Abstract

A growing body of research has tested the protective effect of pre-COVID-19 CSR reputation or during-COVID-19 CSR action for hospitality and tourism firms but has obtained inconclusive results. These inconclusive results may have been because of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation. From the perspective of institutional theory, we use a sample of Chinese hospitality and tourism listed firms during the COVID-19 pandemic and a cluster-adjusted panel data regression with robust standard errors to reveal that the decoupling of a firm’s during-COVID-19 CSR action from its pre-COVID-19 CSR reputation negatively impacts firm value, and the negative impact is amplified for firms under stronger stakeholder scrutiny. Our findings could contribute to institutional theory by proving that decoupling is under close stakeholder scrutiny during crises and by identifying a specific type of CSR decoupling, and could offer practical implications for firms to protect their firm values during crises.

Keywords

Introduction

The hospitality and tourism (H&T) industry was among the industries most negatively impacted by coronavirus disease 2019 (COVID-19) (Assaf et al., 2022; Assaf and Scuderi, 2020). A significant decline in stock returns emerged during the pandemic (Valadkhani, 2023). Evidence shows that in addition to industrial (Abdelsalam et al., 2023) and institutional (Lee and Chen, 2022) differences, the negative effect of COVID-19 on firm performance differs among firms with distinct firm-specific features such as firm size (Harjoto et al., 2021) and asset turnover (Poretti and Heo, 2022), corporate governance features such as ownership structure (Eckey and Memmel, 2022) and board diversity (Jawed et al., 2023), and strategies such as internationalization (Lin and Falk, 2022) and business diversity (Jawed et al., 2023). Among the impacts of these firm features, the protective effects of both pre-COVID-19 corporate social responsibility (CSR) reputation (Bae et al., 2021; Lee, 2022; Poursoleyman et al., 2023) and during-COVID-19 CSR action (Zhu and Zhang, 2022) have attracted increasing attention. The protective effect of CSR, which originates in its stakeholder logic, reflects the concept that CSR helps develop a reciprocal relationship among various stakeholders, and the stakeholder trust and cooperation generated from such a relationship in both normal times and during crises can protect firms against the consequences of COVID-19. Specifically, investors tend to believe that firms with a high pre-COVID-19 CSR reputation or that take substantial during-COVID-19 CSR action are more resilient to COVID-19 and, thus, less likely to withdraw their investments in these firms or more likely to buy their shares. Therefore, stock returns experience a milder decline and take a shorter time to recover for firms with a higher level of CSR performance (Ding et al., 2021). However, in the research, an agreement cannot be reached on the existence of the protective effects of these two types of CSR strategies. Some studies confirmed the protective effect of pre-COVID-19 CSR reputation (Ding et al., 2021; Poursoleyman et al., 2023) or during-COVID-19 CSR action (Zhu and Zhang, 2022). In contrast to these findings, other studies found that pre-COVID-19 CSR reputation (Bae et al., 2021) or during-COVID-19 CSR action (Chen et al., 2022) is inefficient in protecting the firm value during COVID-19.

Relative to firms in other industries, although firms in the H&T industry have been more adversely impacted by the pandemic, they actively participated in CSR activities during COVID-19 (Gürlek and Kılıç, 2021; Qiu et al., 2021). The reason for this anomalous phenomenon might be that H&T firms expected to use CSR activities to protect their firm values during COVID-19. However, only a small number of studies tested the protective effect of pre-COVID-19 CSR reputation or during-COVID-19 CSR action in the H&T industry context, and the results are also inconclusive (Qiu et al., 2021; Shin et al., 2021; Yeon et al., 2021). One possible reason for the inconclusive results might be that pre-COVID-19 CSR reputation and during-COVID-19 CSR action do not impact firm value alone. For example, Qiu et al. (2021) noticed that CSR actions during COVID-19 in firms with a better historical CSR reputation can attract additional stakeholder attention. Investors and other stakeholders may consider both and respond accordingly. However, the fragmented nature of studies in the general industry context and the limited number of studies in the H&T industry result in a failure to answer the research question of why the results of the protective effects of pre-COVID-19 CSR reputation and during-COVID-19 CSR action are inconclusive.

A firm’s pre-COVID-19 CSR reputation may set a standard in stakeholders’ minds to expect a level of its during-COVID-19 CSR action, and the decoupling of a firm’s during-COVID-19 CSR action from its pre-COVID-19 CSR reputation may significantly affect firm value. Unlike the argument of institutional theory that decoupling is unlikely to be scrutinized by stakeholders (Meyer and Rowan, 1977; Zajac and Westphal, 2004), Marquis and Qian (2014) argued that symbolic CSR activities are under the close scrutiny of various stakeholders. Prior studies noted that investors can distinguish between genuine and symbolic CSR activities (Bae et al., 2021), and only authentic and genuine CSR activities can protect firm value (He and Harris, 2020). Therefore, rather than testing the direct impact of pre-COVID-19 CSR reputation or during-COVID-19 CSR action, we examine the possible negative impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on firm value.

Moreover, since decoupling may negatively impact firm value once stakeholders recognize the decoupling, the extent of the stakeholder scrutiny may strengthen that negative impact. Prior studies revealed that firm age is a commonly used indicator of stakeholder embeddedness (Gao and Hafsi, 2017; Marquis and Qian, 2014), and larger firms (Gao and Hafsi, 2017; Lyons et al., 2016; Wang and Qiao, 2022) and more internationalized firms (Kang, 2013) are considered more visible to stakeholders. Because firm visibility is highly associated with stakeholder scrutiny, and stakeholder embeddedness provides substantial access for stakeholders to scrutinize firm CSR activities, firm age, firm size, and internationalization may be considered typical indicators of stakeholder scrutiny, and the stronger the stakeholder scrutiny of one firm’s decoupling is, the more likely it is to be punished by stakeholders. Therefore, the impact of stakeholder scrutiny is also considered by testing the moderating effects of firm age, firm size, and internationalization.

To fill the above research gaps, we aim to examine the impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on H&T firm value and the moderating effect of stakeholder scrutiny. Using a sample of Chinese H&T listed firms during COVID-19, we find that the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation negatively impacts firm value and that stakeholder scrutiny significantly strengthens this negative impact. Unlike prior studies focused predominantly on testing the protective effect of pre-COVID-19 CSR reputation (Marco-Lajara et al., 2022; Yeon et al., 2021) or during-COVID-19 CSR action (Qiu et al., 2021; Shin et al., 2021) on H&T firm value, we are among the first to analyze the joint impact of pre-COVID-19 CSR reputation and during-COVID-19 CSR action. The findings support the argument that stakeholders evaluate firms’ CSR by comparing it with their expectations (Wang and Qiao, 2022) by highlighting that stakeholders set their expectations based on firms’ previous CSR reputation.

The findings of this study make important theoretical and practical contributions. Theoretically, through this study, we significantly contribute to institutional theory by highlighting that decoupling is scrutinized by stakeholders and by identifying a new type of CSR decoupling. Inspired by Marquis and Qian’s (2014) research that showed that symbolic CSR activities are closely scrutinized by various stakeholders, we empirically prove that stakeholders can punish firms for decoupling and that punishments are enhanced for firms that face stronger stakeholder scrutiny. In addition to other types of CSR decoupling recognized by prior studies (Gull et al., 2022; Tashman et al., 2019), we identify a new type of CSR decoupling, which is the decoupling of during-crisis CSR action from precrisis CSR reputation. In addition to the theoretical contributions, these findings can offer practical implications for H&T firms to protect firm value during crises through the strategic use of CSR activities.

Literature review and hypotheses development

Protective effect of pre-COVID-19 CSR reputation

Two distinct CSR logics prevail as to why firms conduct CSR activities: stakeholder logic and shareholder logic. Using the stakeholder logic of CSR, prior studies demonstrated that hospitality and tourism firms’ CSR performance in normal times positively affects returns on advertising spending (Assaf et al., 2017), firm competitiveness (Nguyen et al., 2019), and firm performance (Uyar et al., 2023). During COVID-19, the effect of firms’ pre-COVID-19 CSR reputation on firm performance during COVID-19 has attracted increasing attention; however, most studies focused on the general industry context. Some studies argued that CSR reputation helps develop a reciprocal relationship among various stakeholders, stakeholder trust and cooperation generated from such a relationship in normal times can protect firms against COVID-19, and thus, pre-COVID-19 CSR reputation significantly enhances employees’ psychological capital (Mao et al., 2021) and organizational commitment (Filimonau et al., 2020) and reduces firm risk (Huang and Ye, 2021) during COVID-19. A larger body of studies tested the effect of pre-COVID-19 CSR reputation on firm value. Some studies confirmed the positive financial outcomes of pre-COVID-19 CSR reputation (Ding et al., 2021; Poursoleyman et al., 2023). For example, Poursoleyman et al. (2023) confirmed that pre-COVID-19 CSR reputation significantly increases firms’ resilience against adverse shocks from the pandemic.

In line with the inconclusive relationships between CSR and hospitality and tourism firm financial outcomes in normal times (Lee et al., 2023), the protective effect of pre-COVID-19 CSR reputation remains inconclusive since some other studies found its nonsignificant (Bae et al., 2021) or even negative impact on firm value (Huang et al., 2021). Such a nonsignificant or negative effect originates in the shareholder logic of CSR that CSR activities are conducted at the expense of shareholder wealth; thus, CSR could not protect firm value during COVID-19 (Bae et al., 2021; Huang et al., 2021). For instance, Bae et al. (2021) suggested that precrisis CSR reputation is ineffective in shielding shareholder value during COVID-19.

Compared with the large number of studies in the general industry context, only a small number of studies examined the protective effect of pre-COVID-19 CSR reputation for H&T firms (Marco-Lajara et al., 2022; Yeon et al., 2021). For instance, Marco-Lajara et al. (2022) demonstrated a positive impact of pre-COVID-19 CSR reputation on resilience and a positive impact of resilience on hotel performance. However, such a limited number of studies cannot provide sufficient evidence for the protective effect of pre-COVID-19 CSR reputation for H&T firms.

Protective effect of during-COVID-19 CSR action

Firms’ CSR spending increased considerably during the COVID-19 pandemic (Gürlek and Kılıç, 2021). CSR activities were implemented in response to the pandemic to support firms’ key stakeholders (He and Harris, 2020). Therefore, in addition to pre-COVID-19 CSR reputation, the protective effect of firms’ during-COVID-19 CSR action attracted increasing academic attention. In the general industry context, stakeholder logic and shareholder logic also exist for during-COVID-19 CSR action. Some studies confirmed that during-COVID-19 CSR action significantly protects firm value during COVID-19 (Zhu and Zhang, 2022). For instance, Zhu and Zhang (2022) confirmed that firms obtain positive abnormal stock returns through philanthropic donations during COVID-19. Contrary to these findings, other studies demonstrated that during-COVID-19 CSR action is inefficient in protecting firm value against COVID-19 (Chen et al., 2022). For instance, Chen et al. (2022) found that investors react negatively to COVID-19-related philanthropic donations.

A large body of studies discussed the during-COVID-19 CSR action of H&T firms; however, most focused on the impact of during-COVID-19 CSR action on employee or customer outcomes (Sun et al., 2022; Tong et al., 2021). Only a small set of studies discussed the effect of during-COVID-19 CSR action on H&T firm value and found inconclusive results (Qiu et al., 2021; Shin et al., 2021). For instance, Qiu et al. (2021) investigated the impact of COVID-19-related CSR activities on hospitality firm stock returns in the Chinese stock market and found that engaging in CSR activities can significantly increase stock returns. However, Shin et al. (2021) found that providing free accommodations to healthcare workers during COVID-19 has a negative impact on hotels’ firm values.

The decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation

From the perspective of institutional theory, firms often face the dilemma that conformity to institutional rules for external legitimacy creates conflicts and inconsistencies in technical activities for internal efficiency (Luo et al., 2017; Meyer and Rowan, 1977). Decoupling, which refers to the strategic use of the misalignment between institutional rules and activities, is an important device to resolve conflicts between legitimacy and efficiency (Meyer and Rowan, 1977). In CSR research, CSR decoupling normally refers to a symbolic strategy that can manifest as the misalignment between firms’ CSR reporting and CSR performance (Gull et al., 2022; Tashman et al., 2019) or the rapid adoption of poor quality CSR reporting (Luo et al., 2017).

However, the advantage of decoupling depends on the assumption that stakeholders do not scrutinize decoupling. Otherwise, scrutiny accompanies and produces illegitimacy (Hawn and Ioannou, 2016; Meyer and Rowan, 1977). Therefore, firms tend to minimize scrutiny by both internal and external stakeholders (Meyer and Rowan, 1977; Zajac and Westphal, 2004). Stakeholders such as accrediting agencies, boards of trustees, government agencies, and individuals also tend to minimize scrutiny because they tend to function as organized representatives of society, and maintaining stable and predictable relationships with firms is better than relying on scrutiny (Meyer and Rowan, 1977). Among the limited number of studies examining the outcomes of CSR decoupling, some confirmed that CSR decoupling can improve firm performance if it is not recognized by stakeholders (Schons and Steinmeier, 2016). However, a small number of studies noted that decoupling is closely scrutinized by stakeholders (Marquis and Qian, 2014); thus, CSR decoupling negatively impacts firm performance (Hawn and Ioannou, 2016).

In line with the symbolic nature of decoupling, in the case of COVID-19, the misalignment between during-COVID-19 CSR action and pre-COVID-19 CSR reputation can be defined as a specific form of CSR decoupling. The historical CSR reputation can be considered to represent stakeholder expectations, which guides firms’ during-COVID-19 CSR action in a way that those with a higher pre-COVID-19 CSR reputation are expected to invest more in during-COVID-19 CSR action (Rolf, 2023). Moreover, firms’ low during-COVID-19 CSR action can be treated as a symbolic strategy to maintain internal efficiency by constraining costs during COVID-19 and external legitimacy by responding to stakeholder expectations. High CSR decoupling means that a firm’s during-COVID-19 CSR action cannot live up to its pre-COVID-19 CSR reputation.

We argue that CSR decoupling negatively impacts firm value because the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation was closely scrutinized by stakeholders during COVID-19. Although institutional theory argues that firms and stakeholders tend to minimize scrutiny when firms engage in decoupling strategies (Meyer and Rowan, 1977; Zajac and Westphal, 2004), stakeholders paid considerable attention to not only COVID-19 (Wang et al., 2022a) but also COVID-19-related CSR activities (Bae et al., 2021) during the pandemic, especially for firms in the H&T industry—one of the most adversely impacted industries (Qiu et al., 2021). During COVID-19, firms are expected to engage in CSR activities to help contain the spread of COVID-19 and protect their stakeholders (Mao et al., 2021; Qiu et al., 2021). In this case, even though firms tend to avoid scrutiny, stakeholders may closely monitor and evaluate firms’ during-COVID-19 CSR action since these COVID-19-related CSR actions are directly and closely related to stakeholder interests.

Once stakeholders notice decoupling, its symbolic nature may lead stakeholders to question the motives of firms’ during-COVID-19 CSR action because prior studies found that public-serving, altruistic, or intrinsic motives are more effective in obtaining positive stakeholder responses, whereas self-serving, egoistic, or extrinsic motives are likely to translate to negative responses (Lin et al., 2022). It was proven that firms are expected by various stakeholders to engage in CSR activities (Vaughan and Koh, 2023) and stakeholders may not only reward firms’ CSR activities but also have the power to punish firms if these CSR activities fail to satisfy their expectations (Wang and Qiao, 2022). Given that stakeholders can distinguish genuine from symbolic CSR activities (Bae et al., 2021) and that only genuine CSR activities provide a protective effect on firm value (He and Harris, 2020), greater decoupling means that stakeholders’ expectations are less likely to be satisfied, and the corresponding stakeholder punishments rather than rewards hinder investors’ evaluations. Therefore, the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation may negatively affect firm value. Therefore, we hypothesize the following:

The decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation has a negative impact on H&T firm value during the COVID-19 pandemic.

Stakeholder scrutiny

Prior studies noted that firms whose activities are more strongly scrutinized are more likely to respond substantially to stakeholder expectations (Marquis and Qian, 2014), and symbolic CSR actions can only yield a positive effect on firm performance for actions directed toward low-proximity stakeholders because these stakeholders have greater difficulty distinguishing between symbolic and substantial CSR actions (Schons and Steinmeier, 2016). We argue that firms that face stronger stakeholder scrutiny may be more severely punished for the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation than are firms that face weaker stakeholder scrutiny.

Firm age, firm size, and internationalization may be essential indicators for stakeholder scrutiny because older, larger, and more internationalized firms face higher scrutiny or scrutiny from a larger number of stakeholders. Since older firms are more deeply embedded in relationships with stakeholders such as the government than young firms (Gao and Hafsi, 2017; Marquis and Qian, 2014), embeddedness provides stakeholders with more convenient access to firm CSR activities. Thus, older firms may be faced with higher stakeholder scrutiny. Large firms are more visible to stakeholders than are small firms (Cordeiro and Tewari, 2015). Such visibility exposes larger firms and their CSR activities to a larger number of stakeholders (Gao and Hafsi, 2017; Wang and Qiao, 2022). Regarding CSR, Lyons et al. (2016) found that relative to large firms, small firms are less subject to stakeholder scrutiny and practice CSR differently. Therefore, larger firms are scrutinized by a larger number of stakeholders regarding CSR activities. Regarding internationalization, international presence enhances the visibility of a firm’s CSR activities to a larger number of stakeholders from both domestic and foreign markets and to influential monitoring bodies, including international activist groups such as high-profile NGOs and international media (Kang, 2013). Therefore, more internationalized firms are under higher scrutiny from a larger number of stakeholders.

During the COVID-19 pandemic, higher scrutiny for older firms, scrutiny from a larger number of stakeholders for larger firms, and higher scrutiny from a larger number of stakeholders for more internationalized firms make the decoupling of these firms’ during-COVID-19 CSR action from pre-COVID-19 CSR reputation more likely to be recognized by stakeholders. Consequently, the corresponding stakeholder punishments may result in a greater decline in firm value. Overall, we hypothesize the following:

The stronger the stakeholder scrutiny is (older, larger, and more internationalized firms), the greater is the negative impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on H&T firm value during the COVID-19 pandemic.

Methodology

Data and sample

The Chinese H&T industry has been greatly affected by the COVID-19 pandemic (Wang et al., 2022b, 2022c). Thus, a sample of Chinese listed H&T firms is used to test the impact of CSR decoupling on firm value. Wuhan city in Hubei Province, where the first confirmed case of COVID-19 was detected, was locked down to contain the spread of the virus. Its reopening is considered to mark a temporary period in the pandemic and its negative impact on the H&T industry. Therefore, we test the hypotheses using a period from 20 January, 2020, the day on which the Chinese government recognized the human-to-human transmission of the SARS-CoV-2 virus, to 7 April, 2020, the last day of the Wuhan city lockdown.

To examine the effect of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation, data were collected from multiple sources. Daily stock returns of Chinese H&T firms, daily confirmed COVID-19 cases, and firm features were collected from the China Stock Market and Accounting Research database (Qiu, et al., 2021; Wang and Qiao, 2023; Wang et al., 2022b). Data on the pre-COVID-19 CSR reputation was collected from the Hexun CSR rating system (Wang and Qiao, 2022). In line with Qiu et al.’s (2021) research, during-COVID-19 CSR action was collected from news on firms’ COVID-19-related CSR activities during the pandemic. Based on all 37 Chinese H&T listed firms, our final sample consists of 1521 firm-day observations of 31 firms after merging these databases and removing observations with missing data for key variables. Detailed information on the pre-COVID-19 CSR reputation and during-COVID-19 CSR action of these firms is presented in Appendix A.

Measurement

Firm value is the dependent variable. Following Sharma and Nicolau (2020) and Wang et al. (2023), firm value was measured as daily stock returns. The decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation (CSR decoupling) was measured by subtracting the normalized value of during-COVID-19 CSR action from the normalized value of pre-COVID-19 CSR reputation. Consistent with studies that measure CSR reputation with CSR performance ratings of the focal year (Carlos and Lewis, 2018), pre-COVID-19 CSR reputation was measured as a firm’s Hexun CSR rating of 2019. Based on the difference-in-difference approach used by Qiu et al. (2021), during-COVID-19 CSR action was operationalized in terms of the natural log of the monetary value of a firm’s COVID-19-related donations plus 1 for firm days on which the firm has CSR donations in place and 0 otherwise. For firms that provided in-kind donations, the monetary value was calculated using the market price of the goods and/or services. For firms that donated more than once, the value of the during-COVID-19 CSR action was calculated as the natural log of the sum of previous donations plus 1 for firm days after each donation. For the moderators, firm age (Firm age) was calculated as the number of years since a firm’s initial public offering, firm size (Firm size) was calculated as the natural log-transformed firm total assets, and internationalization (Internationalization) was measured as the foreign sales ratio, in line with Kang (2013).

We included the number of daily confirmed COVID-19 cases and several key firm features as control variables. Following the literature, we calculated the number of daily confirmed COVID-19 cases (Cases) as the natural log-transformed daily confirmed COVID-19 cases plus 1 in the province where the focal firm is located (Wang et al., 2022a). State-owned enterprises (SOEs) were measured as a binary variable that takes the value of 1 if a firm is controlled by the government and 0 otherwise. The Shenzhen Stock Exchange (Shenzhen) was measured as a binary variable that takes the value of 1 for firms listed on the Shenzhen Stock Exchange and 0 otherwise. Firm profitability (Profitability) was calculated as industry-adjusted return on assets. Leverage (Leverage) was calculated as the ratio of total debts to total assets.

Estimation method

Models (1) and (2) examine the impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on H&T firm value and the moderating effects of firm age, firm size, and internationalization. All firm-level moderators and control variables for 2019 were used to predict firm value. Given that the number of daily confirmed cases of day

Results

Descriptive statistics

Descriptive analysis and correlation.

Note: N = 1521; ***p < .01, **p < .05, *p < .1.

Main analyses

The impact of the CSR decoupling on firm value.

Note: Robust standard errors in parentheses; ***p < .01, **p < .05, *p < .1.

To test the moderating effect of stakeholder scrutiny, Models 2, 3, and 4 include the interaction term between CSR decoupling and firm age, the interaction term between CSR decoupling and firm size, and the interaction term between CSR decoupling and internationalization, respectively. The results in Model 2 suggest that the coefficient of the interaction term between CSR decoupling and firm age is negative and significant (

The coefficient of the interaction term between CSR decoupling and firm age remains significant in Model 5 when including all of the interactions. However, the coefficient of the interaction term between CSR decoupling and internationalization becomes nonsignificant, suggesting that the moderating effect of internationalization is not as stable as firm age. One possible reason for the nonsignificant moderating effects of firm size and firm age might be that older firms were scrutinized to a larger extent than larger or more internationalized firms during the pandemic of COVID-19. Taken together, hypothesis 2 is partially supported.

Regarding the control variables and moderators, the results show that the coefficients of most of the control variables are significant. Specifically, the number of daily confirmed COVID-19 cases is negatively related to firm value, implying that firms operating in more severely infected regions suffer more from COVID-19. In line with prior studies that demonstrated that the impact of COVID-19 varies for firms with different firm-specific features (Harjoto et al., 2021; Lin and Falk, 2022), the results show that most of the control variables are significant. Firm profitability has a negative effect, indicating that the firm value of more profitable firms may have experienced a greater decline during COVID-19. Firms with higher leverage are more adversely impacted by COVID-19. One explanation is that firms with higher risk are evaluated more negatively by investors. SOEs and older firms are more badly hit by the pandemic, reflecting that political legacies or inertia embedded in government ownership and firm age may have significantly hindered their ability to adapt to the new environment during COVID-19. In contrast, larger and more internationalized firms are less severely impacted by COVID-19. One explanation is that the level of business diversity or regional diversity is higher for larger and more internationalized firms. Investors may consider these firms to be more resilient to constraint measures such as social distancing policies, lockdowns, and travel bans. The significant effect of the Shenzhen Stock Exchange may reflect differences in firm features or investor preferences between firms listed on the Shenzhen and Shanghai Stock Exchanges.

Robustness checks

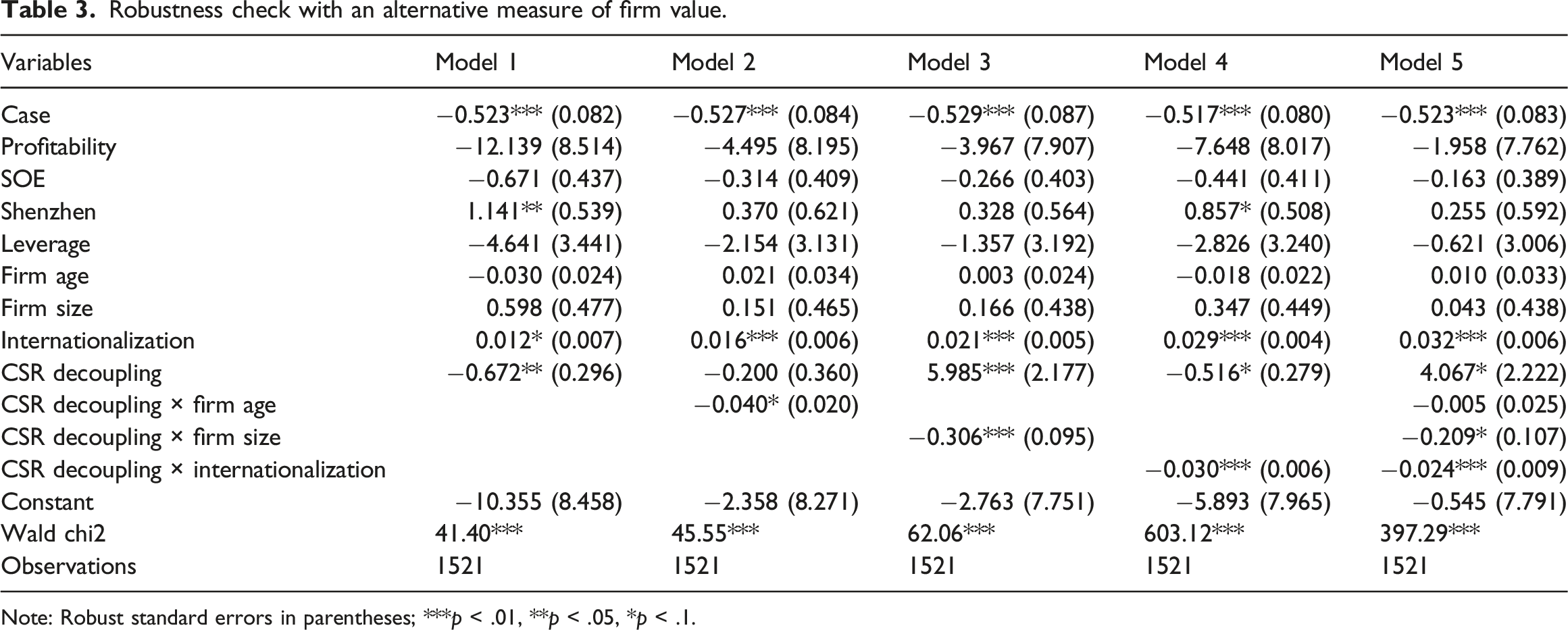

Robustness check with an alternative measure of firm value.

Note: Robust standard errors in parentheses; ***p < .01, **p < .05, *p < .1.

Robustness check with an earlier time period.

Note: Robust standard errors in parentheses; ***p < .01, **p < .05, *p < .1.

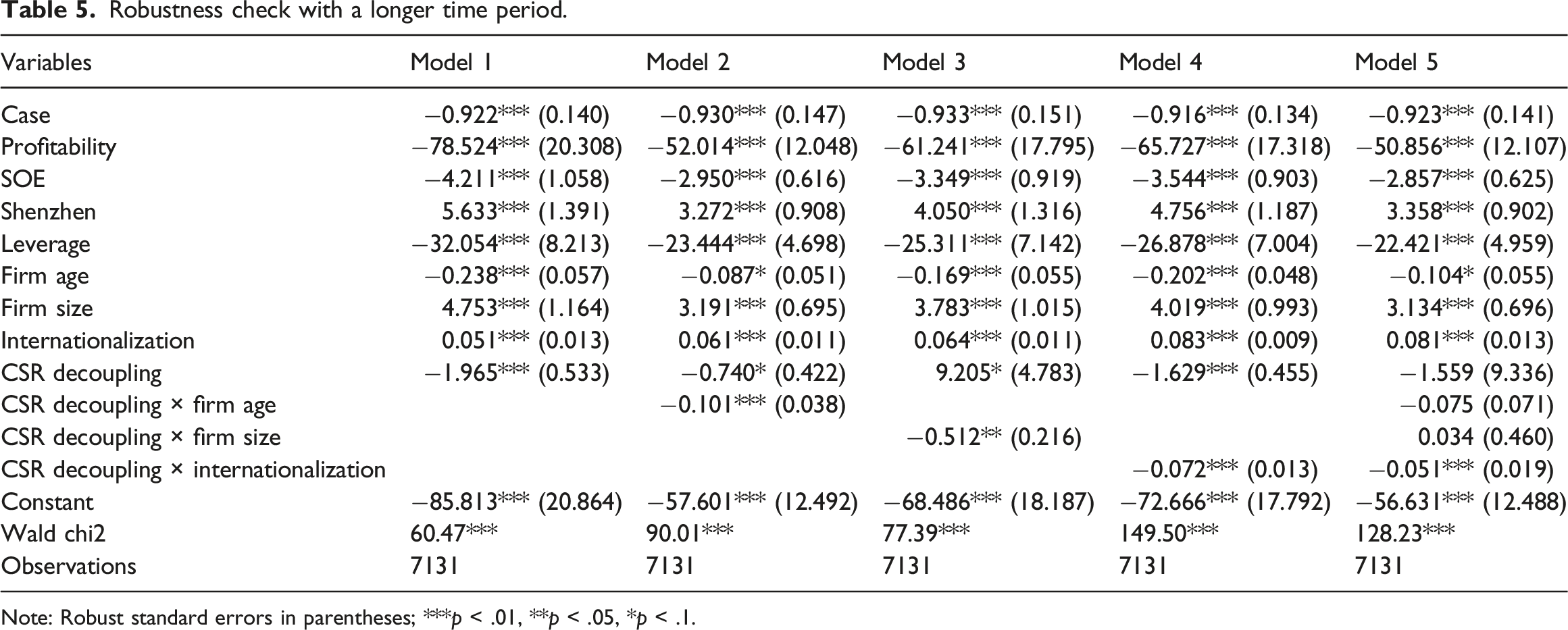

Robustness check with a longer time period.

Note: Robust standard errors in parentheses; ***p < .01, **p < .05, *p < .1.

Conclusions and discussion

Conclusions

The most important finding of this study is that pre-COVID-19 CSR reputation and during-COVID-19 CSR action do not impact firm value alone. The literature examined the protective effect of pre-COVID-19 CSR reputation (Marco-Lajara et al., 2022; Yeon et al., 2021) or during-COVID-19 CSR action (Qiu et al., 2021; Shin et al., 2021) on H&T firm value separately. To our knowledge, only Qiu et al. (2021) considered both pre-COVID-19 CSR reputation and during-COVID-19 CSR action to predict stakeholder attention. Inspired by but going beyond Qiu et al.’s (2021) study, we tested the impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on H&T firm value. The negative impact of decoupling demonstrated that pre-COVID-19 CSR reputation and during-COVID-19 CSR action have a joint impact on firm value, and firm value declines if a firm’s during-COVID-19 CSR action fails to match its pre-COVID-19 CSR reputation. In other words, the higher the historical CSR reputation is, the harder it is for firms to satisfy investors’ and other stakeholders’ expectations regarding firms’ COVID-19-related CSR actions.

The negative impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on H&T firm value and the moderating effect of stakeholder scrutiny found in this study highlight that firms’ CSR activities are closely monitored by stakeholders, and stakeholders evaluate these CSR activities based on the comparison between firms’ during-COVID-19 CSR action and historical CSR reputation. Regarding the impact mechanism of CSR on firm performance, prior studies noted that stakeholders may compare firms’ CSR activities with their expectations and reward or punish firms based on such evaluations (Wang and Qiao, 2022). However, the benchmark on which stakeholders set their expectations is unclear. We go a further step by finding that stakeholders set their expectations based on firms’ historical CSR reputations. If firms’ CSR actions fail to live up to their historical CSR reputations, investors’ and other stakeholders’ punishments lead to negative financial outcomes.

Theoretical implications

In this study, we make important contributions to institutional theory. First, we contribute to institutional theory by proving that decoupling is under close stakeholder scrutiny during crises. Contrary to studies suggesting that firms and stakeholders tend to minimize scrutiny over decoupling strategies (Meyer and Rowan, 1977; Zajac and Westphal, 2004) or that low-proximity stakeholders have greater difficulty scrutinizing symbolic CSR actions directed toward them (Schons and Steinmeier, 2016), the negative impact of CSR decoupling on firm value proved in this study suggests that during crises, symbolic CSR actions are closely scrutinized by stakeholders even though during COVID-19, CSR actions are directed toward the general public, a low-proximity stakeholder. This finding supports the argument that decoupling is monitored and evaluated by stakeholders (Marquis and Qian, 2014) and that firms are punished once stakeholders recognize their decoupling strategies (Hawn and Ioannou, 2016). The significant moderating effect of stakeholder scrutiny further supports this argument by proving that stakeholder scrutiny amplifies the negative impact of the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation on H&T firm value.

Second, we add to institutional theory by focusing on a new type of decoupling, which is the decoupling of during-crisis CSR action from precrisis CSR reputation. Decoupling, defined as the misalignment between institutional rules and activities (Meyer and Rowan, 1977), takes various forms in firm strategies and practices. Regarding CSR decoupling, prior studies suggested that CSR decoupling has various definitions. CSR decoupling can be defined as the misalignment between firms’ CSR reporting and CSR performance (Gull et al., 2022; Tashman et al., 2019) or the rapid adoption of CSR reporting with poor quality (Luo et al., 2017). We recognized a new form of CSR decoupling, which is the decoupling of during-crisis CSR action from precrisis CSR reputation, and demonstrated its significant impact on firm value during crises.

Practical implications

Our findings are of great importance to the decision makers of H&T firms. First, the findings of this study reveal that the decoupling of during-COVID-19 CSR action from pre-COVID-19 CSR reputation negatively impacts firm value. This result indicates that if decision makers want to benefit more from firms’ during-COVID-19 CSR action, the level of such action should match the level of pre-COVID-19 CSR reputation. This finding provides decision makers with a critical guideline to make the decision on the monetary value invested in during-crisis CSR action. The practical implications of prior studies emphasize the absolute value or the industry-adjusted value of corporate philanthropic giving during crises (Qiu et al., 2021). This study recognizes the importance of the value of a firm’s during-crisis CSR action relative to its historical CSR reputation. Therefore, decision makers are highly encouraged to consider firms’ precrisis CSR reputation when conducting their during-crisis CSR action. Specifically, firms with a higher historical CSR reputation should donate more resources to the relief of the crisis to satisfy investors’ and other stakeholders’ expectations. Firms with lower historical CSR reputation can choose to donate less since stakeholders have lower expectations regarding these firms’ during-crisis CSR action.

Second, firms under stronger stakeholder scrutiny need to better match their CSR action during crises with historical CSR reputation. The results of the moderating effect tests show that firms facing stronger stakeholder scrutiny are more severely punished for CSR decoupling. Therefore, firms with certain features, such as an older age, a larger size, or higher internationalization, need to pay more attention to evaluating the range and level of their stakeholder scrutiny. Stakeholder salience theory, which suggests that stakeholders with the features of power, legitimacy, and urgency have a stronger influence on firm outcomes, can be applied to evaluate stakeholders. Based on a systematic evaluation, firms facing stronger scrutiny can take the opportunity to protect their firm value from stakeholder punishments and crises shocks by conducting more genuine during-crisis CSR action.

Limitations and future research

The archival data are inefficient for illustrating the underlying investors’ decision-making processes when comparing pre-COVID-19 CSR reputation and during-COVID-19 CSR action. Moreover, the archival data cannot be used to directly measure stakeholder scrutiny. Therefore, future research can use other methods, such as surveys or experiments, to uncover decision-making processes and directly measure stakeholder scrutiny. In terms of generalizability, we conducted the analyses for an emerging market. Since institutional settings (Hamrouni et al., 2023) and national cultures (Song and Kang, 2019) may shape the motives of CSR and investors’ decision-making processes when evaluating CSR activities, future research can examine the impact of CSR decoupling and the moderating effect of stakeholder scrutiny in other contexts.

Supplemental Material

Supplemental Material - Walk your reputation: The impact of corporate social responsibility decoupling on the hospitality and tourism firm value in the time of crisis

Supplemental Material for Walk your reputation: The impact of corporate social responsibility decoupling on the hospitality and tourism firm value in the time of crisis by Kewen Wang, Yongqi Yu, Xin Wang and Haidong Zheng in Journal of Tourism Economics.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the National Natural Science Foundation of China (ID 71902093).

Supplemental Material

Supplemental material for this article is available online.

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.