Abstract

We adopt a construct validity lens to provide a critical reexamination of established corporate governance research. In particular, we focus on the body of work relying on the theoretical bases of agency theory and involving boards of directors’ independence, CEO duality, equity holdings, and their relationships to corporate financial performance. We offer a five-step protocol involving the following components: (1) establishing the base rate for the phenomenon in question, (2) evaluating the extent to which the dependent variables are germane, (3) evaluating the extent to which the independent variables are germane, (4) determining whether explanatory power is improved as a consequence of improved measurement, and (5) concluding whether previously established estimates should be revised. We implemented the proposed protocol and used alternative measures that reduce threats to construct validity. Results yielded substantially higher estimates of relationships in corporate governance research. Future research can adopt the proposed protocol to understand whether a similar improvement in explanatory power could be achieved in other research domains.

Keywords

Strategic management studies is a fairly young field of inquiry. Specifically, the first volume of Strategic Management Journal was published in 1980 and the Strategic Management Society was created in 1981. As expected of a nascent field of inquiry, the development of strategic management studies was beset by a host of criticism and constructive commentary regarding both its theoretical and methodological foundations and the robustness, or lack thereof, of its research. For example, in an article published in the very first issue of Organizational Research Methods, Hitt, Gimeno, and Hoskisson (1998) identified the lack of attention to measurement as an important problem. Specifically, they noted that “strategic management researchers have shown surprisingly little concern about measurement problems” (p. 29). Addressing issues raised by Hitt et al., construct validity seems to be surfacing to the forefront of the field (e.g., Boyd, Gove, & Hitt, 2005a, 2005b; Boyd & Reuning-Elliott, 1998; Brahma, 2009). However, in an eloquent summary of the state of the science regarding construct validity, Boyd et al. (2005a) lamented that “measurement has been a low-priority topic for strategic management scholars” (p. 367). More recently Ketchen, Ireland, and Baker (2013) revisited a similar theme as follows:

Archival proxies have long played a central role within strategic management research, but the degree to which archival proxies are construct valid measures of theoretical constructs remains a source of concern. In some cases, there does not appear to be a close association between an archival proxy and the construct that the proxy was meant to capture.

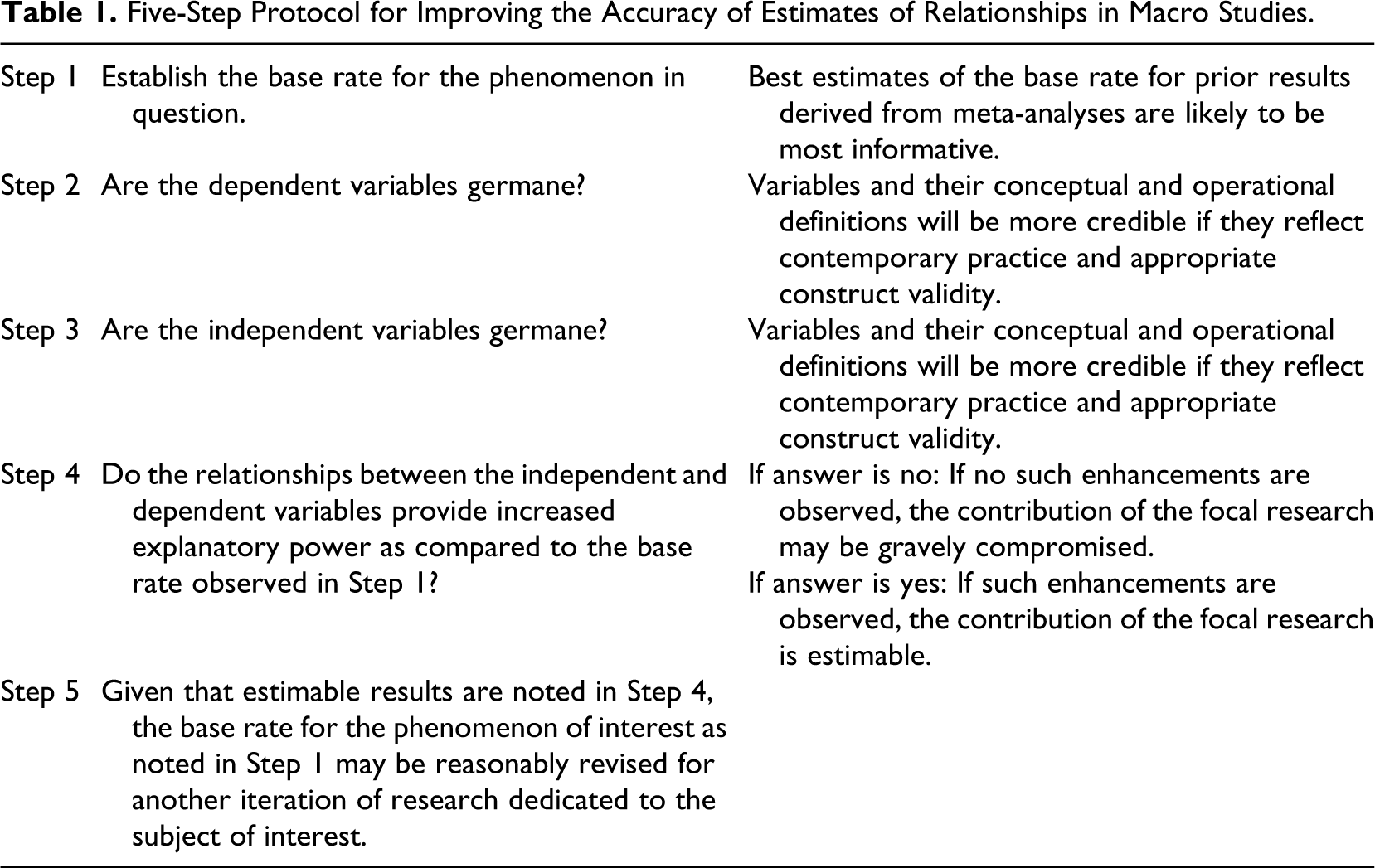

Five-Step Protocol for Improving the Accuracy of Estimates of Relationships in Macro Studies.

In subsequent sections, we first describe a surprising commonality in empirical results across several corporate governance research domains. Second, we argue that this pattern can be explained by common underlying threats to construct validity. Third, we offer a protocol involving five steps to allay these threats. Lastly, having adhered to the five-step protocol, we provide the analyses of heretofore unpublished data that illustrate a clear improvement regarding our knowledge of boards of directors’ independence, CEO duality, equity holdings, and their relationships to corporate financial performance. Although we focus on corporate governance research, we rely on agency theory as a dominant theoretical perspective in strategic management studies.

Making Sense of Homogeneity of Results Using a Construct Validity Lens

Cook and Campbell (1979) and Shadish, Cook, and Campbell (2002) provided a discussion of methodological features that threaten the validity of conclusions. One specific threat related to construct validity is what Cook and Campbell referred to as less than ideal operationalization of constructs (LIOC). This particular threat refers to measures that include contamination (i.e., a measure assesses issues that are not part of the construct) or deficiency (i.e., a measure does not assess issues that are part of the construct but should be assessed). A second threat mentioned by Cook and Campbell is what they refer to as confounding constructs and levels of constructs (CCLC). This occurs when a measure does not include the full range of possible values for a construct of interest.

Notably, the vast majority of research published in the area of corporate governance suffers from the LIOC and CCLC threats. These threats affect both outcomes (i.e., criteria) and predictors. First, consider the issue of less than ideal operationalization of constructs regarding the focal criterion of firm performance. As we describe in the next section, the meta-analytic evidence has relied on return on assets (ROA), return on equity (ROE), and return on investment (ROI). Such measures might be calculated for 1-, 3-, and 5-year periods and be hypothesized to be predicted by, for example, director independence or director equity. In these cases, however, none of these performance variables, irrespective of their magnitude or the extent of their relationship with other measures, provide an indication of direct benefit to shareholders, institutional or otherwise. A company with a relatively high ROA may or may not present with a higher share price over the relevant period; that company may or may not elect to pay dividends or otherwise. Accordingly, such variables do not provide a direct benefit to shareholders, and accordingly, such measures of firm performance suffer from both contamination (i.e., assess issues unrelated to shareholder benefit) and deficiency (i.e., do not assess issues directly related to shareholder benefit).

On the predictor side, corporate governance research relies on the notion of “independence” of the board of directors. Independence is a key construct in most corporate governance research, but unfortunately, its measurement is subject to the CCLC construct validity threat. From the onset of agency theory (e.g., Fama, 1980; Fama & Jensen, 1983a, 1983b; Jensen & Meckling, 1976; Mizruchi, 1983; Ross, 1973; see also Dalton, Hitt, Certo, & Dalton, 2008, for an extended discussion), there has been concern about the independence, or lack thereof, of members of the board of directors. In addition, a recurring theme is the question of whether the CEO should serve simultaneously as chairperson of the board.

We know that by rule, the boards of all publicly traded firms must be comprised of 50% or more independent directors (Gregory, 2009; Sarbanes-Oxley Act, 2002). In addition, we also know that the average S&P 500 board presents with 84% independent directors (SpencerStuart, 2011). For the Fortune 500 with data derived from 2012, the percentage of independent board members is 86.5 (BoardAnalyst, 2012). While these percentages are quite high, they are conceptually understated. Consider, for example, that the average number of board members for Fortune 500 firms is 10.7 (BoardAnalyst, 2012). We also know that all such firms have a CEO (who is not independent by rule; NASDAQ Membership, 2011; New York Stock Exchange [NYSE], 2011a) who always serves on his or her respective board.

In sum, although not acknowledged, it seems that less ideal operationalization of constructs and confounding constructs and levels of constructs may be an important threat to not only the validity of conclusions in agency theory in particular but also corporate governance research more broadly. Specifically, these construct validity issues should lead to small observed correlations between focal variables, regardless of the specific types of relationships examined. In other words, because of measurement contamination and deficiency as well as lack of sufficient variance (i.e., levels of the construct), effect size estimates (e.g., correlations, regression coefficients, proportion of variance explained) involving independence and other variables—regardless of their nature—should be disappointingly small. A brief review of empirical results reported to date seems to underscore the conclusion that adopting a construct validity lens may allow us to reinterpret past findings. Next, we reexamine several such relationships. We do so by offering a brief review of the meta-analytic evidence available, which is the standard for evidence in many scientific fields (Aguinis, Dalton, Bosco, Pierce, & Dalton, 2011; Aguinis, Pierce, Bosco, Dalton, & Dalton, 2011).

Brief Review of Empirical Research Regarding Board Composition

The extensive body of empirical research of board independence issues including several meta-analyses and extensive narrative reviews provides very modest or no support for hypothesized relationships between such constructs and firm performance (Dalton, Daily, Ellstrand, & Johnson, 1998; Dalton et al., 2008; Rhoades, Rechner, & Sundaramurthy, 2000; Wagner, Stimpert, & Fubara, 1998; Walsh & Seward, 1990; see also Zahra & Pearce, 1989). Other summaries echo this perspective. Fogel and Geier (2007), for example, suggested that “there is no predicate, either in logic or in experience, to suggest that a majority of independent directors on a board will guarantee good corporate governance or better financial returns for shareholders” (p. 35). They also noted that the pursuit of board independence is not, even in principle, the appropriate strategy.

Consistent with the guidelines set forth in Table 1, our first step is to establish a base rate for the body of prior research addressing the relationships between board independence issues and performance. For these data we relied on published meta-analyses (M-As) for two reasons. First, the existence of a meta-analysis or several suggests that there is a relatively large body of research addressing such topics. Also, and critically for our purposes, M-As provide a summary mean that provides the best estimate of the relationship between the variables of interest. Accordingly then, by relying on several such M-As, we can derive estimates of the relationships between indicators of board independence and firm performance.

Consider the data upon which Dalton et al. (1998) relied for their meta-analysis of board independence and financial performance. Although not reported by Dalton et al., we used their database to calculate a summary mean and 95% confidence interval (CI) for their results. The overall mean was .015 with a 95% CI of .013 to .018. Dalton et al. also provided meta-analytic data on the relationship between CEO duality (i.e., whether the CEO serves simultaneously as chairperson of the board) and financial performance. That mean estimate was –.041 with a CI of –.019 to –.057. Now, consider results reported by Rhoades et al. (2000) regarding the relationship between board composition and financial performance. The mean effect size is .029, and the 95% CI for this mean estimate ranges from .027 to .030. Next, we sought additional triangulation, which is an important requirement in terms of gathering evidence regarding a phenomenon of interest (cf. Scandura & Williams, 2000). Yet another meta-analysis of board composition and financial performance (Wagner et al., 1998) resulted in a slightly higher relative estimate of the summary mean: r = .068, CI [.065, .071]. Even so, the variance explained is modest, well less than 1%.

In fairness, however, these data and their analyses are based on reports published more than 10 years ago. Accordingly, it may be instructive to compare these results with a more contemporary M-A. For this we rely on Bergh, Aguinis, and Heavey (2011), who conducted a meta-analysis including 864 unique effect sizes based on a collective sample of 308,430 firms as reported in 427 articles. A section of their work also addresses board composition and financial performance. The mean correlation is .035 and the 95% CI around this mean estimate ranges from .031 to .039.

In summary, the mean estimates of relationships between board independence and financial performance are very low. For the relationships over the four M-As on which we rely, these estimates ranged from a low of .015 to a high of .068, with variance explained of .0002 to .004.

Another basic independence notion derived from agency theory is how it might apply to the equity held by members of the board of directors, CEOs, senior executives of the firm, and other constituencies (e.g., institutional investors). One perspective suggests that shareholder and management interests can be aligned by providing an equity stake to executive officers and boards of directors (Boone, Khurana, & Raman, 2011; Jensen & Murphy, 1990; Matta & McGuire, 2008; Shleifer & Vishny, 1997). The counter-perspective provides that equity positions by management and boards often encourage improper and illegal behavior to maintain those managerial equity interests (e.g., Bebchuk & Fried, 2003; Boivie, Lange, McDonald, & Westphal, 2011; Brown & Lee, 2010; Matta & McGuire, 2008; Stuart & Yim, 2010).

Fortunately, there are extensive data that demonstrate the relationship between the equity held by officers and directors of the firm and the financial performance of such firms. From the work of Dalton, Daily, Certo, and Roengpitya (2003), we were able to derive a summary mean (.028) and CI [.021, .034]. Sundaramurthy, Rhoades, and Rechner (2005) also examined the relationship between equity ownership and firm performance. In that case, the mean correlation is .053 and the CI ranges from .047 to .059. The more recent meta-analysis by Bergh et al. (2011) to which we referred earlier also examined equity ownership by the board and firm performance. For the 30 studies on which they had data for this relationship, the summary mean was .07 with CI [.05, .10]. Thus, the percentage of variance explained is very modest and ranges from .003 to .005.

In sum, the meta-analytic evidence gathered thus far suggests that results are disappointedly homogeneous across studies and databases. Moreover, effect size estimates are vanishingly small. These findings are quite consistent across various types of research questions. The only commonality across these diverse bodies of work seems to be the reliance on the same types of measures for predictors (i.e., independence) and outcomes (i.e., firm performance) that suffer from the same threats to construct validity.

Improving the Operationalization of Firm Performance: Total Shareholder Return and Shareholder Voice via “Withhold the Vote”

In the previous section of our article, we established the base rate for the phenomenon of interest (i.e., Step 1 in our protocol). In this section we address whether the dependent variable(s) are germane, including issues about construct validity (i.e., Step 2). As an illustration, we will rely on a firm performance measure rarely relied on in macro studies that relates directly to the individual shareholder. It is referred to as total shareholder return (TSR). In a search of the Econlit and Business Source Premier databases we found only one instance of its use in studies examining, for example, director independence, director equity, and board duality. So, although not used regularly by strategic management scholars, TSRs are now a common indicator of corporate performance and are included in annual reports to shareholders and in Securities and Exchange Commission (SEC) 10-K submissions. There is, then, no doubt that TSRs reflect contemporary practice. TSR is computed as follows:

There is another contemporary development in corporate governance that provides a direct enablement for shareholders. This measure, too, provides another example of an operational connection between theory and practice. Shareholders have increasingly leveraged their statutory capability to “withhold” their vote(s) for directors in the proxy process (for an extended discussion of the development of these enablements such as SEC rule 14a-11 and the Dodd-Frank Wall Street Reform and Consumer Protection Act, 2010, see American Bar Association, 2011; Dougherty, 2011; Goodman, Hing, & Ostrager, 2011). This is a consequential empowerment. Consider that “in recent years, shareholders have relied increasingly on ‘withhold the vote’ or ‘vote against’ campaigns to signal disapproval of board candidates or board policies, instead of seeking to run and elect alternative nominees. These negative campaigns can be powerful catalysts for change” (American Bar Association, 2011, p. 111). This, too, is a consequential enablement whereby shareholders, individuals who own relatively few shares in the enterprise or institutional investors who may hold the vast majority of the firm’s equity, may directly register their disapproval by withholding their vote for the renewal of directors (including the CEO in his or her capacity as a member of the board). This variable, too, reflects contemporary practice and improved construct validity as well.

Improving the Operationalization of Board Independence: Related Party Directors

We continue to follow the five-step protocol summarized in Table 1 by addressing whether the independent variable(s) are germane, including issues about construct validity (i.e., Step 3). NYSE and NASDAQ guidelines provide an interesting insight with regard to the independence or otherwise of board members (see Gregory, 2009; NYSE, 2011b). These include elements such as having no material relationship with the company, not being an employee of the company within the last 3 years, and not having received more than $120,000 during any 12-month period from the company (not including compensation as a director). Notably, what is not included is a person referred to as a “related party” director (aka a “constituent director,” “constituency” director, a “designated” director, a “representative” director, or a “special interests” director; for general discussion, see, e.g., Morris, Herzeca, & Kamps, 2008; Nathan, 2010; Veasey & Guglielmo, 2008). Thus, the proportion of related party directors on a board can serve as an alternative measure of independence.

Among the earliest examples of such directors were agreements between U.S. automobile industries and its unions. In some cases, the union had bargained for a seat on the automobile company’s board of directors. With regard to the “loyalty” issue to which we referred, what would be most observers’ intuition about whose loyalty was served by the union’s representative on the board of directors? At this time, in fairness, such an arrangement was unusual. In later years, this phenomenon (potentially unaligned “outside” director loyalty) was often observed in venture capital (VC)–backed company’s boards of directors (Director Accountability and Board Effectiveness, 2007). Again, the basic issue was the extent to which such directors aligned their loyalty with the company on whose board they served or of the VC-backed company that arranged for their membership on the board. Do such directors have a parochial perspective, and will they, accordingly, advocate the views of the parties they represent? More recently, another interesting aspect of this phenomenon includes the U.S. federal government, which under the authority of TARP (Troubled Asset Relief Program) named new directors for several benefitted companies (e.g., “TARP Companies Make More Changes to Board Composition,” 2009; “Treasury Names Five New Directors to GM’s Board,” 2009). This trend toward related party directors on various boards is no longer a curiosity. Indeed, driven largely by activist investors, the number of such constituency directors has been estimated at 400 (Nathan, 2010). This is yet another aspect of the contemporary publicly traded company and its intersection with board independence that has, to our knowledge, not been addressed by the academy.

Reexamination of Substantive Construct-Level Relationships Using Improved Measurements

For this section in our article, we refer to Table 1’s Step 4, in which it is suggested that relationships between independent and dependent variables that reflect contemporary practice and improved construct validity be compared to measures without that character. The issue is whether the former relationships provide increased explanatory power compared to the latter.

In addressing Step 1 in our protocol, we reported meta-analytically derived mean estimates of hypothesized relationships between commonly relied upon constructs in corporate governance research, particularly those grounded in agency theory. Moreover, we have suggested that research based on contemporary operationalizations of these variables (e.g., total shareholder returns, percentage of votes withheld, related party directors) may provide better estimates of underlying construct-level relationships (i.e., Steps 2 and 3). The data on which we relied for the following sections are publicly available and drawn or derived from BoardAnalyst.com (board independence, CEO duality, officer and director’s equity, institutionally held equity, outside related directors, votes withheld), Wharton Research Data Services (WRDS; total shareholder returns; https://wrds-web.wharton.upenn.edu/wrds/), and AnnualReports.com. Moreover, the data used for our analyses are available from the senior author upon request.

Duality: Should the CEO Serve Simultaneously as Chairperson of the Board?

As noted earlier, Dalton et al. (1998) provided meta-analytic data on the relationship between CEO duality (i.e., whether the CEO serves simultaneously as chairperson of the board) and financial performance. That mean estimate was –.041. When we relied on percentage of vote withheld, however, the relationship was .19. In terms of our ability to explain firm performance, analyses relying on traditional measures resulted in .17% of variance explained, whereas our reanalysis based on percentage of vote withheld, a measure more proximal to shareholders, the percentage of variance explained is increased to 3.61%.

Boards of Directors Independence and Firm Performance

Prior meta-analyses of the relationship between board independence and firm performance resulted in mean estimates of .015 (Dalton et al., 1998), .029 (Rhoades et al., 2000), .068 (Wagner et al., 1998), and .035 (Bergh et al., 2011). Our analyses of the percentage of independent board members with TSRs, however, provided a substantially higher estimate of .133.

Officer and Directors Equity, Institutionally Held Equity, and Firm Performance

Prior meta-analyses provided estimates of the relationship between officer and director equity and firm performance. Such relationships have been uniformly modest: .028 (Dalton et al., 2003), .053 (Sundaramurthy et al., 2005), and .07 (Bergh et al., 2011).

Our analyses relying on TSRs as the dependent variable provide an interesting result. While the relationships between for 1-, 3-, and 5-year TSRs and officer and director equity are unremarkable (.036, –.004, and .022 respectively), the relationship between officer and director equity and 10-year TSRs, however, is a comparatively notable, .18. In terms of proportion of variance explained, past research suggests that it ranges from .08% to .49%. Using TSR as the measure of firm performance leads to an estimate as high as 3.24%.

The prior meta-analyses to which we referred did not address institutional equity. Our analyses of 1-, 3-, 5-, and 10-year TSRs and institutional equity held in firms were not consequential: .02, –.046, .056, and .001. So in this particular case, improving the construct validity of the outcome measure did not produce a substantial change in the results.

On the Bearing of Related Party Directors

In an earlier section we argued that related party directors constitute a far more robust threat to director independence than the commonly relied upon simple tally (usually the percentage of independent directors on the board). Interestingly, our results—consistent with prior results—suggest the basic notion that director independence is simply not an issue with regard to TSRs. Also, it is of no consequence with regard to withheld votes.

The relationship between the percentage of related party directors on the board and TSRs was .029 (1-year TSRs), .015 (3-year TSRs), –.052 (5-year TSRs), and –.064 (10-year TSRs). The relationship between the percentage of related party directors and withheld votes was –.039 (1-year TSRs), .064 (3-year TSRs), –.054 (5-year TSRs), and –.001 (10-year TSRs). In other words, our proposed solution for improving the measurement of the independence construct did not lead to a substantial improvement in the resulting effect size estimate.

Discussion

In this section, we arrive at the fifth and last step of the protocol summarized in Table 1. Because we were able to provide substantially higher estimates of relationships when relying on measures that reflect contemporary practice and improved construct validity, we do believe—consistent with Step 5—that we have exceeded the previous base rates for the phenomena in question. The meta-analyses that we reviewed resulted in bivariate correlations that are homogeneously low.

Step 5 also suggests that higher base rates warrant other iterations of research dedicated to the subject of interest. Given the demonstrated base rates, the relationships of interest may now be reasonably considered and included in other analyses, including those examining moderating and mediating effects and structural equation modeling (e.g., Aguinis, Bergh, & Joo, 2011).

There are other, perhaps more subtle but no less impactful, examples of improved measures in corporate governance. Consider the executive committee of the board, for which there are no guidelines for the independence of its membership. Consider also that 38.3% of the Fortune 500 companies do have executive committees (BoardAnalyst, 2012). Committees of this sort enjoy broad authority as illustrated by the charter of the Wal-Mart board of directors:

The Executive Committee is appointed by the Board to exercise the powers and duties of the Board between Board meetings and while the Board is not in session, and implement the policy decisions of the Board… The Executive Committee shall have the authority to exercise all powers and authority of the Board, including without limitation the powers and authority enumerated in the By-laws of the Company. (Wal-Mart, 2011)

In this spirit, perhaps there is some promise for “profile” analyses. Perhaps a firm relying on a CEO who serves simultaneously as chairperson of the board, utilizes an executive committee (on which the CEO/board chairperson of the firm also acts as chairperson), and is composed of a high percentage of related party directors will be associated with different outcomes than will a polar opposite example—CEO and board chairperson are separate, no executive committee, no related party directors.

The potential advantages of the techniques on which we have relied are clearly not restricted to research relying on the agency theoretical bases and the common corporate governance variables reported in our article. Consider, for example, that any macro research could be driven, or at the least supplemented, by attention to corporate governance dependent variables that are relied upon in contemporary practice. Fortunately, driven by the guidelines of the Securities and Exchange Commission, such variables are easily identified. Also, it is notable that these indicators are not only now available to the SEC, but constitute notice of reliance on such indicators to the filer’s many constituencies.

In 2003, for example, the SEC released the guidelines of the Management Discussion and Analysis (MD&A) section that would henceforth be required for 10-K (annual report) filings (SEC, 2003). In this MD&A filing, the key performance indicators on which the filing company relies must be reported (SEC, 2006). Such a dictate is an important enablement to the research community. On an annual basis, for instance, researchers can be aware of the performance indicators on which filers rely. Beyond that, researchers can easily track changes in these reported indicators over time.

Similarly, in 2006 the SEC provided guidelines for the Compensation Discussion and Analysis (CD&A) section of 10-k (annual report) filings (SEC, 2006). These guidelines require that indicators of company performance upon which the filing company relies in setting compensation policies for its named executive officers (NEOs–CEO, CFO, and the three most highly compensated individuals [other than the CEO and CFO]) must be included in the filing. Through this filing, then, researchers can determine exactly what indicators of company performance are consequential to the firm. As previously noted, the reliance on such corporate performance data in the 10-K, CD&A data are not only filed through the SEC, but also constitute notice of such reliance to the filer’s many constituencies.

With regard to contemporary practice and improved construct validity, our work may have demonstrated some improvement in the scale of relationships associated with corporate governance. Boyd et al. (2005a, 2005b) provided an alert to the academy about the extant threats related to measurement problems in strategic management research, including construct validity. Based on a data base of M-As from 1980 to 2011 described by Aguinis, Dalton, et al. (2011), we conducted an examination of the summary means of M-As in macro studies prior to 2005 and those in the period after the publication of the Boyd et al. articles. The summary mean for the prior period was .21; in the subsequent period, the summary mean was .22. Thus, unfortunately, it seems that not much progress has been made and much work remains to be done. We hope that our proposed five-step protocol will be instrumental in guiding such future efforts.

Footnotes

Acknowledgments

We thank Brian Boyd and four Organizational Research Methods anonymous reviewers for highly constructive and detailed feedback that allowed us to improve our manuscript substantially.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.