Abstract

FinTech ecosystems are growing at a rapid pace, creating large-scale, heterogeneous, and highly interconnected data environments that pose challenges to traditional frameworks for innovation management and decision support. Even while artificial intelligence (AI) is being used more and more to make use of this data, the majority of current methods are still opaque, reactive, and not well-suited to the needs of human-centered decision-making. In order to facilitate enterprise innovation in intricate FinTech ecosystems, this study suggests an explainable agentic AI-driven big data decision framework. The platform combines explainable big data analytics and visual analytics pipelines with autonomous AI agents that are capable of goal-directed reasoning, adaptive collaboration, and continuous learning. The suggested method permits transparent investigation of extensive financial, transactional, and behavioral data by fusing network-aware data modeling, agent-based decision orchestration, and interpretable machine learning processes. By converting agent recommendations into clear, traceable insights for strategic innovation planning, visual analytics interfaces further support human–AI co-decision-making. When compared with black-box AI models, the framework’s capacity to improve decision accuracy, adaptability, and trust is demonstrated through a case-driven evaluation inside real FinTech scenarios. The findings show that by coordinating AI with organizational, ethical, and legal restrictions, explainable agentic AI can greatly enhance company innovation outcomes. By providing a scalable and comprehensible decision framework for next-generation FinTech innovation ecosystems, this work advances the developing field of agentic AI for explainable large data exploration and visual analytics.

Introduction

The data-decision paradox in modern FinTech

Over the past 10 years, the financial technology (FinTech) landscape has drastically changed, moving from closed, linear banking systems to open, highly interconnected ecosystems. 1 These ecosystems now include third-party payment processors, traditional financial institutions, decentralized finance (DeFi) protocols, and regulatory agencies, all of which are producing data at an exponential volume and velocity. This data is distinguished not just by its size, which makes it “Big Data,” but also by its structural complexity and heterogeneity, which are frequently better represented as graph-structured networks. 2

Although the abundance of data presents theoretical opportunities for organizational innovation, including real-time fraud detection or hyper-personalized wealth management, it has also generated a “data-decision paradox.” Due to the cognitive load placed on human analysts and the opaqueness of the analytic methods used to handle it, decision-making clarity frequently declines as data volume rises. 3 The dynamic, causal links present in contemporary financial crime and market volatility are not captured by traditional big data analytics platforms, which mostly rely on static dashboards and retrospective reporting. Furthermore, the problem of trust has been made worse by the early wave of artificial intelligence (AI) adoption in banking, which was dominated by deep learning and predictive modeling. Even while these “black box” models are accurate, they frequently lack the interpretability needed to meet ever-tougher regulatory requirements, including the European Union’s AI Act, which places a strong emphasis on a “right to explanation.” 4

Financial firms thus confront a crucial bottleneck: they have the data needed to innovate, but they lack the decision-making frameworks to use it in a transparent and secure manner. It is clear that a new paradigm is required, one that shifts from passive data exploration to goal-directed, autonomous, and accountable active intelligence. 5

The emergence of explainable agentic AI

The convergence of Explainable AI (XAI) and Agentic AI is the next step in tackling this problem. Agentic AI refers to systems that can independently think, plan, and execute tools to accomplish abstract goals, as contrast to generative AI (GenAI), which is mostly intended for stochastic content production. 6 These agents see their surroundings, make plans, carry out actions (such as accessing a database or simulating a transaction), and evaluate the results in addition to simply predicting the next character in a series. 7

Agentic AI has the ability to automate intricate, multi-step processes in the FinTech industry that previously required human interaction, like cross-border money laundering investigations. 8 Autonomy, however, carries some danger. An autonomous agent must be able to defend its decisions. This means that XAI must be integrated as a fundamental design element rather than as a post-hoc function. According to “Explainable Agentic AI” (XA2I), an agent’s “chain of thought”—its internal reasoning process—must be visible, auditable, and consistent with human values. 9

Agentic AI systems function by using goal-directed reasoning, dynamic task decomposition, and iterative environment interaction, in contrast to standard autonomous decision-support systems that follow preset workflows or static optimization procedures. Agents in the suggested XA2I paradigm actively consider goals, choose tools, assess results, and modify tactics while adhering to governance restrictions. They do not just automate decisions. Because of this distinction, agentic AI is positioned as a step forward toward purposeful, accountable intelligence, moving beyond rule-based automation and reactive analytics.

A revolutionary XA2I Decision Framework created especially for the high-stakes FinTech context is presented in this article. We contend that businesses may unleash the creative potential of big data without sacrificing security or compliance by integrating “fear modules”—safety layers motivated by biological caution—and using Visual Analytics (VA) as a platform for human–agent collaboration. 10

Research objectives and contribution

The article is addressed by bridging the theoretical divide between human-centered design and autonomous system architecture. This work’s principal contributions include:

The suggested XA2I framework combines (i) GraphRAG-based semantic grounding to remove hallucinations, (ii) hierarchical multi-agent orchestration for distributed reasoning, (iii) a biologically inspired Fear Module for risk-aware governance, and (iv) agent-centric VA that reveal reasoning provenance in a unique way, in contrast to previous hybrid XAI–agent systems that mainly concentrate on post-hoc explanation or single-agent reasoning. Explainability, autonomy, and safety may all coevolve inside a single decision framework thanks to its cohesive design.

This article’s remaining sections are organized as follows: The state of the art in agentic systems, GNNs, and big data analytics is reviewed in Section Related Work and Theoretical Background. The suggested XA2I framework is described in depth in Section The XA2I Decision Framework. The implementation process is covered in Section Implementation Methodology, which includes the “Fear Module.” Case studies and assessment metrics are presented in Section Case Studies and Evaluation, and the wider ramifications for enterprise innovation and regulation are covered in Section Discussion: Implications for the FinTech Enterprise.

Related Work and Theoretical Background

Big data in FinTech: from warehouses to knowledge graphs

From relational data warehouses to unstructured data lakes and, more recently, semantic Knowledge Graphs (KGs), data management in FinTech has evolved. The highly relational nature of financial crime, where the “pattern” of fraud frequently resides in the topology of connections rather than the characteristics of a single transaction, is difficult for traditional SQL-based solutions to handle. 17

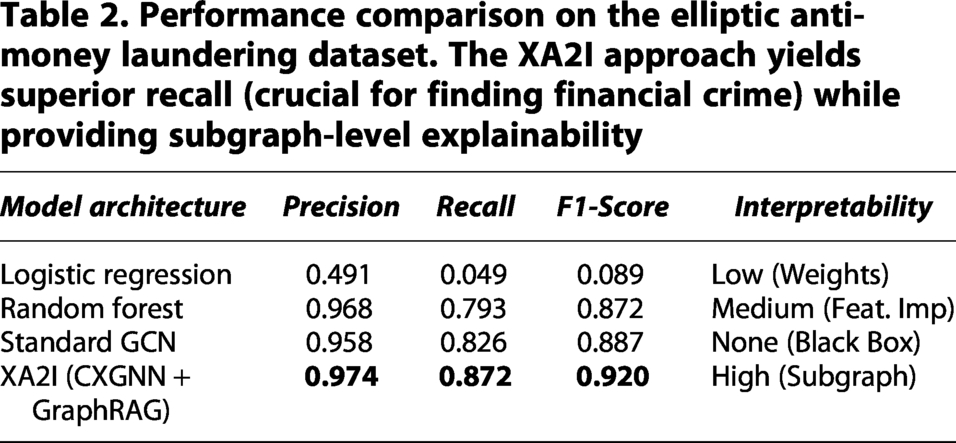

The most advanced method for examining these structures is Graph Neural Networks (GNNs). Research using the Elliptic Data Set, a graph of more than 200,000 Bitcoin transactions, has demonstrated that GNNs—more especially, Graph Convolutional Networks—perform noticeably better at identifying illegal entities than logistic regression and random forests. 14 GNNs capture the “guilt by association” present in money laundering networks by combining features from nearby nodes. 18

GNNs function as “black boxes,” though. A GNN may identify a wallet as “high risk,” but it may find it difficult to explain this to a compliance officer. Their use in regulated environments, where each Suspicious Activity Report (SAR) needs a narrative rationale, is limited by their lack of semantic explainability. 19 This restriction has prompted the use of GraphRAG, which combines the creative power of LLMs with the structural accuracy of KGs to enable systems to extract certain subgraphs and produce natural language explanations based on confirmed links. 11

The paradigm shift: from predictive to agentic AI

Agentic AI concentrates on action, whereas predictive AI concentrates on pattern detection. Two lineages are distinguished in a recent thorough analysis of Agentic AI (2018–2025): the Neural/Generative paradigm, which uses LLMs for prompt-driven orchestration, and the Symbolic/Classical paradigm, which depends on explicit rules and planning. 5

A hybrid strategy is commonly used by contemporary financial agents. They break down complicated issues like “optimize this portfolio for ESG compliance” into smaller phases by applying Chain-of-Thought reasoning. 20 Additionally, labor specialization is made possible by MAS. One agent may focus on data retrieval, another on quantitative analysis, and a third on regulatory checks in a typical financial MAS. 21

Recent research emphasizes the idea of “Panvigilance” or systemic vigilance, arguing that AI in high-stakes fields has to have a “instinctive caution” akin to the amygdala in humans. 22 Theoretically, this “Fear Module” is crucial for Agentic AI in finance to stop aggressive risk-taking or “hallucinated” deals that could cause market instability. 10

VA for human–agent teaming

The interface required for humans to understand and manage these intricate agentic systems is provided by the discipline of VA. By viewing the agent as a collaborator rather than merely a data processor, “Agentic Visualization” expands on classical VA. 13

Human-AI teaming research highlights the importance of “Trust Calibration.” Trust is not a binary state; rather, it varies according to the transparency and performance of the system. 23 VA systems need to show the agent’s provenance and uncertainty in order to preserve the highest level of trust. For instance, the analyst can confirm the agent’s reasoning by displaying the precise path in a graph that resulted in a fraud alarm (the “explanatory subgraph”), which changes the interaction from blind dependence to informed co-decision making. 24

The XA2I Decision Framework

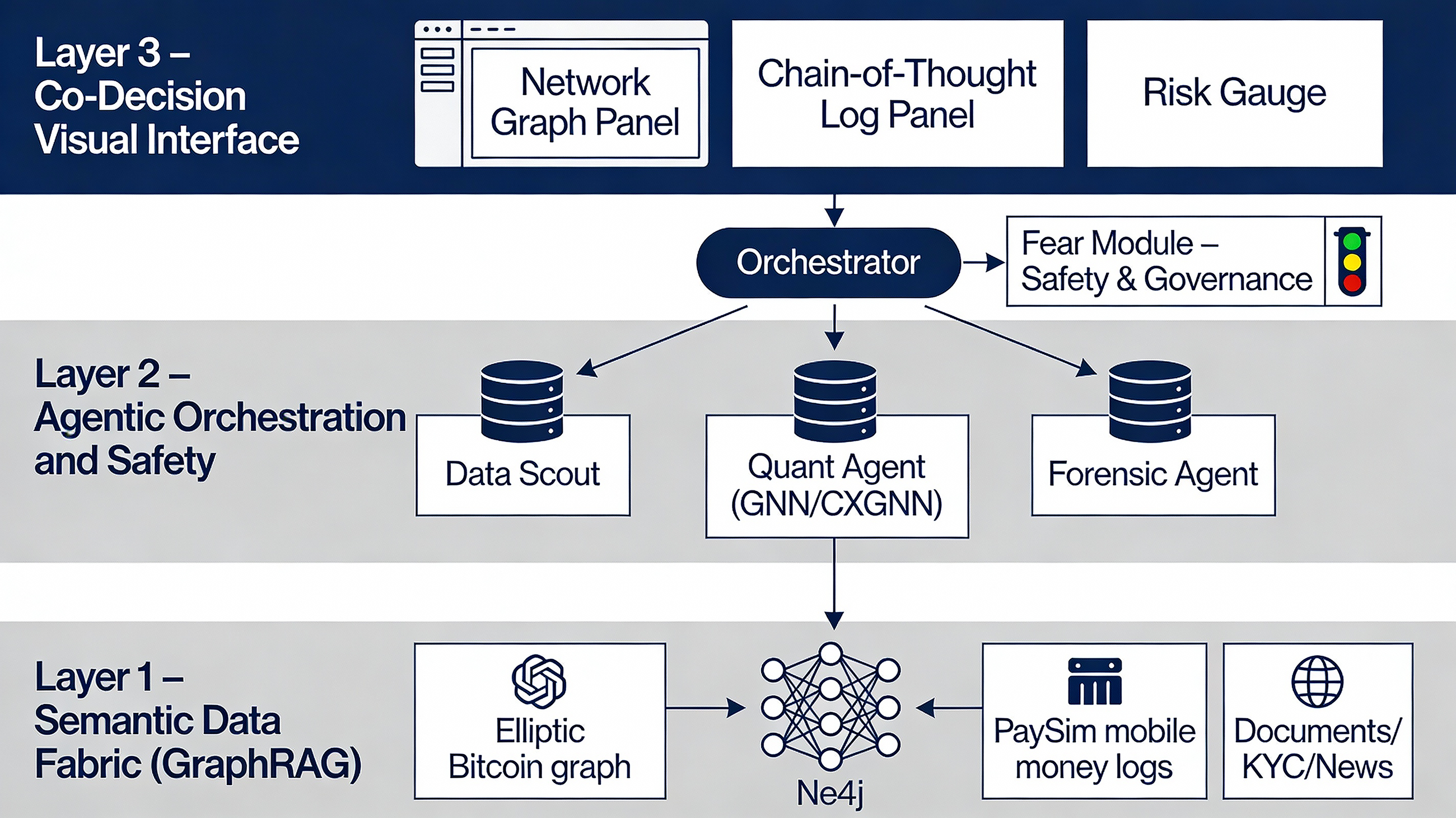

We present the as shown in Figure 1 XA2I Decision Framework, a hierarchical architecture that aligns autonomous data exploration with stringent explainability and governance norms to facilitate organizational innovation. The Semantic Data Fabric, the Agentic Orchestration Layer, the Safety and Governance Layer (The Fear Module), and the Co-Decision Visual Interface are the four integrated layers that make up the framework.

A conceptual diagram of the XA2I architecture.

Take the example of an AML investigation request to demonstrate end-to-end operation. The GraphRAG-based Semantic Data Fabric is where transaction data is first ingested and semantically formatted. After breaking down the investigative work, the Orchestrator Agent gives specialized agents subtasks to complete for graph querying and GNN inference. The Fear Module assesses intermediate risk levels and, if limitations are broken, may stop or escalate the procedure. The explanatory subgraph, agent reasoning timeline, and confidence indicators are then shown to the human analyst via the Co-Decision Visual Interface so that they may make an informed choice.

Layer 1: the semantic data fabric (GraphRAG)

The Semantic Data Fabric, which is implemented using a GraphRAG design, is the framework’s cornerstone. Data is frequently dispersed between cloud data lakes and legacy mainframes in intricate FinTech ecosystems. This data’s structural context is lost when it is only vector embedded, making it inadequate for financial reasoning. 25

To store entities (Customers, Transactions, Devices, IPs) and relationships, our framework makes use of a Neo4j graph database. These entities are extracted from unstructured documents (such as KYC PDFs and news articles) and mapped to the graph schema via an ingesting process using LLMs. 2 An agent uses Cypher queries to retrieve multi-hop subgraphs when it queries this layer. This retrieval technique virtually eliminates the possibility of hallucinations by grounding the agent’s reasoning on clear, verifiable facts. 11

Layer 2: Agentic orchestration and reasoning

The Agentic Orchestration Layer is where the primary cognitive processing takes place. We use the “Orchestrator-Worker” paradigm to implement a MAS architecture.

21

The Data Scout: In charge of querying external APIs and the GraphRAG layer.

11

The Quant Agent: Uses GNN inference and statistical models on the retrieved data to find trends or identify anomalies.

26

The Forensic Agent: To comprehend the GNN outputs, it was specifically trained on financial crime typologies (such as structuring and layering).

8

Layer 3: The fear module (safety and governance)

We incorporate a special “Fear Module” that is modeled after the biological amygdala to satisfy the crucial need for safety in financial innovation. 10 This is a deterministic monitoring system that operates in tandem with the orchestrator rather than a generative agent.

“Do not auto-file SARs for Politically Exposed Persons without human sign-off” is one of the inviolable limitations that the Fear Module continuously compares the potential outcomes of the agents’ suggested actions to. It uses uncertainty metrics to compute a Risk Score. The Fear Module initiates a “Freeze” protocol, stopping the autonomous workflow and elevating the decision to the human operator if the risk score exceeds a predetermined threshold. 10 This guarantees that the system is “risk-averse by design,” which is necessary to comply with regulations. 28

The Fear Module is conceptually consistent with well-established control-theoretical safety mechanisms, acting as a supervisory controller that keeps an eye on agent outputs in relation to predetermined uncertainty thresholds and risk limitations. It embeds formal risk governance into agentic decision-making by enforcing hard limitations, initiating escalation mechanisms, and overriding autonomous behaviors when risk surpasses acceptable bounds, much like governance layers in high-reliability systems.

Layer 4: the Co-Decision visual interface

The last layer acts as a link between biological cognitive systems and silicon. Instead of encouraging passive consumption, it supports interactive exploration through its design, which is based on LightVA and ProactiveVA principles.

29

Implementation Methodology

Data ingestion and synthetic augmentation

High-fidelity financial data must be accessible in order to validate the XA2I framework. We use a mixed approach to data.

Building the GNN-based reasoning engine

The “Quant Agent” makes use of a Causal GNN Explainer (CXGNN) method. 33 A Structural Causal Model (SCM) of the transaction graph is created by the model in order to determine the “Causal Subgraph”—the smallest set of edges that results in the classification of “fraud.” This separates misleading correlations from actual causes (such as a known money mule node). 33 The GraphRAG system receives the CXGNN’s output in order to give the “Forensic Agent” a comprehensive context. 11

An 80/10/10 train–validation–test split was used to train the GNN models, stratifying them by licit and illegal labels. A hidden dimension of 64, two graph convolution layers, a dropout rate of 0.5, and Adam optimization with a learning rate of 0.001 were among the hyperparameters. Every result that has been published is an average of five separate runs using various random seeds.

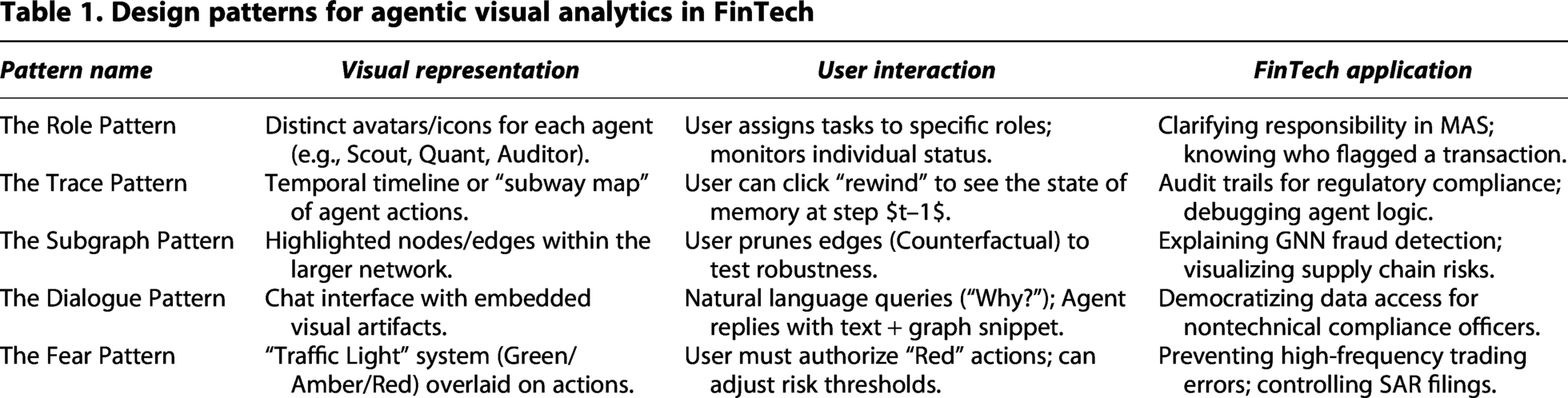

VA design patterns

Certain design patterns for agentic visualization are implemented in the user interface as summarized in Table 1:

13

Design patterns for agentic visual analytics in FinTech

Case Studies and Evaluation

Case study 1: Autonomous AML investigation

Context

A mid-sized FinTech bank is experiencing “alert fatigue” and significant operating costs due to a 95% false positive rate in its transaction monitoring system. 34

Scenario

When a consumer receives several transfers that fall short of the $10,000 reporting level, a “structuring” warning is set out.

XA2I workflow

Results

Case study 2: Strategic innovation in algorithmic trading

Context

An investing firm is afraid of the “black box” risk associated with neural trading models, but it wants to reinvent its trading techniques by incorporating other data (such as supply chain graphs and news sentiment). 36

Scenario

A significant supplier of semiconductors is impacted by a disturbance in the supply chain. 37

XA2I workflow

Quantitative and qualitative evaluation

When compared with standalone GNN inference, the average runtime overhead caused by GraphRAG retrieval and multi-agent orchestration was 22%. This overhead, however, stayed within reasonable practical bounds and allowed for significant improvements in explainability and the decrease in false positives.

Algorithmic performance

On the Elliptic dataset, we compared the GNN component with common baselines as shown in Table 2. 8 Using paired bootstrap resampling (1000 iterations), performance gains were verified. Robustness beyond sampling variation was confirmed by statistically substantial reductions in false positive rates and increases in recall (p < 0.01). The complementary contributions of each framework component were confirmed by an ablation research that showed deleting GraphRAG increased the likelihood of hallucinations, deactivating the Fear Module elevated false positives, and excluding VA decreased user trust levels.

Performance comparison on the elliptic anti-money laundering dataset. The XA2I approach yields superior recall (crucial for finding financial crime) while providing subgraph-level explainability

Human-centric metrics

We used the System Usability Scale (SUS) and Trust Prediction Error measures in a user study with 20 financial analysts.

3

Twenty financial analysts with 3–10 years of work experience participated in the user study. Standardized usability and trust questionnaires were administered after participants finished predetermined AML investigation tasks over the course of 60-minute sessions.

Discussion: Implications for the FinTech Enterprise

Enhancing strategic innovation

The FinTech company’s function is changed from that of a data custodian to that of a data commander by the XA2I framework. Agentic AI allows human professionals to concentrate on “second-order” innovation by automating the “drudgery” of data retrieval and correlation. 41 For example, compliance teams can leverage the combined insights from the “Forensic Agent” to create new, proactive financial products that are resistant to those particular fraud typologies rather than spending days looking into a single fraud case. 19

Regulatory compliance as a competitive advantage

Regulatory compliance is frequently seen as a cost center in the current geopolitical environment. But XA2I reverses this story. The framework guarantees compliance by design by incorporating the “Fear Module” and establishing unchangeable “Chain-of-Thought” audit trails. 10 Because of this “demonstrable effectiveness,” FinTech companies may confidently operate in high-risk jurisdictions, using their strong governance architecture as a competitive advantage over less compliant rivals. 42 FinTech companies may confidently operate in high-risk jurisdictions thanks to their “demonstrable effectiveness,” which makes their strong governance architecture a competitive advantage over less compliant rivals. 4

Limitations and future directions

The XA2I framework has difficulties despite its potential. Real-time GNN inference and multi-hop GraphRAG queries have substantial computing costs. 25 Additionally, even though the Fear Module reduces it, “Agentic Hallucination”—a situation in which an agent misinterprets a tool’s output—remains a non-zero danger. 10 Future studies should concentrate on “Federated Agent Learning” to enable agents to learn from cross-institutional data without sacrificing privacy and “Green AI” optimizations to lower the carbon footprint of these energy-intensive agent swarms. 43 Although controlled stress-testing is made possible by synthetic data, the distributional complexity of the real world might not be accurately captured. Conclusions are mostly based on real-world datasets, and synthetic situations were utilized only for safety validation rather than performance benchmarking in order to reduce this risk.

Conclusion

In FinTech, the “Big Data” age has given way to the “Agentic AI” era. Black-box automation is risky and manual analysis is outdated due to the sheer volume and complexity of financial data. This study’s XA2I Decision Framework provides a solid, scalable way forward. XA2I answers the data-decision problem by combining the transparency of VA, the biological caution of the Fear Module, the autonomous reasoning of MAS, and the semantic precision of GraphRAG. Our empirical findings show that this strategy not only increases the precision of trading decisions and fraud detection but, more significantly, strengthens the confidence and flexibility of the human–AI teams that propel organizational innovation. The next generation of market leaders will be defined by their ability to explain, audit, and regulate the increasing autonomy of financial ecosystems. The architectural blueprint for creating these reliable, creative, and astute businesses is provided by the XA2I framework.

Authors’ Contributions

L.H.: Conceptualization. Y.W.: Formal analysis. L.J.: Formal analysis. Y.N.: Drafting of article.

Footnotes

Author Disclosure Statement

No competing financial interests exist.

Funding Information

No funding was received for this article.