Abstract

In the Canary Islands (Spain), the tourism boom has been paralleled by sharp growth in the car rental sector. However, this economic activity is associated with problems such as rising levels of vehicle emissions. In this article, we discuss, on the one hand, the introduction of a tax to internalise the costs of emissions from car rental fleets and, on the other, the measures to reward users who rent environmentally-friendly cars. For this purpose, we propose a model based on statistical decision theory, from which a Bayesian rule is derived. According to this model, the tax increases with the number of days the car is rented but decreases in line with the environmental efficiency of the vehicle. A data sample of visitors to the Canary Islands is used to compare the covariates involved in computing the number of car rental days and the corresponding tax payable.

Introduction

In Europe, the transport sector produces almost a quarter of the greenhouse gas emissions recorded and is the main cause of air pollution in cities. The only sustainable response to this challenge is the implementation of an irreversible shift towards low-emission forms of transport (Diemer and Dittrich, 2018), as acknowledged in the European Strategy for Low-Emission Mobility, which was adopted in July 2016. This revolution in transport patterns has begun, but for significant results to be achieved, the uptake of low and zero-emission vehicles must accelerate greatly in the coming years.

Emissions from cars are a major problem for most cities, but in certain areas, their impact is especially acute. For example, at popular tourist destinations, large numbers of people arrive during concentrated periods of time and provoke a sharp rise in traffic levels, mainly due to the use of rented cars.

One such destination is the Canary Islands (Spain), where the car rental sector has enjoyed uninterrupted growth since 2011, spurred by the booming tourist trade. In recent years, hotel and apartment occupancy rates have been at record levels, underpinning the demand for car rental services. The Canary Islands Federation of car importers and dealers reported that turnover in this sector was around 520 million euros in 2017, 6% higher than in 2016. Reflecting the importance of this sector to public finances, the Canary Islands Government obtained sales tax the Indirect Canary Islandas tax (IGIC) revenue of some 49 million euros, from car rentals alone. Another Spanish tourist destination greatly affected by the emissions from car rental fleets is that of the Balearic Islands. In this territory, large numbers of vehicles arrive from the mainland (thus contributing nothing to local finances), causing serious problems in terms of congestion and emissions (Palmer-Tous and Riera, 2005).

To address the problem of emissions, an environmentally-friendly alternative is to promote the use of low-emission transport, such as hybrids and electric vehicles. At present, the main obstacle to the large-scale adoption of these alternatives is the fact that electric vehicles have yet to overcome the vicious circle of supply and demand; on the one hand, there are few recharge points because the numbers of electric vehicles are still very low; on the other hand, drivers are reluctant to change, not only because electric cars are expensive, but also because recharge points are few and far between. In this respect, Liao et al. (2017) observed that according to most studies in this field, the three aspects of electric cars that most limit their acceptance are price, range and charging infrastructure. In addition, regarding an aspect as fundamental as the vehicle’s source of energy, Valeri and Cerchi (2016) observed in some individuals an inherent resistance to change.

To promote environmentally-friendly and fuel-efficient transport, the Canary Islands Parliament recently eliminated the IGIC on electric vehicles and reduced the tax on hybrids to 6.5%.

In many European countries, fuel taxes are used as a means of controlling rates of vehicle emissions. However, taxation is frequently criticised on the grounds that it is employed more as a source of revenue than for environmental reasons.

Several research studies have analysed the question of fuel taxation. Some have concluded that fuel taxes are not designed as an efficient instrument to reduce emissions (see Sterner, 2007) or to correct externalities but merely to obtain revenues (Rietveld and van Woudenberg, 2005; Santos, 2017). Some have proposed alternative instruments (Frondel and Vance, 2011; Sterner, 2007). Montag (2015) advocated a more intensive use of fuel taxes, arguing that at present, this is the best instrument available for controlling levels of vehicle emissions and suggested a specific Pigouvian tax on fuel to bring the marginal cost of driving in line with marginal social costs. Such a fuel tax would depend on the type of fuel, the level of emissions produced and the rate of consumption. An alternative to this was suggested by Parry (2012), who proposed a tax based on the distance driven, to be measured by a GPS device installed in each vehicle. Bjertnaes (2017), assuming rational behaviour by consumers, described a utility function developed for a fuel tax that would correct externalities according to fuel consumption and road use. Other analysts have observed that, in addition to fuel, vehicle emissions may be influenced by lifestyle and sociocultural factors (Brand, 2019). Most researchers agree, however, that fiscal measures are among the main instruments available to the government for internalising the externalities produced by road transport. In this field, a wide range of regulatory measures have been applied in Europe, but there is a growing consensus that it is preferable to regulate less and instead to apply specific taxes based on the ‘polluter pays’ principle, with fixed taxes on the purchase price and variable ones on the use made of the vehicle (Palmer-Tous and Riera, 2005). Empirical studies have proposed fiscal measures to internalise the externalities produced by rental cars in tourism-reliant areas (Palmer-Tous et al., 2007), while externalities such as pollution and traffic congestion have also been studied by Aguiló et al. (2005), Bakhat and Rosselló (2013) and Saenz and Rosselló (2014).

Unlike the type of tax proposed by Palmer-Tous et al. (2007), ours is variable and dynamic. As a Pigouvian tax, it is intended to internalise negative externalities, but at the same time, it rewards those who rent an environmentally-friendly car. Such a tax directly affects the user and is expected to promote a change in the mode of transport adopted, fostering the use of electric vehicles. Moreover, in contrast to other fiscal instruments that target emissions, this tax is dynamic in the sense that the greater the emissions reduction achieved, the lower the tax load imposed. Another consideration of importance is that the tax we propose may be ring-fenced, with the revenue obtained being employed to provide or enhance infrastructure for electric vehicles, thus facilitating access to electric cars for the population at large (Langbhroek et al., 2019). Studies have analysed tourism patterns taking into account the average duration of car rentals. This is an important topic because recent empirical studies have shown, for example, that the average duration of car rental by tourists is positively related to the total length of stay and to the total expenditure at the destination (Aguiló et al., 2017). Therefore, policymakers, institutions and businesses reliant on the tourism sector would benefit from knowing not only the frequency and duration of car rentals but also the effects produced on exogenous variables. The rest of this article is organised as follows. The second section presents the statistical model used, and the tax instrument we propose is described in the third section. The following section sets out the relevant data for tourist stays in the Canary Islands, identifies the factors that determine characteristics of car rentals in the islands and considers the taxes paid in this respect. Finally, the main conclusions drawn are summarised in the fifth section.

The statistical model

It is widely accepted that public policies should promote the use of less polluting vehicles as part of a sustainable public transport system. In this article, we propose a tax that internalises the external costs of the emissions from rented cars in tourist areas. At the same time, this tax rewards tourists who hire a car identified as being environmentally efficient, thus promoting the use of such vehicles. In designing this tax, the variable to be modelled is the duration, N days, of car rental by a tourist. N is a random variable censored at zero, and therefore, we assume a shifted (truncated or censored at zero) Poisson (SP) distribution, with parameter

This discrete distribution is different from the zero-truncated Poisson (ZTP) distribution described by Palmer-Tous et al. (2007), who also considered the zero-truncated negative binomial (ZTNB) distribution.

The mean and variance of the distribution (1) are given by:

Given a sample

Since

In addition to the above, various factors (geographical, cultural, behavioural, etc.) influence individuals’ patterns of behaviour. For instance, tourists act differently according to whether they are at home or at their destination. Empirically, there is evidence that overdispersion is related to the heterogeneity of the population. In this case, the parameter θ can be considered a random variable that takes different values among different tourists, reflecting uncertainty about this parameter. In practice, the tourist population is non-homogeneous in the sense that it includes tourists of different ages, nationalities and so on. The prior distribution may also reflect their differing propensities to hire a car. The probability mass function of N in the tourist population is given by:

From a Bayesian standpoint,

The gamma distribution is the natural conjugate family for Poisson observations (see, for instance, Berger, 1985), which has the advantage that the posterior will also be from this family and can be found by simply updating the rules, thus avoiding the need for any numerical integration. One of the main problems with the Bayesian approach is the need to know the prior distribution. In this article, we adopt an empirical Bayesian approach, which can be viewed as a compromise between the Bayesian and the classical approach (see Casella, 1985; Robbins, 1964), and where the parameters of the prior distributions can be estimated from the data. To do so, we need the marginal (unconditional) distribution of N, which is obtained by applying (2), which produces the following well-known result:

for

respectively, and β is a dispersion parameter. Thus, the index of dispersion of this distribution is:

which may exhibit infra-dispersion or overdispersion. When

The proposed tax instrument

The tax we propose is modelled as follows. The number of days an individual hires a car is specified by the random variable N following the probability mass function

The loss function most commonly used is the quadratic loss function given by

The above procedure describes the tax that an individual must pay when θ is known. However, the population of tourists who hire cars is heterogeneous with a prior distribution

which is the mean of the prior distribution and which coincides with the mean of the unknown tax

In practice, some kind of experience is usually available. Let us suppose that a consistent sample can be obtained of the number of tourists who rent vehicles, with different types of emission labels, and that the maximum value of these is

Observe that given a sample

where

The policymaker must now calculate the best estimator of the expected number of cars to be rented in the following period (year) given the past experience of car rentals. This is done by computing the Bayes estimator of

which can be written as

where

We now have all the ingredients needed to formulate an expression for the tax to be charged to a customer who hires a car for a total of

The expression (6) assures us that at the beginning of the process, that is,

In practice, if the tax authority wishes the initial rate to be a value other than 1, it could simply be replaced (6) by:

where

The following relations of the Bayes rate are compatible with the ideas outlined above in relation to the internalisation of the externalities produced by car rentals.

The expression (8) indicates that, ceteris paribus, the tax rate increases with the number of rental days, internalising the externality related to pollution. On the other hand, the expression (9) indicates that, ceteris paribus, the tax rate decreases with the value of the efficiency identification tag, thus promoting the use of less polluting vehicles. The system seems fair, in the sense that the tax paid is proportional to the estimate derived from prior experience. The model, therefore, meets the specifications established.

Properties of the tax and elasticity

Furthermore, expression (7) can be rewritten as:

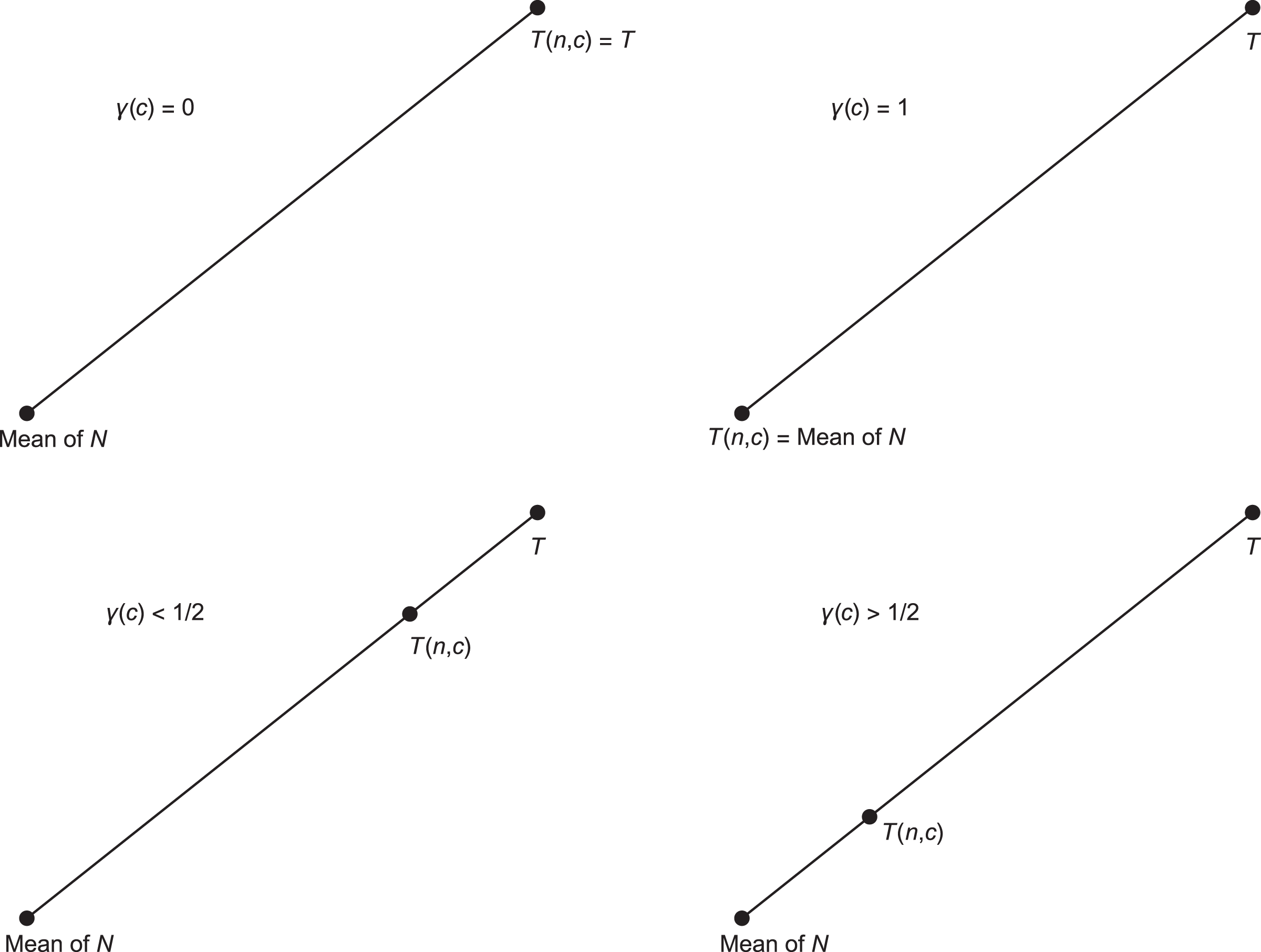

and therefore, the Bayesian tax can be written as the convex (weighted) sum of the a priori tax, T, and the number of days a customer hires a car, where the weighted factor

Here,

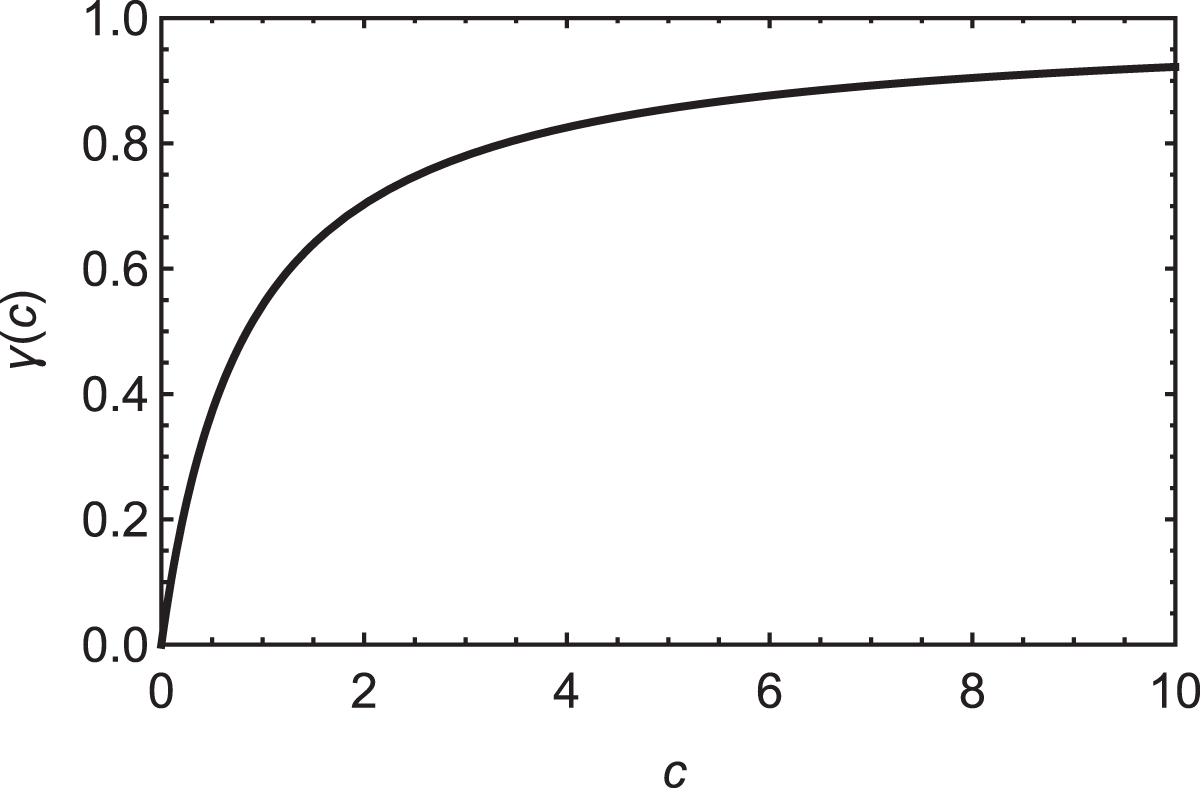

Note that

Graphic representation of the expression given in equation (11) for different values of c.

This interpretation is in accordance with Figure 2, which represents the expression given in equation (10). As can be seen, a value of

Graphic representation of the tax proposed for different values of

In conclusion, it seems clear that the weighted solution provided in equation (10) is a good linear approximation to the Bayes solution of using the posterior mean.

Expressions (8) and (9) can also be used to derive estimators of the elasticity of the proposed tax, measuring changes according to the number of days the car is rented and according to the category of environmentally-friendly tag applicable to the car in question. These estimators are obtained by:

respectively.

Empirical results

The model was implemented using a database compiled from the Canary Islands Tourist Expenditure Survey, conducted by the Canary Islands Institute of Statistics (ISTAC). This survey took the form of approximately 39,000 personal interviews with tourists on the day of their departure, among the 16 million visitors to the Canary Islands in 2017. Our study population includes the tourists who rented a car for at least 1 day and for no more than 27 consecutive days. After data cleansing, 6277 pooled observations remained.

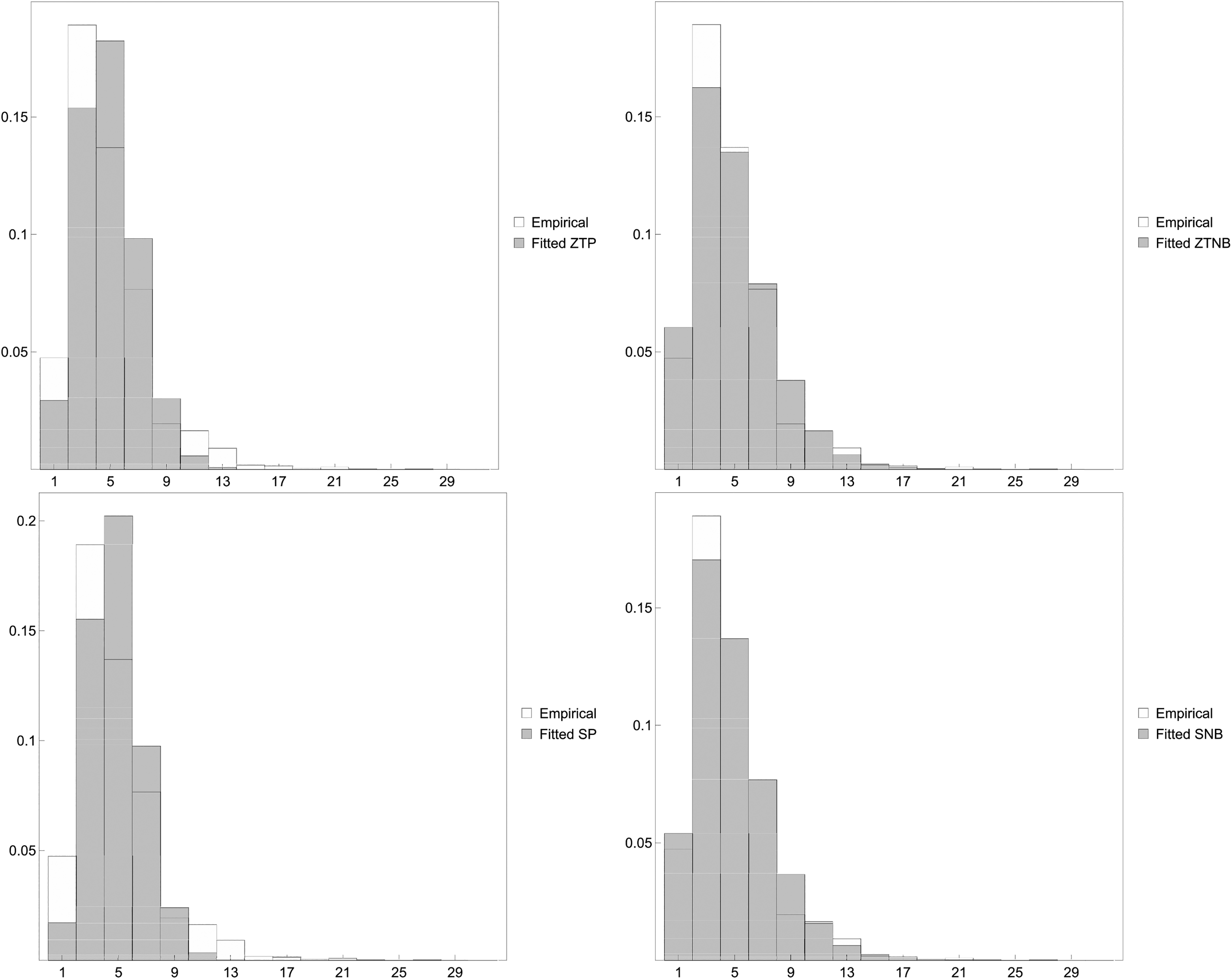

For comparison purposes, the following distribution models were used to fit the data: ZTP, ZTNB, zero-inflated Poisson and zero-inflated negative binomial. The latter two were previously used in a comparable context by Palmer-Tous et al. (2007).

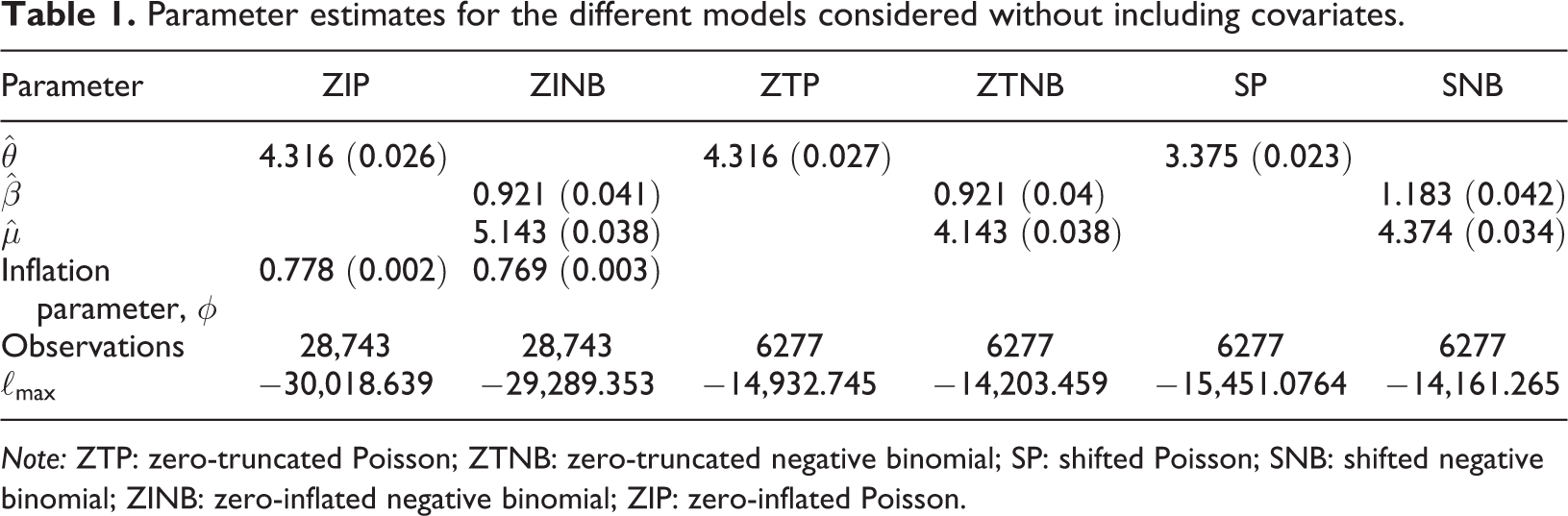

All the models have been estimated using the maximum likelihood method, and as observed in Table 1 and Figure 3, there do not seem to be significant differences between the classic models used in the literature and the modelling proposed in this work.

Parameter estimates for the different models considered without including covariates.

Note: ZTP: zero-truncated Poisson; ZTNB: zero-truncated negative binomial; SP: shifted Poisson; SNB: shifted negative binomial; ZINB: zero-inflated negative binomial; ZIP: zero-inflated Poisson.

Empirical smooth distribution of the variable ‘Car rental days’ and degree of fit for the ZTP, ZTNB, SP and SNB models. ZTP: zero-truncated Poisson; ZTNB: zero-truncated negative binomial; SP: shifted Poisson; SNB: shifted negative binomial.

We now estimate the parameters for the above models when covariates are included, to determine the suitability of each one in comparison with others discussed in previous research and mentioned above (see Palmer-Tous et al., 2007). To do so, let

which is reminiscent of the log link that is widely used in the statistical literature in this field. Here,

To define the covariates, various aspects should be considered. Barros and Pinto (2010) and Thrane and Farstad (2011) point out that services at tourist destinations are complex, and therefore, social factors and circumstantial conditions should be taken into account in any description of tourist expenditure. Brida et al. (2013) conducted a review of these questions, identified over 900 regressors that might explain tourist expenditure and classified them into four groups: economic, sociodemographic, trip-related and psychographic.

The variables we use to estimate the duration of car rental are similar to those cited by Alegre and Pou (2006), Wang and Davidson (2010), Marrocu et al. (2015), Ferrer-Rosell et al. (2015), Disegna and Osti (2016) and Gómez-Déniz et al. (2020) in their analyses of tourist demand. Aguiló et al. (2017) identified regressors concerning spending on transport at the destination, and these are also included in our study, together with those proposed by Palmer-Tous et al. (2007) regarding the application of a tax on car rentals at tourist destinations. The regressors incorporated in the present study were divided into four categories, the main descriptive statistics of which are listed in Table 2:

Descriptive statistics of variables that influence the duration of car rental.

Trip-related variables (General variables) are as follows:

(1) EXPENDITURE: The spending on goods and services at the destination, per person per day. Table 2 presents that the average tourist expenditure on car rental during the study period was 43.53 euros. Aguiló et al. (2017) classified tourist expenditure by type and observed a positive relationship between total expenditure at destination and expenditure on transport at destination. Accordingly, a higher expenditure at destination is associated with a greater duration of car rental. Similarly, Palmer-Tous et al. (2007) observed a positive and significant relationship between expenditure at destination and the number of days of car rental.

(2) STAY: The ‘length of stay’ variable is defined as the logarithm of the length of stay for the set of tourists who visit the Canary Islands and rent a car. The average value obtained is 9 days, with a minimum of 1 and a maximum of 150. Length of stay is one of the variables most frequently included in models of tourist expenditure (Brida et al., 2013). Palmer-Tous et al. (2007) reported obtaining a positive relationship between length of stay and daily expenditure on transport. However, as explained by Thrane and Farstad (2011), it seems that the positive association between length of stay and expenditure at the destination is weaker for longer-stay holidays. Nevertheless, longer stays are expected to increase the probability of a lengthier period of car rental.

(3) REPEAT: The ‘Repeat’ variable reflects the number of times the tourist has visited the Canary Islands before. It is a dichotomous variable that distinguishes whether tourists have previous experience of the destination. According to a review by Brida et al. (2013), 73% of the studies conducted in this respect have concluded that ‘Repeat’ is not a significant factor. The remaining 27% of the studies considered reported a positive, significant association between prior experience and expenditure. Aguiló et al. (2017) observed the same relationship, although in this case the association was not statistically significant.

Variables associated with trip motivation among tourists who rent a car:

(4) SUN and BEACH. This is a dummy variable that takes the value 1 when the main reason for visiting the Canary Islands is to enjoy the sun and beach offered and 0 otherwise. This variable is related to the trip motivation referring to activities such as hiking and cultural visits (Laesser and Crouch, 2006).

(5) HOLIDAY: This, too, is a dummy variable and is assigned the value 1 when the reason for travelling is to take a holiday and 0 otherwise. This variable defines the purpose of the trip, and hence, the needs the traveller intends to satisfy, such as leisure, business or family visit (Laesser and Crouch, 2006). This variable sometimes overlaps with ‘Sun and Beach’, related to activities. When this happens, both are considered to form the purpose of the trip, following Brida et al. (2013).

These two variables were also considered separately by Gómez-Déniz et al. (2020), who suggest that each may produce different effects. In this respect, Aguiló et al. (2017) observed a negative relationship between daily expenditure on transport at the destination and the reason for the trip, when this was to spend most of the time at the beach.

Variables associated with the personal characteristics of tourists who rent a car:

(6) AGE (in years): Table 2 presents that on average, the tourists surveyed were in their 40s. The youngest were aged 16 years, and the oldest, 86 years. Langbhroek et al. (2019) reported that the average age of tourists who rented electric cars was 46 years. Age is one of the various sociodemographic variables that can be used to characterise tourists and can be expressed in years or may be grouped into intervals of years. According to Alegre and Pou (2006), Brida et al. (2013) and Saayman and Saayman (2009), the relation between age and tourism expenditure is inconclusive.

(7) GENDER: A dummy variable that takes the value 1 for male tourists and 0 for females. Approximately 53% of visitors who rent a car are men. This variable was also incorporated by Palmer-Tous et al. (2007) as a sociodemographic variable, who examined the possible association between gender and the duration of car rental. No significant relation was found.

(8) INCOME: This variable represents the different income levels of tourists. It is ordered as follows: 1 = 12,000–24,000 euros; 2 = 24,001–36,000 euros; 3 = 36,001–48,000 euros; 4 = 48,001–60,000 euros; 5 = 60,001–72,000 euros; 6 =72,001–84,000 euros; 7 = over 84,000 euros.

The data in Table 2 present that the average tourist’s income is between 36,000 and 48,000 euros. In this respect, Thrane and Farstad (2011) reported a positive association between income and tourism expenditure.

(9) JOB: This sociodemographic variable (Alegre and Pou, 2006) includes employment status, differentiating by professional level, to study its impact on the length of tourist stay. In our study, 10 such levels are distinguished, among which middle-level employees form the largest group: 10 = company owner, 9 = self-employed/liberal profession, 8 = skilled employee, 7 = middle-level employee, 6 = unskilled employee, 5 = other worker, 4 = student, 3 = retired, 2 = homemaker, 1 = unemployed.

(10) NATIONALITY: This variable focuses on the tourist’s country of residence to differentiate foreign from domestic travel (Alegre and Pou, 2006; Brida et al., 2013; Wang and Davidson, 2010). The counties identified are Germany, the United Kingdom, Spain and the Nordic countries. Most of the tourists who rent cars in the Canary Islands are from the United Kingdom, followed by Spanish nationals from the mainland, Germans and those from the Nordic countries.

Variables associated with vacation characteristics:

(11) ACCOMMODATION: The type of accommodation is divided into six categories: 6 = five-star hotels, 5 = four-star hotel/apart-hotel, 4 = one/two/three-star hotel/apart-hotel, 3 = non-hotel accommodation, such as apartment, country cottage, self-catering accommodation, 2 = own home or that of friends or family and 1 = other types of accommodation. This variable has been used previously by Alegre and Pou (2006) and Palmer-Tous et al. (2007), who included it as a dummy to distinguish between hotel and non-hotel accommodation.

(12) GROUP: The number of persons travelling together. According to the data, most tourist groups are composed of two people; in our sample, the average was three. Groups composed of more than five people only accounted for 1.43% of the study population, and so it was not considered necessary to distinguish different categories (sizes) of rental car.

(13) BOOKINGADVANCE: This variable describes the extent to which the holiday was planned. Booking holidays in advance usually enables tourists to obtain lower prices and to choose from a wider range of models. This variable is divided into the following categories: 0 = the interviewee did not know when the reservation was made (because someone else had made it), 1 = the holiday was booked less than 1 week in advance, 2 = 1 week in advance, 3 = 2 weeks in advance, 4 = 3 to 4 weeks in advance, 5 = 1 to 2 months in advance, 6 = 2 to 3 months in advance, 7= more than 3 months in advance. Aguiló and Juaneda (2000), Brida et al. (2013) and Kozak et al. (2008) included advance booking time among the determinants of tourist spending. Gómez-Déniz and Pérez-Rodrguez (2019) also considered this question and included it as a dichotomous variable, observing that tourists who organise their vacations in good time can often obtain a slight reduction in cost while maintaining their preferences.

(14) LOW COST: This dummy variable takes the value 1 if the tourist has flown to the Canary Islands with a low-cost company and 0 otherwise.

(15) TRIM 1: Dummy variable. Travelling in low season (spring–summer).

(16) TRIM 2: Dummy variable. Travelling in high season (autumn–winter).

Summarising the vacation characteristics recorded, and as detailed in Table 2, most visitors to the Canary Islands who rent a car during their holiday stay in apartments, country cottages or self-catering accommodation. The group size ranges from 1 to 10, but on average, most tourist parties are composed of two or three persons. Most of those who rent a car, book their holidays 1 month in advance, 56% use low-cost companies. On the other hand, 37% of people visiting the islands in low season rent a car, instead 30% of those travelling in high season rent a car.

Results

Analysis of the results obtained shows that the duration of car rental by tourists in the Canary Islands depends on the covariates included in the model (see Table 3). Most of the coefficients obtained are statistically significant between 5% and 10%. Those for expenditure at the destination and for length of stay are positive and statistically significant. Thus, greater expenditure at the destination and longer stays are both associated with a greater duration of car rental, which is consistent with the findings reported by Palmer-Tous et al. (2007) and Aguiló et al. (2017).

Parameter estimates for the models considered, with covariates.

Note: ZTP: zero-truncated Poisson; ZTNB: zero-truncated negative binomial; SP: shifted Poisson; SNB: shifted negative binomial; ZINB: zero-inflated negative binomial; ZIP: zero-inflated Poisson.

Among the coefficients related to trip motivation, the association for the sun-and-beach mode was statistically significant and negative, meaning that tourists who come to the Canary Islands intending to spend most of their time at the beach will probably make less use of car rentals. Specifically, they are less likely to visit other areas of the island on which they are staying and when they do, spend less time doing so. Corroborating this conclusion,García Sánchezet al. (2013) and Gómez-Déniz et al. (2020) indicated that daily tourist expenditure at the destination is greater when the main reason for visiting the islands is not ‘Sun and Beach’. However, when the main reason for visiting the islands is to take a holiday, the probability of the visitor renting a car is greater; in other words, the variable ‘Holiday’ is positively associated with expenditure at the destination (Gómez-Déniz et al., 2020).

With respect to the influence of personal characteristics on the duration of car rentals by tourists, a positive and statistically significant association was obtained for age, gender, income, employment and nationality, which is in line with the findings reported by Aguiló et al. (2012) and Palmer-Tous et al. (2007), who also detected a positive relationship between age and car rental. Masiero and Zoltan (2013) reported that male (vs. female) and older men (vs. younger men) were more likely to use private transport at the destination. The tourist’s level of income is also significantly associated with the duration of car rental, which is in accordance with Palmer-Tous et al. (2007). Regarding nationality, British and Nordic tourists are less likely to rent a car, while Spanish and German visitors are more likely to do so.

Among the variables reflecting vacation characteristics, positive significant coefficients were obtained for group size and booking in advance. According to Gómez-Déniz et al. (2020), although tourists who travel in a group often obtain a slight reduction in cost, they spend more at the destination, which supports the results of our analysis. Following Brida et al. (2013) regarding the effect of group size on tourism expenditure, it seems reasonable to assume that when the total rental cost of a car depends on the number of people travelling together, the per capita expenditure will decrease as the number of travellers increases. This is borne out by our results, which show that the average duration of car rental is greater among tourists who travel as a group. For the variable ‘Booking in advance’, the results obtained show that those who plan their trip further in advance tend to rent a car for a longer period. In this respect, Masiero et al. (2015) found that booking in advance reduces costs, while Schwartz (2010) found that tourists are willing to pay more when they are booking a trip to be taken in the near future.

The variables Accommodation, Low cost and Trim 2 were inversely associated with the duration of car rentals. In this respect, Aguiló et al. (2012) reported that the use of some types of accommodation decreases the probability of car rental. Similarly, Alegre and Pou (2006) observed that tourists who stay in hotels usually spend less time at the destination than those who stay in apartments. In our own study, the most frequent type of accommodation used by tourists who rented cars was that of non-hotel accommodation, including apartments. Palmer-Tous et al. (2007) included a dummy variable to differentiate between hotel and non-hotel accommodation and observed an inverse relationship between accommodation and car rental days, which corroborates our findings. We believe that tourists who stay in better-quality hotels tend to make less use of car rentals, doing so only for specific purposes or to visit places of special interest (Langbhroek et al., 2019). Finally, tourists who use low-cost carriers to travel to the Canary Islands will save money, in comparison to those who fly with full-cost companies, but this saving is not always reflected in increased spending at the destination. Moreover, low-cost flights are often used by lower income tourists, who normally spend less at the destination than those with higher incomes (see Dobruszkes, 2013; Eugenio and Inchausti-Sintes, 2016).

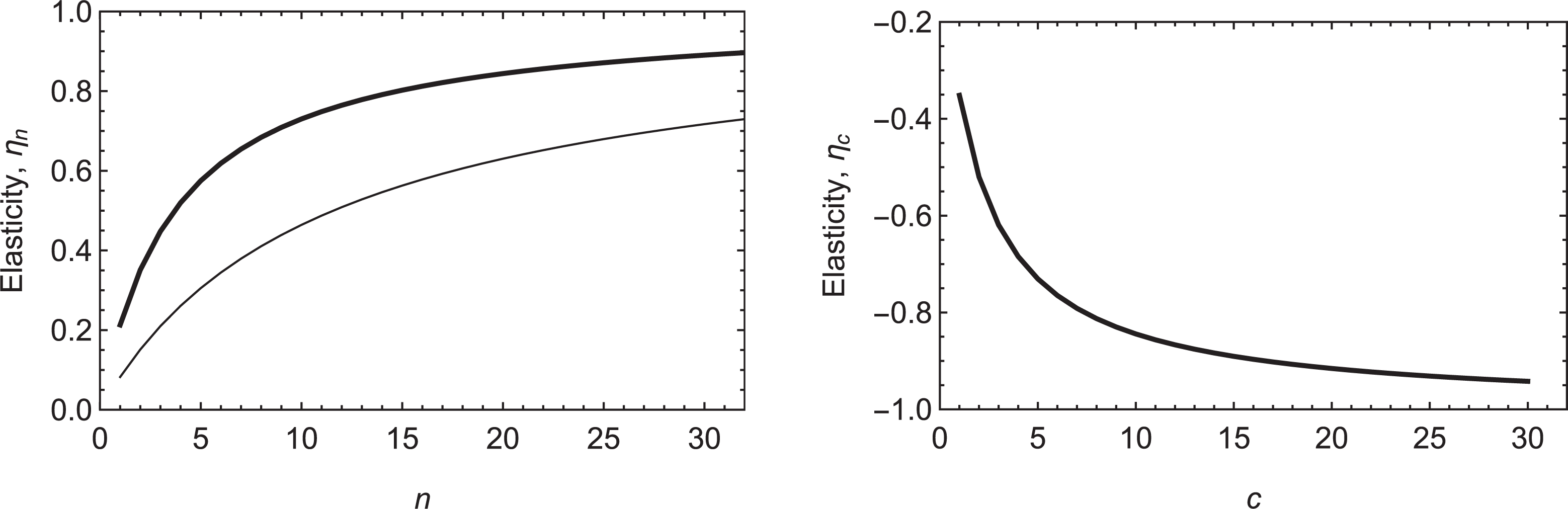

Figure 4 shows the twofold effect of the proposed tax on car rentals. On the one hand, the tax rate changes according to the duration of the car rental (left) and, on the other hand, according to the use or otherwise of a car tagged c as environmentally friendly (right). In the graphs on the left, the thick and thin lines correspond to the calculated elasticity without and with covariates, respectively. As can be seen, the tax elasticity with respect to the duration of car rental is slightly lower when the covariates are included. In the latter case, the average elasticity is 0.42 versus the reference value of 0.60, that is, when changes in tax rates are jointly explained by the duration of the rental and by the type of car rented. This suggests that the covariates buffer the changes in the reference elasticity rate. The ‘gap’ occurs because the duration of car rental depends on personal characteristics such as the reason for the vacation, the length of stay, the income level and whether the tourist is travelling alone or in a group (see Table 3). From equation (12), the dependence of

The elasticity of the proposed tax, measuring the change in the tax in response to changes in the duration of car rental (left) and the change arising from the rental of a car identified as environmentally friendly by tag c (right). The thick line represents elasticity without considering covariates, and the thin line, the elasticity when covariates are included.

Computing the tax and simulating its collection

In this section, we calculate the tax payable, according to the duration of car rental and the category of environmental efficiency of the car. Table 4 presents the results obtained for

Percentage of tax payable according to duration of rental and environmental efficiency tag c.

From the estimates presented in Table 4, the proposed tax functions as follows. Assuming a baseline rate of 1 euro per day, when a tourist rents a vehicle of the type that is least environmentally efficient, that is, tagged as

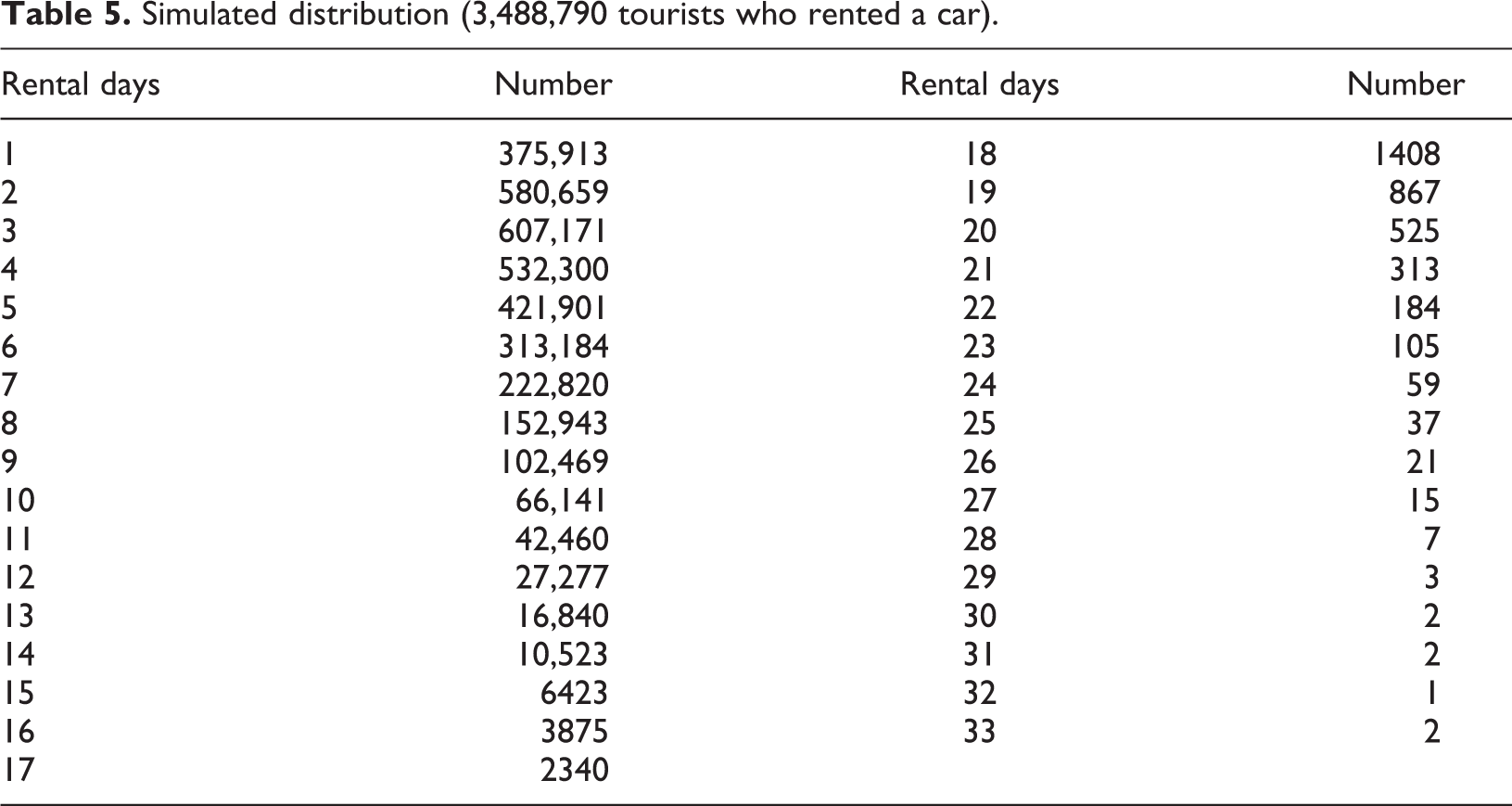

The following simulation was performed to estimate the revenue obtained from applying the proposed tax. Taking into account that in 2017, 15,975,507 tourists visited the Canary Islands and that 78.16% of them did not rent vehicles, we simulated the empirical distribution of the 3,448,790 tourists who did rent vehicles, using distribution (3) with the same mean and variance as in the sample. The empirical distribution obtained is presented in Table 5. The values corresponding to each of the rental days, ni, are randomly distributed among the five environmental tags considered, cj, which provides the quantities

Simulated distribution (3,488,790 tourists who rented a car).

The revenues expected from the proposed tax on car rentals according to their environmental efficiency are presented in Table 6. The baseline tax rates considered were 1, 5, 10 and 15 euros. For example, at the lowest rate, the expected total revenue from application of the tax would be 8,806,030 euros, which is in line with the result calculated by Palmer-Tous et al. (2007).

Collection simulation.

Final comments

Assuming that, for the environment, a sustainable car rental system is desirable, this article describes a statistical model based on the SNB distribution, which is used to represent the pattern of car rentals (by duration) in the Canary Islands, a popular destination for tourists. The proposed distribution may exhibit either overdispersion or underdispersion, as is appropriate for modelling patterns of car rentals. We propose a corrective Bayesian tax determined by the individual and collective experience of car rental. This tax increases with the number of rental days, thus internalising the externality related to the pollution produced, but decreases with the greater environmental efficiency of the vehicle.

The proposed tax is levied directly on the consumer and is based on the emissions produced from the car rental operation. However, unlike most taxes on emissions, it is not based on fuel consumption but is determined by each tourist’s individual decision regarding the model of car hired and the duration of the rental. If the tourist rents an environmentally inefficient car (

In the medium term, the impact of this tax on tourists’ car rental behaviour will lead car rental firms to expand their fleet of low-emission or electric vehicles. This outcome reflects the fact that consumer choices strongly influence the development of transport systems. However, these choices, in turn, are subject to government policies and the goods and services offered in the market (Diemer and Dittrich, 2018).

Nevertheless, the desired effect of such a tax, that is, provoking behavioural change among tourists and car rental firms, would not be achieved if it did not provide the necessary instruments to ‘break the circle’. To do so, the proposed tax should be ring-fenced, that is, the revenues collected should be used to improve transport infrastructures and, specifically, to promote the use of zero-emission vehicles. It has been observed that such a goal is more likely to be achieved in insular markets, as is the case of the Canary Islands (FENEVAL, 2018; Langbhroek et al., 2019).

In the short term, a new tax such as the one described would increase the demand for electric and hybrid cars and thus increase the average rental price. This is because the purchase price of zero and low-emission cars is currently higher than that of conventional vehicles. To alleviate this impact, many governments have implemented policies to encourage the use of electric vehicles (Hess et al., 2012; Mabit and Fosgerau, 2011, 2014). For example, in the Canary Islands, a law was recently passed to promote the purchase of low-emission vehicles, according to which electric and hybrid cars, purchased to form part of a rental fleet, would be taxed at 0% and 6.5%, respectively. However, and as observed by Palmer-Tous and Riera (2005), such measures to encourage the purchase of environmentally efficient vehicles are merely complementary; by themselves, they do not address the goal of reducing emissions. The tax we propose, therefore, is complementary to the fiscal measures currently being applied.

The market for electric vehicles is expanding rapidly. This fact, together with high levels of competition among manufacturers, leads us to believe that in the relatively near future electric cars will become price competitive with fossil-fuel vehicles and that financial incentives to purchase them will be unnecessary. Indeed, some governments already prefer to regulate the market directly; for example, the Balearic Islands administration, instead of specific taxes on emissions, has issued a new regulation according to which 2% of the fleet of rental vehicles must be electric by 2020. The Government has stated, moreover, that this percentage will rise progressively until 2035, when all rental cars on the islands must be electric. In addition, the vehicle rental companies are now obliged to report the number of vehicles in daily use and the type of technology used (FENEVAL, 2018).

An important feature of the present study is that the duration of car rental was modelled taking certain covariates into account. Thus, we were able to analyse the marginal effects of economic and sociodemographic factors related to the duration of car rentals by tourists. Our results show that in the Canary Islands, this duration depends on variables related to lifestyles and sociocultural factors, which corroborates the earlier findings of Brand (2019).

Footnotes

Acknowledgements

The authors thank the associate editor and two anonymous referees for their constructive comments and suggestions, which have greatly helped us improve the article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: EGD was partially funded by grant ECO2017-85577-P (Ministerio de Economía, Industria y Competitividad. Agencia Estatal de Investigación).