Abstract

It is important to understand the implications of participation in global value chains (GVCs) in horticulture for farmer and worker upgrading/downgrading. This article examines the functioning and dynamics of supermarket driven GVCs in a high-value export crop, baby corn, to understand the significance of standards in farms and pack houses in India. It explores patterns of governance, smallholder inclusion, economic and social upgrading, or lack of it, and its determinants and changing nature of farmer and labor linkages. This article presents case studies of farmers and various types of labor on farms and in pack houses, based on interviews with the exporter and facilitator management staff, field visits to the operations and a personal interview survey of 76 farmers and workers across the entire value chain of baby corn in western India conducted during 2011–2012.

Introduction

The nature of global food markets is a highly debated issue as it concerns food security, food safety and development. The fact that supermarkets are the value-chain drivers of global food markets makes it an even more contested issue. Supermarkets are interested in food, especially fresh fruits and vegetables (FFVs), because they help to attract customers and enhance the quality of a store; provide opportunities for value addition through ‘pre-packs’ for ‘time poor, cash rich’ customers; and offer high margins (30%–40%) (Stichele, Wal, & Oldenziel, 2006). Although supermarket buyers do not own any farms or factories, their standards of quality and supply, through their sourcing networks, extend right up to farms and farm workers, with implications for their families (Bonanno & Cavalcanti, 2012).

The major reasons for which global supermarkets source FFVs from India include lower cost, diversification of sourcing risk, ethnic appeal for Indians abroad and rise of primary marketing organizations (PMOs) as suppliers. In this context, it is increasingly important to understand the implications for farmer and worker upgrading/downgrading resulting from participation in global value chains (GVCs) in horticulture. This article examines the functioning and dynamics of supermarket-driven GVCs in Baby Corn, a high-value export crop, to understand the significance of standards in farms and pack houses in India. Although farm workers were at the lowest end of agribusiness value chains, until recently, scholars often excluded labor issues from the analysis, which ended with primary producers, that is, farmers. There are only a few studies in the African and Latin American contexts, which try to understand labor issues in such networks (Barrientos & Kritzinger, 2004; Selwyn, 2009; Barrientos & Visser, 2012; Bonanno & Cavalcanti, 2012). Additionally, it has been argued, more generally, that the GVC framework and analysis has found it difficult to incorporate analysis of class relations (Barrientos, Gereffi, & Rossi, 2011; Selwyn, 2012).

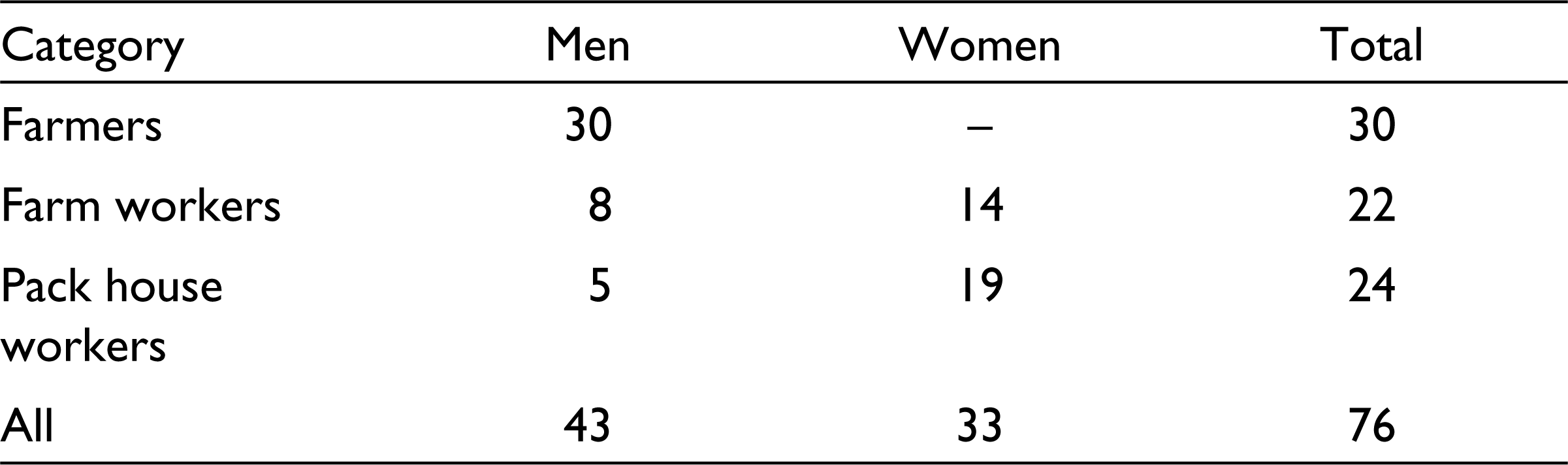

The article explores patterns of governance, small holder inclusion, upgrading or lack of it, and its determinants, and the changing nature of farmer and labor linkages, with the help of case studies of farmers and various types of labor, on farms and pack houses. It assesses whether and how economic upgrading has taken place and whether it has led to social upgrading for small farmers and various types of workers in the chain. The analysis is based on interviews with the exporter and facilitator management staff, field visits to the operations and a personal interview survey of 76 farmers and workers across the entire value chain of baby corn in the local area carried out during 2011 and 2012 (Table 1).

Distribution of Surveyed Farmers, Farm Workers and Pack House Workers

This article is organized as follows. The second section provides an analytical framework and details of the context. The third section explores the working of the GVC in terms of profile and strategies of the lead player, that is, the exporter who has organized the chain in India. The fourth section assesses the GVC impact on farmers and the fifth section assesses their impact on workers, on farms and pack houses. The sixth section focuses on upgrading aspects across all small actors in the chain, that is, service providers, farmers, farm workers and pack house workers. The seventh section concludes with policy and practice implications of GVCs in countries like India, from the perspective of the small farmers and the workers.

Governance and Upgrading: An Analytical Framework

The GVC analysis drew attention to the role of value creation, value differentiation and value capture in a coordinated process of production, distribution and retail, whereas a parallel literature around Global Production Networks (GPNs) has placed more emphasis on the institutional or social embeddedness of production, and power relations between actors (Barrientos et al., 2011; Selwyn, 2007). Governance, central to GVC, can be defined as non-market coordination of economic activities, and refers to key actors in the chain that determine the inter-firm division of labor and shape the capacities of participants to upgrade their activities (Gereffi, 2001). This can include defining products, processes, and standards for suppliers (Gibbon, 2001). GVCs across products and countries differ significantly with respect to how strongly governance is exercised, how concentrated it is and how many lead firms exercise governance over GVC members (Bain, 2010; Gereffi, Humphrey, Kaplinsky, & Sturgeon, 2001). Governance can be public, private or collective in terms of actors; facilitative, regulatory, or distributive in terms of impact; and local, national, regional or global in terms of its domain (Mayers & Pickles, 2010). Gove-rnance is required when suppliers lack technical competence or market knowledge (Eapen, Jeyaranjan, Harilal, Swaminathan, & Kanji, 2003), and for product differentiation. Governance exercised by GVC drivers has consequences not only for inclusion/exclusion of firms in networks, but also for the opportunities for economic and social upgrading.

Economic upgrading refers to ‘capabilities within a chain for accessing better markets, and/or in more developmental terms, development of weaker players or “moving up the value chain” either by shifting to more rewarding functional positions or by making products that have more value added invested in them and that can provide better returns to producers’ (Gibbon & Ponte, 2005, pp. 87–88). Economic upgrading can also be defined as the ability of producers ‘to make better products, to make products more efficiently, or to move into more skilled activities’ (Pietrobelli & Rabellotti, 2006, p. 1), known as product, process, functional and inter-sectoral or inter-chain upgrading. Economic upgrading embodies a capital dimension and a labor dimension. The former refers to the use of new machinery or advanced technology and the latter refers to skill development or to increased dexterity and productivity on the part of workers.

Social upgrading, by contrast, is the process of improvement in the rights and entitlements of workers as social actors such as wages, safe and healthy work conditions, social protection mechanisms, freedom of association and non-discrimination, besides absence of forced and child labor, which enhances the quality of their employment (Barrientos et al., 2011). Social upgrading can be subdivided into two components: measurable standards and enabling rights. The former are easily observable and quantifiable aspects of well-being of the workers, such as type of employment, wage level, social protection and working hours, including sex ratios and unionization levels of workers. However, measurable standards are often the outcome of complex bargaining processes, framed by the enabling rights of workers, which are less easily quantified, such as freedom of association, the right to collective bargaining, non-discrimination, voice and empowerment. Lack of access to enabling rights undermines the ability of workers—or specific groups of workers, such as women or migrants—to negotiate improvements in their working conditions that can enhance their well-being (Rossi, 2013).

Economic upgrading is important for social upgrading as the former allows firms to earn economic rents by creating entry barriers, in the absence of which firms may resort to cost cutting at the expense of labor because of competitive pressures. However, economic upgrading does not automatically translate into social upgrading for farmers or workers through better wages and working conditions and may be accompanied by social downgrading. Similarly, social upgrading can also occur without economic upgrading, and a country/sector/firm may experience simultaneous ‘downgrading’ in economic and social terms (Milberg & Winkler, 2011). The links between economic and social upgrading/downgrading are often complex, with different types of workers experiencing different outcomes including downgrading, on the same production site (Barrientos et al., 2011; Rossi, 2013). Furthermore, economic and social upgrading can be complimentary or substitutes depending on the local economy context, such as other employment opportunities, social discrimination and labor regulation. Local actors and factors such as state regulation, class relations (including caste in countries like India), labor unions and bargaining power in GVCs also affect labor processes and outcomes (Goto, 2011; Selwyn, 2012), and thus, economic upgrading is often a necessary, but not a sufficient condition for social upgrading (Goto, 2011). Economic and social upgrading/downgrading of firms/workers is also influenced by stakeholder positioning within the GVC, the type of work performed and the status of workers within a given category of work (Barrientos et al., 2011).

Baby Corn Production and Trade in the Indian Context

India is the second largest producer of vegetables after China (15% of world production from 2.8% of land). However, India’s share in the world horticultural trade is less than 2 per cent. Thailand is the largest exporter of baby corn, accounting for 80 per cent of world exports of the product, with 39 per cent of its production being exported in the early 2000s. Thailand exported more canned baby corn (77% in value and 94% in volume terms) than fresh baby corn (Anonymous, 2006). Other exporters of baby corn include China, Kenya, Zimbabwe and Zambia. Major baby corn markets were in the European Union, the United States, Malaysia, Taiwan, Japan and Australia. India, with 10 million tons of production had only a 1.75 per cent share of world baby corn production in 1998. In the UK market, Indian exporters faced stiff competition from Thailand owing to its lower production costs, high yields and multiple crops in a year, technological advantage for frozen baby corn (can sell even third and fourth pickings) and the availability of on-farm skilled family labor with long market-learning experiences that reduce supervision costs. In the supplies to the UK, 70 per cent of the vegetables are pre-packed at source and 100 per cent are airlifted, making 50 per cent of cost. Furthermore, 75 per cent of vegetable produce exported is ‘grown to standards’ (interviews with supermarkets and their suppliers in the UK).

There are considerable variations across markets in terms of their preferences and distribution systems. Baby corn is usually consumed fresh; however, frozen and canned baby corn is also sold. The United States usually imports fresh baby corn; however, baby corn is rarely sold in supermarkets, but is bought by high-end restaurants. European countries import fresh baby corn both in loose and pre-packed forms, though the latter is more prevalent. The UK is the largest market in Europe for fresh baby corn, which is distributed through supermarkets. In the Middle East, Saudi Arabia is the largest importer of canned baby corn. Some Asian countries like Japan and Malaysia also import canned baby corn (Pandey, Sudhir, Raman, & Deepali, 2010).

Sri Lanka, Thailand, Zimbabwe, Zambia and Kenya export to Europe, whereas Netherlands imports baby corn from Asia and Africa and re-exports to northern Europe and the Middle East. In EU/UK, supermarkets have created a category approach that was extended to the fresh produce category during the late 1990s because of the complexity of importing from several countries to maintain year-round supplies of consistent quality. Accordingly, supermarkets nominate a selected product range to a few importers who are responsible for the building up of supply-chain relationships in exporting countries (Anonymous, n/d).

Baby corn is a short-duration crop taking 45–60 days for harvesting, and multiple crops can be cultivated in 1 year. At the global level, its consumption is the highest in Asia. Its cultivation for exports was introduced by Thailand during the early 1970s, and later by other countries such as Guatemala, Zambia, Zimbabwe and South Africa (Anonymous, n.d.). Average recovery rate of baby corn is up to 10 per cent, however, it ranges from 6 to 12 per cent depending on factors such as season, labor availability, family engagements and festive seasons that might delay harvesting. The processing cost is the same for export and domestic markets, but packing cost is higher for export market due to punnets, freeze packs and carton boxes. The produce destined for the domestic market is packed in poly bags. Most of the packing work is manual (Gandhi, Sachdeva, Kapur, & Rattan, 2009). The baby corn has a shelf life of 5 days with 95 per cent humidity at 1 °C temperature (Anonymous, n.d.). The freshly harvested cobs are to be pre-cooled at 2–3 °C for 10–15 minutes, to remove field heat. They are processed, that is, split, dehusked and their silk is removed. After grading and sorting, the cobs are packed in punnets and wrapped in polythene sheets for export. The lower-grade baby corn produce is sold to the domestic supermarkets, such as More and Big Bazaar, and in the wholesale market (Anonymous, n.d.).

Major states producing baby corn in India under contract farming include Punjab, Haryana, Karnataka, Western Uttar Pradesh, Maharashtra, Gujarat, Andhra Pradesh and Meghalaya. The main corporate players are Monsoon Agro, Pune; Namdhari Fresh (NF), Bangalore; Field Fresh (FF), Gurgaon; and Champion Agro in Gujarat. NF, a unit of Namdhari Seeds Private Limited, Bangalore—a leading exporter of baby corn—combines corporate farming (on owned and leased land) and contract farming for production of baby corn and other crops, and had supermarkets (18) in Bangalore, besides export operations (Singh & Singla, 2011).

Field Fresh Baby Corn Production and Export

FF is a part of the Bharti Enterprises, an Indian conglomerate with its operations spread over 21 countries and presence in various sectors such as telecoms, financial services, real estate and retail. The group, with its mission to link farmers with the supermarkets in the United States and the UK incorporated Field Fresh Foods Pvt. Ltd, in 2004, a joint venture (JV) with ELRo Holdings, an investment arm of the Rothschild family with a strong British base, which was restructured in 2008 as a JV of three partners including Del Monte, Asia Pacific through its Bharti–Del Monte India Private Limited and Bharti Enterprises as two major partners, and Rothschild as a minor partner.

FF decided to focus on niche international markets in fruits and vegetables rather than grains, oilseeds or other farm commodities. The company exported a wide range of fruits such as Thomson seedless grapes, mangoes, pomegranates and litchi. By 2008, the company became the third largest Indian exporter of fresh grapes to the EU/UK. The financial results, however, were not commensurate with the efforts; that year, the whole industry made a loss and FF was no different. It was exporting various fruits such as pomegranate, grapes and litchi up to 2006, when it also started exporting baby corn, sweet corn, chillies and sugar snaps. However, fruits were abandoned as a category, as fruit growers were scattered and not suitable for quality production for export, and even service providers could not deliver quality; there was competition from local market and high price fluctuations, besides a limited export window for Indian fruits (Pandey et al., 2010).

The processed products of the company (50% of which are imported) are marketed and sold under the Del Monte brand, whereas fresh produce is sold in the brand name of FF both in export and domestic markets. Initially, it supplied fresh and processed products to Bharti’s Easy Day supermarkets for 1 year (its supermarket chain is now sold to Futures Group, which is India’s largest supermarket in terms of number of stores run by it under various brands, such as Easy Day, Niligiris, Aadhaar, Big Apple and Big Bazaar). Thereafter, FF decided to focus on a single product and use that product to debug the entire value chain. In parallel to the venture in fruit, the FF business team had investigated vegetable cultivation where the cropping cycle from seed to harvest could be managed, not only from a quality perspective but also from the perspective of enhancing value capture—both for the farmer and the company. Thus, baby corn was chosen as a crop for export.

The company, like its major competitor in export markets, NF, also combines corporate farming (on 300 acres of leased land from the Government of Punjab for 99 years) and contract farming with 350 growers in Punjab and thousands in Maharashtra. Its own farm and the growers’ farms are certified for Global GAP and Tesco’s Nature’s Choice standards, whereas the pack house is British Retail Consortium (BRC) certified for Food Safety and ISO: 22000-2005 certified. The company had earlier tried corporate farming on land leased from farmers in Punjab for export crops like ladyfinger and bitter guard, which proved unviable due to high supervision costs and overheads, besides the employee (corporate farming) model, which did not suit demands of farming, as it required round-the-clock presence on farms. Of the other options, although it started with contract farming, because of the difficulties of managing a large number of small farmers over a dispersed area, it soon moved to a facilitator model each working with 400–700 farmers on behalf of the company in Maharashtra.

The company works with farmers through third parties, that is, suppliers, in Amritsar district of Punjab and also in Nashik, Pune and Satara districts of Maharashtra. FF moved into Maharashtra to expand the market size, reduce the shipping costs and maintain a regular flow in the supply of baby corn throughout the year in the export market. Through this expansion, it diversified its supply base, as three to four crops could be cultivated in a year, owing to the existence of more suitable agroclimatic conditions. The company provides technical support including seeds on 50 per cent advance payment through its extension team, whereas supplier farmers themselves arrange for logistics and finance.

The harvesting of baby corn requires good supervision and specific pruning practices, because the company accepts only first and second pickings for exports. The company supplies to farmers plastic crates (with capacity of 15–17 kg), tags printed with codes (given to each farmer free of charge), seeds (on credit with 50% advance payment) and the crop harvesting date. This eases traceability of produce in case of a problem in the destination market. Daily picking continues for about 10–12 days during summers, whereas it lasts for 20–22 days, on alternate days, during winters. As the third and fourth pickings are not fit for human consumption but are nutritious, these, along with green stalks, are sold in the market as animal feed, or used for feeding milch cattle that enhances milk yield (5%–10%), both in terms of volume size and fat content.

The company sold 38 per cent of its baby corn output to export markets and the rest in the domestic market. However, 60 per cent of its revenue comes from export markets and 40 per cent from the domestic market. While exporting baby corn, marketing costs account for as much as 75.5 per cent of total cost or value, which is largely air freight cost (71% in case of EU markets). Processing costs another 20 per cent, with production (raw material or crop produce) being just 5.5 per cent of the final value of the product. The other major marketing costs are customs clearances (19%), maximum residue limit (MRL) testing (1.3%), insurance cost (5.4%) and inland freight (3.6%). On the other hand, in the domestic market, marketing costs are only 8.5 per cent and production another 21 per cent, with processing being as much as 70.5 per cent of total value of the final product (Gandhi et al., 2009).

FF started with 50 tons of export in 2005–2006, and reached 400 tons in 2007–2008, 1,200 tons in 2010–2011 and 1,800 tons in 2011–2012. In 2011–2012, the export portfolio comprised of sweet corn (1,100 tons), baby corn (600 tons) and chillies (125 tons). The average price realized in export baby corn market is between ₹200/kg and ₹250/kg. Major importers in the UK include Wheelmoor, Wellpack, and Bar Foods, the latter being the largest importer and supplier to major supermarkets in the UK, accounting for 20 per cent of its baby corn market. The other European importers include Summerfield, Nature’s Pride, MWW, Bud Holland and Tesco (Chaba, 2012). The importers make four to five visits a year to the production areas, although supermarket buyers never visit.

Among various models tried by FF, contract farming has been the most successful. Instead of directly managing the land and taking on the associated risks, FF provides local farmers with a written guarantee that the company will purchase all the produce grown within specified quality and quantity parameters, and assures them of sustained technical support. Teams of extension workers at FF meet regularly with farmers and share the latest soil management techniques, better seeds and implements. After the harvest, FF transfers the money directly into the farmer’s bank account within a week of delivery, thus building further trust and transparency in the relationship. With contract farming, the company can trace produce to its source—traceability and batch control being key elements of ensuring standards compliance. The extension teams sensitize farmers towards optimum use of resources like water and minimizing the use of chemical fertilizers and pesticides. They also promote crop rotation and other progressive agricultural practices like inter-cropping with sugar cane and mint, not only to ensure proper soil and water management but also to enhance the return per acre (Pandey et al., 2010, p. 7). An acre of baby corn produces 3.5 tons of corn and 12 tons of fodder. With a recovery rate of 10 per cent, varying from 8 per cent in summer to 12 per cent in winter, this gives 3.5 quintals of baby corn. The gross output of 3.5 tons is bought at ₹5/kg. The baby corn production cost is ₹10,000 per acre compared with ₹15,000 for sweet corn, major costs being seed, labour, irrigation and land-lease rent.

By 2010, hundreds of farmers in Punjab and Maharashtra supplying FF were Global GAP certified. Although equal quantities of baby corn were produced in each region, the sourcing model differed. In Punjab, the company had a direct commercial relation with over 200 farmers, whereas, in Maharashtra, the company was engaged with over 3,500 farmers through ‘agri-entrepreneurs’, as FF called them. These agri-entrepreneurs recruited and managed small farmers and provided technical services such as crop demonstration plots and crop advisory. Depending on the capacity of an agri-entrepreneur, FF provided soft funding up to USD 200,000 to allow the agri-entrepreneur to build technical and physical capacity. By 2009, FF had become the largest Indian exporter of fresh baby corn, selling 500 metric tons (handling over 6,000 tons of raw materials) and capturing over 10 per cent of the UK retail market (Pandey et al., 2010).

Contract Farming Operations

Besides its corporate farm and contract farming in Punjab, FF has contracted 3,500 farmers in Pune, Nasik and Satara districts of Maharashtra, having 2,200 acres of baby corn, 700 acres of sweet corn and 100 acres of chili, which are managed by a service provider or a facilitator. There are three seasons of baby corn in Maharashtra, as against two in Punjab. Each farmer is given to grow one crop of baby corn in a given plot and then another crop before going for baby corn in the same plot again. Generally, a farmer in Maharashtra grows one crop of baby corn in a given plot in 1 year under contract farming. The Global Gap certification costs ₹6,000 per acre annually, with FF obtaining recognition under the PMO provision of the Global GAP norms.

FF has a total staff of 35 persons, including five regional officers, 15 extension officers, six quality managers, and six operations managers. It also employed 15 supervisors who were not on the company payroll. The regional office looks after product movement, and the head office oversees export and logistics. Contracts comprise mostly small and marginal farmers who have no overlapping production across various crops, that is, sweet corn, baby corn and chillies. No farmer grew baby corn before it had begun to be exported by the company. The introduction of the crop has led to replacement of sugarcane and has fodder value for farmers who are also into dairying. No chemical plant protection products are used in baby corn production and all operations are manual, although there is no organic production of the crop as yet.

The procurement and processing are being managed by a service provider (FAC). The service provider also has 15 field staff. The FAC was registered as a partnership firm in 2004. It had a working capital of ₹10 million (₹2 million by each partner) in 2012. It was earlier into grapes and tomatoes for the local market and for Walmart. FAC faced competition from MSLS, Reliance Fresh and Sun Pint, which were exporting grapes even before they entered the market. Somnath Consultants—another small local firm—obtained the certification for FF on the service-provider managed pack house. FAC had handled 117 tons of grapes (15 containers), which increased to 85 containers by 2010. The FAC started facilitation of baby corn exports in 2007 with 117 containers. The turnover of the company is ₹50 million, of which 50 per cent is baby corn, 20 per cent grapes and sweet corn each and 10 per cent vegetables. FAC is a supplier for FF for all produce. The FAC also packs grapes for MSLS for a facilitation fee for entire harvesting and packing activity. There is competition in service provision domain too, as there are 20 players like FAC who facilitate grape and baby corn production and packing, such as Shruti in Karad in baby corn, AT More and Evergreen in grapes, for exporters and modern supermarkets. Market knowledge and ability to take market risk is an issue; for example, even FF sells on consignment basis and pays a fixed rate to FAC.

FF conducts fortnightly meetings in the village, either at gram sabhas or at the house of the large farmers. Sometimes, non-baby corn farmers are also invited to the meetings. There is no condition of the minimum size of the land holding to be able to supply to the company. Farmers are generally selected based on financial condition, geographical location, creditworthiness, availability of labor in the area and assured irrigation facilities. The company prefers that the service provider works with small growers because of labor intensive and frequent harvesting of the crop, which can be done better with family labor. The soil testing is mandatory before growing the crop. It is carried out at farmer’s cost at the laboratories of the Maharashtra State Grape Growers’ Federation, Deepak Fertilizers Ltd., Sugar mills, in case of sugarcane growers and private laboratories. The company has a formal, written and non-registered contract with the farmers through the service provider. There is a tripartite acreage agreement with the farmers. The language of the contract is vernacular (Marathi). The duration of the contract is 1 year, which is revised annually. The company provides seed, extension service and farm pick-up facility to the farmers. The company provides 5 kg seed/acre at the rate of ₹60/kg.

The executive (extension) monitors and coordinates the supply schedules, as guided by the assistant manager (extension), who, in turn, is guided by a senior manager (West). The executive is given monthly sowing targets for baby corn in each region. The service provider appoints a sub-facilitator at each sub-district level who operates through a local office. The sub-service provider has a license from APMC market, which is valid for 1 year. The sub-service provider pays for the produce supplied to farmers through cheque. The sub-service provider is paid commission by the service provider.

The company’s service provider has a written contract with farmers, which specifies seed supply on credit by the service provider and stipulates that the farmer follows specific crop management practices. It also specifies the price of the produce for all the three seasons in a year, spot weighing and farm pick-up, and payment through cheque within 15 days of harvesting the crop. It is specified that the company will bear the cost of lifting the produce but the farmer will have to buy the packing material on his/her own for B grade produce. The produce has to be harvested as per the company’s guidelines. Furthermore, the company (service provider) is not responsible for any natural calamity. The harvesting costs are met by growers and rejected produce is the responsibility of the farmers. The service provider also specifies the criteria for selection of farmers: farmers must have land suitable for baby corn cultivation; produce should be residue free and there should be availability of fertilizers, ample irrigation and electricity supply through a legal connection.

The company bears the Global GAP group certification cost. On-farm expenses, such as construction of fertilizer store, toilet for workers and disposal pit for Global GAP certification, are borne by the farmer. The annual cost of group certification of baby corn varies from ₹5,000 to 10,000 per farmer.

In the winter season, harvesting usually starts 60–62 days after sowing, and, in the summer season, it starts 54–56 days after sowing. It is usually carried out by women, and about 17–18 working days are required to harvest one acre of the crop. After harvesting, it is packed in nylon bags with each containing 35–38 kg, or 15 kg crates. In the summer season, crates are generally preferred to pack baby corn, as nylon bags absorb more heat during summer, and, thus, produce has to be kept in a pre-cooling chamber for more time. The rejection rate in baby corn is 3–4 per cent, which happens due to over-matured cobs which are sold in Vashi APMC (fresh produce wholesale) market in 500 g and 1 kg packs, as B and C grades.

Although baby corn is considered a family-labor-based smallholder crop, a labor contractor–based system is practiced in baby corn and onion in Shiror taluka of Pune district, wherein the contractor has a group of 10–12 workers, mainly women, and provides pick-up and drop-off facility to workers. This labor mainly belongs to the neighboring villages in a 25–30 km radius. The farmer pays the wage to the contractor, from which he deducts his commission of ₹20/day. He then hands over the wages to the workers, which amount to ₹100/day for women and ₹150/day for men. This type of labor is trained labor and is commonly used in farm operations such as sowing, weeding and harvesting. The contractor remains at the field and supervises them. The contracted laborers work from 10:30

FF has six field staff in baby corn to provide extension to the farmers, and there is no direct link between the firm and the farmers. There are 300 to 400 farmers in Nasik area alone for the entire year, with 45–50 farmers who grow baby corn twice a year with a one-season gap in between. The company has an APMC license to buy baby corn from farmers directly and pays a market fee. Under the contract, the service provider (FAC) is paid for farm handling, packing and quality management, on a per-kilogram basis. There are monthly targets of harvest and delivery.

FF had 138 baby corn farmers and 65 acres under the crop in 11 villages of four talukas (sub-districts) of Pune district and one taluka of Ahmednagar district in December 2011, when the study was carried out. As per company information, about 60 per cent of the farmers were marginal, 27 per cent small, 10 per cent semi-medium, and 3 per cent medium farmers.

Processing for Export

The company makes use of two leased pack houses, one in Karad (Satara district) and the other in Pimpalgaon (Nasik district). The major activities at the pack house include pre-cooling, packing and dispatching of the produce for export. The size of the pack house is about 15,000 sq. ft. and it is managed by three people: pack house in-charge, quality control in-charge and an executive. Each pack house also has two men and women supervisors each, who are paid by the service provider. Men supervisors oversee the activities of both men and women workers. One male supervisor each is allotted for trimming and peeling activity. The women supervisors are generally group leaders of the workers. Their main role is to understand the physical problems of the women workers and to bring them to the pack house on time. There are 150 workers each, 75 per cent of whom are women, who are provided by contractors for pack houses dedicated to production of baby corn. Two out of five of the supervisors at each pack house are women; many of them have been upgraded from the status of worker to supervisor. About 60 per cent of labor is meant only for baby corn, and 40 per cent is shifted from baby corn to grapes or grapes to baby corn.

To avoid the transportation losses due to spoilage, the produce is transported during the night when temperature is low. On arrival of the produce at the pack house during night, it is transferred to the crates, which are then shifted to the cold store for six to 7 hours at 3–4 °C. The next day, slitting is carried out by the male workers. After slitting, peeling (husk and silk removal) is carried out by women workers. There should not be any hair on the tip of the cob and the tip of the cob should not be broken. After peeling, produce is sorted and graded for over-matured, misshaped, broken tip, dehydrated and defected cobs. Trimming in diameter and length is then carried out as per the buyer’s requirements. Packing is then done in 80 g, 125 g or 135 g punnets. About 36–44 punnets are kept in crates for cold storage at 0–2 °C. Before cold storage, these crates are passed through a metal detector for detection of any metals in the produce. About 36 punnets are packed in one box the next day, 6 hours before dispatching the produce, and each box usually weighs around 6.1 kg. The pre-cooling temperature of 0–4 °C has to be maintained for baby corn in the pack house. The processed produce is carried in cold chain and airlifted to the export market destination.

The payment to the service provider is pre-agreed and on a per-kilogram basis. It amounts to ₹6–8/kg, over and above ₹42, which is the cost of handling and processing. The company monitors produce quality and labor conditions compliance at the pack house. These workers are provided on-the-job training by the company staff. Most of the labor (80% of whom are women) are local, whereas male laborers are migrants from within as well as outside the state. There is a weekly break for the pack house workers. The attrition rate among workers is 25 per cent, and the service provider uses labor contractors for the supply of labor for the pack house. The service provider provides pick-up and drop-off facility to workers, especially women.

Labor management at the pack house is crucial, as the grape and baby corn seasons overlap, and labor allocation becomes crucial. Sometimes, in order to cope with labor shortage, production is scheduled accordingly. This generally happens during festival seasons. Each pack house has a local labor supply. The laborers work in 7–8 groups of 30–35 workers each. The daily wages are the same for regular and seasonal labor, that is, ₹150 for women and ₹200–250 for men. Labor groups, especially the packing team, are given packing targets in terms of number of crates graded and packed in a day and are given bonus at the rate of ₹5–10 per crate if they exceed the target. Only 10 per cent of workers exceed the target of a minimum of 18 crates/day. The average earning per worker per day is ₹200, although some efficient women workers may also earn ₹250/day. No worker earns less than ₹100/day. The workers are paid weekly and are also supposed to maintain standards of hygiene, and, on failing to do so, are asked to leave. No mobile phones are allowed inside the pack house.

Contract Farmer Profile, Value Sharing and Value Chain Inclusion

The average age of a baby corn farmer is 35.4 years and average schooling is 7 years with one-fourth having no formal education. Most baby corn farmers have small and marginal landholdings. In fact, these who make up 83 per cent of all interviewed growers were not the first ones to work with FF, which had introduced the crop in the region. The first contract growers were medium and semi-medium farmers with 2 to 6 ha of land. Most of the farmers picked up the baby corn crop from FF and fellow contract farmers. It was adopted as it gave higher income, because the company offered a fixed and high price and picked up harvested produce from the field. It also yielded good quality fodder for milch animals, and this was important for farmers because most of them owned livestock.

The average size of holding of a baby corn grower is 4.11 acres (1.6 ha) ranging from 1.69 to 12 acres, and baby corn crop accounts for 22 per cent of operated area (0.91 acres or 0.38 ha) ranging from 0.25 acres to 1.25 acres (32%–10.4% of the operated area). This is close to the average size of holding in the state, that is, 4.1 acres. There is not much leasing in or leasing out of land in the region (Table 2). However, 75 per cent of the Gross Cropped Area (GCA) is devoted to high value crops, with wheat accounting for only 6.7 per cent and fodder another 17 per cent of the GCA (Table 3). Although farmers do not own many machines, pickup trucks are more common with medium and semi-medium farmers, and electric motors, sprayers and bullock carts are the norm for all. Tractors are hired for land preparation by most of the farmers. The average cropping intensity is 145, with the highest among marginal farmers being 199 and the lowest among medium farmers being 101. Thus, average crops taken in a year is 2.7, with the highest among small farmers being 2.87 and the lowest among medium farmers being two. Most of the inputs other than seed supplied by the company are bought from Primary Agricultural Co-operative Societies (PACSs) and traders/input dealers. About 63.3 per cent of farmers are members of PACSs. Besides taking credit, farmers also avail the seeds, fertilizers, micronutrients and knap sack spray pumps from the PACS. There is no interest on credit up to ₹50,000 and only a 2 per cent interest was charged up to a loan amount of ₹1 million. A majority of farmers (57%) do not depend on hired labor for baby corn work, and there is a system of labor exchange prevalent in some villages. Harvesting attracts the highest daily wage rate compared with other tasks, such as weeding or sowing, which are all carried out mostly by women, whereas men do work related to ploughing and irrigation. The crop is remunerative due to high yield, lower transaction cost, better and free extension and a good price because of high quality. The surveyed farmers have been contract growers for an average of 2.67 years, with relatively larger ones (medium and semi-medium) having association for three to 4 years, whereas marginal and small only for 2.5 years each on an average. The most common duration is one to 2 years (for 33% of farmers). Baby corn is on average grown on 2 acres because of its multiple cropping seasons, accounting for 34 per cent of gross cropped area and even higher for small farmers (43%), followed by fodder, sugarcane and onion in that order (Table 3).

Farmer Category Wise Average Size of Land Holding of Field Fresh Farmers (acres)

Category Wise Distribution of Farmers by Cropping Pattern and Cropping Intensity

The majority of farmers have lift irrigation as water sources for their crops, followed by wells (26%) and tube wells (10%). In total, 87 per cent have electric motors for irrigation. There are only two marginal farmers dependent on canal irrigation. Only two medium farmers have area under drip or sprinkler irrigation as they grew high value crops. Interestingly, there are very few tractors and trailers around, but more of bullock carts and even pickup trucks. Among the farmers, 33.3 per cent of the marginal, 81.2 per cent of small, 66.7 per cent of semi-medium and 50 per cent of the medium used hired tractor for land preparation.

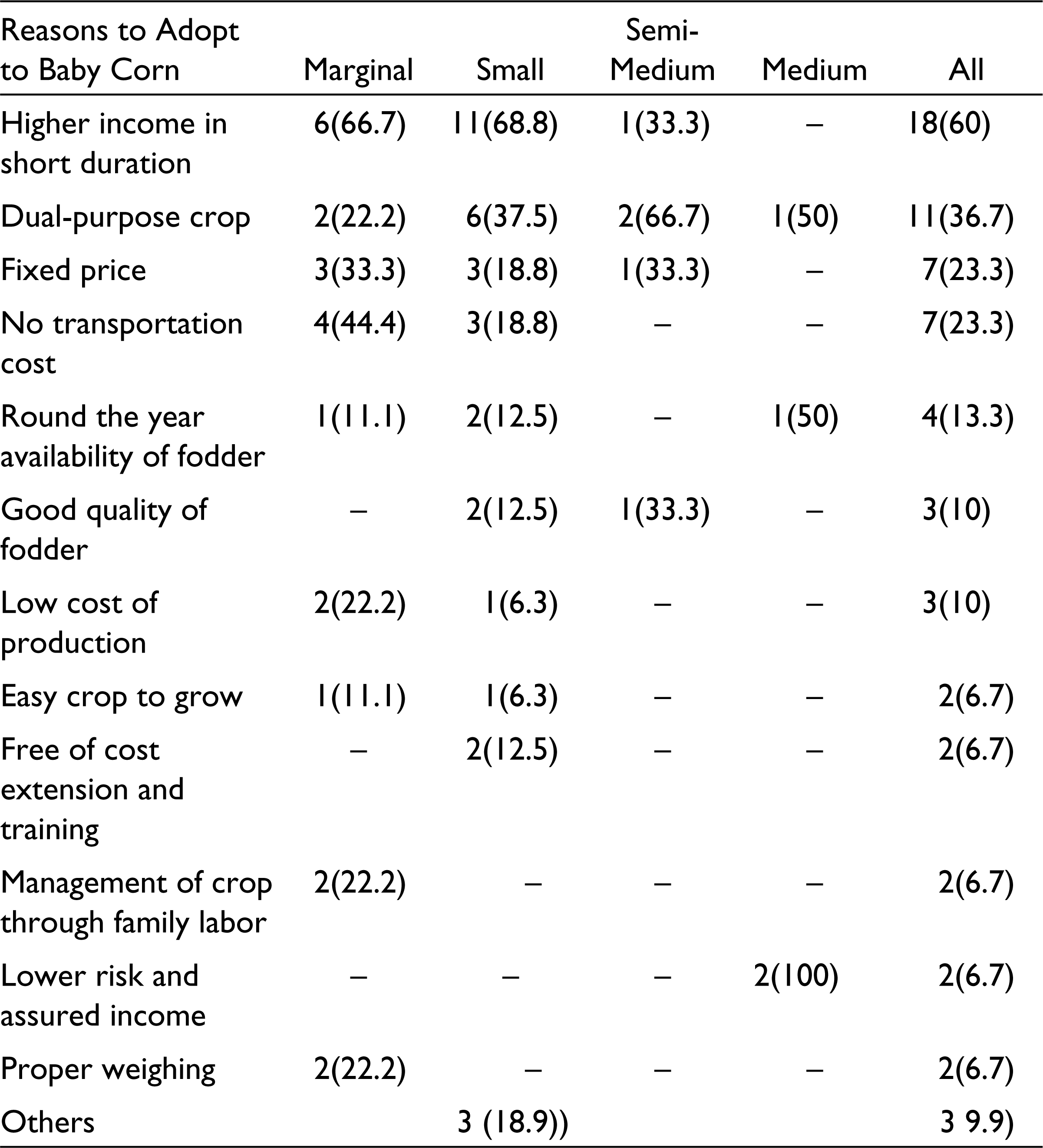

The contract with the company is the major reason for getting into cultivation of baby corn (67%), with small and marginal farmers also learning about it from other farmers (20%) or both the sources (13%). Baby corn fits the local context as it is perceived as a short duration crop, which is suitable for small farmers, and gives high income besides giving fodder as a byproduct (Table 4). Major factors in higher income after baby corn contract are as follows: better extension (73%) and, therefore, lower cost and higher yields; higher yield due to seed quality (53%), lower cost due to farm pick-up (37%) and also quality-based higher price (27%) and fixed prices (30%), besides lower wastage due to better practices (13%).

Category Wise Distribution of Farmers by Reasons to Adopt Baby Corn

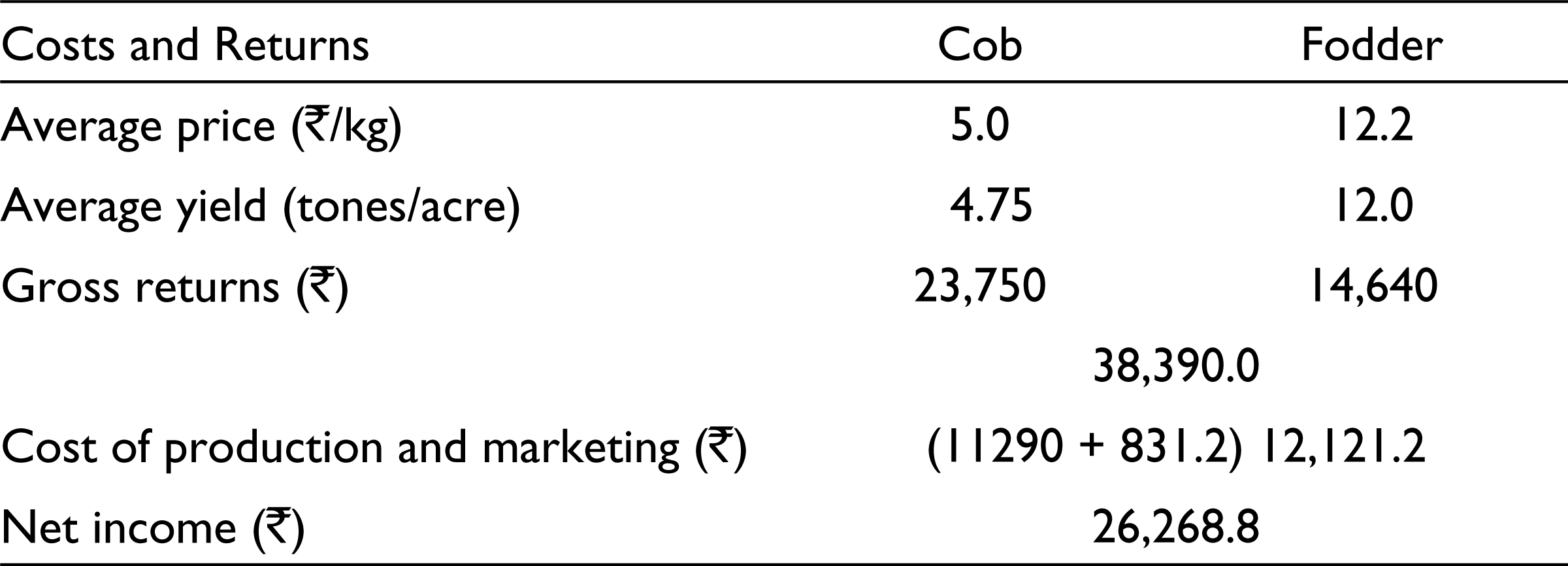

Seed and fertilizers are major costs in baby corn cultivation, accounting for 17 per cent and 27 per cent of the total cost of production, with labor, especially harvesting labor, costs accounting for another 17 per cent and weeding about 14 per cent, which is the same as the cost of land preparation (Table 5).

Costs and Returns in Baby Corn (Per Acre)

About 26.7 per cent of farmers are of the view that after linkage with the company, not only the quality of baby corn, but also of the other crops has increased. In baby corn, yield has increased due to timely harvest, and thus rejection rates are also lower. In all, 56.7 per cent of farmers agree that Global Gap certification has to be adopted strictly. For 16.7 per cent of farmers, supermarkets such as Star Bazaar and Big Bazaar were the new markets. Farmers not only started to supply baby corn but also vegetables such as cauliflower, cabbage and beetroot to these new markets. Half the farmers report that because of the technical guidance, inputs were used in proper ratio as per requirement of the crop. As per the need of the company, farmers also started to undergo soil testing before the sowing of the new crop, and 40 per cent also report that water usage in the crops has reduced. Some farmers started to use sprinkler for irrigation. Besides providing the extension and training to the farmers regarding the cultivation of baby corn at fortnight intervals, the company also arranged first-aid trainings (accidental) and Global GAP ‘group’ trainings for the farmers. After linking with the company, 13.3 per cent of the farmers started to use organic manures in sugarcane. Increased use of family labor was reported by 40 per cent of the farmers.

Baby Corn Farm Workers: Profile and Work Dynamics

A majority of farmers do not resort to the use of hired labor, but 30 per cent of the small and semi-medium landholders have to combine hired labor with family labor. Furthermore, 56.7 per cent of the farmers reported difference in men and women worker wages because of the task differences. The farmers pay ₹80/day for weeding, ₹100 for sowing and ₹120 for harvesting of baby corn to women workers, who form the largest part of the workforce for these activities. Men are largely concentrated in ploughing- and irrigation-related work and receive between ₹125 to ₹200/day. For both women and men, these daily wage rates are even lower than those under Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS). Contracted women and men workers receive only ₹100 and ₹150, respectively. On the other hand, permanent attached workers get ₹200/day per pair of husband and wife workers if they are local residents, or a 6-monthly rate of ₹45,000 per pair if they are migrants. Permanent migrant labor is also given food grains, one pair of clothes and some medicines. The permanent local workers are paid only wages. The farmers extend credit only to the permanent workers.

The wages are paid daily to the new casual workers, whereas regularly hired casual workers are paid weekly. Casual labor is usually hired from the same village. If the farmers do not find the casual labor in the villages, then they search for labour in other surrounding villages. Casual labor works from 10

The survey shows that 78.6 per cent and 87.5 per cent full-time women and men farmworkers belong to nearby villages. The average age of the men and the women workers is found to be about 32 years and 35 years, respectively. Furthermore, 50 per cent of men workers are married, 37.5 per cent unmarried and 12.5 per cent divorced. In the case of women workers, about 93 per cent are married and 7 per cent are divorced. About 50 per cent of men workers are Thakkars, 37.5 per cent Maratha and 12.5 per cent Adivasi (scheduled tribe). The profile of women workers is similar, that is, Thakkars represent 43 per cent, Maratha 36 per cent and Adivasi 21 percent. Most of the men and women workers speak only Marathi, except for one man and women worker each who speak Hindi as well. Of the total workers, 37.5 per cent of men and 50 per cent of women never went to school, whereas 12–14 per cent of men and women workers each have education between first and fifth standard, and 36–37 per cent of men and women workers each have between sixth and ninth standard. Only one male worker is a matriculate. Thus, the average number of years in school is only 4.4 in case of men and 3.5 in case of women workers. In total, 80 per cent of men workers have mobile phones, in contrast to only a small percentage of women workers.

The average land holding is 1.28 acres in the case of women and 0.66 acres in the case of men workers. One livestock, mostly cow or goat, is possessed by 71.4 per cent of women and 62.5 per cent of men workers. The average number of years in farm work is higher for men workers (9.19 years), compared to that of women workers (8.25 years). However, women workers have a relatively longer presence (greater than 3 years) in baby corn work, in comparison with the men workers. About 35.7 per cent of women and 50 per cent of men workers have Below Poverty Line (BPL) cards. Only 7.1 per cent of women and 12.5 per cent of men workers have MGNREGS cards, whereas 78.6 per cent of women and 62.5 per cent of men workers have ration cards. The ATM cards are possessed by 14.3 per cent of women and 12.5 per cent of men workers.

The Wage System

The permanent workers stay at the farmhouse of the farm owner and are provided with all the basic amenities, such as living room, toilet, bathroom, television, firewood and drinking water from the well. Their electricity expenses are also borne by the farm owner. The permanent workers reported that they have to work for seven to 8 hours a day for 6 days a week. Saturday is usually off, because it is the day for the weekly market at the village. Workers are also provided with food grains, clothing and medical care. The wages are generally revised yearly based on prevailing wages in the locality and labor availability in the area. If there is a labor shortage, farm owners are willing to pay more. Permanent workers also reported that the farm owner keeps ₹1,000 per month as caution money and gives it during any emergency to the worker. These workers could avail two casual leaves per month. Besides that they are also given leave of 10–15 days during the crop off season. The children of the permanent workers stay at the house, and one woman among the farm workers’ family looks after them.

The casual women workers are paid daily wages of ₹60–₹70 for weeding and sowing and ₹100–₹120 for harvesting. Casual men workers are paid ₹200/day for ploughing and ₹150/day for spraying. They work from 10

About 58 per cent of women and 75 per cent of men workers reported health and safety problems while working on the farms, which include pain in legs, arms, back and swelling in feet. Some women workers reported that it is difficult for them to do domestic work at home after doing the farm work. About 41 per cent of workers reported that they have to work on the farm even when sick to avoid wage cut. Only in the case of about 36 per cent of women and 25 per cent of men workers, health expenses were borne by the farm owners. About 42 per cent of women and 25 per cent of men workers have awareness about NREGS. They reported that wages in MGNREGS are between ₹100 and ₹125/day and one person per family could get three to 4 months’ work under this program. Many workers reported that they would not do the MGNREGS work next year due to low wages, non-regular employment, non-suitability of work and distant location of work.

About 36 per cent of workers reported that they would continue as farm workers because of higher wage rates in baby corn farming. Of the total, 23 per cent attributed their continuation in farming to lack of skills in other sectors, 18 per cent to good relations with employers, whereas 9 per cent reported that they would continue as they did not have any other option or regular employment. Fixed working hours and easier work in farming were also reported as some reasons to carry on work as a farm worker.

About 50 per cent of men workers want to remain as farm workers even after 10 years. About 87.5 per cent of women workers would like to continue their work as farm workers to sustain their families and settle their children. However, 21.4 per cent of women workers reported that they would stop once they developed their own land for cultivation and their children became independent. They also reported that due to lack of skills, they could not get job elsewhere. Most of the workers are not in favor of their children following them into farm work.

Pack House Workers: Profile and Work Dynamics

The pack house workers belong to the nearby villages and are situated within a radius of 25–30 km from the pack house at Pimpalgaon in Niphad taluka of Nasik district. All the workers work full time in the pack house. The average age of the women workers is 27 years and that of men is 26 years. About 60 per cent of men workers are unmarried. A majority of women workers are married (58%). Furthermore, all men and 68 per cent of women workers were Hindu, and 32 per cent of women workers Muslim by religion. The average numbers of years in school turned out to be 6 years in the case of male workers compared to 5.5 years in case of female workers. On average, men workers are associated with the pack house for 2.7 years, and women workers for 2.9 years.

The workers generally work 25 days per month. The workers are given leave on Saturday due to the power cut, and when there were no export orders. If there is an increased workload, then workers from the same neighborhood are granted casual leave in groups. Workers are not paid for leave on Saturday, or any casual leave availed and off day due to absence of export orders. The women workers are generally paid ₹100/day; those working in packing are paid ₹110/day. The men workers are paid ₹150/day. All workers including women supervisor are paid weekly, usually on Tuesday or Wednesday, in cash by the employer due to the weekly market on Wednesday.

Usually, there is no extra wage for overtime work in the pack house. However, during oversupply and increased export orders, workers are paid an additional ₹15–20/hour. All these workers are directly employed by the facilitator who provides the pick-up and drop-off facility to the workers. For this purpose, he has hired four four-wheelers at a daily payment of ₹1,500. All the activities that are needed to be carried out are generally specified to the workers by the men supervisors.

The training to the workers is given not by the facilitator but by the company who arranges an induction program for new workers, which orients them about the processes from the start to the end. Training is also provided based on group (operations). Sometimes, individual training is also given for specific tasks. Training is given on what should be allowed inside the pack house and in hygiene (for example, if workers go to the toilet, they should wash their hands). One worker in the pack house distributes the Iso Propyl Alcohol (IPA) solution in the pack house after every hour so that workers maintain clean hands. They are also trained to use the Sodium Hypochloride solution to clean plates, chopping tables and knives at the end of the day. Wearing caps and aprons is mandatory for the workers working inside the pack house. If the company finds a new buyer for export whose size requirements are different, then the workers are trained again on how much to trim the baby corn in terms of length and diameter.

About 68 per cent of women and 40 per cent of men workers have BPL cards. Only 5 per cent of women workers have MGNREGS cards. None of the men workers have MGNREGS cards. All women and 80 per cent of men workers have public distribution system (ration) cards. About 16 per cent of women and 20 per cent of men workers also use ATM cards to withdraw cash.

Of the total, 32 per cent of women workers reported that they work in the pack house even when they are sick. Of these, 83 per cent reported that if they do not work, their wages would be deducted. On the other hand, about 42 per cent of women workers do not work when they are ill. Among men workers, 40 per cent of workers worked when sick, as all revealed that as otherwise their salary would be taken away.

All workers opined that they would continue to work on the pack house. Of these, about 29 per cent reported that they work due to higher salary, while another 21 per cent reported their continuation to fixed working hours. Pack house as a safer place to work due to the presence of more women workers was reported by about 17 per cent of workers; 12.5 per cent of workers attributed their working with the service provider to location of work near to their place of living and good working conditions on the pack house; 8 per cent each opined that they continued on the pack house due to the timely and transparent system of payment. Round the year availability of work, good quality of work, relation with the service provider and availability of work at one place are some of the other reasons reported by the pack house workers to continue their work.

The Gendering of Tasks in Farms and Pack Houses

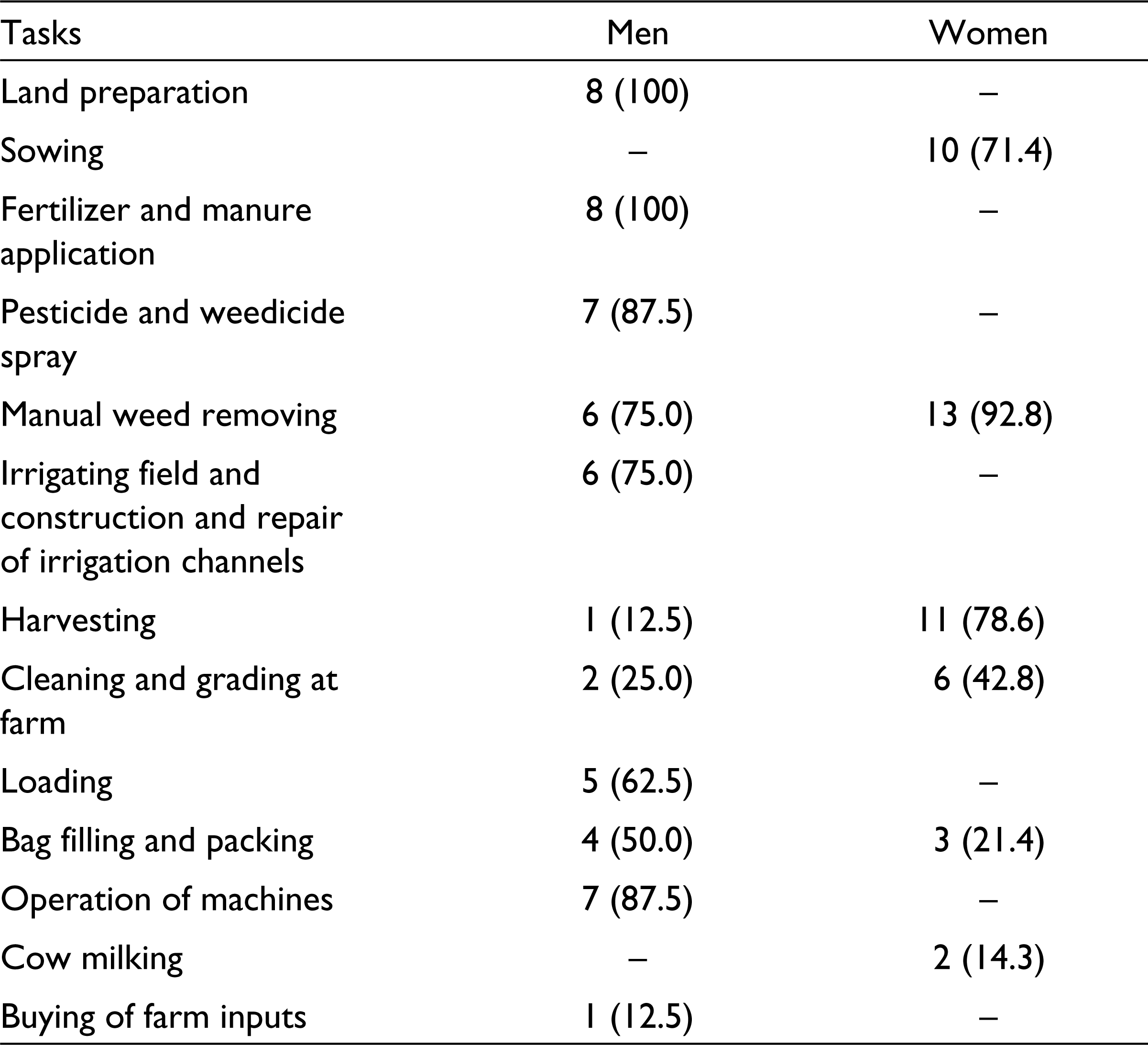

The permanent men workers are hired for land preparation, operation of machines and for applying fertilizers, manures, pesticides and weedicides. They also undertake works related to irrigation. Harvesting, packing in gunny bags and grading could be carried out by both men and women casual workers. Sowing, harvesting and weeding are the major activities in baby corn primarily carried out by casual women workers (Table 6). The contractual women workers are commonly hired for farm operations such as sowing, weeding and harvesting in the Shiror taluka of Pune district. The contractor remains on the field and supervises workers. This system is mainly used in baby corn and onion. The permanent women workers also feed animals, milk cows, etc.

Distribution of Worker Responses on Gendering of Tasks by Task and Type of Worker

In the pack house, men workers carry out the unloading of the produce, putting produce in the crates, moving produce to the cold store, moving empty/filled crates in the pack house and slitting, whereas women workers mostly peel (husk and silk removal), grade and weigh the graded produce. Punnet packing and putting produce in punnets are the activities at the pack house, which can be carried out interchangeably by men and women workers.

About 87.5 per cent of women and all men workers reported that the farm owner specifies the different farm activities needed to be carried out. Half of women workers are of the view that they should be paid the same wage as that of men workers. On the other hand, only 12.5 per cent of men workers are in favor of equal wages for men and women workers. About 79 per cent of women workers are of the view that men and women doing the same or similar work should receive the same wage, as they are of the view that both men and women workers work for the same duration in the pack house. Additionally, 83 per cent of men workers and 21 per cent of women workers are against the same wages for both men and women workers, as they opined that men workers work harder than women and were generally head of the household. All men workers and 63 per cent of women workers reported that their wages were revised on yearly basis. The wages increased by ₹10–15/day for workers and ₹1,000 per month for supervisors. No worker reported any discrimination of any kind by service provider, supervisor and the company’s pack house staff.

Upgrading of Stakeholders: Service Providers, Farmers and Farm and Pack-House Workers

That value generation and value sharing is the crux of the sustainable value chains was communicated by the service provider when he stated that, ‘[o]f the value generated in the chain, farmers and packer get 20 percent each and 60 percent goes to exporters and supermarkets’. Besides this, the other indicator of whether value created in the chain is shared is upgrading of suppliers, farmers and workers, which is discussed below.

Service Provider (FAC) Upgrading

The FAC has upgraded its business in terms of having its own pack house catering to higher volumes. In 2007, FAC packed 117 tonnes of baby corn, which increased to 350 tonnes in 2010. It started operations in Nasik district in its Dhindori taluka and has now moved to Kalvan and Navgav in Nasik and Pune and Karad districts. They have also been approached by another exporting firm but are not able to cater to it because of the limited capacity and the motive to limit risk. In terms of product upgrading, this is the first supplier to supply ‘residue free’ chillies to FF since 2009. It has also started packing chillies in 200-g packs, as per new orders and grapes in punnets and pouches. In terms of functional upgrading, whereas earlier it was involved only in harvesting and packing of grapes, now it is doing the entire cycle from growing to packing in baby corn.

The service provider margin came down from 35 per cent in 2004 to 15 per cent in 2011, but as volume had gone up, income was still increasing. This can be called upgrading, although it is not one of those traditionally considered to be so—product, process, or functional—but just a scale-up of the same product, as pointed by Ponte and Ewert (2009).

Farmer Upgrading

The average area planted under baby corn had increased by 50 per cent, the yield by 6 per cent, and the price by 40 per cent, all in nominal terms over 5 years from 2005–2006 to 2010–2011. The export quality produce was only 50 per cent of the total produce in 2005–2006, which had increased to 70–80 per cent by 2010–2011. An indicator of farmer well-being in the baby corn value chain is that the area under the crop had grown from 0.6 acres in 2005–2006 to 0.9 acres on an average, and the average price had risen from ₹3.5/kg to ₹5/kg over the 5-year period. As far as certification is concerned, it was reported that sometimes some farmers show their house facilities as farm facilities for workers to get Global Gap certification as they live on farm. Also, ‘on paper, all farmers and area is Global Gap certified but actually some produce from non-certified areas and farmers also goes for exports’ (FAC). About 90 per cent of the farmers reported changes in asset acquisition after linking with the company, especially acquisition of pucca houses, refrigerators, cooking gas and two-wheelers and cars to some extent. About 67 per cent had color TV, 43 per cent pucca houses, 60 per cent had two-wheelers and car and fridges were owned by only 10 per cent. Even cooking stove and cooking gas were owned by only 27 per cent. However, all farmers had mobiles, which they used more for availing extension advice from specialists (73%), buying agricultural inputs from dealers (57%), contacting labor for farm work (40%) and also for obtaining market price information from output agents and traders and custom hiring agricultural machines and equipment from other farmers. Some used mobile-based calendar for the sowing date and other reminders for input use.

Since 2010, farmers are provided with free information on package of practices (PoP) through PACS and Indian Farmers Fertiliser Co-operative (IFFCO) Kisan Sanchar (Farmer Communication) Ltd. (IKSL), which is a tri-partite venture of Star Global Resources (35% equity), IFFCO (35% equity), and Airtel (30% equity). Since 2007, FF, a sister concern of Bharti Airtel, has been providing green Sim cards to farmers who can receive five voice calls in a day in the local language for a user fee of ₹100. They also have access to a helpline and expert opinion. Three farmers (10% of total sample) had also become producer organizers/facilitators for the company, as they were assigned the role of sub-service provider. They also supplied their own produce.

Farm Worker Upgrading

FAC claims that it supplies gloves, caps, aprons and first-aid kits to workers. It claims that wages have increased by 80 per cent from 2004 to 2011, with women’s wages increasing from ₹82 to ₹150 and men’s wages increasing from ₹100 to ₹200 in the same period. About 42.8 per cent of women and 37.5 per cent of men workers found baby corn to be a safer crop to work with, in comparison with others, because they found it to be less labor intensive; it has low doses of fertilizer application and there is no spraying of any pesticides that adversely impact on worker’s health. Some of the workers receive tea, drinking water and healthcare facilities. One permanent worker reported that he could get money and two wheeler in emergency from the employing farmer.

About 36 per cent of women workers also reported that they gained new skills such as knowledge of type of produce to be harvested while working in the new crop such as baby corn. About 35.7 per cent of women and 25 per cent of men workers reported that they had gained more respect from employers due to the skills in working with baby corn and the labor shortage in the area. Two permanent workers reported that their employer treats them like family members, due to the importance of their work. About 14 per cent of women workers reported that the employer provides drop-off facility if they sometimes get delayed at work. Most of the workers reported that they do the fixed amount of work on a given day. For 35.7 per cent of women workers, harvesting is an easier job, as they stand while carrying out the operation in baby corn, whereas they have to carry out harvesting by sitting down in respect to all other crops. For 25 per cent of the men workers, use of tractor, basal application of fertilizers and packing of baby corn were new tasks for them. Bag filling in baby corn was new work for about 14 per cent of women workers. In total, 21 per cent of women workers reported that they had to harvest the crop very carefully and timely to avoid the rejections at the pack house. Most of the workers reported that they were given training by the farm owner while working in the field. Some workers who also owned land and cultivated baby corn received training from company extension officers and farm owners. Some women workers who were hired through contractor were guided by contractor and farm owner. The training was mainly given for sowing and harvesting in the baby corn.

About 62 per cent of men workers reported that the average wage rate for men increased from ₹48/day in 2000–2001 to ₹90/day in 2005–2006, and further to ₹140/day in 2010–2011. Similarly, 71 per cent of women workers reported that average wages for women had increased from ₹37/day in 2000–2001 to ₹72/day in 2005–2006, and to ₹110/day in 2010–2011. The average number of days worked during a year had also reportedly increased during 2010–2011. The major reasons reported for increase in the wage rate and working days were: increase in demand for skilled labor, emergence of new crops for export and inflation. About 37 per cent of men and 7 per cent of women workers found that training hours had also increased over the previous years due to the emergence of new work in crops like baby corn. Men and women workers also agreed that their work composition had also changed from casual to regular, and less skilled to more skilled; 12 per cent of men and 14 per cent of women workers reported that they could now avail casual leave; 14 per cent of women workers reported that they were now getting the pick-up and drop-off facility. Workers also found that workplace discrimination had declined, alternative employment opportunities had increased and terms of work for women workers had improved over the years.

About 53 per cent of women workers revealed that women’s wage rate had increased from ₹68/day to ₹100/day over the same period. The average number of days wad also reported to have increased over the same period. About 53 per cent of women and 60 per cent of men workers reported that the number of training hours had also increased during the last 5 years. In total, 40 per cent of men and 16 per cent of women workers reported that they had become more skilled during the last 5 years. About 11 per cent of women workers became regular pack house workers; 20 per cent of men workers had reported that they could now avail advances and casual leaves; and about 5 per cent of women workers reported that pack house facilities had increased since the last 5 years. Workers also reported that workplace discrimination had now disappeared. Many workers reported that alternative employment opportunities and better terms of conditions for women workers had become better. On an average, men were able to get employment for 22 days a month with an 8-hour workday, and women for 18 days with a 7.5-hour workday.

However, the associational power of workers (Selwyn, 2007) is missing, as there is no unionization of the workers; they are all casual labor and work as agricultural labor as well as on their own farms during off season, and are employed in farms and pack houses through contractors. None of the pack house workers reported any collective bargaining of wages with the employer.

Pack House Worker Upgrading

As far as pack house workers are concerned, the working conditions are reasonable. The pack house has washrooms, eating place for workers and a changing room. Workers are not given any tea break and only a 1-hour lunch break. The only injury to workers can be in slitting and cutting of cobs that leads to finger cutting, which happens once or twice a week on an average at the pack house. On the other hand, economic upgrading in terms of nature of employment has not happened, as, of the service provider’s total labor in baby corn in 2004–2005, 40 per cent of workers were regular, which remained the same even in 2011. Labor, which had been working with FAC for more than 1 year, was less than 40 per cent in 2005–2006, as well in 2010–2011.

Workers revealed that all processes in baby corn processing in the pack house are safer. Packing the produce through machines and passing produce through the metal detector are the new processes and machines with which to work for some of the workers. Workers gain new skills through continuous periodical trainings. They become aware of how to keep the surroundings neat and clean. Some of the women workers who carried out the peeling felt that their assignment was safer than other workers who were doing slitting and trimming, where there was chance of the finger injury. Many women workers reported that they felt safe to work in the pack house due the presence of more women workers. The workers also receive workplace facilities such as a 45-minute lunch break, clean drinking water and toilet facilities. They also felt that it was easy to work in the pack house due to air-conditioned facilities. Earlier, all workers in the pack house had to carry out all activities. With the passage of time, there was differentiation of activities, which made the routinized work easier for workers.

The service provider provides the pick-up and drop-off facility to the workers. Moreover, workers have to work for only 8 hours. During extra supply orders, workers are paid for overtime. Even if any assignment is carried out wrongly by the workers, the procedures are explained in a polite manner. Workers earn more respect from the employer because of their skills in baby corn. The job is made easier by shifting between the different activities in the pack house. They opined that shuffling gave better opportunity to work and learn by interacting with different employees and did not get bored from work.

Since the crop was new in the area, all the operations in the baby corn were new. It generated more employment opportunities in the area. One male and two female workers were promoted to the role of supervision. Workers also reported that they get regular work in the pack house as earlier they were casual workers. As casual workers, they received low wages and irregular employment and had no lunch time. Learning of new kinds of work was due mainly to interchange of roles assigned.

Another measure of worker upgrading or downgrading could be obtained from the fact that companies like FAC also violate labor laws, although this can cause trouble if they are caught. That goes to show that even minimum labor laws are not being complied with. There was even a case of one of the service-providing companies, related to FAC, being wound up due to labor regulation violations. No worker is given work for more than 60 days regularly to avoid labor laws regarding regularization of casual workers. However, the workers are picked up and dropped off to their place of residence by FAC, which shows workers get more respect now, and this represents social upgrading. Even the structural power of workers (Selwyn, 2007) in the pack house operations was not observed, as the opportunity cost of labor is low in local areas and, therefore, cannot be used to create hurdles in export-oriented processing operations.

Conclusions

The above case study of baby corn export value chain in India shows that GVCs can be inclusive of small producers and suppliers provided mechanisms are created at the global and local levels of the chains. In the case of baby corn, it was due to the provision of PMO under Global GAP that small producers could be certified as a group, which lowered the cost of certification and also made the exporter responsible for getting produce to the standards as a PMO. Furthermore, the case study shows that the chain networks are locally well-entrenched and have leveraged local systems of labor mobilization and management from existing networks. Supermarket standards have led to upgrading for some workers (especially at the pack houses), but also downgrading through the use of contractors to increase flexibility to cope with cost pressures from supermarkets.

The above case study shows that it is possible to include smallholders in high value chains in crops like baby corn that are less expensive to grow and fit with the local needs, such as dairy development, as seen in the use of byproducts. Thus, it is possible to identify suitable crops for smallholders and value chains without putting farmers at risk.

What emerges as crucial is the role of service providers who are the real drivers of local systems for export production, as they belong to local areas and leverage their networks for production and labor supply. In other contexts, they are known as brokers, for example, in the grape export sector in Brazil (Bonanno & Cavalcanti, 2012). The exporters only engage in minimum interface with farmers as required due to certification systems, that is, smallholder group certification and traceability requirements, which are indirectly enforced by supermarket buyers. It was common in baby corn and grape in India to find a service provider working with multiple exporters or managing multiple leased pack houses or crops.

The above analysis also shows that although there are plenty of standards being brought into food value chains by global buyers, they often do not percolate down to the farms and workers, as seen in other similar contexts (Bonanno & Cavalcanti, 2012). They are either not implemented at all or implemented poorly. There are also local conditions, which do not permit adequate implementation of such standards, as there are cost pressures on smallholder producers who employ workers on farms. The contract labor arrangement has also led to poor enforcement of labor and wage standards, as the buying agencies do not employ workers directly and, thus, do not feel liable for ensuring labor well-being and conditions of work. The buyers depend on agencies and formal procedures to enforce standards and do not undertake adequate monitoring, which has cost implications. The supermarket buyers are more concerned with the quality and regular supply and managing the interface with producers.

In fact, labor processes also differ in terms of activities required in harvesting and packing, depending on whether produce is meant for export or domestic market. This was also observed in Brazil, where grapes meant for export had 34 operations per harvest cycle compared with just 9 for domestic market (Selwyn, 2012). This leads to differences in labor processes and workers’ structural power in the chain, although in the Indian context, harvest and packing workers were not able to translate this structural power to their advantage, as there was no worker unionization and the opportunity cost of labor due to abundant local labor supply was low.

Skilled labor required for baby corn is provided by contractors, as it is traditionally locally available in and around the state, although facilitators/pack house operators would not like to directly employ labor for various reasons. In such situations, it is important to bring in the worker interest by way of wages being part of the compensation terms for farmers and other intermediaries. Whenever workers are organized, that helps in getting better work conditions and wages. But, there are no non-government organizations (NGOs) involved in helping such groups in better bargaining or cleaning of the GVCs in any significant way. The role of the state is not effective as of now, as farm sector minimum wages are not enforced. MGNREGS has helped some worker communities in low wage areas, but, in high-value crop work like grapes or vegetables, it does not seem to make a difference. Furthermore, since there is a predominance of women workers in such networks, there is need to bring in more gender equitable work conditions, which make the lives of women workers safer and better as they help the chains perform better and remain competitive. This can be part of the chain driver’s strategy, as well as of the workers’ unions or NGOs in such situations.

While attempting upgradation of networks, upgrading of workers needs to be prioritized, alongside that of growers, in order to make them better workers as well as entrepreneurs who could take up part of the value-addition activity as groups or associations. GPNs are not just about value creation and capture by the driver, but also about value sharing with others, especially weaker/smaller stakeholders in the chains, from a livelihood perspective.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received financial support for field work for this research from University of Manchester based project ‘capturing the gains’ during 2012–2014.