Abstract

Public sector unions push for unmerited wage increases, exacerbating inflation and deficits. Despite this conventional wisdom, governments in several European countries successfully limited public sector wage growth during the 1980s and 1990s. This article argues that the recent rise in public sector wage inflation in the eurozone is an unintended consequence of the shift towards Economic and Monetary Union. I argue that monetary union’s predecessors, the European Monetary System and Maastricht, imposed an institutional constraint on governments, which enhanced their ability to impose moderation: national-level, inflation-averse central banks that could punish rent-seeking sectoral wage-setters via monetary contraction. Monetary union’s alteration of this constraint weakened governments’ capabilities to deny inflationary settlements.

Many have addressed the implications of the public sector’s sheltered status on unions’ wage strategies vis-à-vis the government. Because the public sector is a monopoly provider of necessary and price-inelastic services, conventional wisdom suggests that its unions push for unmerited wage increases, exacerbating inflation and fiscal deficits. The argument in this article challenges this conventional view, drawing upon the experience of countries that participated in the European Monetary System (EMS) and, later, Economic and Monetary Union (EMU). During the 1980s and the early and mid-1990s, differences in sectoral wage inflation (measured in terms of Blanchard’s wage efficiency units – real wage growth minus changes in labour productivity) between the public and manufacturing sectors were relatively low within the EMU10 (the original EMU12 excluding Greece and Luxembourg,

1

Figure 1).

2

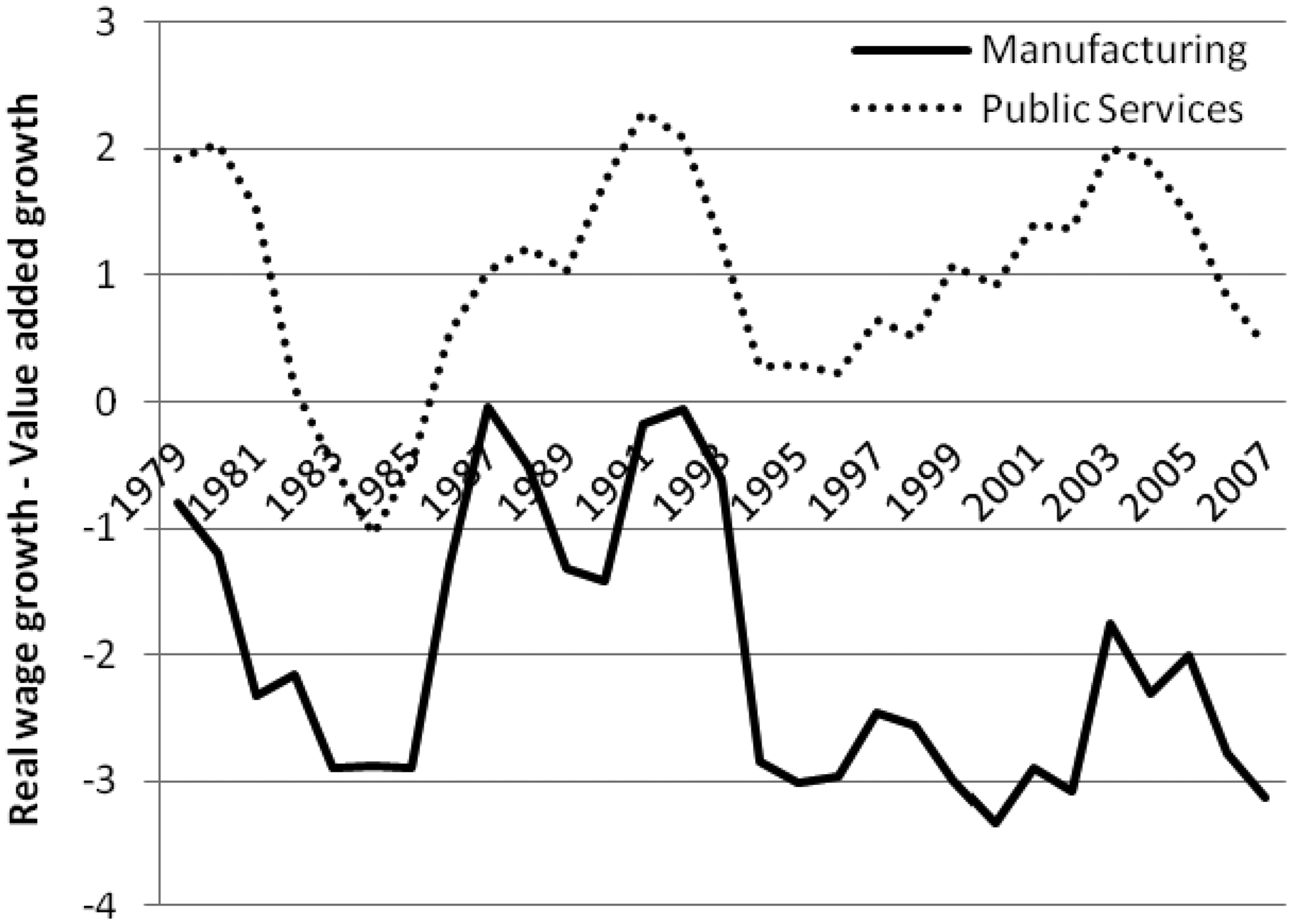

Only in the late 1990s and 2000s did sectoral wage inflation divergence arise.

Sectoral wage inflation, EMU10 (three-year moving average). Data source: EU KLEMS.

The introduction of EMU coincided with significant sectoral divergence within its member states. Were such developments linked or merely coincidental? This question merits exploration for two reasons. First, the lack of sectoral divergence prior to the late 1990s in EMU countries is puzzling in light of what has been said in the literature on sectoral interests. Much of the political debate that emerged in the 1990s focused predominantly on Sweden in the late 1970s and early 1980s, discussing the consequences of rent capture by public sector unions for centralization. The inclusion of the low-productivity public sector in centralized wage agreements placed an inflationary squeeze on the export sector, limiting what manufacturing employers could pay their (more productive) workers. In contrast to Sweden, various EMS governments imposed austerity measures to enforce pay freezes, or pay cuts, on the public sector during the 1980s, and all EMU10 governments limited public sector pay growth during the 1990s to qualify for Maastricht. Instances of public sector pay restraint even arose in countries such as Italy, Spain, and Portugal, countries that lacked the corporatist institutions deemed necessary to deliver wage moderation (Hassel, 2003). These experiences provide a sharp contrast to those witnessed in Sweden, which has emerged as a poster example of public sector militancy gone wrong.

Second, this divergence merits exploration because it suggests that EMU may have introduced an institutional arrangement that imposes lax constraints on governments to control rent-seeking public sector interests. Though EMU was predicted to be a constraining institutional regime via its removal of monetary and exchange rate policies, developments in public sector labour markets indicate that monetary union, compared with its institutional predecessors, has not provided sufficient penalties to governments for limiting public sector wage expansion. Encompassing trade union organizations dominated by public sector interests, as argued by Garrett and Way (1999), produce deleterious consequences for private sector interests. If not countered with deflation in other sectors, public wage expansion produces inflationary pressures that ultimately lead to a less competitive real exchange rate, which under monetary union is purely a function of relative national inflation, to the detriment of exposed sector interests. Ironically, the move to EMU has further exacerbated this effect by removing national-level institutions that previously offered governments leverage over public sector interests. In the current European debt crisis, public sector unions continue to drag their feet on public wage adjustment. Although such crises should provoke deterioration in the nominal exchange rate, via either depreciation or devaluation, providing some assistance to the export sector, a common currency precludes this option.

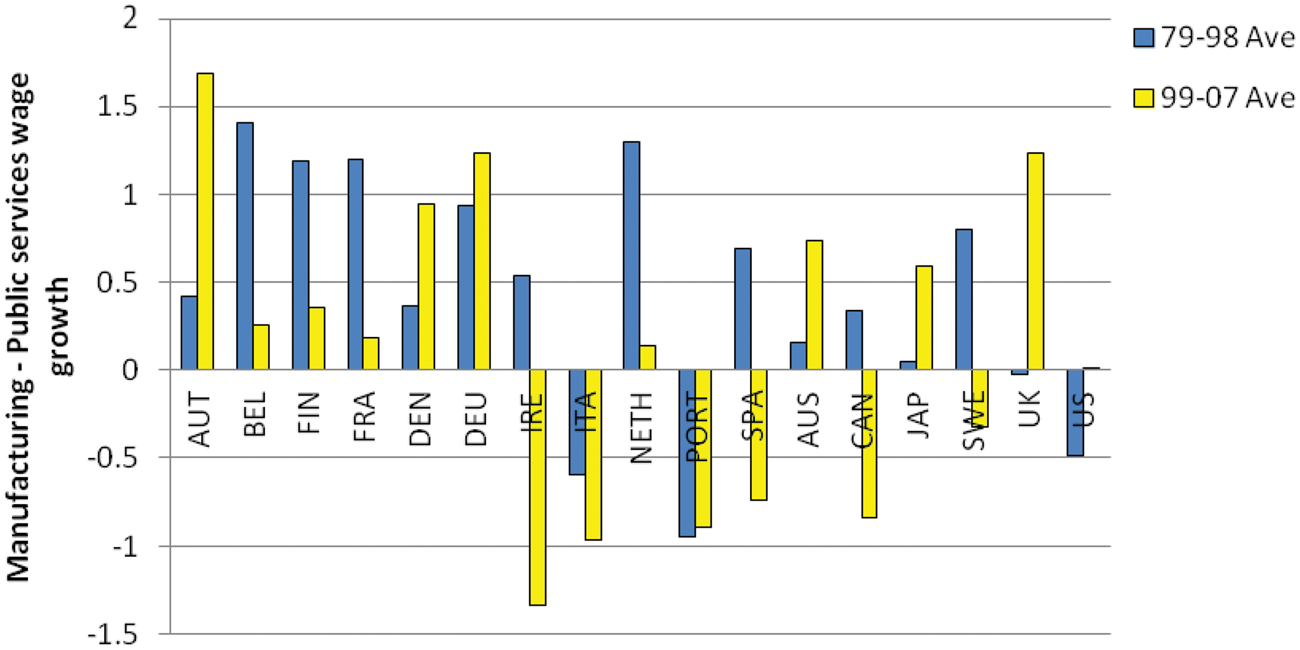

The institutional argument developed here, a theoretical and empirical expansion of that developed by Johnston and Hancké (2009), contrasts wage-bargaining dynamics under EMU with its institutional predecessors, the EMS’s Exchange Rate Mechanism (ERM, 1979–98) and the Maastricht Regime (1992–8). ERM and Maastricht imposed one important restriction upon governments that facilitated the enforcement of wage moderation: inflation-averse, national-level central banks. Under the EMS, countries pegged their currencies to the German Mark, shadowing the Bundesbank’s anti-inflationary stance. Because public sector wage-setters encompassed a significant portion of the labour force, their wage decisions, if inflationary, would provoke monetary tightening from inflation-averse central banks. Monetary tightening, although of relative insignificance to public sector unions with secure employment, had significant consequences for governments whose continued appeasement of public sector wage inflation could prolong contractionary pain. Once the commitment to a hard currency policy was made, public sector compliance was required to fulfil adjustment and, owing to its lower productivity, involved lower wage allowances compared with those granted in manufacturing (Figure 2). In 1992, Maastricht further reinforced this institutional constraint via stringent inflation and deficit criteria. Consequently, wage growth in public services, relative to the manufacturing sector, remained restrained.

Differences in sectoral wage growth. Data source: EU KLEMS.

Monetary union, however, altered the nature of this institutional constraint. Although the European Central Bank (ECB) was also non-accommodating, national public sector unions no longer carried a significant weight within its reaction function, as they had done for national central banks. Consequently, the monetary threat the ECB posed to governments was dampened. The Stability and Growth Pact (SGP) was meant to deter governments’ temptation to discontinue fiscal austerity, but its penalties for breaching the 3 percent limit failed to include Maastricht’s exclusionary threat. The absence of inflationary-reactive national central banks did not affect exposed sector employers because competitiveness pressures continued to constrain their wage strategies. Employers in the public sector, on the other hand, inherited a less constraining negotiation space with unions that had little to gain from wage moderation.

Monetary union, trade unions, and sectoral wage interests

Wage-setting behaviour under the conditions of monetary union received much attention, both before 1999 and after. Some argued that in EMU, with its asymmetric structure consisting of a centralized monetary policy and separate wage-bargaining systems, national wage-setters would no longer be constrained in their wage demands by inflation-averse monetary authorities. Once monetary policy was transferred to the ECB, national unions would pursue high wage increases (Hall and Franzese, 1998; Soskice and Iversen, 1998). EMU significantly reduced the size of individual wage-setters in relation to the central bank, moving national-level wage-setting towards a situation where national labour unions are strong enough to extract high wage increases yet small enough not to bear the full cost of inflation (Calmfors and Driffill, 1988).

These arguments were rooted in analysis of the impact of non-accommodating central banks on wage-setters’ decisions to control their wages. Scharpf (1991) advanced the notion that conservative/monetarist governments limit the wage decisions of self-interested unions. An accommodating government committed to the pursuit of full employment is fundamentally defenceless against uncooperative unions because it cannot respond to aggressive wage claims with contraction. However, once monetary non-accommodation is delegated to the central bank, wage moderation on behalf of unions ceases to be a concession and becomes a ‘self-interested union response’ (Scharpf, 1991: 172). If central banks are non-accommodating, enforcing an inflationary rule or shadowing a central bank that has one, the unemployment costs of inflationary wage settlements increase, prompting unions to exert greater restraint in their wage demands (Franzese, 2001; Hall, 1994; Iversen, 1998). Consequently, several anticipated that the removal of non-accommodating macroeconomic institutions from the national level would provoke wage inflation by unions (Hall and Franzese, 1998; Hancké and Soskice, 2003; Soskice and Iversen, 1998).

Although these arguments provide an explanation for increased wage moderation across EMU candidates prior to 1999, they fail to explain developments under monetary union. At the aggregate level, wage inflation did not increase after 1999 and, for the manufacturing sector, wage settlements remained below productivity developments. Literature on sectoral interests offers multiple reasons why sheltered sectors witness greater wage excess than exposed ones. The political economy stream of this literature focused on competition’s impact on employers’ price mark-up strategies (Crouch, 1990; Iversen, 1999). Wage inflation produces lower unemployment costs for public employees than for manufacturing employees because increased labour costs can be financed through taxes or deficit spending rather than employment shedding. Garrett and Way (1999) outlined that large public sector unions’ pursuit of rent capture has repercussions on the exposed sector and the economy at large.

In the economics stream of this literature, dominated by Baumol’s insights, sectoral divergence arises as a result of productivity differentials (Baumol and Bowen, 1965). Wages at the national level rise and fall together, yet sector productivity does not. Some sectors, such as services, experience static productivity growth while others, such as manufacturing, experience higher productivity growth. As a consequence of a wage equality ‘constraint’ across sectors, service sectors, where productivity cannot be easily enhanced given the labour intensity of production, are subject to a ‘cost disease’ that ultimately fuels inflation. 3 Amalgamating trade integration into a dual sectoral framework, Balassa (1964) and Samuelson (1964) suggested that increased trade integration exacerbates wage divergence between dynamic, exposed sectors and sluggish, sheltered sectors because competition further enhances productivity in exposed sectors.

Though one can question the accuracy of public sector productivity data, a similar EMU divergence pattern emerges when examining time effects of sectoral wage growth. Figure 2 presents average differences in manufacturing and public sector (hourly) wage growth (that is, not accounting for productivity) for 11 countries that participated in the EMS either directly or indirectly during the 1980s and 1990s, as well as for six non-participants (Australia, Canada, Japan, Sweden, the UK, and the USA), for two periods: the EMS/Maastricht period (1979–98) and the EMU period (1999–2007). Negative differences indicate that wage growth in public services exceeds that in manufacturing, whereas positive differences indicate the contrary. With the exception of Italy, a country that failed to adjust to the EMS’s hard currency policy until the 1990s, and Portugal, a 1992 entrant, annual wage growth in EMS public sectors remained consistently below that in manufacturing between 1979 and 1998, leading to the rise of significant wage gaps. In contrast, the majority of non-EMS countries witnessed either minimal differences in sectoral wage growth (Australia, Japan, and the UK) or negative differences in sectoral wage growth (USA) during this time. Sweden’s positive wage differentials can be explained by the manufacturing employers’ abandonment of centralized wage-bargaining in 1982, which enabled them to grant more lucrative wage settlements to address labour shortages (Pontusson and Swenson, 1996).

The majority of EMS countries that joined EMU (Austria and Germany excluded), however, witnessed a deterioration in manufacturing and public sector wage growth differentials between the 1979–98 and 1999–2007 periods. For four EMU countries (Belgium, Finland, France, and the Netherlands), manufacturing/public sector wage growth differentials remained slightly positive yet, relative to the EMS period, these difference had significantly declined. For Italy, negative sectoral wage growth differentials under EMS became more negative under EMU. In contrast to EMU member states, the majority of non-EMS/EMU countries (with the exception of Canada and Sweden) witnessed an improvement in manufacturing and public sector wage growth differences between the EMS/Maastricht and EMU periods. Considering Figures 1 and 2 simultaneously, EMU appears to have marked a wage shift where public sector unions were able to initiate catch-up with their manufacturing counterparts relative to the 1980s and 1990s; this catch-up effort, however, does not overwhelmingly reveal itself in non-EMU member states, where wage growth differentials disproportionately improved in favour of the manufacturing sector between the 1979–98 and 1999–2007 periods.

Other institutional theories fall short of explaining these wage developments. From a Varieties of Capitalism perspective, several coordinated market economies (Belgium and the Netherlands) witnessed reductions in wage differences between the EMS and EMU periods, whereas others (Germany and Austria) and several liberal market economies (Australia, the UK, and the USA) witnessed improvements. Bargaining institutions may account for Germany’s and Austria’s improvements in manufacturing and public sector wage differences after 1999 (both have trade-led pattern bargaining systems with limited bargaining rights for the public sector), yet they fail to explain why uncoordinated labour markets share similar trajectories. Aside from developments in Germany and Austria, there is some semblance of an EMU/non-EMU divide in wage dynamics before and after 1999. I argue that public sector pay restraint during the 1980s and 1990s in the EMS and the rise of public sector wage inflation under EMU can be understood if one contextualizes the institutional constraints that the EMS/Maastricht regimes placed on public employers and how EMU altered the nature of these constraints. The next section outlines the theoretical argument.

A theoretical explanation of sectoral divergence under monetary union

Assumptions and theoretical foundations

The discussion of the pre-EMU era as an institutional construct that facilitated public sector wage restraint begins with the assumption of a dual-sector economy consisting of an exposed sector and a public sector. Employers and unions in the exposed sector are presented with limited price mark-up abilities, given the presence of competition. Because competition increases the unemployment costs associated with wage increases, unions in the exposed sector have a greater (employment) incentive to exert wage moderation. Employers and unions in the public sector encounter minimal competition. They are (near) monopoly suppliers and, because public services are universally provided, their services are relatively immune from concepts of price elasticity, though higher spending on such services should impose higher tax burdens. Public sector unions have little incentive to restrain wages, employment-wise, because domestic demand for public services is relatively fixed.

It is important to emphasize that the bargaining game between employers and unions is located at the sectoral, not the national, level. It is assumed that sectoral wage-setters are large enough to affect national inflation, yet are not so encompassing that they would internalize their actions (Olson, 1982). This implies that the game’s underlying conditions place actors at the apex of the Calmfors–Driffill curve, which underlies the hump-shaped relationship between (national) union centralization and unemployment/inflation. The location of this apex, however, differs according to sector. Outlined by Danthine and Hunt (1994), the Calmfors–Driffill curve becomes flatter as competition/trade integration increases. Hence this apex should be lower for exposed sectors, because employers who are more limited in mark-up strategies will select employment shedding in response to rising labour costs, which should in turn prompt exposed sector unions to internalize their wage decisions.

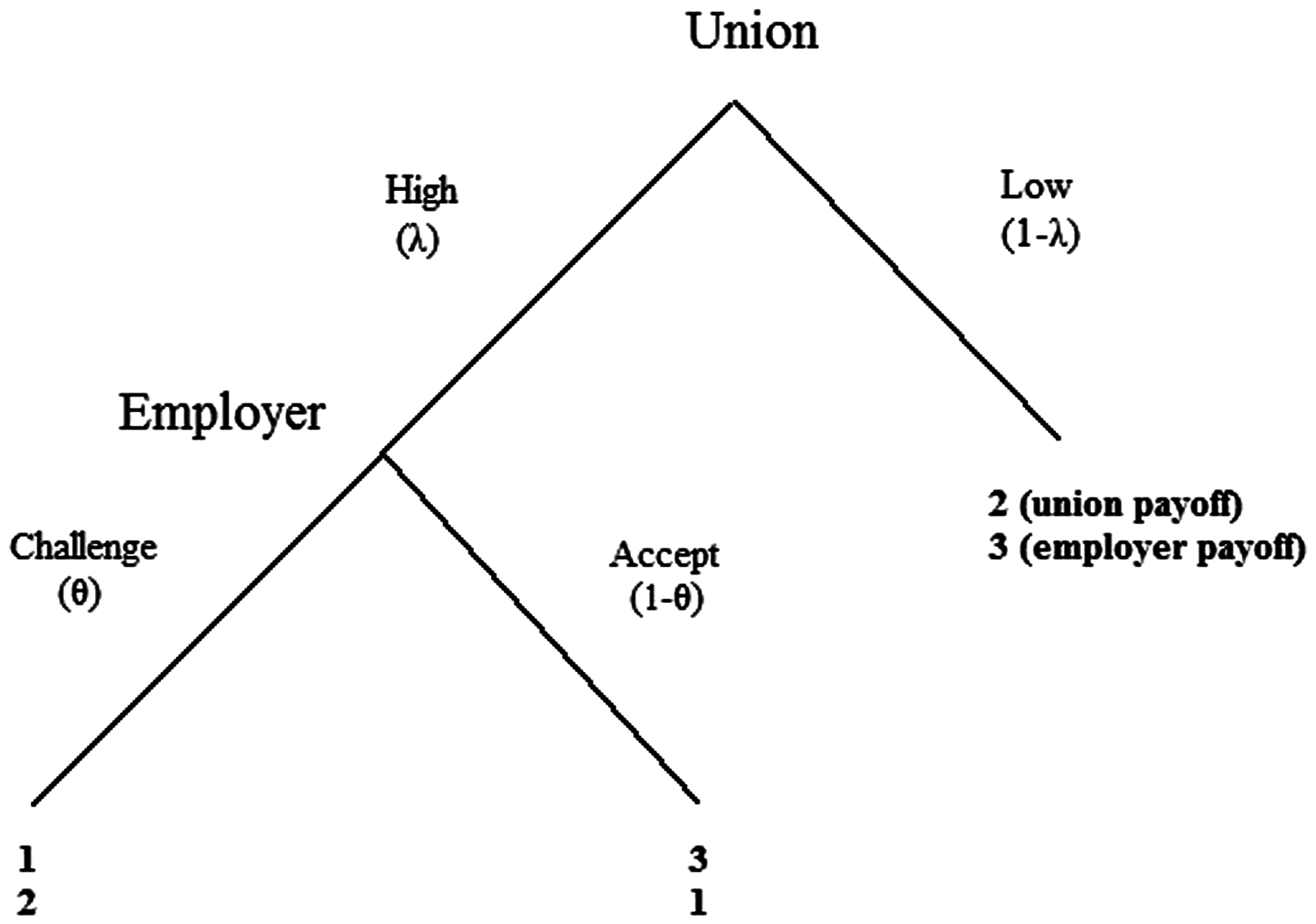

Beginning with a simple sequential bargaining game, unions propose either a high or a low wage settlement. High/low wage settlements are defined as those where the awarded nominal wage growth surpasses/falls behind the sum of productivity and inflation. If a low settlement is proposed (call this LOW), the employer accepts and the game ceases. If a high settlement is proposed, the employer can either challenge the union and impose a low wage settlement at the expense of industrial action (call this STRIKE LOW), or it can accept the proposal either as a consequence of the union’s success in an industrial dispute or in an attempt to pre-empt industrial action (call this (STRIKE) HIGH). Figure 3 provides a simple game tree with all possible equilibria. Regarding preference rankings, employers, regardless of sector, prefer LOW to STRIKE LOW, which is preferred to (STRIKE) HIGH. Likewise, unions, regardless of sector, prefer (STRIKE) HIGH to LOW, which is preferred to STRIKE LOW.

Sequential bargaining game between sectoral wage-setters.

The union’s strategy for proposing high versus low depends upon whether it is a ‘strong’ (probability of λ) or a ‘weak’ (probability of 1−λ) type. Likewise, the employer’s strategy for challenging or accepting high wage settlements depends upon whether it is a ‘strong’ (probability of θ) or a ‘weak’ type (probability of 1−θ). Both θ and λ are influenced by organizational strength and underlying economic conditions (that is, labour shortages/surpluses, exposure to competition, etc.). Much of the political literature concludes that public sector unions are in a stronger bargaining position than their private sector counterparts vis-à-vis employers; hence, in the public sector, the ratio of λ to θ should be larger than in the manufacturing sector, where competitiveness constraints endow employers with a higher value of θ. Accordingly, the resulting wage equilibrium for the public sector in Figure 3 should gravitate towards (STRIKE) HIGH, because employers’ payoffs are larger for lower values of θ (θ ≤ 1/3), whereas that for the manufacturing sector should gravitate towards LOW.

In repeated bargaining games, actors can establish reputations that alter the perceived values of θ and λ. Weak employers can establish a ‘strong-type’ reputation if they repeatedly deviate from their rational strategy of consent and challenge high settlements. Such behaviour yields lower payoffs in the short run, yet repeated deviation may fool unions that the employer is strong, convincing them to consent to moderation in the long run. In perturbed reputational games, players may find the short-term loss from imitating deviant strategies outweighed by long-term gains from spurring opponents’ doubts about their motivations. If public sector unions are unaware of a government’s type, a weak government, in resisting the temptation to inflate, can develop a reputation for being anti-inflationary, decreasing inflation expectations in the future (Backus and Driffill, 1985). Institutions play a crucial role in this situation if they introduce penalties for inflated wage settlements. Over time, employers can defer to institutions that expand θ, hence increasing their probability of being a strong type.

In the transition from a Keynesian regime, where governments accommodate inflation, towards a monetarist one, where they do not, rent capture from unions can trigger central banks to raise interest rates, dampening aggregate demand and ultimately increasing short-term unemployment (Cukierman and Lippi, 1999; Iversen, 1998). Although Iversen (1999) and Franzese (2001) argue explicitly that monetary tightening is of little concern to public sector unions that possess secure employment, both authors miss incentives on behalf of the state to avoid macroeconomic contraction. Governments care a great deal about unemployment developments in the private sector, given the implications for re-election. Governments can avoid the unemployment consequences associated with public sector inflation via tax financing. Such moves, however, introduce political repercussions if the private sector is forced to adjust to a monetarist regime. The political consequences associated with increased short-term unemployment and interest rates can induce governments to enforce moderation on unions, increasing θ and shifting the bargaining equilibrium towards that achieved within the manufacturing sector.

Institutions confining the state: The ERM and Maastricht

EMU’s institutional predecessors introduced a pivotal institution that facilitated governments’ deliverance of public sector wage moderation: national-level inflation-averse central banks whose reaction functions allotted a significant weight to sectoral wage-setters. The EMS sponsored inflation aversion amongst its member states’ monetary authorities, not through central bank independence but via participation in fixed exchange rate arrangements with the Bundesbank, which was highly anti-inflationary. The pursuit of a credible hard currency stance required the imposition of pay restraint on the public sector. Because the public sector constituted a significant share of the national labour force, inflationary wage settlements could have an impact on national inflation and consequently provoke monetary tightening from an inflation-averse bank. A monetarist regime imposed costs (higher interest rates and dampened aggregate demand) on inflationary (public sector) wage settlements, and consequently governments were pressed with higher penalties for consent. The potential for aggregate demand repercussions, in other words, prompted governments to change their bargaining stance; some did so earlier than others.

The Netherlands entered the ERM with a hard currency policy vis-à-vis Germany in place. Dutch private sector unions consented to wage adjustment under the 1982 Wassenaar Accord, but public sector adjustment required the unilateral imposition of pay austerity in 1983/4. Austria also initiated a (bilateral) hard currency policy with Germany in the late 1970s; public sector adjustment was internalized in the union movement because Austria’s monopoly union confederation, ÖGB, supported the peg to suppress shop-floor bargaining. Denmark announced its commitment to a hard currency policy in 1982; Schülter’s government intensified its obligation to austerity via public sector real wage cuts in 1984 and 1985. After a public sector wage freeze in 1982, an austerity programme in 1983, and a national incomes policy in 1986, France incurred its last (major) devaluation with the German Mark, around 6 percent, in 1986. Walsh (1999) claims that Italian monetary adjustment began in 1988, although Weber (1991) doubts whether Italy moved away from a soft currency stance during the 1980s. Spain and Portugal, which entered the EMS in 1989 and 1992 respectively, failed to make the required adjustments in the 1980s but succeeded in both endeavours during the 1990s.

One can question the endogeneity of non-accommodating central banks’ influence on public sector wage adjustment. (Rightist) business-friendly governments are more likely to impose such institutions if they are predisposed to public sector austerity. Although conversion to a hard currency policy was steered by right-of-centre coalitions for three of the ERM’s earlier converts (Belgium, Denmark, and the Netherlands), partisanship did not dictate adjustment in all EMS countries, or the lack of it in non-EMS countries. France’s Mitterrand and Austria’s Kreisky governments demonstrated that leftist governments could initiate the transition to a hard currency stance, while Thatcher battled British unions under an accommodating central bank. In countries where the conversion was initiated under right-of-centre governments, non-accommodating central banks remained ‘sticky’ once they left office; in Denmark, Rasmussen’s Social Democrats further institutionalized the Danish Central Bank’s hard currency commitment with a formal separation of powers arrangement in 1993.

The widening of the ERM’s exchange rate bands to ±15 percent in 1992 dampened the EMS’s hard currency conditions, yet the Maastricht inflation criterion further reinforced inflation-targeting. Some EMS member states (Denmark) maintained strict exchange rate targets after the crisis. Maastricht’s nominal criteria imposed two conditions that enhanced central bank non-accommodation. It introduced an explicit inflation target: inflation could be no more than 1.5 percentage points higher than that in the EMU’s top three performers. It also initiated banking legislation reforms that prompted several candidate countries to significantly enhance legal independence. Maastricht’s 3 percent deficit criterion provided an additional constraint for governments in public sector bargaining; 4 in addition to demand retraction repercussions for public sector wage inflation via an inflation-targeting central bank, Maastricht’s inflation and deficit criteria held a further political advantage for binding governments’ hands; penalties associated with reneging – EMU exclusion – were politically substantial. Countries with a history of public sector wage excess could not negotiate more lenient terms. If consolidation was not achieved, the country in question would be excluded from entry.

Central bank reaction functions and supranational institutional shift: Governments going it alone

The conversion to a non-accommodating monetary policy, via the ERM and Maastricht, enhanced public employers’ bargaining reputations by introducing institutional penalties for high public sector wage settlements. As public sector unions perceived these institutions as credible over time, the public sector bargaining equilibrium in EMS member states shifted from (STRIKE) HIGH to LOW. Monetary union was not intended to alter the EMS/Maastricht design, and its institutions, the ECB and SGP most notably, bore striking a resemblance to their predecessors. One important feature that the ECB lacked, however, was the incentive and capacity to react to sectoral wage-setters in member states with monetary contraction. Likewise, the SGP was blunted relative to its Maastricht predecessor, because exclusion penalties became obsolete once countries gained membership.

Unlike in a national framework, national public sector wage-setters, with the possible exception of those in larger member states (for example Germany), were not encompassing enough to influence EMU aggregate inflation. This altered the bargaining game between governments and public sector unions, because the credible value of θ decreased. Under EMS/Maastricht, public sector wage inflation prompted monetary retraction from national central banks, because these wage-setters constituted a significant proportion (20–33 percent) of the labour force. Under EMU, however, the weight of national public wage-setters, relative to the EMU labour force as a whole, declined substantially. For EMU’s small member states, public sector influence in the central bank’s reaction function, if measured as the proportion of these wage-setters to the relevant labour force, dropped from roughly 20–30 percent to less than 1 percent in the transition to the ECB. Public sector unions in EMU’s largest member state, Germany, witnessed a similar decline (from 25 percent to 8 percent), although they continued to carry some, albeit minor, weight in EMU wage inflation outcomes. Because public sector unions’ wage decisions no longer featured in the central bank’s reaction function, governments could no longer rely upon a credible threat of monetary tightening during pay negotiations.

Little changed for exposed sector wage-bargaining actors under monetary union. Competitiveness pressures, reinforced by a common currency, continued to limit employers’ mark-up abilities, leaving the ratio of bargaining power between manufacturing unions and employers relatively unchanged. Public employers, however, were deprived of a crucial institution that enabled them to enforce wage moderation. The ECB did not target national wage developments as had its nationally domiciled predecessors, and EMU entry rendered obsolete the political threat of exclusion for failing to meet the deficit/inflation criteria. EMU’s alteration of these institutions, which governments had relied upon to deliver wage moderation during the 1980s and 1990s, reduced the institutional penalties for public sector wage excess, altering the balance between λ and θ within public sector bargaining in favour of unions.

Empirical model

A cross-sectional time-series analysis is employed to test how EMU’s alteration of the economic penalties associated with public sector wage excess affected wage differentials between the public and manufacturing sectors after 1998. Although growth models of wages in efficiency units (WEU) have become increasingly popular, relative sectoral wage growth/inflation models are less common, owing to data availability issues with sectoral productivity. The EU KLEMS Database, the product of a major consortium of research and national statistics institutes across the European Union, has produced standardized sectoral-level data, including productivity data via growth accounting, for the EU25. The availability of this data set makes it possible to scrutinize the above theory in greater detail, because it provides rough measures of productivity growth differentials between sectors. It limits the selection of non-E(M)U countries for control purposes, however, because data on only five non-EU countries are available (Australia, Canada, Korea, Japan, and the United States).

Baccaro and Simoni (2010) employ a WEU growth model to test the influence of collective-bargaining institutions and their interaction with union governance on the delivery of national wage restraint. I depart from the authors’ model, and introduce two slight modifications. First, a sectoral model, rather than a national one, is used, in line with the theory above. Second, I modify the construction of the dependent variable, examining only wage growth differentials between sectors, and hence moving sectoral productivity differentials to the left-hand side. This is done to isolate the impact of EMU on wage dynamics alone, because my theoretical model assumes that EMU’s sectoral bargaining power shift operates through wages rather than productivity developments. EMU may alter sectoral productivity differences through trade integration’s enhancement of exposed sector productivity (the Balassa/Samuelson effect). Hence, including both wage growth and productivity growth on the right-hand side captures two wage inflation ‘effects’, one operating through wage-bargaining power (argued above) and one through productivity. The use of productivity differentials as a control on the left-hand side rectifies this problem. The estimated equation is as follows:

Measuring monetary threats and relevant controls

Influence of central bank non-accommodation on sectoral wage differences

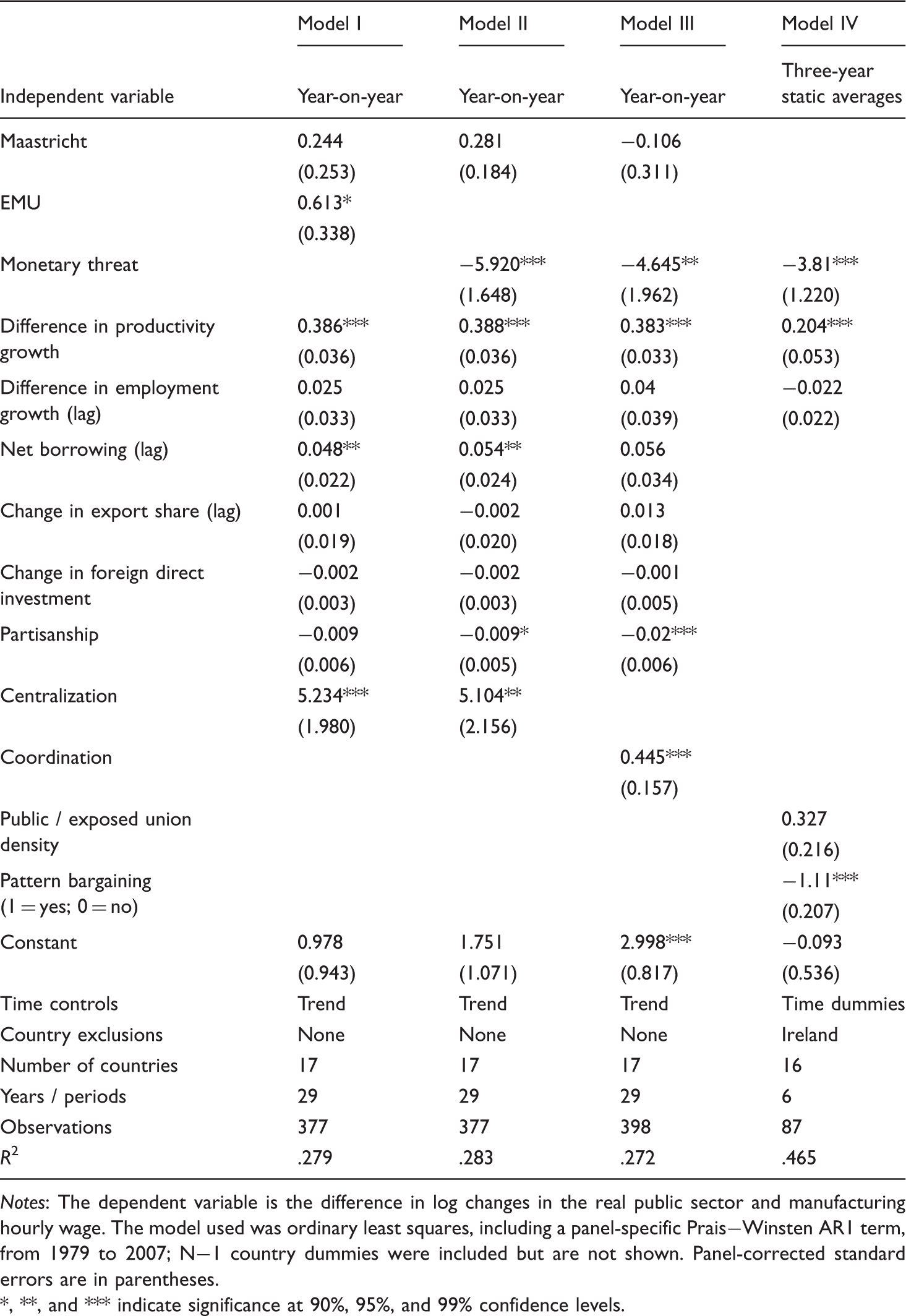

Notes: The dependent variable is the difference in log changes in the real public sector and manufacturing hourly wage. The model used was ordinary least squares, including a panel-specific Prais−Winsten AR1 term, from 1979 to 2007; N−1 country dummies were included but are not shown. Panel-corrected standard errors are in parentheses.

, **, and *** indicate significance at 90%, 95%, and 99% confidence levels.

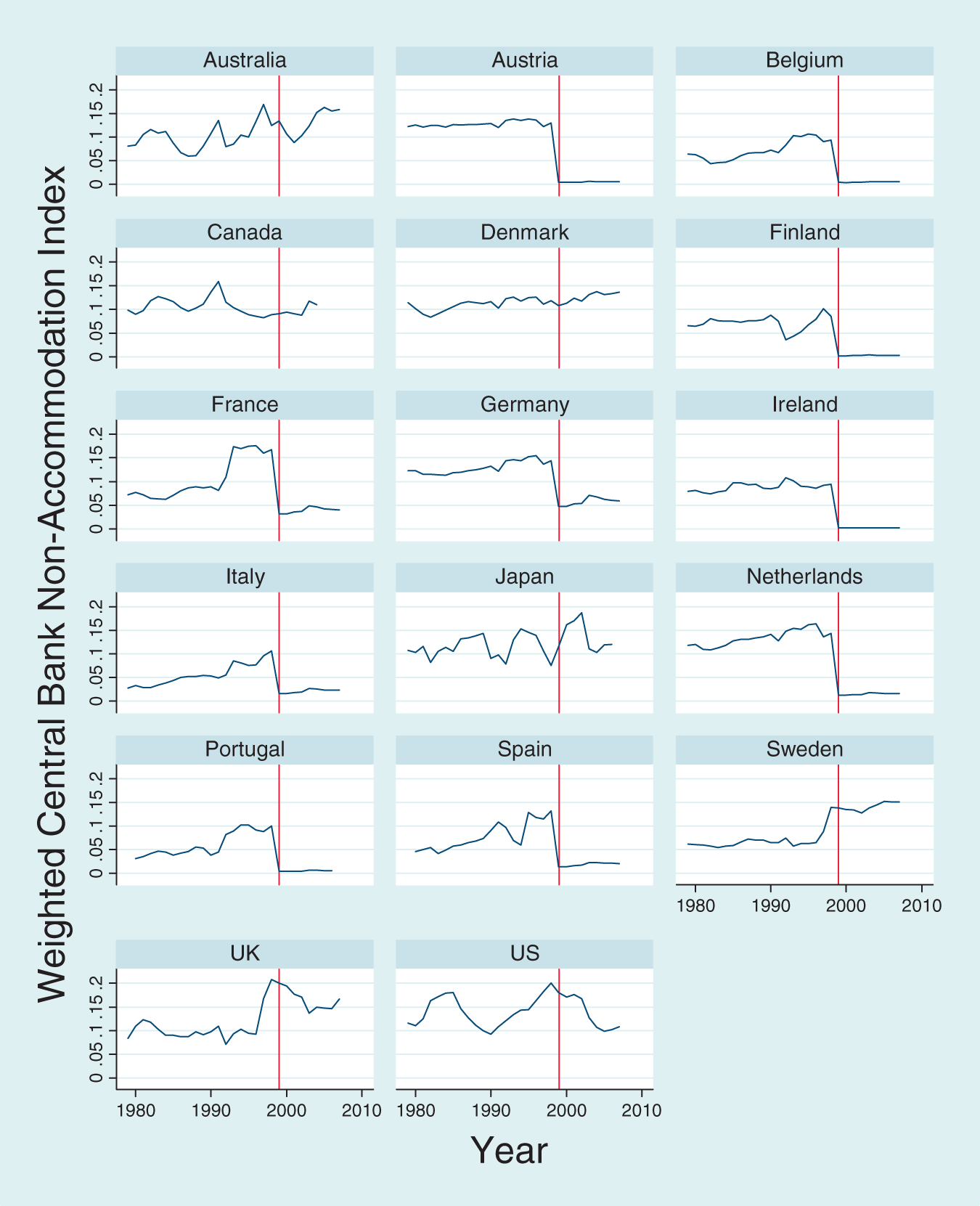

The measure for a monetary threat used here is constructed in an identical manner to Iversen’s index, with three modifications. First, four-year moving averages, rather than static averages, are used, maintaining a larger sample size. Second, the normalized nominal effective exchange rate is averaged with the Cukierman (1992) CBI index only, because his is the most detailed and up-to-date of the three that Iversen uses. Thirdly, in order to capture the EMU effect, the index is weighted according to the public sector employment share within an economy that the central bank targets. Weighting Iversen’s non-accommodation index in this manner produces a conditional monetary threat: non-accommodating central banks matter to governments only if their size is significant enough to generate a monetary response. 6 If central banks, such as the ECB, are non-accommodating but public sector unions have minimal weight in their reaction functions, governments will come under less pressure from a monetary authority to reduce wage growth.

For countries under EMU, the ECB’s (higher) non-accommodation index is weighted against national public sector employment relative to total employment within the EMU economy (see Figure 4). Weighting the non-accommodation index captures the feasibility of a monetary threat against public sector unions, because it accounts for their size in the relevant inflation aggregate. It also enables one to determine whether the EMU effect was heterogeneous according to country size. German public sector unions, for example, may continue to observe wage moderation under EMU, given that they constitute a more notable (albeit much smaller compared with the EMS) share of the central bank’s targeted labour force. A monetary threat should be less acute for governments in countries with smaller public sectors because these unions have a marginal weight in the bank’s reaction function. This is crucial to examining the impact of monetary union on wage developments, because EMU substantially decreased the weight of public sector unions in aggregate inflation developments.

Central bank monetary threat (weighted by public sector size).

Economic controls include differences in sectoral employment growth, net public lending, export share growth and growth in foreign direct investment (FDI). The lag of sectoral employment growth was included as a control, rather than its present value, in order to correct for endogeneity problems with the dependent variable – employment growth differentials too may be determined by wage growth differentials. A lag term of net public lending was used given endogeneity problems with the dependent variable. The beta coefficient on net public lending should be positive; past deficits (negative balances) should prompt governments to limit (present) public sector wage increases. Changes in the export share, also run on a lag to avoid endogeneity problems with manufacturing sector wage growth, were included as a proxy for international market exposure; positive export share growth should increase differences in public and manufacturing sector wage growth, given its dampening effect on the latter. The sign on the beta coefficient of FDI growth, a proxy for capital mobility, is ambiguous given that capital flight may produce similar wage-dampening effects on the public and manufacturing sectors. Growth in gross domestic product was specifically excluded given endogeneity problems with the dependent variable and multicollinearity problems with sectoral productivity differentials.

Institutional controls include bargaining centralization, wage coordination (assessed via two proxies: an aggregate measure and a pattern bargaining coordination dummy, a more specific measure of cross-sectoral coordination), partisanship, and sectoral union density. Given that centralization and wage coordination have been identified as promoting wage compression (Kahn, 1998; Wallerstein, 1999), the sign on both variables should be positive; public sector unions should secure higher wage growth relative to manufacturing in more centralized/coordinated regimes than in decentralized/uncoordinated regimes. Regressions were also run using a pattern bargaining coordination dummy because this method of cross-sectoral coordination, compared with uncoordinated and centrally coordinated bargaining, enhances exposed sector unions’ bargaining strength vis-à-vis the sheltered sector unions (Traxler and Brandl, 2010). Partisanship, measured as the proportion of legislative seats occupied by right-wing parties, should be negatively correlated with public sector wage growth and hence differences in public sector and manufacturing wage growth. Finally, sectoral union density, measured as the ratio of membership of the three largest public sector affiliates to the three largest exposed sector affiliates in a country’s largest union confederation, should be positively correlated with public and manufacturing wage growth differences. Because Traxler and Brandl’s (2010) sectoral organization and pattern bargaining data are provided over three-year average periods from 1985 to 2002, these regressions were run on three-year static average observations over 16 countries (data for Ireland are unavailable).

An ordinary least squares (OLS) regression method with panel-corrected standard errors (PCSE) was applied to test the baseline model above, which corrects for both country-specific heteroscedasticity and spatial correlation of errors (Beck and Katz, 1995). 7 A Wooldridge test for autocorrelation indicated the presence of serial correlation, 8 so all models included a panel-specific Prais–Winsten autoregressive transformation. 9 (N − 1) country dummies were included to control for country-specific omitted variables. Time dummies were omitted in the year-on-year regressions given clear multicollinearity problems with the Maastricht dummy and the weighted monetary threat variable. However, for the three-year static average regressions, the Maastricht dummy was excluded because the period averages spliced Maastricht with the EMU and pre-1992 periods; hence (n − 1) time-period dummies were used. A time trend was included to test whether the widening of public sector and manufacturing wage growth differentials occurred in all countries over time or was EMU-specific.

Results

Regression results are presented in Table 1. Column IV presents results from the three-year static average model; general economic controls were dropped in order to preserve the (smaller) sample, because several countries lacked FDI and deficit data until the mid-1990s.

Beginning with model I, the crude EMU dummy is significantly positive, suggesting that wage growth in EMU’s public sectors, relative to wage growth in manufacturing, was on average 0.6 percent higher per year than it was in non-EMU and non-Maastricht years; given the inclusion of the Maastricht dummy in model I, non-Maastricht and non-EMU years serve as the benchmark. This indicates that, over 10 years in monetary union, public and manufacturing wage differentials would widen by 6 percent within individual member states, relative to the era of national central banks outside of Maastricht. A Wald test of the Maastricht and EMU dummies indicated that the EMU coefficient was also significantly higher than that for the Maastricht dummy (χ2(1) = 6.73; p-value = .010).

The second measure of the EMU effect, the (weighted) monetary threat, also produced the expected results. Between 1979 and 1998, EMS participants witnessed sweeping increases in central bank non-accommodation. This was the result not only of the adherence of a currency peg to an anti-inflationary anchor currency, the German Mark, but also, for some peripheral economies, of the enhancement of legal CBI during the 1990s. The weight of public sector employment in national economies, on the other hand, was relatively stable during this period. Between 1979 and 1998, the weighted monetary threat increased by 0.063 in absolute terms, on average, for (current) EMU member states. Taking the results from models II and III into consideration, this implies that this enhanced monetary threat led to, on average, a 0.3–0.37 percent per year reduction in public and manufacturing wage growth differentials over the EMS period. Assuming a country made the hard currency transition to EMS in 1980, this indicates that public and manufacturing wage differentials would narrow by 5.7–7.0 percent by 1998.

The transition to EMU was more extreme. The average decrease in the weighted monetary threat in the transition to EMU, owing solely to the reduced weight of national public sector wage-setters in the ECB’s reaction function, was roughly 0.107 in absolute terms, ranging from a 0.095 decrease in Germany to a 0.13 decrease in the Netherlands. Using results from models II/III, such magnitudes of change imply that, in the EMU period, annual public wage growth increased by a magnitude of 0.64 percent/0.50 percent per annum vis-à-vis manufacturing wage growth, owing to the reduced weight of public sector bargaining actors in the ECB’s reaction function. Similar to the EMU dummy, this would amount to the rise of a 6.4 percent/5.0 percent differential in public and manufacturing wages after 10 years in EMU. These increases would have been subtler for larger countries (that is, Germany) although the predicted relative increase – 0.57 percent/0.44 percent per annum – is still considerable.

Economic controls yielded the expected significant results (differences in sectoral productivity growth and lagged net borrowing) or were insignificant (lagged sectoral employment growth, lagged export share, and FDI growth). Institutional controls also exhibited the expected results. Partisanship was negatively correlated with differences in public sector and manufacturing wage growth (although significant for only two models). Centralization and wage coordination were positively correlated with differences in public and manufacturing wage growth and retained significance in all models. The ratio of sectoral unionization was positively correlated with widening sectoral wage growth differences, as expected, yet its significance fell slightly below 90 percent (p-value of 0.129). The pattern bargaining dummy was significantly associated with reduced public sector wage growth, by over 1.1 percent, vis-à-vis the manufacturing sector; this may explain why Germany and Austria, the only two EMU countries with pattern bargaining systems, retained public sector wage moderation after 1999. The Maastricht dummy performed as expected vis-à-vis the EMU dummy, as indicated in the Wald test for model I, yet Maastricht sectoral wage growth differentials were not significantly different from those in non-Maastricht/EMU years. One explanation for the latter result could be the holistic nature of the constraint. The rush to qualify for Maastricht was a catalyst for national social pacts whose effectiveness at producing wage moderation in both the public and the private sectors was witnessed in countries that had previously lacked the corporatist institutions to produce tripartite deals (Hassel, 2003).

Conclusion

Despite being a project that was widely supported by private employers and candidate country governments (Sandholtz, 1993), EMU introduced an asymmetrical rift in bargaining constraints within national labour markets. Under the EMS and Maastricht, wage-setters in all sectors were constrained in rent-seeking behaviour. Private employers relied upon competitive constraints to limit rent-seeking opportunism, while governments utilized non-accommodating central banks and Maastricht’s threat of EMU exclusion to enhance their bargaining reputation. By reducing the influence of public sector wages in the central bank’s reaction function and attaching less severe political penalties to the inflation/deficit criteria, EMU altered the nature of these constraints, to the detriment of governments’ hold-out capabilities. Private employers in the exposed sector could continue to rely upon competitiveness constraints, which were further reinforced by a common currency, in bargaining negotiations. However, EMU indirectly penalized these employers by altering rent-seeking dynamics in public sector labour markets; EMU promoted a shift from a symmetrical bargaining arrangement, where wage-setters in the exposed and sheltered public sectors were constrained by national institutions, to an asymmetrical bargaining regime where one segment of the labour market continued to be constrained in its self-maximizing behaviour by competitiveness while another segment (the public sector) was less so.

Feedback effects of institutional change are not new. However, with the noteworthy exception of Thelen and Van Wijnbergen (2003), who discuss the implications of negative feedback effects of wage militancy on employer bargaining coverage, much talk of feedback effects within the institutional literature focuses on their tendency to promote institutional resilience (Pierson, 1996) rather than their capacity to yield institutional instability. This analysis demonstrates the severity of negative feedback effects on actors who promote institutional change. Though Frieden’s (1991) dissection of exchange rate policy preferences along sectoral lines teaches us important lessons about the role of preferences in instigating change towards fixed exchange rate regimes and monetary union, asymmetrical institutional design can lead to severe repercussions for these actors, forcing them to compensate for groups that find themselves unconstrained in their behaviour.

In countries where some level of public sector pay moderation was maintained, price competitiveness surged. Between 1999 and 2007, Germany and Austria witnessed the highest export share growth in EMU, thanks in part to the role of pattern bargaining and the lack of formal public sector bargaining rights in enhancing state bargaining power. For countries that lacked these national institutions, however, the manufacturing sector was forced to compensate via significant deflation in order to remain competitive (Ireland, Finland, and the Netherlands) or to accept competitive decline (Italy, Portugal, and, the most extreme case of fiscal excess, Greece). EMU’s corporatist countries were not exempt from rises in significant public sector wage excess. The Netherlands and Ireland witnessed a substantial rise in public sector wage growth in the early 2000s, yet both were able to rely upon traditional national tripartite arrangements to eventually redress these excesses by 2003. EMU’s southern countries, however, have proven less able to rely upon national bargaining institutions to keep the public sector in check. Their decline in wage competitiveness could be indicative of the consequences of removing institutional constraints and the absence of national substitutes. Rather than temporary austerity measures, EMU’s fiscal future may require a bridge between its (collective-bargaining) institutional haves and have-nots.

Footnotes

Acknowledgements

I thank David Andrews, Zsofi Barta, Colin Crouch, John Driffill, Richard Jackman, Costanza Rodriguez-d’Acri, Waltraud Schelkle, Marco Simoni, participants at the 18th International Council for European Studies Conference, the 2011 Pacific Northwest Political Science Association, the European Union Center of California’s 4th Annual Workshop on EU integration, and three anonymous reviewers for comments and feedback. I owe Bob Hancké a particular debt of gratitude for his consistent advice and feedback. Any errors are my sole responsibility.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.