Abstract

Switzerland is considering implementing a strategic energy reserve, a novel policy instrument that remunerates power plant operators for storing a minimum amount of energy in reservoirs to convert into electricity when called upon. The policy is envisioned for the winter period, when the country’s large hydropower reservoirs tend to be nearly depleted. This study analyzes the impact of such a strategic energy reserve on security of supply, consumer costs, international trade, and sustainability. A hybrid simulation model is developed that combines agent-based modeling and system dynamics. The simulations show that the reserve can improve short-term security of supply but does not improve long-term security of supply as it does not impact domestic investments or reduce the import dependency in winter. The reserve leads to a slight increase in consumer costs, even when including the reduction in outage costs. A larger reserve is more effective at reducing the supply risk but is proportionally costly. Lastly, we find that the policy induces scarcity periods that would not have occurred otherwise, which means that the reserve should have a high strike price to ensure it is only called upon as a last resort. We conclude that there is no structural need for a strategic energy reserve, as it only increases short-term security of supply and does not contribute to solving the structural problem. Any implementation should be done on an ad hoc basis, conditional on a short-term generation adequacy assessment. This has the potential to minimize the associated costs while maximizing the benefits.

Keywords

Introduction

The advance of intermittent renewable power sources in Europe has reignited concerns over security of supply (Bhagwat, Richstein, Chappin, & de Vries, 2016). This has led several countries to implement capacity mechanisms (Neuhoff et al., 2016) or maintain double structures, retaining conventional power plants as backup (Sinn, 2017). A popular capacity mechanism that has been implemented in several countries, including Sweden and Belgium, is the strategic (capacity) reserve, which keeps generation capacity out of the market, to be used in times of supply shortages. Similar to the strategic capacity reserve is a strategic energy reserve, which has not yet been implemented anywhere but might be implemented in Switzerland in the near future (SFOE, 2018a), and could conceivably be adopted in other countries if and when energy storage develops further and the policy is proven effective. A strategic energy reserve is a policy instrument that remunerates power plant operators to hold a certain amount of energy in reserve and make it available to be converted into electricity in times of scarcity.

Switzerland, a small Alpine nation with plentiful flexible hydropower plants and virtually no conventional fossil power plants, has committed to phasing out nuclear power, the stable baseload power source that currently provides slightly over one-third of its electricity (SFOE, 2018c), and to instead promote renewables and energy efficiency. Due to its large share of seasonally available hydropower electricity, Switzerland depends strongly on electricity imports in winter and exports in summer. Substituting nuclear power for solar power, which also has strong seasonal variation, will exacerbate this pattern. Even though the Swiss import capacity is relatively high, it is increasingly congested due to an increase in European cross-border trading. This import dependency is a growing concern because of the continued lack of electricity trading agreement with the European Union (EU) and consequent exclusion to EU market coupling (van Baal & Finger, 2019). Concerns also exist about the continued availability of winter imports when neighboring countries are themselves phasing out nuclear and coal power in favor of seasonal renewables. This situation has led the Swiss government to propose a strategic energy reserve specifically for the winter period. In Switzerland, such a reserve is assumed to increase security of supply, as this energy can be called on in winter, when the hydropower reservoirs are normally close to depletion (SFOE, 2018b). However, because strategic energy reserves are a novel policy instrument, there is little research or experience to draw from regarding its actual impact. Therefore, the analysis in this study uses a hybrid simulation model, combining elements from agent-based modeling and system dynamics. Specifically, we model the impact a strategic energy reserve would have on security of supply, the cost to consumers, international trade, and sustainability. While the Swiss situation is unique, the energy transition in Switzerland is similar to other countries: promoting renewables while simultaneously phasing out conventional baseload generation such as coal or nuclear.

This study is the first to explore the strategic energy reserve as a policy instrument. We look at its potential impact on security of supply, consumer cost, international trade, and sustainability. The next section examines the strategic energy reserve in more detail by discussing its design characteristics and potential pitfalls. The “Model description” section will explain the hybrid model, describing the general simulation model and the strategic energy reserve algorithm in detail. The “Scenarios” section explains the scenarios we used to simulate the strategic energy reserve and the baseline with which we compare the results. The results of the simulations are then presented and discussed in the “Results and analysis” section, where the impact of the design parameters of reserve size and strike price will be separately explored, as well as the sensitivity to electricity demand growth. The “Conclusions” section concludes the article, summarizing the results and offering recommendations for future research.

Strategic energy reserve

The strategic energy reserve is a novel energy policy instrument that remunerates operators of energy reservoirs for keeping a certain amount of energy in reserve. This energy can be called upon and converted in times of scarcity, preventing blackouts and increasing overall security of supply. While strategic reserves have been implemented in electricity systems in other countries, they have exclusively been strategic capacity reserves, not energy reserves. Strategic energy reserves are not yet a realistic option for many countries, as energy storage is not (yet) well-developed. Switzerland has a relatively large number of hydropower storage reservoirs—totaling approximately 8.8 TWh compared to an annual demand of approximately 60 TWh (SFOE, 2018c)—which makes it an ideal case study for this type of policy. Development of large-scale energy storage might make this policy an option for other countries in the future as well.

Reserve design

There are many different ways of designing strategic energy reserves. Variations can be introduced in the participation eligibility requirements, participant selection criteria, how the participating operators are remunerated, how the reserve itself is operated, and the timing and implementation of the reserve.

We analyze an energy-only strategic reserve, which means that participating power plant operators are free to use the full capacity of the power plant in the market and are only required to keep the contracted amount of energy in reserve, ready to be converted into electricity. The reserved energy is dispatched when the market price exceeds a predefined strike price, a common dispatch design for strategic capacity reserves (Bhagwat et al., 2016) that we implement for the strategic energy reserve as well.

The strike price should be higher than any supply or demand flexibility option, such that the reserve is only called on as a last resort. When energy is taken off the market and put into the reserve, the market price should see a slight increase in prices associated with the reduction of supply. Energy reservoir operators will bid slightly higher in the spot market because of the increase in opportunity cost, as will be explained in the next section. However, the strike price also serves as a sort of price cap, reducing scarcity prices and revenues, which potentially impacts the business model of certain power plant operators. An optimally designed strike price balances these two effects in order to leave investment signals in the electricity market unaffected.

Availability of reserved energy in scarcity periods

In order for a strategic energy reserve to contribute meaningfully to security of supply, the reserved energy needs to be available for use in periods of scarcity. However, a strategic energy reserve that does not place any capacity requirements on participation involves an inherent risk that the energy is unavailable. If the power plant is already running at full capacity during the scarcity period, the additional energy in reserve cannot be accessed at that same moment. The risk can be lowered if the energy reserve is spread out over many separate reservoirs, minimizing the chance that none of the reserved energy is accessible. The Swiss government specifically rejects capacity reservations, and therefore implicitly accepts this risk (SFOE, 2018b). The risk is unlikely to materialize in Switzerland, as installed capacity is almost double peak demand (Demiray et al., 2018). Thus, scarcity is unlikely to occur if there is unreserved water in the hydropower reservoirs.

A second risk exists in defining the eligibility requirements. Technological neutrality, often seen as a desirable characteristic for policies, implies that all dispatchable power plants can participate if they can keep a type of energy, ready to be converted into electricity, in reserve: natural gas, coal, nuclear fuel, or water at altitude in hydropower plants. A nuclear power plant that continuously provides electricity cannot meaningfully increase short-term security of supply simply by having more nuclear fuel in storage. Such a plant will almost certainly already be running during the scarcity period as it has a strong financial incentive to do so, and no technical limitations. In case there are technical limitations, any energy in reserve would also be inaccessible. This argument holds for most (fossil) fuel-based power plants, as they can simply buy more fuel when their reserve runs low, assuming they have unhindered access to global primary energy markets. The only power plants that meaningfully contribute more to security of supply by participating in the strategic energy reserve are those that are at risk of running out with no possibility of replenishing the reservoirs. Hydropower reservoirs, for instance, tend to run low or even dry in winter, and they cannot easily replenish these by buying more fuel. Other examples include solar plus storage, or municipal waste incineration plants.

Model description

A hybrid simulation model has been developed for this study that builds on the same core principles of a System Dynamics (SD) model developed in earlier studies (van Baal, Verhoog, & Finger, 2017; Verhoog, van Baal, & Finger, 2018). The hybrid model was developed on the Ventity™ 2.1 software platform and builds upon the SD-only model by integrating elements from agent-based modeling (ABM). SD and ABM have both seen many successful applications to energy systems and socio-technical transitions (Ahmad, Mat Tahar, Muhammad-Sukki, Munir, & Abdul Rahim, 2016; Li, Trutnevyte, & Strachan, 2015). Their difference has been described as “modeling the forest or modeling the trees” (Milling & Schieritz, 2003). They excel in their application to energy systems and transitions because they do not rely on idealized assumptions about equilibria, optima, rationality, or perfect information like other methodologies, but instead work with tailored assumptions based on the case at hand. However, they are rarely combined, despite the theoretical benefits of combining a system perspective and agent-level interactions (Swinerd & McNaught, 2012).

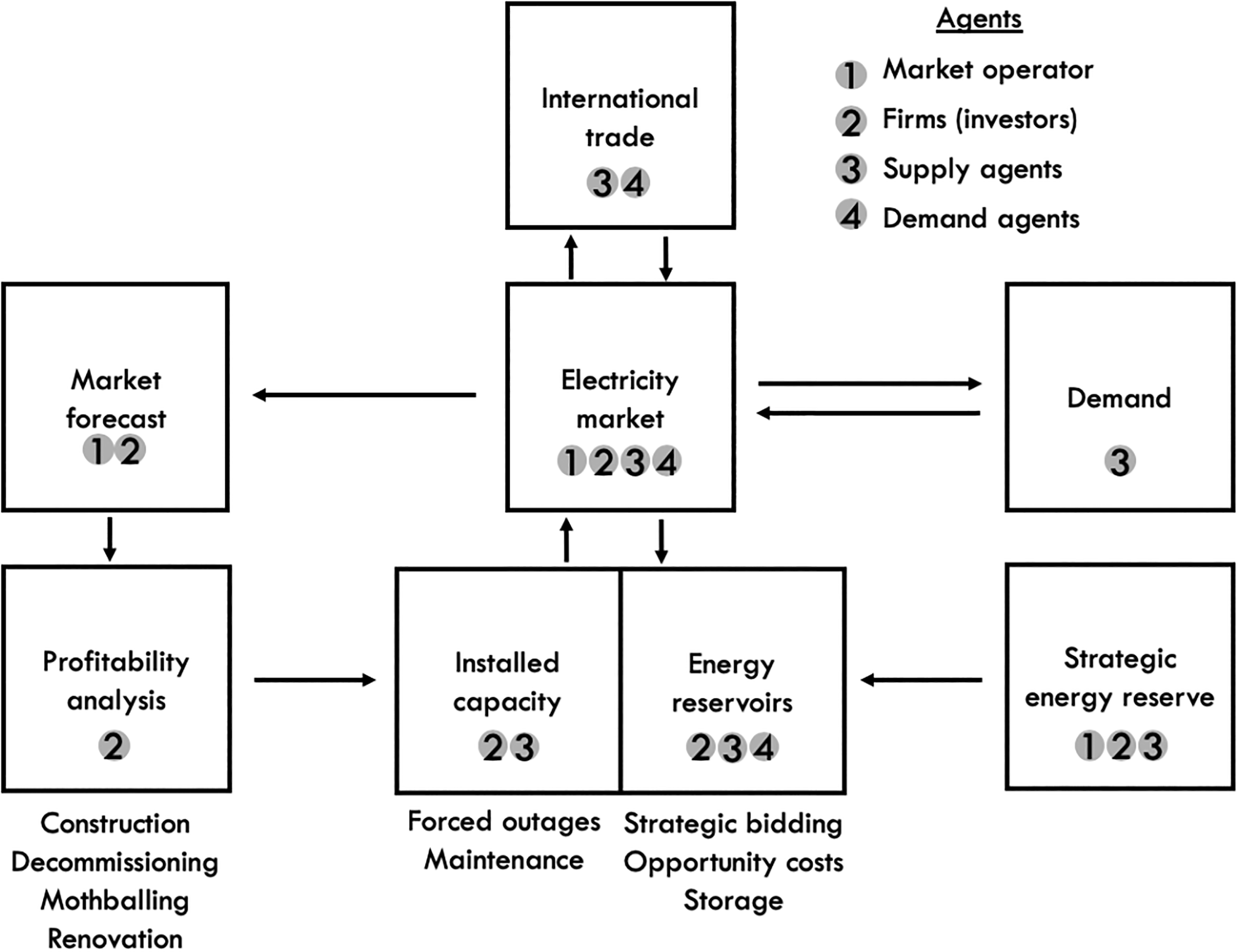

The model runs in chronological order in typical SD fashion, updating all variables hourly. Each individual agent has a rich internal structure based on SD architecture (stocks, flows, auxiliaries). These internal structures, combined with the links between the agents (the network), form the system and its emergent behavior. On top of the chronological simulation model, agents can trigger specific algorithms (‘actions’) to be executed either at the end or the beginning of a timestep. Actions can contain multiple steps that will execute ‘instantaneously’ in the model time progression, that is, before the simulation continues to the next timestep. Through actions, agents can interact with other agents or change parameters, reconfiguring the system. Agents are represented and can be interacted with in an aggregated manner, as stocks in SD as well as individually. This integrated hybrid design allows us to add plant-level mechanics and inter-agent competition while maintaining a system perspective. Figure 1 provides an abstract overview of the model. The separate components of the model are explained in the following sections.

Abstract overview of model agents and modules. Arrows indicate direct interaction between modules.

Spot Market

The electricity spot market is the most central part of the model, and the power plants, energy reservoirs, international trade, and demand all tie into it. Based on their own market forecast, firms make economic decisions concerning their power plants that eventually impact the spot market again. Besides operating the spot market, a market operator aggregates and distributes public market data to the firms, and implements policies, including the strategic energy reserve. The market operator acts as a power exchange and collects all bids from both supply and demand agents each hour. Each bid contains a capacity (MW) and price (€/MWh) pair for the next hour, representing the maximum price a demand agent is willing to pay for the consumption of electricity or the minimum price a supply agent is willing to accept for providing electricity. The market operator clears the market by matching the bids, setting a uniform market price equal to the marginal bid, dispatching the corresponding power plants, and allocating the generated electricity to the corresponding demand agents. Figure 2 provides a graphic overview of this process.

Merit-order dispatch of the spot market.

Supply

The supply side consists of supply agents (power plants) that deliver price and capacity bids to the market operator each hour. Power plants are required to bid their full available capacity. They choose a corresponding price based on the marginal cost of generation, which consists of the fuel price, carbon price, and other variable operating costs. Supply technologies with a finite primary energy supply and flexible dispatching, such as reservoir hydropower and waste incineration, have a premium on top of their marginal cost to reflect their opportunity costs. If one unit of electricity can only be produced once, and the timing can be influenced, the operator has the option to wait and produce the unit of electricity when prices are higher rather than lower. While the bidding price should be in the range of normal market prices, the operator has the opportunity to decrease or increase the chance of being dispatched by bidding higher or lower, respectively. Thus, their price bid should be higher than marginal costs to reflect this opportunity for higher profits. The ability to wait for higher prices is lower when the reservoir is nearly full, as the operator risks overflowing if it does not start producing electricity. Conversely, when the reservoir is nearly depleted, the operator can bid higher as it can wait longer for those prices to appear. We calculate the bidding price for each marginal unit of electricity according to equation (1):

Here f denotes the filling grade, or the percentage of the energy reservoir that is full, Pmax is the maximum price that the investor is using as a reference to bid, and MC is the marginal cost. The bidding price scales linearly with the filling grade, asking for the marginal generation costs when the reservoir is full, and approaches the maximum price when the reservoir is nearly empty. The approach is similar as that used, for instance, by Osorio and van Ackere (2016). The formula explains why there is no opportunity cost when the power plants have an assumed infinite supply of primary energy (such as gas or nuclear fuel), as this resembles a full reservoir, in which case the bidding price goes down to the marginal cost. Power plant operators change their maximum bidding price at the end of each year based on the past market performance of the plant according to equations (2) and (3):

The maximum price bid in any given year

Production of intermittent renewables at any given hour is calculated by multiplying the installed capacity of the power plant by a yearly profile. The model contains hourly profiles for wind and solar production in MW-production per MW-installed, created by taking hourly production data in Switzerland for 2015−2017 (OPSD, n.d.) and subsequently dividing those values by the installed capacity at that time for each hour of the year. Production data of run-of-river hydropower and inflow for reservoir hydropower plants were similarly created from Swiss data for 2012−2014 (SFOE, n.d.).

All power plants have a standard forced outage rate (FOR) of 0.04, with a mean time to repair of 67 h, in line with averages from other studies (Mohanta, Sadhu, & Chakrabarti, 2004). Every hour, a power plant has a small chance of being forced off-line. If this happens, the plant will be off-line for 67 h before resuming operation. A FOR of 0.04 means that a power plant will be off-line for an average of 4% of the year. Nuclear power plants are the only technology that also have planned outages (or maintenance). Maintenance periods are scheduled for the summer months, with as little temporal overlap between the different nuclear plants as possible. Maintenance lasts approximately 1.5 month for each power plant, in order to bring the overall utilization factor of the nuclear plants in line with historically observed values (SFOE, 2018c).

Demand

The demand side is modeled similarly to the supply side, in that each demand agent supplies price and capacity bids to the market operator each hour. Demand agents represent consumer load, demand response, interruptible contracts, and the storage demand. The price bid of consumer load (the bulk of the demand) is set to the theoretical value of lost load (VOLL), which we set constant at €3000/MWh—the maximum price allowed in the European Power Exchange (EPEX) market 1 and in line with other studies (Osorio & van Ackere, 2016). Since this is much higher than any other supply or demand option, this part of demand is the most inflexible. If there is not enough available power supply to meet demand, the ‘marginal bid’ will always be that of the consumer load, setting the price at VOLL, constituting a supply shortage or blackout. The cost of outages, defined as the product of the VOLL and the amount of load not served, is thus included in the modeled electricity price (Bhagwat et al., 2016). The consumer load at any given moment is generated from multiplying a yearly profile by the annual total load. The annual total load grows linearly from the observed value in 2017 (SFOE, 2018c). Our baseline scenario implements a growth percentage of 1%; other growth percentages are explored in the “Sensitivity to electricity demand” section. The yearly profiles were constructed by dividing the hourly values of consumer load for 2015−2017 in Switzerland, obtained from ENTSO-E (n.d.), by the annual total load. Using fixed yearly profiles in this way means the load curve for consumer load is mostly exogenous. However, demand for demand response, interruptible contracts, storage, and exports is fully endogenous, so the demand side is still relatively flexible. We will explore the impact of demand response in one of our scenarios.

Demand response operators have a fixed price bid, displacing their demand to a later moment when the electricity price is lower than their bid. Their capacity bids are subtracted from the consumer load. Interruptible contracts, which represent large (industrial) consumers that choose not to consume electricity when a certain price is reached, do not displace their abated consumption to a future time period. We assume approximately 5% of peak electricity demand is on an interruptible contract, at a price of €800/MWh, which is within the range of estimates by other studies (Cepeda & Finon, 2011; de Vries & Heijnen, 2008). Storage demand agents, representing pumped hydropower, are directly coupled to a supply agent and place their price bids based on the same opportunity cost as their supply equivalent, taking into account round-trip efficiency losses. In this way, storage operators buy and sell electricity as much as they can to maximize their own profits (Densing, 2013).

International trade

International trade functions within the merit order curve as supply (import) or demand (export) agents. There are supply and demand agents to represent each neighboring country. In the case of Switzerland, these are Germany, Italy, and France. Their capacity bid is the net transfer capacity (NTC), which can change every hour, and the price bid is the foreign spot price, which also varies hourly. At each hour of simulation, the NTC value for each country is calculated by multiplying the maximum NTC by a yearly profile. The hourly foreign spot price is calculated similarly by multiplying an annual average spot price by a yearly profile. The profiles were created by taking hourly NTC and spot price values for 2015−2017 from the ENTSO-E Transparency Platform for each neighboring country (ENTSO-E, n.d.) and dividing each hourly value by their yearly average (prices) or maximum (NTC). These profiles do not change over the run of the simulation, meaning that the foreign prices are exogenous and are not dependent, for instance, on how much is being traded with Switzerland. The underlying assumption is that the Switzerland is a price-taker on the international electricity market. However, the annual mean spot price and maximum NTC values can change. Future maximum NTC values are taken from the ENTSO-E Ten-Year Network Development Plan (ENTSO-E, 2014). We implement a simple linear growth percentage for the foreign spot prices. The Swiss domestic electricity price is strongly impacted by the foreign spot price developments because of the difference in market size. 2 Since we implement foreign prices as exogenous scenarios, we use indicators based on the difference of the national and foreign spot prices to look at the reserve effectiveness, rather than the absolute spot price in Switzerland. These indicators are described in more detail in the “Indicators” section.

Part of the international trade is also done via so-called long-term contracts (LTC), which are fixed-price call option contracts with French nuclear operators and have long been an important part of the business models of Swiss electricity companies. These LTC have their own supply agents and compete for NTC with the normal trade entity. The LTC will be slowly phased out, as they are due to expire in the coming decades and will not be renewed (VSE, 2012). We assume a strike price of €35 per MWh for these LTC, in line with other studies (Osorio & van Ackere, 2016).

Some political uncertainty exists regarding the Swiss relationship with the EU, which impacts electricity trading conditions for Switzerland as all neighboring countries are EU Member States (van Baal & Finger, 2019). Notably, the exclusion to so-called market coupling causes an increase in unscheduled power flows, or ‘loop flows’, through Switzerland, that reduce the available import capacity. While this article is not intended to be a political analysis, electricity imports strongly contribute to security of supply in Switzerland, so the impact of these loop flows must be considered. We decide to implement a reduction of 30% of NTC, a value resembling the actual situation in Switzerland (ElCom, 2017). That value is kept constant in the future, not further aggravating or alleviating the political situation. As loop flows are expected, but are by nature unscheduled and unpredictable, we model half of the NTC reduction as a constant, flat reduction, while the other half is stochastic, modeled as forced outages of the import supply agents similar to power plant outages.

Investors

Investors are economic decision-making agents, impacting the long-term development of the electricity market. Investors base their decisions on financial analyses based on their own information. They have access to the general market data provided by the market operator and plant-level data for the power plants they own. Investors base their decisions based on the profitability index as shown in equation (4):

Here Cn denotes the cash flow (profits or costs) at period n, and r is the discount rate, which we implement as the sum of the weighted average cost of capital (WACC) of the investor and a risk premium that depends on the type of investment. The profitability index is compared to a hurdle rate to decide whether or not an investment decision is made. For simplicity, we keep the hurdle and discount rates constant. Investors forecast prices 5 years into the future using basic linear trend extrapolation on the past 3 years of performance of their assets, correcting for expected changes in installed capacity. These include all capacity currently in construction and all capacity expected to reach the end of its operational lifetime within 3 years.

Investors have the ability to make financial decisions: apply for permits or invest in new power plants, or mothball, renovate, or decommission existing power plants that they own. When the profitability index of a new power plant exceeds the investor hurdle rate, the investor will decide to invest, starting the construction of a new power plant, if it already has the permit to construct such a power plant. If not, the investor will apply for a permit. Permits are granted after a specific permitting time (see the Appendix 1) or rejected if there is no more domestic potential in the case of wind or solar. Such limits (Osorio & van Ackere, 2016) are implemented but not reached in any of our simulations. Permits expire if the investor does not commit to invest within a certain number of years, which we assume is 3 years. It is important that these two decision points exist for each new power plant, because the project profitability might change between the two moments: a power plant can be taken off-line, another investor can start constructing a new power plant, or the policy (subsidy) environment can change. Endogenous investments are made for wind, solar, and combined cycle natural gas. Investments in reservoir, pumped storage, and run-of-river hydropower are implemented exogenously in line with projections of the Swiss government (Demiray et al., 2018), because of their limited expansion potential (SFOE, 2012). Other power plants are not considered for investments.

If a power plant is not profitable in the next year—meaning the expected profits do not exceed the yearly fixed operating costs—the investor will mothball the power plant for 1 year, temporarily placing it out of use. If a power plant is at least 10 years old, and not expected to be profitable in the following year or at any time in the coming 5 years, the investor will decommission the power plant. If the power plant has less than 5 years remaining operational lifetime, the investor can decide to renovate the power plant. If the renovation profitability index exceeds the investment hurdle rate of the investor, the plant is renovated. Renovation extends the operational lifetime by 5 years and is assumed to cost 25% of the original investment cost. The option to renovate exists also for the nuclear power plants, as the timing for the phaseout is only indicative, which means the schedule is not certain (van Baal et al., 2017). All power plants are decommissioned at the end of their operational lifetime.

Strategic energy reserve

The strategic energy reserve policy has not been finalized in Switzerland, so the model implementation has to make certain assumptions. The implementation of the storage reserve is done by the market operator, who collects participants’ bids specifying an amount of energy (MWh) and price (€/MWh) at the start of October. Only reservoir hydropower and waste incineration plants can participate, in order to combat the risks described in the “Availability of reserved energy in scarcity periods” section. Participants will be chosen based on the price element of their bid (lowest first) until the energy target of the reserve is met. The marginal bid will set a uniform price per MWh to remunerate all participating supply agents. The energy target or size of the reserve is set in advance. The reserved energy will be released, meaning operators can bid the energy into the market normally, after the winter period (start of April). The total policy cost of the reserve will be the remuneration paid out to the participating supply agents, less any revenues received from selling the reserved water at the strike price, as this will go to the market operator.

Supply agents make their bids for the strategic energy reserve based on the expected lost profits by participation. The lost profits are calculated by taking the markup (the selling price above the marginal costs of production) when selling the energy at the opportune moment, when prices are high (winter), minus the markup when selling the energy at a less opportune moment, when the energy is released (summer). For this reason, supply agents use the difference between the summer and winter selling prices observed in the year before to bid. The market operator will allow a maximum of 30% 3 of the storage capacity of a power plant to be in the reserve, in order to avoid losing the production capacity of that power plant on the spot market too early. Storage operators will always bid the maximum energy they are allowed to offer.

Participating supply agents keep their reserved energy in stock and use the remaining energy to bid into the spot market as normal. However, the opportunity cost changes because the reserved energy cannot be used. Equation (5) shows how the bidding behavior changes.

Scenarios

We first test the effectiveness of a strategic energy reserve in a business as usual (‘BAU’) scenario that does not have any additional policies. The initial conditions are modeled after the Swiss electricity system of 2018. The future technology costs are implemented as the average or mean values projected by the National Renewable Energy Laboratory (NREL, 2018) and carbon costs as forecasted by the Swiss government (Demiray et al., 2018). The full set of initial conditions can be found in the Appendix 1. The annual electricity demand growth rate is set at 1%, and the annual growth rate of foreign spot prices at 1.5%, in line with long-term historically observed values.

In a second scenario (‘RES’), the effectiveness of a strategic energy reserve is explored if new renewable energy sources are simultaneously promoted through government policy, such that the targets of the Swiss government are met. There are many different types of renewable promotion schemes possible, but the exact type of promotion is not relevant to our study because we do not seek to assess the effectiveness or cost of such a policy. The RES scenario assumes the policy works as intended. A dynamic subsidy on renewable electricity production is implemented that remains high enough to make both wind and solar profitable throughout the simulation and disappears when the investment targets are met. In this way, the targets are met, over-subsidization will not happen, while subsidy-free investments above the target remain possible if the market conditions allow. Other than the renewables promotion policy, the RES scenario is identical to the BAU scenario.

In a third and final scenario (‘DR’), the effectiveness of a strategic reserve in the presence of a growing share of demand response is tested. A separate scenario is chosen for demand response because it has the potential to significantly contribute to security of supply (Khan, Verzijlbergh, Sakinci, & De Vries, 2018), while the high uncertainty surrounding its potential scale and profitability makes it difficult to implement via endogenous investments. In the DR scenario, demand response is assumed to grow linearly such that by 2035, 10% of peak demand is covered by demand response. This estimate was made looking at the potential of demand response in developed countries (Gils, 2014). Demand response replaces the regular, inflexible, consumer load in the model, meaning there is no increase in total power demand and only an increase in demand flexibility. A price of €500 per MWh is assumed for all demand response assets, which is lower than the interruptible contracts but higher than most supply options. The DR scenario is fully equivalent to the BAU scenario other than this exogenously forced development of demand response.

For each of these scenarios, baseline simulations (‘BL’) are run and compared with the results of simulations with a strategic energy reserve (‘SER’). All simulations run from 2018 to 2035, with the strategic energy reserve implemented in 2020 until the end of the simulation. To account for the stochastic nature of the forced outages, 300 simulations are run for each setup. After 300 simulations, no quantitative differences were found.

The strategic energy reserve size tested in the main scenarios is 0.80 TWh. This is the equivalent of approximately 5 days of Swiss domestic demand and approximately 9% of the total storage capacity of all Swiss hydropower reservoirs, and within the range the Swiss government has explored (SFOE, 2018b). However, both larger and smaller reserve sizes are conceivable. Therefore, the impact of the reserve size on the reserve effectiveness is separately explored in the “Impact of design parameters on reserve effectiveness” section.

The strike price should at least be higher than any supply or demand flexibility option, to ensure the reserve is only called on as a last resort. A strike price of €2500/MWh is assumed in the main scenarios, which is higher than any other supply option. Determining an optimal strike price, as described in the “Reserve design” section, is beyond the scope of this article. However, a range of different strike prices is explored in the “Impact of design parameters on reserve effectiveness” section.

Results and analysis

Indicators

This section discusses the results of the simulations. The effectiveness of the strategic energy reserve is evaluated with 10 different indicators, which are classified into four groups: security of supply, cost, trade, and sustainability. For security of supply, the following two indicators are explored: [SH] Shortage hours (hours per year): the average number of hours of shortage per year. [DD] Dispatch duration (hours per year): the average number of hours the strategic energy reserve was called upon per year.

For cost, the following two indicators are explored: [RC] Reserve cost (million € per year): average cost of the energy reserve, in million per year, consisting of the remuneration to the reserve participants minus any revenue made from selling the reserved energy at the strike price. [CC] Consumer cost (€ per MWh): sum of the average electricity price and the reserve cost divided by the annual consumption.

For trade, the following four indicators are explored: [PD] Foreign price difference (€ per MWh): the yearly average difference between the domestic average electricity price and the metric average of the electricity price in neighboring countries. [TD] Trade deficit (million € per year): the net sum of revenues resulting from importing (+) and exporting (−). [AI] Annual energy independence: part of demand met by domestic production, calculated by dividing annual demand minus the net imports by the annual demand. [WI] Winter energy independence: part of demand met by domestic production in winter (January through March).

Lastly, for sustainability, the following two indicators are explored: [RE] Renewable energy production (TWh): the production of wind and solar combined in the final year of simulation. [GP] Gas production (TWh): the production of natural gas power plants in the final year of simulation.

Table 1 shows the results of the simulations. Values for the indicators are averaged over the 15-year period that the strategic reserve is active in our simulations (2020−2035) except for the sustainability indicators RE and GP, which are based only on the final year of simulation. The results for each group of indicators are discussed in the following sections.

Results of main scenarios.a

a Mean values and 90% confidence intervals for each indicator.

Security of supply

In the BAU scenarios, we found virtually no security of supply issues, with an average of 0.03 shortage hours per year in both the baseline and the reserve scenario. At least some shortages are to be expected in any system with stochastic plant outages given the small chance of critical power plants shutting down simultaneously. This effect does not go away when a strategic energy reserve policy is in place, which explains why the value is the same in both scenarios.

We find a more significant number of shortages in the RES scenarios. This is an interesting finding on its own, as these scenarios have a higher amount of domestic supply because of the renewable subsidy. Apparently, the presence of the intermittent renewables introduces some supply risk. The bulk of new renewables is solar, production of which is mostly done in summer and does not significantly contribute to security of supply in winter. The reserve functions as intended and reduces the risk of shortages significantly, from 6.1 to 1.6 h per year.

Interestingly, we find that the dispatch duration in the SER scenarios is somewhat higher than the shortage hours in the baseline for all scenarios. This effect is minimal in the RES scenario, but considering not all shortage hours are prevented, it indicates shortages were prevented that would not have happened without the reserve in place. This can happen if generation capacity is taken off the market early because of the energy reservation, creating scarcity on the market that can be solved by releasing the energy again, a risk identified in the “Strategic energy reserve” section.

Cost

The reserve costs an approximate 46 million euro per year in the BAU and DR scenarios. This is higher than, but in the same order of magnitude as, the costs envisioned by the Swiss government, which estimate the costs for a 0.775 to 1.525 TWh reserve at 15−30 million CHF (SFOE, 2018b). Counter-intuitively, when the reserve gets dispatched more to prevent shortages (RES scenarios), the total cost is higher. Intuitively, the cost should be lower as the earnings from selling the energy at the strike price remunerate the market operator, and thus contribute to lowering the total cost. However, the presence of supply shortages also means the electricity price will be higher overall because of scarcity, even before the strategic reserve gets dispatched. Scarcity prices in winter increase the seasonal price difference, which is what hydropower operators use to make their bids for the strategic energy reserve. Consequently, the compensation they receive increases, making the reserve more costly.

The consumer cost is marginally higher in all scenarios with the reserve compared to the baseline. The consumer cost is the sum of the electricity price and the tariff rider to pay for the reserve cost, if the reserve is active. This tariff rider assumes the cost is borne equally by all consumers and is thus simply the reserve cost divided by the total annual demand. Note that the electricity price includes the cost of outages, as all lost load is priced at VOLL. In theory, the strategic energy reserve could reduce the consumer cost by the reduction of shortages and associated cost of outages. The reserve strike price of €2500/MWh is close to the VOLL of €3000/MWh, which means this effect is likely small. Therefore, it is unsurprising that the consumer cost is higher in all scenarios with the reserve compared to the baseline. The RES scenarios show that renewables depress the average electricity price and thereby the consumer cost, even if the risks of outage and subsequent higher costs of outage are included.

Trading conditions

We do not find significant changes in cross-border trade conditions because of the strategic energy reserve. The policy has no impact on energy dependence, either over the year (AI) or during the winter period (WI). This can be expected given that the policy is not designed to promote new investments. However, considering one of the rationales behind the policy was to increase security of supply in winter, the policy cannot be considered a long-term solution, as it does not contribute to structurally improve the situation.

The average electricity price in Switzerland is higher than the average price in the neighboring countries (PD) in all scenarios. Nuclear energy currently serves as baseload electricity in Switzerland. The phaseout of this nuclear capacity turns Switzerland into a net importer. The flexible hydropower plants will then more often serve to meet peak demand when electricity is already being imported. Hydropower operators can then bid higher than the import price, whereas before they would have competed with imports for peak demand and would have had to bid lower.

Sustainability

We do not find a strong effect on sustainability indicators because of the reserve. In all scenarios, we find there are slightly fewer renewables in the scenario with the strategic reserve compared to the baseline, but the effect is too small to be conclusive. Similarly, there is virtually no difference in the amount of electricity production from gas power plants. What little production there is comes from the existing thermal power plants; none of the simulations found new investments in thermal power plants. The target of 14.4 TWh renewables by 2035 is almost met in the RES scenarios, which is to be expected considering delays in construction and permitting and the way the subsidies are implemented. Interestingly, the BAU and DR scenarios have well over 10 TWh of renewables by 2035 as well, showing that considerable investments in new renewables will happen regardless of the subsidy, but that the targets will not be met without government support.

Impact of design parameters on reserve effectiveness

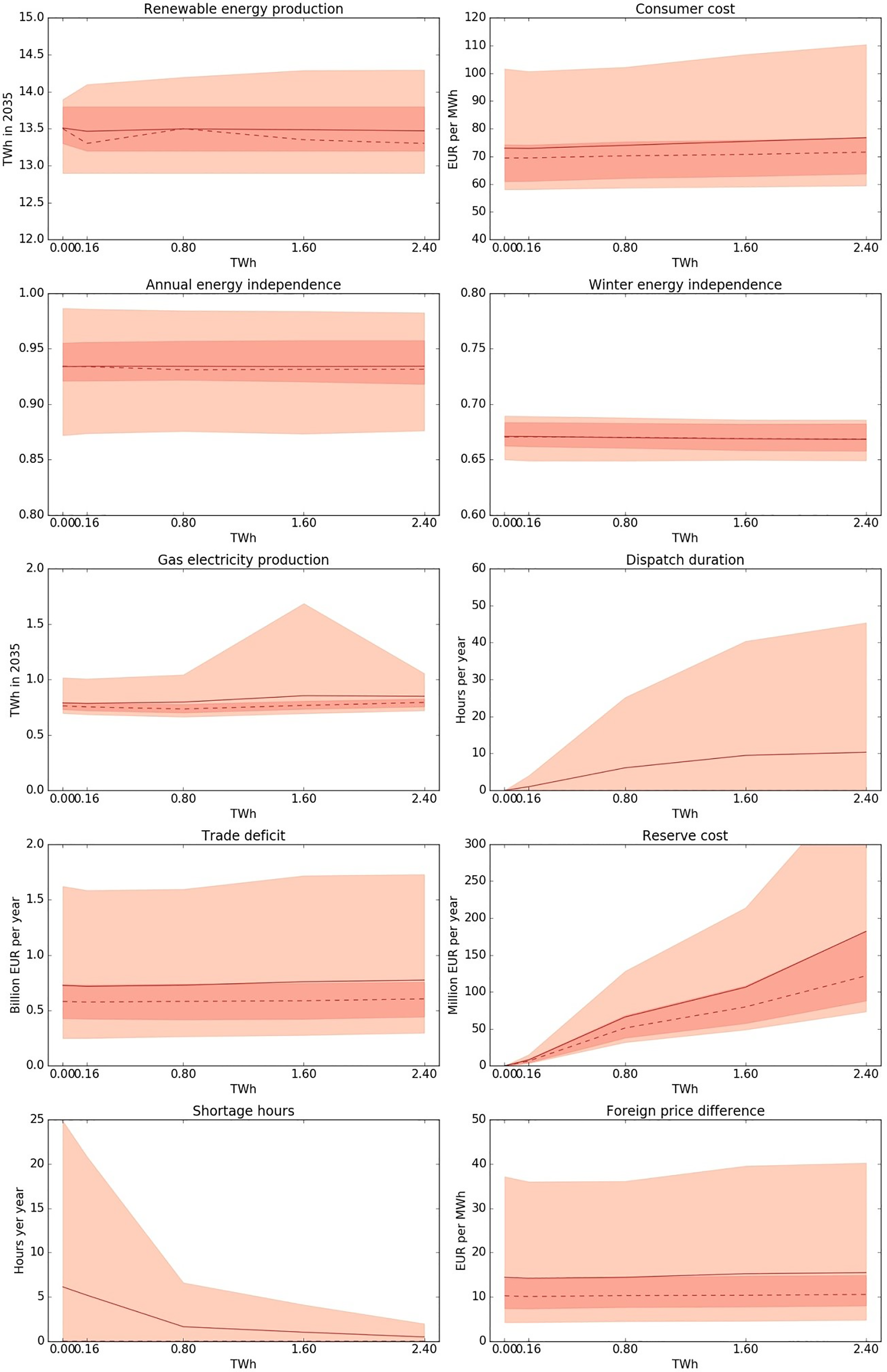

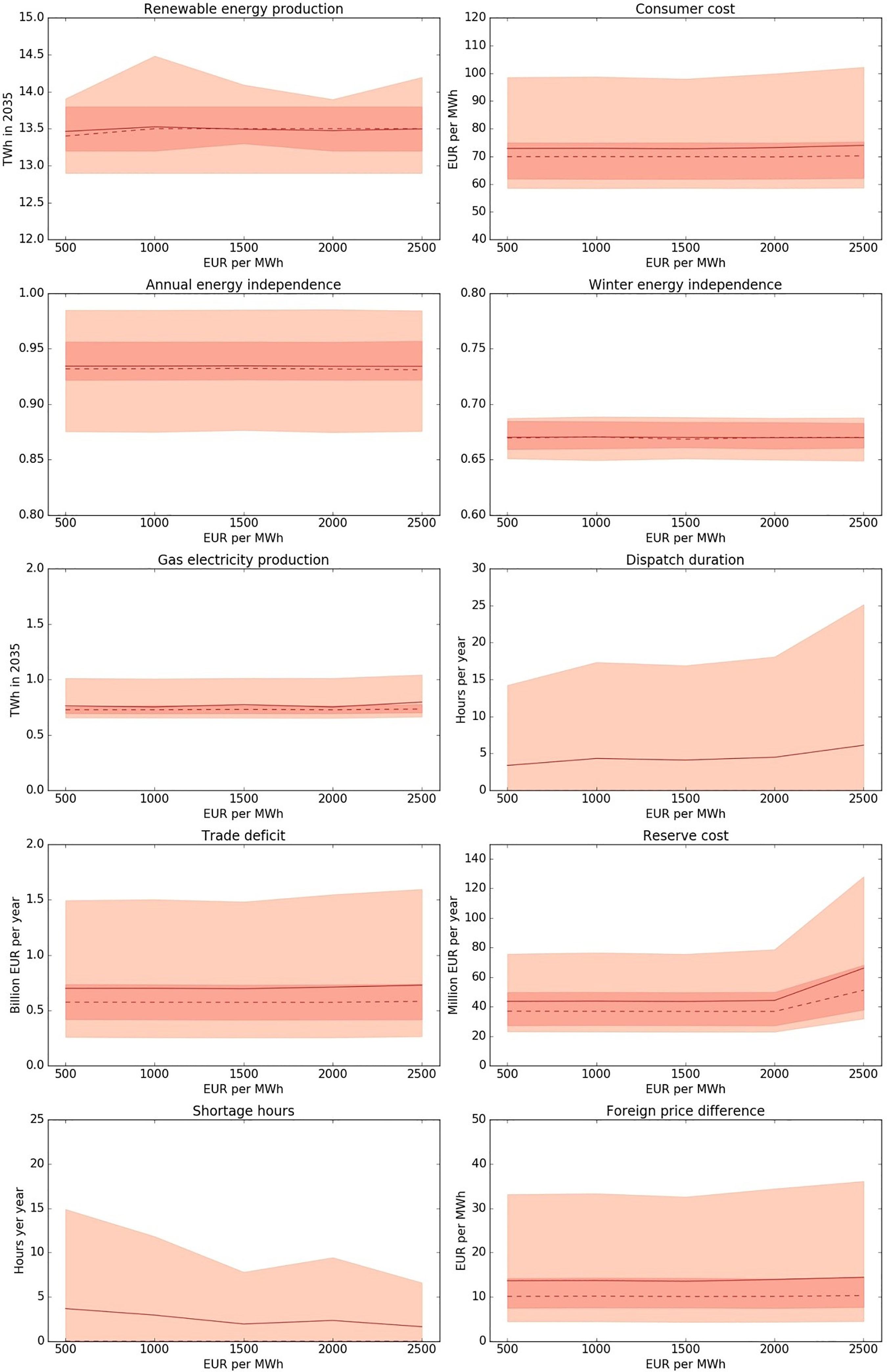

The reserve size of 0.80 TWh and the strike price of €2500 per MWh were implemented in all the main scenarios. In this section, we explore the impact of these parameters and additional reserve sizes of 0.16 TWh, 1.60 TWh, and 2.40 TWh, which are the approximate equivalents of 1, 10, and 15 days of Swiss electricity demand, respectively. A reserve size higher than 2.40 TWh is improbable as this already represents about 27% of all hydropower reservoir storage capacity in Switzerland. We explore additional strike prices of €2000, €1500, €1000, and €500 per MWh. We implement these design parameters in the RES scenario, as the reserve was dispatched most frequently in this scenario, so the impact of the parameters should be most visible. The results for the reserve size and strike price variations are plotted in Figures 3 and 4, respectively.

Results of RES-SER simulations with varying reserve size. Shown values are means, medians (dashed lines), 50%, and 90% confidence intervals.

Results of RES-SER simulations with varying reserve strike price. Shown values are means, medians (dashed lines), 50%, and 90% confidence intervals.

The reserve cost, dispatch duration, shortage hours, and consumer cost are the indicators that are most impacted by the change in reserve size. The other indicators remain largely the same independent of the reserve size, although a slight upward trend can be seen in the foreign price difference and trade deficit. The reserve cost is found to increase linearly with the reserve size: a strategic energy reserve of 2.40 TWh costs €182 million per year, approximately three times as much as the 0.80 TWh reserve.

The dispatch duration increases with the reserve size, with the curve being concave rather than linear like the reserve cost. The dispatch duration is always higher than the number of shortage hours found in the baseline. This seems to confirm the hypothesis that the strategic energy reserve creates, and remediates, scarcity periods, although this effect does not seem to grow proportionally when the reserve size increases. The shortage hours have a negative concave relation to the reserve size. The largest difference in shortage hours is between 0.16 TWh and 0.80 TWh, whereas the difference between 1.60 TWh and 2.40 TWh is comparatively small. These decreasing marginal benefits to the reserve size hint at an optimal reserve size that minimizes costs but maximizes benefits in terms of the reduction in shortage risk. However, from a social perspective, the consumer costs are always higher compared to the baseline, indicating that consumers are better off accepting the small risk of supply shortages rather than paying for the strategic energy reserve. This is based on a VOLL of €3000/MWh, which is based on the current maximum spot price in the EPEX market but is nonetheless a relatively low value of VOLL and too simplistic for prolonged outages (Ratha, Iggland, & Andersson, 2013). This implies that the true cost of outages could be higher. Therefore, it is not possible to conclude definitively that a strategic energy reserve is not cost-effective.

Changes in the strike price most affect the shortage hours, reserve cost, and dispatch duration. The other variables mostly remain stable. Lowering the strike price increases the number of shortage hours. At a very low strike price (such as €500 per MWh), the number of shortages is only marginally lower than in the baseline scenario. This is consistent with the purpose of the strategic energy reserve. A high strike price ensures the reserve is only used as a last measure when all other options have been exhausted. Lowering the strike price also seems to slightly decrease the reserve cost. However, this effect seems to level off for strike prices lower than €2000 per MWh. A lower strike price should mean that the reserve gets dispatched faster, as the electricity spot price does not have to rise as high before the reserve gets called on. While an increase in dispatch duration would be expected with lower strike prices, this does not seem to be the case. We find a slight decrease in dispatch duration at a lower strike price.

Sensitivity to electricity demand

In this section, we explore how demand growth impacts the reserve effectiveness. Future electricity demand is an uncertain parameter, as there are simultaneous efforts to promote energy efficiency (which reduces electricity demand), but also to electrify heating and mobility services (which potentially increases electricity demand). In our main scenarios, we implemented an annual electricity demand growing at a rate of 1% per year. Here we explore demand growth percentages of between −2% and +2%. Since the baseline changes when we change the demand growth, we simulate new baselines (RES-BL) as well as new scenarios with the strategic energy reserve (RES-SER) for each demand growth percentage. The results are plotted in Figure 5.

Results of RES-SER (red) and RES-BL (blue) simulations with varying demand growth rates. Values shown are means and 90% confidence intervals.

As is immediately visible, almost all indicators are significantly impacted by the demand growth, as expected. Demand growth has a positive relation with the indicators for consumer cost, foreign price difference, renewable and gas electricity production, trade deficit, and shortage hours. It has a negative relation with annual and winter energy independence. In the simulations with a strategic energy reserve, higher demand growth induces a higher reserve cost and dispatch duration. In the highest demand growth scenario, shortage hours are proportionally reduced by the strategic energy reserve. There are still approximately 10 shortage hours in the scenario with the highest demand growth rate. This indicates that higher demand might warrant a larger strategic energy reserve to reduce the risk of supply shortages to an acceptable level.

The dispatch duration is significantly larger than the shortage hours in the baseline scenarios, for all demand growth rates. We even observe reserve dispatches while the baseline did not have any shortage hours, in the lower demand growth scenarios. This confirms what the main simulations already shown: that the strategic energy reserve can cause scarcity that would not have occurred without the reserve. The consumer cost with the reserve is slightly higher for all demand growth percentages—as we also found for the main scenarios—showing that the total cost of outages (priced at VOLL) is lower than the cost of the strategic reserve on average.

Model limitations

We only investigated some of the domestic effects and cross-border effects that impact Switzerland (import dependency and trade deficit). However, other cross-border effects are feasible, as other studies have shown for similar policies (e.g. Bhagwat, Richstein, Chappin, Iychettira, & de Vries, 2017; Cepeda & Finon, 2011). In interconnected power systems, the benefits of a strategic energy reserve can spill over to the neighboring systems, stabilizing their grid while they do not pay for the reserve. Furthermore, since the strike price effectively serves as a price cap, it can distort price and investment signals. Internationally operating firms can decide to construct power plants, especially those that rely on scarcity rent for profitability, in adjacent countries where the price is not capped. However, the policy might also incentivize domestic storage capacity investments as it can generate additional revenues for storage operators. Because of these price and investment signals, it is also feasible investment incentives for interconnectors are affected. Further research should look at the impact of a strategic energy reserve on such (cross-border) investment signals and spillover effects.

We chose not to look at investments into batteries or hydropower plants, even though these technologies are likely most affected by the strategic energy reserve policy. The potential of hydropower is already almost fully utilized in Switzerland; there is a relatively small amount of reservoir hydropower that can feasibly be built (SFOE, 2012) and it would not have been realistic to include market-based investments. Investments into large-scale batteries would also highly unrealistic because their policy environment, market potential, and future investment and operating costs are highly uncertain and subject to change. Nonetheless, further research should investigate how a strategic energy reserve policy would change the investment incentives in these technologies.

Another potential consequence of a strategic energy reserve that we did not look at is the exercise of market power. In our model, all power plant owners are required to bid all of their available capacity. Strategic withholding of capacity by firms could trigger the strategic energy reserve and increase prices for all other power plants that the firm owns. While this risk exists in all electricity markets, the presence of a strategic energy reserve can increase the number of hours with high prices and makes it easier to trigger them, giving a higher incentive to firms to withhold capacity.

Lastly, this study is not a generation adequacy study for Switzerland’s power grid and should not be interpreted as such. It is important to look at many more factors than we have included in this study to determine whether an electricity system is adequate and to determine the risk of supply shortages. Furthermore, such a study cannot be conducted in isolation for Switzerland and would have to look at the interconnected European grid. This study has looked only at how a strategic reserve would be able to reduce potential supply shortages, and how such a policy would impact the electricity market conditions in Switzerland. The strategic energy reserve has the potential to be more effective and less costly if the dimensions of the reserve are coupled and made conditional on short-term generation adequacy assessments. This could eliminate the costs of operating a (large) reserve in those years where it is not strictly necessary to do so.

Conclusions

This study has explored the effectiveness of a strategic energy reserve to increase security of supply for the Swiss energy system during the energy transition. The ongoing Swiss energy transition is characterized by a nuclear phaseout and simultaneous promotion of energy efficiency and renewable energy sources such as solar and wind. While the Swiss power system, characterized by a high interconnection and a large share of hydropower, is unique, the Swiss energy transition is similar to other countries that promote renewables and plan on phasing out conventional baseload power plants, whether coal or nuclear. Further advances in energy storage technologies might make strategic energy reserves a possible policy for other countries as well.

The results show that a strategic energy reserve contributes to short-term security of supply because it is able to decrease the risk of supply shortages in winter in Switzerland. Especially when a large number of intermittent renewable power sources are introduced into the electricity system, the availability of flexible hydropower assets in winter contributes to security of supply and the strategic energy reserve can ensure the last-resort availability of such assets. However, it cannot completely eliminate the risk of outage, as we find some supply shortages, even in scenarios with a very large strategic energy reserve. This is because there is an inherent risk that the reserved energy is inaccessible, either because the power plant is already running and cannot increase its production capacity or because the power plant is in a forced outage. These risks should be minimized by spreading the strategic energy reserve over multiple power plants. We further find that the strategic energy reserve is more frequently dispatched than shortage hours occur in the baseline simulations for all scenarios. This shows that the policy creates scarcity on the market that would not have occurred otherwise. Therefore, the reserve should be made as small as possible to prevent such artificial scarcity.

The results further show that the strategic energy reserve becomes more costly, rather than cheaper, if it is called on, even though the revenues from selling reserved energy serve to compensate the total cost. This is because of scarcity prices: it will become inherently more attractive for a power plant operator to sell its energy in the market during the scarcity periods, rather than participate in the reserve and only be compensated for operational costs if the energy is called upon. Thus, power plant operators will need higher compensation for participating in the reserve if scarcity periods are more likely to occur.

Larger strategic reserves further reduce the risk of supply shortages, but with diminishing returns to scale. However, the costs are proportional to the size, which suggests there is an optimal reserve size that finds a trade-off between minimizing the supply risk and policy cost. However, a strategic energy reserve was found to increase the cost of electricity supply to consumers in all scenarios, as any potential outages are less costly than operating the strategic energy reserve. The reserve was modeled with a fixed size and time period, and outages were priced at a relatively low VOLL. A tailored strategic energy reserve based on a forecasted short-term need might cost less and have more merit. Therefore, any strategic energy reserve implementation should be done on an ad hoc basis, based on a short-term generation adequacy assessment.

We did not find any significant impact on investment incentives. This can partly be explained because we did not model investments into hydropower assets, which are the largest participants of the energy reserve and receive most of the additional revenue. However, the investments in domestic renewables or natural gas are not impacted, nor is the reliance on imports in the winter period reduced. This shows that the policy does not contribute to long-term security of supply and does not contribute to solving the structural problem of winter import dependency. This further supports the conclusion that a strategic energy reserve should only be considered a short-term solution. Future research on strategic energy reserves should look at cross-border investment and spillover effects in more detail and evaluate the effectiveness of a strategic energy reserve when conditional on a short-term generation adequacy assessment.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Appendix 1

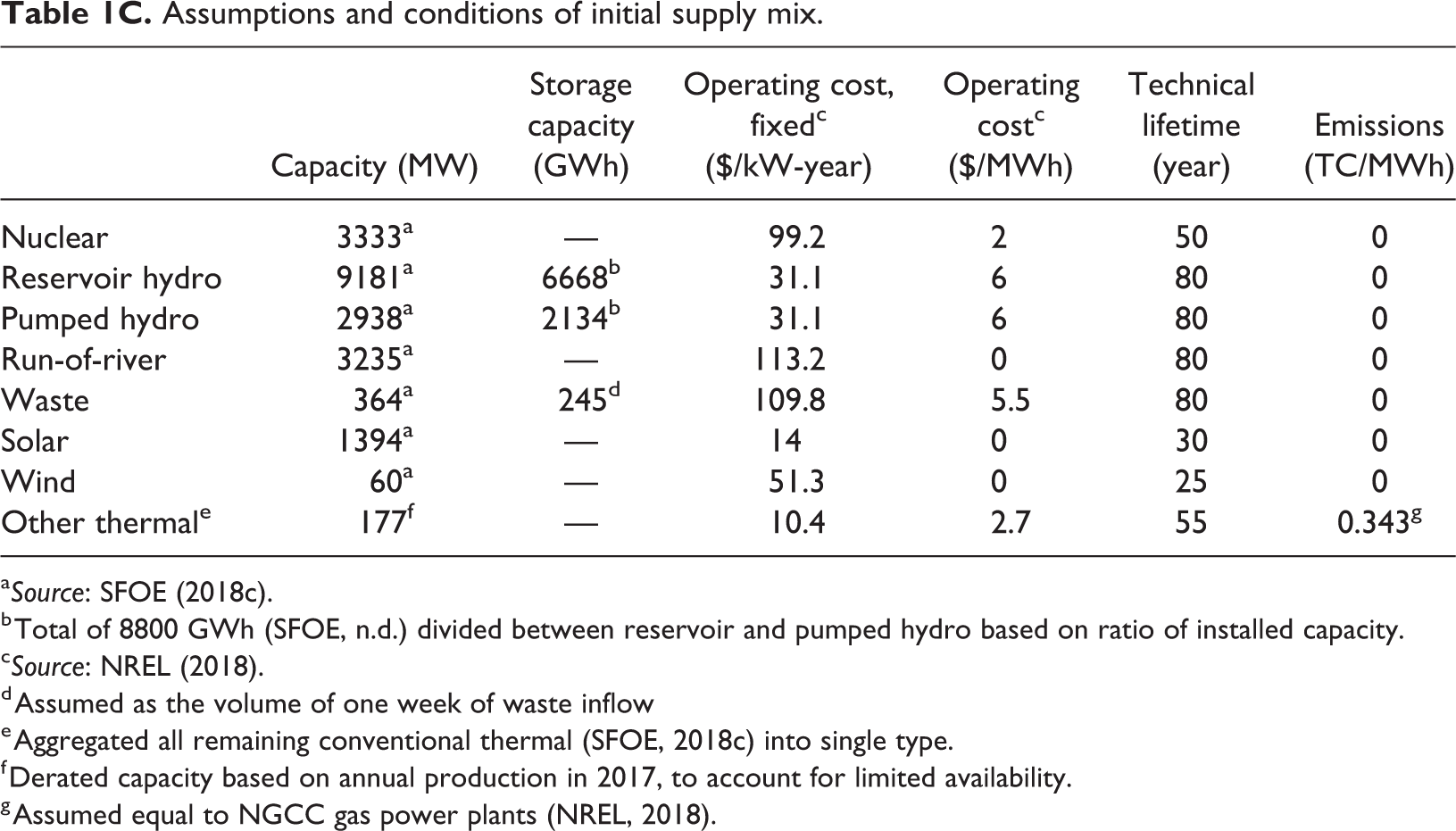

Assumptions and conditions of initial supply mix.

| Capacity (MW) | Storage capacity (GWh) | Operating cost, fixedc ($/kW-year) | Operating costc ($/MWh) | Technical lifetime (year) | Emissions (TC/MWh) | |

|---|---|---|---|---|---|---|

| Nuclear | 3333a | — | 99.2 | 2 | 50 | 0 |

| Reservoir hydro | 9181a | 6668b | 31.1 | 6 | 80 | 0 |

| Pumped hydro | 2938a | 2134b | 31.1 | 6 | 80 | 0 |

| Run-of-river | 3235a | — | 113.2 | 0 | 80 | 0 |

| Waste | 364a | 245d | 109.8 | 5.5 | 80 | 0 |

| Solar | 1394a | — | 14 | 0 | 30 | 0 |

| Wind | 60a | — | 51.3 | 0 | 25 | 0 |

| Other thermale | 177f | — | 10.4 | 2.7 | 55 | 0.343g |

a Source: SFOE (2018c).

b Total of 8800 GWh (SFOE, n.d.) divided between reservoir and pumped hydro based on ratio of installed capacity.

c Source: NREL (2018).

d Assumed as the volume of one week of waste inflow

e Aggregated all remaining conventional thermal (SFOE, 2018c) into single type.

f Derated capacity based on annual production in 2017, to account for limited availability.

g Assumed equal to NGCC gas power plants (NREL, 2018).