Abstract

Abstract

Agent banking involves the provision of banking services through non-conventional means such as retail outlets with the use of technology. In developing countries, such as Bangladesh, agent banking acts as a medium between the rural unbanked majorities and banking services that they would otherwise not have access to. The case analyzes how innovation in the banking sector can aid poor people to gain access to financial institutions through the Agrani Doer banking business model. It elaborates on the rules and regulations of agent banking and how the first state bank of Bangladesh, Agrani Bank, establishes coverage to places not deemed possible before. The concept of agent banking, in an illustrative case, is linked to Ansoff’s Growth Matrix as Agrani Bank uses technology and innovation in its business strategies to achieve its desired growth goals.

Introduction

Bangladesh is a developing country located in the northeastern part of South Asia. As of February 2018, it is estimated to host an immense population of 165.748 million (Worldometers, 2018). Being the 44th largest economy in terms of gross domestic product (GDP), which stands at USD228.4 billion (The World Factbook, 2017), Bangladesh has achieved a staggering 6 percent growth in average annual real GDP over the past two decades. With rising exports (USD 34.835 billion, July 2016–June 2017), remittances from workers (USD10.591 billion, July 2016–June 2017), and positive current account balances, the country is now shifting away from its agrarian structure (15.1 percent of the GDP) to a manufacturing (28.6 percent of the GDP) and service-based (56.3 percent of the GDP) economy. Within the thriving service sector, the banking industry plays a vital role in the economy of Bangladesh, as it contributes to all other sectors through credit disbursement, recovery, and trends in growth. However, a large amount of the Bangladeshi population has no physical access to financial institutions. While traditional banking services are provided through branches, automated teller machines (ATMs), and the Internet, a majority of Bangladeshi citizens cannot reach these locations. As a result, agent banking becomes a more feasible option. To ensure greater financial help for the masses, Bangladesh Bank (Central Bank of Bangladesh) has prepared guidelines for agent banking.

Agent banking happens through retail outlets in the nation’s rural areas. From the bank’s perspective, it no longer has to incur costs for setting up a bank branch. For the public, agent banking is a way to access services and to complete financial transactions safely. For agents, it is a way to generate additional income by providing banking services (Tarazi & Breloff, 2011).

Current Financial Market and Agent Banking

Bangladesh Bank has control over the monetary policies of the government as well as all the commercial banks. Following the country’s independence, the government had initially nationalized the entire domestic banking system, proceeding to reorganize and rename the various existing banks. In the 1980s, however, the privatization of commercial banks revolutionized the overall banking system (Alam, 2000). Over the succeeding years, the banking sector of Bangladesh has gone through radical changes under the supervision of Bangladesh Bank. Currently, the country has 57 scheduled banks that operate under full control and supervision of the Bangladesh Bank, empowered through Bangladesh Bank Order, 1972 and Bank Company Act, 1991, respectively. The present banking sector can be segmented into five major categories: state-owned commercial banks (SOCB), private commercial banks (PCB), specialized banks (SDBs), foreign commercial banks (FCB), and financial institutions (FI) (Ahmed, Nisha & Rifat, 2016).

State Owned Commercial Banks (SOCBs)

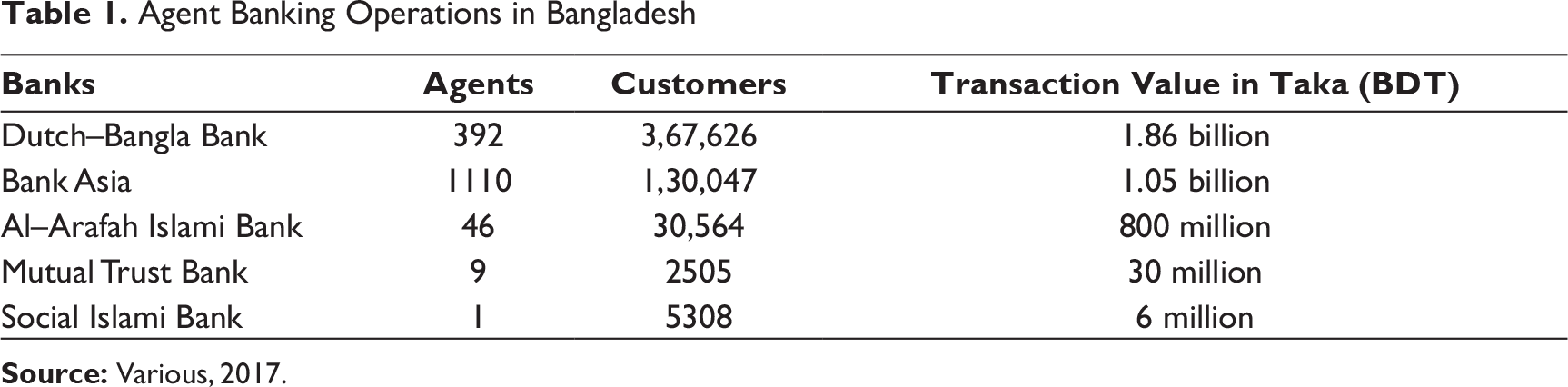

There are six SOCBs (over 3750 branches) that are fully or majorly owned by the government of Bangladesh. Among the state SOCBs, only Agrani Bank offers agent banking.

Private Commercial Banks (PCBs)

There are 40 PCBs that are majorly owned by private entities. The PCBs can be categorized into two sub-groups as follows:

Conventional PCBs

There are 32 conventional PCBs that perform conventional banking functions. Among them, six PCBs offer agent banking services in different parts of Bangladesh.

Islami Shariah–based PCBs

These banks operate their activities based on the Islami Shariah principles. There are eight Islami Shariah-based PCBs in the nation.

Specialized Banks (SDBs)

There are two SDBs in operation which have specific objectives like agricultural or industrial development and are fully or majorly owned by the government of Bangladesh.

Foreign Commercial Banks (FCBs)

There are nine FCBs in the country whose main branches are located abroad.

Financial Institutions (FIs)

These non-bank FIs are managed by the Bangladesh Bank and regulated under the Financial Institution Act, 1993. There are 33 FIs in operation where two are fully government-owned, one is a SOCB subsidiary, 15 are private domestic initiatives, and 15 are joint venture initiatives (Bangladesh Bank, 2018).

However, despite the large number of banks in operation, the multitudes, especially in the rural areas, still could not avail banking services. Hence, the concept of agent banking emerged to take banking facilities to the doorstep of all.

Agent Banking Operations in Bangladesh

Agent Banking Initiative: Bangladesh Context

Agent banking refers to financial services that are not carried out by conventional banks and instead use non-bank retail agents by relying on devices such as card readers, point-of-sale (POS) terminal, or mobile phones for real-time transaction processing (InterResearch, 2017). A banking agent is a retail outlet contracted by a licensed deposit-taking financial institution or a mobile money operator that allows it to provide a range of financial services to customers (Ogah, Okwe & Adeoye, 2015).

Prior approval from the Bangladesh Bank is required for banks to offer agent banking 1

Bangladesh Bank–approved agent banking includes the following activities:

º Collect small value cash deposits and cash withdrawals (ceiling is determined by BB. At present, a customer can withdraw and deposit two times per day; each transaction cannot be more than BDT 25,000.00); º Foreign remittance payment in local currency (BDT); º Facilitate small value loan disbursement and recovery of loans, installments; º Facilitate utility bill payment; º Cash payments under social safety net program of the government; º Facilitate fund transfer (ceiling determined by BB); º Balance inquiry; º Collect and process forms/documents in relation to account opening, loan application, credit and debit card application from public; º Post-sanction monitoring of loans and advances and follow-up of loan recovery. º Receive clearing cheque. º Other functions like collecting insurance premiums including micro-insurance.

Agents are prone to violate regulations mostly in two cases—when it comes to an option to make more profit violating the rule and regulations or oppositely if the regulation incur a cost to the business and second to entertain customer demands and maintain conventions/common practices. For example, authority has found many of them not printing auto-generated receipts after most of the transactions since they had to pay for the thermal paper roll. Another example of a common violation of a regulation is providing separate bank-like deposit slips to the customers when they deposit cash to the agent points as this is the conventional paperwork practiced in the branches through our system generates auto receipts and sends SMS notification after every transaction. To address the mentioned violation regarding printing and providing auto-generated receipts, first the concerned agents were issued a warning letter reminding them of the regulation. At the same time, field officers were instructed to counsel agents and monitor more closely for any repetition of such violation. Alongside with these steps customer awareness and literacy deemed necessary and for that reason, the bank displayed instruction boards in the agent points clearly mentioning not to leave without the auto-generated receipt. Warning and reminding of the regulation did not work right away for some cases and authority had to counsel them on how these violations may degrade overall service quality and make this trust-depended business fragile. Also, authority had to teach them why sign-sealed papers are unnecessary here and how to convince customers in this regard.

Additionally, the agents may face technical problems as they operate in distant rural areas with frequent power outages, weak Internet connections and lack of skilled technological support providers. In such cases, their services tend to be inefficient and slow which may lead to aggravated and dissatisfied customers. As such, banks are continuously developing to minimize these issues and create a more effective and efficient environment for agent banking. Moreover, agents are receiving training on how to handle customers’ queries and dissatisfaction patiently and effectively (InterResearch, 2017).

Agent Banking Business Model in Bangladesh

According to Bangladesh Bank’s Guidelines on Agent Banking for the Banks released in 2013, an agent can act on behalf of more than one bank at a time. However, at the customer endpoint, a retail outlet or subagent, an agent represents and offers banking services for a single bank. The agents are equipped with information technology (IT) devices that connect with the bank’s server mostly through cell phone–based Internet (i.e., GPRS) or other data connections (i.e., WiFi, 3G). The agent banking model, with a technology-based banking concept, ensures appropriate security with real-time banking for customers. Its transactions are integrated with the bank’s core banking solution. Magnetic strip bank cards or mobile phones are used to access the client’s bank account. Transactions take place in real-time through information and communication technology (ICT) devices integrated with the bank’s systems.

However, there remains a possibility of customers or retail agents committing fraud, or a bank’s equipment/other property getting stolen from an agent’s premises. Moreover, financial loss for banks or agents can occur from data leaks, hacker attacks, inadequate physical or electronic security, and/or poor backup systems (Lyman, Ivatury & Staschen, 2006). Apart from all other known risks in providing retail banking and financial transactions, agent banking specifically has a risk of robbery and hijacking during cash handling and cash re-balancing to and from a nearby bank branch. As per the business model, all the cash required for agent banking belongs to the agent. The agent needs to deposit the excessive cash to a specific account at its linked branch while it may be required to bring back cash in case of low liquidity. As agent banking covers rural and remote areas, linked branches are often far from the service points. Thus, carrying cash worth few hundred thousand on a regular basis is very risky.

To mitigate the risk, the authority has tried to select agents with regular cash handling experience and existing business network in the locality. Having the capacity to handle large amount of cash and a certain level of influence in the operating area allows these agents to take the risk. To manage the level of risk, agents are instructed to do the following:

Keep sufficient amount of credit in the account and cash on hand. Generally, every service area has a measurable demand for debit–credit amount and in cases that agents hold onto an amount exceeding the requirement, the need for re-balancing declines; Managing cash flow to and from his/her other business accounts more effectively to support this business; Maintaining good relationship with law enforcers.

However, transaction cannot occur if there is a failure in communication. A customer gets instant confirmation of their transaction through visual basis (screen-based like SMS text message), voice message (in case of Agrani), or article (debit or credit slip). The bank brands the agent banking business so that customers can recognize that the agent provides services on behalf of the bank. The agent, on the other hand, has to deposit a fixed amount of money or have a set credit limit with the bank to make transactions with clients. Any transaction tried beyond the set limit will automatically be stopped by the system (Bangladesh Bank, 2018).

Creation of Agrani Doer Banking

Agrani Bank Limited (hereafter ABL) is the first state-owned commercial bank in Bangladesh to introduce agent banking. It is a leading commercial bank with 941 outlets located throughout the country. The financial products and services of ABL can be classified as general (i.e., personal), corporate, business, agriculture, and rural banking, small- and medium-sized enterprise (SME) financing, merchant banking, banking for non-resident Bangladeshi, and Islamic banking. With the intent to include the people who are not under the banking net of Bangladesh in the financial arena, ABL established the Agrani Doer agent banking operation in 20 districts (out of 64) of the country with over 200 agents. A team of employees in ABL monitors activities around rural areas where sub-agents provide banking services through smart technologies. The bank has signed up for partnership with Doer Services Limited to serve the agent banking service.

Channel Partners and Process Ownership of Agent Banking Business

Operational Infrastructure

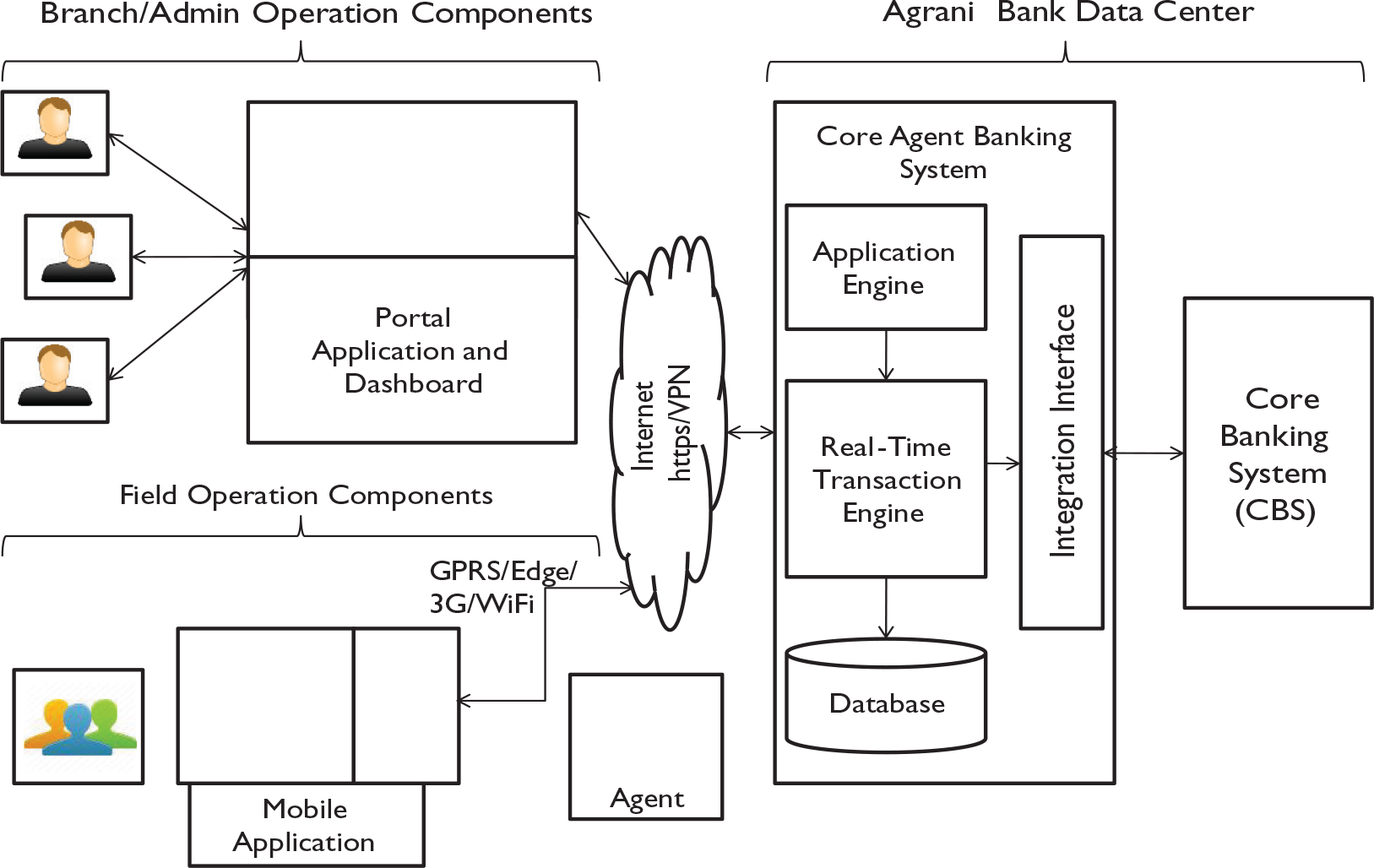

Infrastructure serves the company’s needs and connects its various sectors together, consisting of functions such as accounting, finance, planning, quality assurance, and general management. It enables effective operation of financial intermediaries of the bank including elements, such as payment systems, credit information bureaus, and collateral registries. Agrani Doer banking provides an end-to-end agent banking ecosystem through its technology infrastructure (Figure 1).

Cash in–Cash out Operations

With cash in–cash out operations, every transaction hits the sub-agent’s account, which the agent must maintain with funds to continue transactions. According to Agrani Doer, the combination of a “quick response card” and disbursement-point “biometric authentication” (fingerprint) helps reduce benefit diversion to unintended individuals. Both the government and customers benefit from this feature. With biometric authentication in place, incidences such as tampering with muster rolls with absentee names, names of deceased people, and issuing several identity cards in a single name are reduced. Figure 2 shows a scenario that describes a typical sequence:

Determining ABL’s Business-Level Strategy

Business-level strategies relate to the different ways that an individual business unit can compete in its chosen markets (Burnes, 2014; Vancil & Lorange, 1975). A bank must align its marketing strategies with its business strategies if it has to sustain in the existing challenging market. Similarly, ABL has to combine its tactics and strategies to achieve its growth goals.

Product–Market Expansion Grid

The product–market expansion grid (also known as Ansoff’s Growth Matrix) (Ansoff, 1957) is a widely utilized tool for marketing and strategic management. The grid presents four alternative choices to determine an organization’s growth strategies, which distinguish products and markets according to their technical and market novelty (Zeschky, Winterhalter & Gassmann, 2014). These consist of (a) Market penetration: by pushing existing products in its current market segments; (b) Market development: by developing new markets for the existing products; (c) Product development: by developing new products for the existing markets; and (d) Diversification: by developing new products for new markets. In the next section, we can observe how ABL has used the matrix to link its marketing strategies with its general strategic direction, thereby achieving growth.

Market Penetration

The penetration rate of commercial banks in rural areas is non-significant or very low (John, 2016). Despite efforts to increase access to financial services (including small-value BDT 10 account openings), the level of micro-savings have not been encouraging in Bangladesh. As of June 30, 2017, there have been 17.1 million BDT 10 accounts opened by banks with an estimated deposit of BDT 13.11 billion by the people. Moreover, loans amounting to BDT 538.2 million have been disbursed among the BDT 10 account holders by banks (Uddin, 2017).

In Bangladesh, ABL has a large client base in rural and semi-rural settings. With the development in the financial sector, it is easier for banks, who may be small players or new entrants, to gain market share since all the players are experiencing growth. There may be an opportunity to increase market share in segments that have been abandoned by other conventional banks (Ahmed, Ahmed, Shimul & Zuñiga, 2015). This is further possible due to the complexities related to creating a bank account, such as high minimum account balance requirements, account maintenance fees, and other similar factors, all of which discourage many civilians from opening bank accounts (John, 2016).

Market Development

A new avenue for pursuing growth through innovation is with nascent market applications (Meyer, 2007). Banks in Bangladesh have swiftly adopted various technological advancements, such as the use of ATMs, POS, credit and debit cards, mobile phones for banking services, Internet banking, online banking, and tele-banking. Moreover, mobile banking has emerged as the most effective platform for increasing the reach of financial services (John, 2016). At present, Bangladesh is estimated to have 145.114 million mobile phone subscriptions, with Internet access (over 80.483 million) spreading quickly across the country (Bangladesh Telecommunication Regulatory Commission, 2017). This platform is effective in increasing the reach of financial services, especially in new rural markets that are unbanked (John, 2016).

In Bangladesh, poor people cannot access basic financial options such as loans. The ABL targets new customers such as women entrepreneurs and small enterprises while Doer promotes Agrani loan products in concentrated areas. According to Agrani Doer banking, they are mainly opening savings accounts and are interested in targeting price conscious customers who want regular transactions or banking services as well as remittance beneficiaries, small entrepreneurs, and more.

Product Development

In the banking sector, new product development is an important aspect of service marketing (Edgett & Jones, 1991). Product innovation (i.e., small-value deposits, loans for women entrepreneurs) may allow a bank to serve new needs or improve a product position in relation to competitors (Sauer & O’Donnell, 2006). Due to high operating and set up costs, out of 57 banks, only a handful operate in rural areas as they are not very profitable. On the other hand, mobile banking can allow banks to operate at lower costs. This initiative can be achieved through agent banking customers along with the unbanked rural customers. Moreover, it may also enhance the differentiation of Agrani’s services.

Diversification

Diversification, as a strategic option, suggests that a bank will develop into segments that venture beyond existing products and markets. For a bank to be more focused, it must pay attention to its operating costs and service quality that can satisfy current customers while attracting new ones. In addition, banks must seek newer sources of income (Kotler & Fox, 1995). The ABL works for collective savings and deposit schemes for rural or unbanked rural people. Proper communication through advertising campaigns, social and religious gathering (i.e., Eid, puja), local celebrity/community leader endorsements, and innovative financial products (in the process of development by the bank) can further enhance the brand of Agrani bank.

Moving Forward

Banks can capitalize on relevant innovations; however, it is essential to maintain a physical presence within the mass market they want to serve, and to be well aware of the demographics of the people in this group (Rao, 2013). Agent banking is rapidly becoming recognized as a viable strategy in Bangladesh for extending formal financial services to the poor and rural areas. The agent banking model is evolving in the country. With the Bangladesh Bank Guideline on Agent Banking (2013), regulations now play a central role in enabling its spread. However, banks have been struggling in promoting financial inclusion through low-cost delivery models that are not only profitable but also protect customers and the integrity of financial services.

There is no one-size-fits-all regulatory solution for providing financial services through agents. Markets may experiment with a number of approaches before finding one that works. As a result, these agent banking regulations have adopted a test-and-learn approach, permitting financial sector experimentation, monitoring the market, and ultimately developing regulations based on identified market needs.

Acknowledgments

The authors gratefully acknowledge the aid of InterResearch, Bangladesh, to fund the study. They also convey appreciation to Mr. Ahmad Rasul (CEO and Managing Director) and Bony Tasneem (Vice President) of DOER for their insight, thoughts and input during the preparation of this case study.