Abstract

Abstract

This exploratory paper analyses, theoretically with some numerical examples, the relationship between tax evasion and provision of public goods. In this model, we incorporate tax evasion leading to a fall in the supply of public goods. We investigate the relation between provision of public goods and wages of workers engaged in the production of public goods and an intermediate private goods. We show that under plausible conditions, and parameter values, fall in the number of taxpayers leads not only to fall in the provision of public goods, but also lowers wages. We find a threshold level of marginal cost associated with supply of public goods, above which the rise in the number of taxpayers may still lower provision of public goods and worker’s wages.

Introduction

The economics of tax evasion and that of the provision of public goods are intensely discussed and debated in the literature. The present paper aims at addressing a pressing question on whether tax evasion and its implications for provision of public goods could also affect the wage and employment outcomes in an economy. To answer this question, which we think is scarcely dealt with in the large literature, we would principally assume that a considerably large section of the workers does not pay any income-related taxes. This seems a disturbing but realistic assumption for many poor countries. For example, only 1.7 per cent of Indians paid income taxes in the 2015–2016 assessment year. It is needless to mention that a country does not collect its taxes from income-related sources only. Provision of public goods and many other activities of the government are financed by several other forms of taxes and often via deficit financing. However, it will not infringe upon the basic principles of public finance if one assumes that provision of some public goods is made contingent on collection of direct taxes only. 1

Conversely, user fees or charges can finance public facilities. Non-payment of fees may jeopardize the provision of public goods. Local public transport or children’s parks are tentative examples.

We review a large literature that discusses both these aspects, but somewhat independently, with a few exceptions. The literature is expected to set the appropriate motivation for an analytical exercise on the complex interplay briefly discussed earlier. The analysis is set in a general equilibrium framework. We wish to arrive at a combination of the tax rate and the provision of public goods that maximizes social welfare. Any departure from that leads to a significant decrease in the equilibrium wage–employment configuration. In other words, we attempt to see the effect of tax evasion on the provision of public goods and on the economy-wide wages of the workers.

This approach may be deemed realistic enough in view of the large body of empirical evidence, which clearly suggests that tax evasion cannot be brought down to zero, regardless of the expanse and sincerity of coverage and preventive measures. At the same time, very few countries, not to speak of the developing ones, do have a provision of public goods that can be considered as socially optimal. This further suggests that we do expect initial choices as interior solutions made by the social planner, such that deviations lead to adverse outcomes.

The rest of the paper is organized as follows. The second section discusses the literature, the third section develops the model. We obtain equilibrium configuration for no evasion and the case of evasion in this section. Subsequently we discuss stability of the equilibrium and impact of monitoring. The last section concludes.

Related Literature

According to the International Tax Compact (2010), tax evasion refers to illegal practices to escape taxation. It includes cases where taxable income, profits liable to tax, or other taxable activities are concealed, the amount and/or the source of income are misrepresented, or tax reducing factors such as deductions, exemptions or credits are deliberately overstated.

One of the seminal works in the study of tax evasion was that of Allingham and Sandmo (1972), which analysed an individual taxpayer’s decision on whether and to what extent taxes could be avoided by deliberate underreporting. In their model, the true taxable income is known by the taxpayer but is not costlessly observed by the tax-collecting agency providing information-theoretic explanations behind evasion. Since then, a number of papers by Yitzhaki (1974, the popular Yitzhaki puzzle which shows that higher marginal tax rates raises compliance), Cowell and Gordon (1988, showing that, tax hikes when the economy is over endowed with public goods, may reduce tax evasion), Falkinger (1995, showing that the risk aversion of a taxpayer evading taxes increases with higher consumption of public goods), Marjit et al. (2000), Myles (2000), Saha (2001), Fearon (2009), Hokamp (2014), etc. offer various dimensions related to tax evasion and public goods provision, including delivery of public services.

In Myles (2000), for example, a number of implications based on political culture about provision of public goods is quite clear. These show how the presence of non-concavity owing to tax evasion complicates the analysis and generates difficult trade-offs for the government. A policy designed to raise the level of provision through higher taxes, may be harmful to the low-income consumers. High amounts of government provision will also encourage tax evasion, as this is the best response of the low-income groups. The most significant finding of the paper is the extent to which the claim that public goods should be entirely provided by the government is rejected. According to Myles (2000), even though these results cannot be taken as definitive, they do provide sufficient evidence to justify further reassessment of the role of government provision versus incentivizing private provision and evaluating the motives behind tax evasion.

From a modelling perspective, choices have to be made about the representation of preferences and the information the consumers have about the government. Rather than being inconsequential, these choices have a significant impact on the nature of optimal policy. However, results to date cast some doubt on the instrumental preference model (Murdoch & Sandler, 1997) in large populations but do offer support in small ones. The analysis in this paper also assumes that the government is concerned with maximization of welfare. It should be noted at this juncture that a large part of the documented corrupt practices emanate from public organizations. This has been dealt with veritably in the related literature. We offer a few snapshots to facilitate the direction of the current paper. For example, De Vaal and Ebben (2011) have discussed bureaucratic corruption and tried to determine if corruption affects growth positively or negatively. They constructed a two-layered model that deals with the direct and indirect effects of corruption. The first layer deals with the relation between corruption and growth in an institutional vacuum. Presence of corruption in an institutional vacuum lowers growth by lowering the inputs of productive public goods and labour. In the second layer when institutions are taken into consideration, the results are ambiguous. Corruption negatively affects these institutions only when political stability and protection of property rights is above some threshold level. Hence, the initial institutional environment is important for assessing the corruption–growth relationship.

One of the more recent papers in the literature of tax evasion and public goods provision is by Hokamp (2014) which makes a combined analysis of back auditing and the agent’s age in the context of tax evasion. This paper finds that heterogeneity of age leads to fluctuations in tax evasion only when lapse of time effects are considered. By lapse of time effect or back auditing, the author refers to the idea of a set of previous tax-relevant period being also factored into the analysis along with the actual time period. It is stated that older agents are more compliant due to evolution of social norms over their life cycles and are expected to demonstrate lesser tax evasion. It is also established in this paper that provision of public goods leads to more tax evasion. Indeed, the technical probability of a Pareto optimal provision of public goods is rather small.

It needs to be reminded that, generally, or in the context of our paper, provision of public goods is not limited to physical infrastructure and subsidized food grains only. The delivery of public services, including such activities as that of tax collection, is also significantly affected by corrupt practices by the officials. As pointed out by Marjit et al. (2000), a form of corruption is harassment from the tax-collecting officials who threaten the individuals on grounds of reporting them as tax evaders, unless a bribe is paid. In their model, whoever files income tax ends up paying harassment cost to avoid punitive action. The auditor is able to effortlessly observe the taxpayer’s income and extract the entire surplus from not going to the court. To deal with this issue the model incorporates honest taxpayers and different types of auditors. So in equilibrium corruption still occurs, but some of the taxpayers do go to court against harassment. The auditors are still able to extract the entire surplus from the corrupt taxpayers, but introduction of heterogeneity among auditors and taxpayers leads to different levels of harassment in equilibrium. Harassment cost dissuades poor taxpayers from participating in the bribery game leading to both distributional and revenue consequences. One of the outcomes is a reduction in the provision of public goods. The richer individuals are not in much need of public goods and hence are not affected by the shortage. The poorer sections do not pay for public goods and do not participate in the bribery game. They are left as net gainers no matter what amount of public goods are provided. In our paper, we show that while some public goods may still be provided, fall in nominal wages for the participating labour force could lead to overall welfare loss. On a similar note, Fearon (2009) investigates the contracting decision of governments to audit or outsource the provision of public goods given hidden bribes and information asymmetries (importantly, see Slemrod & Yitzhaki, 2002). The audit mechanism is concerned with provision of public goods within the public sector, given asymmetry of information regarding cost of production between the department (principal) and the bureau (agent). Outsourcing is represented by Nash bargaining between the government and a foreign monopoly firm regarding the price of public goods. During bargaining, firm offers to bribe the government to make it shift from auditing to outsourcing. Only with a weak legislature will bribery be successful. For a strong regime, bribery will not work.

Given this background, we wish to see if the act of evasion leads to other forms of welfare loss not accounted for in the literature—the fall in wage rates for the evaders is one such possibility. Before we develop the model in the third section, it might be worth discussing the general validity and acceptability of the proposition here. Tax evasion and poor coverage of the tax net has many adverse effects. Unlike the context of this paper, where tax evasion lowers wages directly, one may generally argue that revenue deficits either lead to curtailment of public goods and services, or maintain it by deficit financing, inflation is a natural outcome, leading to a fall in the real income. Yet, the evaders do not internalize this possibility, because the savings from evasion typically outweighs the costs associated with it. Further, more realistically, the evaders and the consumers of public goods are not drawn from the same set, as briefly discussed earlier. The adverse impacts of tax evasion by richer sections are normally faced by the poorer households creating a natural impasse. Admittedly, the present paper does not model all of these, but shows how non-compliance with tax burden affects wages directly. The rest is left for future attention.

A Model

Consider an economy where there are three entities, namely the firm, the individuals and the government. The firms produce private goods (or a vector of private goods) with the help of labour and capital. We will assume that the stock of capital is given in this economy, such that marginal product of capital determines the return in the competitive factor market. Individuals consume private goods out of their labour income, which is equal to the marginal product in the labour market. The utility of the individual depends on the consumption of both private goods and public goods, H and G, respectively. We will assume that the price of the private goods (H) is set at Ph, while the shadow price of the public goods (G) is Pg. The price of G is determined by the conditions of socially optimal provision of public goods created by the third entity in the economy, namely the government.

Given this structure, we intend to first obtain the socially optimal level of public goods (G*) and the equilibrium amount of private goods produced in this economy (H*). The wage and employment levels in equilibrium are obtained from this configuration. It should be mentioned here that in terms of a general equilibrium system of equations, we derive the equilibrium levels of each of these variables based on the optimal provision of public goods. This in turn is obtained from a tax rate ‘t’ imposed on the individuals by the government in order to finance the production of the public goods. The production of public goods uses H along with labour and follows the standard characteristics of a neoclassical production function:

In this model, we consider that tax evasion leading to fall in tax revenue is of the nature where a section of the individuals do not pay taxes, by hiding their income completely (we shall discuss the stability conditions and interior equilibrium in the end). For all practical purposes, this could be like renting out property and receiving rents in cash without official records associated with it. Several such examples have been discussed in Saha, Roy, and Kar (2014), showing how undocumented income leads to consumption parity between private sector and public sector workers. In our model, unreported income and non-payment of direct taxes should affect the provision of public goods and in turn affect the demand for private goods as an input required for production of public goods. Subsequently, the wage rates must fall everywhere. Therefore, under plausible conditions, an individual may suffer from a decline in the real wage not compensated by savings from tax evasion. It is easy to think of a developing country with extensive informal arrangements, where this form of evasion is clearly possible. Analytically, this is same as everybody paying only λ fraction of tw, 0<t<1 where t is the due direct tax rate and w is the wage. It seems that a section reporting no income and therefore paying no direct taxes is quite common in countries with large shadow economies such as in Asia, Africa or South America (Dreher & Schneider, 2010). 2

According to the present model, for developing countries, ‘non-reporting’ and non-taxation of income earned by a section of the population implies that the total tax revenue of the government is lower by a factor F, when government can calculate the GDP and potential direct tax revenue. Compared to this, the standard modelling practice shows that tax-evaders report an income wr < w and therefore evade a tax revenue of t(w – wr) with probability (p < 1) of being caught and paying a penalty γ > 0 (if audited at a cost c > 0) of a fixed amount (or as proportion of the true income). As long as , n > 0, n being the number of evaders, the impact on state revenue is the same.

No Evasion

Firms

The identical firms in the economy produce a commodity as per the production function:

This production function is subject to the cost constraint wL + rk ≤ M such that the profit of each firm is given by

It is easy to see that under competitive conditions, the firms would pay w to the workers and r to the owners of capital.

Individuals

Let there be L homogeneous individuals with the following utility function:

This utility function is maximized subject to a budget constraint given as:

where w(1 – t) is the post-tax income of individuals that must pay for the consumption of the two goods H and G given respective prices. We will determine ‘b’ with the price of H given exogenously. Equation (4) determines the optimal amount of

Government

Given G a s the level of public goods provision and L as the number of homogeneous individuals, the aggregate inverse demand for G in the economy is given by

The assumption of linear demand for non-excludable, non-rival public goods is standard. Gruber (2013), for example, shows that, social-efficiency-maximizing condition for the public goods is

The total benefit (TB) from the provision of public goods is given by

The aggregate supply of G is given by MC(G) = c + mG, where we define c as the cost of collecting taxes and m as the marginal cost of supplying one unit of G.

Thus, the total cost (TC) is written as:

We know that the socially optimal level of provision of G occurs where

Or,

From the FOC, we solve for

Here,

However, we consider that the supply of G is entirely financed by tax, such that, the total tax to be collected by the government (TT) for provision of G* amount of public goods is

Substituting G* from above,

The per capita tax rate is then determined as,

Or,

Given the tax rate, we now calculate the wage and employment in this economy from the utility functions and the profit functions, respectively, where

Using Equations (3) and (4), the FOCs of this optimization are as follows:

Consequently,

However, we already know that the supply of public goods by the government equals,

However, one should note that public goods are typically priced in terms of the total tax collected divided by the supply (using Equation 7), that is,

Since the shadow price must be equal to the true price, equating (11) and (12), we get the equilibrium wage (w*) in the economy from (13):

The determination of w* available in Equation (14) is based on a numerical solution as a function of L only:

Parameter values considered for the numerical solution is available in Appendix A.

Having solved for w*, we now find the employment in H and G as LH and (L – LH), under the assumption of full employment and free mobility of workers.

We consider the profit function of the firm as given by 4

The stock of capital is assumed to be fixed and exogenously given.

This solves for

Thus,

Hence, we obtain the optimal production of the private good (H*). Subtracting

So this completes the determination of all the endogenous variables in the system, namely,

Tax Evasion

The aforementioned specifications constitute a system of general equilibrium with no tax evasion. Hence, financing the required level of public goods should not be difficult in this situation. However, if we relax this assumption of no tax evasion, either less tax is collected per worker or some workers do not pay any taxes at all. We assume that the second is a more plausible case for developing countries, where informal arrangements lead to suppression of taxable income through various means (see Marjit & Kar, 2011). We have explained this in Footnote 2.

Going by this argument, the impact of a fall in total tax collection on the public goods and more importantly on wages and employment is to be obtained in terms of a comparative static exercise, through a change in L. Let us first try to determine the change in public goods provision owing to tax evasion. Here we use the supply side equilibrium value of public goods provision or

In the absence of monitors and penalty associated with tax evasion, all individuals may potentially evade taxes. Two things can happen, consequent on such behaviour. The direct impact of a lower tax collection on a lower provision of public goods may render labour services engaged in the production of G less desired. It should also lower the demand for H used as an input in the production of G. If we assume that full employment of labour prevails in this economy, the wage rate must adjust downward for all workers. How is this different from everybody evading taxes by a small margin? In the latter case, a lower tax allows all workers to retain a higher w (1–t). The tax collection falls nevertheless. The provision of public goods suffers, and subsequently lowers employment in G, directly, and via the indirect employment effect created in H. Once again, if full employment prevails, 5

In particular, sector G may be part of the public works department, which in most countries have rigid hiring and firing regulations and cannot lay off workers easily. A wage cut or temporary suspension of benefits is quite common, however. The private sector producing H may nonetheless fire workers. In either case, it creates a pressure on the wages for all workers and the adverse effects may have to be internalized subsequently by evaders.

However, in order to formally derive this relation, we need to determine the change in wages due to a change in L, that is,

We obtain,

where the notation

Overall, we find that

For detailed calculation, see Appendix B.

This when compared to the per capita tax rate in (10), generates a threshold per unit cost of provision of public goods,

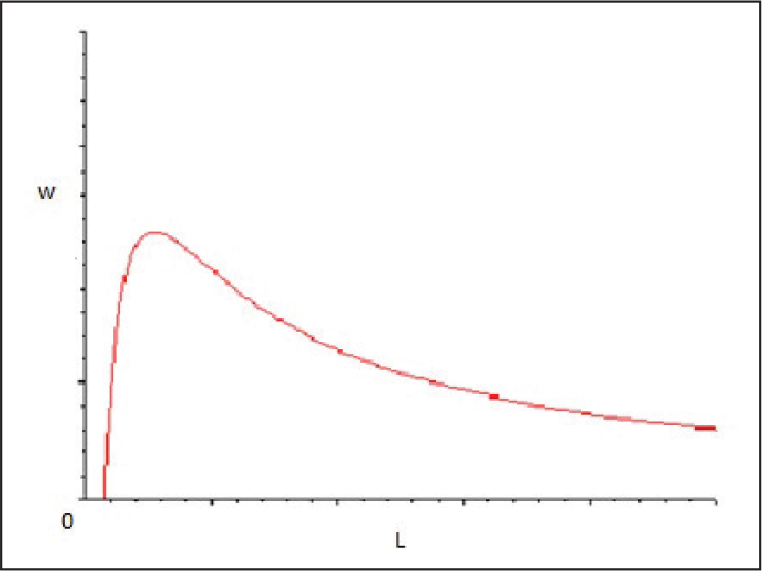

Equation (17) is valid for the equilibrium value of b* as already determined. Importantly, this relationship provides a more direct connection to Figure A1 in the Appendix A, where with fall in L, wage falls for a given value of c, but if condition (17) is valid, then for higher per unit costs associated with provision of public goods, wages may fall even if L rises. Thus, evasion may only conditionally hurt every worker and the provision of the public goods. Indeed, Lindsay and Dougan (2013) show that increase in volunteers contributing towards public goods provision may create disutility and the situation may be salvaged as long as there is some coordination between a smaller set of citizens. Conversely, provision of public goods may go down overall.

The aforementioned relation shows that a fall in the number of taxpayers lowers wages if the per unit cost of supplying public goods is less than the right hand side of (17). When there is tax evasion, the production of public goods will fall. Hence the demand for labour in the public sector will fall. A fall in the production of public goods will also lead to a fall in the demand for private goods used as an intermediate. A fall in demand for labour in both these sectors will lead to a fall in wages of the labourers. On the other hand, the individuals would want to consume more private goods with the additional money they now get after evading taxes. This may lead to a rise in the demand for private goods. Correspondingly, there will be a rise in the demand of labour in the private sector in order to produce more private goods. Hence, this would lead to a rise in the wages of those employed in the private sector. Therefore, our result that the change in wages owing to tax evasion will be negative is only conditionally true.

A Further Note on the Stability of the Equilibrium

We can assume that the equilibrium values obtained for pre-tax evasion are stable as they are calculated on the basis of standard maximization of utility and profit functions for the individuals and the firms, respectively. Deviation from that would mean not obtaining maximum utility or profit, and there is no reason for rational individuals and firms to do that. On introducing tax evasion, we observe a fall or a rise in these endogenous variables. When the amount of tax evasion is known, the deviation from the non-evasion equilibrium values of these endogenous variables can be calculated from the comparative static exercises. It is to be seen if the new higher or lower values will be stable or not.

Public goods are always associated with the free-rider problem. As long as individuals know that at least one individual is paying taxes and public goods are being supplied, the selfish decision maker chooses zero contribution. 7

This is not considering the literature on warm-glow effects (Andreoni, 1990).

Introduction of Monitors

Now let us assume that a proportion of the population is constituted by monitors who oversee cases of potential evasion. The job of the monitors is to ensure that nobody evades taxes and in case of violations, reporting the same to the government. The evader would then be charged a penalty by the government. Here, we assume that the monitors are corrupt too. They let go off an evader if the evader pays a certain amount of bribe to the monitor, which is a share of the amount of tax that the individual evades. Hence, either the evader does not get caught or gets caught and goes free by paying a bribe. The government never gets to know who evades and cannot charge the penalty. This is an extreme assumption, by which the government earns no extra revenue by employing monitors and creates an environment of rent seeking, instead.

Since the government does not collect additional revenue, the provision of public goods remains at the previous level, but the demand for both private and public goods must rise. The reason is that, monitors by receiving bribes demand more of these, and the individuals by retaining more income than under full tax regime, demand more as well. If this raises the price of the private goods and the factor returns, the public goods must be produced by an even lesser amount. In other words, introduction of monitors without enforceable outcomes is welfare reducing in term of the provision of public goods. The wage and employment levels for the entire economy are ambiguous in this case.

Concluding Remarks

Effect of tax evasion on public goods provision and wage levels in an economy is of considerable importance for the larger perspective of public economics. In this paper, we try to determine the provision of public goods, the demand for private goods, the optimal tax rate, the wage level of the workers and the distribution of employment between the private and the public sectors. In the presence of tax evasion, we measure the effect on the equilibrium values of public goods provision and wages. We see that public goods provision decreases with an increase in tax evasion. The effect of tax evasion on wages is, however, ambiguous. The equilibrium that we obtain has been argued to be a stable one.

We have also discussed a case where regulators oversee compliance with tax payments. We argued that unless outcomes are enforceable, introduction of monitors may lead to further reduction in the provision of public goods, partly because of the cost associated with employing monitors, but also because of possibility of rent seeking by these regulators. However, due to the presence of bribes and unpaid taxes distributed between monitors and taxpayers, the aggregate demand for private goods may rise in the economy and raise employment. These possibilities need to be explored in greater detail with more rigorous analytical modelling.

Appendix A

We substituted, a = 2, t = 0.4, ta = 0.5, m = 1, and c = 0.6, in Equation (13),

The substitution generates the following solution for w*:

such that, the relationship between w and L can be graphically obtained as (for positive values of L and w),

Appendix B

Here again, we use the notation M to represent

We have

We have already obtained,

Hence,

On cancelling (1–θ) and solving,

On dividing both numerator and denominator by L, we obtain:

where t is the tax rate.

From Equation (2), we can say that whether

or,

or,

or,

such that,

Acknowledgements

The authors thank an anonymous reviewer for many helpful comments. The remaining errors are our own.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.