Abstract

Market access for pharmaceuticals has become a key issue in the Italian National Health Service, for at least three reasons: (i) market access delays are very high in Italy compared to other countries; (ii) drug policy is mostly driven by cost-containment both at national and regional/local levels; (iii) pharmaceutical policies have been decentralised, thus creating a very fragmented environment. These issues highlight the importance of market access and account management both at the national and the regional/local levels. The organization of market access by pharmaceutical companies in a complex environment, such as the Italian one, has never been investigated in the literature so far. Hence, this research contributes to fill the gap, surveying the industry’s perceptions and reactions on a wide range of dimensions concerning market access. More specifically, this paper aims at answering the following research questions: how is market access defined and organised? In which phases of the product life-cycle do companies invest more in market access? Which are the perceived most appropriate tools for market access? Which are the perceived main obstacles to market access? How is the market access performance evaluated? The research question has been investigated through a structured questionnaire, which has been subject to a validation process. Responders were selected according to size (sales) in order to include firms that are more likely to introduce structural changes and to create sub-units. Overall, 43 companies accounting for a cumulated 80% market share (retail + hospitals) were involved. The questionnaire was sent to the General director/Chief executive, who selected the key informant(s). Results show that (i) market access is mostly associated with public affairs and pricing and reimbursement functions; only those companies, whose responder has associated market access with a commercial activity, invest more on actions aimed at fostering market penetration; (ii) market access benefits from tools that (a) increase the knowledge of the relevant target and (b) give evidence of the drug’s value (economic evaluation and Health Technology Assessment) or its financial sustainability (budget impact analysis) and (iii) access to regional markets seems to be the most critical issue, thus confirming access problems deriving from decentralisation.

Introduction

Market access (MA) for pharmaceuticals has become a big issue in the Italian National Health Service (NHS) for at least three reasons.

First, cost-containment has being one of the most important driver of the Italian pharmaceutical policy since 1994, when the national drug formulary was completely re-defined. 1 A drug national budget (set as a % over public health funds) has been enforced by law in 2001 and changed many times. At present, pharmaceuticals are subject to a budget on retail market (13.3% of public health fund) and a hospital budget (2.4% of public health funds). Should the retail budget be overrun, the industry and the distribution have to pay back the difference. In the case the hospital budget is overcome, regions are in charge of covering the deficit. 2 Whereas retail budget has been always respected, drugs hospital budget has never been respected so far, because it was underestimated, and will be possibly overcome in the future, because most of the new and most expensive drugs are used in hospital settings. Regions have been consequently pushed to adopt cost-containment actions to get at least closer to hospital drugs budget.

Second, time to patients’ access to medicines in Italy is very long compared to other countries. According to the last estimates provided by Efpia, 3 Italy shows a 306 average days delay between marketing authorisation and patients’ access (hospital and retail delays combined). Time to market in Italy is longer than in all European countries, excluding few smaller countries (Belgium and Slovakia) and only 66% of new drugs approved at 31/12/2006 were prescribed as of end 2008. 3 In addition, price negotiation to get national approval has become tougher for pharmaceutical companies. In principle, reimbursement and prices should be simultaneously negotiated by the National Drugs Agency (Aifa – Agenzia Italiana del Farmaco) and the company that holds the relevant marketing authorisation, considering therapeutic added value (and prices of comparators), impact on drug budget, prices in other countries and cost–benefit ratio for the most innovative drugs. Actually, prices of least expensive comparators, lowest prices in other countries and impact on drug budget are the most important drivers of the negotiation. This is one of the reasons why ex-factory prices in Italy are lower than in most other European Union countries. 4

Finally, national approval does not necessarily mean immediate regional and local access. Regions have been putting many barriers to time to market and market penetration, including regional binding formularies, public procurement based on the lowest offer price, budget constraints at the hospital level, prescription targets for general practitioners and specialists on most expensive drugs and generics (or genericated molecules, which are reference priced) quotas. These regional policies have been enhanced because regions are responsible for hospital drugs budget and, even more importantly, for global health care budget. In fact, regions are accountable for any deficit they incur on health care and may use both regional taxes, co-payment (which are very unpopular) and cost-containment measures to cover this deficit. Regional barriers add an average extra delay of 160 days to national MA for onco drugs, with huge differences across regions and products. Regional binding formularies were the most important driver of regional differences in MA (measured as time to market), whereas higher prices and impact on drugs budget mostly explain market penetration differences across products. 5

Research question

The Italian payers’ environment can be definitely considered an interesting case study for MA management by pharmaceutical companies. Decision making on reimbursement status, prices and inclusion into regional formularies takes extensively into consideration added value. Cost–benefit analysis is used (at least in principle) for most innovative drugs, but budget impact is much more important for payers, with a different perspective used at the national (drug budget, including retail and hospital markets) and regional (total health care budget and hospital drug budget) levels. Finally, the payers’ landscape is more complicated than in other countries due to a strong differentiation across regions.

This environment highlights the importance of MA and account management both at the national and the regional/local levels, if compared to the traditional marketing tools mostly focused on advice to prescribers.

The organization of MA by pharmaceutical companies in a complex environment, such as the Italian one, and has never been investigated so far. Only one publication 6 scrutinized whether regional officers consider useful the relationships with regional affairs manager, who are usually involved in MA. Hence, this research contributes to fill the literature gap, surveying the industry’s perceptions and reactions on a wide range of dimensions concerning MA.

More specifically, this paper aims at answering the following questions: how is MA defined and organised? In which phases of the product life-cycle do companies invest more in MA? Which are the perceived most appropriate tools for MA? Which are the perceived main obstacles to MA? How is the MA performance evaluated?

The following sections will describe methods, sample profile and main findings of the survey. Results are finally discussed in light of the key aspects of payers’ environment (Conclusions section).

Method

There are not specific references on the relationship between the regulatory environment and MA management by the pharmaceutical industry.

The literature stresses the impact of environmental dynamics on new products performance, 7 the strategic reaction by the pharmaceutical companies to the environment aimed at gaining competitive advantages, for example through M&A 8 – 11 and internationalisation processes, 12 and the impact of the regulatory context on investment in innovation: for example Chao and Kavadias 13 pointed out that an unstable environment produces incremental innovation, whereas a complex environment generates radical innovation.

A second group of references links MA with strategic and operational marketing. More specifically, Yeoh 14 identifies five key variables to consider for successful MA. These variables can be summarized as the identification of competitive advantages of the new product in advance (i.e. when a clinical trial is started). According to other authors,15,16 MA is much more facilitated if the appropriate marketing mix is decided at market launch. Marketing mix tools include product (branding and stock), price, promotion and distribution channels. Better use of internal resources and competences (R&D and Marketing & Sales) is considered essential for successful MA according to another group of researchers. 17 – 20 A minority 21 does not recognize the need to adjust internal organizational solutions to manage MA. According to these authors, the environmental factors and the organizational structure do not have a significant impact on the access of a new product to the market and its performance, whereas more resources should be invested in product development.

The literature was useful to put the research questions into the general context of MA issues but was not enough to lay down the questionnaire. Hence, a draft questionnaire was prepared and discussed with eight representatives of large multinational companies (with a total 32% market share), through semi-structured interviews. The questionnaire was validated by two responders coming from a medium-size multinational company and a national one. This is consistent with the exploratory nature of the investigation, where questionnaires are generally discussed and validated by a small sample of potential interviewees and then pre tested on a pilot sample. 22

Responders were selected according to size (sales) in order to increase the probability of including firms that are more likely to have introduced structural changes and differentiation. 23 Forty-three companies, accounting for a cumulated 80% market share (retail + hospitals) were involved. The survey was carried out consistently with the relevant literature. 24 The questionnaire was sent to the general director/chief executive (of the Italian company/the Italian affiliate, in the case of multinational companies), who selected the key informant(s) and was self-administered by responders.

Sample profile

Twenty-one companies out of the 43 sent back the questionnaire. They account for 56.8% of global sales and 70.4% of the target (2008 data). Eight largest companies, which account for a cumulated 38.5% of the market, answered the questionnaire. The distribution by revenue size of the other 13 companies (included in sample) is similar to that of non-responders, thus reducing possible bias.

Size and sales force of the 21 companies

Responders have diverse qualifications: Market Access Director, Director of the Italian Division, Corporate Affairs, Marketing and Sales, Health Economics and Outcome Research and Pricing and Reimbursement. On average, they have been covering this position for 3 years, while the overall average presence in the company is 8 years.

How is MA defined and organized?

Definition of MA

MA is mostly associated with public affairs issues (14 out of 21 companies). Other companies have linked MA either with commercial activity or with both public affairs and marketing and sales. Ten companies have adopted a formal definition of MA. However, this definition varies across companies: (i) ‘access’ has been differently interpreted as ‘access of patients to drugs’ and ‘drugs to market (and patients)’ or ‘action aimed at removing barriers to access’; (ii) good relationships with stakeholders and third-party payers have been particularly stressed in five statements; (iii) three companies have explicitly linked MA with value proposition (i.e. MA linked with value based pricing, reimbursement status, distribution channels, etc.).

Current organization of MA and organizational changes driven by MA issues

The perception of MA as a critical issue has led to important organizational changes. In 11 companies, the reorganization has been driven by the need of a greater integration between organizational units involved in MA. In eight companies, a general reoriganisation has been interpreted as an anticipation of a broad MA-oriented strategy, whereas four responders declared that their reorganization led to a more systematic use of MA tools. Organizational changes have especially concerned larger companies with a prevalent retail business. This is consistent with Wang’s 23 findings, confirming that size is a predictor of structural change. These changes have brought either to the introduction of a cross-functional MA (10 companies) or the creation of a MA unit and the enlargement of the staff dedicated to MA (11 companies). Larger companies have emphasized, more than the others, the cross-functional nature of MA, generally associated with the presence of a MA Director. This is particularly true for those companies that have emphasized the public affairs nature of MA. Almost all 10 companies that do not have a dedicated MA unit, consider MA as a cross-functional activity, without any MA Director.

The number of people working for MA, irrespective of the way MA is organized, is linked with the company’s size. Companies with more and less than 500 million Euros turnover have, respectively, more and less than 10 people working in MA units/functions, if any. In most cases people are hired from either another pharmaceutical company or internally from the commercial function. The former strategy is a way of exploiting other firms’ investments and managing competition through osmotic circulation of knowledge, competencies and skills. The latter is often a way of granting career opportunities for those who have not room for advancing their carrier position into marketing and sales function. Expertise on public affairs is rarely acquired from other sectors and consultancy companies.

The coordination of operational units directly or indirectly involved in MA depends on the existence of a MA Director. Should there be a MA Director, he is accountable for coordination. When a MA Director does not exist, coordination follows a functional logic (Figure 1).

MA organization. MA: market access; MAD: MA Director.

Noticeably, there is a clear linkage between the way MA is organized and the core activities attributed to MA. Companies with a dedicated MA unit are focused on Price and Reimbursement (P&R) and Health Technology Assessment (HTA) functions. If the MA is cross-functional, without a MA Director, the relevant companies are much more willing to involve Marketing and Sales function, should MA be perceived closer to a commercial activity. In contrast, where MA is perceived closer to a public affairs function, companies tend to involve Regulatory Affairs, Regional Affairs, and the Product Managers.

In which phases of the products’ life-cycle do companies invest more in MA?

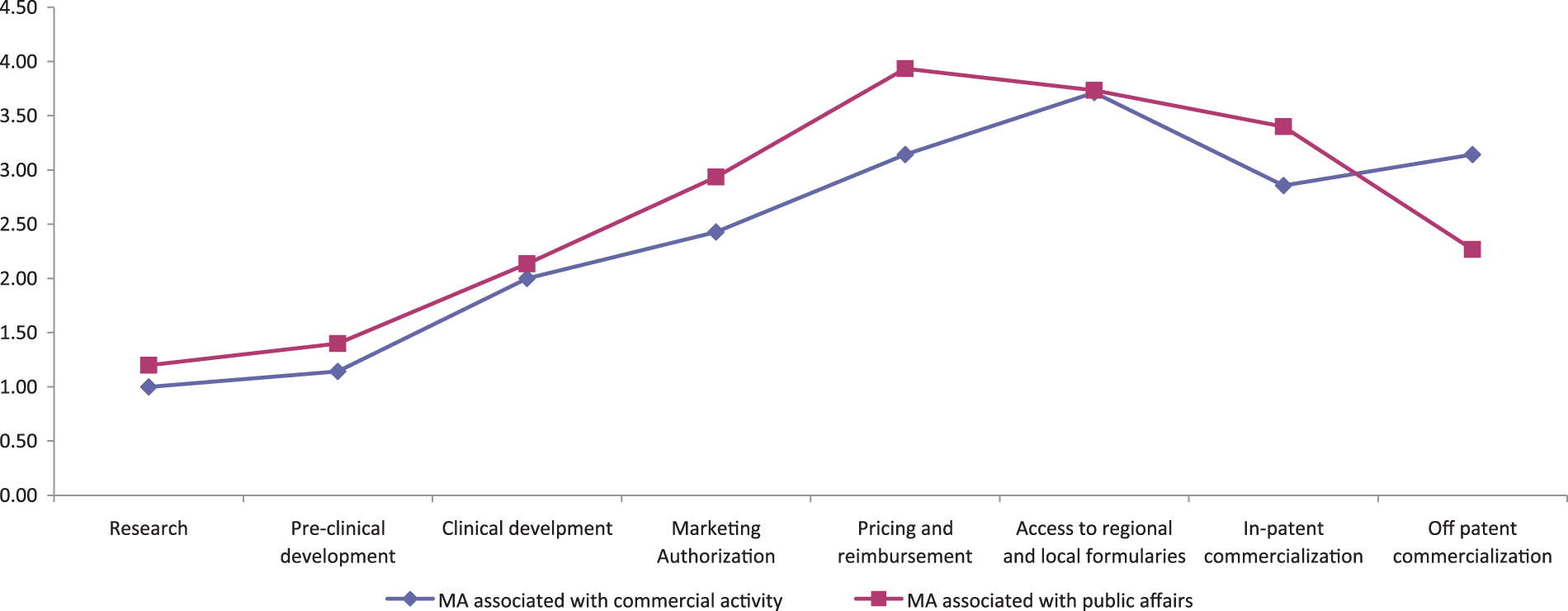

The intensity of the investment in MA shows common trends and important differences across companies. Responders have recognised that data for MA should be collected well before Marketing Authorisation, but after Phase II. Hence, the investment in MA is rather negligible during the research and pre-clinical development phases. Afterwards, this investment shows a constant increase, with an apex when P&R are negotiated with the national Drugs Agency and access to regional and local formularies is managed. Less critical, but still substantial, appears the investment in MA activities in the phases of commercialization (Figure 2).

Perceived investment in MA activity throughout the product’s life cycle (scale from 0 to 5). MA: market access.

Should MA be associated with a public affairs issue, a comparatively higher importance is given to earlier phases of the product’s life cycle (Figure 3). For these companies the most critical phase is represented by P&R negotiation, whereas the investment in MA shows a sharp decrease after patent expiration. Companies that associate MA with commercial activities put greater effort in accessing regional and local formularies and continuously invest throughout all commercial phases, both when the product is in-patent and off-patent.

Perceived investment in MA activity throughout the product’s life cycle (scale from 0 to 5) by companies that associate MA with commercial or public affairs issues. MA: market access.

Which are the perceived most appropriate tools for MA?

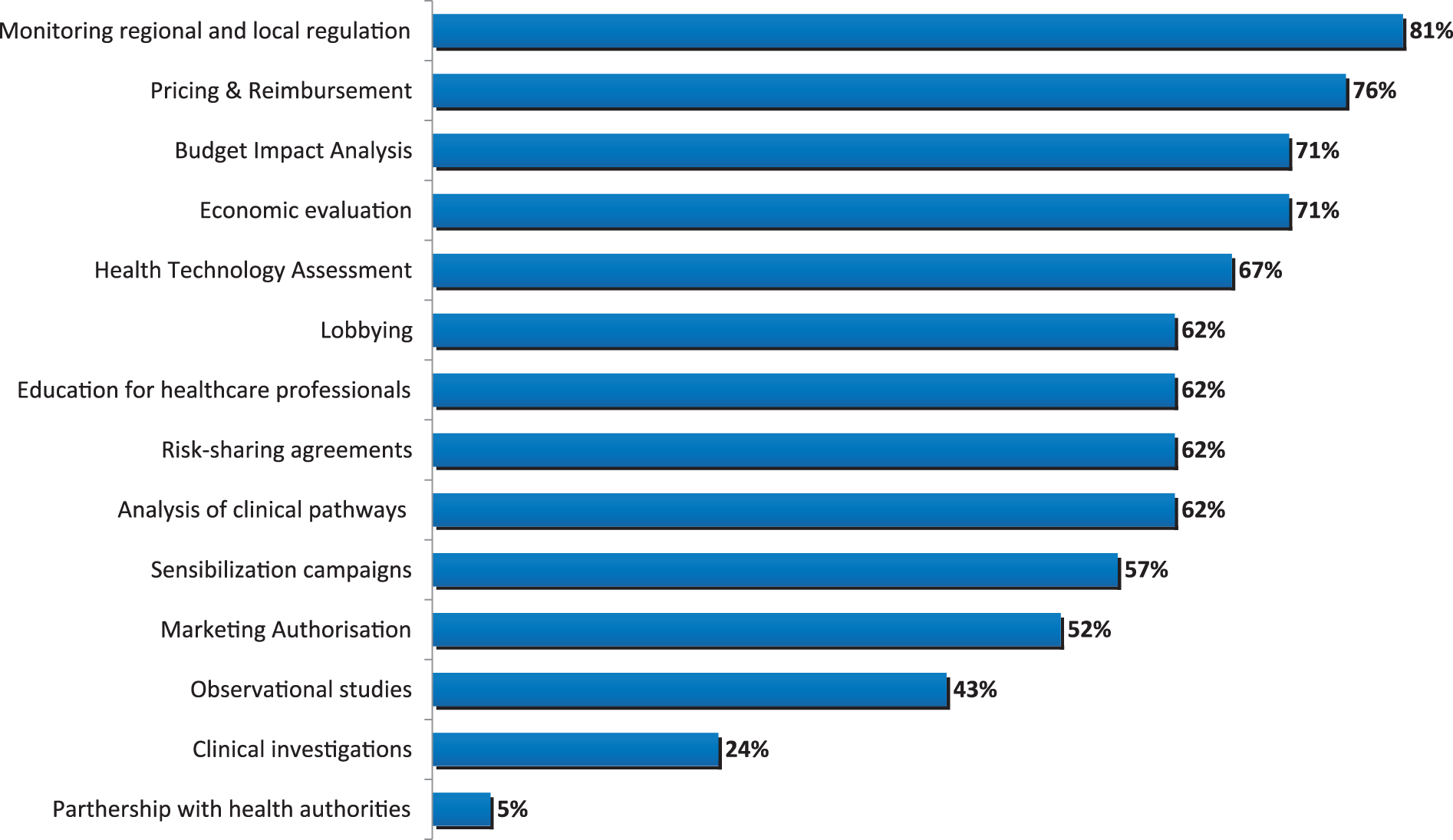

Most companies consider monitoring regional regulation as well as P&R negotiations as central activities for MA (Figure 4). This is consistent with the evidence shown by the concentration of MA investments in these phases (Figure 3).

Activities included in MA. MA: market access. Note: Number of responders that have included the relevant activity in MA over the 21 responders.

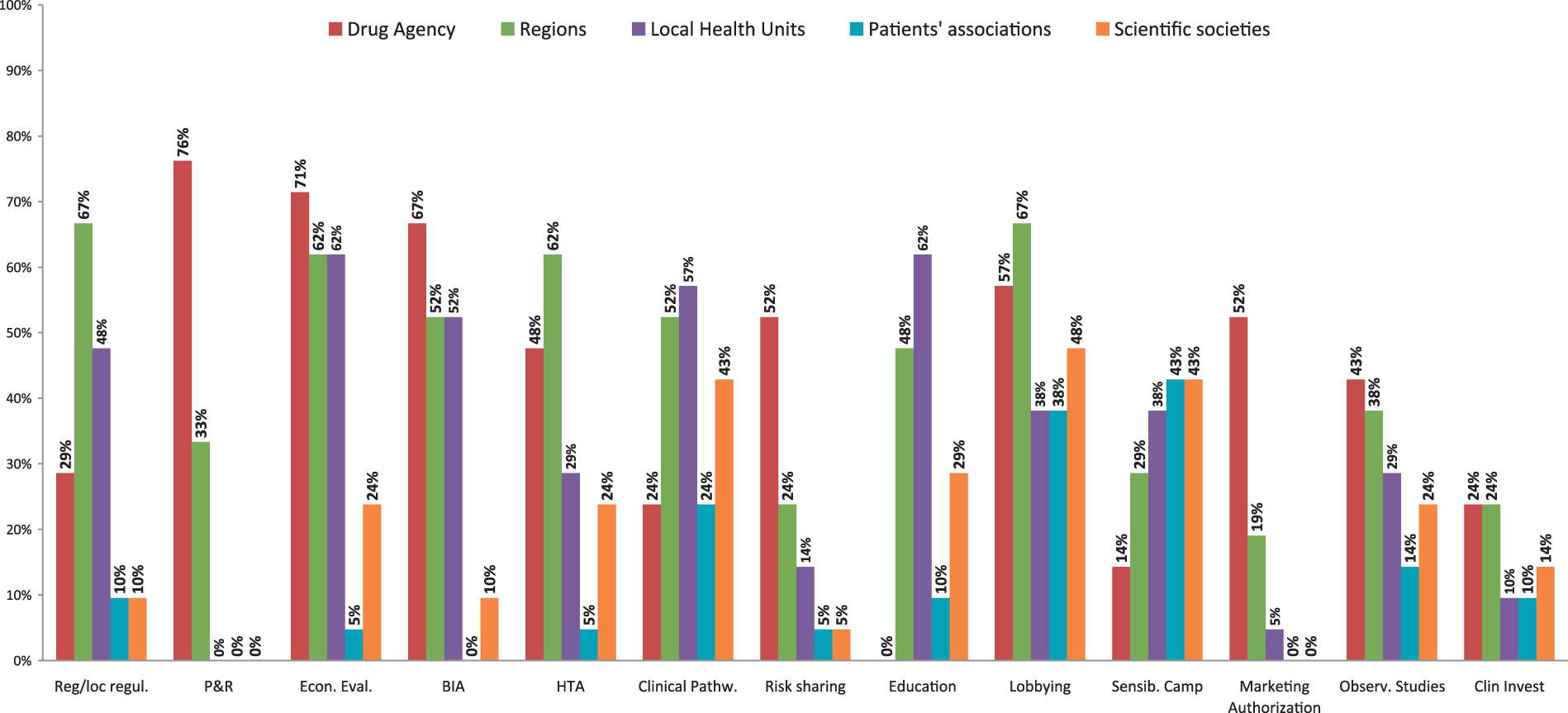

The majority (70%) considers HTA (including economic evaluation and budget impact analysis) important for MA. Economic evaluation is considered more important at the national level, because it is formally required for very innovative and orphan drugs. Within the P&R negotiation, the role of conditional pricing and reimbursement (including risk sharing and payment for performance agreements) is growing.25,26 These agreements are welcomed by (i) the payers because they could make sustainable and outcome-dependent the reimbursement of new and expensive drugs and (ii) the pharmaceutical companies, that can maintain listed prices within the corridor set by the parent company and reduce the risk of cross-reference pricing and parallel trade. Budget impact analysis and the impact of new drugs on healthcare organizations, if any, are considered important at the regional and local levels too, because regions and health authorities are responsible for health care budget (Figure 5).

Target of MA activities. MA: market access. Note: Percentage of responders that have included the relevant target for each MA activity over the 21 responders.

A smaller, but still substantial importance is given to clinical pathways, which are mainly defined and managed by health authorities and the regions. These pathways are consistent with disease management and should help overcoming a silos budget mentality. Pathways could be used to maximize the perception of drugs’ value and to improve the image of pharmaceutical companies.

Lobbying has been included among MA activities too. The preferred targets for lobbying are national and regional politicians and scientific societies. Politicians are supposed to be the ultimate decision-maker. Scientific societies are the preferred target to vehicle dossier on added value and severity of targeted disease and to put pressure on public decision makers to make new drugs penetrating the market. In addition, scientific societies have been quoted as extremely useful to manage drug budget constraint and to make fundable expensive drugs. For example, they have lobbied to change cancer drug infusion payment system from a diagnostic related group-based fee-for-service to a retrospective payment of drugs based upon costs sustained by hospitals.

Observational studies and clinical investigations are considered less important. This opinion is consistent with what has been found for the investment in MA throughout the drug’s life cycle. Even if MA issues are faced well before the product is launched into the market, P&R and access to regional formularies, where economic arguments are put at stake, are the most critical phases.

Which are the perceived main obstacles to MA?

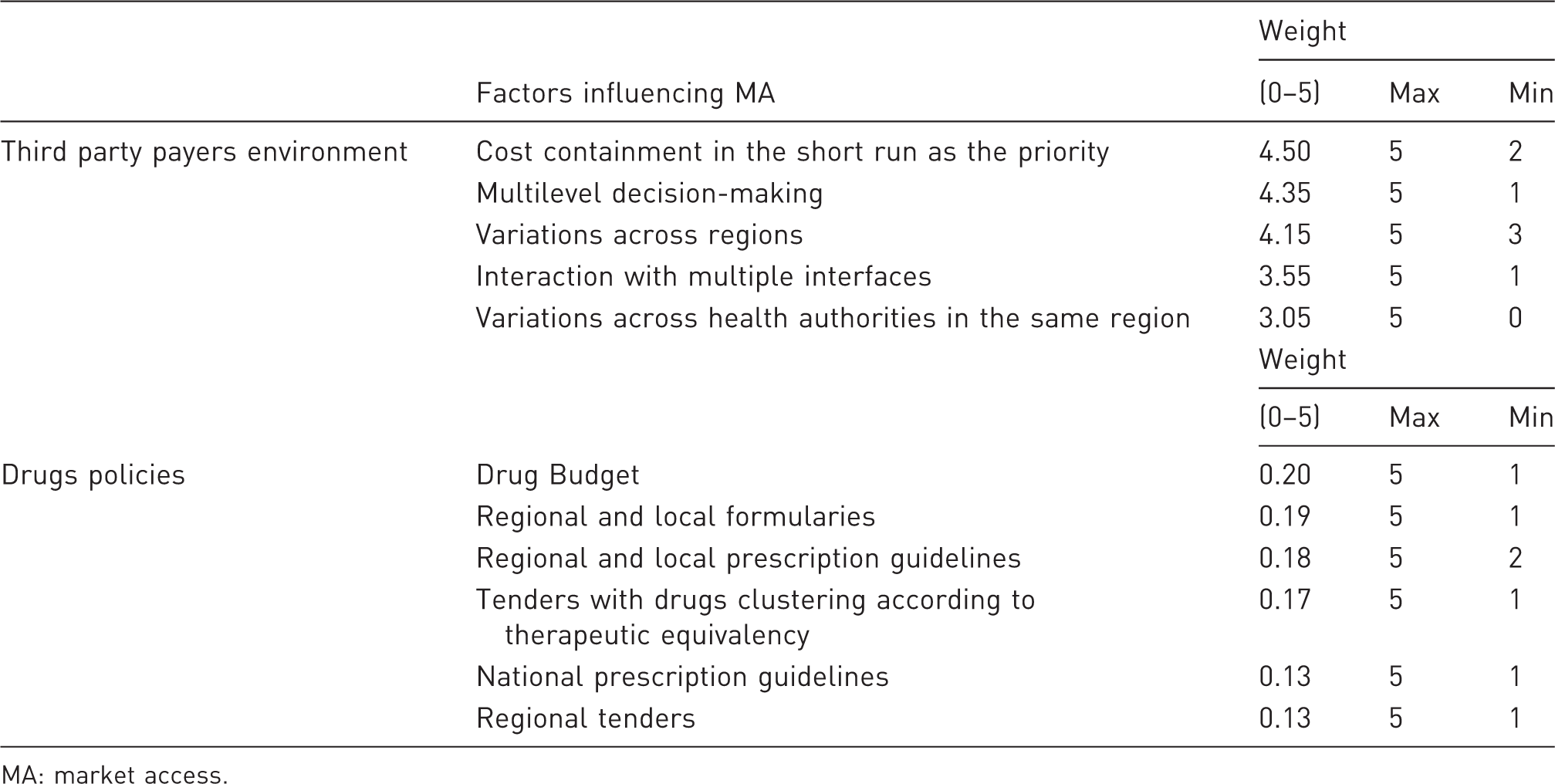

Factors influencing MA: third-party payers environment and drugs policies

MA: market access.

The general regulatory context and the policies have been consistently ranked as obstacles to MA. Priority given to cost-containment issues in the short run and variations in the regulatory context across regions, together with a multi-level decision-making process (national, regional and local) have been identified as the most important barriers to MA.

In fact, within a silos budgeting approach, there is no room for resource allocation driven by value for money and general affordability of a new drug for the health care system as a whole. In such a context, economic evaluation and health care budget impact analysis are, at least partially, disregarded. This happens both at national and at regional levels. The national Drugs Agency is generally responsible for setting prices and reimbursement status consistently with the drug budget. The regions are accountable for any deficit they incur on hospital drugs budget and no region has respected the budget so far. 27

Regional formularies and guidelines have been perceived as an important obstacle to MA, too. Time to market is negatively influenced by binding regional formularies. 5 Moreover, the multi-level decision-making process adds uncertainty on the final assessment. A recent survey 28 has found that 7 out of 16 onco drugs, already approved by the national Drugs Agency, were either refused or approved for more restricted indication in some regions and that, considering all regions and the 16 products, the inclusion into the regional formulary was denied in 13.75% cases.

Regional procurement policies have been ranked after formularies, but perceived as an important obstacle, too. Clustering drugs, according to indication (fourth Anatomical Therapeutic Chemical classification Level), has been judged particularly critical, because (i) it makes more products, including patent protected and off patent drugs, competing one another and (ii) competition mostly rely on prices, because clustered products are considered therapeutically equivalent. The impact of centralisation of procurement either at the regional level or through hospitals’ network has been investigated, too. The perception on this topic is controversial. Thus, it has been ranked lower than clustering. This is possibly due to the one-off nature of regional tenders: the company will either fully gain or loose the regional market. Hence, the industry faces, when the tenders are managed by regions, a higher risk for a larger potential payoff.

If the organization of a pharmaceutical company perspective is taken into account, regional autonomy and variability implies the necessity to acquire or internally generate specialized knowledge of each regional context, reducing the exploitment of knowledge economies.

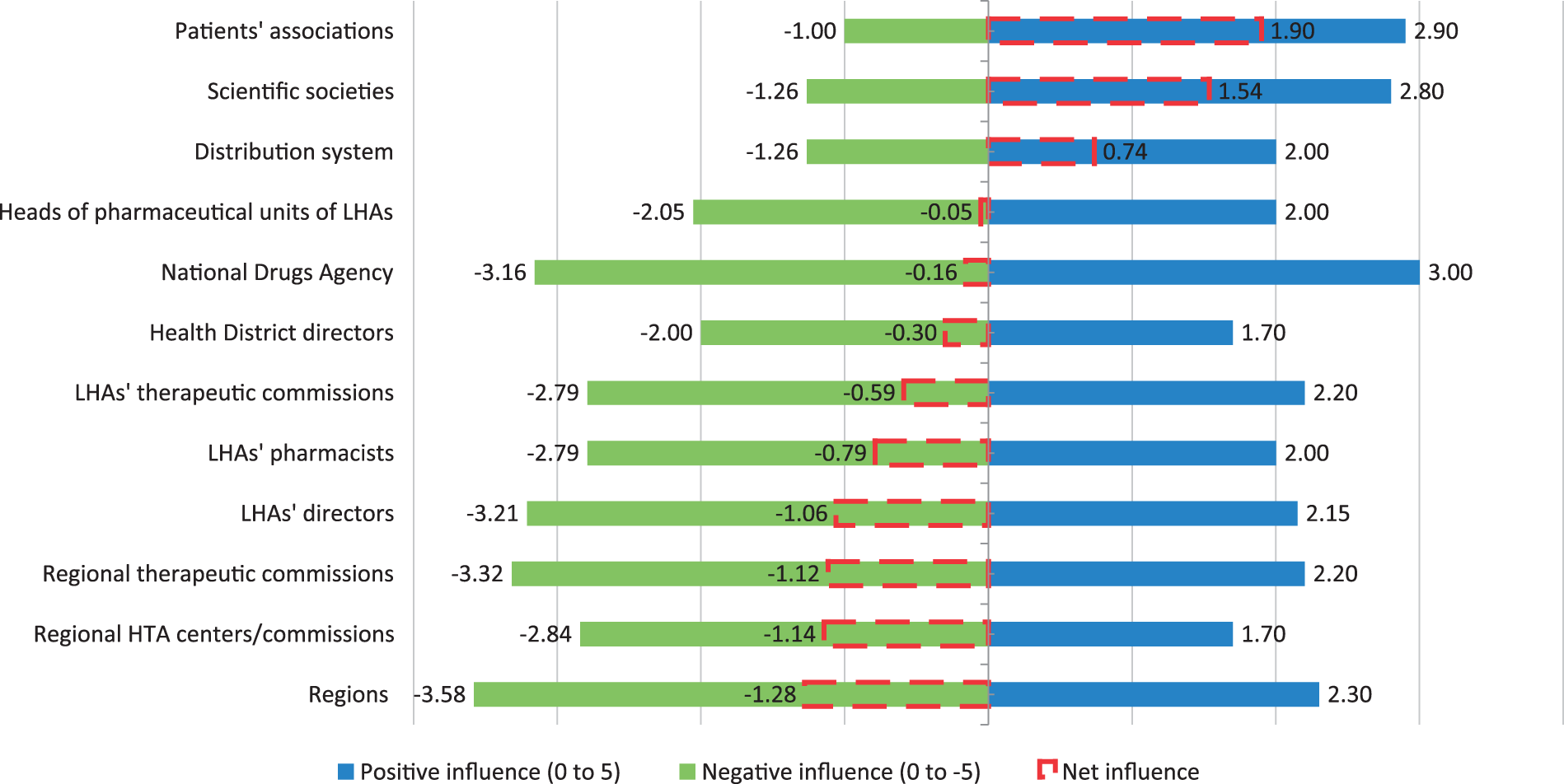

Figure 6 illustrates the perceived average (positive or negative) impact of stakeholders on MA; the dashed area shows the net effect. As expected, patients’ associations and scientific societies have been perceived to have a net positive influence on MA. Wholesalers and pharmacists are reported to contribute positively, too. This result can be explained considering that the distribution payment is based on price margins. Among third-party payers, Regional Governments are perceived to have the most negative impact on MA, followed by the local health authorities and the national Drugs Agency. In principle, regions may contribute positively to MA: differently from the national Drugs Agency, which is focused on the spending cap on pharmaceuticals, they manage the whole health care budget and may consider that additional costs due to new drugs may be, at least partially, offset by savings in other health care services. However, hurdles posed by Regional HTA programmes and formularies and huge variations across regions have been judged much more important. Local health authorities seem to be less critical than regions, because their cost-containment actions have a more limited territorial impact. The national Drug Agency has received high negative and positive scores, with a negligible net effect. It is likely that responders have been strongly influenced by their negotiation experience with the Agency that could have been positive for some drugs and negative for others.

Average perceived impact that major actors have on MA. MA: market access; LHA: Local Health Authority.

How is the MA performance evaluated?

Evaluation criteria of MA performance

MA: market access; PR: price and reimbursement.

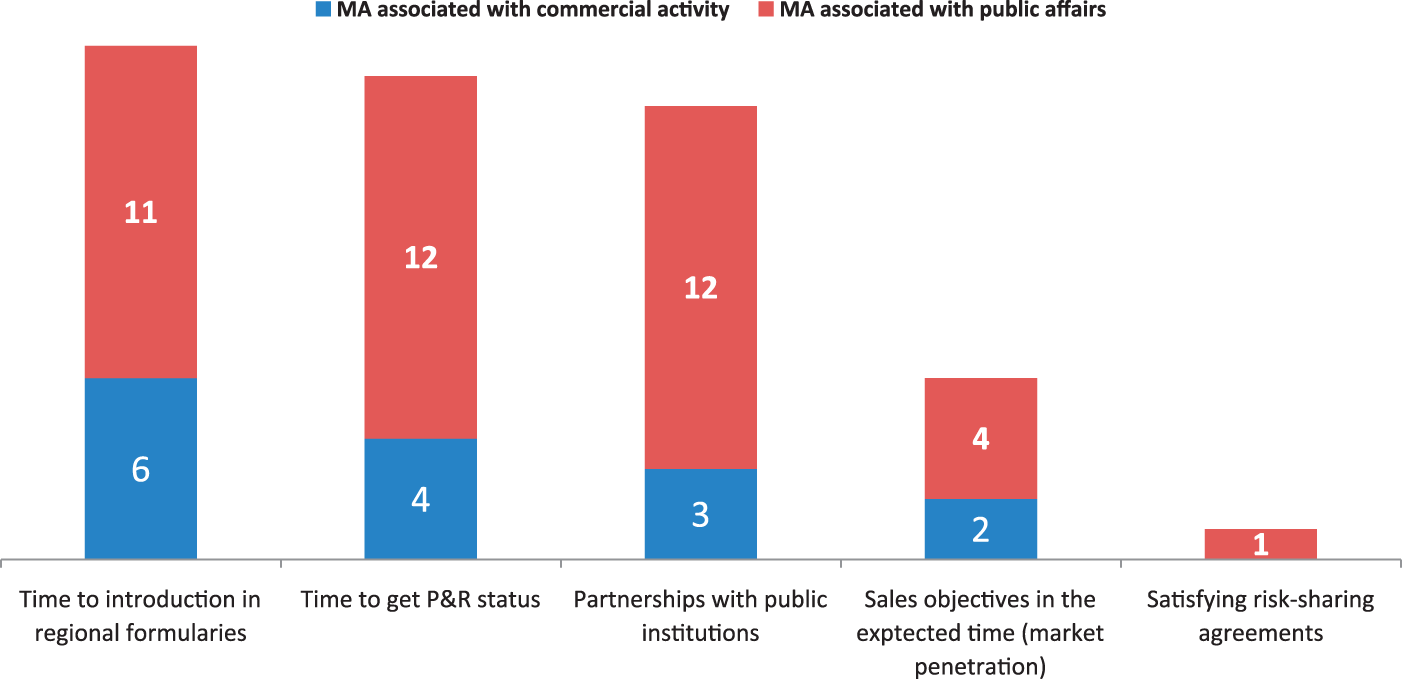

Evaluation criteria of MA performance: MA associated with commercial activity and public affairs issues. MA: market access.

Conclusions

The importance of MA has been increasing in the last years in the Italian NHS, due to (i) the complex and multi-level decision-making of third-party payers, (ii) the prevalence of a short-term policy mostly oriented by the cost-containment imperative and (iii) the increasing role of MA of actors other than final end-users (clinicians and patients).

The literature has either focused on description of policies, 1 or the perception of regional officers 6 on the relationships with MA managers coming from the industry, or the impact of policies on MA. 5 This paper has scrutinised how MA is managed by companies operating in Italy, issue that has never been considered so far.

Results show that (i) MA is mostly associated with public affairs and P&R issues, whereas those companies, whose responder has associated MA with a commercial activity, invest more on actions aimed at fostering market penetration; (ii) MA benefits from tools that (a) increase the knowledge of the relevant target and (b) give evidence of the drug’s value (economic evaluation, HTA) or its financial sustainability for the payer (budget impact analysis) and (iii) access to regional markets seems to be the most critical issue. This can be ascribed to the fragmentation of pharmaceutical policies at the regional level. In addition, a key perceived barrier is the drug budget constraint. A short-term silos budgeting is perceived as a critical obstacle to MA, considering that the value dossier usually stresses the impact of drugs on the health care system (e.g. avoiding hospitalisation). Interestingly, the national Drugs Agency, which mostly looks at the drugs budget, appears to be less critical than regions in the eye of the pharmaceutical companies, which are more focused on health care budget and, in principle, should consider the impact of drugs on other (avoided) health care services. It seems that a negative perception over fragmentation has counterbalanced the possibility that a broader budget impact analysis is considered at the regional level. Another possible explanation is that those companies in which MA is managed by the Public Affairs and Marketing & Sales Departments stress their investments at central and regional levels, respectively. Public Affairs are more focused on added value dossier, whereas Marketing & Sales Departments are usually more focused on traditional sales management.

The paper has some limitations. First, the sample includes only one Italian affiliates of multinational companies and one generic company. Italian companies, which traditionally have relied on co-marketing, have being mostly focused on market penetration and possibly never thought at MA (restrictively interpreted as time-to-market) as a critical issue. Most generic companies are likely to be too small to consider the investment in MA as a priority. In addition, added value of generics should be not demonstrated to get market entry. Finally, generic companies mostly rely on sales representatives who, depending on the market structure, focus their action on the supply-chain or the prescribers.

Second, the role of responders (who have been selected by the general director of the Italian affiliate) is very different across companies. This may reflect the way MA is organised but can have an important impact on answers based on perception.

Despite these limitations, the paper presents a complete analysis of MA strategies by the industry in Italy, which shows one of the most complex and challenging environment for companies.

Further research may (i) scrutinise performance issues: which organisational structure/incentive scheme has been more effective on time-to-market and market penetration? and (ii) provide more insights on regional and local policies: which regions have favoured/obstacled market penetration in the short and long run? Which information are required by regions to include drugs in regional formularies? Which are the cost and benefit of adapting MA strategies to local environment?

Footnotes

Acknowledgements

This Research has been carried out thanks to an unconditional grant from eight companies, which sustain the activity of the Pharmaceutical Observatory (CERGAS Bocconi): AstraZeneca, Bayer, Eli Lilly, GSK, MSD, Novartis, Pfizer and Roche.

Funding

This research has received an unconditional grant from the above mentioned pharmaceutical companies.

Conflict of interest

The authors declare that there are no conflicts of interest.

Author's Biographies

Claudio Jommi is Associate Professor of Management at the Department of Pharmaceutical Sciences, Faculty of Pharmacy, University of Novara. He is also Director of the Pharmaceutical Observatory at Cergas (Centre for Research on Health and Social Care Management) Bocconi University, and Professor at SDA Bocconi, Public Management and Policy Department, where he Coordinates the Specialisation in Pharmaceuticals and Medical Technologies, Master in International Health Management Economics and Policy. His research activity is focused on pharmaceutical economics, policy and management, market access for pharmaceuticals, comparative analysis of health care systems, decision-making in healthcare. He has published in several refereed academic journals, including Health Policy, Pharmacoeconomics, International Journal of Health Planning and Management, Public Money and Management.

Monica Otto holds a Degree in Public Management from Bocconi University and a Phd in Business Administration and Management at Bocconi University. She is a contracted research fellow in the Pharmaceutical Observatory of Cergas Bocconi, Department of Policy Analysis and Public Management of Bocconi University. She is the Director of the SDA Bocconi Master of Public Management. Her main research topics and teaching activities include public administration and management, business – government relations, pharmaceutical economics, policy and management, and public policies promoting innovation (life sciences).

Patrizio Armeni is PhD candidate in Business Administration and Management at Bocconi University. He is also research fellow at Cergas Bocconi, and collaborates as instructor at SDA Bocconi, Public Management and Policy Department. His research activity is focused on pharmaceutical policy (Pharmaceutical Observator, Cergas), economic evaluation of medical technologies and healthcare management.

Nunzia Clea Alessandra De Luca received her degree in Business Administration from University of Parma. She is Data and Survey Manager at Cergas where she is mainly involved in the Observatory on Italian Healthcare Management (OASI) and the Pharmaceutical Observatory; her areas of activity include Evaluation and Pharmaceutical Policies, Health Policy and Institutions, and Operations Management and Primary Health Care.