different elasticities of demand. It is expected that the demand for residential land to be different than the demand for commercial or industrial land; therefore, the impact of split-rate taxation varies across different types of land use.

It is worth noting that the implementation of a split-rate tax can not only affect existing properties but also encourage new construction. Oates and Schwab (1997) found that Pittsburgh experienced a significant increase in building activity with several major new office buildings in the central business district (CBD) after its adoption of the split-rate tax. Plassmann and Tideman (2000) also showed that the number of permits significantly rises after the implementation of split-rate taxation. Banzhaf and Lavery (2010) demonstrated that split-rate taxes raise the average capital/land ratio and the primary impact comes from more housing units, rather than bigger units. Our analysis focuses on its impact on the aggregate property tax base which combines the impacts on both existing and new properties. It would be helpful to distinguish between the impact on the value of land and existing structures and that on property values driven by new construction. Due to data limitations, this study does not decompose the effects into the two, but it is an interesting question to address if the data becomes available.

This article uses evidence from PA municipalities that adopted split-rate taxation to investigate the impacts of a split-rate tax on the tax base, which has implications for changes in tax revenue. In addition, we can also learn from those split-rate tax municipalities about how to successfully implement split-rate property taxation as well as lessons or concerns with the implementation. In particular, the study estimates the impact of split-rate property taxation on total property market values using panel data from PA municipalities. It also explores differential impacts across types of land use, such as residential, industrial, and commercial properties. Further, the research separately examines the tax's impact on land values using a recently published dataset.

The results show that the estimated impact of switching from traditional property taxation to split-rate taxation on total market values is significant and positive, but the average impact resulting from further changes in split-rate tax parameters on total market values during the sample period (1990–2018) appears to be smaller. The findings suggest that the tax base may rise after the implementation. As expected, the impacts differ across property types. Switching to split-rate taxation has significant and positive impacts on residential and commercial properties. Commercial properties seem to benefit the most from split-rate taxation among the three property types examined. In addition, the analysis on land values does not suggest that land values would drastically fall; the effect is estimated to be no larger than a 2 percent reduction in land values, should a municipality implement a split-rate tax that taxes land at twice the millage of buildings.

Empirical Specifications

The empirical analysis consists of two parts. First, we estimate the impact of split-rate taxation on aggregate market values, followed by the estimation of differential impacts by property type. Secondly, the study investigates its influence on land values.

Analysis on Aggregate Market Values

Property values depend on various factors, including location attributes, property features, economic conditions, housing demand as well as tax policy. This study considers the following empirical model to estimate the effect of split-rate taxation on aggregate market values:

To capture the real estate tax structure, two tax variables are included. One is the effective total tax rate on land (

The model also takes valuation practices into account. The Pennsylvania STEB was established by the General Assembly in 1947 to compensate for the lack of assessment uniformity statewide in distributing school subsidies. STEB determines the aggregate market value of properties in each subdivision for each calendar year (market value data for our dependent variable). In addition, STEB also computes the common level ratio (the ratio of assessed value to market value) for each county and uses the common level ratio from the previous year to assist with the determination of the range of valid sales used to calculate current market values. 4 We include the lagged natural logarithm of common level ratio as well as the change in the log of common level ratio to account for changes in the market valuation process.

As discussed in the literature, economic and demographic factors also influence real estate market values. Our model includes a set of county-level economic and demographic variables to control for their potential effects. In particular, personal income per capita and unemployment rate are included to account for changes in economic conditions. We expect jurisdictions with higher per capita income to have higher market values. In addition, the following demographic control variables are included: population, percentage of the population that are White, and percentage of population aged 65 and above. 5

One econometric concern with the model above is the endogeneity problem associated with the lagged common level ratio (

We estimate equation (2) via two-stage least squares to obtain the baseline regression results on total market values. To better understand the impacts of split-rate taxation, we consider two alternative specifications. First, we replace the tax rate ratio variable with a policy dummy variable indicating whether a municipality implements a split-rate tax in a given year and estimate a two-way fixed effect model. The policy dummy takes the value of one for municipalities during time periods they implemented a split-rate tax; and zero, otherwise. This alternative specification is shown below:

Secondly, we consider another alternative specification similar to equation (2) except that the tax rate ratio variable is replaced with the difference between the land tax rate and the structure tax rate (land tax rate–structure tax rate). Note that the estimated effect of split-rate taxation from the dummy specification is identified from municipalities that adopted (or rescinded) the split-rate tax during the sample period whereas the impact estimated using the other two specifications is identified from municipalities that changed their tax rate ratio or tax rate difference during the sample period.

After estimating the impact on total market values, we replace the dependent variable with market values by property type to explore differential impacts among residential, industrial, and commercial real estate. As discussed above, three specifications for the split-rate tax variable are considered for the estimation of differential effects.

Analysis on Land Values

The empirical model is similar to equation (1) except that the dependent variable is replaced by the natural logarithm of land values in municipality i at time t and the set of controls for market valuation practices (

Data

The empirical analysis employs aggregate market values and land values as outcome measures. The market value dataset is obtained from STEB; it includes aggregate property market values for all PA municipalities over the period 1990–2018. 8 In addition, the dataset includes the breakdowns of total market values by property type, such as residential, industrial, and commercial types. We use this dataset to examine the impact on the tax base.

The second dataset is the land value dataset from Davis et al. (2020), a Federal Housing Finance Agency working paper. The authors use over 14 million appraisals to derive estimates of land values. 9 These yearly estimates of the average price of land and the average share of house value attributable to land provide the first comprehensive view of land values across the United States. Specifically, the authors use data on cost-approach appraisals from the Uniform Residential Appraisal Report submissions collected by Fannie Mae and Freddie Mac. The study goes through several steps to reduce bias from appraisals with redevelopment concerns and when tied to biased tax assessments. The authors estimate two versions of land values, a standardized one-fourth acre lot value and an “as-is” value. We use the standardized values in this study as the standardization method corrects for the tendency of price-per-acre to fall with size, known as the plattage effect; whereas, the “as-is” values do not correct for this effect.

The Davis et al. (2020) data include a balanced panel from 2012 to 2018 at various levels of geography. This study uses the ZIP code level standardized land value data for Pennsylvania. We chose ZIP codes to optimize across several data limitations including sample size, geographic coverage, and fine geographic detail. The land value data panel includes 3,346 observations at the ZIP code-year level.

In order to match the land value data to the tax policy data, we aggregate the ZIP code data to the county subdivision geography. We use a Census crosswalk file to identify the intersections between each county subdivision and ZIP code. As these two geographies’ borders do not align, the intersections have various amounts of corresponding areas; in other words, each intersection may contain all or only a portion of the county subdivision or ZIP code that constitutes the intersection. This implies the need to weight the ZIP codes’ standardized land values that together constitute a county subdivision. We use the county subdivision housing unit percentage as our weights. For example, six ZIP codes intersect with Abington Township, a county subdivision of Montgomery County. These six ZIP codes each have different estimates of their standardized land values. We weight each ZIP code's land value by the share of Abington Township housing units that reside in each of the ZIP codes. Then, we sum these weighted values over all six ZIP codes. We use housing unit percentage as our preferred weight instead of other measures such as population percentage or land area percentage due to the nature of the property tax being applied to the housing unit. 10 The resulting aggregated land value dataset includes 1,246 unique municipalities, roughly half of the 2,563 municipalities for which we have tax rate data. Of these municipalities, seven institute a split-rate tax. 11

Our main variable of interest is the split-rate tax variable, land-to-structure tax rate ratio (land millage rate/structure millage rate). 12 We update the split-rate tax data used in Yang (2014) by adding split-rate tax information for recent years. Separate tax rates on land and structures are collected for all split-rate taxing jurisdictions by hand. This involved searches on municipal websites or contacting county tax assessment offices directly. Corresponding county and school district property taxes for these split-rate taxing jurisdictions are obtained from Pennsylvania Department of Community and Economic Development (DCED). In addition, we also obtain tax rates at all levels of government for municipalities with conventional property taxes (a uniform tax rate on land and structures) from DCED. 13 The summation of these millage rates on land (which is identical to the total millage rate on structures for jurisdictions with traditional property taxes) enters the model, allowing us to control for the total level of taxation on land. The information on historical and current common level ratios is extracted from STEB website.

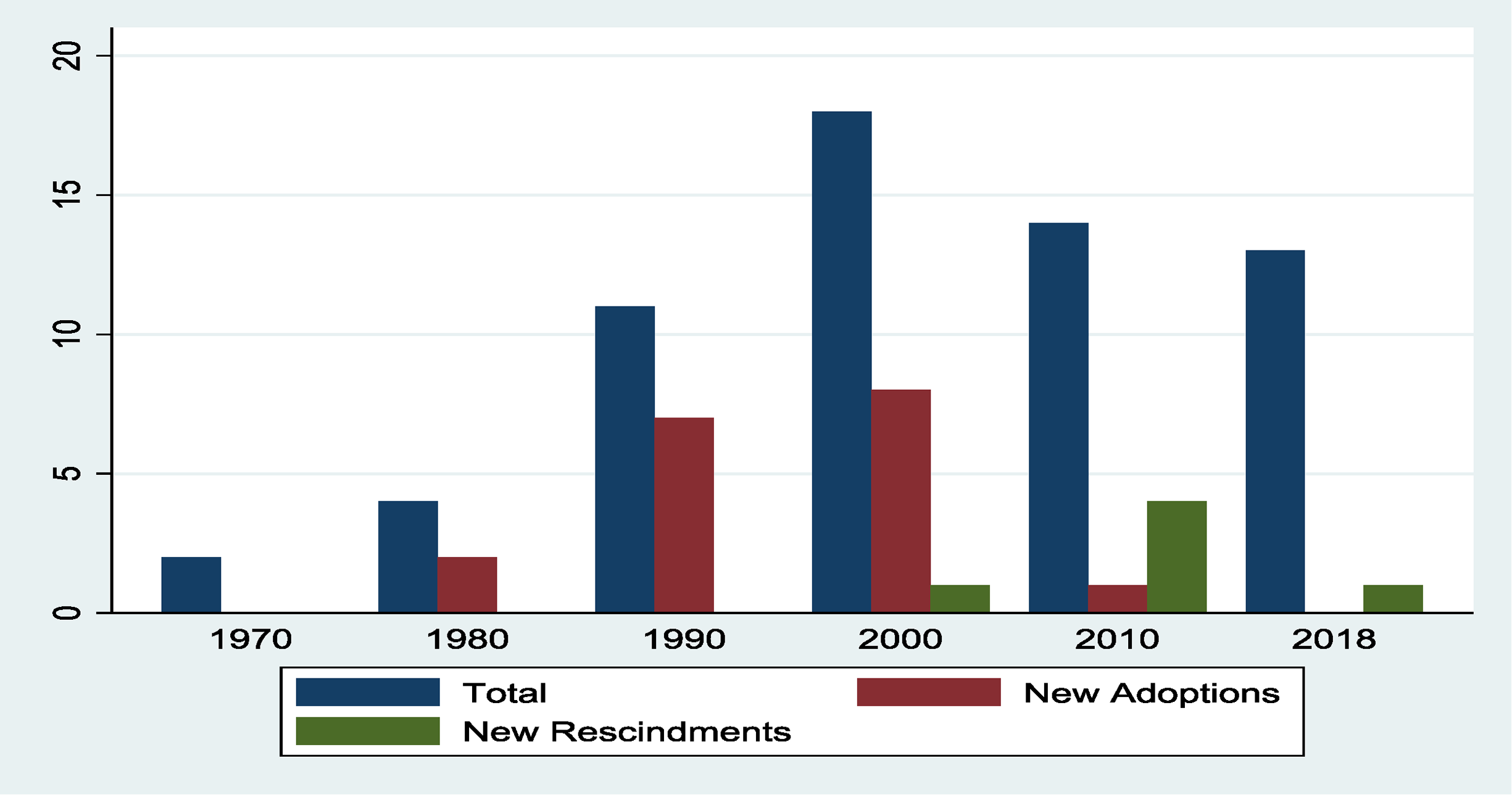

About twenty municipalities in PA implemented split-rate taxes over our sample period. Figure 1 shows the total number of municipalities with split-rate taxation as well as new adoptions and new rescindments by each specified year. By 1980, for instance, a total of four municipalities implemented a split-rate tax, and two of them adopted the tax between 1971 and 1980 (referred to as “new adoptions”). As displayed in the figure, the total number peaked in 2000. In general, our sample includes the period when the total number of split-rate jurisdictions peaked as well as recent rescindments of split-rate taxes, providing important variation for the empirical analysis.

Implementation of split-rate taxation in PA.

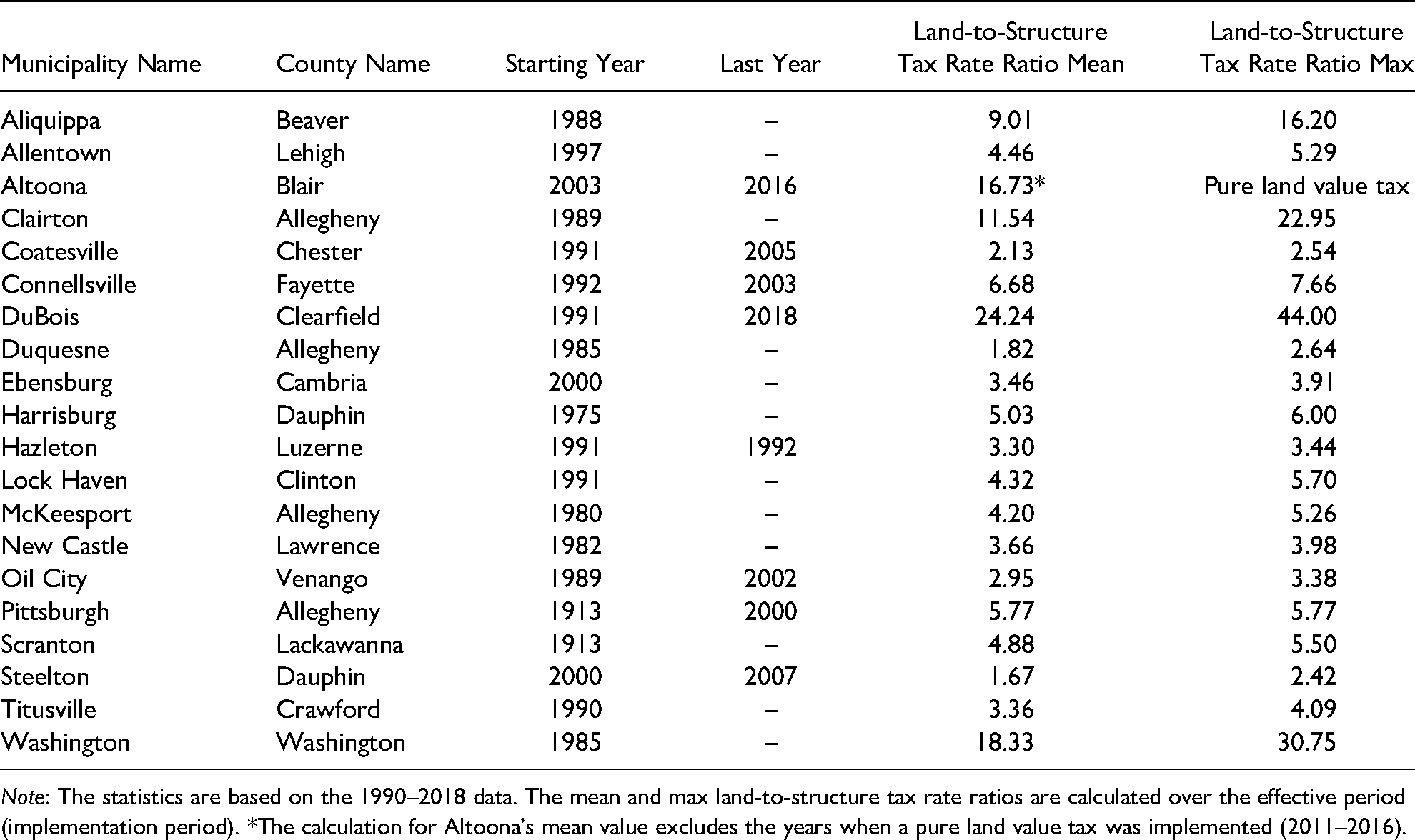

Our data sample also shows significant variation in the split-rate tax variable across municipalities and time. Table 1 shows a list of split-rate taxing jurisdictions with information on corresponding land-to-structure tax rate ratios. Split-rate municipalities are located in sixteen counties across Pennsylvania. Altoona is the only municipality that ever imposed a pure land value tax at the municipality level (2011–2016), but it switched back to traditional property taxation in 2017. The summary statistics show that the land-to-structure tax rate ratio varies across municipalities and time, offering us a great chance to examine the impacts of split-rate taxation. All of these split-rate municipalities are included in the analysis on market values; whereas, only the cities of Aliquippa, Allentown, Altoona, Clairton, DuBois, Harrisburg, Scranton, and Washington are included in the analysis on land values (due to land value data availability).

Split-Rate Municipalities in PA.

Note: The statistics are based on the 1990–2018 data. The mean and max land-to-structure tax rate ratios are calculated over the effective period (implementation period). *The calculation for Altoona's mean value excludes the years when a pure land value tax was implemented (2011–2016).

Results

Estimated Impact on Market Values

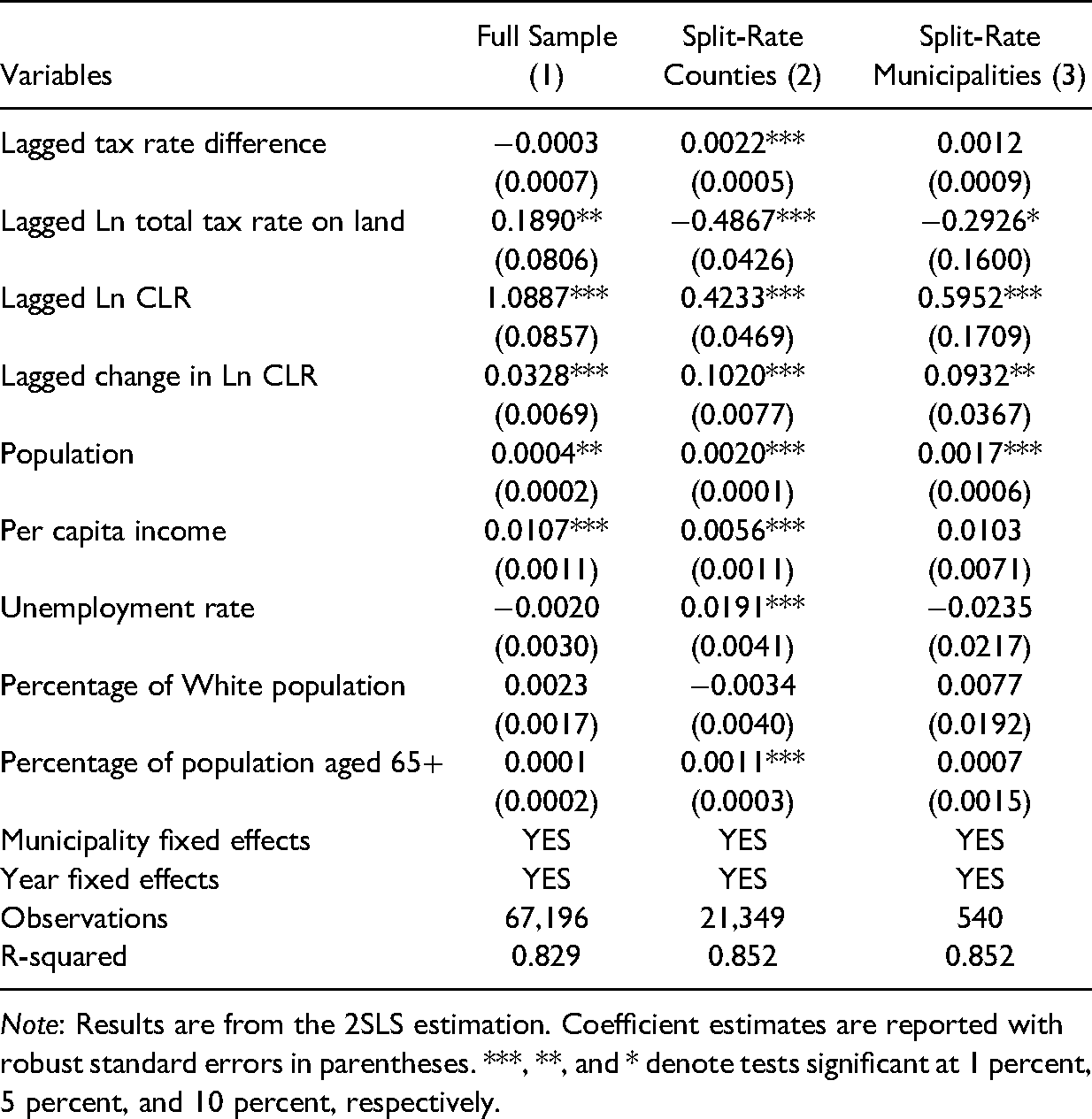

The estimated effects on aggregate market values are reported in Table 2. The land-to-structure tax rate ratio is used as the policy variable in the estimation. The empirical model is estimated using the full sample that includes all municipalities in Pennsylvania (1), the sample with all municipalities in the counties where split-rate municipalities are located, referred to as the split-rate counties sample (2), and the sample with split-rate municipalities only (3). Different samples are used to cope with potential concerns with the estimation. In particular, the split-rate counties sample uses nonsplit-rate municipalities in the counties where split-rate municipalities are located as the control group to mitigate potential omitted variable bias that may arise when using the full sample with data limitations on control variables. Further, the sample with split-rate municipalities only is used to explore the policy intensity effect, that is, how varying split-rate tax parameters would affect the outcomes. This sample focuses on variation in the intensity of the policy among split-rate municipalities and examines the influence of further tuning the policy parameters. The results are different across samples. An examination of the estimated coefficient on the total tax rate on land variable seems to suggest that the regression using the full sample may suffer from omitted variable bias since the sign is counterintuitive compared to the other two. 14 The estimates using the other two samples (split-rate counties and split-rate municipalities) may provide a more accurate picture; therefore, the analysis on aggregate market values by property type will focus on the regression results for the latter two samples. That said, the results from these two samples suggest that the estimated average impact on total market values is zero. 15

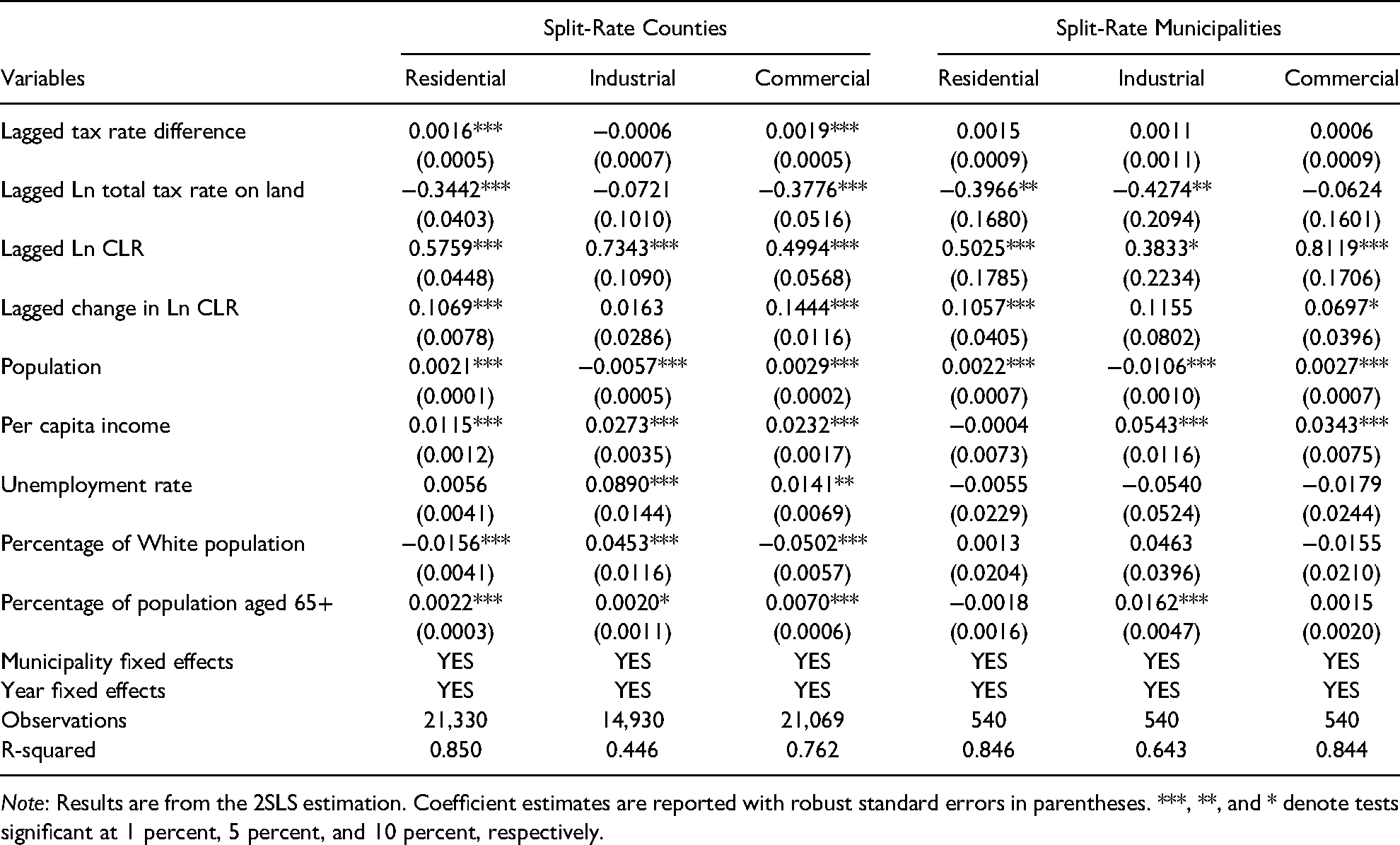

Results on Total Market Values.

Note: Results are from the 2SLS estimation. Coefficient estimates are reported with robust standard errors in parentheses. ***, **, and * denote tests significant at 1 percent, 5 percent, and 10 percent, respectively.

Table 3 reports the set of results from the regressions using the tax rate difference specification. The results from the split-rate counties sample suggest that aggregate market values would rise by about 0.22 percent per unit increase in the tax rate difference. The impact is insignificant in regressions using the other two samples. The regression with the full sample still appears to suffer from omitted variable bias for the same reason mentioned above. The insignificant results from the split-rate municipalities sample suggest that further tuning split-rate tax rate ratios does not seem to have a significant impact on aggregate market values during our sample period.

Results on Total Market Values (Alternative Specification 1).

Note: Results are from the 2SLS estimation. Coefficient estimates are reported with robust standard errors in parentheses. ***, **, and * denote tests significant at 1 percent, 5 percent, and 10 percent, respectively.

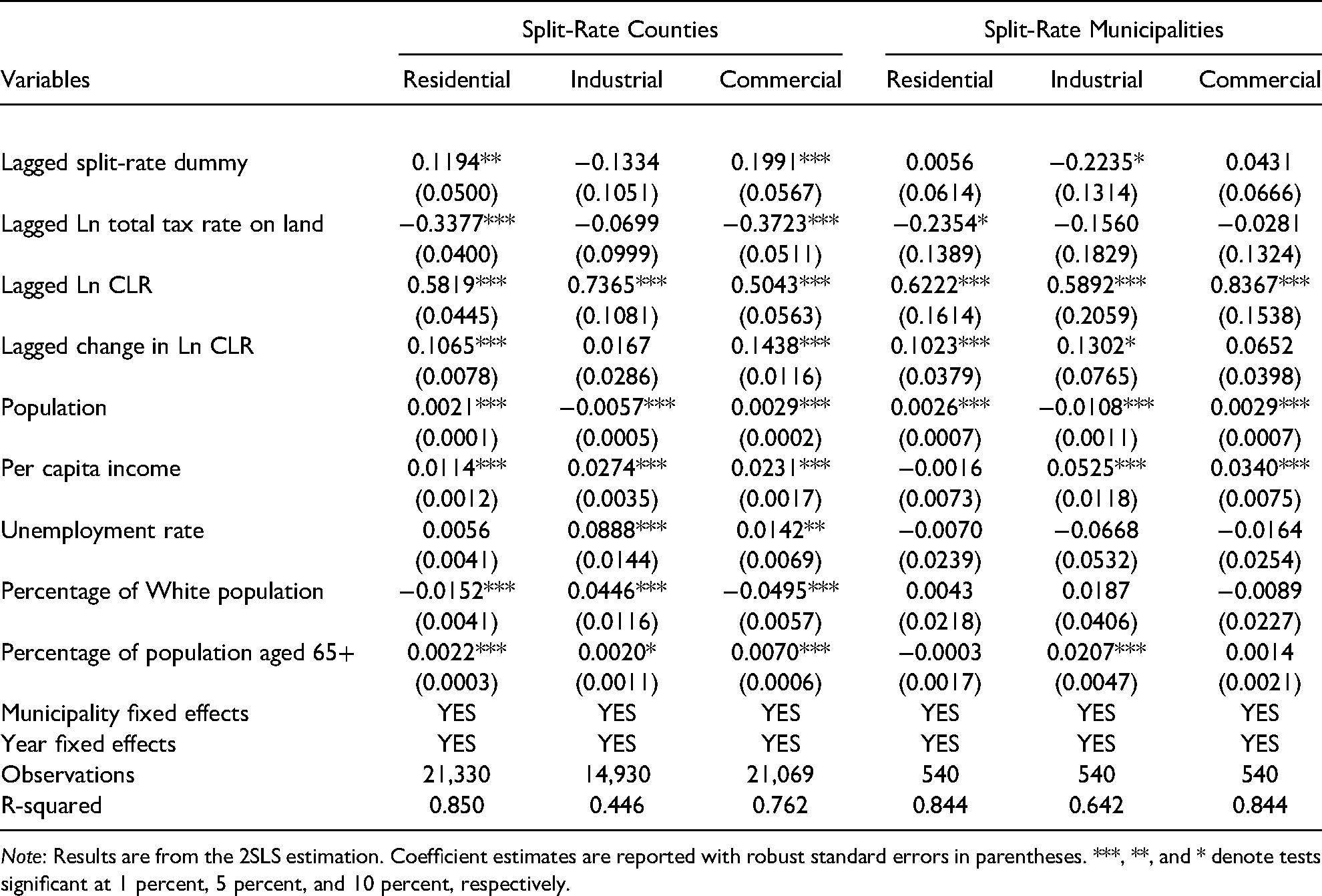

Table 4 displays the results from the models with the policy dummy variable. The estimated impact of switching from conventional property taxation to split-rate taxation is significantly positive using the split-rate counties sample. Again, the results from the full sample are likely to suffer from omitted variable bias.

Results on Total Market Values (Alternative Specification 2).

Note: Results are from the 2SLS estimation. Coefficient estimates are reported with robust standard errors in parentheses. ***, **, and * denote tests significant at 1 percent, 5 percent, and 10 percent, respectively.

To sum up, based on the split-rate counties sample, the results on aggregate market values suggest that the estimated impact of switching to split-rate taxation on total market values is significant and positive, raising total market values by about 21.5 percent, as indicated by the results from the policy dummy specification. After implementation, changes in the tax rate ratio do not seem to affect market values much during the sample period. Increases in the tax rate difference result in higher market values. To compare the estimates across specifications, one can make the estimates from the tax rate ratio and tax rate difference specifications comparable to the one from the policy dummy specification (Banzhaf and Lavery 2010). That is, we can multiply the estimated coefficient on the tax rate ratio or tax rate difference variable by the difference between the average value of this variable for split-rate municipalities and the value for municipalities with conventional property taxation. Following this approach, the tax rate difference model would suggest that the estimated impact (evaluated at the mean) of split-rate taxation is positive, raising aggregate market values by about 12.2 percent. 16

Differential Impacts on Market Values by Property Type

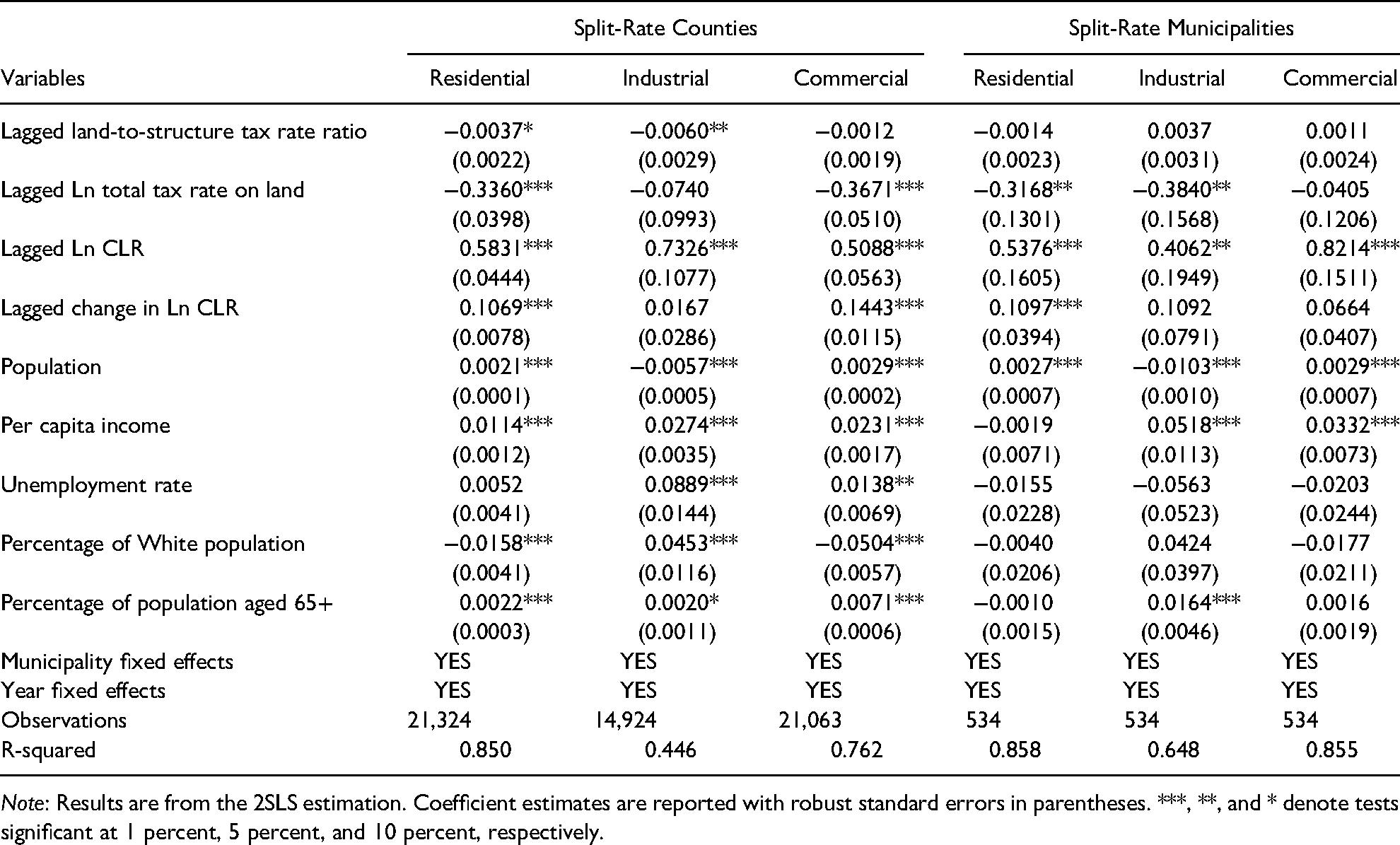

We estimate the models with the three specifications mentioned above for three types of properties: residential, industrial, and commercial. As discussed above, we focus on the results for the split-rate counties sample and the split-rate municipalities sample. Table 5 presents the results from the models using the tax rate ratio specification. Based on the split-rate counties sample, the estimated impact varies across property types with a negative impact on residential and industrial properties, but no impact on commercial properties. It is worth noting that when we allow for nonlinear effects by adding the squared tax rate ratio variable, the negative impact becomes insignificant. 17 The results from the regressions using the split-rate municipalities sample indicate the impacts on all three types are zero, indicating that further tuning split-rate tax parameters does not generate a significant impact during the sample period.

Differential Impacts by Property Type.

Note: Results are from the 2SLS estimation. Coefficient estimates are reported with robust standard errors in parentheses. ***, **, and * denote tests significant at 1 percent, 5 percent, and 10 percent, respectively.

Table 6 reports the set of results from the regressions using the tax rate difference specification. The results for the split-rate counties sample suggest that there are positive impacts on residential and commercial properties, but no impact on industrial properties. Table 7 shows the results from the regressions using the dummy specification. The results for the split-rate counties sample are generally consistent with Table 6, indicating a positive impact on residential and commercial real estate with a slightly larger impact on commercial properties.

Differential Impacts by Property Type (Alternative Specification 1).

Note: Results are from the 2SLS estimation. Coefficient estimates are reported with robust standard errors in parentheses. ***, **, and * denote tests significant at 1 percent, 5 percent, and 10 percent, respectively.

Differential Impacts by Property Type (Alternative Specification 2).

Note: Results are from the 2SLS estimation. Coefficient estimates are reported with robust standard errors in parentheses. ***, **, and * denote tests significant at 1 percent, 5 percent, and 10 percent, respectively.

In all, the impact on aggregate market values differs by property type. Switching to split-rate taxation has significant and positive impacts on residential and commercial properties (as indicated by the results from the dummy specification). Residential properties are estimated to rise by about 11.9 percent whereas commercial properties are estimated to rise by about 19.9 percent. As discussed in the literature, one can make the estimates from the tax rate ratio and tax rate difference specifications comparable to the one from the policy dummy specification (Banzhaf and Lavery 2010). Following the same approach, the results from the first two specifications suggest that the estimated effect of implementing split-rate taxes (evaluated at the sample mean of the split-rate tax variable) on residential market values ranges from a reduction by 2.3 percent to an increase by 8.9 percent. 18 The estimated impact on industrial properties (evaluated at the sample mean of the split-rate tax variable) ranges from a reduction by 3.8 percent to a zero impact. 19 Similarly, commercial properties are estimated to rise by about 10.5 percent after implementing the average split-rate tax policy. 20 Commercial properties appear to benefit the most from the implementation.

The findings have important implications for the implementation of split-rate taxation. As discussed in the Brueckner (1986) article, raising the tax rate on land without lowering the tax rate on structures is unlikely to generate the expected positive results. In fact, the theory suggests that holding the land-to-structure tax rate ratio constant, an increase in the land tax rate (coupled with an increase in the tax rate on structures by the same amount) depresses both land and building values. This would imply that total market values would fall. Our empirical specification enables us to test this theoretical prediction. The estimated coefficient on the total land tax rate variable is significantly negative, supporting the theoretical prediction. 21

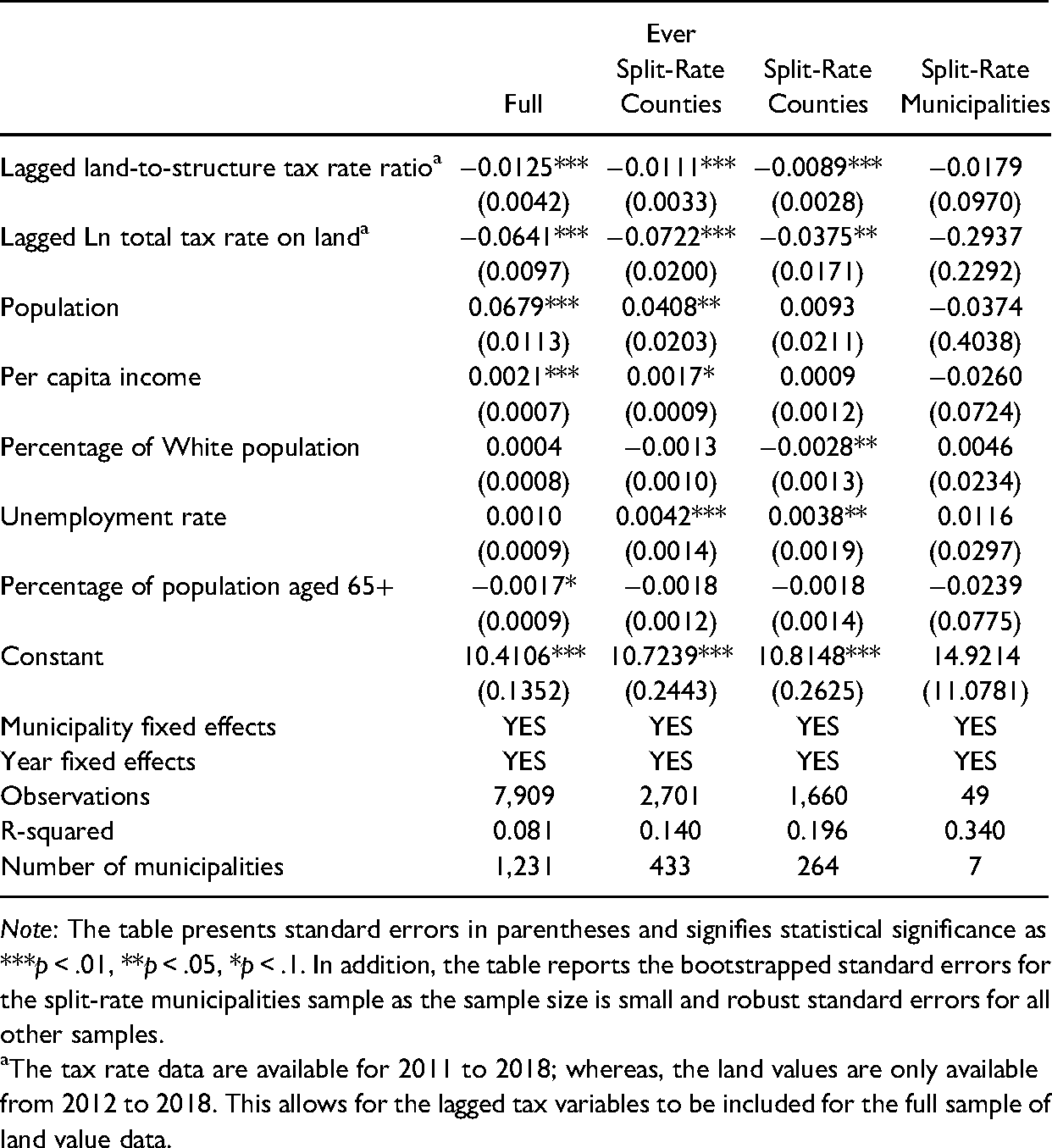

Effect on Land Values (2012–2018).

Note: The table presents standard errors in parentheses and signifies statistical significance as ***p < .01, **p < .05, *p < .1. In addition, the table reports the bootstrapped standard errors for the split-rate municipalities sample as the sample size is small and robust standard errors for all other samples.

aThe tax rate data are available for 2011 to 2018; whereas, the land values are only available from 2012 to 2018. This allows for the lagged tax variables to be included for the full sample of land value data.

Estimated Impact on Land Values

Table 8 presents the effects of split-rate taxation on land values. The estimated impact of a split-rate tax on land values varies based on the sample used. The regressions highlight the importance of choosing a control group from which we compare land values. The first regression uses the full sample of PA municipalities for which we have data. The second identifies counties for which at least one municipality within the county ever adopted a split-rate tax (referred to as the split-rate counties sample above). Municipalities with traditional property taxation in these counties are considered the control group. The third one identifies counties for which at least one municipality within the county had a split-rate tax during the 2012–2018 period. The final regression uses only the variation within the set of municipalities that had a split-rate tax during the 2012–2018 period to identify the effect. This estimation uses a small sample, so we report bootstrapped standard errors.

Across all samples, the estimated sign of the effect is negative; the magnitude of the estimated impact ranges from −0.89 to −1.79 percent change in average land values per unit change in the tax rate ratio. 22 The estimates are all statistically significant except for the split-rate municipality sample. In combination, land values are estimated to remain unchanged or fall slightly, by no more than roughly 2 percent, should a municipality implement a split-rate tax that taxes land at twice the millage of buildings. 23 Assuming a linear impact, a municipality could expect land values to fall by at most 8–12 percent if the land was taxed at five or seven times the rate of buildings, respectively. 24

There are important caveats. Given the data limitations surrounding land values, these results are based on seven municipalities in Pennsylvania. Further, no municipality switched to a split-rate tax during the 2012–2018 time period, though one municipality, Altoona City, does transition back to a standard property tax from a pure land value tax. 25 Further, only three municipalities alter their split-rate tax ratio during the sample period; those that did make a change do so by unconventionally reducing the ratio. In other words, these municipalities reduced the tax burden on land relative to structures, precisely the opposite of the desired implementation of split-rate taxation. The relevance of these impacts are important, but should be kept in context with the differences between these localities and municipalities debating a split-rate tax.

The control variables in the model mostly agree with expectations. As the total tax rate on land in a jurisdiction rises, land values fall. Land values are higher in municipalities with higher population and per capital income. Surprisingly, municipalities with higher unemployment rates appear to have higher land values, though the effect is small. The share of White residents is negatively associated with land values. Lastly, land values fall with higher percentages of elderly population.

Conclusion

The experience of PA municipalities with split-rate taxation reveals important implications for cities debating implementing a change in their property tax regime. The results suggest that there is a significant impact on real estate market values when switching from conventional property taxation to split-rate property taxation, but the average impact from changing split-rate tax parameters on total market values during the sample period (1990–2018) appears to be smaller. As expected, the impact differs across property types. Switching to split-rate taxation has significant and positive impacts on residential and commercial properties. The average impact (evaluated at the sample mean) of varying split-rate tax parameters on residential market values ranges from a reduction by 2.3 percent to an increase by 8.9 percent in our sample. Aggregate commercial property values are estimated to rise by about 10.5 percent after implementing the average split-rate tax policy. Commercial properties seem to benefit the most from split-rate taxation among the three property types. The findings may have important implications for jurisdictions attempting to revive commercial districts.

In addition, the study finds that the effect of split-rate taxation on land values is negative during the sample period. At most, one may expect land values to fall by about 2 percent if a municipality implements a split-rate tax that taxes land at twice the millage of buildings. The findings suggest that there is a potential need to adjust expectations of the tax base for land values when implementing a split-rate tax. It does not appear that land values would drastically fall, at least in the experience of PA municipalities with split-rate taxation from 2012 to 2018.

Our findings also shed light on the implementation of split-rate taxation. The results provide compelling evidence that raising the tax rate on land without lowering the tax rate on structures is unlikely to generate the expected positive results. Consistent with the theoretical prediction, we find that holding the land-to-structure tax rate ratio constant, an increase in the land tax rate (coupled with an increase in the tax rate on structures by the same amount) depresses both land and building values. The findings have important implications for policy makers interested in implementing a split-rate tax. That said, we recognize that the quality of market value and land value data affects our estimates. Using appropriate valuation methods is crucial for the implementation of split-rate taxation as well as for researchers examining the impacts.

Footnotes

Acknowledgments

The authors would like to thank the Lincoln Institute and Invest Detroit for the financial support for this research. They are grateful to county assessment officers for their help with data collection. The authors also thank Mark Skidmore, Adam Langley, Dan McMillen, David Merriman, John Anderson, and Andrew Hanson for very valuable suggestions and comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Lincoln Institute of Land Policy.