Abstract

We examine the impact of signals regarding the Eurozone’s bail-out commitment on government bond spreads in the Eurozone’s periphery, analysing the effect of positive, negative and mixed statements and decisions by the EU, the ECB and Germany. We construct a dataset of relevant events, and estimate their effects using distributed lag models, providing a number of robustness checks. Our main argument is that investors react to statements from credible actors, but largely ignore statements from less-credible actors, awaiting actual decisions. Accordingly, positive statements from the ECB have clear effects, while those from Germany and the EU do not. Furthermore, ECB decisions appear to be anticipated and thus have no short-term effects, while we find clear effects of positive decisions by Germany and the EU.

Introduction

Europe’s sovereign debt crisis illustrates that bond investors have to assess not only whether they can trust national governments to remain solvent, but also whether they can expect external actors to provide necessary support when a country is no longer able to service its debt. However, existing studies on sovereign debt overwhelmingly focus on national sources of default risk and leave international factors aside (e.g. Bechtel, 2009; Bernhard and Leblang, 2006; Breen and McMenamin, 2013; Hatchondo and Martinez, 2010; Kolb, 2011; Mosley, 2003; Sattler, 2013).

After the disclosure of Greece’s actual public deficit in October 2009, the Eurozone witnessed a dramatic divergence in long-term government bond yields, with Germany on one side, and Greece, Ireland, Italy, Portugal and Spain (referred to as the GIIPS countries) on the other. We argue that national factors alone are insufficient to explain these spreads, as they are also shaped by markets’ beliefs regarding the probability of bail-outs and the extent of risk-sharing inside the Eurozone. A more complete model of sovereign bond yields for Eurozone members thus also has to include investors’ assessment of the probability that a country will be rescued in case of insolvency.

This study examines the effects of statements and decisions regarding financial support and different forms of risk-sharing within the Eurozone on the long-term government bond yields of the GIIPS. At the European level, our analysis includes the results of all major summits and meetings and relevant statements by European Union (EU) policy-makers as well as the European Central Bank (ECB)’s crisis-related measures and statements. We also examine the effects of statements and decisions by Germany -- by far the largest economy and creditor within the Eurozone. We argue that investors continuously update their trust in the commitment of Eurozone policy-makers to avoid sovereign defaults among its members.

This study makes a number of contributions vis-a-vis several strands of existing literature. As mentioned, the role of international factors in determining default risks has so far garnered limited academic interest (notable exceptions are Goldbach and Fahrholz, 2011; Smeets and Zimmermann, 2013). By analysing the effects of international factors on bond markets, we contribute both to the general literature on the relation between financial markets and politics (Bechtel, 2009; Bechtel and Schneider, 2010; Bernhard and Leblang, 2006; Breen and McMenamin, 2013; Sattler, 2013), and to the more specific literature on Europe’s sovereign debt crisis (Aizenman et al., 2013; Beetsma et al., 2013; Beirne and Fratzscher, 2013; Ghosh et al., 2013; De Haan et al., 2014; De Grauwe and Ji, 2012; Lane, 2012; McMenamin et al., 2015; Mohl and Sondermann, 2012). Our results generally confirm that statements and decisions about financial support for stressed economies do have significant effects on markets’ perceptions of default risk.

An additional contribution of this study is the construction of a new dataset, distinguishing between different types of signals and thus allowing a more nuanced and theoretically relevant analysis. The dataset includes all relevant decisions and statements by the EU, the ECB and Germany from 2009 until 2012. In contrast to related studies (Goldbach and Fahrholz, 2011; Smeets and Zimmermann, 2013), we distinguish between positive, negative and mixed statements and decisions, and our analysis demonstrates that this matters, as markets do indeed react differently to these types of signals.

The more detailed dataset also sets our analysis apart from a growing number of studies investigating the effects of crisis news on bond spreads (e.g. Beetsma et al., 2013; Büchel, 2013; Gade et al., 2013; Mink and de Haan, 2013; Mohl and Sondermann, 2012). In contrast to these studies that sort their data into general news categories, we argue that markets should react more strongly to statements by credible actors, whereas the statements of less-credible actors are seen as cheap talk. In line with these expectations, we find that the ECB, arguably the most credible actor in the Eurozone, was able to reassure markets with its statements while positive statements by Germany and the EU had no clear effects. Yet, when European and German policy makers reached positive decisions yields on GIIPS’ bonds did indeed fall.

Theory and hypotheses

It is commonly argued that bond yields respond to changes in the perceived probability of default. The other key drivers of yields are taxability and liquidity, which are less relevant for explaining short-term changes. We therefore assume that changes in bond spreads reflect changes in the issuers’ perceived risks of default (see the Online Appendix for a further discussion of this topic). The crucial question is thus how perceptions of default risks are formed and what influences these perceptions. While the national sources of default risks are already well understood, we argue that its international drivers have received limited attention.

In the vast economic literature on sovereign debt, there are two broad views on how to account for investors’ perceived probability of being repaid in full. The first and widely accepted view holds that a country’s solvency and thus the yields it has to pay is determined by a bundle of fundamental variables. Accordingly, a deterioration of the GIIPS’ fiscal positions and economic prospects raised investors’ perceived risk of default and led them to demand higher yields (Aizenman et al., 2013; Ghosh et al., 2013).

While proponents of the second view accept the importance of fundamental variables, they argue that there are multiple equilibria between investors’ perceived probability of default and underlying fundamentals (Beirne and Fratzscher, 2013; Lane, 2012). The surge in spreads within the Eurozone might therefore only be weakly related to fundamentals and rather be driven by self-fulfilling ‘movements of distrust’ (Corsetti and Dedola, 2011; De Grauwe and Ji, 2012). If markets lose trust in the sustainability of countries’ sovereign debt, the argument goes, they demand higher yields which, in turn, makes default more likely without any considerable shift in underlying fundamentals. De Grauwe and Ji (2013: 15) point out, for instance, that ‘a significant part of the surge in the spreads of the peripheral Eurozone countries during 2010--11 was disconnected from underlying increases in the debt to GDP ratios and fiscal space variables’.

While both of these views identify relevant explanations of perceived overall default risks, most existing studies neglect the role of international factors (e.g. De Haan et al., 2014). We argue that investors’ probability of being paid in full not only depends on whether a country remains solvent, but also on the probability of the Eurozone providing assistance in the case of insolvency. In keeping with the terminology of a few earlier studies (e.g. De Grauwe and Ji, 2013; Mosley, 2004), we further argue that investors’ subjective assessments of this probability can be seen as a degree of trust. We define trust as investors’ subjective probability ranging from 0 to 1, where 1 would indicate certainty that countries will be bailed out and 0 would indicate certainty that they will not be -- and that the no bail-out clause of the Maastricht treaty will be honoured. In other words, trust here relates to a subclass of investment risk in which an actor’s expected gains reflect uncertainty regarding the bail-out commitment of the Eurozone.

We assume that the more skeptical investors are about the solvency of governments, the more important their degree of trust in the Eurozone’s bail-out commitment becomes. In line with previous studies showing that financial market reactions are not constant over time (for an overview see De Haan et al., 2014), we expect the effect of bail-out commitments to be strongest in times of crisis where markets question a government’s ability and willingness to service its liabilities on its own. This insight is particularly relevant for the Eurozone’s periphery: as markets have gradually lost confidence in national governments, they have looked to the Eurozone’s key policy-makers for reassurance. Accordingly, spreads on the GIIPS’s ten-year bonds should be strongly dependent on signals regarding the Eurozone’s commitment to avoid default among its members.

Taking the efficient market hypothesis as our theoretical point of departure (Fama, 1991), we assume that bond yields reflect all relevant and publicly available information. Put differently, markets should only react to information that is credible and not already priced in. Conversely, information that is anticipated or deemed non-credible should not systematically influence bond yields (e.g. Bechtel and Schneider, 2010; Bernhard and Leblang, 2006; Schneider et al., 2009). We therefore expect that new and credible information regarding the extent of risk-sharing inside the Eurozone influences investors’ level of trust, which, in turn, shapes their overall assessment of the probability of being repaid in full, and thus ultimately the yields they demand on government bonds. In other words, investors update their level of trust in light of statements and decisions that contain unanticipated and reliable information about the Eurozone’s bail-out commitment.

To examine this empirically, we look at relevant statements and decisions by three actors: at the European level, we focus on the collective decisions and statements by the European Council, the Economic and Financial Affairs Council (ECOFIN) and the Euro-group, as well as the ECB, and analyse their effects on GIIPS’ spreads. 1 This includes the results of all major Eurozone summits and meetings, all standard and non-standard policy measures by the ECB, as well as all relevant statements by the EU and ECB policy-makers between 2009 and 2012. With regard to the influence of specific countries, we limit our analysis to Germany -- the largest economy and creditor in the Eurozone. Here, we investigate the effects of relevant statements and decisions by the Bundestag and major policy-makers such as Chancellor Merkel, Finance Minister Schäuble and the heads of the ruling coalition parties.

We further distinguish between positive, negative and mixed statements and decisions. Positive statements and decisions generally reflect the EU’s, Germany’s or the ECB’s willingness to save the Euro, to provide financial support to the GIIPS and to avoid debt restructuring, defaults or the exit of countries from the Economic and Monetary Union (EMU). More specifically, the following measures and proposals fall under this category. First, statements and decisions to bail-out troubled Eurozone economies, to set-up or increase the European Financial Stability Facility (EFSF) or the ESM (European Stability Mechanism), to mutualize debt in the form of Eurobonds or to set up a common deposit insurance scheme for Eurozone banks (Corsetti et al., 2013). Second, the ECB’s Security Markets Program (SMP), and Outright Monetary Transactions (OMT), as well as its Long Term Re-Financing Operations (LTRO) also fall in the positive category. The SMP and OMT programs can be interpreted as attempts to reassure markets that temporarily illiquid governments will not be forced to default on their debt. Negative statements, in contrast, reflect actors’ reluctance towards all these points and their acceptance of debt restructuring, defaults or the exit of countries from the EMU. Lastly, mixed statements and decisions are ambivalent in that they allude to both positive and negative elements. Employing these categories, our baseline hypothesis is as follows. H1: Positive statements and decisions lower the spreads between GIIPS bonds and German bonds, while negative statements and decisions increase them.

The effects of mixed signals are naturally more ambiguous as they depend on the balance between positive and negative elements. If these elements cancel each other out, mixed signals should not change investors’ level of trust. If, however, either positive or negative elements dominate, mixed statements and decisions could have either positive or negative effects. Still, we would expect that these effects are smaller than those of signals with clearer contents. Based on these considerations, we derive the following hypothesis. H2: Mixed signals have weaker effects than clear positive or negative ones.

Within the Eurozone, we argue that the ECB’s decisions are easier to predict than those of Germany and the EU. It not only has the weakest incentives to engage in cheap talk, but also has the greatest capacity to bail-out weak economies and to guarantee financial stability inside the EMU. In contrast, elected officials both in Germany and at the European level are caught between the demands of their domestic audiences and those of the bond markets. Their aim is not only to reassure the markets but also to assuage their constituents’ skepticism towards bail-outs. The tension between these two goals creates an incentive to conceal their true preferences with regard to the relative importance of their goals and to engage in threats and bluffs (Bechtel and Schneider, 2010: 210). As a result, statements by the ECB are expected to have greater effects than those of German and European policy-makers. We thus derive the following hypothesis. H3: For the ECB, the effect of statements is larger than that of decisions, while for Germany and the EU, decisions have larger effects than statements.

Data on statements and decisions

To test our hypotheses, we examine the period from 1 January 2009, until 31 December 2012. This includes a period of relative tranquility on European bond markets lasting until the revelation of new budgetary figures by Greece’s government in October 2009 and the resulting periods of extreme volatility.

For the period in question, we have used several different sources to construct a dataset of statements and decisions by Germany, the ECB as well as the European Council, ECOFIN and the Eurogroup. Following Beetsma et al. (2013), our main source is a daily newsflash provided by the web site Eurointelligence (2014). Eurointelligence is a specialist, internet-based service that covers the most important daily political, economic and financial events within the Eurozone. It does so by combining its own reporting on EMU with an extensive coverage of Eurozone related news in both international and national information sources. It does not only contain the most important news from Brussels and Frankfurt, but also extensively covers German decisions and statements. We chose Eurointelligence as our main data source as it arguably provides a more balanced and complete account of daily, Eurozone related statements and decisions than any single national newspaper or press agency. 2

Our second main data source, complementing Eurointelligence, is the comprehensive online chronology of the Euro-crisis compiled by the European Commission (2014). This web page contains all relevant decisions and statements by Eurozone institutions and policymakers over our sample period. We primarily used it to code decisions by the European Council, the ECOFIN and the Euro-group as well as to crosscheck and verify the completeness and accuracy of statements and decisions obtained from Eurointelligence. Lastly, we complemented the above sources with a list of crisis related events provided by Smeets and Zimmermann (2013), an online Euro-crisis timeline by the think tank Bruegel (2014), and the documentation service of the German parliament (German Bundestag, 2014).

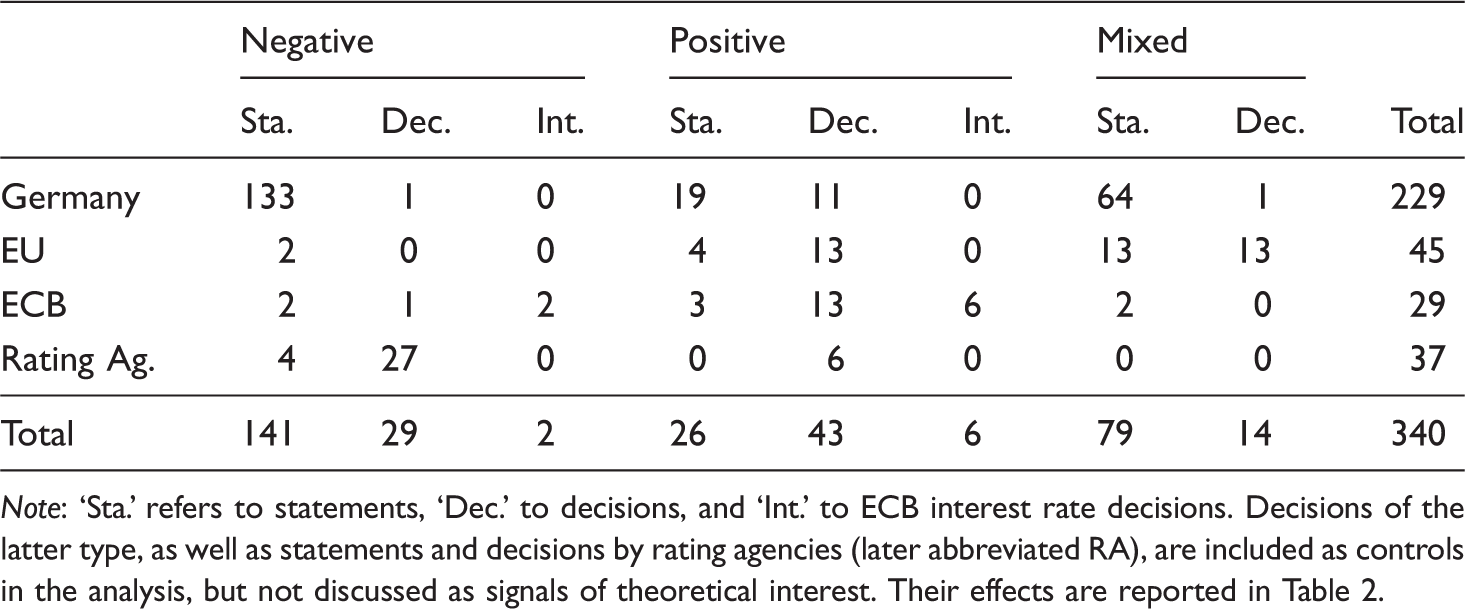

Frequencies of events in the dataset by event type.

Note: ‘Sta.’ refers to statements, ‘Dec.’ to decisions, and ‘Int.’ to ECB interest rate decisions. Decisions of the latter type, as well as statements and decisions by rating agencies (later abbreviated RA), are included as controls in the analysis, but not discussed as signals of theoretical interest. Their effects are reported in Table 2.

A few points are worth noting about the distribution shown in Table 1. First, it is clear that the EU rarely makes purely negative decisions or statements. In the data, there are only two negative statements, and no purely negative decisions. The EU’s decisions are split 50/50 between positive and mixed ones (13 of each), while its statements are mostly mixed (13 versus 4 positive and 2 negative). This seems to suggest that when the EU makes a decision with negative implications, it still attempts to mix it with positive elements to reassure the market. The ECB, on the other hand, almost exclusively makes positive decisions, while making a few statements that are fairly evenly split between negative, positive and mixed. It is also worth noting that Germany by far is the most active sender, accounting for two thirds of the signals in our data. Most of these signals are statements, and over half of these 229 statements come from either Chancellor Merkel or Finance Minister Schäuble. The rest generally falls on other members of the coalition government and high party officials. Most of these statements are negative (61%) or mixed (30%), while German decisions tend to be positive (85%).

Method

As our goal is to identify the impact of certain events on asset prices, our analysis could loosely be classified as an event study (e.g. MacKinlay, 1997), although it would not be a typical example of this approach. As explained above, we are interested how the statements and decisions in our dataset influence bond spreads. We use the rates on German 10-year bonds to measure general market movement in normal returns, and define spreads from the German rates as abnormal rates of return. 3 According to our argument, these abnormal rates of return on long-term government debt by the GIIPS countries will be inversely related to investors’ confidence in receiving all future cash flows in full and on time. The lower the perceived overall risk of default, the lower the spreads from German bonds, and as explained above, this overall risk is partly a function of the perceived likelihood of a country receiving international help in the case of need. 4

Before specifying our model, we make some final adjustments to the data. First, as events can only be expected to have effects on trading days, we move events that take place on non-trading days to the first subsequent trading day. This applies to 13 of our 340 events, eight of which are moved one day, while 5 are moved two days. Consistent with this approach, we treat the dependent variable as continuous over time, ignoring days on which market positions are fixed. Second, as daily bond rates essentially contain the last trading day’s value plus the current day’s innovation, we must expect the data to be integrated of the first order, I(1). Such data are non-stationary, i.e. lacking certain time-invariant statistical properties, making them unfit for statistical analysis, unless they are co-integrated with other covariates in the model. In this case, we do not expect co-integration, and we therefore calculate first-differences of the data (daily changes) to achieve stationarity. However, to also reduce the challenge of autoregressive heteroskedasticity, we take the natural logarithm of the spreads before differencing. In other words, we log-difference the data to get our dependent variable. 5

Our study has a few additional features that set it apart from most event studies. First, our theoretical motivation leads us to examine many different kinds of events, rather than a single type. Furthermore, we have a large number of events, some of which inevitably occur within the same short time frames. Of our 340 registered events, 56 take place on the same day as one other, and nine take place on the same as two other events. 6 Furthermore, as our data provide a fairly exhaustive list of the most important European-level events expected to matter for crisis-country bond rates, it also provides key events that need to be controlled for in the estimation of a given event type’s effect (but note that we also control for national events in the robustness section). The effects should thus be estimated jointly, in a single model for all event types. In contrast to event studies that select subsets of data within windows around the events, we therefore retain the original time series format of our dependent variable.

Nevertheless, the notion of event windows within which impacts are examined remains important. We need to determine how the effects of specific events are to be modelled. As a preliminary step, we examine the effects of isolated events, which we define as those that have no other events taking place within a window of 12 trading days surrounding them [−5, 6]. We further leave aside what we have coded as weak statements, which leaves us with eight isolated events. Figure 1 shows the average absolute change in the log-differenced spreads over time for these eight events. The plot suggests that the effects largely appear on the same day as the events, although a considerable part also appears on the next day. As the large number of signals in the data calls for rather short windows, we will therefore initially focus on a two-day [0, 1] window, as shown in dark grey in the figure. However, as a robustness check, we also report models expanding the window one day in each direction (i.e. [−1, 1] and [0, 2]).

Average impact of isolated events over time. Note: Isolated events are defined as signals with no other registered events within the window [−5, 6], i.e. starting five trading days before and ending six trading days after the signal in question (N of events = 8, N of outcomes = 40 per day, N of total observations over six days = 240). The shaded areas represent the three different windows captured by the DL models reported below, i.e. [−1, 1], [0, 1], and [0, 2].

Expanding the event window in this way will help capturing short-term anticipation or delayed reactions. In contrast, long-term anticipation would pose a harder challenge: if markets perfectly anticipate events far in advance, there would be no clear short-term effects at all. However, as Bechtel and Schneider (2010) note, there is considerable uncertainty surrounding European policy-making, rendering the outcomes very hard to predict. Furthermore, if markets do anticipate some outcomes, this would lead to an underestimation of their actual effects, providing conservative estimates. In other words, finding short-term effects in an analysis of this kind suggests the events in question were not fully anticipated.

Full results for the AR(2)DL panel model.

Note:

As we analyse all five GIIPS countries, we treat the data as panel data. This increases the statistical power of our tests, which is particularly useful for rare event types. The log-differencing of the spreads makes the series highly comparable in terms of relevant statistical properties, such as means and variances. As we might expect given the differencing, both a Hausman test and an F-test of inconsistency between the ‘within’ estimator (with country-fixed effects) and a pooled model confirm that the intercepts do not vary between countries (p > 0.9). We therefore report a model of the latter kind (although the other alternative would yield virtually identical results). To further validate the panel model, we also report results from country-specific models in the results and robustness section.

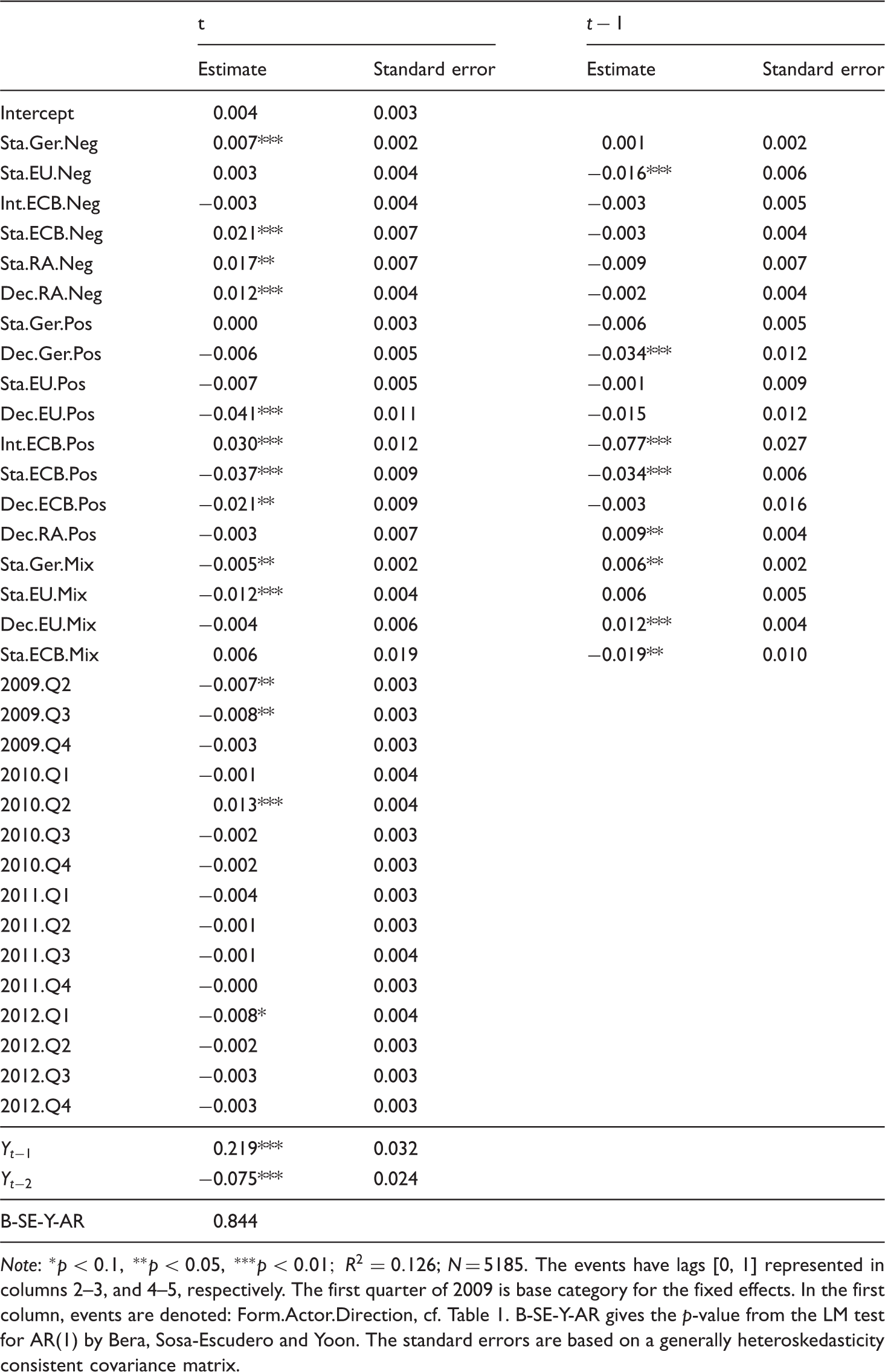

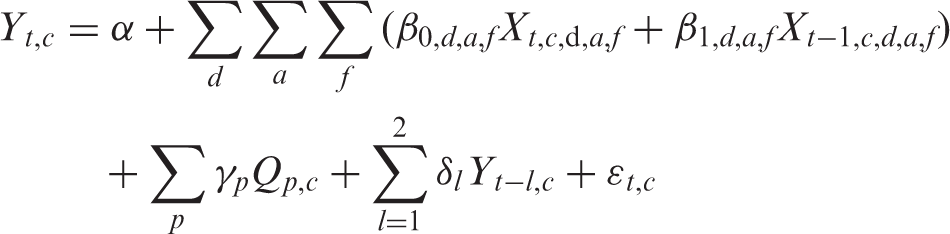

Specifying our initial model, we include a one-day lagged event-matrix (

However, even with two lags of the dependent variable, significant autoregressive conditional heteroskedasticity (ARCH) remains (Engle, 1982). It is worth noting that in the presence of non-spherical errors (i.e. autocorrelation or heteroskedasticity), the ordinary least squares (OLS) estimator is still the best linear unbiased estimator (BLUE), assuming the model is otherwise appropriate (see Kennedy, 2008). If the model represents a reasonable approximation to the observed patterns, heteroskedasticity would only undermine the standard errors. We thus initially report an AR(2)DL model, using a heteroskedasticity consistent (HC) variance–covariance matrix, robust both to heteroskedasticity between the series as well as ARCH (see White, 1980). However, while OLS is still BLUE in the case of non-spherical errors, such errors may signal a misspecification that would bias the estimates (King and Roberts, 2014). Furthermore, GARCH estimators may offer notable efficiency gains in the presence of ARCH (Bollerslev, 1986). Thus, to assess whether GARCH models would produce different results, we report country-specific ARDL-GARCH(1,1) estimates together with the country-specific ARDL results in the results and robustness section.

Formally, the initial AR(2)DL panel model with the [0,1]-window can be expressed as

Results and robustness

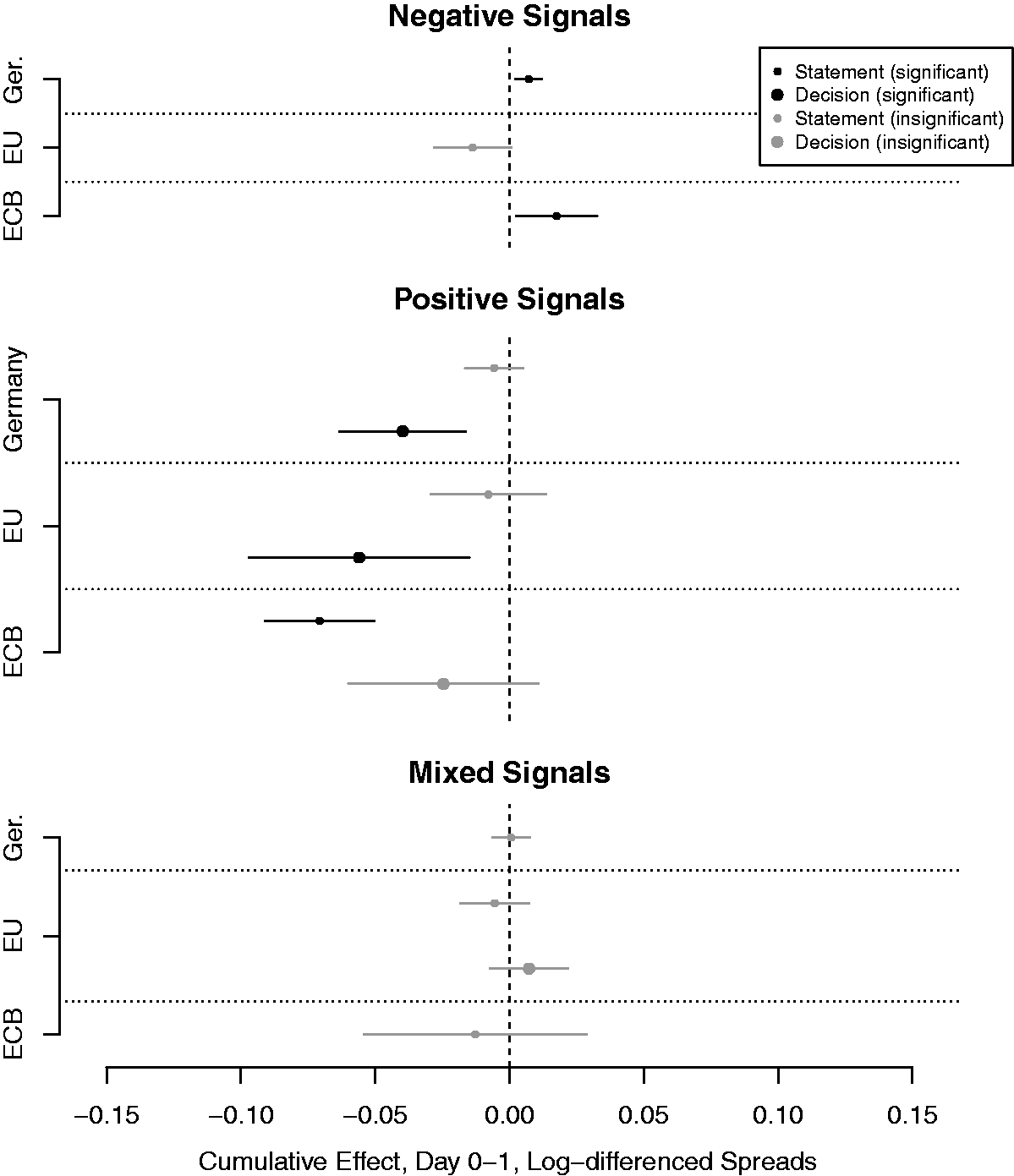

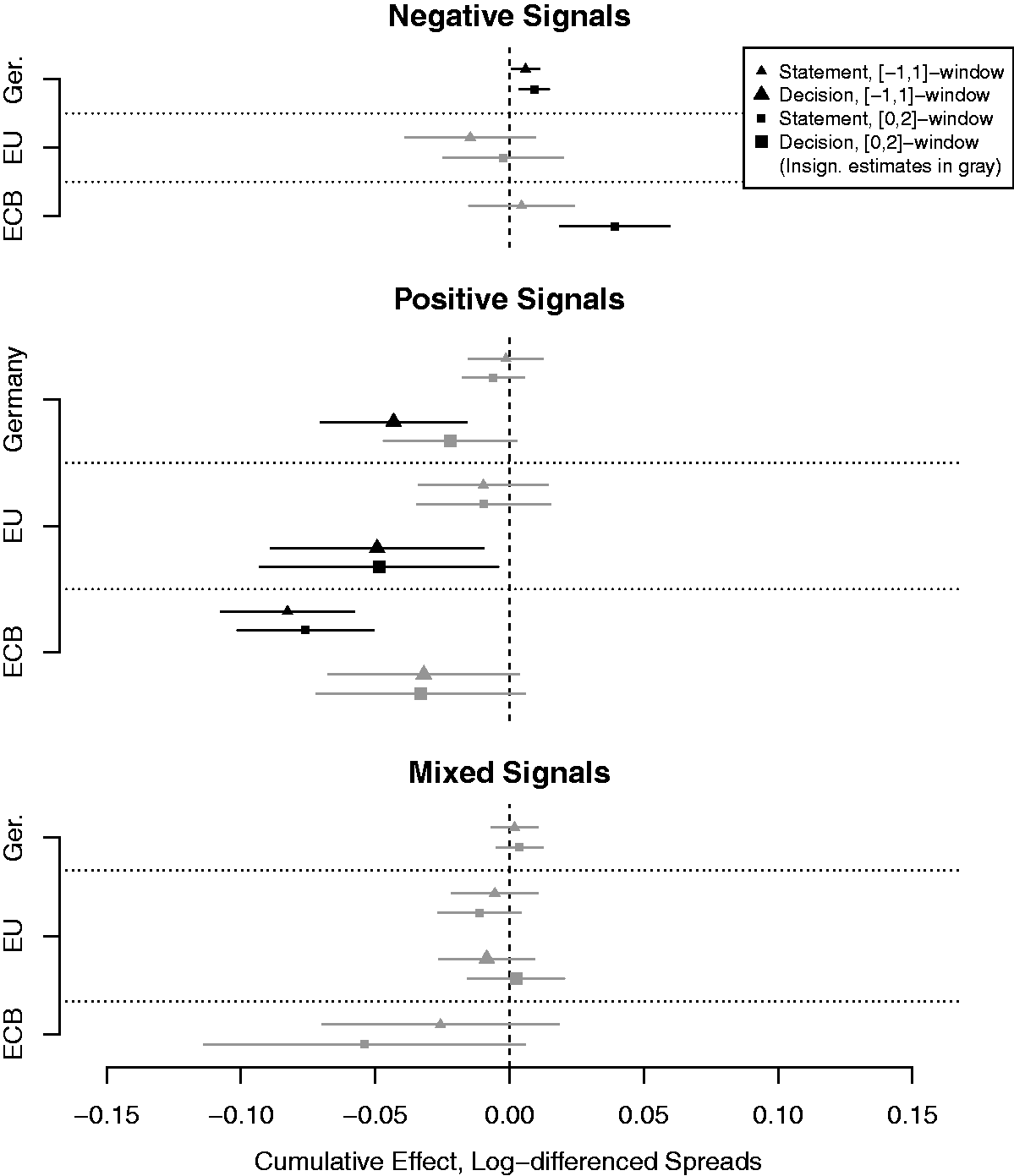

The key results of our main analysis are shown in Figure 2, while the full set of estimates is shown in Table 2. The figure reports cumulative effects over the [0, 1] window in question ( Estimated average effects across the GIIPS countries. Note: The reported effects are calculated as

With regard to positive signals, hypothesis 1 receives reasonably strong support. All estimates are in the expected direction, reducing spreads, and three out of six are clearly significant. More importantly, the results are perfectly consistent with a combination of hypotheses 3 and 1. Hypothesis 3 holds that among signals from Germany and the EU, decisions should have the greatest impact, while ECB statements should be more important than decisions, as the ECB will generally act in accordance with its statements enabling investors to anticipate its future policies. Thus, for the types of signals expected to matter the most for each actor, hypothesis 1 holds: Positive decisions by the EU and Germany have significant effects, while their statements do not. In contrast, ECB statements have significant effects, while ECB decisions do not.

Our results thus show that German and EU policy-makers were able to reassure markets when they sent clear and strong signals in the form of decisions. With regard to Germany and the EU, actions mattered more than words. While these results are partly in line with other studies (e.g. Mohl and Sondermann, 2012), they underline the importance of distinguishing between what policy-makers say and what they actually do. The finding that ECB statements matter more than ECB decisions is also consistent with the argument above regarding the differences between the ECB and the other actors. Although it should be noted that our coding strategy mainly captures the strongest and most important ECB statements, these statements from the ECB appear to enjoy far greater credibility than those of other actors. Our results thus concur with more policy-orientated studies on the Euro crisis, showing that the ECB was able to reassure markets by what is now commonly known as forward guidance. Markets seem to have believed that the ECB would honour its commitment to save the Euro.

Hypothesis 2, which holds that effects should be weaker for mixed results, also appears to hold, as no mixed signal is found to have a significant effect, while several types of positive and negative signals do. This underlines the importance of distinguishing between clearly positive or negative signals, and more ambivalent ones. Eurozone crisis meetings that produced mixed results had no significant effects on spreads. This result is all the more important as many of the most important attempts by the EU to reassure markets fall under this category. More generally, the results presented above confirm the overall argument of this study that European politics plays an important role for investors’ assessments of default risks.

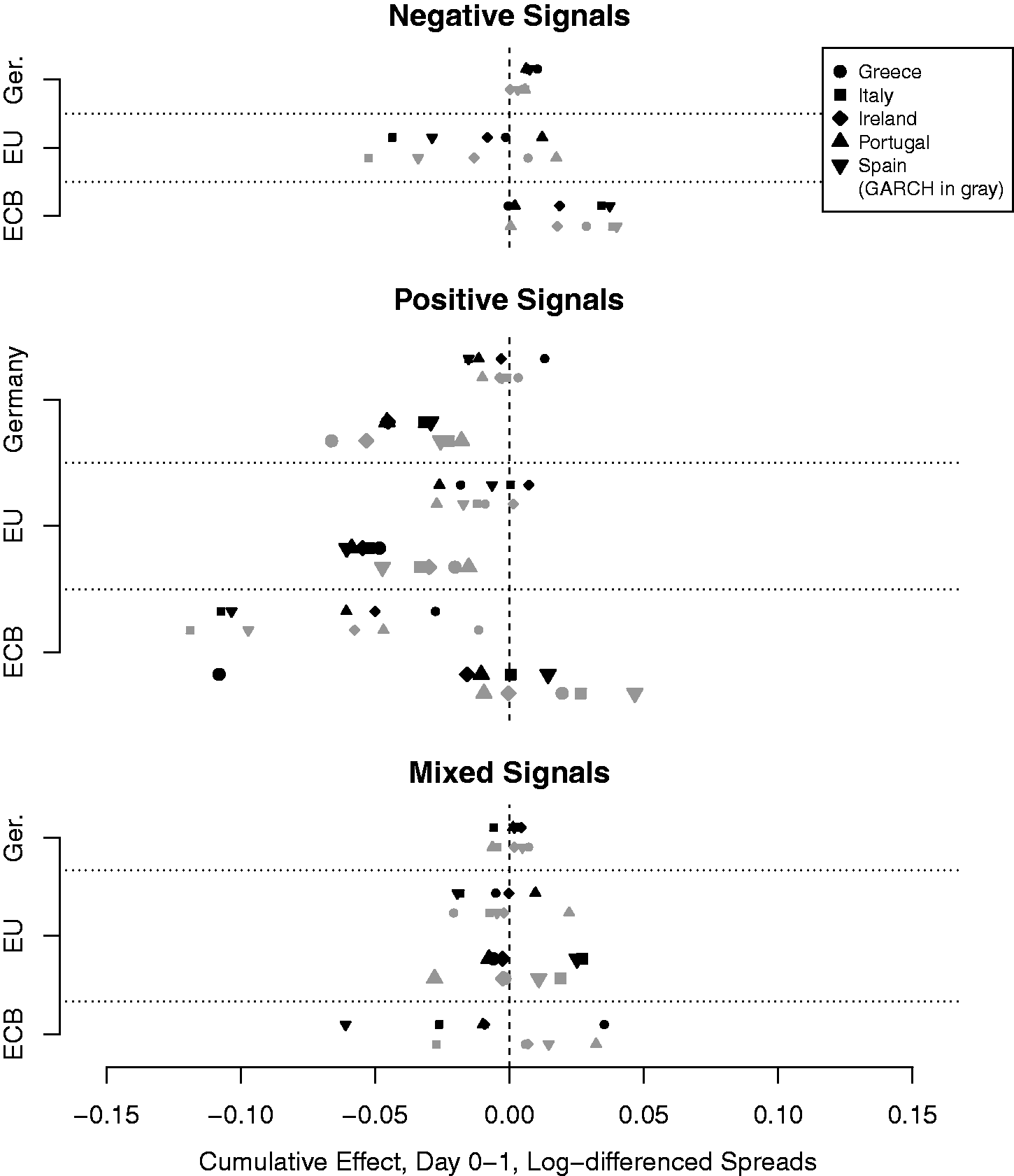

Having presented the results of our main model, we now turn to a set of robustness checks. First, while our diagnostic tests suggest the countries in question are sufficiently similar to be analysed together, a relevant question is whether the results may be driven by specific countries, rather than capturing general patterns. In Figure 3, we therefore report the results of country specific models.

9

For presentational convenience, and as the statistical power of these models is limited, we focus on the point estimates of the parameters (the full results are available in an Online Appendix). As we might expect, the spread of the estimates generally reflects the size of the confidence intervals in Figure 2. More importantly, however, for the event types shown to have significant effects in Figure 2, the country-specific estimates consistently have the same sign. In other words, the effects reported in Figure 2 appear to apply quite generally, even if the magnitudes vary somewhat.

ARDL and ARDL-GARCH(1,1) estimates by country. Note: The reported effects are calculated as

Figure 3 also shows estimates from country-specific GARCH models (Bollerslev, 1986). These models have a conditional mean equal to the AR(2)DL model given in equation 1, and a GARCH(1,1) variance model. In other words, the conditional variance is given by

Another key question is whether the results reported in Figure 2 hinge on the selected [0, 1] window. To test this, Figure 4 reports panel models similar to equation 1, but expanding the window one day in each direction. In other words, the model captures [−1, 1] and [0, 2] windows, by (respectively) adding leads and lags of the event matrix. Interestingly, while retaining their direction, two estimates that are significant in Figure 2 each lose their significance in one of the two alternative specifications shown in Figure 4. While this may reduce our confidence in these two estimates, we can also give these results a substantive interpretation. Negative ECB statements have a weaker effect when we include movements on the preceding day, and a stronger effect when we include the movements two days after. In other words, the statements may appear to take the market by surprise, and then have a delayed effect in the expected direction. Positive German decisions, on the other hand, have a weaker effect when we include movements two days after they take place. This may suggest that their effects are somewhat temporary, and partly reversed by subsequent reactions in the opposite direction. Overall, however, the key point to notice is that most of the significant estimates in Figure 2 are very similar in Figure 4, suggesting the results generally are quite robust to the choice of event windows.

Results using alternative event windows. Note: The reported effects are calculated as

Still, as the case of positive German decisions illustrate, a key question is how long the effects we find last. We have focused our analysis on short-term effects to be confident in the conclusions we draw. Over a longer time-horizon, identifying the effect of a specific signal becomes hard, if not impossible. Therefore, we do not attempt to model what happens outside the event windows used in the analysis. However, as mentioned in the methods section, the bond spreads series are integrated, retaining a perfect memory of previous shocks. Thus, short-term changes will have lasting impacts, unless they are fully reversed outside the event windows. In other words, while we leave the issue of long-term effects aside here, the changes we identify are likely to have long-term consequences.

Conclusion

The growing dependence of governments on international bond markets is a key feature of the international economic order. Rising yields on sovereign debt not only burden states’ budgets and limit their ability to use fiscal policy pro-actively, but can even push otherwise solvent states to the brink of default. Preserving markets’ trust is thus one of the key aims of economic policy-making. Hitherto, studies of default risk have mainly focused on the role of national policy-making, while the role of external actors has garnered limited academic interest.

We have examined this issue by looking at Europe’s sovereign debt crisis. The more investors question the solvency of a Eurozone country, the more we expect their trust in the Eurozone’s commitment to rescue stressed economies to matter. The period we investigate (2009–2012) is thus one in which European-level policy-making should be particularly important, and our results are likely to be more pronounced than they would be for other periods. This is consistent with the argument that the reactions of financial markets vary over time (D’Agostino and Ehrmann, 2013; De Haan et al., 2014). Notably, most of the events we examine took place before ECB President Mario Draghi’s pledge to do ‘whatever it takes’ (on 26 July 2012), and our results mainly apply to this period. If we exclude all events after this point (including the speech itself), all our substantive results would remain as reported. However, our data do not permit us to reliably assess whether events after this point had weaker effects (which may be likely), and we leave it for future research to examine this issue further.

Our results suggest that policy-makers are indeed able to reassure markets by sending clearly positive signals. However, the effect of such signals depends on the credibility of the actors involved. We argue that credible actors are able to move markets through their statements, while less-credible actors need substantial decisions to reassure markets, as their statements are largely discounted as cheap talk. In line with these expectations, we find that positive statements by the ECB have a significant effect on spreads, while those from Germany and the EU are largely ignored. In the eyes of investors, independent central bankers appear to enjoy far greater credibility than officials from either Germany or the EU, allowing ECB decisions to be anticipated based on earlier statements. Accordingly, decisions by Germany and the EU produce clear and immediate reactions, while decisions by the ECB appear to be anticipated to the extent that they do not have short-term effects.

With regard to negative signals, we find that statements by Germany and the ECB have significant effects on spreads. Our results thus lend at least partial support to the argument that negative signals generally have increased bond spreads (Beetsma et al., 2013; Mohl and Sondermann, 2012). Furthermore, the effect of negative German statements is consistent with the claim that Germany’s reluctant approach has increased the GIIPS’ spreads, making the crisis worse (e.g. Paterson, 2011). However, the effect of positive German decisions also illustrates that Germany’s role is somewhat more ambiguous than this claim suggests. Lastly, we find no significant effects of mixed statements and decisions. As many important EU crisis meetings indeed had mixed outcomes, this finding might to some extent explain why EU decisions have been seen as ineffective by many observers.

Overall, our findings indicate that European politics does have a significant impact on the price of sovereign debt. What European policy-makers say and do regarding bail-outs and the extent of risk-sharing inside the EMU matters a great deal to bond markets. However, our study also demonstrates the importance of simultaneously distinguishing between positive, negative and mixed signals, between statements and decisions, as well as between credible and less-credible actors. Lastly, it could be noted that while our results are consistent with the argument that credible statements permit anticipation of decisions, further research could strengthen this argument by employing more direct tests. Such research could link decisions to statements, distinguishing between decisions that could be inferred from previous statements and those that could not. According to our argument, we would expect stronger effects for unpredictable decisions than for predictable ones. Similarly, we should see greater effects for statements that allow the anticipation of later decisions. 10

Footnotes

Acknowledgements

The authors have contributed equally and are listed in alphabetical order. This paper was presented at the ECPR General Conference, Glasgow, 3–6 September 2014, and at the 55th Annual Convention of the International Studies Association (ISA), Toronto, 26–29 March 2014. We are very grateful for comments and advice from Michael Bechtel, Steve Heinke, Cavit Pakel, Frank Schimmelfennig, Gerald Schneider, Stefanie Walter, Andreas Wenger, Thomas Winzen, three anonymous reviewers, and members of the ETH colloquium on European Politics, as well as the participants of the annual retreat of the ETH Center for Security Studies.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.