Abstract

The present study attempts to examine the impact of microfinance on certain dimensions of women empowerment, namely economic, social, political and psychological. Quasi-experimental design comprising of control group (180) and treatment group (190) has been employed to assess the impact of microfinance on women empowerment. The findings revealed positively significant but moderate level of impact of microfinance on economic, political and psychological dimensions of women empowerment and only smaller overall impact on social empowerment. In addition, case studies further supported microfinance programme has substantially empowered women in terms of economic, political, social and psychological dimensions. More importantly, ambiguity over social empowerment was cleared.

Keywords

Introduction

Across the globe, women population, is poorer and often deprived of basic facilities such as healthcare, clean water, sanitation and education. Women’s work often goes unpaid and they are subjected to several forms of violence (United Nations, 2015). To end feminization of poverty, microfinance has been recognized as one of the major and effective interventions (Chant, 2014). Microfinance has been largely targeting women on certain grounds. First, women are credit constrained to start micro or small enterprises particularly in a male-dominated society where their role is confined to handling household chores and thus, women often fall under the debt trap of informal moneylenders and are exploited by them (Madichie & Nkamnehe, 2010). Second, women are considered as disciplined, good credit risk, that is, low on default rates and more likely to share their benefits with the entire family and improve children’s health and education (Fofana et al., 2015; Gomez, 2013). In India, women have been the primary target group of microfinance programmes mostly by mobilizing them in self-help groups (SHGs). Women are more likely to assemble together and form self-selected groups to address their common problems and in doing so, they ease up the work of microfinance providers whereby transaction costs can be saved to a greater extent. Thus, a huge number (90%) of SHGs formed belong to women only (Batra & Sumanjeet, 2012). The present article mainly focuses on microfinance services disbursed through a major mission mode programme ‘National Rural Livelihood Mission (NRLM)’ that replaced the earlier poverty alleviation programme ‘Swarna Jayanti Gram Swarozgar Yojana’ in 2013. The redesigned and restructured programme has been launched by the Ministry of Rural Development, Government of India. The programme anticipates reducing women’s poverty by enabling them to start microenterprises and empowering them in all the spheres of life. The programme aims to achieve the global goals of poverty reduction and women empowerment agreed at United Nations under Sustainable Development Goals in 2015, the successor of Millennium Development Goals. However, the contribution of microfinance towards women empowerment is ambiguous as documented in the literature for two broad reasons. First, some empirical studies claim that microfinance does impact women empowerment, while others state that microfinance does not significantly empower women in one or the other domains. Second, the measurement of empowerment has not been valid, given the cultural and geographical context, time horizon as well as its multidimensional character. Women’s empowerment has been considered multidimensional in nature and occurs across the dimensions of economic, social and cultural, legal, political and psychological. There is a wide consensus among researchers that empowerment is a complex multidimensional process that occurs at individual, community and organizational levels involving the domains of health, economic, political, natural resources and spiritual and is fostered by knowledge, agency, opportunity, capacity building, resources and sustainability. The various domains of empowerment are interdependent and each domain is facilitated by or dependent on another domain (Hennink et al., 2012; Malhotra & Schuler, 2005). The broader and holistic empowerment of women is an open-ended process and is of utmost importance to eliminate marginalization, devaluation, subalternism, displacement and dispensability, particularly of women in India (Misra, 2006). The present study attempts to address these concerns and develops and evaluates context-specific empowerment under the four widely agreed dimensions—economic, social, political and psychological—and hence, defines empowerment as a process of change by which individuals or groups with limited choice, freedom and power are enabled to gain and leverage power that enhances their ability to exercise choice and freedom in ways that positively contribute to their well-being (Ganle et al., 2015).

This empirical article is documented in the context of Kashmir valley of Jammu and Kashmir Union Territory, India, which undoubtedly bears a strong practical relevance as few research were made in this regional context. Data have been mainly collected from women’s SHGs mobilized and nurtured under the flagship programme NRLM. With particular reference to Kashmir, women are far behind in empowerment and still counted among the disadvantaged sections of the society. Women are generally exposed to domestic violence. As per Census 2011, literacy rate of women is comparatively lower than their counterparts and women in rural areas of Kashmir still live in marginalized conditions. In addition, labour force participation rate is lowest (10.6%) for women in Kashmir compared to other states (RBI, 2015).

Self-help Group Model of Microfinance and Women

Women’s group-based models are more instrumental for eradication of poverty and empowerment of women (Galab & Rao, 2003). It is believed that SHG approach leads to women empowerment more effectively. An experimental study of SHGs in India reports increase in women’s awareness of rights, independent savings and active involvement of women in political areas. There is also a reduction in verbal, physical and emotional abuse of women. Hence, women in SHGs are empowered overtime compared to those women who do not participate in SHGs (Swain & Wallentin, 2009). The case studies from SHGs in Pakistan and Malawi indicate that reliance of women in SHG on social capital and accessing microfinance helps them to achieve collective business plans, generate own income, expand asset base, increase savings and utilize pooled resources for consumption expenditure or emergency needs such as healthcare; thus, women in SHGs contribute to whole family welfare (Rashid & Jonathan, 2014). Women participating in microfinance, no doubt, take part in expenditure decisions and gain asset ownership, which ultimately leads to reduction in domestic conflicts. Evidence reveals that participation of women in SHGs and accessing microfinance led them to increase monthly income, expenditure and savings. However, confronting various obstacles in getting financial assistance is also a true story for members of SHGs in certain contexts (Srinivas, 2015).

Literature Review and Hypotheses Development

Employing traditional narrow view of women empowerment, earlier studies have largely revealed constructive effect of microfinance programmes on several indicators, for instance, on surveying 1,300 women clients in Bangladesh it was found that mobility, ability to make purchases and major household decisions, economic security (assets), political and legal awareness, participation in protests and campaigns, control over assets and income as a result of continuous financial support to the families have improved (Hashmi et al., 1996); in a comparison of 316 established clients (who accessed and utilized four loans) with 231 new clients of microfinance institutions (MFIs) in the context of Ghana, an increase could be observed in physical capital (sewing machine, refrigerator and electric cooker), financial capital (savings and subscription for client welfare schemes) and human capital (children’s education and health status of household members), as established clients were significantly benefited from microfinance (Adjei et al., 2009); in another study of 305 women members of MFIs operating in Tanzania who were in the programme for more than 3 years (treatment group) and 149 women non-members from non-programme areas (control group), impact on women’s better control over their economic resources (saving, income & assets), say in decisions, freedom of movement and participation in activities happening outside home as well, increase in self-esteem and self-efficacy could be observed (Kato & Kratzer, 2013). However, in the recent studies, there is a transition in notion in relation to empowerment. Empowerment is contemplated as a complex, multidimensional process that involves different spheres, namely social and cultural, health, economic, legal, political and psychological natural resources and spiritual (Hennink et al., 2012; Malhotra & Schuler, 2005; Misra, 2006). In line with this kind of comprehension, we reviewed those studies, in specific, that examine impact of microfinance on allied domains of empowerment.

Microfinance and Women’s Economic Empowerment

Economic empowerment pertains to access to economic resources, such as income, assets, savings and exercising control over these resources. Economic empowerment is the elite that can further lead to social, political and psychological empowerment. On certain indicators such as income, asset generation, consumption expenditure, savings, loan utilization, considered for measuring economic empowerment domain, definite impact has been found in quantitative investigations (Sinha et al., 2012; Weber & Ahmad, 2014). On the other hand, doubt has been raised about the unique role of microfinance programmes in economic empowerment of women. A qualitative investigation by Rehman et al. (2015) revealed improvement in economic conditions in terms of household purchase decisions but detected age, education, family type and marital status as other important determinants. Similar observations were drawn in a quantitative analysis by Addai (2017) while recognizing education and marital status equally determining women’s economic empowerment as microfinance do. Women participating in microfinance, no doubt, take part in expenditure decisions and gain asset ownership that can be expected to reduce their domestic conflicts. However, women’s long-term memberships in MFIs can also lead to marital conflicts between husband and wife. In addition to it, women’s increasing workload cannot be overlooked (Arku & Arku, 2009) as women are overburdened with a dual work of household chores along with operating their income generating activities (Haile et al., 2012). It is also argued that the presence of women in micro-credit programmes has a limited effect on women’s access to material resources consisting of education and employment (Mahmud, 2003). Sometimes accessing loans and possession of household assets can have an adverse effect on women’s decision-making power (Lavoori & Paramanik, 2014). Some notable systematic reviews could not be conclusive about the impact of microfinance on poor people due to inappropriate methodological designs employed in several studies; thus, stern need of mixed method research with well-designed experimental methods suitable to particular context was brought into limelight (Brody et al., 2017; Duvendack et al., 2011). Bayulgen (2015) and Rehman et al. (2015) argue though microfinance can improve women’s financial base, decision-making process and bargaining power and reduce dependency and further strengthen their voice, yet microfinance cannot be an empowering tool for all kinds of women, but majority of them are also impacted though insignificantly. Inclusion of perfect control group in cross-sectional comparison can be one of the ways to overcome methodological problems that increase bias in impact assessments.

Microfinance and Women’s Social Empowerment

Social empowerment refers to individual’s independence to live life freely, enjoy free mobility with social status and liberal interaction with people around. There is evidence claiming microfinance as instrumental in socially empowering women (Addai, 2017). Microfinance services can result in women’s self-confidence, ability to face problems, control over the use of money, decision-making ability, participation in public issues and ownership over productive as well as consumer assets (Sinha et al., 2012). These findings could be further confirmed from studies employing qualitative tools of investigation. While examining economic, health and education, social and political domains Rehman et al. (2015) could find a noticeable effect on social empowerment of women (children’s marriage, visit to MFIs and visit to social gatherings). However, external environment can also have a tremendous bearing on social empowerment of women; for instance, in Pakistan, Weber and Ahmad (2014) posed some questions to respondents in relation to social empowerment in addition to financial empowerment mainly regarding household decision-making matters such as purchases, children’s schooling and marriage and freedom of movement. In their investigation, though massive improvement was observed as a mobility indicator of women after microfinance participation, other remaining indicators were found amenable to external societal interferences.

Microfinance and Women’s Political Empowerment

Political empowerment can be understood as one’s awareness of political domain, and it is characterized by participation in political activities. It is believed that women who are economically better-off and are assembled in groups are more likely to be empowered in political arena. It is argued that the small nature of microfinance loans can hardly lead to significant improvements in clients’ business, leaving their socio-economic status stable. However, prior experience with political activism can increase the proclivity of microfinance clients to care about and participate in politics more (Bayulgen, 2015). Further, participation of women in the microfinance programmes particularly through group mechanism can lead to their greater awareness about politics and confidence to take active part in local government (panchayats). Women in SHG model of microfinance are more likely to show interest in contesting in elections and attend various meetings of Grama Sabhas where they can raise their demands for developmental schemes, benefiting their localities (Brody et al., 2017; Sreermulu & Hushenkhan, 2008). Studies based on experimental approach of comparing women SHG members with non-members further support definite effect of the intervention on political empowerment index (Garai et al., 2012). Membership in the microfinance can be another factor that can strengthen the political empowerment of women, in terms of their awareness of the political field and participation in political activities particularly through casting votes and supporting political party. In contrast, there are such instances as well where microfinance cannot be claimed as a tool to empower women in political domain. Rehman et al. (2015) also found in their study that participation of women in the intervention has not resulted in the increasing awareness about their rights and women still caste votes as per their family choice. Hence, contribution of microfinance towards political empowerment of women seems doubtful, which needs further investigation.

Microfinance and Women’s Psychological Empowerment

Psychological empowerment also called personal em-powerment points out internal strength of an individual and is characterized by increased self-confidence, self-reliance, self-esteem, decreased psychological distress, challenging gender norms and so on. Microfinance is believed to increase collective efficacy, proactive attitude, self-esteem and self-efficacy of women. However, improvement in this particular empowerment domain over a longer period of time is not yet clear. Despite the positive contribution of microfinance towards women’s psychological empowerment, increase in women’s stress and strain cannot be overlooked (Moyle et al., 2006). While alternatively using the term ‘Power Within’ for psychological empowerment, Kim et al. (2007) found microfinance has the potential to enhance self-confidence, financial confidence and challenging gender norms ability among women. Another study assessing psychological empowerment of women participating in microfinance programme divulged increase in personal control beliefs and social network size (active group members) (Hansen, 2015). It is vividly clear that efficacy of microfinance on this particular domain is still inconclusive.

Research Methodology

Data Collection

The study covers Kashmir valley of Union Territory of J&K, India and through structured interview schedule, the primary data have been collected from women SHG members registered under the scheme Umeed of the mission mode programme ‘National Rural Livelihood Mission’. Secondary data have also been utilized for the present study and were gathered from several books, journals, websites, block offices and regional offices of National Rural Livelihood Mission.

Sample Selection

A sample of 370 has been drawn from the total number of SHG members following Krejcie and Morgan’s (1970) formulae of sample size determination. Multi-stage (mixed) sampling has been employed in the study. At the initial stage, 4 out of a total 10 districts of Kashmir have been selected purposively. These four selected districts had higher concentration of bank-linked SHGs and had been graduated to highest doses of bank loans. In the second stage, four respective blocks have been selected from each district as these were the only blocks where SHGs were linked to banks for provision of basic financial services. At the third stage, blocks have been divided into six clusters each, and three clusters have been chosen for the study on random basis. In the final stage, respondents have been selected randomly from all the chosen clusters for which prior random numbers were generated in a spreadsheet.

Methodological Design

In order to assess impact, quasi-experimental design has been employed for the present study. The quasi-experimental approach, also called pipeline approach, is such a design in which new borrowers/microfinance clients that are at first/initial loan cycle form the control group, whereas, established borrowers/mature clients who are at second or higher loan cycle make the treatment group. This pipeline approach has been found apt for the present study due to selection bias and complexity in tracing non-borrowers/non-members (Adjei et al., 2009; Kumar, 2013; Nilakantan et al., 2013; Weber & Ahmad, 2014). The selection bias arises mainly from two sources as believed by the researchers. These are: (a) self-selection as well as non-random selection of participants into the programme and (b) non-random selection of places to implement the programme. The first source of bias ‘Self-selection’ arises if one group would consist of SHG members and the other group non-members. The second source of bias arises when one group consists of members from a programme village and another group members from non-programme village. In the present model of microfinance programme (National Rural Livelihood Mission), women participants are non-randomly selected, for example, poor households, widow-headed households, households affected due to natural calamities and so on. In the same way, villages that are economically far behind or backward are targeted for programme implementation. Keeping this in view, selecting members and non-members in the programme village or members from villages with microfinance programme and non-members from villages without the programme or intervention would fetch biased programme impact estimation. Hence, based on the above arguments a different quasi-experimental design (pipeline approach) is employed in which both the treatment and control groups are self-selected. In this design, both the groups share common characteristics and will result in bias-free impact estimation (Chowdhury, 2000, 2008, 2009; Chowdhury et al., 2016; Coleman, 1999). The total sample of 370 respondents consists of 180 new borrowers (control group) and 190 established borrowers (treatment group).

Qualitative Approach

In addition to quantitative approach, qualitative approach has also been employed in the present study with the purpose to get more clear insights and understanding regarding impact of microfinance intervention on women empowerment. Several qualitative research tools such as focus group discussions, in-depth interviews, field notes, observation and case stories have been well utilized in a good number of studies (Ganle et al., 2015; Kato & Kratzer, 2013; Kim et al., 2007; Moyle et al., 2006). In one of the research studies, extensive interviews were conducted with 20 microfinance loan recipients from 4 countries to record changes in women’s lives (Leach & Sitaram, 2002). Another study is wholly based on case study approach in which unstructured interviews were conducted with 15 women microfinance clients to ensure thorough understanding about women empowerment (Rehman et al., 2015). In the present study, case study tool has been mainly employed to confirm hypotheses tested in quantitative analysis.

Development of the Scale and Statistics Used

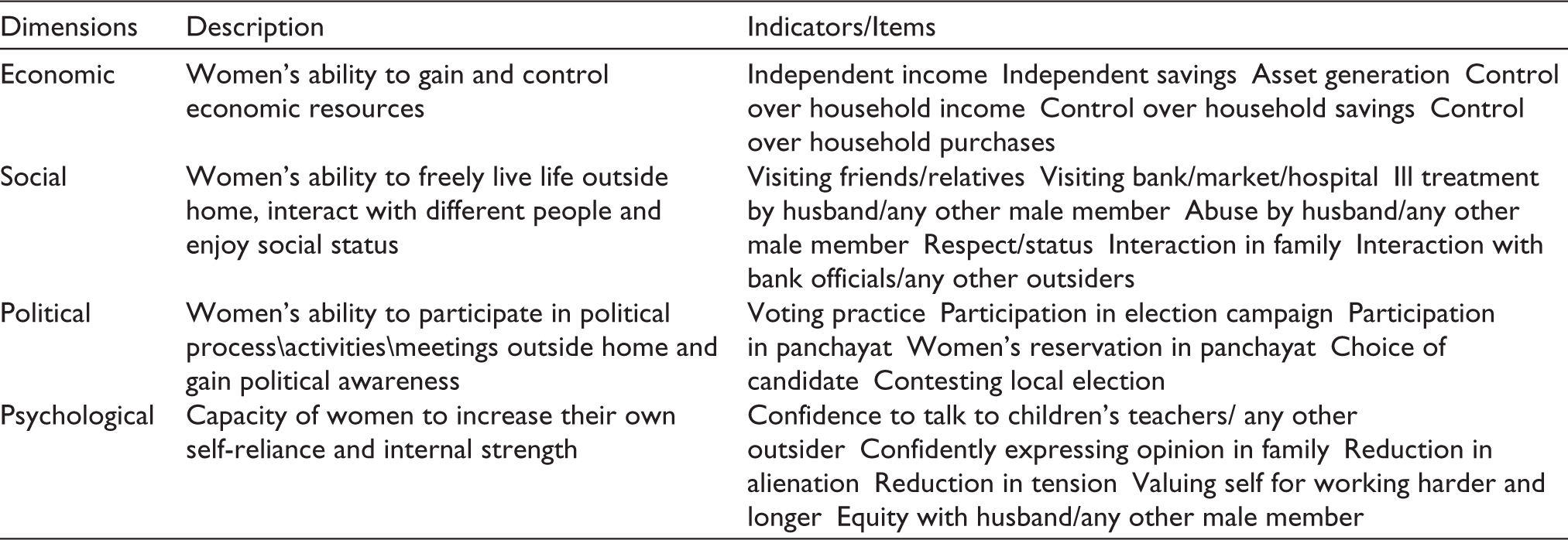

Women empowerment has been investigated under four domains—economic, social, political and psychological—based on literature survey and exploratory interviews/discussions conducted with the respondents. The various dimensions along with their description and items used to measure women empowerment on 5-point Likert scale are presented in Table 1.

Measurement Scale of Women’s Empowerment

Prior to conducting the final field survey, post literature survey, few focus group discussions were held in Ganderbal and Budgam district for framing the scale of empowerment (shown as above) as there is a wide agreement among researchers that empowerment is a context-specific phenomenon and thus, the same items measuring women empowerment stand invalid in other contexts (Porter, 2013; Schuler et al., 2010). After devising an empowerment framework considering the dimensions of economic, social, political and psychological, pre-testing of the interview schedule was conducted in two districts, namely Budgam and Ganderbal. During pilot survey, 100 respondents were interviewed to collect data for identifying various factors of empowerment. For the development of women empowerment measurement scale, exploratory factor analysis (EFA) has been performed based on pilot survey data. Based on data collected during final survey, confirmatory factor analysis (CFA) has been performed to confirm the structures or factors retrieved by previously used EFA. In order to analyse the impact of microfinance on different empowerment dimensions, an independent samples t-test has been used to compare two independent groups of respondents. The analysis of the primary data has been performed by SPSS and AMOS 21.

Results and Discussion

Pre-testing

In order to explore the diverse domains of women empowerment, EFA was performed on 25 items with orthogonal rotation (Varimax) using the data collected from 100 women SHG members. Factor analysis is a data reduction tool and is used to identify the underlying structures called latent variables. A latent variable is basically a construct that cannot be measured directly but only with a set of observed variables (Field, 2009). In the preliminary stage, sample adequacy for factor analysis was examined through KMO (0.622) and Bartlett’s test (χ2 = 1849.881) significant (0.000) with 300 degrees of freedom, indicating sufficient correlations between items. EFA could extract four factors with satisfactory loadings (>0.5). The cumulative variance explained by four factors revealed 59.516 per cent with eigen value greater than 1 (2.972). However, three items, namely ill treatment by husband/any other household member, abuse by husband/any other household member and contesting elections in panchayat had poor loadings, that is, <0.50 as well as cross loadings. Hence, these three poorly loaded/problematic items were dropped.

Exploratory factor analysis (revised) was conducted again while removing the above problematic items. The loadings for each of the items of empowerment dimensions were revealed very well (>0.50) and the cumulative variance explained by all the four factors increased to 63.873 per cent with eigen value greater than 1 (2.798). Hence, after achieving revised and satisfactory EFA results, the scale of women empowerment consisting of 22 items was finalized. The items that could cluster under the respective underlying components suggest that component 1 represents economic empowerment, component 2 represents social empowerment, component 3 represents political empowerment and component 4 represents psychological empowerment.

In this study, EFA was followed by CFA, which is generally used to develop measures and validate the constructs. It is also used as a secondary step to confirm the factors or structures identified earlier during EFA. In the present study, CFA is preceded by an empirical base, that is, EFA performed on pilot survey data (Demirbag et al., 2006; Field, 2009).

CFA has been evaluated with the help of various goodness of fit as well as badness of fit indices. The various model fit indices basically test whether the predicted model fits the sample data. AMOS output table yielded various model fit indices. The chi-square value is 349.214 with 161 degrees of freedom and minimum discrepancy divided by degree of freedom (CMIN/df) ratio of 2.169. The value of standardized root mean square residual (SRMR) is 0.0418 and root mean square error of approximation (RMSEA) value is 0.056 with its corresponding PCLOSE value of 0.098. The goodness of fit index (GFI) is 0.918, comparative fit index (CFI) is 0.972 and Tucker–Lewis index (TLI) is 0.967. All the model fit indices indicate good fit of the model.

In order to achieve construct validity, both convergent and discriminant validity must be evaluated, that is, testing for convergence across different measures of the same construct as well as testing for divergence between two distinct constructs (Campbell & Fiske, 1959). In order to establish construct validity, CFA can be used as primary tool (Hair et al., 2010). Further, according to Bagozzi and Phillips (1991), CFA can best be utilized for examining convergent and discriminant validity of the measurement scale. According to Hair et al. (2010), convergent validity can better be assessed by examining factor loadings, average variance extracted (AVE) and composite reliability.

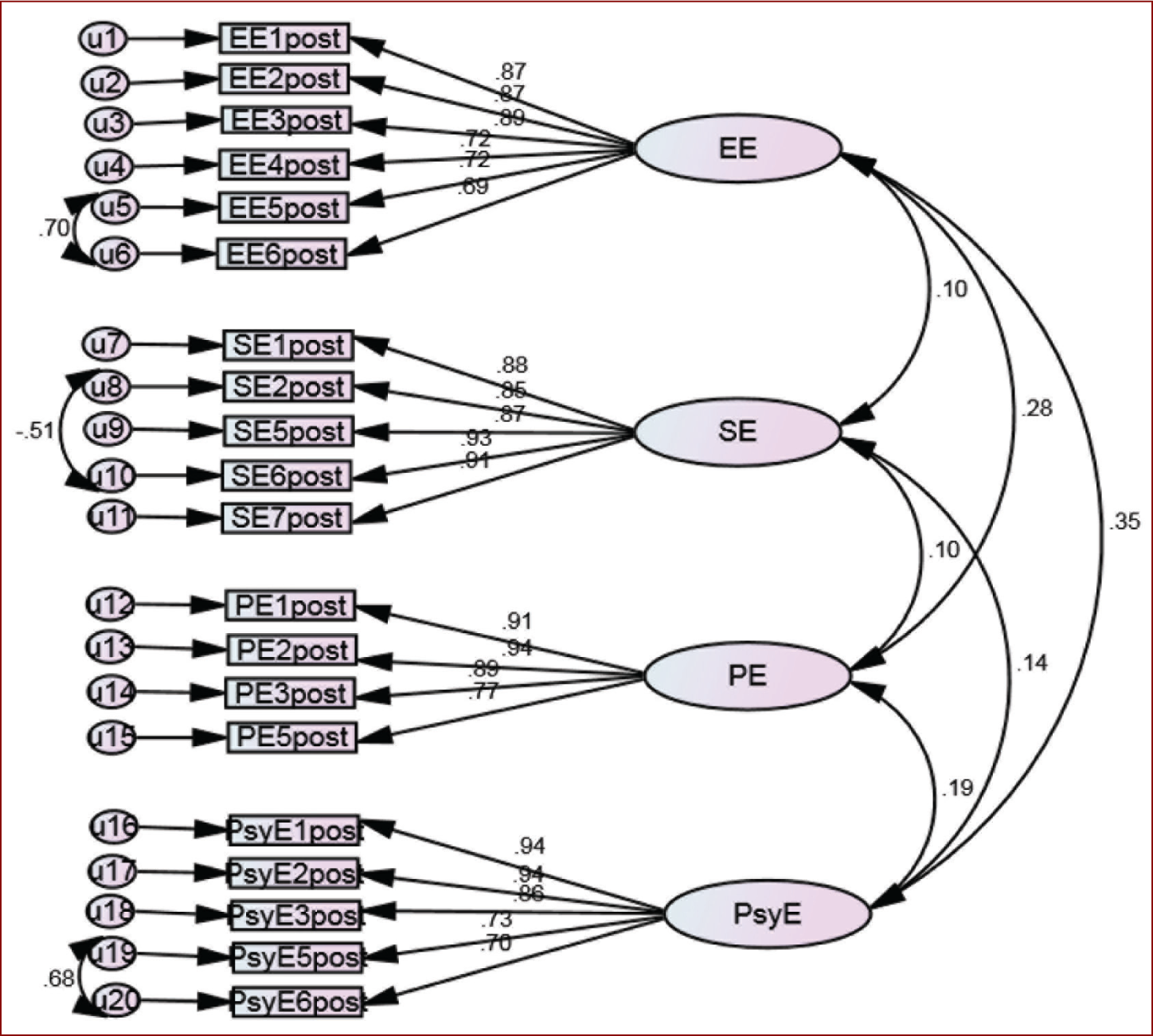

It is clearly depicted in Figure 1 that all the items have satisfactory factor loadings (>0.5 or ideally >0.7), thus providing the evidence of convergent validity. As depicted in Table 2, AVE for all the constructs is above the threshold value of 0.50, meaning all the latent variables explain more than 50 per cent of the overall variance. Composite reliability for all the constructs is either close to 0.7 or greater than 0.7, providing further rich evidence of convergent validity.

In CFA, discriminant validity is achieved by comparing the AVE with the squared correlation between two constructs and the validity is good if the square root of AVE is greater than inter-construct correlations (Hair et al., 2010; Malhotra & Dash, 2011). It can be observed from Table 2 that all the square root of AVE values are greater than inter-construct correlations, supplying sufficient evidence of discriminant validity.

Reliability and Validity Analysis

Analysis of the Impact of Microfinance on Economic, Social, Political and Psychological Empowerment

The analysis involves two groups: control group (new borrowers) who are on first loan cycle and treatment group (established borrowers) who are on second or higher loan cycle. Exploration of data across groups yielded approximately normal distribution and thus, an independent samples t-Test has been used for impact assessment (Field, 2009; Hopkins et al., 2018; Malhotra & Dash, 2011).

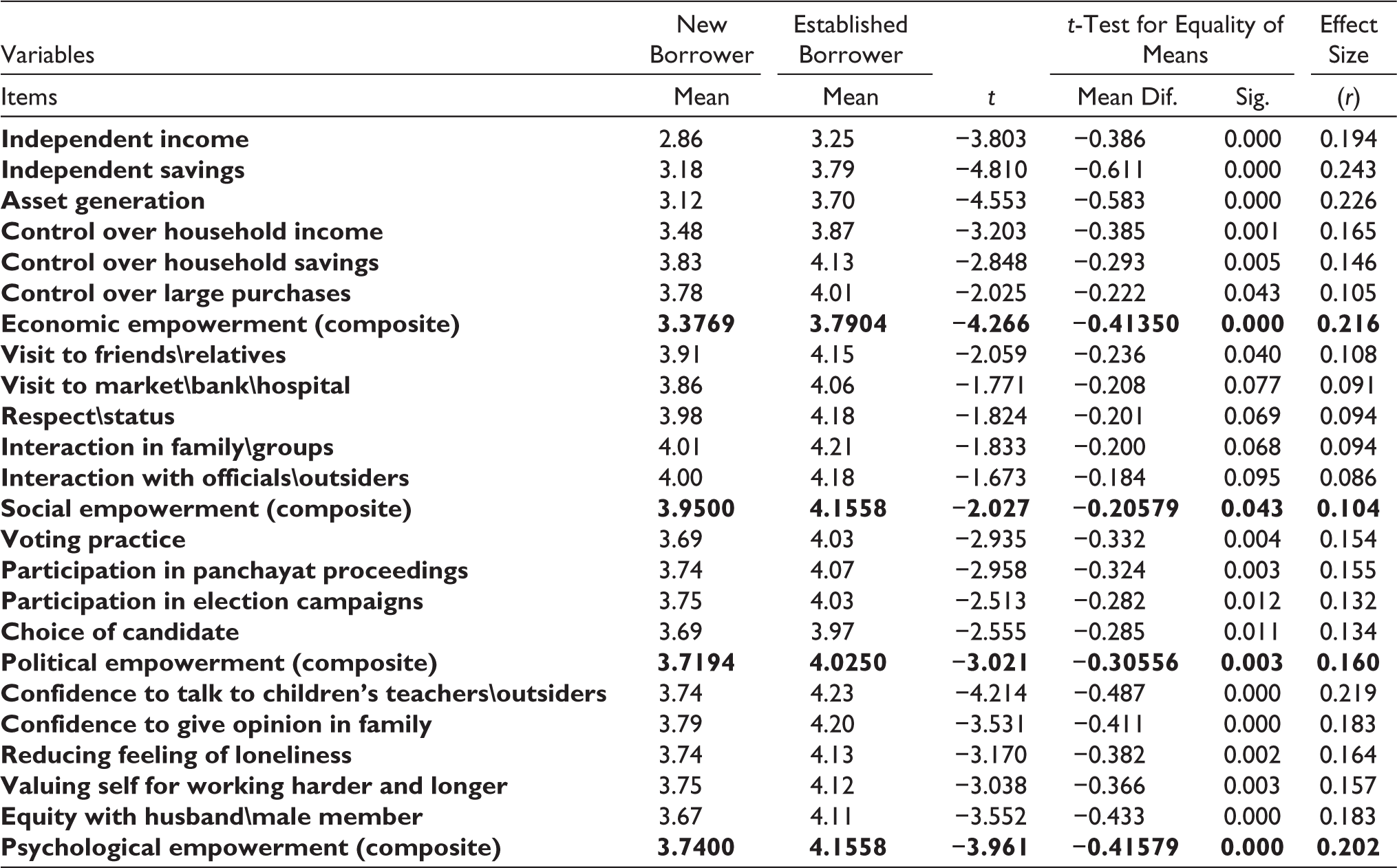

It can be observed from Table 3 that means of treatment group are more or less greater than those of control group for each of the individual items of economic, social, political and psychological empowerment. In case of economic empowerment, the differences between means of two groups are significant (t = −4.266, p ≤ 0.05), leading us to accept the proposed hypothesis while rejecting its null hypothesis. These results suggest positive and significant impact of microfinance intervention on economic empowerment of women beneficiaries with moderate level of impact (r < 0.50). These findings were corroborated with Sinha et al. (2012) who found substantial impact of microfinance SHG-bank linkage programme on economic empowerment compared to social empowerment of women. Adjei et al. (2009) also found substantial increase in asset base, savings and other household expenditures in case of established borrowers compared to new clients.

Impact Estimation

For social empowerment, notably insignificant impact (p > 0.05) on all the individual items (visit to market\bank\hospital, respect\status, interaction in family\groups, interaction with officials\outsiders) except visit to friends\relatives (p < 0.05) has been noticed in the present study. However, overall impact is significant (t = -2.027, p < 0.05), indicating positively significant impact of microfinance intervention on social empowerment of women clients. Further, effect size indicated small impact (r = 0.10) on treatment group.

As far as political empowerment is concerned, positively significant (t = −3.021, p < 0.05) change has been noticed in case of treatment group compared to control group with moderate impact level (r = 0.160). Similarly, for all the sub-variables related to psychological empowerment, there are positively significant differences in means (t = −3.961, p < 0.05) between experimental groups with moderate level of impact (r = 0.202). In consistency with previous research, Garai et al. (2012) also found microfinance through SHG approach positively impacts personal, economic and political empowerment of women beneficiaries as well as their decision-making ability in family. While analysing the impact of microfinance through SHG mechanism on personal and economic empowerment of women, Moyle et al. (2006) revealed increase in self-esteem, self-efficacy and reduction in psychological distress.

Qualitative Evidence: Report from Case Studies

Though a good number of interesting case stories have been experienced during the field survey, this study reports some selected case stories chosen, one from each district (Baramulla, Budgam, Ganderbal and Kupwara). These case studies along with brief narratives are presented below:

Case Study 1

This case study is from Singhpora block of district Baramulla recorded after a visit to the place during the month of December in 2017.

Zamrooda is a 40-year-old woman and has been a member of Hyderi SHG from last 4 years. She stated that she had no hope of earning a livelihood and was earning only a meagre amount of money by doing wage work before the programme and was wandering and looking for opportunities to earn a sufficient livelihood. Then she heard about the formation of SHG under Umeed scheme of National Rural Livelihood Mission. Zamrooda together with other women belonging to poor socio-economic section formed a group in which initially they were required to contribute and save ₹100 each. After few months, they were given an amount of ₹15,000 from the revolving fund (internal lending). She had received ₹5,000 out of total amount received and took an initiative to bring cloth for embroidery. After a year, the group was eligible for bank loans. She has taken bank loans twice of ₹50,000 and then ₹100,000. She has now formally started a business venture of embroidery making and also engaged women employees to work with her. She along with other women does embroidery work on shawls, pheran and stoles. She operates her business at her house and this way she is easily able to maintain a balance between household chores and her business life. Zamrooda, an entrepreneur, generates her own income and contributes to household purchases as well as children’s education by paying school fees. She is able to participate in all kinds of decision-making at household level which she was previously denied. She has been able to improve both the business and communication skills. Before joining SHG, she was unable to speak not only outside but also in her house. Now, she fearlessly talks to her husband, in-laws and outsiders including officials. Being illiterate though she was not able to sign the documents and being in the programme she has learnt about signature also. Before the intervention, she was restricted to move outside or visit her maternal home or any other place. Being in the programme, she is able to freely move to any place and also make her in-laws realize the importance of her mobility for the betterment of the household. She is now able to participate in any public meeting and caste vote according to her own choice. Earlier, she used to consult her spouse or in-laws to caste vote in their interest. She has been able to reduce anxiety about which she narrated a brief story.

Before the Program, one of my children fell ill at one night and there was emergency to take him to hospital. I went to neighbors for help who were well-off and at least had a vehicle that could have helped me to reach hospital. They mercilessly hesitated to help us and took us for granted. I had no money in my hands, but somehow I managed to reach hospital. After consulting a doctor, I was asked to bring some drugs for the recovery of my child. As I had no money, I handed over my watch to medicate to purchase some drugs. Now the situation has altogether changed, my financial condition is such a sound that I can even afford to grant a hefty amount to the same neighbor who had hesitated to help me earlier.

She is so busy with her business that workload is a happy moment for her as she is able to bring money, comfort and joy to her family. Prior to programme intervention, she was unable to value her work but after being setting her own business venture, she has been able to respect herself by doing productive work and she is able to value herself equal to her husband. She could even manage her household expenditure alone when her husband met with a catastrophe. She explains how she has become strong to overcome contingencies confidently

Once my husband fell ill and his health was continuously deteriorating for complete three months. I could manage all the household expenditures of my own and take care of the entire household for which the credit goes to the Program that helped me to stand on my own feet.

The programme has brought lot of changes in her life though she stated the problem of marketing her products. She wants a good market for her products at a reasonable margin. Similar kinds of problems have been reported in one study of Bangladesh that obstructs micro-entrepreneurs from performing innovative businesses (Ferdousi, 2015).

Case Study II

The second case study is from block Khansahib of district Budgam recorded after a visit to the place during the month of December in 2017.

Hafeeza has been an SHG member for last 4 years. The group has been graduated to formal financial services through bank linkage and made eligible for bank loans. Hafeeza has taken two doses of bank loans. The initial bank loan was ₹30,000 and second bank loan was of the amount of ₹40,000. She has started venture of cattle rearing and utilized a space at her own house. She manages her business alone and sells cattle in local market of her own. She is easily able to manage her business along with her household chores, as she operates her business at home. She is now able to earn income, meet personal expenditures such as clothes, shoes and even golden ornaments and contribute to overall household expenditure. She explains that she has been able to get rid of anxiety and tension after participation in the programme

Before joining SHG, as my spouse has been working as a laborer and our earnings were insufficient. I was not able to ask him for my personal expenditures because his earnings were meager to meet even household expenditures. My husband was often getting depressed and many times he met accidents. But now I am able to bring many things not only for myself but for children and entire household as well.

Prior to intervention, Hafeeza was not able to move to certain places, for lack of money in her hand. Thus, she was unaware about market, bank or any other place. Moreover, she was not able to talk to outsiders. But the scenario has altogether changed and after being in the programme, it has become easy for her to move to places, to explore markets, bank, hospital or any other place in her locality. She has gained confidence to talk to people without any fear. Her status at home as well as outside has raised and thus, she considers herself as important member of the household. Rehman et al. (2015) also employed qualitative approach and conducted open-ended discussion with 15 women microfinance clients and revealed women are empowered in economic, social and political domains as well as improved their health and education of their children. Hafeeza narrates how Umeed has changed her life

Before the Program, I was never consulted at home regarding any matter and was treated as unworthy family member. Even though I was unaware about panchayats, but now I go to any public or panchayat meetings without any restriction. I can go even anywhere now I like. More importantly, I have been able to get rid of loneliness, as I meet and interact with other group members freely. Really, Umeed has brought me a new life and Umeed has really become my life.

Hafeeza wants her longer association with the programme and wants to further expand her venture and achieve more success in this endeavour.

Case Study III

This case study is from Lar block of district Ganderbal recorded after a visit to the place during the month of December in 2017.

Neelofar has been an SHG member for last 4 years. She lives in the hilly areas of Boniputus village that generally lacks access to basic amenities. She was earlier a dependent member of her family, and her father earns livelihood by doing wage work. Belonging to very low-income family, it was becoming extremely difficult for her to fulfil her basic needs. Despite all odds, she has been able to continue her education. She is pursuing her graduation in Arts, which was made possible only after joining the programme. Being a microfinance programme participant, she has taken a bank loan of ₹15,000 in addition to Village Organization loans (internal lending) of ₹30,000. She has started a tailoring boutique at her own house. She has invested loan amounts for purchasing few sewing machines and other required things. She employs and trains other girls from her locality in her boutique. On an average, she is able to stitch five to six suits in a day. She gets customers both from her locality and from distant villages. She is able to manage her business along with her studies and household chores. She has become independent and earns sufficient income to meet not only her own requirements but of the entire household as well. She is able to move to far places freely and get rid of the feelings of anxiety/loneliness. She narrates

Being in the intervention, I learned many skills and got my business mind developed. Even though I have brothers, since I started earning from my business and meet many household requirements, my status has raised and my father treats me as his son instead of daughter.

Before the programme, Neelofar was not able to participate in any kinds of decisions in the household. She was fully reliant on her family and had to ask for money to meet all the needs. Very low income of the family was restricting her to meet her requirements. After joining SHG and generating her income from her own venture, she has been participating in all the decision-making matters. She is able to purchase whatever she likes with her own income. She has started living a comfortable and satisfied life. Neelofar wants to further expand her business venture and increase customer base by making every potential customer aware of her boutique. A case study approach by Rashid and Jonathan (2014) of SHG members revealed that women achieve collective business plans, generate income, increase their asset base and savings and also contribute to the entire family welfare. Neelofar further narrates

I feel wonderful being in the venture, I wish all the girls like me to join the Program and become independent member of the family.

Case Study IV

This case study is from block Kupwara of district Kupwara recorded after a visit to the place during the month of December in 2017.

Samia has been an SHG member as well as group leader for last 5 years. Samia is highly qualified and has done master’s in arts and thus has been in search of job prior to programme intervention. She has received three doses of bank loans of ₹50,000, ₹50,000 and ₹100,000. She has invested these loans for the establishment of a dairy farm. She has started the venture from zero and has well established the farm. She has employed one person to take care of the farm as well as manages her farm herself too. She has constructed a shed close to her house and thus, is able to maintain work–life balance. She is able to produce approximately 100 kg of milk in a day that is sold in a local market, and she is able to earn hefty amount of income monthly. Further, she is able to save money even after repaying loan instalments. She spends income on herself as well as children’s education. She is now able to participate in every household matter, which she was previously denied before joining the programme. She narrates

I used to purchase limited things for myself and home. Also, even though I had a friendly relationship with my husband but I was not wholly consulted in decisions regarding every household matter. However, since I joined the Program and started earning good amount of money I purchase many things for myself, children as well as for the house. Now I also take part in every household matter, as I am respected much more than before.

She has gained confidence to talk to officials and visit market, banks or any other place. Her status both in her own home and in community has sufficiently improved. Earlier, before joining SHG, she was confined to the walls of home and was not aware about panchayats or the meetings held there. After being in the programme, she is able to move to places without any restrictions. She has been able to improve her communication skills while facing people at large. She narrates as

Engagement with the business venture has brought me respect, dignity and fame. I have become a role model in my locality. I am often invited to many programs related to entrepreneurship and to inspire other aspiring women entrepreneurs. I have gained confidence to speak while facing hundreds of people together. I also got an opportunity to meet and interact with great personalities and officials.

In their group discussions and semi-structured interviews with microfinance clients (SHG members), Guerin et al. (2013) also revealed enhanced status, dignity and respect for women in intervention. Besides, not only women’s dependence on men decreased but women clients also contributed to household finance. Samia, an SHG entrepreneur, is living an independent and happy life and is an inspiration for other women belonging to low-income families.

This case study indicates that not all women micro-entrepreneurs are driven by necessity; rather, there is every possibility of opportunity-based women micro-entrepreneurs as well, that is, women have also been pulled towards entrepreneurial opportunities.

In all the case studies discussed earlier, it is clear that women are mostly inclined towards home-based micro-entrepreneurial activities. In the context of rural Vietnam, women micro-credit borrowers were also seen involved in necessity-driven entrepreneurship that were mostly home-based and employing 0–5 employees in their enterprises (Nguyen et al., 2014). An open-ended discussion with microfinance participants by Chhay (2011) also revealed that microfinance is one of the powerful tools contributing towards women’s economic Empowerment that further enhances social, political and psychological empowerment by creating jobs and self-employment options for them.

Conclusion and Policy Implications

In order to empower women and eradicate their poverty, access to microfinance through group mechanism is instrumentally implemented. There have been a host of studies examining impact of microfinance on one or the other domains of empowerment. However, this article assesses holistic women empowerment impact. The results from quantitative analysis revealed participation of women in microfinance significantly leads to their economic empowerment (increased income, savings, asset possession as well as greater control over household income, savings and large purchases). The results of social empowerment have also been found favourable for treatment category, though statistically insignificant impact has been noticed for individual items except visit to friends/relatives, indicating no substantial impact on social empowerment of women. However, composite score revealed significant overall social empowerment impact. Under the domain of political empowerment, it has been found treatment group enjoys more voting practice, participate freely in election campaign and panchayats as well as exert greater choice of candidate during elections. As far as psychological empowerment is concerned, women clients who were in the microfinance intervention for longer duration reported higher self-confidence in talking to children’s teachers/any other outsiders, express their opinion freely in family, are more likely to get rid of the feeling of alienation, have increased feeling of self-worth for working harder and longer than any other in their household and are more likely to enjoy equity with their husbands/any other male members in the household. Further, effect size indicated moderate level of impact in case of economic, political and psychological empowerment and only smaller impact in case of social empowerment. No doubt, new borrowers as control category are also somewhat influenced by the microfinance intervention; however, comparing them with treatment category (established borrowers) that have been substantially empowered leads us to detect exact impact of microfinance.

The findings from the case stories were found consistent with the above findings. In case stories, women revealed how their lives have altogether been transformed after their participation in the programme and establishment of their new business ventures through which they generate income and other economic resources, exert their bargaining power that help them to make their own choices. Case studies further supported that women in the microfinance intervention for a longer period are more likely to be economically, socially, politically and psychologically empowered. Hence, it can be deduced that participation of women in microfinance substantially impels them towards economic, social, political and psychological empowerment. This article contributes to the existing body of literature which states that access to microfinance can be an effective intervention towards holistic empowerment of women.

Since it was found in this study that attaining maturity (increasing membership) in microfinance programme and large size of microfinance loans has largely impacted women empowerment, thus the programme needs to be strengthened in these parameters, that is, maintain client’s participation in the intervention in the long run and ensure access to increasingly higher amount of micro-credit on continuous and consistent basis. Further, it is suggested that policymakers would make an increasing effort to target more and more women in the intervention and include a broad range of microfinance services other than financial that would intensively benefit the target clients. Women empowerment is a route to poverty eradication; hence, the programme would emphasize on holistic empowerment of women. Moreover, qualitative approach (Case Stories) unveiled marketing problems such as no bulk customers, pricing issues and unawareness among potential customers that women encounter in their businesses. This pivotal finding would further hasten policymakers to take some initiatives towards the end of these marketing-related problems. There is a need that the government agencies should provide marketing expertise for these enterprises by conducting market research in their product areas. It would encourage more women to start and operate their own business ventures successfully.

In this study, researchers put their ample efforts to minimize bias while keeping in view the time and financial constraints, but there still remained few serious and unavoidable loopholes. At the time of data collection, respondents had generally taken three doses of bank loans as the programme (National Rural Livelihood Mission) was reconstructed just 5 years ago and respondents were in SHG membership for 4–5years. A larger span of their membership would enrich the study results. Further, geographical scope of the study is somewhat narrow and is just confined to Kashmir valley. Extension in the study area would fetch a more in-depth understanding of the problem.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.