Abstract

Chinese tourism demands in Australia have increased exponentially in recent time, driven largely by increases in the number of visitors. The hidden important fact of this market is its high price sensitivity, which is vital to the growth of the dominant Chinese tourism segment in the total inbound sector of the country. This article addresses a concern of the tourism industry regarding a possible policy change on a tourist visa fee for Chinese nationals that potentially has adverse impacts on the economy. The article demonstrates that the revenue objective of an increase in the visa fee for Chinese visitors is unlikely to be a successful policy, as it will take a long time for the visa revenue to compensate for the losses of gross domestic product. In the extreme, the GDP losses may never be compensated adequately by the increased visa revenue.

Introduction

The Australian government has a history of ratcheting up the fees and charges on the tourism industry (Forsyth et al., 2014). This time, visa fees for Chinese visitors are continuously under review. Admittedly, visas are an important instrument that governments use to control who can enter their countries for specific purposes (Artal-Tur et al., 2016). The immediate effect of such an instrument is to ensure security for a country where undesirable foreign nationals are screened and prevented from entering. However, visa fees are also treated as a revenue raising device in many destinations where the politically safer option of ‘tax exporting’ is preferred (Forsyth and Dwyer, 2002).

Chinese tourism demands in Australia have been exponentially increasing in recent years, driven largely by increased economic growth in China, to the extent that the strong growth of this market could be misinterpreted in a way that Chinese visitors are not price-conscious. Thus, government and businesses could fall into a trap of making decisions without consideration of price implications when Chinese visitors, in contrast, are indeed very price sensitive (Pham et al., 2017).

Until recently, each visitor from China was charged $135 by the Australian Government for a multiple entry 3-year visas to Australia, an amount that from 1 July 2017 has been raised to $140 (Australian Government, 2017b). The Australian government has also announced that it will now offer multiple entry 10-year visas for the Chinese nationals. While the extended period of the visas is certainly welcomed by the industry as this is deemed very likely to stimulate more Chinese visitors to the country, the 10-year visas will incur a higher fee of $1000 (Australian Government, 2015). This new 10-year entry visas will co-exist with the current 3-year visas, but it is not clear for how long.

The tourism industry in Australia has had good reasons to be concerned that the Federal government would continue to pursue revenue raising policies affecting the demand for inbound tourism, particularly as regards an expanding market such as China. For some time, having flagged the possibility of a tax on foreign backpackers working in Australia, parliament subsequently enacted legislation requiring the lodgement of tax returns from foreign backpackers (Australian Government, 2017a). This policy has caused considerable concern to the tourism industry which lobbied strongly but unsuccessfully against the tax. Unfortunately, government focus seems to be on revenue raising, regardless of the potential effect on the tourism sector and the economy. The government estimated in the 2015 budget that this measure would bring $540 million into the government coffers over the forward estimates (Australian Government, 2015) and this appears to be regarded as sufficient justification for the tax.

Concern over the increased visa fee for Chinese visitors to Australia comes at a time when other countries are reducing such fees in their attempt to gain tourist numbers and expenditure. The significance of visa effects is well recognized, and visa fee reductions have been used to attract more tourists across many countries. For example, in 2014, the Canadian government granted a 10-year period for all visa applications, with the fee reduced from CAN$150 to CAN$100 (Canadian High Commission, 2014). The United States introduced 10-year multiple entry visas for Chinese visitors in 2014 at no additional cost to the basic visa processing fee of US$160 (US Department of State, 2017). In 2015, the Singapore government extended the Multi Journey Visas for Chinese nationals from 2 years to 10 years (Singapore Government, 2015).

The government’s budget-driven focus is further evidenced by its reluctance to undertake any modelling of the potential impacts of a visa fee change. Given government treatment of tourism as a ‘taxation cash cow’, the peak industry body (private sector) of the Australian tourism industry expressed its great concern at the very early stage of this policy development that the $1000 10-year visa fee for visitors from China might eventually replace the (then) $135 three-year fee for a revenue purpose with an adverse effect on the nation’s largest inbound tourism market. Moreover, as emphasized by the industry, if the replacement eventuates, affecting only against Chinese visitors, this could easily be seen as a form of market discrimination, perhaps with political implications. In this context, the present study was initiated by industry to inform the government of the potential economic impacts of the possible policy change on Australia’s fastest growing inbound tourism market, as well as on the national economy.

This article examines the adverse impacts of the replacement scenario on the Australian economy for two purposes. On the one hand, it pre-empts such a move by pointing out explicitly the likely severe adverse impacts that the industry is concerned about. On the other hand, the present study will provide a general framework to assess the impacts on the economy not only of the increased visa fee, but also other general cases, for example, a passenger movement charge or new taxes, which could eventually raise the cost of travelling for tourists. While focussed on the Australian context, the issues discussed are relevant to all countries that attempt to manipulate visa fees or other charges as part of a general border security or tourism revenue earning strategy, with regard to the Chinese market.

The overall impact of an increase in a visa fee is determined in a multi-stage process. In the first instance, the price elasticity of demand for the tourist markets (China in this case) is obtained so that the loss of visitors can be subsequently derived. The revenue from the increased visa fee is calculated only on the basis of the visitors who are not deterred by the policy change. In the second stage, the economy-wide impacts (or the cost of the policy) are estimated through an appropriately constructed economic model.

Using a dynamic computable general equilibrium (CGE) model for tourism, this article explains, not only how a loss of inbound tourism demand would affect the destination (Australian) economy over time, but also why the particular policy option contemplated would bring about a structural change among the industries in the economy. This article provides an up-to-date contribution to the empirical literature of visa fee policy, through the context of Chinese visitors to Australia.

Finally, the stream of future visa revenue is discounted to the base year so that it can be compared directly with the economy-wide impacts of the policy. Essentially, both CGE modelling technique and the cost benefit analysis are used to assess the final outcome of the policy. This way, the feedback of visa fee revenue is isolated so that impacts on the economy are purely due to the policy option.

Modelling approach

The CGE modelling technique began more than 50 years ago (Johansen, 1960). The technique has gained its popularity ever since in economic impact analysis, not only in academic works but also in the policymaking of governments across many countries. In Australia, CGE modelling took root in the 1970s with the ORANI model in which Dixon et al. (1977) and Dixon et al. (1982) brought the Armington and Leontief techniques together to overcome the flip-flop problem of trade flows in Johansen’s prototype CGE model (Dixon and Rimmer, 2010). Subsequently, this has led to voluminous ORANI-style models for many countries around the world, including the well-known global GTAP model (Hertel, 1997).

The advantage of the CGE modelling technique is due to its incorporation of the micro-economic theory with the input–output (I-O) foundation. The I-O foundation alone could not capture the effects of relative price movements on resource reallocation among industries when resources in an economy are limited (Dixon and Parmenter, 1996; Dwyer et al., 2004; Dwyer, 2015; Zhou et al., 1997).

CGE modelling is very versatile in its applications. Tourism economic impact analysis has increasingly adopted the modelling technique over the past two decades. Among the early empirical tourism analyses, Adams and Parmenter (1995) validated Copeland’s (1991) theoretical observation of tourism contribution to a quite small, quite open economy. Since then, tourism CGE models have sprung increasingly throughout many countries. Examples of the early development are Madden’s model that featured international tourism, interstate tourism and Olympic operations for the Australian regional model (Madden, 1997, 2002), Blake’s tourism model for Spain with explicit domestic and inbound tourism sectors (2000) and Sugiyarto et al. (2003) with explicit inbound tourism sector.

Common CGE applications in tourism include assessments of taxation tourism policies on the host economy (Forsyth et al., 2014; Gooroochurn and Milner, 2005; Gooroochurn and Sinclair, 2005; Gago et al., 2009; Meng et al., 2013; Ponjan and Thirawat, 2016), evaluations of tourism events such as Olympic games on the host economy (Giessecke and Madden, 2007; Li et al., 2011; Madden, 2002, 2006), the Dutch Disease and tourism sectors (Dwyer et al., 2016; Inchausti-Sintes, 2015; Pham et al., 2015); and assessments of climate change mitigation on tourism (Dwyer et al., 2012; Meng and Pham, 2015; Pham et al., 2010). The above list is not exhaustive but at least it provides a brief account on the development of tourism CGE modelling from the mainstream CGE modelling.

The tourism CGE model used in this article is similar to the approach in Madden (1997, 2002) in that the dynamic Monash Multi-Regional Forecasting model (Adams, 2008) was augmented to explicitly account for tourism. CGE models that use the conventional I-O tables do not have tourism sectors explicitly in the model, as tourism is not identified in the system of national accounts. If a meal is paid to a local restaurant by a household for a usual dining out, it is not classified as tourism consumption. However, if it is paid for by the same household to a restaurant during a holiday trip, it is defined as tourism consumption. More meals required by tourists will increase the cost for local residents to dine out – a crowding out effect. This condition applies to all goods and services that tourists consume. The need to separate tourism consumption from other final demands is important in tourism economic modelling as it allows for a more accurate impact analysis.

The model used in this article explicitly incorporates tourism in the Australian state I-O database with three broad sectors: domestic, inbound and outbound tourism. A tourism sector is modelled as a broker who gathers all goods and services in a bundle and sells this bundle as a combined (tourism) output to an associate tourism market – a specific user. The domestic and outbound tourism sectors are associated with the household sector, while inbound tourism is attributed to the export demand by foreign nationals. For outbound tourism, only the expenditure before and after the trip that is spent within the domestic economy is included in the domestic tourism sector. Within the domestic component, only the non-business tourism sector is modelled explicitly. Domestic business tourism is included in the industries’ production cost in the I-O database and could not be extracted out due to data unavailability. However, as the visa fee increase is strictly related to the Chinese segment of the inbound market, the impact analysis here is not compromised when the domestic business sector is not explicitly modelled.

A typical CGE model comprises an I-O database with producing industries (supply) and final users (demand). The industries employ workers and acquire capital and intermediate inputs to produce goods and services, which are then purchased by final users such as household consumption, investment, government consumption and exports. Both supply and demand are governed by the optimization theory. The producers will particularly choose their input mix to minimize their production cost for a given market price of their output; and the household sector will select a consumption bundle to maximize their ‘satisfaction 1 ’ at a given level of income.

An algebraic representation of a CGE model can be specified as

where X 1 is a vector of variables endogenously determined by a set of differentiable equations F(.) and X 2 is another vector of variables that are exogenous to the equation system.

Typically, the F(.) equation system describes Demands for goods and services by industries, investment, household, government and exports; Demands for labour and capital by industries; Total production costs of industries; Market prices that users pay with explicit components of industry production costs, government net taxes, import costs and add-on costs such as transportation and retail margins; and Market clearing conditions for supply and demand.

Often, CGE models are used either in a short-run or a long-run time frame in comparative static simulations. A short-run scenario would assume rigid real wages and flexible employment adjustment; and fixed capital stocks with flexible rates of return. Alternatively, a long-run scenario would allow the real wages to be flexible, and employment is not affected by any shocks as the labour market is adjusted by changes in the real wages. At the same time, capital stocks now can be built while the rates of return are adjusted towards a pre-determined level. Simulation results are estimated on an average basis for a typical year in a chosen time frame.

In this article, the model was run in a dynamic setting (Dixon and Rimmer, 1998, 2002), in which both employment and the real wages can change immediately when a shock occurs. However, employment will gradually move back to the base level with the real wages deviating from the base level to reflect the nature of a comparative long-run closure. In the dynamic setting, capital stocks are linked over time. The quantities of capital stocks at the end of a year are a net sum of capital stock values at the beginning of the year, plus additional investment minus the amount of capital usage (depreciation) through the year. For every additional percentage point of capital growth, the model assumes a requirement of an increase in the marginal rate of return (Dixon and Rimmer, 1998, 2002).

When values of some exogenous variables move or deviate from their initial values in the base case, a simulation will compute results of the endogenous variables through the system of the model equations. The model is run using the GEMPACK software (Harrison et al., 2014).

Shock calculation and the baseline

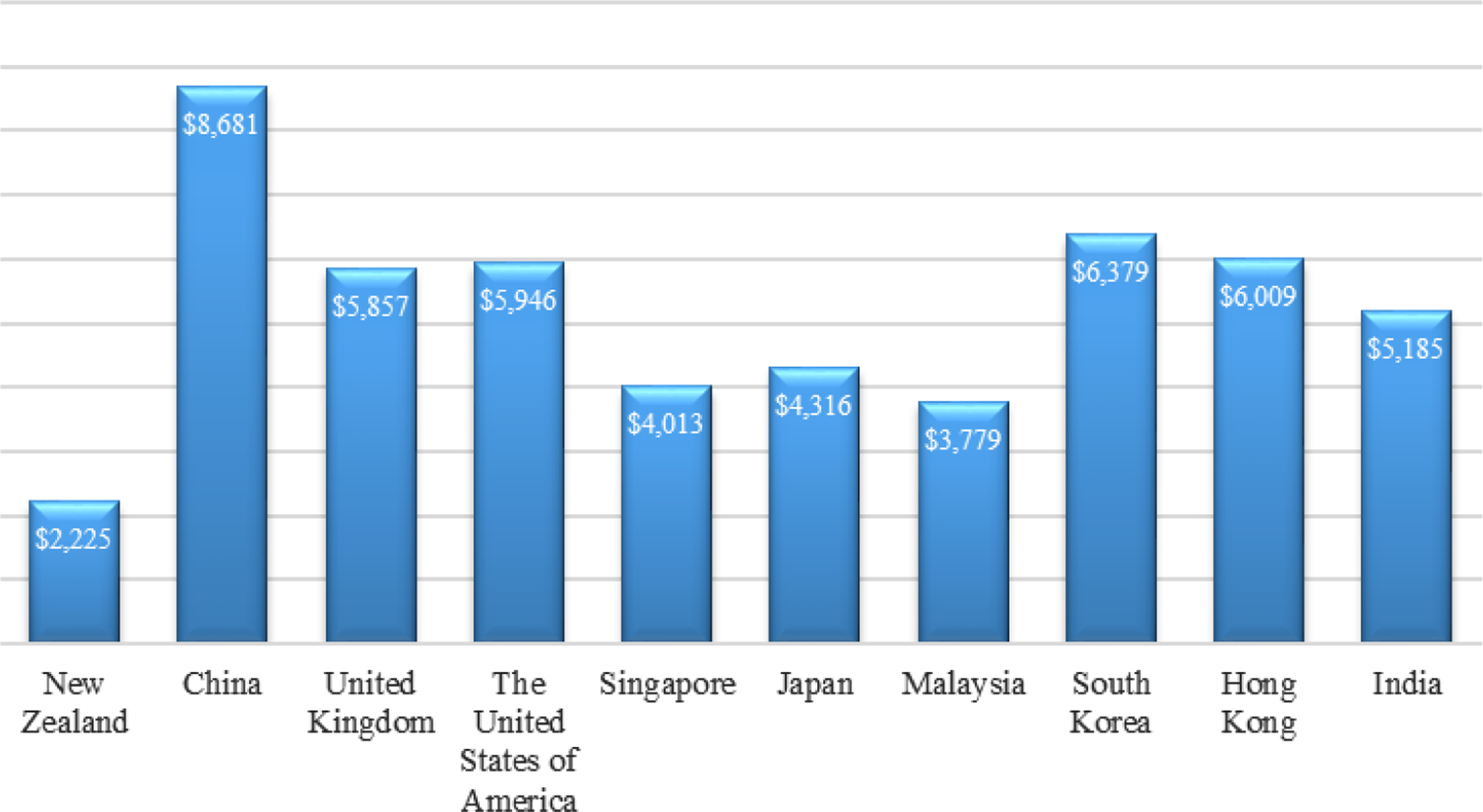

The most recent International Visitor Survey data from Tourism Research Australia, TRA hereafter, (2016a) indicates that on average of each trip, Chinese visitors spend the most ($8681) compared to visitors from all other countries on each trip (Figure 1). Modelling was undertaken using the former $135 visa fee. If the 3-year tourist visa ($135) for Chinese is replaced by the 10-year visas ($1000), the visa will cost $865 extra for each applicant. To meet this increase in the extra cost, for those tourists not deterred by the increased fee, there is a range of possible options to budget their travel expenses:

Cut down expenditure on other items to absorb the additional visa fee while maintaining the total spend unchanged.

Increase travel budget to accommodate for a proportion of the $865 and at the same time cut spending on other expenditure items.

Maintain the current expenditure volume and pattern (existing demand for travel, including average nights per trip as indicated by TRA’s latest forecasts in 2016) and increase the total budget by $865 to pay for the visa fee.

Average total trip spend in 2015, selected inbound tourism markets, Australia.

Regardless which option a tourist might adopt, all options have the same effect that Chinese visitors are now worse off due to an increase of the average trip cost. They either have to cut their spending while in Australia or cut spending from other demands to pay for the trip. On the basis of an average spend of $8681, the additional cost of a tourist visa ($865) will imply approximately a 10% increase on average for all Chinese visitors for all purposes as indicated in Figure 1. The increase is far more significant than the historical annual changes in any series of consumer price indexes in Australia, including the two specific domestic and international holiday travel and accommodation price indexes (Australian Bureau of Statistics, ABS hereafter, 2017).

This increase will, no doubt, lead to an adverse impact on arrivals. The extent of the reduction in arrivals depends upon the sensitivity of Chinese demand to changes in the price of a visit to Australia. The sensitivity is obtained from Pham et al. (2017) who examined the main economic drivers of Chinese visitors to Australia using an econometric model to estimate the effects of income, prices and transport costs on arrival numbers. The tourism price index for Chinese visitors uses the two tourism price indexes published by the Australian Bureau of Statistics, one for domestic and one for international travellers, including both ground and travel costs. Of interest here is that this study found that Chinese visitation to Australia is associated with relatively high short- and long-run total trip price elasticities. The short-term own-price elasticity of Chinese visitors with respect to Australia as a destination was estimated to be −4.2. Applying this elasticity value to the effect of the potential visa fee increase on total trip cost, the adverse impact could potentially involve a 42% reduction in tourist arrivals from China.

Extremely few studies have investigated outbound tourism demand from China. The specific price elasticity for Chinese visitors here is greater than the aggregate price elasticity of −2.5 for inbound visitors to Australia that was estimated in Seetaram (2010), using panel data across 10 countries, 2 including China. While the 4.2 price elasticity is the only estimate currently for Chinese visitors for Australia, it is consistent with other studies, though not many, assessing explicitly price responsiveness of Chinese visitors, given the large proportion of first-time travellers. A recent study of tourists to Malaysia (Habibi and Rahim, 2009) estimated a price elasticity of demand for visitors from China of −8.09, the highest price sensitivity of the 10 inbound markets studied. The value of 4.2 is measured using a price series combining both travel cost and cost of living in the destination of Chinese visitor (Pham et al., 2017). Divisekera (1995) estimated individual long-run elasticities for travel cost (–3.6) and cost of living (–3.5) for Japanese visitors to Australia. Thus the sum of these individual elasticities will be much higher than that of Chinese visitors. Another recent study of visitors to New Zealand found that Chinese FIT 3 segment alongside Koreans are the most price sensitive market segments with respects to demand for tourism products within New Zealand (Schiff and Becken, 2011). Schiff and Becken take their findings to confirm anecdotal evidence that the Chinese tour group market is a discount market where low prices are essential to remain competitive as a destination. They also claim that the sensitivity of Chinese arrivals towards destination prices is an important piece of information for inbound tour operators who deal with Chinese wholesalers (Schiff and Becken, 2011).

TRA data over the period 2010–2011 to 2014–2015 indicate that first-time visitors to Australia account for nearly 50% of the total visitors from China. The rest are return visitors, who would be very likely to have travelled on their multi-entry visas (TRA, personal communication). In this scenario, only the first-time visitors are effectively affected by the increase in the visa fee. Thus, it is more likely the impact would be just half of the full extent, that is, 21% reduction in arrivals from China if the replacement of tourist visa fee of $1000 goes ahead.

The impact of a 21% reduction in arrivals from China is measured against a baseline scenario, in which the Australia economy is projected to grow under two main assumptions over the next 10 years. These include annual GDP growth for the Australian economy and growth in inbound tourism demand across the top 10 inbound markets. The baseline for tourism demands of the top 10 markets is taken from TRA’s forecasts (TRA, 2016b).

For GDP growth, the latest International Monetary Fund’s Global Outlook report (IMF, 2016) indicates that ‘in Australia, growth is expected to remain below potential at 2.5 percent in 2016, but to rise above potential to 3 percent over the next two years, supported in part by a more competitive currency’ (IMF, 2016: 19). We adopt IMF’s assumption and extend the Australian GDP growth smoothing down to 2.7% over the period to 2024–2025. Online Appendix 1 presents forecast assumptions of the Australian GDP and tourism demands by inbound markets in more detail.

Simulation results

Figure 2 presents the source of the stimulus in our scenario – the introduction of the visa fee that causes a 21% reduction in Chinese visitor nights (or arrivals) over the projection period. The baseline reflects the visitor nights of Chinese visitors in the index form 4 (2015–2016 = 1). The continuous line shows the effect of the increased visa fee over the whole projection period. The ‘visa cost effect’ line remains below the baseline throughout the whole forecast period to reflect the one-off shock of the visa policy change. Unless stated otherwise, results herein are presented in percentage cumulative deviation form.

Chinese visitor nights – cumulative growth index.

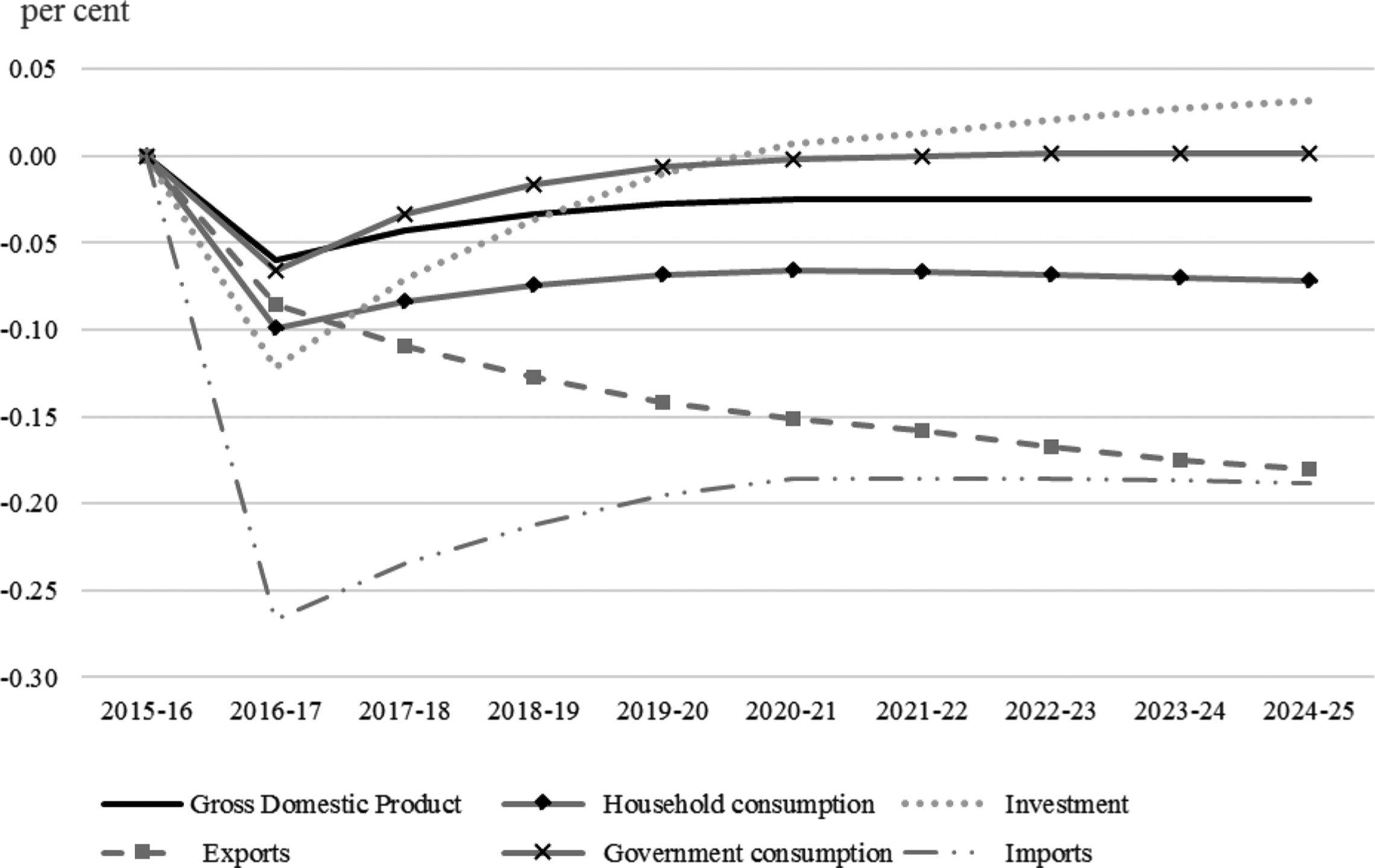

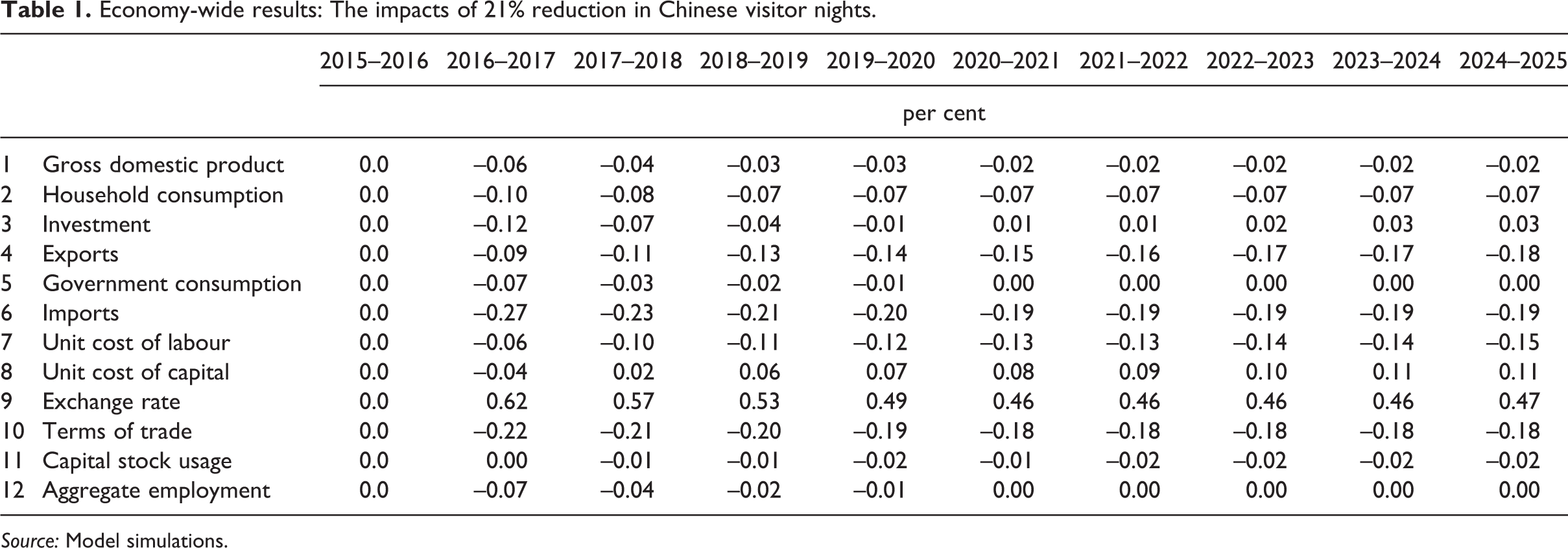

Figure 3 and Table 1 report the impacts at the macro level over the next 9 years due to a 21% reduction in Chinese visitor nights as a result of the increase in visa fee in 2016–2017. Our analysis will start from 2016 to 2017 and then move to subsequent years for the long-run adjustment effects.

Economy-wide results.

Economy-wide results: The impacts of 21% reduction in Chinese visitor nights.

Source: Model simulations.

The reduction of 21% in Chinese inbound tourism demand is equivalent to a reduction of 0.4% in total exports in the first instance. A drop in export demand makes the Australian dollar depreciate. In Table 1, row 9 represents the value of the Australian dollar per unit of the foreign currency after inflation has been removed. An increase in this ratio (0.62%) means that more Australian dollars are required to exchange for the same unit of foreign currency, reflecting a depreciation in the values of the Australian dollar that makes goods and services from Australia relatively cheaper for exports while imported goods and services are more expensive for Australian residents. Indeed, except for the Chinese inbound sector, all exporting sectors expand their exports, which limits the reduction in total export to only 0.09% compared to the baseline (row 4, Table 1), much less than the initial 0.4%.

Typically, a depreciation of the exchange rate is associated with a decline in the terms of trade (TOT), which is measured as the ratio of the Australian export and import prices, denominated in the foreign currency. The decline in the TOT (row 10, Table 1) affects the Australian household sector’s consumption level, as the household now can buy less imported goods from the same volume of exports.

The net loss of exports (reduced inbound tourism from China) directly lowers employment demand (row 12, Table 1) by 0.07% below the baseline level. As a result, the real wage is reduced by 0.06% (row 7, Table 1). The combined effect will lower household income and household consumption subsequently by 0.1% (row 2, Table 1). The overall weaker total demand – across household consumption, investment and so on over the whole economy – leads to a lower requirement of investment by 0.12% (row 3, Table 1).

Of all the economic variables, import volume is reduced the most (0.27%) due to two reasons. The first reason relates to the lower total demand in the economy. The second reason is due to the depreciation of the exchange rate that makes imported goods and services relatively more expensive. Thus, domestic consumers switch towards domestic sources instead – a substitution effect.

In the long run, we assume that all workers who would like to get a job will find a job on the basis that they are willing to accept the wage rate that the industries can afford to offer. In this case, the unit cost of labour (row 7) will continue to decline to absorb the redundant employment and help restore the same employment level as in the baseline scenario (row 12). Ultimately, the increase in the visa fee will lower the wage rate by 0.15% below the wage rate in the business-as-usual scenario.

The lower wage rate and the depreciation of the exchange rate could stimulate export growth in some industries, not all, above their baseline level in the long run. Among the expanding export sectors are the mining industries, namely black coal, iron ore, gas and metal products. These are very capital intensive industries. As usual for mining industries, increases in their exports require associated investment. This explains a ‘bounce back’ in investment from 2017 to 2018 onward. It is the increased mining investment that make the exchange rate appreciate gradually from 2017–2018 to 2020–2021, as portrayed by a declining part of the real devaluation variable in Figure 4 over the period. As the exchange rate gradually appreciates from 2017–2018 to 2020–2021, this continuously erodes growth in all other non-mining exports (Online Appendix 3), before employment could reach the baseline level again (Table 1). The analysis here portrays a structural change, in which mining exports gradually compensate for the loss of tourism export at the expense of the non-mining exports. While the Chinese inbound tourism sector reduced constantly at 21% below the baseline, the effect of the additional investment in the mining sectors worsens the adverse impacts on total exports by further declines as seen in Figure 3. In the long term, total exports decline by 0.18% below the baseline. This loss is made up of a 0.09% reduction in the year when the increased visa fee is introduced and subsequently induced further by another 0.09% due to crowding out effect of the mining sector to create a total loss of 0.18% in the long run (Table 1).

Impacts on real devaluation and the TOT. TOT: terms of trade.

In a comparative static simulation, this long-run loss will not be able to be identified, as a single typical year in the comparative static mode will mask the sequential changes of the exchange rates over time. The pattern of the long-run loss in the post shock period is consistent with the findings in Pham et al. (2015), in which an increase in exports of black coal and iron ore resulted in a net reduction in total exports for Australia. The dynamic tourism CGE model used in this study certainly adds a novelty to the tourism impacts analysis in that it identifies the interesting pattern of the structural change in the Australian economy when tourism export demand is cut back. Given the fact that the mining industries are the major exporting industries in the Australian economy, it is not surprising to see this pattern as a response from the economy to the reduction in tourism export demand. The decrease in tourism exports is not replaced evenly across all other exporting industries, as the expansion in mining and its associated investment creates an appreciation in the exchange rates that limits export growth in the non-mining sectors.

The immediate effect of the introduction of the new visa fee is relatively larger than the impact in the longer-run. GDP will be reduced by 0.06% initially but this adverse impact is slowly moderated to just 0.025% below the baseline. Investment in the mining industries plays an important role in the recovery of the economy from the tourism shock. The annual loss of household consumption will dwindle down from 0.1% to 0.07% after 2 years. As tourism is a labour-intensive sector, lower demand will make labour available at a lower cost to other industries; real wages will drop; and as a result, most industries will substitute labour for capital. The demand for capital across all industries in the economy is reduced by 0.02% (row 11) when employment is fully utilized again.

The analysis above is based on an average of trip spend of $8681 per person for all Chinese visitors to Australia. The average was calculated across all purposes including holiday, visiting families and friends (VFR), education, employment and other. Among these purposes, education has the highest average spend ($27,000) compared to the others. It is important to note that the averages of trip spend for visitors in the holiday ($5332) and VFR ($5307) groups are lower than the averages of all other purposes, though these two groups actually take up nearly 74% of total the Chinese visitors to Australia (TRA, 2016a). Visitors falling into these two markets segments would face an increase of 16% rather than just 10% for the average case if the proposed 10-year visa replaces existing visa fees. As such, the reduction in visitor nights could well be at 33.6% rather than 21% reduction as in the above case study. The impacts in this situation are much more severe. The effects on the holiday and VFR segments of Chinese inbound tourism are presented in Table 2.

Macro results – the impacts of 33.6% reduction in Chinese visitor nights.

Source: Model simulations.

In the results set out in Tables 1 and 2, the additional revenue from the visa fee was omitted from the simulations, implying that changes to the economy are mainly from the price response of Chinese visitors. We avoided incorporating the revenue in simulations as there are many options that the revenue can be used for. Depending on how and where the additional revenue is targeting, this will give a different result and the effects of additional revenue will mask the actual impacts of the price response from Chinese visitors. Consequently, in our analysis, the negative impact on GDP is entirely due to the increase in the visa fee. In Table 3, the extra tax revenue from visa fees is added back to GDP to identify the net effect of the increased visa fee.

Net and cumulative benefits of the increase in visa fee – $ million.

Source: Authors’ estimates.

Reduced visitation from Chines tourists as a result of the increased visa fee results in a loss of GDP to Australia. In Tables 1 and 2, GDP is measured in constant prices – that is, in real terms. The loss in GDP can be compared to the stream of extra revenues that the increase in the visa fee brings to the economy over the next 9 years. The scenarios reflecting a 21% and 33.6% reduction Chinese tourism demand can provide lower and upper limits of the possible net effects. The revenue change is calculated on the basis of forecasts for the number of first-time visitors, deducted for the loss of visitors due to price increases using the estimated price elasticities. The resultant visitor numbers are then multiplied by $865 for every year from 2016–2017 to 2024–2025. The revenue stream is then converted to the 2016–2017 values. We assume a constant discount rate of 2.4% – the inflation rate from IMF’s forecast for 2017.

Table 3 provides data for the effect estimation for both cases. The net yearly economic effects are the sum of the GDP loss and the discounted revenue received for the same year. The net cumulative economic effects at year t are given by the total of net effects from 2016–2017 up to year t.

Based on the average spend of $8681 per visitor, the increase in the visa fee could incur annual losses in the first 3 years before resulting in a net positive effect in the fourth year, 2019–2020. The total net economic loss of these three years is $592 million. It will take 6 years in total for the visa revenue to recover this total loss and generate a total of $710 million by 2024–2025. While the government could justify the sunk cost for the first 3 years for the long-term revenue objective, it is unlikely that tourism businesses can sustain 3 years with losses for the government to reap the tax benefit, as nearly 95% of tourism businesses are in the form of self-employed, micro and small sizes (TRA, 2016c). Given the importance of Chinese tourists in Australia’s tourism profile, the visa fee increase is likely to substantially erode the profitability and perhaps survival of many firms in the tourism industry.

Given that a large proportion (74%) of Chinese visitors fall within the holiday and VFR groups with lower averages of spend per person, the effects of the increased visa fee are likely to be even more severe for this market segment. For holiday and VFR tourists from China, replacement of the current visa fee by a $1000 10-year fee is likely to result in a greater proportionate increase in trip costs than for the ‘all tourist’ Chinese market and hence a greater than proportionate reduction in associated visitor numbers. In this scenario, the strong net negative effects impacts are from two sources: larger GDP losses and a much lower visitor base for the visa revenue. The net loss will occur every year over the next decade, amounting to a total loss of $3.4 billion by 2024–2025.

Conclusions

Visas are an effective tool for the governments to ensure secure borders for their countries. However, if too protective or too revenue-oriented, visas could be detrimental to the host economy due to potential losses of tourism revenue and foreign direct investment opportunity from overseas countries.

If the replacement scenario is implemented in Australia, the change of visa fee for Chinese visitors is large, ranging from the average of 10% to 16% of the spending per person for Chinese visitors. These magnitudes are much larger than any historical price changes would suggest.

China currently plays an important role to help Australia’s tourism sector reach the Potential target, which is a whole-of-government and industry long-term strategy to develop the tourism industry (Australian Government, 2016). The Chinese market has risen to be the greatest contributor to the Australian inbound tourism revenue in 2015, accounting for at least 20% in total. Growth from this market still has much more potential in the coming years given China’s transition towards a consumption-based economy.

The Australian tourism sector is on its trajectory to reach the lower limit of $115 billion of the potential. The achievement so far has been due to a raft of reforms that the government has implemented. These include the aviation reform to allow more direct flights to Australia from a range of countries including China, quicker visa processing, widening the eligibility criteria for working holiday maker visa to enlarge the employment base for the sector and an extensive marketing campaign.

Imposing a 10-year visa fee of $1000 for Chinese visitors is a risky approach if this scheme replaces the existing 3-year visa fee, as this increase will erode the demand from the largest market of the Australian inbound sector. It will effectively defeat the efforts that other reforms have made. The range of negative impacts is large for the tourism sector to overcome. This will raise a question as to whether or not the government is fully committed to the Potential target that both the government and the industry have set up. Changes to conditions of visa application such as administrative procedures, complexity of requirements and fees and charges could restrict or open up market access for foreign nationals (Liu and McKercher, 2014). Consequently, this will lower business confidence in the sector, could affect the long-term investment strategy of investors and potentially be detrimental to trade and inflow of foreign direct investment (Neumayer, 2011; Song et al., 2012).

Although Chinese visitors are increasing their overseas travel, travel is a luxury consumption for the Chinese. There is growing evidence that Chinese visitiors are sensitive to price changes to most of the long-haul destinations and towards Australia in particular (Habibi and Rahim, 2009; Pham et al., 2017; Schiff and Becken, 2011). Unless the Australian government has other non-economic objectives, increasing the visitor visa fee for Chinese visitors to $1000 would be a counter-productive policy that will cause damage to the industry in many years to come, on both demand and supply sides. Treating the visa fee issue as purely a revenue raising exercise involves placing short-term budgetary considerations ahead of future tourism market growth. To date, the Australian government has declined to take the longer-term perspective that the tourism industry would welcome. While the replacement scenario has not taken place as yet, tension between the industry and government is likely to continue as the government seeks other revenue generating mechanisms that might impact on tourism. There are various other options available to the Australian government involving changed visa fees but an essential input into policy formulation is a better understanding of the relevant price elasticities of demand for all visitors to Australia including Chinese nationals. This issue should now be a priority area of research.

Footnotes

Acknowledgements

The authors would like to thank Associate Professor John Asafu-Adjaye for his valuable comments and suggestions. Thanks are also due to Professor Susanne Becken for her strong support during this project. The authors would like to thank Tourism Research Australia for their data and constant support. As usual, any errors remain with the authors.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Supplemental material

Supplementary material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.