Abstract

Neurofinance is a relatively new area of research that strives to understand financial decision making by combining insights from psychology and neuroscience with theories of finance. Using behavioral experiments, neurofinance studies how we evaluate information about financial options that are uncertain, time-constrained, risky, and strategic in nature and how financial decisions are influenced by emotions, psychological biases, stress, and individual differences (such as gender, genes, neuroanatomy, and personality). In addition, it studies how the brain processes financial information and how individual decisions arise within it. Finally, by combining these experiments with computational models, neurofinance aims to provide an alternative explanation for the apparent failure of classic finance theories. Here we provide an introduction to neurofinance and look at how it is rooted in different fields of study. We review early findings and implications and conclude with open questions in neurofinance.

Finance studies money and markets which includes anything from the interest rate on your savings account to stock markets to the impact of new tax laws on a country’s economy. Traditional finance describes how prices develop and how to best allocate economic resources when financial options are uncertain, time-constrained, risky, and strategic in nature (Peterson, 2010). Economic bubbles such as the housing market bubble are just one indicator that investors are not always able to rationally evaluate and incorporate information in their financial decisions, thus violating a key assumption of traditional finance. Consequently, behavioral finance—a subfield of behavioral economics—emerged to empirically study and account for these violations. By incorporating insights from other social sciences such as psychology and sociology it demonstrated that our financial decisions are influenced by emotions, psychological biases, stress, and individual differences. The insights gained and their impact on financial theories caused some researchers to go one step further and ask how and why these violations arise in the brain and whether incorporating findings from neuroscience could further improve existing models, thus giving rise to the field of neurofinance.

Neurofinance strives to understand financial decision making by combining insights from fields such as psychology and neuroscience with traditional theories of finance. In addition to explaining individual and market behavior as a function of classic financial variables, it aims to explain how neural and physiological signals relate and give rise to individual differences in financial decision making. To this end, neurofinance incorporates noninvasive measures of neural and physiological activity. Functional magnetic resonance imaging (fMRI) and electroencephalography (EEG) are indirect measures of local brain activity. These are complemented by physiological signals such as heart rate, skin conductance, eye movements, and hormones as well as genetic analysis (Cohen, 2005; Rangel, Camerer, & Montague, 2008). Note that all of these methods are correlational in nature and generally do not allow causal conclusions (Poldrack, 2006). To establish a causal relationship to the observed behavior, researchers manipulate neural and physiological signals by using direct transcranial magnetic stimulation (TMS), by studying patients with brain damage, or by administering hormone- and neurotransmitter-manipulating drugs.

Neurofinance partially incorporates behavioral finance but adds two major goals: (a) elucidating the biological (neural and physiological) mechanisms of behaviors of financial market participants (Tseng, 2006); (b) providing a physiologically motivated, alternative explanation for the apparent failure of standard finance theories.

This review provides an introduction to neurofinance. As it is beyond the current scope to discuss every aspect of neurofinance, we will focus on the primary topics and present a selection of representative findings. We then identify the most promising areas for future research that could lead to societal benefits and to building bridges between neuroscience and applications in business and everyday financial decision making.

To further the dialogue between neuroscience and other fields studying decision making at an individual and organizational level, we offer examples of experimental studies where integration of neural data helped test hypotheses from economics and finance that would otherwise have been difficult to address. Organizational scholars could employ neuroscientific methodology to answer questions where the physiological data can provide unique metrics, such as in deciphering individual differences in decision making and leadership skills, including differences in processing information, understanding the delicate balance of extrinsic and intrinsic motivation on performance and decision making, explaining the underlying cognitive processes in group decisions, and finally adding an additional layer of explanation to consumer choice behavior.

The paper is structured as follows. The second section reviews research on financial decision making, first within traditional finance and then in neuroscience and psychology. The third section looks at how investor behavior can be studied and described by combining approaches and findings from these different fields. Special attention will be paid to gender differences in financial decision making. Finally, the fourth section identifies open questions in neurofinance. To aid the reader, we included a glossary of the most common neuroscientific and financial terms referred to throughout the text in Table 1.

Financial Decision Making

From Traditional Finance to Behavioral Economics

Traditional financial theory centers around the efficient market hypothesis (EMH), which states that one cannot consistently beat the market (Fama, 1998). It claims that all available information is rationally evaluated and incorporated in prices leaving little to no arbitrage opportunities. However, highly successful investors such as Warren Buffett as well as prolonged economic bubbles are difficult to explain with the standard EMH, and many question its validity. Its primary assumption that we are rational agents with perfect information who make decisions that maximize their (expected) utility (Cohen, 2005; Markowitz, 1952) appears to be frequently violated. As a result these models often fail to explain how individuals make decisions under real circumstances. 1 For instance, empirical studies revealed that investors demonstrate loss aversion (Rabin, 2000) or do not update their preference in the face of new evidence (Barberis & Thaler, 2003), both of which violate the principle of expected utility.

More recently, behavioral finance and behavioral economics (Camerer, Loewenstein, & Rabin, 2011) emerged to describe and explain systematic biases and deviations from the assumption of rational decision making (Camerer, 2004; Kahneman & Tversky, 1979; Simon, 1956). These fields rose to prominence when Kahneman and Tversky conducted a series of behavioral experiments that involved choices between risky prospects in an attempt to quantify these deviations. They subsequently developed prospect theory which captures several observations: (a) “losses loom larger than gains,” which results in separate value functions for losses and gains, and (b) people tend to overweight low probabilities and underweight moderate and high probabilities, which translates into a nonlinear transformation of probabilities (Tversky & Kahneman, 1992). It also describes (c) the reflection effect, which shows that people are risk-averse for prospects of gains and risk-seeking for prospects involving losses (Camerer, 2004; Madan, Ludvig, & Spetch, 2017).

Although numerous studies demonstrate that incorporating insights from behavior and psychology can reduce the discrepancies between theory and empirical evidence, the predictive power of these more realistic models still needs to be improved (Hirshleifer, 2015). Therefore, a primary goal of neurofinance is to further improve models of financial decision making and market behavior by investigating how the brain processes financial information and makes decisions.

A Biological Perspective

When traditional finance and economics talk about maximizing utility and wealth they usually mean utility and wealth that is derived from goods and money. Biology and psychology would argue that maximizing this utility is only one aspect of achieving a larger goal, that is, to maximize our biological fitness (chances of survival) and our overall well-being. As such, the observed deviations from economically optimal choices may actually be biologically optimal. Cognitive limitations may also prevent people from maximizing their utility causing them to satisfice that is to aim for a satisfactory or “good enough” result rather than the optimal solution (Cohen, 2005; Simon, 1956).

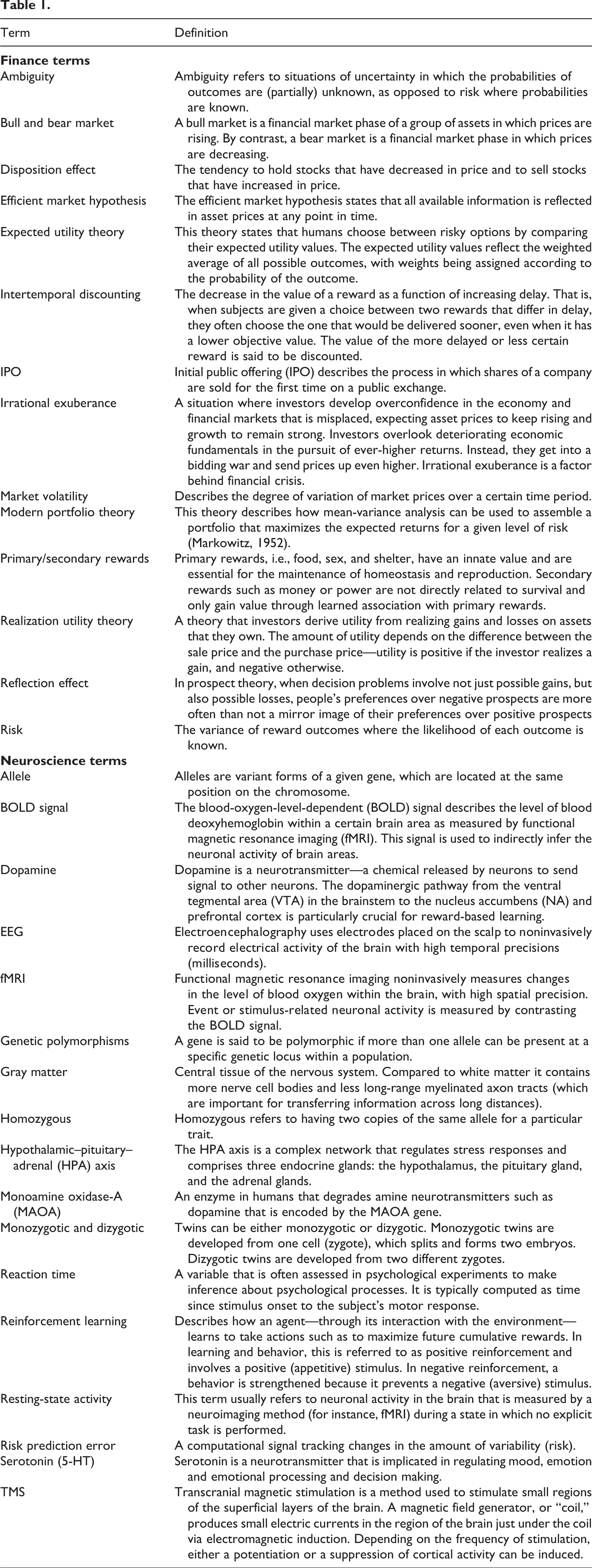

As the human brain has evolved over millions of years to survive in natural environments (and not in financial markets) it should not come as a surprise that humans often struggle with financial decisions. Evolutionary pressure has provided animals and humans with two basic motivational tendencies: approach and avoidance (Elliot & Thrash, 2002; Knutson & Greer, 2008). They are associated with positive and negative affective states, often referred to as rewards and punishments (Alcaro & Panksepp, 2011), respectively. Despite their opposing effects on behavior, the two mechanisms are thought to be mediated by distinct but largely interconnected neural pathways (Alcaro & Panksepp, 2011; Bromberg-Martin, Matsumoto, & Hikosaka, 2010). Both the approach and avoidance system include brain regions that have been associated with financial concepts such as reward and risk on the one hand, and with emotions on the other hand. Figure 1 below shows several such regions. The substantia nigra/ventral tegmental area (SN/VTA) and the ventral striatum (left) are part of the dopaminergic system and are consistently (though not exclusively) associated with reward and reward-based learning and thus approach behavior. The insula and amygdala (right) are hypothesized to be part of an avoidance system (Knutson & Greer, 2008; Paulus, Rogalsky, Simmons, Feinstein, & Stein, 2003; see Figure 1 right). The insula is consistently linked to risk and uncertainty though an at least equally large literature describes its role in disgust, pain, empathy, and bodily states. The amygdala, too, was primarily associated with emotional relevance detection, in particular fear, before its potential role in financial decision making was further elucidated (Canessa et al., 2013; De Martino, Camerer, & Adolphs, 2010; Weller, Levin, Shiv, & Bechara, 2007).

Most frequently identified structures in reward and risk processing.

Finally, these neural systems have evolved mechanisms to quickly adapt to new environments. The brain’s capacity to dynamically change its structure and functions is termed neuroplasticity and underlies the ability of humans and animals to learn. For instance, through their interaction with the environment humans and animals learn to select actions associated with rewards and avoid actions associated with punishments. This reward-based learning is primarily mediated by the dopaminergic system, which drives learning that is based on primary (e.g., food) and secondary (e.g., money) rewards (Valentin & O’Doherty, 2009). Many behavioral patterns that are considered irrational in financial decision making are consistent with reward-based learning where previous choices are positively reinforced, that is, more likely to be repeated if they were followed by a gain in the past. For instance, investors prefer to rebuy stocks that they have previously sold for a gain (Barber, Lee, Liu, & Odean, 2014). Investors’ likelihood to participate in an IPO auction further increases if they have made high returns in previous IPO auctions (Kaustia & Knüpfer, 2008), and subjects who experience high returns and low variance from their savings increase their saving rate more than investors who did not make such positive experiences (Choi, Laibson, Madrian, & Metrick, 2009).

From an evolutionary point of view money is a special reward. While food and sex (called primary rewards) will generally contribute to our survival, a piece of metal will not until it is minted into a coin for which we can buy food. In other words, money and other secondary rewards are only valuable due to their association with primary rewards. While such secondary rewards recruit similar brain mechanisms they do not necessarily lead to equally well-adapted decisions. First, in contrast to consumable rewards such as food, money is nonperishable and degraded less by delay, that is, discounted less steeply (Odum, 2011). Second, secondary rewards are unlikely to have contributed to the evolution of the approach and avoidance system. Thus, our neural “hardware” is somewhat ignorant of the properties of secondary rewards and will try to maximize them in the same manner as primary rewards. As a consequence, our brains are not particularly adept at generating advantageous financial decisions. In fact, their biologically adapted nature is likely the cause of several behavioral biases, such as attention to extreme outcomes and maximization of relative, subjective rather than objective gains (Platt & Huettel, 2008) and may explain the well-known “irrational exuberance” (Shiller, 2016) in financial markets.

For instance, using naïve reinforcement learning in financial decisions does not seem to effectively increase the performance of individual investors. In financial markets high past returns (rewards) do not need to be associated with future gains because market prices can show mean-reverting behavior. Accordingly, buying stocks which had previously been sold for gains—a behavior that reflects reinforcement learning—does not reliably increase financial investor performance (Strahilevitz, Odean, & Barber, 2011). Because financial events such as market crashes are rare we have little experience with them. As a result, learning from past outcomes leads to underweighting of low-probability events until they occur, and overweighting when they occur (Hertwig, Barron, Weber, & Erev, 2004). Compared to primary rewards such as food, money can also be stored for a longer time, demanding a longer time-horizon in decision making. Therefore, human behavior exhibits the tendency to quickly collect sufficient rewards (cf. intertemporal discounting) to prevent strong, potentially life-threatening losses, rather than to maximize long-term reward accumulation.

Taken together, financial decisions are very different from the decisions that drove the evolution of the human brain. This difference is best seen in so-called “cognitive illusions” which occur when our assumptions about the world are violated. As financial markets are very different from nature, our assumptions are violated more frequently, leading to suboptimal decisions. This is akin to visual illusions, where the brain creates false perceptions due to assumptions that are inaccurate in these cases. Examining financial decisions using a neurobiological perspective can reveal such underlying—possibly wrong—assumptions and help explain puzzling financial phenomena as well as inform future financial and economic models. It may also explain individual differences in financial decision making, why some people take risks and others don’t, and why our preferences may change over time.

Developing the Basis for Prediction of Investors’ Behavior

Components of Financial Decision Making

Standard financial theories state that decisions should maximize (expected) utilities that are derived from (expected) value, risk (variance), and (nonlinear) probabilities. As these theories were not driven by biological or psychological considerations, early neurofinance investigated whether the human brain explicitly tracks utilities, expected values, risks and probabilities.

Using fMRI, Preuschoff, Bossaerts, and Quartz (2006) demonstrated that brain regions such as the ventral striatum, midbrain, and bilateral insula respond to probability, risk, and errors in judging risk (Preuschoff, Quartz, & Bossaerts, 2008). This suggests that the human brain values risky gambles by evaluating their expected reward and risk, as suggested by modern portfolio theory (Markowitz, 1952).

Neural correlates have also been reported for other summary statistics frequently used in finance such as the spread of outcomes (variance/risk) and the asymmetry in the distribution of outcomes (skewness). In one study, modeling behavioral choices using the mean-variance-skewness model revealed that variance activated the parietal cortex while individual differences in positive skewness preference correlated with BOLD activation in the ventral striatum, anterior insula and the inferior frontal gyrus. Negative skewness, on the other hand, correlated with activity in the dorsomedial prefrontal cortex (dmPFC) but no brain area correlated with skewness in general (Symmonds, Wright, Bach, & Dolan, 2011). Similarly, Wu, Bossaerts, and Knutson (2011) found that activity in the ventral striatum (nucleus accumbens; NAcc) was correlated with the individual’s tendency to approach (prefer) positively skewed gambles, while anterior insula activity correlated with avoidance of negatively skewed gambles. These findings suggest that individual differences in affective and neural responses may provide predictions on individual choice.

A meta-analysis of financial risk-taking studies performed in 2012 (Wu, Sacchet, & Knutson, 2012) demonstrated that the statistical moments of risky financial options (contrasting high vs. low mean, variance, and skewness) activate loci in the ventral striatum. Mean and variance also activated bilateral anterior insula and anterior cingulate cortex—areas implicated in effort and expected energy expense (Prévost, Pessiglione, Météreau, Cléry-Melin, & Dreher, 2010), and in conflict resolution (Botvinick, Nystrom, Fissell, Carter, & Cohen, 1999; Brown & Braver, 2008), as well as in functions such as proprioception and empathy (Singer, Critchley, & Preuschoff, 2009). The meta-analysis included only 4 studies that specifically compared high to low skewness and found that general skewness activated the ventral striatum (including the NAcc), but common activation of the anterior insula was not in evidence. These studies suggest that while ventral striatal activity is associated with risk-seeking financial choices, anterior insula activity is associated with risk-avoidant choices in investment tasks (Kuhnen & Knutson, 2005), consistent with signaling risk prediction and risk prediction error (Preuschoff et al., 2008).

Together, these findings show that it is the subcortical, phylogenetically older brain substrates together with insular cortex that mediate decision making under risk rather than more recently evolved parts of the neocortex, suggesting a fundamental role of affect in financial decision making.

Risk versus ambiguity in the brain

Understanding how risk and other forms of uncertainty are processed in the brain is of particular interest for financial decision making. In most real-life choices, such as in weather forecasts for distant tourist destinations or betting in games with unknown rules, probabilities are based on meager or conflicting evidence (Schultz et al., 2008). At the other extreme, such as in gambling on a roulette wheel, probability can be confidently judged from relative frequencies, from event histories, or based on an accepted theory (Hsu, 2005). These two forms of uncertain events are called ambiguous and risky, respectively. Ambiguity refers to situations of uncertainty in which the probabilities of outcome are incompletely known, as opposed to risk where probabilities are known (Ellsberg, 1961). In financial decision making in the real world (Glimcher, Camerer, Fehr, & Poldrack, 2009), risk and ambiguity (uncertainty) exist on a continuum, and while some uncertainty can be reduced and estimated, a portion will remain irreducible (Lo & Mueller, 2010).

In economics and finance, risk and ambiguity are generally treated as distinct forms of uncertainty. Behavioral models of choice under risk are relatively well-established, but both for risk and ambiguity individual choice remains difficult to predict. Thus, neurofinance may provide answers to two open questions: (a) Are risk and ambiguity two truly distinct concepts or just two facets of the same? (b) Can we identify other variables (e.g., physiological signals) that are taken into account when individuals evaluate gambles and thus improve prediction of choice? As we will show in the remainder of this section, investigating how risk and ambiguity are processed in the brain paints a picture that is more complex than what traditional economic and financial models have assumed.

Consistent with observations in decision making under risk, some studies reported insular activation in response to ambiguity (Huettel, Stowe, Gordon, Warner, & Platt, 2006) and classification uncertainty (Grinband, Hirsch, & Ferrera, 2006). The results of neuroimaging studies comparing risk and ambiguity, however, do not show a consistent picture. For example, to investigate ambiguity, Hsu, Bhatt, Adolphs, Tranel, Camerer (2005) compared choices between certain and uncertain monetary outcomes involving three experimental treatments in which the uncertain option dissociated between ambiguity and risk based on different amounts of information. The authors observed that lateral orbitofrontal cortex (OFC) and the amygdala showed higher response to ambiguity compared to risk. Conversely, risky gambles elicited stronger BOLD signal in dopaminoceptive areas such as the dorsomedial striatum (caudate nucleus), in the precuneus and the premotor cortex.

Subsequently, Huettel and colleagues (2006) found that risk and ambiguity share many of the same neural substrates overall, including the insula, but that regions of the prefrontal cortex, dorsolateral prefrontal cortex (DLPFC) especially, were highly correlated with individual ambiguity preferences, whereas regions of the posterior parietal cortex and intraparietal sulcus were correlated with individual risk preferences. In support of this finding, TMS of the intraparietal sulcus reduced risk-taking in risky decision trials (Coutlee, Kiyonaga, Korb, Huettel, & Egner, 2016). Although behaviorally choices under risk and under ambiguity were markedly different, with no correlation between levels of risk and ambiguity aversion, subjective value under both risk and ambiguity was correlated with BOLD activity in the medial prefrontal cortex (mPFC), the striatum, the posterior cingulate cortex, and the amygdala. No brain area was uniquely related to either ambiguity or risk parameters, which contrasts with previous findings that suggested a dissociation of the neural circuits (Huettel et al., 2006).

Levy, Snell, Nelson, Rustichini, and Glimcher (2010) conducted an fMRI study using the classic Ellsberg urn experiment (Ellsberg, 1961) in which subjects are asked to place a bet on drawing either a red or a blue marble from an urn in which the color of a portion of marbles is unknown. Ambiguity activated the lateral OFC, replicating the previous results (Hsu et al., 2005; Huettel et al., 2006). In addition, it has also been demonstrated that subjects with orbitofrontal damage are less averse to ambiguity (and to risk) than control subjects with temporal lobe lesions (Hsu et al., 2005). This finding contributed to the characterization of the central OFC’s primary function—computation and comparison of subjective values—that we now know is specific and causally related to economic choice behavior (Padoa-Schioppa & Cai, 2011).

Humans are generally ambiguity averse and the level of sensitivity to ambiguity depends on the level of perceived confidence: Feeling confident about one’s own expertise (Heath & Tversky, 1991) as well as feeling lucky may decrease ambiguity aversion (Pulford & Gill, 2014). Payzan-LeNestour and Bossaerts (2011) confirmed humans’ sensitivity to ambiguity by showing that participants’ tendency to explore in a six-arm restless bandit task decreased with estimation uncertainty (ambiguity) but not with other types of uncertainty such as risk.

In summary, the activation in the insula, striatum, and the parietal cortex is associated with the level of risk, while the cingulate cortex, amygdala, and frontocortical areas (DLPFC, mPFC) have been implicated in the encoding of ambiguity. Yet, only some of the evidence is consistent with the proposal of dual dissociation between risk and ambiguity (Huettel et al., 2006; Payzan-LeNestour, Dunne, Bossaerts, & O’Doherty, 2013). Correctly predicting probability and risk and experiencing errors in judging risk could modulate learning of expected rewards, which is a function ascribed to subcortical dopaminoceptive structures (McClure, Berns, & Montague, 2003). Further investigations in this area of decision making invoke, therefore, the context of learning under ambiguity and await further application in neurofinance (Bach & Dolan, 2012; Payzan-LeNestour et al., 2013).

Models of Financial Decision Making

Another promising avenue within neurofinance is its potential to dissociate between competing theoretical models of financial choice. In a first step, researchers have set out to identify the neural correlates of different behavioral models. For instance, it has been demonstrated using fMRI that the expected utility of an option is represented principally in the mPFC and the NAcc, a result replicated many times since (Knutson, Fong, Bennett, Adams, & Hommer, 2003; Seymour, Daw, Dayan, Singer, & Dolan, 2007; Yacubian et al., 2006; see the reward network in the brain in Figure 1 left). Hsu, Krajbich, Zhao, and Camerer (2009) showed that most subjects exhibit nonlinear probability functions by overweighting low probabilities and underweighting mid to high probabilities, which is consistent with prospect theory and in contrast to expected utility theory. This nonlinear probability function was reflected in the BOLD response in the striatum, the cingulate gyrus (implicated in value encoding; Rushworth, Noonan, Boorman, Walton, & Behrens, 2011), and frontal operculum adjacent to the insula (involved in risk processing; see Figure 1 right). This suggests that probability is encoded nonlinearly in the brain, supporting the central features of prospect theory: concavity reflecting risk aversion in the domain of gains and convexity portraying risk-seeking in the domain of losses, which together illustrate the reflection effect. However, as discussed by Boorman and Sallet (2009), while these results are encouraging, expected utility and prospect theory are not the only models supported by imaging studies.

A competing model of decision making under uncertainty, which involves a mean-variance analysis (Markowitz, 1952), is equally supported (Christopoulos, Tobler, Bossaerts, Dolan, & Schultz, 2009). That is, the processing of value in the brain was found to be dependent, to some extent, on the level of risk (Christopoulos et al., 2009).

Furthermore, neural data have been used to test models of investor behavior, such as the “realization utility” theory of trading (Frydman, Barberis, Camerer, Bossaerts, & Rangel, 2014). Participants traded 3 types of stocks in an experimental market while fMRI data were acquired. Activity in the ventromedial prefrontal cortex (vmPFC) correlated with the capital gain, that is, the decision value under realization utility theory, but not with the net expected value of future returns. Activity in the ventral striatum, an area known to encode information about changes in relative reward value, showed a positive response when subjects sold (realized) these capital gains versus when they were holding them. The neural data thus provided direct evidence of the key mechanism at work in the realization utility model.

Frydman and Camerer (2016) used a fictional stock trading paradigm and fMRI to show that when a stock is not owned, the news from a price increase generates a reward prediction error signal in the ventral striatum reflecting the regret from selling too early. During the presentation of a price update screen, after the subject has already made his or her investment decision, a decrease in the neural signal in the ventral striatum was observed when a subject saw a price increase for a recently sold stock. Specifically, the fMRI signal in the vmPFC when a participant could repurchase a stock was negatively correlated with the foregone capital gain. Together with previous research that demonstrated brain activity related to counterfactual information about unselected reward (Lohrenz, McCabe, Camerer, & Montague, 2007), these findings support the hypothesis that regret also contributes to realization utility.

In addition to evaluating financial models, neurofinance research aims to develop new, biologically motivated models of financial decision making. One of the best supported models today is the anticipatory affect model. This model proposes that anticipation of financial outcomes involving uncertain large gains (positively skewed distribution of outcomes) are likely to elicit positive arousal and activate the NAcc, while anticipation of financial outcomes involving uncertain large losses (negatively skewed distribution of outcomes) are likely to elicit negative arousal and activate the anterior insula (Knutson & Greer, 2008). The relative activation of those neural circuits and emotional states leads to approach and avoidance behaviors, respectively, indicating that emotional arousal in anticipation of outcomes can shape behavior. Thus, compared to traditional financial models, the anticipatory affect model takes into account the numerous experimental findings showing that emotions (Baker & Wurgler, 2007; Habib, Cassotti, Moutier, Houdé, & Borst, 2015; Nguyen & Noussair, 2014; Schwager & Rothermund, 2013; Stancak et al., 2015) as well as anticipation (Kuhnen & Knutson, 2011; Ma, Hu, Pei, & Xiang, 2015) play a crucial role in financial decisions.

Individual Differences in Financial Decision Making

Financial decisions vary greatly across individuals. These individual differences are apparent in people’s willingness to gamble or to take financial risks and in preference for short- versus long-term investments. Consequently, the financial success under similar environmental conditions strongly varies between subjects and only a few investors continuously beat the market. These differences could be partially explained by variations in the biological makeup of the individual, including differences in the genome, in the pharmacological systems, the morphology, as well as the functioning of the brain. An accurate understanding and assessment of those biological differences may help to make better predictions for the behavior and performance of investors, which might be used to select the best candidate for asset management or to train asset managers. In the following section we will review these biological differences.

Genetics

Genetic studies ask whether investors are predisposed to certain behavior or whether investment behavior is significantly shaped by environmental conditions. To do so, researchers use twin studies to compare monozygotic and dizygotic twins in their investment behavior. If monozygotic twins are more identical in their investment decision than dizygotic twins, then one can infer that genetics plays a role. Using laboratory tasks these studies suggest that about 20% of the variance in financial risk-taking can be explained by genetic factors (Cesarini, Johannesson, Lichtenstein, Sandewall, & Wallace, 2010). These findings were later confirmed using real-world portfolio allocation data from a large group of twins (Barnea, Cronqvist, & Siegel, 2010; Cesarini et al., 2010), and extended to other aspects of financial decision making, including the choice to invest in “socially responsible” investment funds (Cesarini et al., 2010) or the individual preferences for value versus growth investment (Cronqvist, Siegel, & Yu, 2015). These findings suggest that individual variation in financial decision making is to some extent heritable.

To elucidate the genetic configurations underlying investment behavior and performance, researchers focused on polymorphisms of genes that modulate the dopaminergic and serotonergic system as those pharmacological systems have been implicated in investment decisions. One such gene is the dopamine receptor D4 (DRD4) gene, which has been linked to pathological gambling (Comings et al., 1999; Perez de Castro, Ibanez, Torres, Saiz-Ruiz, & Fernandez-Piqueras, 1997) and financial risk-taking in healthy humans (Kuhnen & Chiao, 2009). Specifically, carriers of the 7-repeated allele (L-allele) of this gene were found to take more risk than noncarriers (Kuhnen & Chiao, 2009). While Wall Street traders are as likely to carry this allele as nontraders, successful traders were more likely to be homozygous for the L-allele (Sapra, Beavin, & Zak, 2012). Another interesting gene is the DAT1 gene, which regulates the dopamine transporter. It has been associated with individual differences in risk aversion in that 9-repeat allele carriers of the DAT1 gene tend to be more risk-taking (Heitland et al., 2012) when deciding about gains (Zhong et al., 2009) compared to 10-repeat allele carriers.

Beside genes that modulate dopamine, the 5-HTTLPR gene modulating serotonergic activity was also associated with financial risk-taking. Short-allele carriers were shown to take less financial risk in general (Kuhnen & Chiao, 2009; Kuhnen, Samanez-Larkin, & Knutson, 2013) and particularly after receiving gains (Heitland et al., 2012). In addition, short allele carriers have increased loss aversion compared to long-allele carriers (He et al., 2010). Finally, financial risk aversion is influenced by polymorphisms of the genes coding for monoamine oxidase-A (MAOA), which modulates serotonergic, dopaminergic, and noradrenergic activity. Carriers of the MAO-L polymorphism take more financial risks (Frydman, Camerer, Bossaerts, & Rangel, 2011).

These genetic studies emphasize the crucial role of the biological system in financial decision making and show that genes which modulate the dopaminergic and serotonergic system influence financial decision making. Although several first candidate genes have been identified, more large-scale studies are required to understand their influence on different components of financial decision-making.

Anatomy

As neuroscientific studies repeatedly revealed that the specific aspects of financial decision making, such as risk-taking, are shaped by specific brain networks (Components of Financial Decision Making), it is conceivable that structural differences in those brain networks partially underlie individual variations in financial decisions. Structural differences may include the surface area or cortical thickness of brain areas and the extent of gray matter tissue. Those differences can be quantified noninvasively by MRI-based techniques and related to individual differences in financial decisions using statistical analysis.

Using this approach, Nasiriavanaki et al. (2015) found that risk-averse subjects have altered gray matter volume compared to risk-seeking subjects. Subjects who took higher financial risks in the balloon analog risk task had larger gray matter volume in the anterior insula compared to subjects who took fewer risks. In addition, risk-averse subjects have lower gray matter volume in the posterior parietal cortex compared to risk-seeking subjects (Gilaie-Dotan et al., 2014). Finally, subjects with a risk-taking bias as indexed by the Cambridge Gambling Task displayed lower gray matter density in the ventral striatum (Schneider et al., 2012). Together, these findings indicate that individual differences in risk-taking behavior are related to some extent to the gray matter volumes of the brain networks underlying risk-taking, including the anterior insula, ventral striatum, and the posterior parietal cortex. Because gray matter volume does not significantly change within a short time range, those characteristics might serve as relatively stable biological markers for prediction of individual financial behavior.

This principle applies not only to risk-taking, but also to individual differences in loss aversion, where neuromorphometric results dovetail with fMRI studies. Subjects with high loss aversion in financial gambles have higher gray matter volume of the centromedial amygdala nuclei compared to subjects with low loss aversion (Canessa et al., 2013). Subjects with amygdala lesions exhibit a dramatic absence of loss aversion, while other aspects of financial decisions, such as risk and value coding, are unaltered (De Martino et al., 2010). This can be explained by one of the well-studied functions of the amygdala, and specifically its central and basal nuclei that regulate the output of the amygdala, in fear- and anxiety-related avoidance behavior. Furthermore, loss-averse subjects had lower gray matter volume in the bilateral posterior insula as well as in the left medial frontal gyrus (Markett, Heeren, Montag, Weber, & Reuter, 2016).

Brain activity and functional connectivity

Individual brain structure is a strong candidate biological marker for relatively stable individual differences. Functional imaging provides further candidates through the exploration of neuronal processes underlying financial decision making as well as the functional connectivity between brain regions. Risk-averse subjects appear to differ from risk-seeking subjects in their brain activation during all stages of financial decision making, including anticipation of risk/rewards, choosing between risky options and processing the outcome of risky choices. During the anticipation of an outcome of a high-risk gamble, risk-seeking subjects were shown to have lower activation within the ventral striatum and anterior insula compared to risk-averse subjects (Rudorf, Preuschoff, & Weber, 2012). Given that the anterior insula has repeatedly been implicated in the processing of risk (Huettel et al., 2006; Preuschoff et al., 2006; Preuschoff et al., 2008), this increase observed in risk-averse participants might indicate an overestimation of risk. The insula is directly structurally connected with the NAcc (ventral striatum; Leong, Pestilli, Wu, Samanez-Larkin, & Knutson, 2016), and this connection was found to be altered in subjects preferring highly skewed gambles (Leong et al., 2016). Thus, insular-induced overestimation of risk might modulate the NAcc activity and associated functions, such as approach behavior (Kuhnen & Knutson, 2005) and reinforcement learning (Schultz, 2002).

During the processing of outcomes of risky choices, a slightly different network was found to be associated with risk aversion. Specifically, risk-averse subjects showed reduced risk prediction error signals in the anterior insula, the inferior frontal gyrus and the anterior cingulate (Rudorf et al., 2012). The risk prediction error is represented by the insular cortex to adjust the estimated risk based on the outcome of a risky gamble, a process that seems to be disrupted in risk-averse subject. As a consequence, risk-averse subjects might continue to overestimate the risk, because they do not appropriately adjust the expectation of risk, when gambles had been shown to be less risky than expected (Rudorf et al., 2012).

Risk-taking behavior can be predicted to some extent by resting-state data. Specifically, more risk-taking individuals have decreased resting-state activation of the PFC (Gianotti et al., 2009), weaker positive functional connectivity between the right inferior frontal gyrus and the insula, and stronger negative connectivity between NAcc and parieto-occipital cortex (Cox et al., 2010). Furthermore, increased NAcc activity predicted within-subjects’ risky choices during financial investment tasks on a trial-by-trial basis by, whereas insula activity predicted risk-averse behavior (Kuhnen & Knutson, 2005). These findings indicate that functional activation data can provide valuable information for the understanding and prediction of individual financial decisions.

Loss-averse subjects can also be identified by the specific pattern of their neuronal activation. During financial decision making, increased activation of the anterior insula (Paulus et al., 2003) and the NAcc (Matthews, Simmons, Lane, & Paulus, 2004) were associated with increased harm avoidance. In line with this finding, subjects that showed high avoidance for decisions harming others were also found to have increased activation in the anterior insula and anterior cingulate cortex during the decision to financially harm others (Greening et al., 2014). Furthermore, during the anticipation of outcomes, and in particular of losses, increased activation of the insula, the amygdala and the putamen (Canessa et al., 2013) was seen in loss-averse subjects compared to more loss-tolerant subjects.

Hormones

Several studies have investigated the role of testosterone and cortisol in financial decision making. Individual testosterone reactivity has been shown to influence future economic risk-taking in men. Coates and Herbert (2008) tested the “winner effect” in professional traders on a London stock exchange. The effect describes androgenic priming—a positive feedback response of testosterone to competitive situations—wherein the winning male emerges with an increase in testosterone, while the loser experiences a drop. In a small (N = 17) sample of high-frequency traders, testosterone levels were measured in the morning and in the afternoon. On days when morning testosterone was high, the traders returned an afternoon profit significantly higher than on “low-testosterone” days. The “winner effect” could therefore lead to a higher probability of subsequent winning and increased risk-taking on the next round of trading. Interestingly, this relationship was stronger among experienced traders, suggesting that testosterone response may have played a role in optimizing long-term performance in high-frequency trading.

A subsequent laboratory study supplied causal evidence linking testosterone with optimism in future price expectations which, at an aggregate level, led to overpricing and market bubbles. Nadler, Jiao, Johnson, Alexander, and Zak (in press) used an experimental asset market paradigm by Smith, Suchanek, and Williams (1988). Two groups of males participated: one group was administered a testosterone and one a placebo gel. After several periods of the trading game, asset prices were higher in the testosterone-treated group relative to placebo. Specifically, testosterone treatment increased three measures of asset overpricing: amplitude, market value amplitude and duration. Thus, testosterone increased optimism about future prices and led to bidding in excess of fundamental value, which at a market level resulted in overpricing. This trend continued as many traders sold overpriced shares and continued to bid despite obvious upward deviations from asset fundamental value, causing a market bubble. Note that testosterone response to winning in women has not been reported, but studies with testosterone administration found that it has no effect on risk-taking (Apicella, Carré, & Dreber, 2015).

Using a similar experimental asset market design, Cueva and colleagues (2015) found that testosterone induced increased optimism about future price changes, while the stress hormone cortisol affected risk preferences directly. Both effects were associated with increased risk-taking and consequent destabilization of prices (a market bubble followed by a crash). In the experiment, male subjects were administered cortisol and testosterone in a double-blind placebo-controlled crossover design. Subjects were shown plots of the price sequence for two “stocks” and had to decide to invest in a stock with either a high or low variance of returns. Both testosterone and cortisol administration resulted in higher investment in riskier stocks but neither hormone was associated with changes in low-risk stock investment. Testosterone administration also increased subjects’ predictions of future stock price, in line with previous studies. Measuring salivary levels of endogenous cortisol and testosterone before and after each trading session, Cueva et al. found that the association between cortisol and risky trading behavior in the market experiment was not present in women. In male and mixed markets but not in female-only markets, pretrading mean group levels of cortisol predicted one third of variability in a market measure of price volatility.

Special focus: gender differences

Differences in decision making between men and women are particularly prominent in financial decisions involving risk. It is generally accepted that on average, women tend to be more risk-averse and less (over)confident compared to men. Surprisingly, the origin of these differences as well as their potential impact on financial markets has been relatively poorly studied. This is in part due to a relatively low number of women working in trading. However, the differences in overconfidence may be of particular interest due to its role in overtrading associated with higher variance and lower performance (Wargo, Baglini, & Nelson, 2010).

Risk-Taking

Ignoring societal and organizational dynamics, a repeated finding in behavioral finance and economics experiments is that women invest less in risky options (Charness & Gneezy, 2012). As most of the experiments have been performed on young nonexpert subjects, their results may not be generalizable to financial experts. Although men tend to buy riskier stocks than women (Feng & Seasholes, 2008), there appear to be no differences between men and women mutual fund managers regarding risk and fund performance (Aggarwal & Boyson, 2016; Atkinson, Baird, & Frye, 2003). Yet, no other subjective or empirical measures of risk or loss aversion have shown significant gender differences.

Two main explanations have been proposed to account for gender differences in risk tolerance: biological-based and social-based (Felton, Gibson, & Sanbonmatsu, 2003). The biological account states that risk tolerance in general can be attributed to sex and gender differences (male–female) driven by hormones and genes (Kuhnen & Chiao, 2009; Pawlowski, Atwal, & Dunbar, 2008), as well as by evolutionary gender-role specialization (Wilson & Daly, 1985: Low, 2015). The social account argues that both genders learn social expectations through a socialization process and behave in accordance with societal expectations (Wood & Eagly, 2012). An evolutionary model of preference-formation (Dekel & Scotchmer, 1999) suggests that men will evolve to be risk takers, while women are overall more averse to uncertainty in all domains except for, perhaps, social decision making (Weber, Blais, & Betz, 2002). However, it is not completely clear how the hunter-gatherer origins map onto contemporary financial decision making behavior and thus calls for further examination. For instance, high risk aversion (as measured by responses in 15 incentivized gambles; Holt & Laury, 2002) is associated with low in-utero testosterone exposure in women (Sapienza, Zingales, & Maestripieri, 2009). In men, risk-taking for gains (but not for losses) is positively related to basal (salivary) testosterone (Schipper, 2012).

In addition to a general lower risk tolerance, other factors may contribute to the difference in investment decisions between men and women. Montford and Goldsmith (2016) conducted a survey among college students and found that women chose to invest significantly less of an imaginary inheritance into stocks (representing the risky choice) versus bonds (the risk-less option). Their analysis suggested that this risk aversion could be due to subjectively lower financial self-efficacy. It is possible that women with a low level of knowledge and experience in financial matters feel less competent when lotteries are framed as investment decisions and are therefore particularly risk-averse in this setting (Gysler, Kruse, & Schubert, 2002). This is in accord with underconfidence of women found in other domains, such as in academia, where in the past two decades men self-cited 70% more than women (King, Bergstrom, Correll, Jacquet, & West, 2016).

Women’s higher risk aversion is domain-specific and depends on a number of variables, including experimental conditions: For instance, women are as risk-taking as men when it comes to social situations but less willing to engage in potentially life-threatening activities (Weber & Blais, 2006). Adolescent girls were more risk-averse than their male counterparts when given the choice of risky lotteries, but in the ambiguous lottery trials, both sexes showed similar marginal valuations of ambiguity (Borghans, Golsteyn, Heckman, & Meijers, 2009). In adults, this is the case for losses but not for gains (Schipper, 2012), and not for investment or insurance contexts (Schubert, Gysler, Brown, & Brachinger, 2000). A recent meta-analysis of behavioral economic experiments involving risky investment choices shows that women’s higher risk aversion is an exception rather than a rule (Filippin & Crosetto, 2014) and that the difference between the sexes, although consistent, is negligible.

Fehr-Duda, De Gennaro, and Schubert (2006) showed that when gambles presented a potential for financial gain (especially when framed as an investment decision), women tended to be more pessimistic, underweighting large probabilities of gain much more than men. However, there were no gender differences in estimating probabilities in the loss domain.

Overconfidence

Women are less overconfident in their assessment of potential future gains than men (Fehr-Duda et al., 2006; Hügelschäfer & Achtziger, 2014). Overconfidence has been linked with higher volatility and lower performance (Biais, Hilton, Mazurier, & Pouget, 2005; Eisenbach & Schmalz, 2015), though the opposite is not necessarily true.

A survey by Beckmann and Menkhoff (2008) found that women finance professionals are as overconfident as men although women were more likely to shy away from competition in hypothetical tournament situations. While women also adjusted their risk exposure more often if their portfolio performed above/below the benchmark, neither of these behaviors implied lower returns. Feng and Seasholes (2008) examined trading activity in China and showed that the gender difference is objectively confirmed only in the size of the portfolio and the size of the trades placed. Men and women’s trading behavior was otherwise quite similar: although men appeared to trade more intensively than women, this difference was not significant after controlling for factors such as number of stocks held and number of trading rights.

A recent survey of over 11,000 nonadvised individual investors in South Africa demonstrated that men traded significantly more than women but did not earn lower returns despite a negative correlation between trading volume (i.e., the number of switches) and total return (Willows & West, 2015). Men were more overconfident, displayed higher risk tolerance and stronger self-efficacy and self-attribution biases compared to women (Willows & West, 2015) resulting in a higher variability of men’s returns over the period of 5 years. The authors suggested that men could perform better in bull markets while women might perform better in bear markets that require diverse risk propensities and behaviors. This potential gender-market or gender-portfolio risk profile match thus merits further investigations.

In an aggregate, this difference in risk-taking behavior may translate into opposite effects on market behavior. For example, in an artificial market experiment, Eckel and Fullbrunn (2015) demonstrated that all-female markets created smaller “bubbles” in asset prices than all-male markets, while “mixed” male/female markets produced midsized bubbles. All-female markets showed much lower positive deviation from fundamental value compared to all-male markets, demonstrating that women are much less likely to generate overpricing in stock exchange transactions. This was in part due to the fact that men tended to forecast significantly higher prices than women, consistent with overestimation of the probability of large gains demonstrated by Fehr-Duda and colleagues (2006). Thus, in financial decision making, women tend to be less optimistic about probabilities of large gains and less risk-tolerant to losses than men, but this behavior is not equivalent to overall higher risk aversion.

Taken together, examinations of historical trading data seem to show that while there is no statistically significant difference in the returns earned by men and women, men trade more and their returns show higher variance, which suggests that women may be better predisposed for certain types of fund management that shields it from excessive long-term volatility.

Other factors

The financial trading profession is heavily male-dominated (globally, only 7% of fund managers were women in 2016; Citywire Smart Alpha, 2016; Coates, 2012; Eckel & Fullbrunn, 2015). One of the reasons might be that the time allowed for decision making in trading is very short (Coates, 2012). Men seem to perform better under time pressure than women (Shurchkov, 2012), and their simple reaction time is also faster than in women across life span (Dykiert, Der, Starr, & Deary, 2012). Another often-invoked evolutionary reason is the hypercompetitiveness of the environment, which favors men. An anthropological study on the willingness to compete among males and females in a hunter-gatherer society found that while both genders were equally willing to compete, males were more competitive in a male-centric task (testing handgrip strength; Apicella & Dreber, 2015). A third reason might be the hypothalamic–pituitary–adrenal (HPA) axis stress response (Kajantie & Phillips, 2006) under time pressure, which differs between the sexes, with premenopausal women showing smaller responses than men. Stress amplifies gender differences in behavior during risky decisions, such that males take more risk and females less risk under stress (Lighthall et al., 2012). Furthermore, under conditions of chronically elevated cortisol the weighting of probabilities of gain/loss changes significantly in men, but not in women. Relative to women, male subjects exhibited greater sensitivity to small probabilities (overweighting) and lesser to large ones after chronic elevation in cortisol levels (Kandasamy et al., 2014).

Ambiguity tolerance

In the real world, female investors weigh risk attributes, such as probability of loss and ambiguity, more heavily than their male colleagues and tend to emphasize risk reduction more than men in portfolio construction (Olsen & Cox, 2001). Experimental evidence shows that women show stronger aversion toward lack of information (i.e., uncertainty) than men, irrespective of familiarity, framing or costs (Powell & Ansic, 1999), which increases with uncertainty (Schubert et al., 2000). Borghans et al. (2009) demonstrated that for low-cost ambiguous gambles adolescent girls showed less ambiguity aversion than boys but the gender difference disappeared as ambiguity increased.

Gysler et al. (2002) studied choices between risky and ambiguous lotteries in a simulated market experiment and found significant gender differences that depended on interactions with two variables: overconfidence and self-assessed market knowledge (competence). Low-knowledge men tended to be more overconfident while high-knowledge women tended to be underconfident, that is, they stated subjective probabilities that were below their knowledge-based accuracy (Gysler et al., 2002). Surprisingly, overconfidence tended to increase ambiguity-seeking behavior only in females, whereas competence tended to dampen the overconfidence effect for men in ambiguous lottery choices, effectively minimizing risk/ambiguity-seeking in financial decisions. This is intriguing as it points toward possible differences in the affective mechanism guiding the decision making process: Women could find the resolution of uncertainty more rewarding or experience higher negative anticipatory affect when faced with ambiguity. Neurofinance provides the tools to further investigate this hypothesis and to unravel the biological basis of the gender differences in financial decision making, which still await investigation.

Discussion

Open Questions

Neurofinance is still in its infancy. So far, it has provided valuable insights into how humans process financial information and how we use this information to make financial decisions. Yet, the most important and arguably most exciting steps are still to come.

First, many of the above results were obtained in the laboratory in isolated and often static environments. But real-life financial decisions take place within a dynamic economic and social context that influences the financial decisions of individuals and might lead to phenomena such as conformism and herding behavior. For instance, investors become more risk-averse immediately following a stock market crash (Cohn, Engelmann, Fehr, & Maréchal, 2015). Obtaining real-life data is particularly difficult for any study involving physiological measures as those are not easy to collect while we go about our daily business. Lo and Repin (2002) were among the first to try this when they equipped professional securities traders with a biofeedback unit to assess how their heart rate, skin conductance, blood volume pulse, electromyographical signals, respiration, and body temperature change with transient market events. More recently, Coates and Herbert (2008) showed that cortisol levels increase across market participants during periods of heightened market volatility possibly leading to collective alterations of financial decision making that amplify the market trends. However, when it comes to obtaining fMRI data we are still confined to the lab where participants nonetheless can be exposed to more realistic scenarios such as experimental market bubbles. Smith, Lohrenz, King, Montague, and Camerer (2014) did just that and found that the price changes during the bubble were positively associated with the aggregated neuronal activity in the NAcc. Subjects that tended to buy as a function of NAcc activity earned lower returns, while subjects with high returns purchased stock less frequently as a function of NAcc activity but also displayed increased insular activity preceding the burst of the bubble (Smith et al., 2014). In addition, another study found that increases in vmPFC activity were associated with the willingness to buy at prices above the fundamental values (De Martino, Fleming, Garrett, & Dolan, 2013).

Second, market behavior is the result of the social and economic interaction of many agents. The original assumption that agents are rational and deviations from rationality are normally distributed has been sufficiently challenged to rethink existing models of price formation in aggregate markets. To accurately model and predict financial markets, new models should also incorporate context-dependent behavioral biases and could even exploit the predictive power of physiological signals (e.g., Kuhnen & Knutson, 2011).

Third, most of the current research is limited to Western industrialized nations. We know that different cultures perceive and process information differently (Hedden, Ketay, Aron, Markus, & Gabrieli, 2008; Weber & Hsee, 1999). This may likely result in different behavioral preferences leading to different aggregate behavior.

Fourth, research is very scant in the domain of financial education, which neurofinance could address by investigating, for example, how we learn from financial information, knowing that there are intuitive biases in how the brain processes quantities and symbolic numbers (Schiebener & Brand, 2015; Thoma, White, Panigrahi, Strowger, & Anderson, 2015). This could provide a basis for designing better training interventions for various populations.

Finally, there are plenty of other areas in finance that should be revisited in light of the above results, from behavioral interventions for individual investors to regulatory policies. The latter currently underestimate or outright ignore the impact of human biases and emotions on investment behavior and overall wealth distribution.

Applications in Finance, Organization and Management

Many researchers, individual investors and financial institutions have long acknowledged that humans are not rational in the traditional economic sense. Neurofinance and its findings as reviewed above present a unique opportunity for investors and institutions to not only redefine rationality but to rethink its impact on financial decisions and investment behaviour. For instance, understanding one’s own biases in reading and comprehending financial information and context-dependent variability in risk-taking preferences could help individuals make more informed investment decisions for their future (such as retirement planning), without overreliance on potentially partial financial advisors. For banks and financial institutions, knowing how different types of clients proceed in their decisions could help shape their offer as well as the presentation of the features of a financial product. Another potential application is to provide real-time monitoring of the physiological system during financial decision making. Traders that are aware of the physiological changes were found to achieve higher performance in trading (Kandasamy et al., 2016). Understanding which computational models of decision making map best onto underlying neural activity could be used to facilitate consumer choice and could find an application in, for example, user interfaces in complex and large purchases, such as choosing a desired car configuration. Such models could take as input choice confidence levels in preselected decision criteria to build more relevant and selective decision trees to facilitate the choice, preventing cognitive overload and decision fatigue.

Organizational scholars will easily find many parallels to neurofinance as they, too, are concerned with decision making in complex, dynamic social and economic environments. Organizational decision making involves anything from the source and impact of extrinsic and intrinsic motivation to social cognition and leadership, which are also key topics in neurofinance and, more generally, neuroeconomics. Understanding how and why biases arise and how they affect social dynamics is key to developing efficient organizational structures.

Footnotes

Authors’ Note

Ewa A. Miendlarzewska and Michael Kometer contributed equally to this work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research of Michael Kometer was supported by the 1st Interdisciplinary Financial Management (IFM) Research Prize (P&K Pühringer Gemeinnützige Stiftung) and the ZZ Vermögensberatung (Schweiz) AG.