Abstract

This research studies the disassociation phenomenon between network and data services that has disrupted the telecom sector in India. We employed grounded theory approach to explore this phenomenon and its impact on the Telecommunication Service Providers (TSPs). We have derived the insights and developed a coding paradigm via a judgmental sample of 19 senior experts at decision-making positions in the Indian telecom sector. Through literature review, we identified the fundamental changes in the Indian telecom sector from 2013 to 2019, when this phenomenon was widely observed. The findings indicate the technology evolution’s role in driving the data-network disassociation in the presence of regulatory forbearance, 4G spectrum availability, hyper-competition, and evolving device ecosystem. These conditions have proved advantageous to Over-The-Top (OTT) players, caused financial stress to the TSPs, and forced them to resort to consolidation measures and shift from voice-based to data-based business models. The study’s insights will help the Industry understand the phenomena, regulatory issues in technology adoption, survival challenges, and decision-making strategies for pre-empting technical disruptions. It also emphasizes being watchful of the competing non-conventional industries from a regulatory perspective.

Keywords

Introduction

Telecommunication service providers (TSPs) offer high-speed internet services over their networks that they set-up, enabling third-party application developers to build platforms for offering Over-The-Top (OTT) services without investing in the underlying networks. The TSPs facilitate mobile data services for the OTT providers to deploy the mobile data to offer voice, video calling, messaging, and audio-visual content. It creates a visible distinction between data and network services. Earlier, the data services were imperceptible and yielded minimal revenues. In the last ten years, Indian telecom industry witnessed this dissociation between data and network services in view of the technology evolution. Using grounded theory approach, we have explored how technology adoption led to this dissociation that affected the growth of the TSPs and OTT communication service providers.

Since its evolution, the telecommunication sector has revolutionized how people communicate, starting with voice calling and gradually moving towards data-driven services. Indian telecommunication sector is among the largest telecom markets globally, with nearly 1172 million wireless subscribers, overall tele-density of 84.46%, and total broadband subscribers of 850.94 million (TRAI, 2023e). In recent years, TSPs have been facing the threat of getting reduced into bit pipes due to OTT companies acting as direct substitutes for the voice and messaging services that drive the revenues of TSPs (Chen, 2019; IANS, 2022). In India, till 2015-2016, despite the rapid growth of data services, voice services remained predominant in the telecom space in terms of revenues and traffic (GSMA, 2016). However, soon after, the growth in voice revenues shrank due to consumers' rapid adoption of OTT services (TRAI, 2019b). Telecom Regulatory Authority of India (TRAI), which regulates TSPs and tracks the industry’s performance in India, reported AGR (Adjusted Gross Revenue) across TSPs in Q1’20 was USD 19.2 billion versus USD 29.3 billion in FY 2017 (TRAI, 2020a).

Consequently, the industry’s monthly ARPU eroded by around 40% over these years (USD 1.86 in Q2’17 vs. USD 0.99 in Q1’20). Mobile data customers increased exponentially from 200 million in October 2016 to 597 million in August 2019 to 833 million in December 2022 (TRAI, 2016b; 2020a; 2023a). Data consumption grew explosively from a meagre 0.2 GB/subscriber/month in October 2016, 9.8 GB/subscriber/month in June 2019, 14.97 GB in Dec 2021, to 17.11 GB/subscriber/month in Dec 2022 (TRAI, 2016b; 2020a; 2023b). To meet this demand, the industry made massive investments in the network and acquired spectrum through auctions. The average Capex by Indian operators for years 2017-19 was more than 50% of revenue versus the global benchmark of 17-19% (ICRA, 2019). While the growth in data traffic is exponential, countries’ telecom industry has globally witnessed tapering off of the revenues questioning the industry’s sustainability (Openet Telecom, 2010). Thus the operators were compelled to change their business model mid-way before fully recovering the capital deployed in 2G and 3G technologies (BBC News, 2020; Roy, 2019).

High-speed networks have encouraged the development of communication applications that support voice, video, and messaging (MNS Consulting, 2017; Sawe, 2016). These services were traditionally provided by mobile operators and were coupled with the access network. These services got decoupled from the access network, meaning that the services are no longer exclusively provided by telecom operators (Antonopoulos et al., 2017). This decoupling of services due to technological innovation involves providing services by the Over-The-Top (OTT) service providers, which pose stiff competition to the TSPs (Farooq & Raju, 2019; IANS, 2022). The OTT applications don’t require permission, license, or integration with the access networks (Kochhar, 2022; Seth, 2022). The OTT providers need minimal investments in only the platforms and reduce the user’s dependence on interconnection and voice roaming, further reducing the TSPs’ revenues (PTI, 2022).

The network operators who invested considerably in building their networks must remain relevant to the subscribers. On the other hand, OTTs have the advantage of unrestricted availability of access networks due to the law of net neutrality (Antonopoulos et al., 2017; Seth, 2022). TSPs are not permitted to create a two-sided business model by charging their customers and OTT players to ensure non-discriminatory access to all the content, whereas OTT providers offer services similar to those of the TSPs (ET Bureau, 2016). Further, the net neutrality law prohibits paid prioritization, blocking, or throttling, which deleverages the telcos’ capability to earn any revenue from the OTT communication provider (Seth, 2022). OTT services are not considered in the scope of telecommunication regulatory obligations such as privacy, emergency call, lawful interception, universal service obligations, taxes & levies, consumer protection and quality of services (ET Bureau, 2016; Sunilkumar, 2023). This regulatory arbitrage provides a relative cost advantage to OTT communication companies as they do not have to purchase the spectrum or licenses to provide communication services. The economic impact of such decoupling may or may not be different if the OTT services have been subjected to similar regulatory and licensing obligations that apply to the voice and messages carried by TSPs.

While voice usage per subscriber nearly doubled during 2013-19, data usage soared 150 times during the same period. The industry witnessed around 25% growth in mobile subscribers taking teledensity in India up from 75.2% to around 90.1% TRAI (TRAI, 2019a). Operator-wise mobile subscriber trends (TRAI, 2020b) show that for most operators, the decline in subscriber count has been very steep during the period under study, especially post-launch of services by Reliance Jio in the year 2016. The decline led to huge loss of revenues to these telcos (John, 2019). The only companies that protected their subscriber base during the period were Airtel, Vodafone, and Idea. Reliance Jio had a meteoric rise from zero to over 200 million customers until 2018 and crossed the 350 million mark in 2019 (Khurana, 2021; TRAI, 2018, 2019c, 2020b).

Traditional telephony relies on a vertically integrated network, where over-the-top communication services are coupled with an underlying bearer network. OTT services have been offered to customers who find these as a direct substitute to the PSTN-based SMS, video & voice services provided by the TSPs (Green & Lancaster, 2006). In the definition presented by Green & Lancaster (Green & Lancaster, 2006), OTT service providers offer a service to the customers for which they may or may not be required to pay. The OTT services are provided without the network operator’s direct involvement in identity, billing, sales, earning revenue, authentication, and traffic routing.

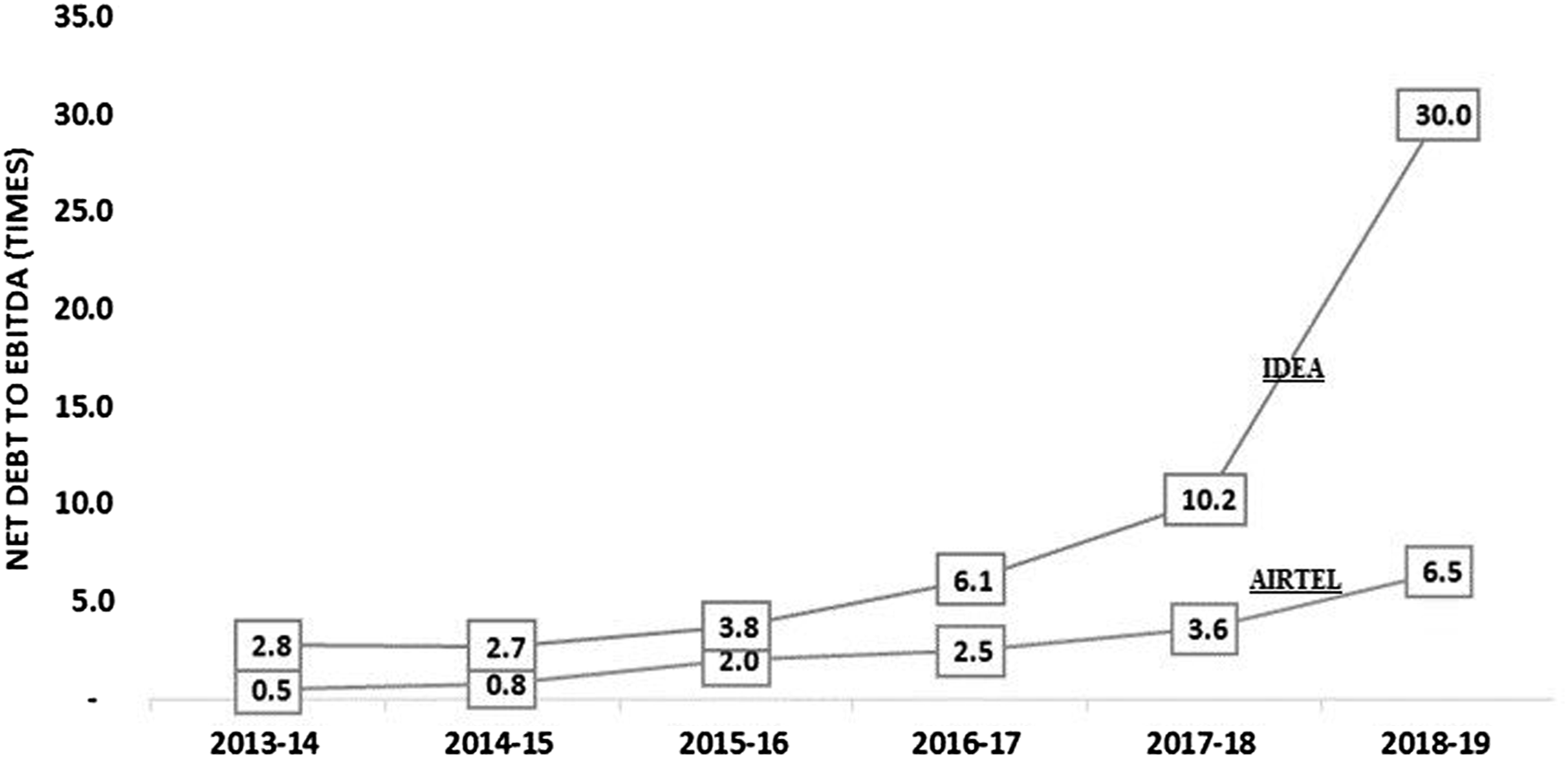

Researchers are addressing several issues, both organizational and environmental, concerning the telecom industry. High-speed internet services have disrupted the digital world through service unbundling and decoupling (Montero & Finger, 2017; Teixeira & Jamieson, 2014). The disruption is propelled by the online business models adopted by several players, and with the advent of Web 2.0, data consumption is centered around applications, video-sharing, social networking sites, and blogging. Decoupling has altered consumer spending patterns that have affected the revenue of the telecom players, as shown in Figures 1, 2 and 3. Messaging (in trillion–per year) (MNS Consulting, 2017). Net Debt to EBITDA ratio (Idea Cellular Services Limited, 2015, 2016; Reliance Industries Limited, 2018, 2019). Revenue trends of GR & AGR in Access Services (TRAI, 2020a).

In the last ten years, the revenue gained by the telecom players through telephone calls severely dropped as customers started using the OTT communication platforms such as Skype, Telegram, and WhatsApp. Also, the text messages service revenue got affected by messaging apps (Seth, 2022; Teixeira & Jamieson, 2014). Figure 1 depicts this continuous decline in the SMS count in overall messages in India and an exponential increase in IP message count facilitated by OTT players. Similar disruption is observed in Europe, Latin America, and Africa. For instance, during the same period, SMS traffic reduced to 19.7% in Kenya due to adopting OTT communication services (Sawe, 2016).

Role of TSPs/OTT in coupled and decoupled environment (Source: Authors’ own).

OTT and telecom services have nearly identical underlying technical architecture but have different reach, business models, and regulations (Bertin et al., 2011). Krancke et al. (2012) argued that regulation must envisage the entire digital value chain and ensure a level playing field among regulated and unregulated competitors. Allouet et al. (2014) emphasized that an unlevelled playing field between TSPs and OTT players created an imbalance in terms of the inability to provide consumer protection, efficient law enforcement, and taxation by the former. This prompted policymakers to craft rules that complement the pace of technological advances.

The telecom industry has been historically hailed for the efficiencies and cascading economic development that it stimulates and is directly linked with the economic development of nations. However, the incumbent TSPs are increasingly finding their business challenged by unregulated over-the-top (OTT) service providers who offer competing communication services, often free of cost to end customers (TRAI, 2015). While regulators, in most cases, were successful in their pursuit of regulating the industry over the previous technological advancements timely, the increased speed with which the decoupling phenomenon found its way did not allow the regulators to take the corrective measures and left the telcos to face this competition on their own.

In order to cope with these challenges, telcos had to re-think their strategies to achieve sustainability. Ries & Trout (2005), while describing the marketing and business strategy of the companies facing competition, advised the companies not to be a hero. “The biggest mistake marketing people make is failing to appreciate the strength of a defensive position.” Since TSPs were the leaders in the voice/SMS communication industry and according to Ries & Trout (2005), only a marketing leader should consider playing defensive, and the best defensive strategy is to attack. The organizations may note that an attack from a competitor would take time, and the bottleneck for the competitor to reach the customer is not the product/service, but the communication to all their consumers that takes a considerable amount of time. The defending organizations could make use of this time to mitigate the attacker’s sales message and to remain alert to all the potential threats arising from any direction.

To meet the technological challenges posed by OTT players, GSMA developed Rich Communications Services (RCS) to standardize rich multimedia communications across diverse communication service provider networks but in a coupled manner. GSMA promoted RCS as the service providers’ way to combat OTT threats. However, RCS was not widely embraced by the TSPs and failed to become a commercial platform on a larger scale. On the voice front, since Voice of LTE (VoLTE) worked on a 4G data network, the cost of providing VoLTE was considerably low compared to the traditional telephonic voice service, and thus the operators could provide free voice services over the VoLTE network. India witnessed the use of VoLTE by only a few telcos to defend themselves and to disrupt the market by providing free voice over the VoLTE network, thereby adding to the misery of the other operators already defending themselves from the free voice from OTT players.

Challenges from new players and technologies are a feature of every industry, and the telecom sector is no exception. Every challenge generates a unique response. Historical evidence proves that the failure to satisfy market needs will eventually lead to the emergence of stakeholders from outside the industry to fill the gap. If there is a need for a service currently not provided by those best equipped to provide it, someone else will come along to fill that need. This is what occurred in the case of railroads (Levitt, 1960), SLR film cameras (Lucas & Goh, 2009), and even SMS (Heinrich, 2014). When disruption causes irreversible decoupling, the organizations can rebalance their revenues by ensuring a dual role between value-creating and capturing activities. Other factors also cause a reduction in financial health, such as increased capital expenditure, changes in pricing methods, reduced subscriber growth, and increased competition (Teixeira & Jamieson, 2014). In response to OTT voice, the launch of entirely free voice service on the back of VoLTE technology in the year 2016 caused a shift of revenues from voice to data. This disruption is proved by the declining voice ARPU and rising data APRU during the year 2017 (TRAI, 2019a).

Gradually following the innovative operators, other operators followed suit and launched free or unlimited bundled packs, causing the data revenue to surpass the voice revenue. While the voice and SMS revenue decreased from 61% in June 2013 to 14% by Dec 2018, data revenue increased from a meager 8% in June 2013 to 53% in Dec 2019 (TRAI, 2019a). This revenue decline was reflected by decreasing mobile ARPU and Return on Capital Employed (ROCE).

Net Debt to Earnings before Interest, Taxes, Depreciation, and Amortization (EBITDA) ratio increased during the transition period (Figure 2). This could result from increased debt or decreased EBITDA levels. The rising Debt to EBITDA ratio makes it difficult for the industry to service fixed obligations. Figure 3 presents the Gross Revenue and Adjusted Gross Revenue of access services in the Indian telecom sector that decreased during 2014-2019.

The Industry AGR decreased from Indian Rupees 155 (‘000 crores) in FY 16-17 to Indian Rupees 103 (‘000 crores) in FY 2018-19, a reduction of approx 34%. Similarly, the Industry’s gross revenue decreased by approx 20% during the same period (TRAI, 2020a). This diminution was primarily due to intense competition in the sector since the entry of a new entrant operator in 2016.

This industry data shows that such an exponential rise in data usage has not resulted in a proportionate increase in the TSPs’ revenue due to a substantial reduction in tariffs and the advent of bundled packs since the entry of a new operator in 2016. The telecom industry is concerned about the growth of OTT communication players and the regulatory imbalance between the telcos and OTT. However, little literature is available on exploring various factors related to the decoupling of networks & services. There was a need to conduct an exploratory study to gain a better understanding and holistic picture of various factors that resulted in and increased the process of disassociation of networks & services. Therefore, this research tries to address the following research questions during various stages of the study – 1) What are the critical factors related to the disassociation of networks & services? 2) How has the latest technology adoption led to the disassociation of networks & services? 3) How does the disassociation of networks & services affect the growth of OTT communication service providers?

Research design

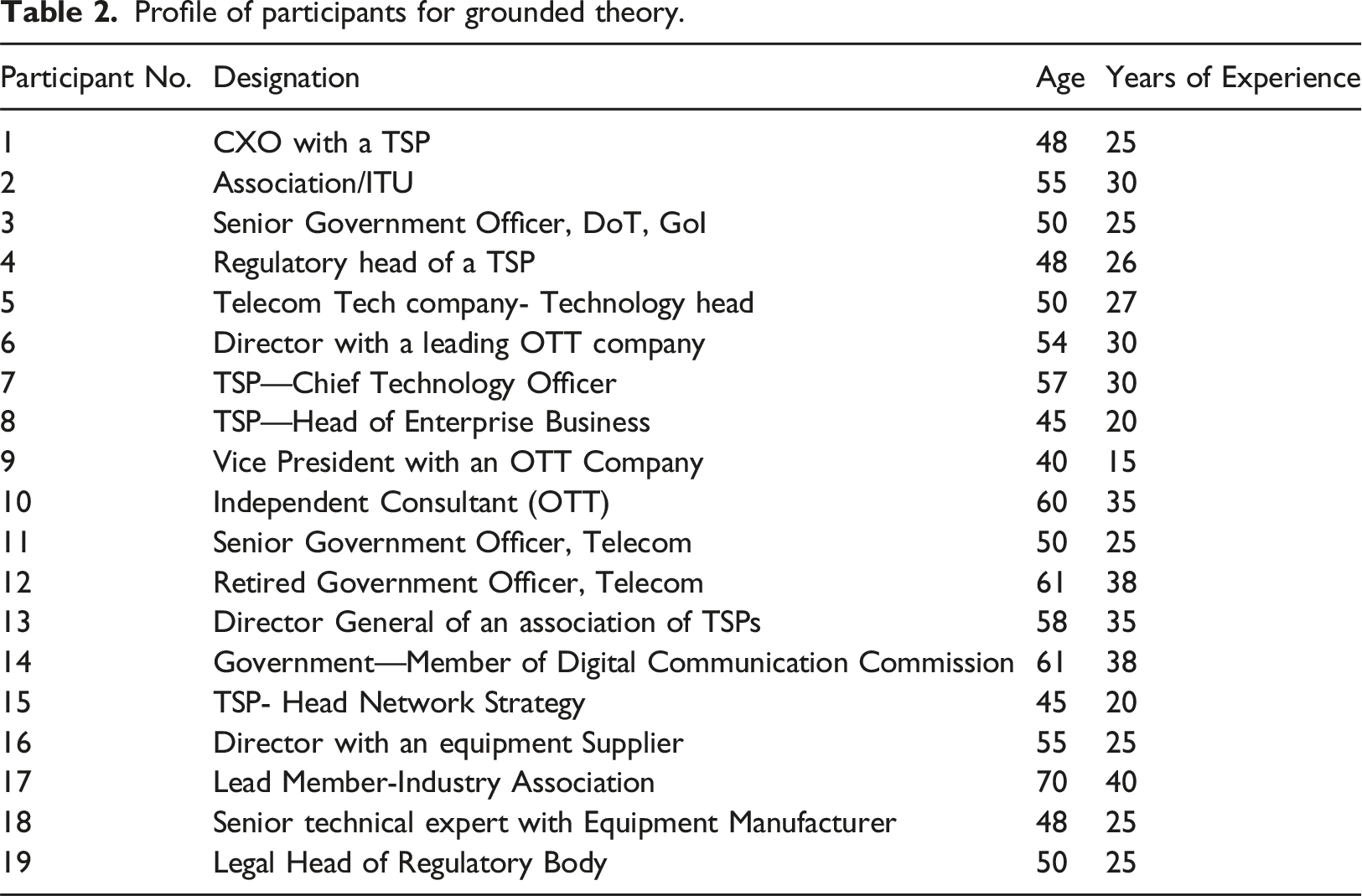

We conducted a grounded theory-based exploratory study (Strauss & Corbin, 1998) and developed a conceptual paradigm explaining the role of decoupling and factors affecting the Indian telecom sector. The conditions, effects, and strategies in response to the dissociation of communication and data services from the access network in the Indian telecom industry could be best understood through the opinion of the persons who had the domain’s experience and had been part of the industry. Therefore, we adopted a non-probability sampling technique and judgment criteria to select the sample for the study. We couldn’t identify any literary work that provided a framework explaining the causes and effects of this disassociation phenomenon on the Indian telecom sector. Therefore, framing a research hypothesis was impractical without enough literature on the factors. Grounded theory seemed to be the most appropriate technique since it helps develop a conceptual structure where no such framework is readily available (Glaser & Strauss, 1967). Several researchers have widely used and advocated expert interviews for qualitative research (Greener, 2008; Strauss & Corbin, 1998; Yin, 2009). This study called for systematically exploring the factors by conducting in-depth interviews with industry experts.

Sampling plan

Profile of participants for grounded theory.

Data collection

The in-depth interview process was conducted using a semi-structured questionnaire. A set of open-ended questions was prepared. The participants gave informed consent to participate in the study and allowed the conversation to be recorded. The transcripts of the interviews were iteratively analyzed while conducting the data collection process in parallel. A constant comparison method was deployed to generate open codes. Memos were also developed for the interviews. Miles & Huberman (1984) state that the data collection and analysis should overlap as it enables the researcher flexibility and opens up new ideas that emerge. Theoretical saturation (Creswell, 2007) was achieved after conducting nineteen interviews when no new codes were generated during the analysis.

Data analysis

Open coding

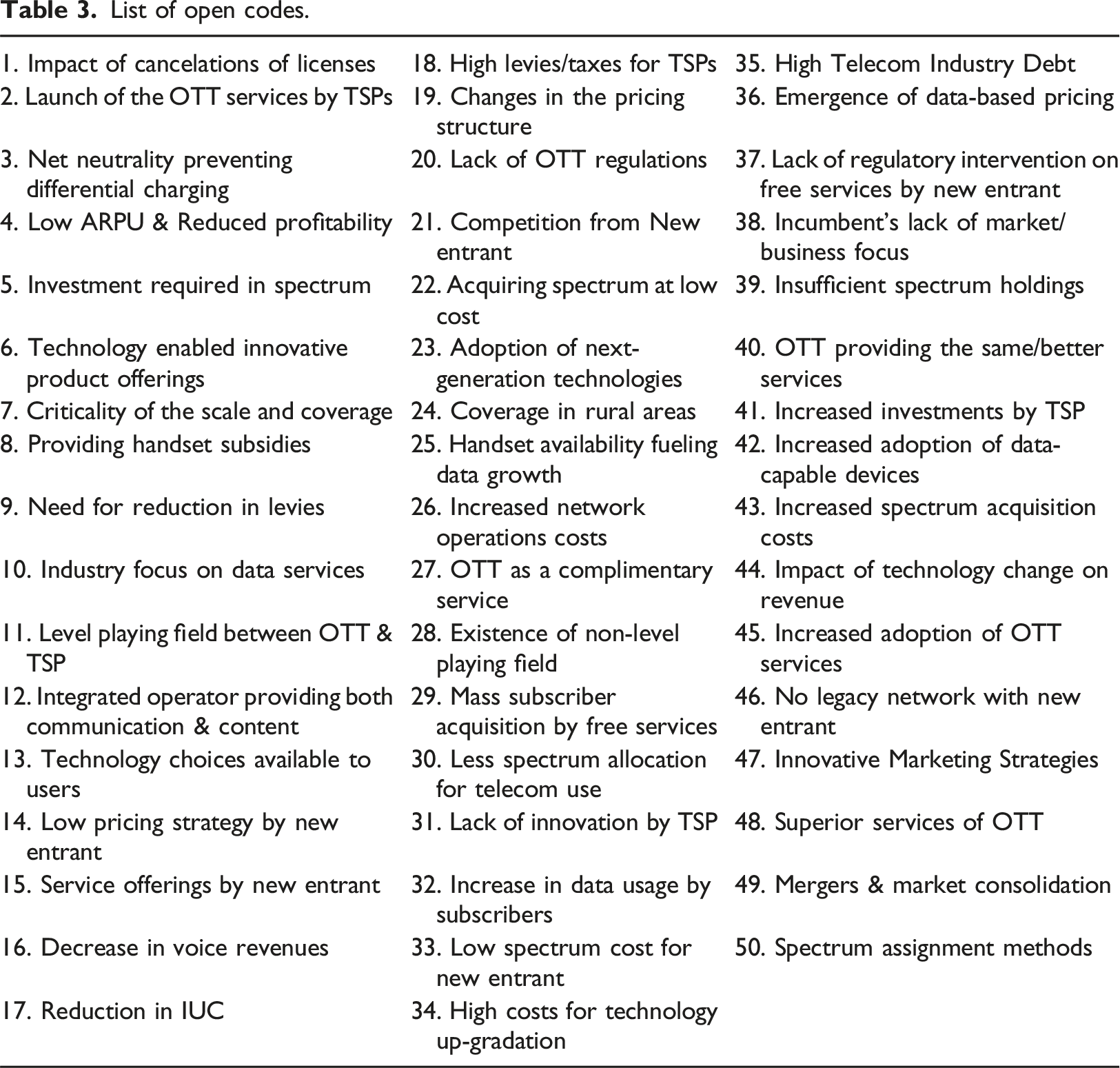

The analysis involved open and axial coding to determine the factors set. MAXQDA software was used to aid in data analysis and visualization. Open coding involves giving a descriptive name to every thought unit or essential section of the transcript. A total set of 233 open codes were identified, with 782 coded segments.

Axial coding

The open codes are grouped based on similar conceptual categories and their typical properties in axial coding. An identified central category would describe the key features of the phenomena. Eight axial codes were identified in the study. Axial coding involves relating the subcategories to a category through an inductive and deductive thinking process (Strauss & Corbin, 1998).

Selective coding

The final step in the coding process is selective coding, which involves interpreting the axial codes and identifying the core category. The process would help the researcher to gain insights and reduce the data into concepts and a set of relational statements (Strauss & Corbin, 1998). We used the coding paradigm as a tool for selective coding (Strauss & Corbin, 1998) that includes explaining all identified codes in the axial coding step-wise and arriving at the core category. Along with the central phenomena, the causal conditions, context or intervening conditions for the strategies, action/interaction strategies, and consequences of strategies are described.

For analysis, an extensive literature review was initially conducted to understand the decoupling and to have a certain degree of theoretical sensitivity before the actual data collection process. From the literature, we found the proliferation of OTT applications and their adoption by subscribers as a factor for decoupling phenomena. However, the literature review also identified certain other key influencing factors of the phenomena. This study was conducted with no preconceived notions to ensure minimal researcher’s bias. The learnings from the literature review were used to frame specific guided questions during the interviews.

List of open codes.

List of Axial Code Categories.

Results and discussion

In the form of axial coding outcomes, the disassociation phenomenon and the associated factors that facilitated it in the Indian context were identified (Table 4).

Technology evolution and adoption

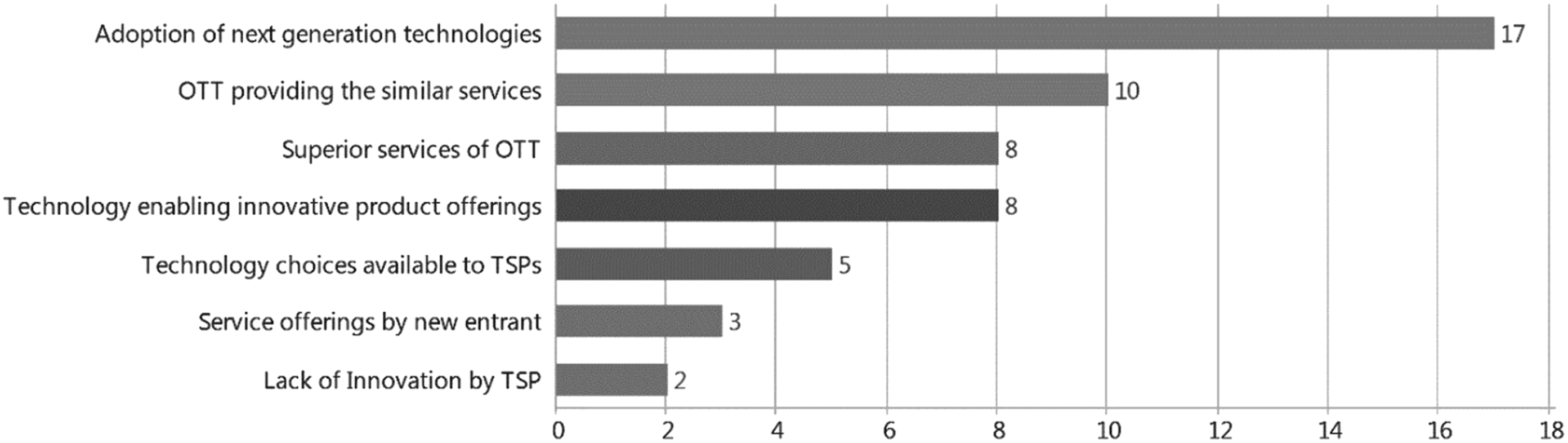

Adopting the next-generation technologies, communication, other services of OTT, and technology-enabled innovative product offerings were identified as the key contributors towards the technology evolution-led decoupling or disassociation phenomenon. The code -sub-code model presented in Figure 4 highlights the frequency of interview segments attributed to each open code connected to the axial category. The technology’s evolution and adoption resulted in the deployment of high coverage and capacity data networks that enabled the OTT players to create various services over the data networks. This ability to create independent services over the data network led to the rise of OTT applications, accelerating the telecom industry’s disassociation phenomenon. The frequency chart (Figure 5) shows the number of participants specifying the sub-codes in their interviews. Code-Subcode model for “Technology Evolution & Adoption”. Participant count in “Technology Evolution & Adoption”.

Financial stress

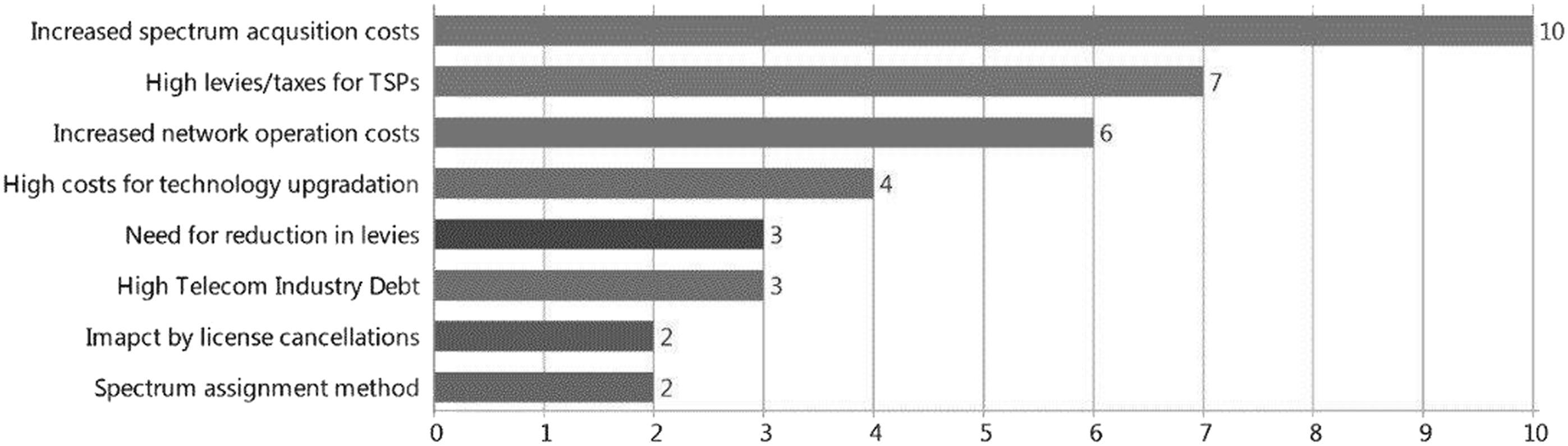

The adoption of more efficient mobile technologies (such as 4G) resulted in a significant reduction in data costs. The advent of new competitors posed a severe threat to existing service providers who relied on their voice-centric business model. On the other hand, the network up-gradation required to stay competitive would need huge investments that, coupled with increasing spectrum costs, burden the sector’s financial health. The code-subcode model and frequency of participants who discussed this category are shown in Figures 6 and 7, respectively. The increased spectrum acquisition costs were cited as the primary reason for financial stress. Several respondents cited the high taxes and levies, increased network operation costs, and high cost of technology adoption resulting in poor financial health. The increased operational costs and capex requirements resulted in high debt levels. Code-Subcode model for “Financial Stress”. Participant count for subcodes in “Financial Stress”.

Shift from voice to data pricing

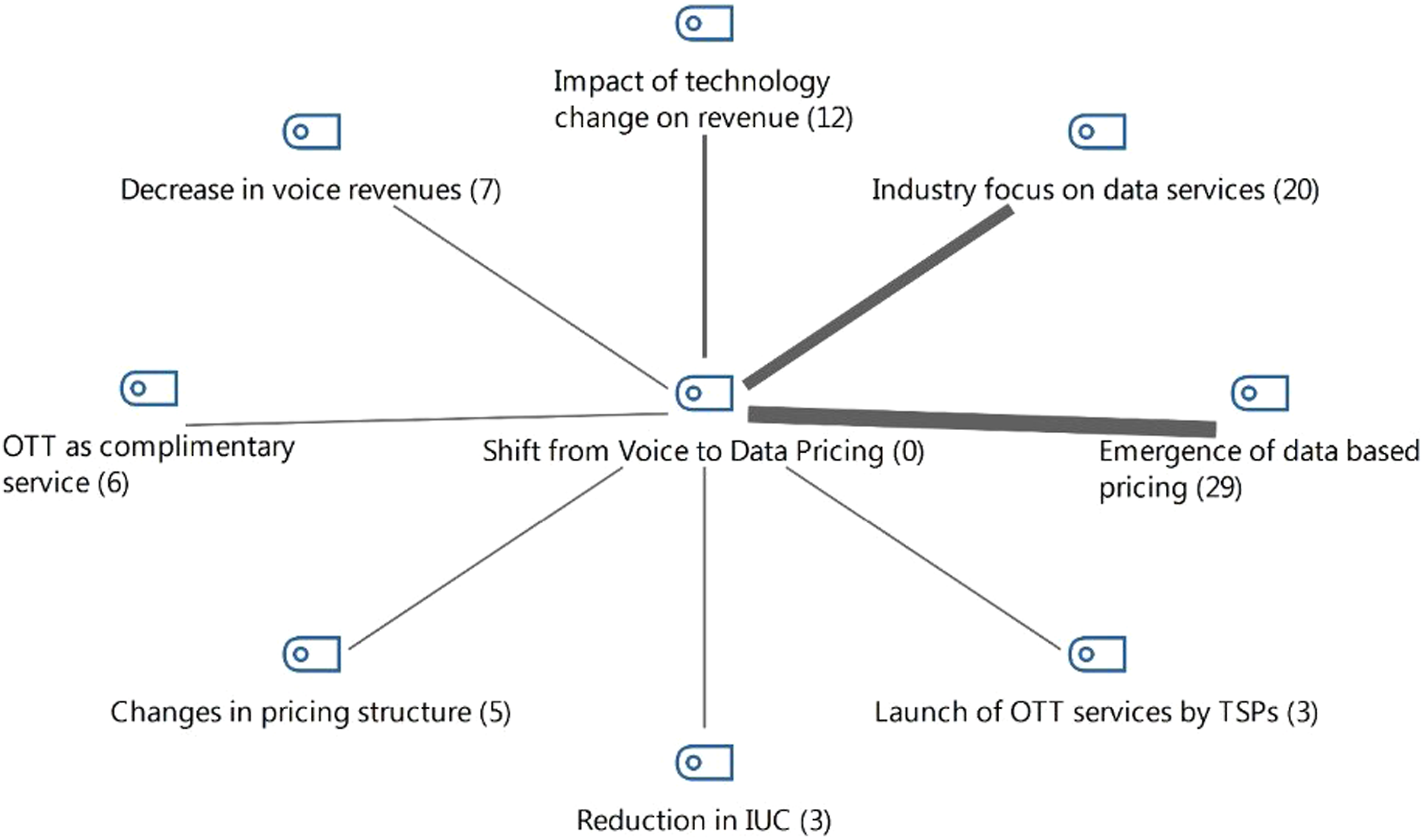

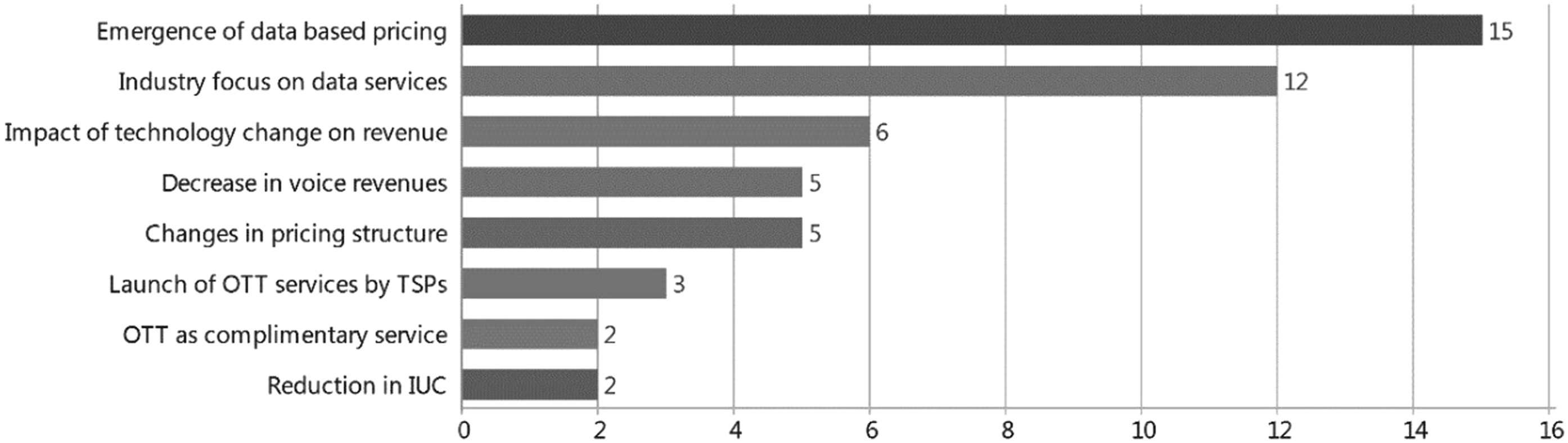

With the advent and adoption of new technologies, the industry shifted from voice to data services. During the 2 G/3G era, the telecom industry was primarily voice-centric, with around 80% of its revenue coming from voice services (TRAI, 2016a, 2017). With new technology supporting higher data speeds on mobile devices, consumer preferences shifted towards data resulting in increased data usage. Over the years, the increased adoption of data services contributed to shifting business models and pricing from voice-centric to data-centric pricing. This pricing shift was inevitable as many factors contributed towards this change, including the “emergence of data-based pricing” and “industry focus on data services.” The code-subcode model and frequency of participants mentioning these factors are depicted in Figures 8 and 9. The industry focus was shifted from a voice-centric to a data-centric view as the data services become the main product of telecom service providers. Participants explained that data consumption was on the rise due to emerging OTT applications and affordable rates of data services. This consumption behavior caused reduced price realization of voice services. Further, reduced interconnection usage charges (IUC) were also cited as a cause of shifting from voice to data-based pricing. Code-Subcode model for “Shift from Voice to Data Pricing”. Participant count in “Shift from Voice to Data Pricing”.

Regulatory forbearance

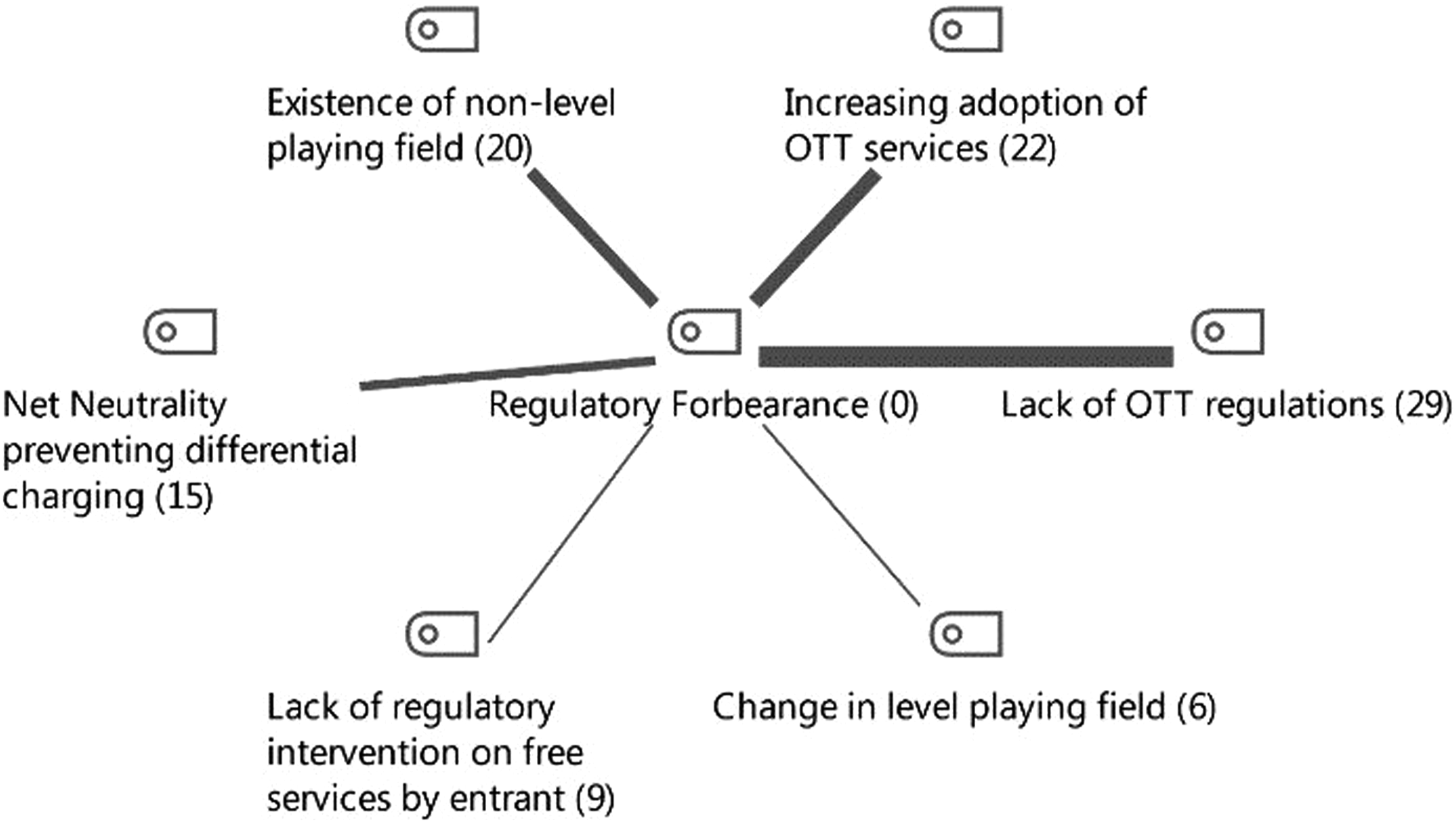

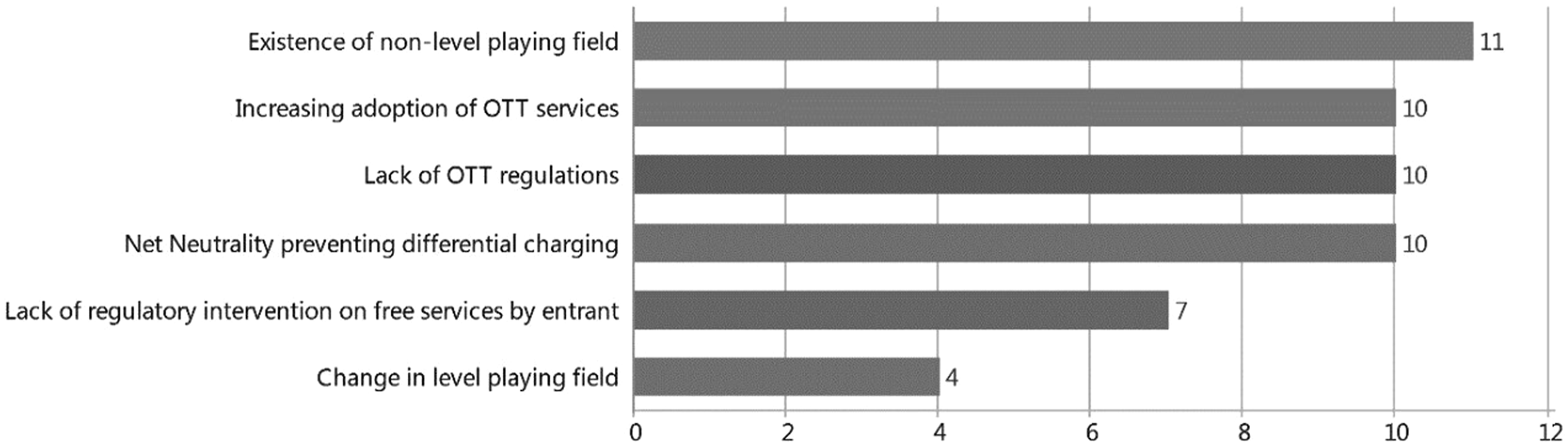

Globally, the regulator’s role is critical to any sector’s development. The regulator’s actions may, on one hand, help create new business opportunities and, on the other, impede the sector’s growth. Similarly, the forbearance by the regulator would also be detrimental to the industry, especially when the industry expects them to provide an indiscriminating encouragement to their investments amidst the competition from the unregulated sector (OTT Players) who have specific cost advantage and have the potential of exploiting the network supported by the TSPs by displacing their service revenue. Further, the regulator’s forbearance against completely free voice tariffs by a new entrant can also cause financial stress in the sector. Figures 10 and 11 highlight the code-subcode model and frequency of interviews discussing this category. The participants viewed the lack of OTT regulations as regulatory forbearance, creating a non-level playing field. While the telecom players were subject to stringent license conditions and levies, there were no such obligations on OTT players. The participants cited that net neutrality regulation further widened the non-level playing field. The net neutrality regulation does not allow TSPs to charge/recoup for the loss caused due to displacement of voice/message traffic to the OTT players that use only the data services provided by the TSPs. Code-Subcode model for “Regulatory forbearance”. Participant count for subcodes in “Regulatory Forbearance”.

The participants' most cited elements of regulatory forbearance were the existence of a non-level playing field, lack of OTT regulations, and compliance to the principles of neutrality. The participants also cited that the lack of regulatory intervention during the entry of new operator resulted in a “competitive imbalance,” causing a massive loss of voice/messaging revenue.

Hyper competition by new entrant(s)

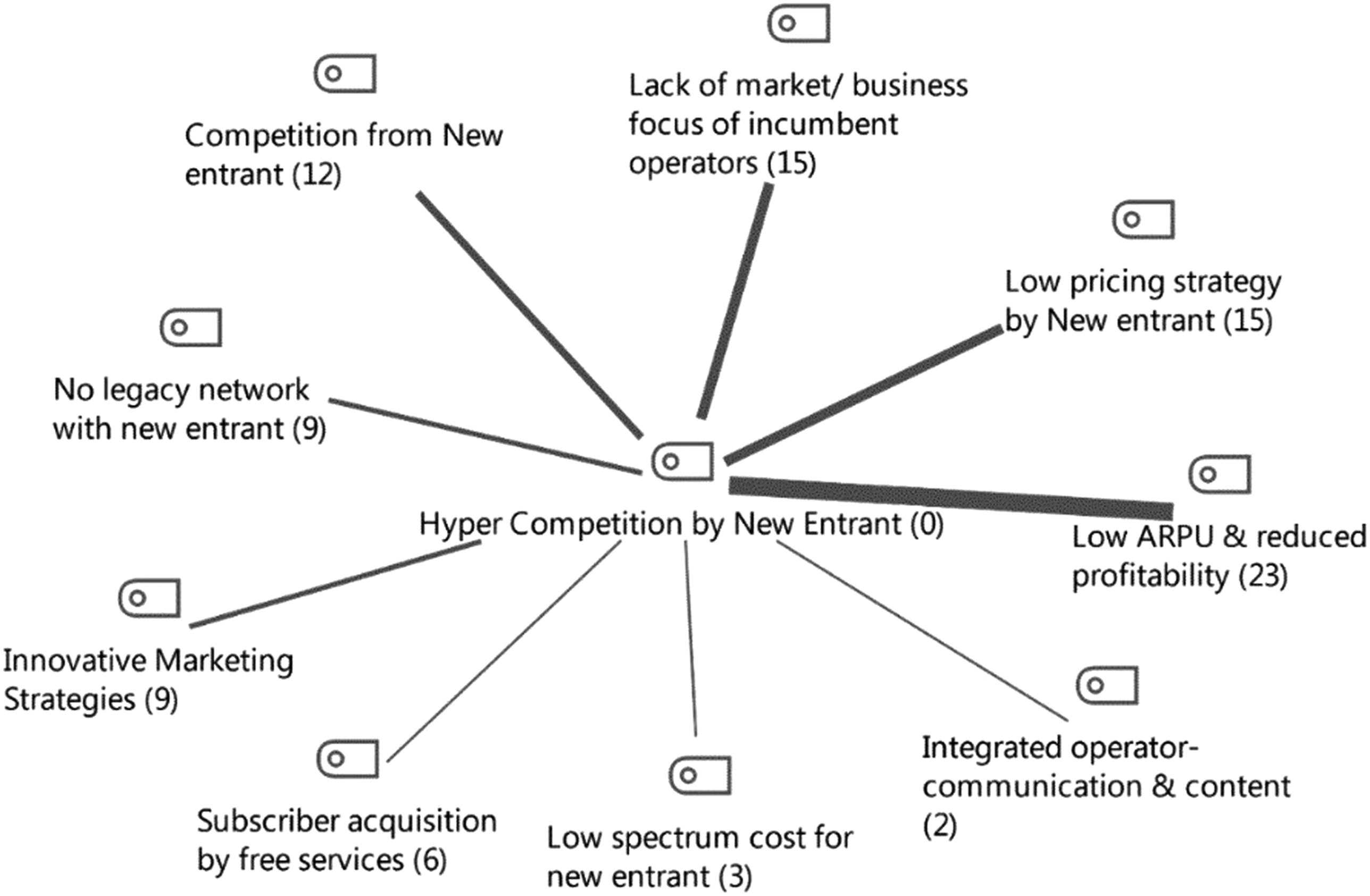

In any competitive market, a new entrant would create a certain level of disruption, and the telecom sector is no exception. However, the magnitude of this disruption was very high in the Indian telecom industry as observed by the dismal financial condition of existing players, which forced them to align their business models with the business strategy of the new entrant. The pricing strategy adopted by the new entrant was to focus on charging for data only. Further, nil investment in 2 G/3G networks helped the new entrant reduce network costs, as compared to the existing players. The new entrant focused on a data-centric business model with a free voice, forcing the other operators to follow the same pricing philosophy. Code-sub code model and participant frequency for each subcode are shown in Figures 12 and 13. Code-Subcode model for “Hyper Competition by New Entrant”. Participant count in “Hyper Competition by New Entrant”.

Low ARPU & reduced profitability, low pricing strategy by new entrant, and lack of market/business focus by incumbent operators were cited as the reasons for hyper-competition from new entrant. No legacy network, low spectrum cost for the new entrant, subscriber acquisition by free services, and innovative marketing strategies were cited as the advantages to the new entrant.

Competition in any sector is essential, which results in providing best-in-class services at reduced prices. Privatizing the telecom sector resulted in competition in the sector, which the state agencies once controlled. But in the last decade, the existing TSPs were subject to competition not just from the OTT players, who provided similar communication services, but also from a new entrant in the telecom market who changed the pricing model of the industry from voice to data, before the other operators changed their technology to support such changes. The strategies of the new entrant and competition from OTT players resulted in low ARPU and reduced profitability for the then-existing TSPs.

Consolidation and network growth

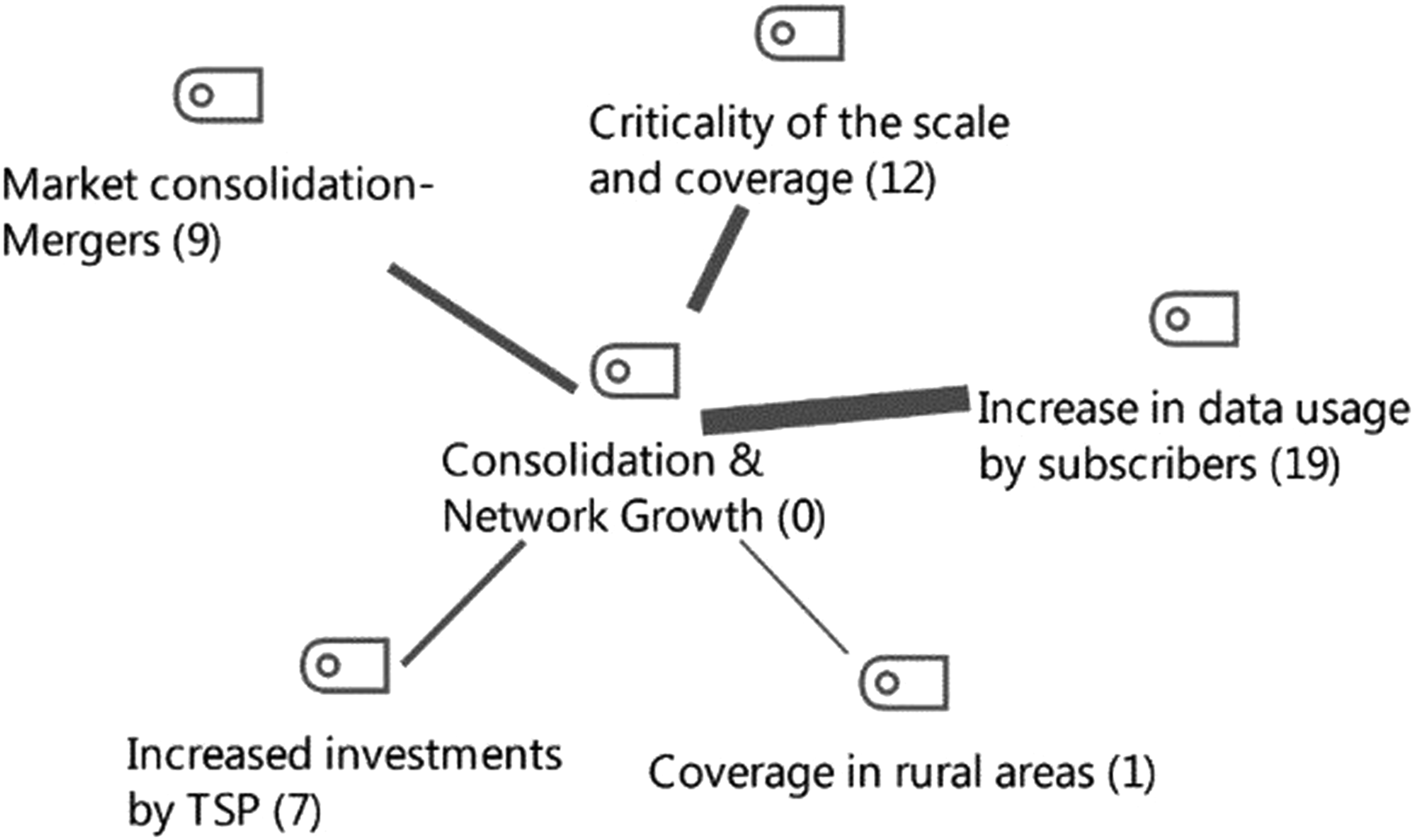

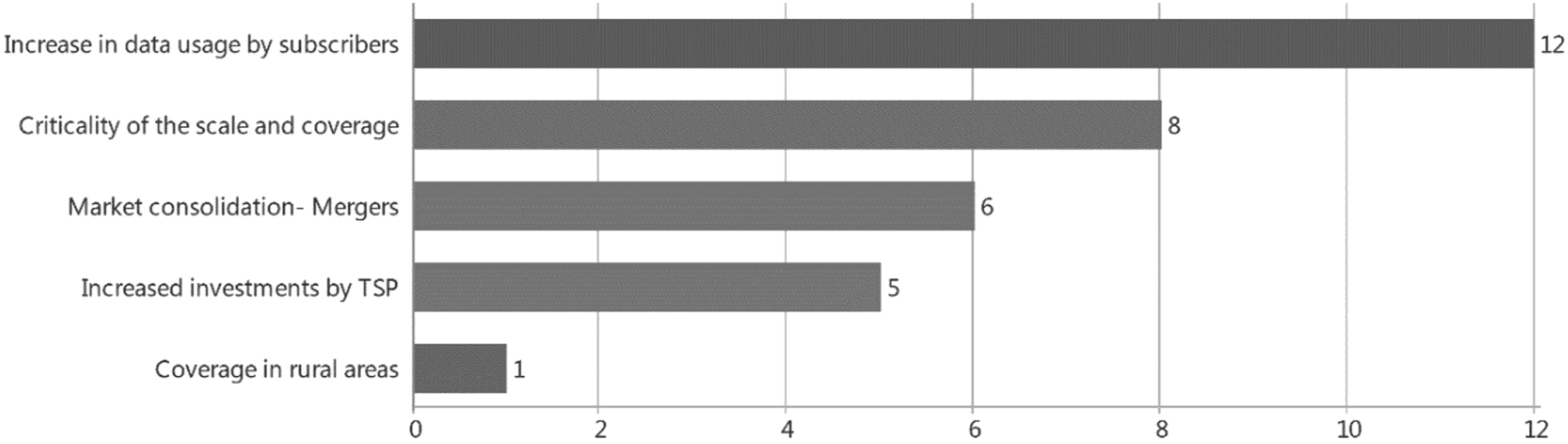

In a competitive market, every player would like to hold their market share and aim to increase their subscriber base and profit by reducing costs. Network growth achieved through economies of scale presents a basic understanding of the market structure. A perfect competitive environment exists when the economies of scale for the organization exhaust at their output level (Panzar & Willig, 1977). This category’s code-sub code model and participant frequency for each sub-code are represented in Figures 14 and 15. Code-Subcode model for “Consolidation & Network Growth”. Participant count for “Consolidation & Network Growth”.

Increased data usages by subscribers and criticality of scale and coverage form an important strategy adopted by a new entrant player that launched the 4G services on a pan-India basis in a single phase, achieving low cost due to a more extensive network from the beginning itself. To compete with a large-sized pan India network, the highly fragmented telecom market resulted in consolidation through merger and acquisition to meet the criticality of scale and coverage that would require significant investments. This changed the competitive landscape dramatically.

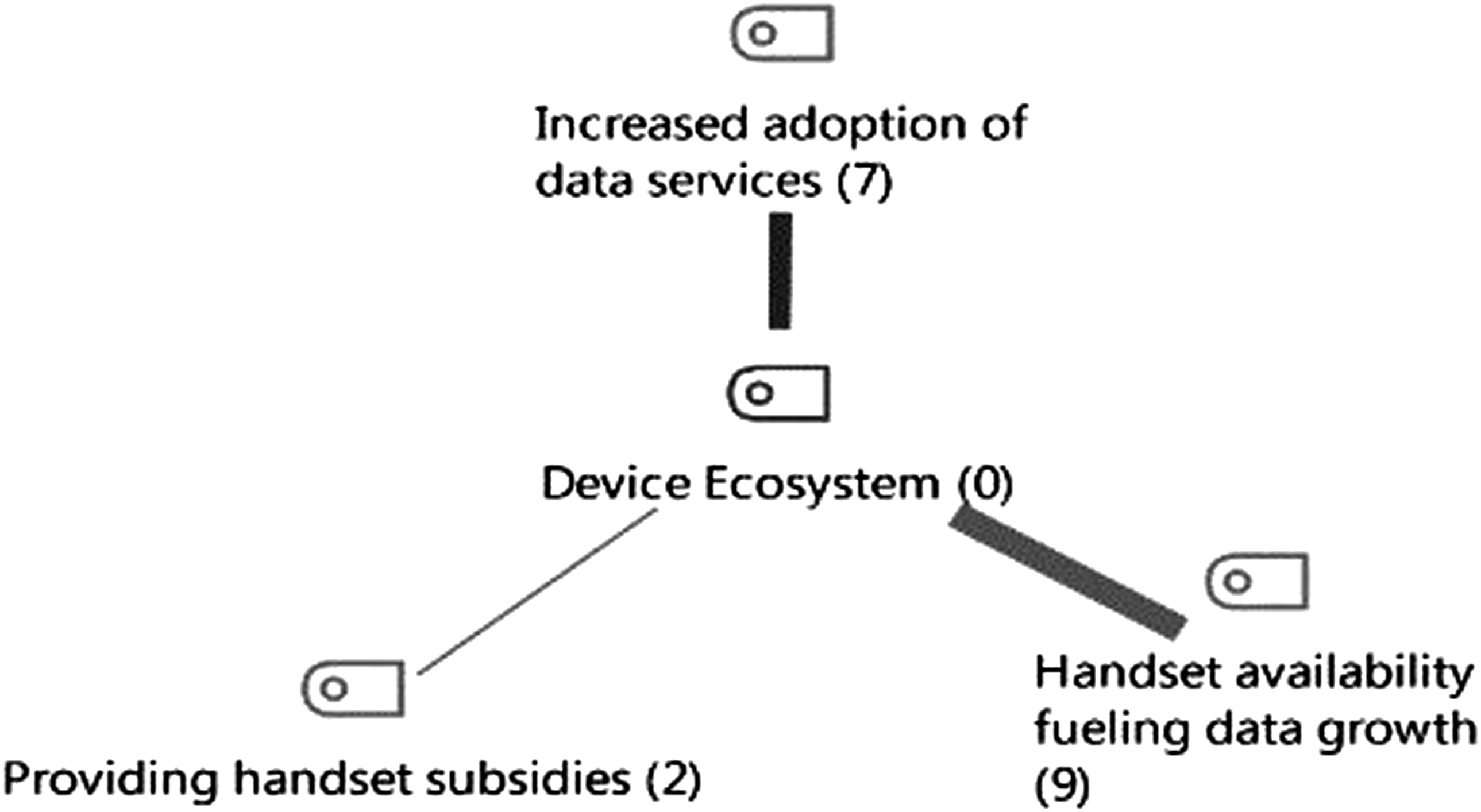

Device ecosystem

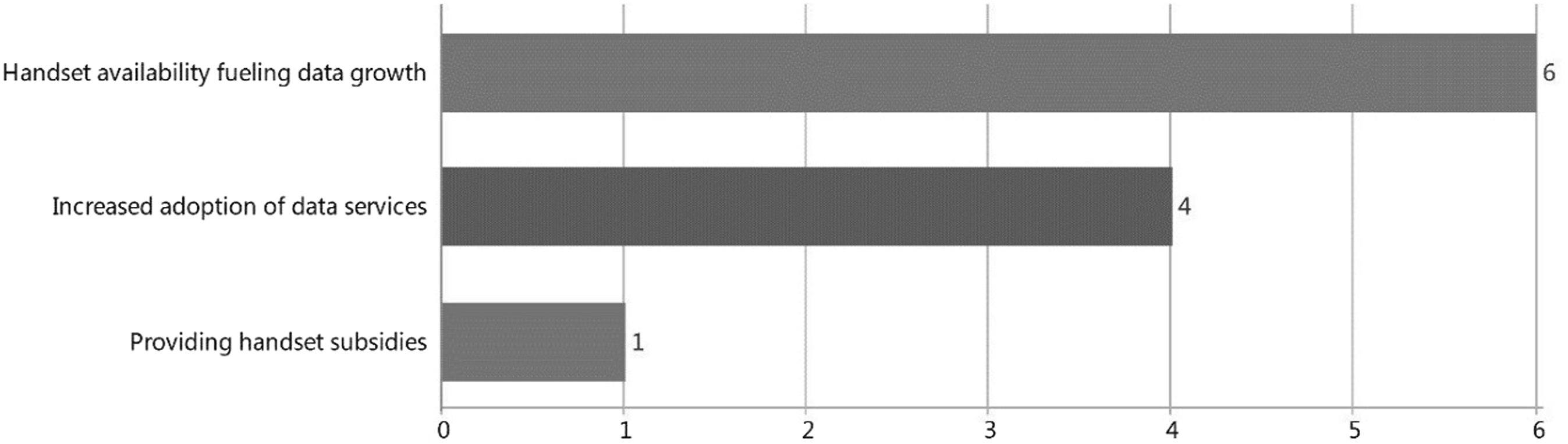

The availability of handsets/devices is critical in the telecom value chain. The penetration of suitable user devices/handsets determines the proliferation of digital services. Affordability is critical for customers to adopt a technological innovation by the masses. Code-sub code model and participant frequency for each sub-code are shown in Figures 16 and 17. The participants linked the data growth to the availability of affordable handsets that directly relate to the increasing adoption of data services. They stated that the availability of a low-cost 4G handset also facilitated the rapid uptake of data services by enabling them to migrate from 2G to 4G. Code-Subcode model for “Device ecosystem”. Participant count for subcodes in “Device ecosystem”.

Providing handset subsidies by the TSPs helped them acquire 4G subscribers, which also added to the financial burden on TSPs.

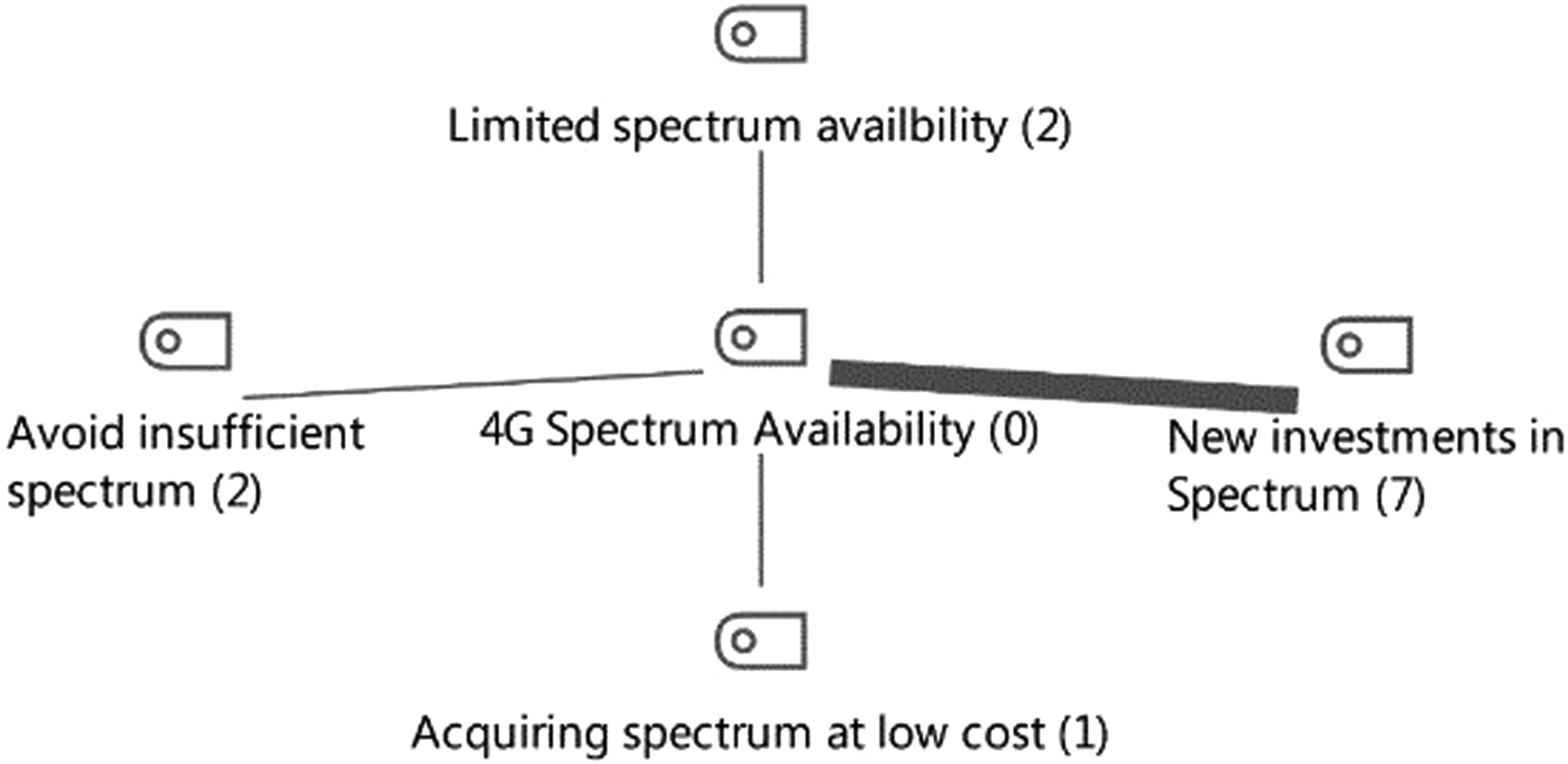

4G spectrum availability

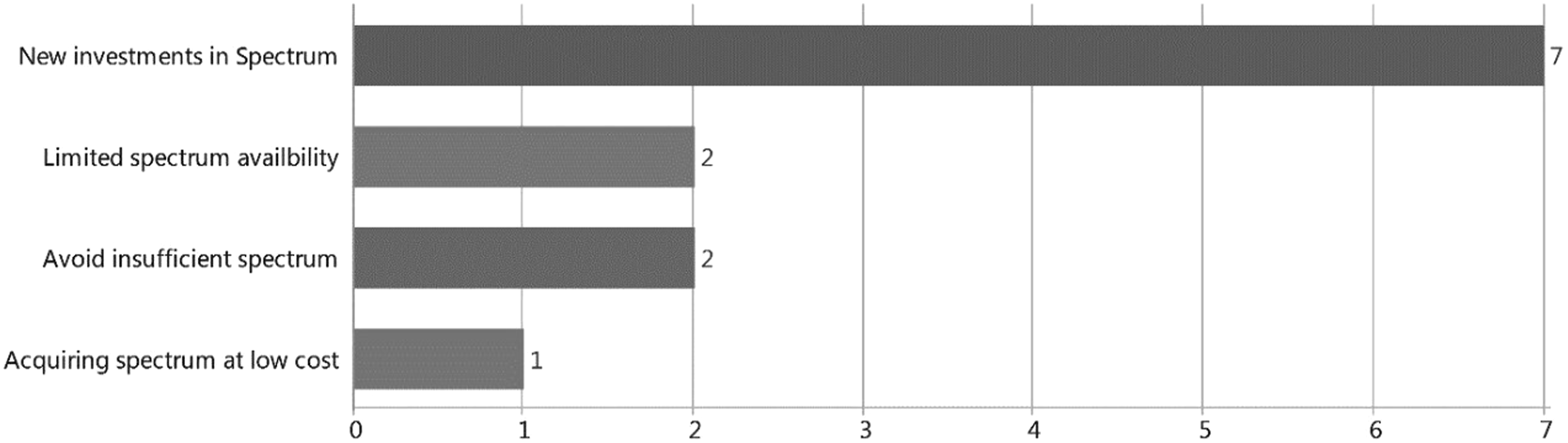

Spectrum is the most critical resource for offering mobile services. The TSPs use license spectrum to offer voice & data services to the customers. Code-sub code model and participant frequency for each sub-code are shown in Figures 18 and 19. Participants cited that increased demand for data services during the decoupling phase required the TSPs to make new investments in acquiring more spectrum at an affordable cost for their sustenance. A lack of investment in the 4G spectrum resulted in a limited capacity and geographical presence, reducing the TSP’s ability to counter the competition from the new entrant and OTT players. Code-Subcode model for “4G Spectrum Availability”. Participant count for subcodes in “4G Spectrum Availability”.

Further to the emergence of the axial categories, selective coding was carried out to integrate these categories for refining them into a theory that helps in understanding the main category describing the central phenomena. The selective coding process involves a description of central phenomena wherein the relationships between the core category and the other categories are explained. A paradigm model is constructed at the end of this process that shows how the linkages are classified as casual conditions, strategies, consequences of strategies, and intervening conditions of the strategies (Strauss & Corbin, 1998). In the quest to understand the decoupling phenomenon, the respondents were asked questions on key factors that resulted in the decoupling phenomena. During the study, it was identified that the participants cited “Technology Evolution and Adoption” as a key factor resulting in decoupling, as shown to be the central phenomenon in the paradigm model (Figure 20). Central phenomenon and its relationships with other categories/codes.

The technological evolution in the Internet’s space has blurred the physical boundaries and redefined how businesses operate. The networks have become increasingly virtualized, resulting in a substantial cost reduction. The technology evolution has enabled the delivery of services using all data/IP networks. A few instances of the interview segments that highlight these findings are- • “Adapting technology to 4G, moving from CS/SDH to all IP” network and continuous evolution of the network to make it efficient for data services” (Participant 15) • “New technology changed the cost of the providing services, ability to provide new services and improving the quality of service” (Participant 6) • “Rapid technology transformation from 2G to 3G to 4G” (Participant 4) • “Network virtualization has also opened up the possibilities for adding new network services, especially in the Enterprise space” (Participant 5) • “Re-design of networks to an all data/IP based network design, leading to increased efficiencies and lower costs” (Participant 13)

The technology adoption resulted in deploying all IP networks where the services provided to the end subscribers are no longer coupled with the data network. The changes in technology have resulted in the telecom service providers losing their power in the value chain, whereas the OTT players have been playing a significant role by developing and providing their communication services. • “As a result, Telcos moved further down in this value chain.”(Participant 5) • “as the OTT service providers have developed their own voice and messaging APPs making the MNOs network for these services redundant.” (Participant 11) • The superior and more flexible services of OTT and its ever-increasing customer adoption have led to the sustenance of the decoupling phenomenon resulting in revenue loss to the telecom service providers. • “it was clear that OTT products were gaining huge traction with customers and that the ‘marriage’ of OTT with 4G LTE could become a very potent force.”(Participant 17) • “Availability of high-speed internet has further encouraged OTT players to provide and enhance their services”(Participant 11) • “These applications do not have high data volume and hence do not yield to higher data consumptions of the user requiring to purchase additional data packs.”(Participant 15)

The technology evolution has resulted in the deployment of high-speed data networks and, thereby, a rise in OTT applications. The OTT applications with high-speed networks and suitable devices are no longer coupled with the network. Therefore, the communications services, such as messaging and voice, can be provided by OTT players in a wholly decoupled manner.

Understanding the relationships of the central phenomena with other categories/codes in the paradigm model provided further insights into the decoupling phenomena. The Indian telecom sector has seen technology-led decoupling of networks & services. As presented in the paradigm model (Figure 20), three categories were classified under the causal conditions for decoupling phenomena as stated by the respondents- (1) Device Ecosystem, (2) Regulatory Forbearance, and (3) 4G Spectrum Availability.

With increasing speeds of mobile data networks, OTT applications are gaining popularity. • “Entire telecom infrastructure is being created by telcos, and telcos bear the license fees & regulatory obligations, while OTT, being an overlay service, get away without any of these challenges.” (Participant 18). • “Absence of strict regulation for OTT service providers has further catalyzed the situation” (Participant 11) • “In the context of a licensing regime in India, the provision of voice and messaging services has led to an uneven playing field.”(Participant 13) • “Offering of subsidized handsets… Increasing subsidies for handsets to encourage customers to migrate from 2G to 4G” (Participant 13) • “but there was a challenge of having 4G enabled handsets for which they made huge efforts and succeeded in mitigating the risk very effectively” (Participant 6) • “Getting 4G feature phones for onboarding 2G subscribers from competitors” (Participant 15) • “They had the largest chunk of 4G capable spectrum that allowed them to build out both coverage and capacity layers.” (Participant 16)

The technology-led decoupling phenomena relate to specific categories which act as intervening conditions. The occurrence of hyper-competition by a new entrant as the intervening condition has either accelerated or decelerated the strategies taken by the organization to tackle the decoupling effect. Some coded segments explaining this are- • “Entry of a new Operator that offered voice for free, thus impacting 85% of the revenue stream of incumbent Operators” (Participant 10) • “Probably the competition among TSPs has hurt their revenue models more than the competition from OTT players” (Participant 3) • “Putting pressure on competition to serve voice on CS network, which had a very short-lived investment” (Participant 15) • “Financial Distress caused by the high demand of Free Minutes and Low-Cost GBs coupled with lack of a 4G Network Infrastructure” (Participant 8) • “The impact of technological changes has created a need for telecom operators in India to review business model” (Participant 4).

The strategies adopted result from the casual and intervening conditions identified for the core phenomena of the study. A strategy adopted by the organizations that affects decoupling phenomena is the “shift from voice to data pricing.” Some coded segments describing this are- • “Telcos’ main business is to sell connectivity. Earlier it was voice connectivity, and now it’s data connectivity” (Participant 6). • “Revenue from voice would certainly go down as more & more people shift to 4G and beyond” (Participant 19). • “Services like voice, SMS, became the byproduct which was offered free of cost.” (Participant 7) • “With new data based network and with pan India presence, voice traffic shifted to through data affecting revenues” (Participant 12) • “Though somewhat capital intensive, TSPs may develop their own OTT platform to launch their own OTT Services” (Participant 11) • “Bundle multiple connectivity products (mobile, wireline, vehicle, DTH) with converged network to increase customer stickiness and loyalty” (Participant 15) • “In the VoLTE free voice environment, this is an enormous benefit for the telcos. So both telcos and OTT players should therefore work toward a symbiotic relationship. That would be a win-win for all stakeholders” (Participant 17)

The consequences of such strategies adopted by the organization, coupled with the impact from the core phenomena, are (1) Consolidation & Network Growth and (2) Financial Stress. The instances of interview segments explaining these outcomes are- • “The revenue earned by Operators from the consumption of data by consumers who use OTT services do not compensate for the full cost of carrying these services on Operator networks” (Participant 13) • “VoLTE has allowed voice services to ride over data networks, as an application, leading to Operators offering voice services for “free.” This has led to revenue losses to incumbent Operators of over 30% over the past two years” (Participant 13). • “The telecom industry is undergoing a difficult transition from voice-centric to data-centric and will remain under pressure in the near term” (Participant 2). • “Clear vision with commitment coupled with minute planning of the state of the art technology with timely execution on pan India basis are the reasons for any new operator’s success” (Participant 12). • “Quickly expanding & modernizing their network to handle growth in data services” (Participant 18). • “The increasing usage also forces higher investments which is a double whammy” (Participant 9) • “Telco cannot sustain the business without having a substantial market share” (Participant 19). • “Accelerated Exits of the weaker players, and Industry M&A was a natural consequence, with the stronger players gaining scale and spectrum” (Participant 16)

The strategies adopted by telecom service providers during the technology-led decoupling phenomenon and the effects of causal and intervening conditions resulted in the exit of weaker players and the requirement of additional investments by the existing players to meet ever increasing demand for data services.

All the aspects related to the data-network disassociation phenomenon that has emerged from the study are supported by the literature as elucidated earlier. Summarizing the evidence, the financial reports of the Telecom Regulatory Authority of India indicate the financial health of the TSPs during the period 2016-2019 (TRAI, 2023a). The intense competition and low minutes of usage led to a decline in ARPU (TRAI, 2023c). As the technology evolved, 3G and 4G adoption enabled high speed and caused a steep rise in data consumption by mobile subscribers. On the other hand, the TSPs, which could merely earn from their traditional voice and messaging services (MNS Consulting, 2017), switched their pricing strategies from voice to data plans (Pandey & Kumar, 2018). Voice traffic gradually became free and bundled within data packs.

The OTT communication and media services have posed a severe threat to the existence of the TSPs. Some key TSPs vanished from the industry, while others coped through mergers. The telecom service providers reduced from 13 to 8 in number in three years (TRAI, 2016b; 2019c). TSPs being the investors in establishing the network architectures and purchasing spectrum and licenses, were no longer leveraging upon their communication services and were reduced merely to being the data transfer pipelines for the OTT players. Not yet governed by any regulatory mechanism, OTT players are under no such obligations. To discuss and contemplate the regulation of communication OTT services (Kochhar, 2022; PTI, 2022), TRAI has recently initiated a fresh consultation process, making way for some hope for the TSPs (TRAI, 2023d).

Concluding remarks

The findings of the research provide insights into the evolving technology-led decoupling phenomenon of the services from the network. The resultant coding paradigm from grounded exploration reveals the causal conditions, adopted strategies, the intervening conditions of the strategies and consequences of these strategies. 4G spectrum availability, evolving device ecosystem and regulatory dynamics of the telecom industry accompanied by hyper-competition generated by the new entrant were identified to lead to a shift in the business strategies. Pricing moved to data-driven plans, bundling free voice and SMS with the data. Telecom companies that could rapidly adapt their services with new technologies could leverage the disassociation in their advantage. The financial stress among the telcos, their network growth and consolidation were the outcomes of the competitive and regulatory dynamics between telecom operators and OTT players.

Historically, voice, messaging, and video services were tightly coupled with the physical layer of the telecommunication network. The telecom services providers (TSPs) were the exclusive providers of these services. TSPs charged their customers based on the usage of these services instead of the actual amount of data (bits or bytes) transferred over the physical layer while providing such services. Over-the-top capabilities have enabled the users to get these services from any third-party application platform while procuring only the data services from the TSP. This phenomenon led to TSPs becoming a dump pipe selling only data in bits instead of communication services. Net neutrality rules, framed to protect the content provider against any discrimination by telecom service providers, have effectively helped the OTT players from any hindrance, throttling, or differential charging for data used for OTT services. The availability of high-speed wireless networks has ensured a reasonably good quality of the OTT service, which otherwise was possible only in the services directly provided by the TSPs. Meeting higher data traffic needs by the customers’ calls for more investment by the TSPs for explanding infrastructural support and spectrum. Globally, the TSPs had been seeking regulator interventions to protect their revenues from being displaced by OTTs. Such displacement was due to the pricing arbitrage between the communication services provided by the licensed operations and those provided by the OTT players. GSMA had been running large-scale campaigns demanding “Same Service, Same Rule.”

TSPs had been requesting regulators for protection, such as disallowing the OTT players to provide communication services without a service license or asking them to pay the same levies as is being paid by licensed operators, or allowing TSPs to charge data differentially based on content. TSPs also intended to charge the OTT players to cover up the shortfall in their revenues caused due to displacement of their legitimate traffic to the OTT platforms. The absence of the required regulatory intervention left no option for the TSPs other than upgrading their networks to VoLTE and RCS messaging that supports OTT-like voice and messaging communication. Adopting these new technologies allowed the TSPs to move their pricing from voice/messaging to data and effectively compete with OTT players.

Though such developments have allowed the TSPs to position their services as a competing product to the OTTs, they have rendered the legacy 2 G/3G networks obsolete, much earlier than their life as many operators were still expanding their 3G operations around the country when the disruption happened. This transformation has forced the TSPs to retire their existing investments prematurely while making considerable investments in the 4G network, resulting in financial stress in the industry, as reflected by the declining revenues and rising debt. It is an ongoing issue as 5G networks are also being rolled out, displacing the incumbent technologies and offerings. The insights from this research show how the technological changes have caused a sudden collapse of the telecom industry’s primary revenue stream due to competition from internet companies in the technology space. The phenomenon can be related to the seminal work by Levitt (Levitt, 1960), marketing myopia. The factors related to decoupling communication services from networks in terms of the conditions driving it and the industry’s response include financial stress, the shift from voice to data economy, regulatory forbearance, hyper-competition, consolidation and network growth, device ecosystem, 4G spectrum availability, and technology evolution and adoption.

Limitations and future directions

The scope of the research was limited to the Indian context, which may be validated through case evidence in the future. Additionally, the findings are qualitative and interpretive in nature. Grounded theory gives rich insights into the grounded realities of the context but is limited by empirical evidence. In future, the applicability of the factors explored in the context of the telecom industry caused by technological disruptions may be verified for other regional markets and compared empirically.

Footnotes

Acknowledgements

The authors acknowledge the infrastructural support from the Indian Institute of Technology Delhi, India.

Declaration of conflicting interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: The First author has worked in the telecom sector for more than thirty years, both in the public and private sectors. However, the qualitative findings of the research are drawn on the actual performance of the Indian telecom industry, involving senior experts' opinions, and are validated through literature.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.